Contemporary Financial and Integrated Reporting: A Comparative Study

VerifiedAdded on 2021/05/31

|18

|3308

|45

Report

AI Summary

This report provides a comprehensive analysis of contemporary financial and integrated reporting, focusing on a comparative study between BHP Billiton Limited and Rio Tinto. It begins with an introduction to the importance of financial statements and the regulatory framework in Australia. The core business operations of both companies are examined, highlighting their roles in the resource sector, followed by an industry analysis that assesses the growth and factors influencing the mining sector. The report then delves into the financial structures of BHP, including capital structure elements and key financial performance indicators such as revenue, assets, and cash flow. It details the key elements of financial performance, including assets like property, plant, and equipment (PPE) and intangible assets, referencing relevant accounting standards. The report also addresses voluntary disclosures made by both companies. Overall, the report provides a detailed overview of the financial reporting practices, accounting treatments, and regulatory compliance of these two major players in the resources industry.

Running head: CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

Contemporary Financial and Integrated Reporting

Name of the Student:

Name of the University:

Author Note

Contemporary Financial and Integrated Reporting

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

Table of Contents

Introduction......................................................................................................................................2

Core business of the company.........................................................................................................2

Industry analysis..............................................................................................................................3

Financial structure of the company..................................................................................................3

Key elements of the financial performance of the corporate entity.................................................4

Assets – PPE and Intangibles..........................................................................................................6

References......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Core business of the company.........................................................................................................2

Industry analysis..............................................................................................................................3

Financial structure of the company..................................................................................................3

Key elements of the financial performance of the corporate entity.................................................4

Assets – PPE and Intangibles..........................................................................................................6

References......................................................................................................................................11

2CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

Introduction

The reflection of the operations that are carried out by a single corporate entity are

presented in the accounting statements of the corporations that are published by the business

entities at the end of the financial years. It can be further stated that the particular format in

which these accounting reports are prepared have been established by the Australian Accounting

Standards Board in Australia. This particular study aims to have an overview into the accounting

statements of the corporate entities in order to ensure the fact that the accounting statements have

been prepared in accordance to the regulatory standards that have been laid down by the

accounting regulatory bodies in Australia.

The corporate entity that has been chosen for the purpose of the study is the BHP Billiton

Limited and the particular company that has been chosen for the purpose of the comparison is

Rio Tinto. This study also aims to have an overview into the accounting treatments and rules that

have been utilized for the purpose of ascertaining the fact whether the financial statements have

been prepared in compliance with the same.

Introduction

The reflection of the operations that are carried out by a single corporate entity are

presented in the accounting statements of the corporations that are published by the business

entities at the end of the financial years. It can be further stated that the particular format in

which these accounting reports are prepared have been established by the Australian Accounting

Standards Board in Australia. This particular study aims to have an overview into the accounting

statements of the corporate entities in order to ensure the fact that the accounting statements have

been prepared in accordance to the regulatory standards that have been laid down by the

accounting regulatory bodies in Australia.

The corporate entity that has been chosen for the purpose of the study is the BHP Billiton

Limited and the particular company that has been chosen for the purpose of the comparison is

Rio Tinto. This study also aims to have an overview into the accounting treatments and rules that

have been utilized for the purpose of ascertaining the fact whether the financial statements have

been prepared in compliance with the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

Core business of the company

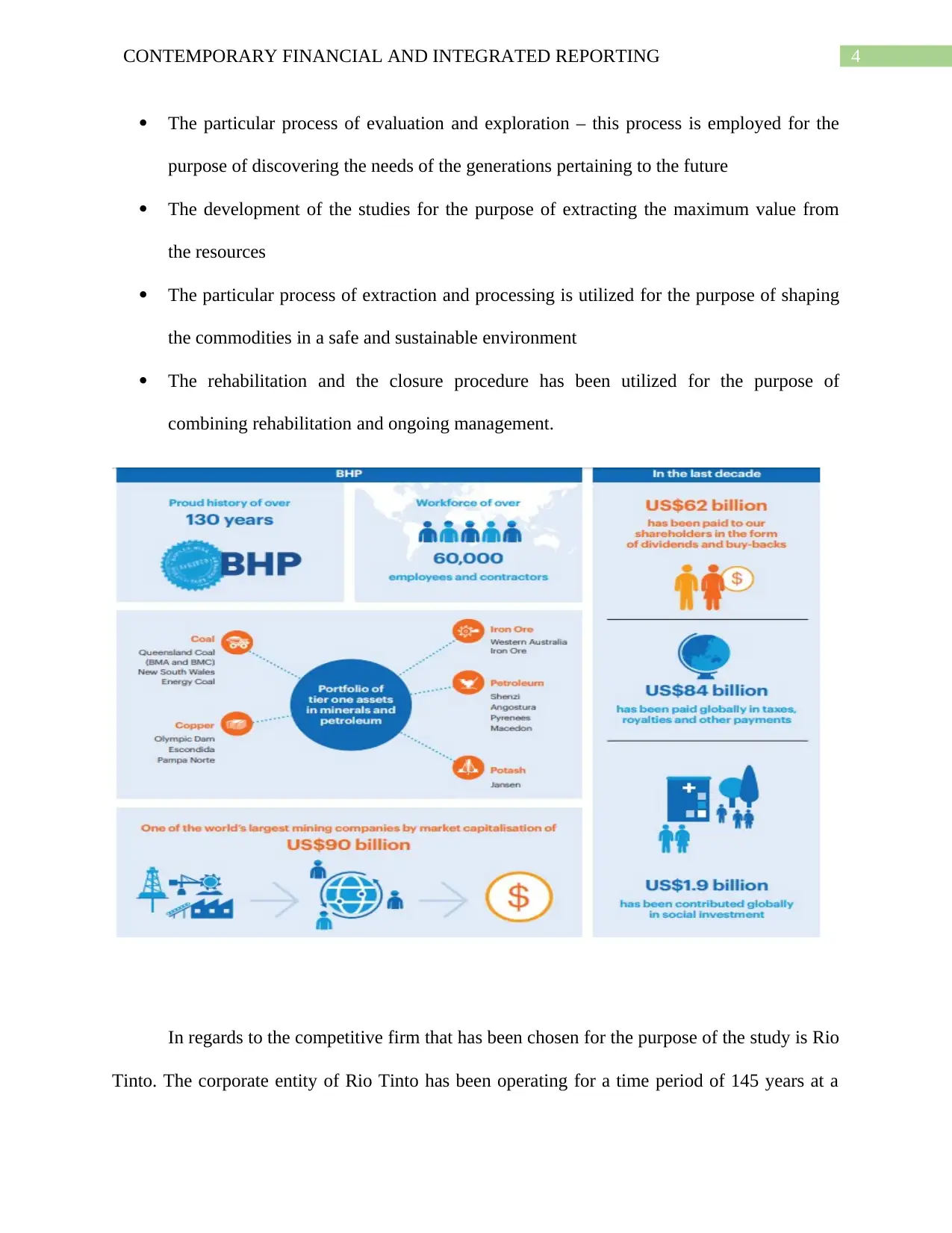

The core business of the chosen company that is BHP Billiton Limited is that the

business organization has been one of the world’s leading resource companies. Furthermore, the

corporate entity primary deals in the processing of the different natural resources like the

minerals, gas and oil. The corporate organization holds a number of 60000 employees and carries

out operations primarily in Australia and America. The products of the company are sold on a

worldwide basis and particularly the marketing and the sales activities are carried out worldwide

through Singapore, Houston and Australia. BHP has been one of the most popular corporate

entities and has been listed on the Australian Stock Exchange. The global headquarter of the

corporate entity has been situated in Melbourne, Australia. The different activities that have been

carried out the business entity are as follows:

Core business of the company

The core business of the chosen company that is BHP Billiton Limited is that the

business organization has been one of the world’s leading resource companies. Furthermore, the

corporate entity primary deals in the processing of the different natural resources like the

minerals, gas and oil. The corporate organization holds a number of 60000 employees and carries

out operations primarily in Australia and America. The products of the company are sold on a

worldwide basis and particularly the marketing and the sales activities are carried out worldwide

through Singapore, Houston and Australia. BHP has been one of the most popular corporate

entities and has been listed on the Australian Stock Exchange. The global headquarter of the

corporate entity has been situated in Melbourne, Australia. The different activities that have been

carried out the business entity are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

The particular process of evaluation and exploration – this process is employed for the

purpose of discovering the needs of the generations pertaining to the future

The development of the studies for the purpose of extracting the maximum value from

the resources

The particular process of extraction and processing is utilized for the purpose of shaping

the commodities in a safe and sustainable environment

The rehabilitation and the closure procedure has been utilized for the purpose of

combining rehabilitation and ongoing management.

In regards to the competitive firm that has been chosen for the purpose of the study is Rio

Tinto. The corporate entity of Rio Tinto has been operating for a time period of 145 years at a

The particular process of evaluation and exploration – this process is employed for the

purpose of discovering the needs of the generations pertaining to the future

The development of the studies for the purpose of extracting the maximum value from

the resources

The particular process of extraction and processing is utilized for the purpose of shaping

the commodities in a safe and sustainable environment

The rehabilitation and the closure procedure has been utilized for the purpose of

combining rehabilitation and ongoing management.

In regards to the competitive firm that has been chosen for the purpose of the study is Rio

Tinto. The corporate entity of Rio Tinto has been operating for a time period of 145 years at a

5CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

stretch. The corporate entity of Rio Tinto has been dealing in the production of the materials that

have been essential to the human existence. The company has been dealing in the materials that

are needed infrastructure, buildings and the network of the transports. The firm deals in a number

of 47000 employees and carries an improved set of values. The particular operations that this

firm deals in range between varieties of products like the iron ore, alumina, bauxite and

aluminum. The other products that are produced by this corporate entity are diamonds, gold,

silver and molybdenum and other energy and minerals (Yong, Lim and Tan 2016).

Industry analysis

The industrial analysis that has been carried out pertains to the fact that the ongoing

process of the recovery has been accelerated at a rate of 3% in the financial year of 2017. The

particular sector that has experienced a sincere growth is the mining sector. The aluminum prices

have also increased in the recent times. The iron ore prices had also experienced a major lift in

the recent times. Therefore, it can be concluded from the above information that the particular

industry of resources has been experiencing significant growth. Furthermore, it can be reliably

stated that the corporate entities belonging to this particular industry has been operating at an

improved state and the particular industry has much chances of further enhancing and improving

in the future. Moreover, the factors that have been enhancing the industry structure are the

availability of skilled and unskilled labor in this particular sector, availability of the raw

materials and the necessary equipment and other related factors (Huber 2017).

stretch. The corporate entity of Rio Tinto has been dealing in the production of the materials that

have been essential to the human existence. The company has been dealing in the materials that

are needed infrastructure, buildings and the network of the transports. The firm deals in a number

of 47000 employees and carries an improved set of values. The particular operations that this

firm deals in range between varieties of products like the iron ore, alumina, bauxite and

aluminum. The other products that are produced by this corporate entity are diamonds, gold,

silver and molybdenum and other energy and minerals (Yong, Lim and Tan 2016).

Industry analysis

The industrial analysis that has been carried out pertains to the fact that the ongoing

process of the recovery has been accelerated at a rate of 3% in the financial year of 2017. The

particular sector that has experienced a sincere growth is the mining sector. The aluminum prices

have also increased in the recent times. The iron ore prices had also experienced a major lift in

the recent times. Therefore, it can be concluded from the above information that the particular

industry of resources has been experiencing significant growth. Furthermore, it can be reliably

stated that the corporate entities belonging to this particular industry has been operating at an

improved state and the particular industry has much chances of further enhancing and improving

in the future. Moreover, the factors that have been enhancing the industry structure are the

availability of skilled and unskilled labor in this particular sector, availability of the raw

materials and the necessary equipment and other related factors (Huber 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

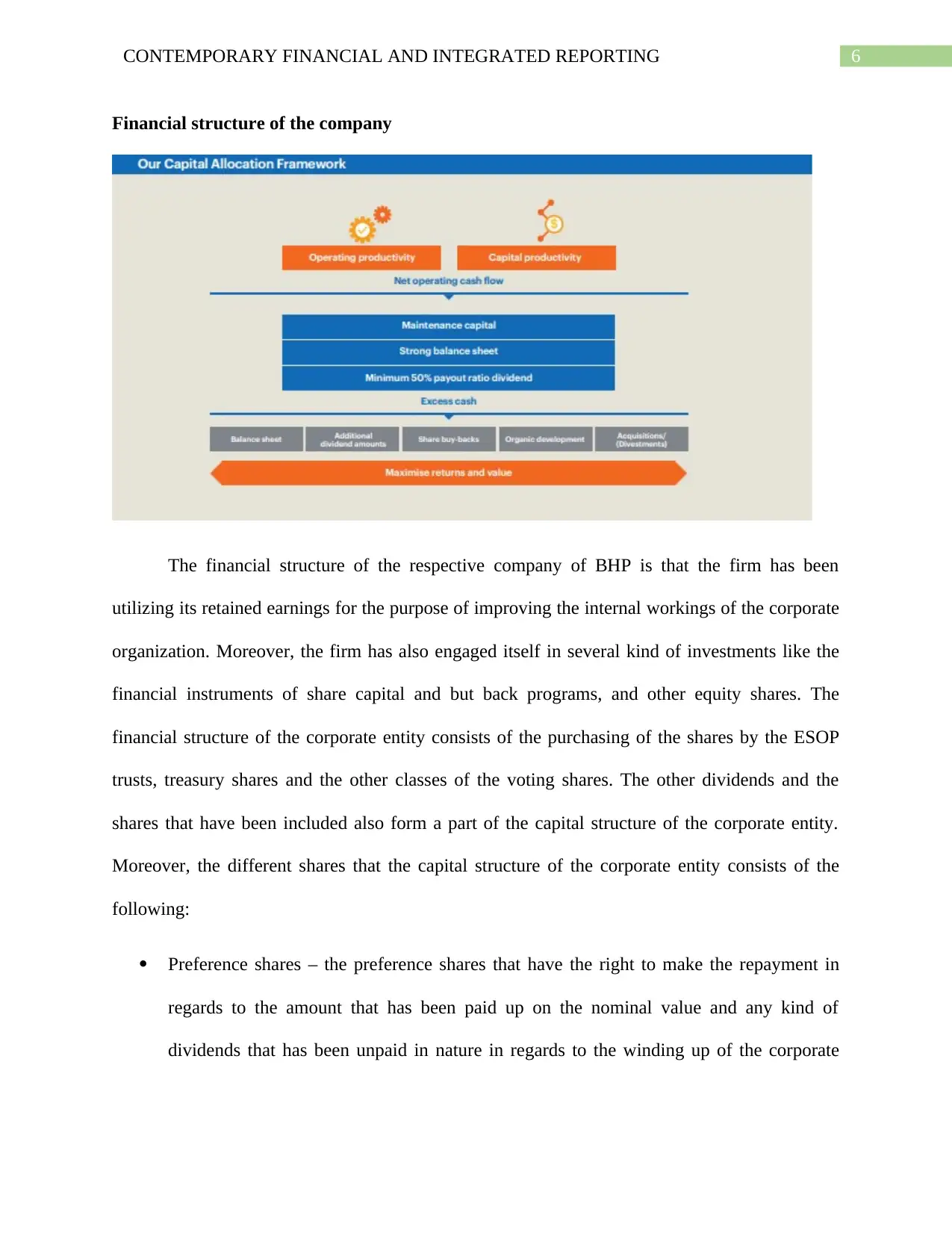

Financial structure of the company

The financial structure of the respective company of BHP is that the firm has been

utilizing its retained earnings for the purpose of improving the internal workings of the corporate

organization. Moreover, the firm has also engaged itself in several kind of investments like the

financial instruments of share capital and but back programs, and other equity shares. The

financial structure of the corporate entity consists of the purchasing of the shares by the ESOP

trusts, treasury shares and the other classes of the voting shares. The other dividends and the

shares that have been included also form a part of the capital structure of the corporate entity.

Moreover, the different shares that the capital structure of the corporate entity consists of the

following:

Preference shares – the preference shares that have the right to make the repayment in

regards to the amount that has been paid up on the nominal value and any kind of

dividends that has been unpaid in nature in regards to the winding up of the corporate

Financial structure of the company

The financial structure of the respective company of BHP is that the firm has been

utilizing its retained earnings for the purpose of improving the internal workings of the corporate

organization. Moreover, the firm has also engaged itself in several kind of investments like the

financial instruments of share capital and but back programs, and other equity shares. The

financial structure of the corporate entity consists of the purchasing of the shares by the ESOP

trusts, treasury shares and the other classes of the voting shares. The other dividends and the

shares that have been included also form a part of the capital structure of the corporate entity.

Moreover, the different shares that the capital structure of the corporate entity consists of the

following:

Preference shares – the preference shares that have the right to make the repayment in

regards to the amount that has been paid up on the nominal value and any kind of

dividends that has been unpaid in nature in regards to the winding up of the corporate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

entities. The holders of the preference shares have resulting in the limitation of the voting

rights.

Treasury shares – the treasury shares are the shares that have been recognized at cost and

have been deducted at equity. When the treasury shares that have been recognized at cost

and have been subtracted from the equity. Any kind of difference between the

consideration and the carrying amounts if have been reissued has been recognized in the

form of retained earnings (Kabir, Rahman and Su 2017).

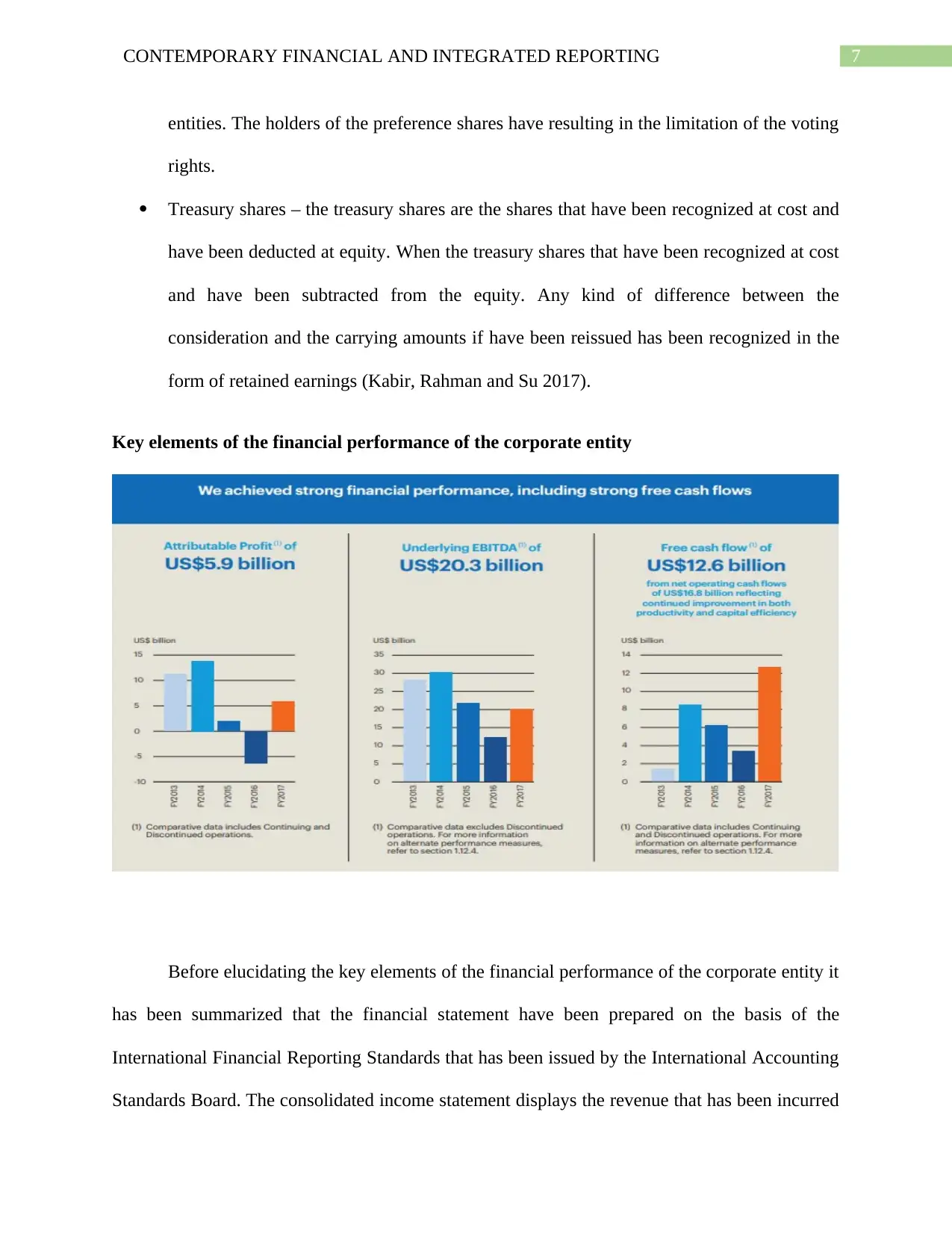

Key elements of the financial performance of the corporate entity

Before elucidating the key elements of the financial performance of the corporate entity it

has been summarized that the financial statement have been prepared on the basis of the

International Financial Reporting Standards that has been issued by the International Accounting

Standards Board. The consolidated income statement displays the revenue that has been incurred

entities. The holders of the preference shares have resulting in the limitation of the voting

rights.

Treasury shares – the treasury shares are the shares that have been recognized at cost and

have been deducted at equity. When the treasury shares that have been recognized at cost

and have been subtracted from the equity. Any kind of difference between the

consideration and the carrying amounts if have been reissued has been recognized in the

form of retained earnings (Kabir, Rahman and Su 2017).

Key elements of the financial performance of the corporate entity

Before elucidating the key elements of the financial performance of the corporate entity it

has been summarized that the financial statement have been prepared on the basis of the

International Financial Reporting Standards that has been issued by the International Accounting

Standards Board. The consolidated income statement displays the revenue that has been incurred

8CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

by the corporate entities. The consolidated balance sheet that has been included in the financial

statements the net profit that has been incurred by the firms has been shown in the consolidated

income statement and has been of the amount $11,753. Furthermore, the consolidated balance

sheet that has been prepared by the corporate entity consists of the components of total assets,

net assets, share capital and the total amount of equity that has been attributed to the shareholders

of the organization of BHP. The total assets of the firm pertains to the amount of $117,006. The

net assets of the firm has been of the particular amount of $62726. The share capital of the

corporate entity that includes the share premiums of $2761 and the total amount of equity that

has been attributed to the shareholders have been included in the financial statements of the

corporate entities and have been of the amount of $57,528. Moreover, the consolidated cash flow

statement that has been included in the accounting statements of the corporate entity is that the

net operating cash flows have been of the amount of $16,804. The other financial information

that has been included in the corporate accounting disclosures of the annual report of the

corporate entity has been that the net debt has been of the amount of $16,321, the underlying

profit that can be attributed has been of the amount of $6732, the underlying EBITDA,

underlying EBIT and the underlying basic earnings per share. These financial components have

been of the amount of $16321, $6732, $20296, @12,389 and $126.5 respectively. It must be

noted here that one of the most significant factor in regards to the corporate reporting is that the

books of accounts or the financial statements includes the financial component of other incomes

that includes the following items:

Expenses in regards to benefits of the employees

Changes in the inventories in regards to the finished goods and work in progress

Raw materials that have been utilized

by the corporate entities. The consolidated balance sheet that has been included in the financial

statements the net profit that has been incurred by the firms has been shown in the consolidated

income statement and has been of the amount $11,753. Furthermore, the consolidated balance

sheet that has been prepared by the corporate entity consists of the components of total assets,

net assets, share capital and the total amount of equity that has been attributed to the shareholders

of the organization of BHP. The total assets of the firm pertains to the amount of $117,006. The

net assets of the firm has been of the particular amount of $62726. The share capital of the

corporate entity that includes the share premiums of $2761 and the total amount of equity that

has been attributed to the shareholders have been included in the financial statements of the

corporate entities and have been of the amount of $57,528. Moreover, the consolidated cash flow

statement that has been included in the accounting statements of the corporate entity is that the

net operating cash flows have been of the amount of $16,804. The other financial information

that has been included in the corporate accounting disclosures of the annual report of the

corporate entity has been that the net debt has been of the amount of $16,321, the underlying

profit that can be attributed has been of the amount of $6732, the underlying EBITDA,

underlying EBIT and the underlying basic earnings per share. These financial components have

been of the amount of $16321, $6732, $20296, @12,389 and $126.5 respectively. It must be

noted here that one of the most significant factor in regards to the corporate reporting is that the

books of accounts or the financial statements includes the financial component of other incomes

that includes the following items:

Expenses in regards to benefits of the employees

Changes in the inventories in regards to the finished goods and work in progress

Raw materials that have been utilized

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

Transportation and freight

External services

Purchase of the commodity by the third parties

The royalties of the government that can be paid or is payable

Evaluation and exploration of the particular expenses that have been incurred by the

firms

Asset impairment

Lease operating rentals

All other operating expenses.

The particular financial component that has been reported after the occurrence of the

reporting date is the financial item of loans and receivables. It has been mentioned in the

accounting report of the corporate entity that in case of the loans and receivables that has been

disclosed after a period of 12 months or more is included under the head of the non-current

assets. This is because the non-current assets refer to those particular assets that have been

realized post the period of more than twelve months.

It must be noted here that no financial disclosures have been provided in the accounting

report of the corporate organization in regards to the fact that there has been a change in the

application of the accounting policies. Therefore, it can be reliably assumed that no change has

been brought about in the treatment of the financial components as directed by the Australian

Accounting Standards Board.

Transportation and freight

External services

Purchase of the commodity by the third parties

The royalties of the government that can be paid or is payable

Evaluation and exploration of the particular expenses that have been incurred by the

firms

Asset impairment

Lease operating rentals

All other operating expenses.

The particular financial component that has been reported after the occurrence of the

reporting date is the financial item of loans and receivables. It has been mentioned in the

accounting report of the corporate entity that in case of the loans and receivables that has been

disclosed after a period of 12 months or more is included under the head of the non-current

assets. This is because the non-current assets refer to those particular assets that have been

realized post the period of more than twelve months.

It must be noted here that no financial disclosures have been provided in the accounting

report of the corporate organization in regards to the fact that there has been a change in the

application of the accounting policies. Therefore, it can be reliably assumed that no change has

been brought about in the treatment of the financial components as directed by the Australian

Accounting Standards Board.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

Assets – PPE and Intangibles

The carrying amount of each of the classes of property, plant and equipment that has been

disclosed in the accounting report of the corporate entity at the reporting date is $80.5 billion. It

must be noted here that the particular accounting standard that has been utilized by the corporate

entity of BHP refers to the particular accounting standard of AASB 116 (Dunbar and Laing

2017).

The intangible assets that has been included in the accounting statements of the corporate

disclosures have been the particular financial component of goodwill and other intangibles. Here,

goodwill refers to the quantified reputation that has been achieved by the firm in the outside

world. The other intangibles include the components of software, licenses and the initial

requirement that is needed for the purpose of acquiring the mineral lease assets (Newberry

2015).

Furthermore, the accounting policy that has been adopted by the corporate entity for the

treatment of the intangible assets is AASB 138 which states the particular format in which the

intangible assets should be valued and measured (Kabir, Rahman and Su 2017).

It has been mentioned in the accounting report of the corporate entity that the non-current

assets have been impaired. The valuation has been calculated using the FVLCD method.

Furthermore, it can be stated that the valuations have been based primarily on the level 3 inputs.

Moreover, the impairment loss that has been incurred by the firm in regards to the non-current

assets have been of the amount of $160 million. This means that corporate entity has carried out

fair value of the financial components which has resulted in a loss (Newberry 2015).

Assets – PPE and Intangibles

The carrying amount of each of the classes of property, plant and equipment that has been

disclosed in the accounting report of the corporate entity at the reporting date is $80.5 billion. It

must be noted here that the particular accounting standard that has been utilized by the corporate

entity of BHP refers to the particular accounting standard of AASB 116 (Dunbar and Laing

2017).

The intangible assets that has been included in the accounting statements of the corporate

disclosures have been the particular financial component of goodwill and other intangibles. Here,

goodwill refers to the quantified reputation that has been achieved by the firm in the outside

world. The other intangibles include the components of software, licenses and the initial

requirement that is needed for the purpose of acquiring the mineral lease assets (Newberry

2015).

Furthermore, the accounting policy that has been adopted by the corporate entity for the

treatment of the intangible assets is AASB 138 which states the particular format in which the

intangible assets should be valued and measured (Kabir, Rahman and Su 2017).

It has been mentioned in the accounting report of the corporate entity that the non-current

assets have been impaired. The valuation has been calculated using the FVLCD method.

Furthermore, it can be stated that the valuations have been based primarily on the level 3 inputs.

Moreover, the impairment loss that has been incurred by the firm in regards to the non-current

assets have been of the amount of $160 million. This means that corporate entity has carried out

fair value of the financial components which has resulted in a loss (Newberry 2015).

11CONTEMPORARY FINANCIAL AND INTEGRATED REPORTING

Voluntary disclosures made by both the companies:

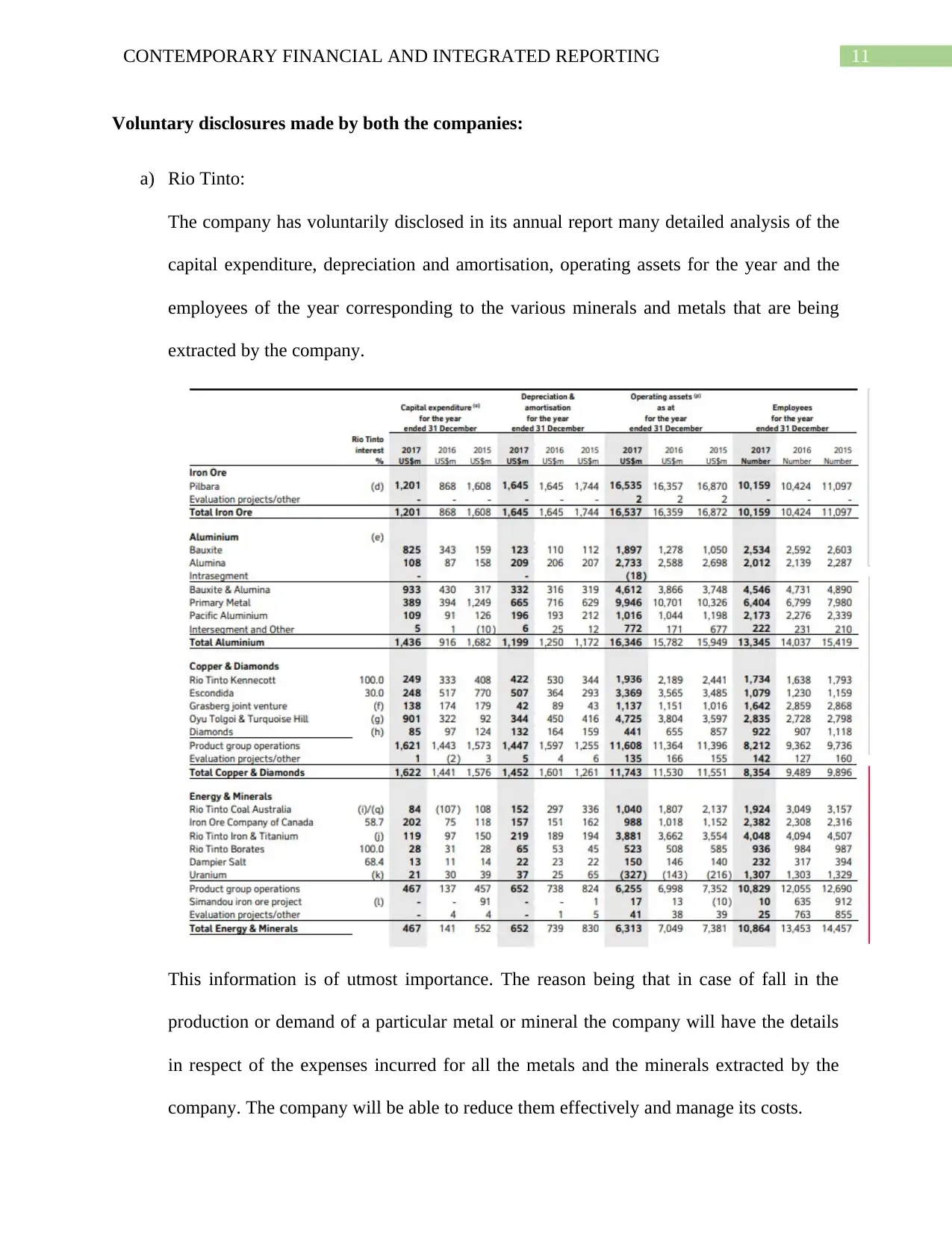

a) Rio Tinto:

The company has voluntarily disclosed in its annual report many detailed analysis of the

capital expenditure, depreciation and amortisation, operating assets for the year and the

employees of the year corresponding to the various minerals and metals that are being

extracted by the company.

This information is of utmost importance. The reason being that in case of fall in the

production or demand of a particular metal or mineral the company will have the details

in respect of the expenses incurred for all the metals and the minerals extracted by the

company. The company will be able to reduce them effectively and manage its costs.

Voluntary disclosures made by both the companies:

a) Rio Tinto:

The company has voluntarily disclosed in its annual report many detailed analysis of the

capital expenditure, depreciation and amortisation, operating assets for the year and the

employees of the year corresponding to the various minerals and metals that are being

extracted by the company.

This information is of utmost importance. The reason being that in case of fall in the

production or demand of a particular metal or mineral the company will have the details

in respect of the expenses incurred for all the metals and the minerals extracted by the

company. The company will be able to reduce them effectively and manage its costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.