Analysis of Contemporary Financial & Integrated Reporting Comparison

VerifiedAdded on 2021/06/16

|17

|4426

|37

Report

AI Summary

This report offers a comparative analysis of the annual reports of Cochlear Limited and CSL Limited, both prominent healthcare companies listed on the ASX. The study delves into their core businesses, operating activities, and financial performance over several years, examining revenue, net profit, and financial structures. It scrutinizes key elements of their financial statements, including Property, Plant, and Equipment (PPE), intangible assets, and accounting policies related to depreciation and impairment. The report also explores voluntary disclosures, deferred tax assets and liabilities, and the companies' approaches to funding. By comparing these aspects, the report provides insights into the financial health and strategic decisions of both companies, offering a comprehensive understanding of their financial reporting practices and performance within the healthcare industry. The analysis includes detailed comparisons of financial figures, accounting policies, and the composition of assets, providing a robust understanding of each company's financial position.

Running head: CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

Contemporary Financial & Integrated Reporting

Name of Student:

Name of University:

Author’s Note:

Contemporary Financial & Integrated Reporting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

Executive Summary

The report intends to interpret and compare the annual report published by Cochlear Limited and

CSL Limed which are listed in ASX. It has been further discerned that both the companies

contribute to the healthcare industry and hence recognized from the same industry. Some of the

main interpretations of the study will describe the core business of the company and provide

complete details of the business segments. It further aims to discuss the industry in which it

operates and give the rationale whether it is growing are declining in nature. It further aims to

critically analyse the financial structure and address how the company is funded with its internal

and external sources. Some of the main research aspects has further described about the key

elements of financial performance report. The next section has included interpretations about

assets such as PPE and Intangibles. This section has analysed and compared the “carrying

amount of each class of Property, Plant, and Equipment, at reporting date” for both the

companies. The discourse of the study has further included the policies associated to “Property,

Plant, and Equipment”. The main findings have been able to reveal that the Cochlear measures

the value of the “Property, Plant, and Equipment” as the cost of asset, minus accumulated

depreciation and impairment loss. The cost of asset is considered as per the incidental costs

which are directly attributable to the acquisition. CSL Limited The depreciation charges

depreciation on the useful life of the assets based on straight-line method. Buildings are

depreciated 5-40 years as per “straight-line method”, plant and equipment are depreciated 3-15

years “straight-line method” and lease improvements are depreciated 5-10 as per “straight-line

method”. The depictions of financial statement of Cochlear Limited have shown that the total

deferred tax amounted to $ 66586 in 2017 and $ 77144 in 2016. In addition to this, the deferred

tax liabilities that identified with $ 5837 in 2017 and 7122 in 2016. The total deferred tax asset

for CSL Limited in 2017 has been depicted as $ 496.5 million and in 2016 as 389 million.

Additionally, the total deferred tax liabilities have amounted to $ 138.2 million in 2017 and

119.2 million in 2016.

Executive Summary

The report intends to interpret and compare the annual report published by Cochlear Limited and

CSL Limed which are listed in ASX. It has been further discerned that both the companies

contribute to the healthcare industry and hence recognized from the same industry. Some of the

main interpretations of the study will describe the core business of the company and provide

complete details of the business segments. It further aims to discuss the industry in which it

operates and give the rationale whether it is growing are declining in nature. It further aims to

critically analyse the financial structure and address how the company is funded with its internal

and external sources. Some of the main research aspects has further described about the key

elements of financial performance report. The next section has included interpretations about

assets such as PPE and Intangibles. This section has analysed and compared the “carrying

amount of each class of Property, Plant, and Equipment, at reporting date” for both the

companies. The discourse of the study has further included the policies associated to “Property,

Plant, and Equipment”. The main findings have been able to reveal that the Cochlear measures

the value of the “Property, Plant, and Equipment” as the cost of asset, minus accumulated

depreciation and impairment loss. The cost of asset is considered as per the incidental costs

which are directly attributable to the acquisition. CSL Limited The depreciation charges

depreciation on the useful life of the assets based on straight-line method. Buildings are

depreciated 5-40 years as per “straight-line method”, plant and equipment are depreciated 3-15

years “straight-line method” and lease improvements are depreciated 5-10 as per “straight-line

method”. The depictions of financial statement of Cochlear Limited have shown that the total

deferred tax amounted to $ 66586 in 2017 and $ 77144 in 2016. In addition to this, the deferred

tax liabilities that identified with $ 5837 in 2017 and 7122 in 2016. The total deferred tax asset

for CSL Limited in 2017 has been depicted as $ 496.5 million and in 2016 as 389 million.

Additionally, the total deferred tax liabilities have amounted to $ 138.2 million in 2017 and

119.2 million in 2016.

2CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

Table of Contents

Introduction......................................................................................................................................3

Company- Introduction, Business & operating activities, Finances and Financial performance....3

Assets – PPE and Intangibles..........................................................................................................5

Leases..............................................................................................................................................7

Voluntary Disclosures.....................................................................................................................8

Accounting for Tax........................................................................................................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

Table of Contents

Introduction......................................................................................................................................3

Company- Introduction, Business & operating activities, Finances and Financial performance....3

Assets – PPE and Intangibles..........................................................................................................5

Leases..............................................................................................................................................7

Voluntary Disclosures.....................................................................................................................8

Accounting for Tax........................................................................................................................12

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

Introduction

The discourse of the report aims to analyse and compare the latest annual report

published by Cochlear Limited and CSL Limed which are listed in ASX. It has been further

discerned that both the companies contribute to the healthcare industry and hence recognized

from the same industry. Some of the main interpretations of the study will describe the core

business of the company and provide complete details of the business segments. It further aims

to discuss the industry in which it operates and give the rationale whether it is growing are

declining in nature. It further aims to critically analyse the financial structure and address how

the company is funded with its internal and external sources. Some of the main research aspects

has further described about the key elements of financial performance report. The next section

has included interpretations about assets such as PPE and Intangibles. This section has analysed

and compared the “carrying amount of each class of Property, Plant, and Equipment, at reporting

date” for both the companies. The discourse of the study has further included the policies

associated to “Property, Plant, and Equipment”. Some of the other depictions of the report has

stated on the composition and relevance of intangible assets. The next section of the study has

determined the real event disclosures associated to the value of lease assets and liabilities. In this

section the study has disclosed the accounts in relation to the lease liabilities and assets. The

fourth section of the report has included assessment for identification of two voluntary

disclosures made by the company in its annual report and this has been also stated with relevance

to the company’s business. The final section has determined the values of “Deferred Tax Assets

and Deferred Tax Liabilities” which are disclosed by the company. This section has further

explained the rationale of using the information provided by the company in the notes to

financial statements (Weygandt, Kimmel and Kieso 2015).

Company- Introduction, Business & operating activities, Finances and Financial

performance

Cochlear Limited headquartered in Sydney is recognized as a medical device company is

designs, supplies and manufacturers “Nucleus cochlear implant, Baha bone conduction implant

and Hybrid electro-acoustic implant”. The operating activities of the company includes

producing three implants for varied range of medical situations. The nucleus is a system which is

Introduction

The discourse of the report aims to analyse and compare the latest annual report

published by Cochlear Limited and CSL Limed which are listed in ASX. It has been further

discerned that both the companies contribute to the healthcare industry and hence recognized

from the same industry. Some of the main interpretations of the study will describe the core

business of the company and provide complete details of the business segments. It further aims

to discuss the industry in which it operates and give the rationale whether it is growing are

declining in nature. It further aims to critically analyse the financial structure and address how

the company is funded with its internal and external sources. Some of the main research aspects

has further described about the key elements of financial performance report. The next section

has included interpretations about assets such as PPE and Intangibles. This section has analysed

and compared the “carrying amount of each class of Property, Plant, and Equipment, at reporting

date” for both the companies. The discourse of the study has further included the policies

associated to “Property, Plant, and Equipment”. Some of the other depictions of the report has

stated on the composition and relevance of intangible assets. The next section of the study has

determined the real event disclosures associated to the value of lease assets and liabilities. In this

section the study has disclosed the accounts in relation to the lease liabilities and assets. The

fourth section of the report has included assessment for identification of two voluntary

disclosures made by the company in its annual report and this has been also stated with relevance

to the company’s business. The final section has determined the values of “Deferred Tax Assets

and Deferred Tax Liabilities” which are disclosed by the company. This section has further

explained the rationale of using the information provided by the company in the notes to

financial statements (Weygandt, Kimmel and Kieso 2015).

Company- Introduction, Business & operating activities, Finances and Financial

performance

Cochlear Limited headquartered in Sydney is recognized as a medical device company is

designs, supplies and manufacturers “Nucleus cochlear implant, Baha bone conduction implant

and Hybrid electro-acoustic implant”. The operating activities of the company includes

producing three implants for varied range of medical situations. The nucleus is a system which is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

a combination of electrical stimulation instrument which is surgically implanted in the backside

of patients ear. This device is able to process the captured sound and sends the signal to the brain

via electrode array. This product is further identified to be a direct descendent of original

cochlear implant. Nucleus was recognized as the first cochlear implant which was approved by

“U.S. Food and Drug Administration”. Hybrid is identified as it electroacoustic system which is

a combination of Cochlear implant with an acoustic hearing aid and appropriate for patients

having residual hearing at lower frequencies (Millo, Barman and Hall 2016). They implant of

hybrid system is considered as the smaller variant for Nucleas with an electrode which relays

oily high-frequency sounds. Whereas, the acoustic device amplifies the newer frequency sounds

and transmits the same to the brain. Baha is depicted as a bone conduction system which

comprises of small titanium implant which is integrated with the bone behind a patient's ear. The

depictions of the financial performance as per the annual report has shown that the company

successfully increasing both sales revenue and net profit in the last three years. This is evident

with sales revenue of 821 million in 2014, 942 million in 2015 and 1158 million in 2016. The

improvement in the net profit is depicted with adjusted net profit of 110 million in financial year

2014, 146 million in 2015 and 189 million in 2016. As per the depictions of the annual report it

is understood that the company relies on internal sources for finance. The changes in the changes

in accounting policies disclosures are identified with "Note 4.2 – Employee benefit liabilities,

Note 4.3 – Share based payments, Note 5.3 – Intangible assets, Note 5.4 – Business

combinations, Note 5.6 – Provisions, Note 5.7 – Contingent liabilities and Note 6.4 – Financial

risk management" (Warren 2016).

CSL Limited is recognized with Global specialty in biotechnology and marketing

products to treat and prevent various types of serious human medical conditions. Some of the

operating line of the production unaffected by the company includes “blood plasma derivatives,

vaccines, antivenom, and cell culture reagents”. These are mainly required for various medical

and genetic research and applications. The company standouts out to its promise for being a

global pioneer in delivering biotechnology solutions and innovative medicines which protects

public health and helps the individuals in life-threatening medical conditions live full life. CSL

commenced its operations in vacant “Walter and Eliza Hall Institute building at the Melbourne

Hospital in 1918”, prior to which it operated in Parkville premises. Some of the major

achievements of the company includes, early production of insulin, development of tetanus

a combination of electrical stimulation instrument which is surgically implanted in the backside

of patients ear. This device is able to process the captured sound and sends the signal to the brain

via electrode array. This product is further identified to be a direct descendent of original

cochlear implant. Nucleus was recognized as the first cochlear implant which was approved by

“U.S. Food and Drug Administration”. Hybrid is identified as it electroacoustic system which is

a combination of Cochlear implant with an acoustic hearing aid and appropriate for patients

having residual hearing at lower frequencies (Millo, Barman and Hall 2016). They implant of

hybrid system is considered as the smaller variant for Nucleas with an electrode which relays

oily high-frequency sounds. Whereas, the acoustic device amplifies the newer frequency sounds

and transmits the same to the brain. Baha is depicted as a bone conduction system which

comprises of small titanium implant which is integrated with the bone behind a patient's ear. The

depictions of the financial performance as per the annual report has shown that the company

successfully increasing both sales revenue and net profit in the last three years. This is evident

with sales revenue of 821 million in 2014, 942 million in 2015 and 1158 million in 2016. The

improvement in the net profit is depicted with adjusted net profit of 110 million in financial year

2014, 146 million in 2015 and 189 million in 2016. As per the depictions of the annual report it

is understood that the company relies on internal sources for finance. The changes in the changes

in accounting policies disclosures are identified with "Note 4.2 – Employee benefit liabilities,

Note 4.3 – Share based payments, Note 5.3 – Intangible assets, Note 5.4 – Business

combinations, Note 5.6 – Provisions, Note 5.7 – Contingent liabilities and Note 6.4 – Financial

risk management" (Warren 2016).

CSL Limited is recognized with Global specialty in biotechnology and marketing

products to treat and prevent various types of serious human medical conditions. Some of the

operating line of the production unaffected by the company includes “blood plasma derivatives,

vaccines, antivenom, and cell culture reagents”. These are mainly required for various medical

and genetic research and applications. The company standouts out to its promise for being a

global pioneer in delivering biotechnology solutions and innovative medicines which protects

public health and helps the individuals in life-threatening medical conditions live full life. CSL

commenced its operations in vacant “Walter and Eliza Hall Institute building at the Melbourne

Hospital in 1918”, prior to which it operated in Parkville premises. Some of the major

achievements of the company includes, early production of insulin, development of tetanus

5CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

vaccine, developing combined vaccine for diphtheria, whooping cough auntie Dennis. The

companies often known for its collaboration with world's first human “papillomavirus vaccine,

Gardasil, building on the pioneering work by Professor Ian Frazer (1994-2005)”. The depictions

based on the financial performance it has been identified that the company has been able to

significantly improve in areas of operating revenue, sales revenue, R&D investment, profit

before income tax expenses, net profit after tax, net cash inflow from operating activities, capital

investment, return on invested capital and basic earnings per-share. The total net profit after tax

has increased from $ 1242 million in 2015 to $ 1337 million in 2016. In addition to this, CSL

awning per-share has improved from $ 2.69 in financially year 15 to 16 to $ 2.94 in financial

year 16 to 17. It has been further discerned that the total operating revenues of the company has

significantly improved in the last five years. This is evident with total operating revenue of $

5100 million in 2012, 5504 million in 2013, 5612 million in 2014, 6115 million in 2015 and

6923 million in 2016. As per the depictions of the annual report it is understood that the

company relies on internal sources for finance. Some of the applicable accounting policies in the

year ended June 2019 has been identified with “AASB 9-Disclosures to financial instruments”

and “AASB 15- Revenue from contracts with customers” (Cataldo and Anthony 2017).

Assets – PPE and Intangibles

The interpretations of annual report of Cochlear Limited has suggested that the

subsequent costs in relation of replacing the asset and complement of property plant and

equipment is capitalized as per carrying amount of the future economic benefits. It has been

depicted that the carrying amount for plant and equipment in 2016 was $ 69425, which increased

to $ 73995 in 2017. The value of the “Property, Plant, and Equipment” is measured as the cost of

asset, minus accumulated depreciation and impairment loss. The cost of asset is considered as

per the incidental costs which are directly attributable to the acquisition. The intangible assets

such as goodwill is accounted by applying acquisition method at the time of business

combination. In addition to this, the goodwill represents the difference among the “cost of

acquisition and fair value of the net identifiable assets acquired”. System costs are also regarded

as intangible assets where the company controls future economic benefits because of the cost

incurred. The composition of the intangible asset is identified with $ 339976 in 2017 and $

224338 in 2016 out of total assets of $ 923,196 in 2017 and $ 816,734 in 2016. This is forming a

vaccine, developing combined vaccine for diphtheria, whooping cough auntie Dennis. The

companies often known for its collaboration with world's first human “papillomavirus vaccine,

Gardasil, building on the pioneering work by Professor Ian Frazer (1994-2005)”. The depictions

based on the financial performance it has been identified that the company has been able to

significantly improve in areas of operating revenue, sales revenue, R&D investment, profit

before income tax expenses, net profit after tax, net cash inflow from operating activities, capital

investment, return on invested capital and basic earnings per-share. The total net profit after tax

has increased from $ 1242 million in 2015 to $ 1337 million in 2016. In addition to this, CSL

awning per-share has improved from $ 2.69 in financially year 15 to 16 to $ 2.94 in financial

year 16 to 17. It has been further discerned that the total operating revenues of the company has

significantly improved in the last five years. This is evident with total operating revenue of $

5100 million in 2012, 5504 million in 2013, 5612 million in 2014, 6115 million in 2015 and

6923 million in 2016. As per the depictions of the annual report it is understood that the

company relies on internal sources for finance. Some of the applicable accounting policies in the

year ended June 2019 has been identified with “AASB 9-Disclosures to financial instruments”

and “AASB 15- Revenue from contracts with customers” (Cataldo and Anthony 2017).

Assets – PPE and Intangibles

The interpretations of annual report of Cochlear Limited has suggested that the

subsequent costs in relation of replacing the asset and complement of property plant and

equipment is capitalized as per carrying amount of the future economic benefits. It has been

depicted that the carrying amount for plant and equipment in 2016 was $ 69425, which increased

to $ 73995 in 2017. The value of the “Property, Plant, and Equipment” is measured as the cost of

asset, minus accumulated depreciation and impairment loss. The cost of asset is considered as

per the incidental costs which are directly attributable to the acquisition. The intangible assets

such as goodwill is accounted by applying acquisition method at the time of business

combination. In addition to this, the goodwill represents the difference among the “cost of

acquisition and fair value of the net identifiable assets acquired”. System costs are also regarded

as intangible assets where the company controls future economic benefits because of the cost

incurred. The composition of the intangible asset is identified with $ 339976 in 2017 and $

224338 in 2016 out of total assets of $ 923,196 in 2017 and $ 816,734 in 2016. This is forming a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

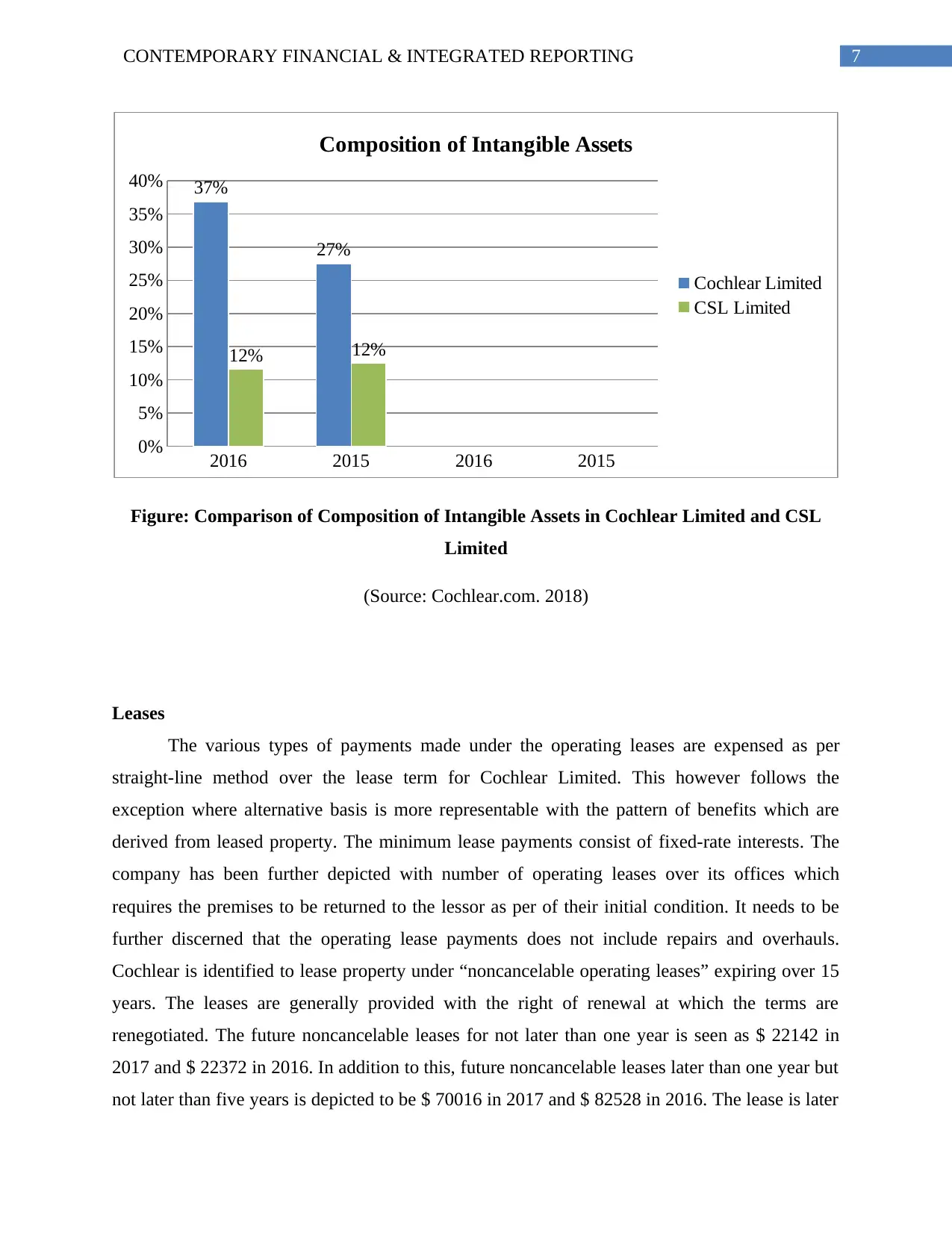

percentage of 36.8% intangibles in 2017 and 27.4% in 2016 respectively. The intangible assets

for the company with indefinite useful life are systematically tested for impairment on an annual

basis (Maynard 2017).

In case of CSL Limited, the value of “Property, Plant, and Equipment” such as land and

buildings, the capital work in progress are recorded at historical cost less the applicable

amortization and depreciation. The depreciation is charged on the useful life of the assets based

on straight-line method. Buildings are depreciated 5-40 years as per “straight-line method”, plant

and equipment are depreciated 3-15 years “straight-line method” and lease improvements are

depreciated 5-10 as per “straight-line method”. The impairment testing of PPE is done when the

impairment trigger is identified (McGuire, Wang and Wilson 2014). Intangible assets are

considered with goodwill, intellectual property and software. The excess of fair value of the

purchase consideration for goodwill is identified with net assets minus incidental expenses which

are recorded as goodwill. It needs to be further understood that goodwill is allocated to the

individual as generating units which represents the lowest value within the group in which

goodwill is monitored. The company believes in amortizing and reviewing for impairment for

those assets which have finite lives. The intangible assets having indefinite useful life are not

subject to amortization and henceforth not tested for impairment. The carrying amount of the

goodwill allocated to the business is seen as $ 688.3 in 2017. It has been further discerned that

goodwill is not amortized but measured at cost less any accumulated impairment losses. The

composition of the intangible asset is discerned with $ 1055.4 million in 2017 and 942.6 million

in 2016 out of total assets of $ 9122.7 in 2017 million and 7562.7 million in 2016. This is

forming a composition percentage of 11.5% intangibles in 2017 and 12.4% in 2016 respectively.

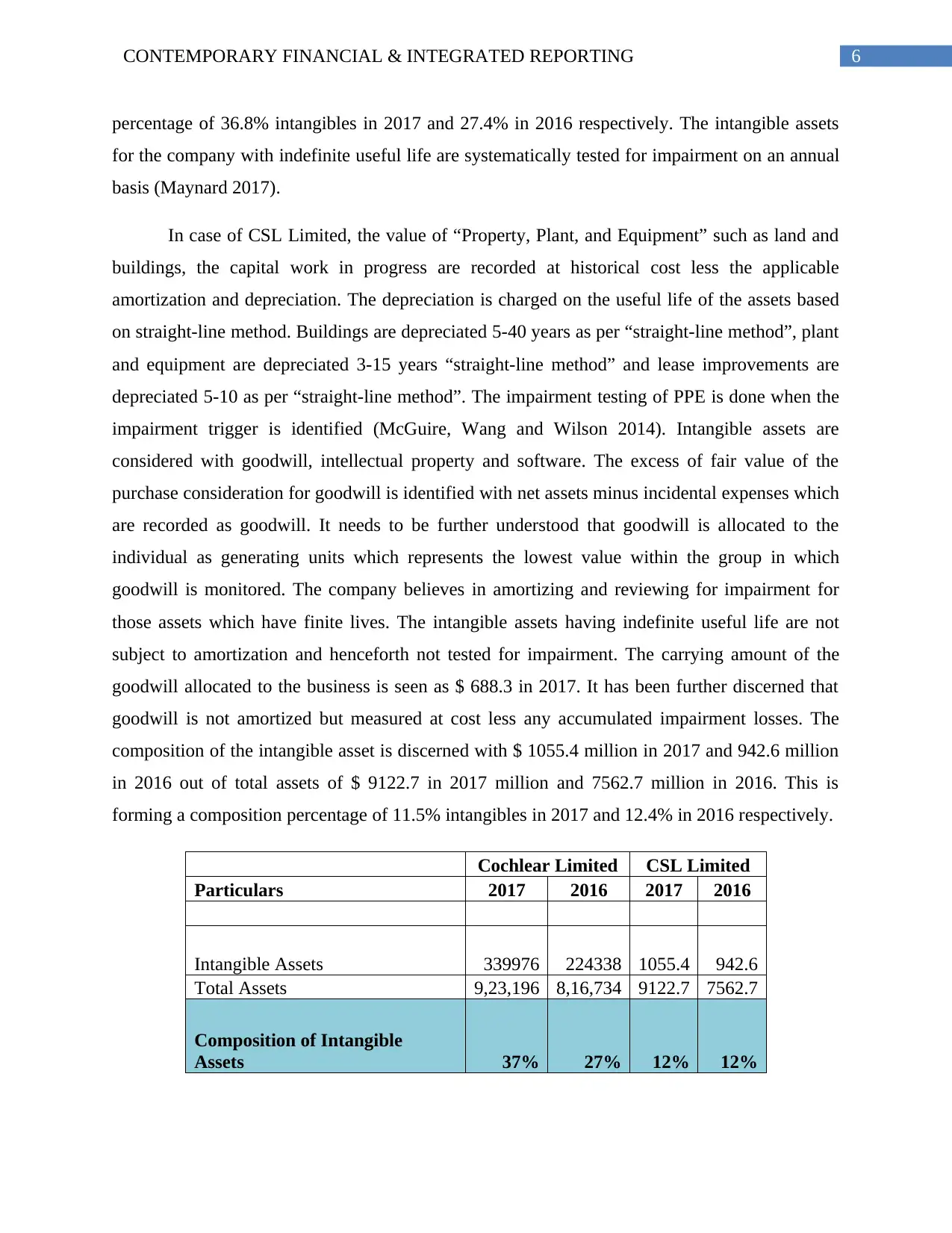

Cochlear Limited CSL Limited

Particulars 2017 2016 2017 2016

Intangible Assets 339976 224338 1055.4 942.6

Total Assets 9,23,196 8,16,734 9122.7 7562.7

Composition of Intangible

Assets 37% 27% 12% 12%

percentage of 36.8% intangibles in 2017 and 27.4% in 2016 respectively. The intangible assets

for the company with indefinite useful life are systematically tested for impairment on an annual

basis (Maynard 2017).

In case of CSL Limited, the value of “Property, Plant, and Equipment” such as land and

buildings, the capital work in progress are recorded at historical cost less the applicable

amortization and depreciation. The depreciation is charged on the useful life of the assets based

on straight-line method. Buildings are depreciated 5-40 years as per “straight-line method”, plant

and equipment are depreciated 3-15 years “straight-line method” and lease improvements are

depreciated 5-10 as per “straight-line method”. The impairment testing of PPE is done when the

impairment trigger is identified (McGuire, Wang and Wilson 2014). Intangible assets are

considered with goodwill, intellectual property and software. The excess of fair value of the

purchase consideration for goodwill is identified with net assets minus incidental expenses which

are recorded as goodwill. It needs to be further understood that goodwill is allocated to the

individual as generating units which represents the lowest value within the group in which

goodwill is monitored. The company believes in amortizing and reviewing for impairment for

those assets which have finite lives. The intangible assets having indefinite useful life are not

subject to amortization and henceforth not tested for impairment. The carrying amount of the

goodwill allocated to the business is seen as $ 688.3 in 2017. It has been further discerned that

goodwill is not amortized but measured at cost less any accumulated impairment losses. The

composition of the intangible asset is discerned with $ 1055.4 million in 2017 and 942.6 million

in 2016 out of total assets of $ 9122.7 in 2017 million and 7562.7 million in 2016. This is

forming a composition percentage of 11.5% intangibles in 2017 and 12.4% in 2016 respectively.

Cochlear Limited CSL Limited

Particulars 2017 2016 2017 2016

Intangible Assets 339976 224338 1055.4 942.6

Total Assets 9,23,196 8,16,734 9122.7 7562.7

Composition of Intangible

Assets 37% 27% 12% 12%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

2016 2015 2016 2015

0%

5%

10%

15%

20%

25%

30%

35%

40% 37%

27%

12% 12%

Composition of Intangible Assets

Cochlear Limited

CSL Limited

Figure: Comparison of Composition of Intangible Assets in Cochlear Limited and CSL

Limited

(Source: Cochlear.com. 2018)

Leases

The various types of payments made under the operating leases are expensed as per

straight-line method over the lease term for Cochlear Limited. This however follows the

exception where alternative basis is more representable with the pattern of benefits which are

derived from leased property. The minimum lease payments consist of fixed-rate interests. The

company has been further depicted with number of operating leases over its offices which

requires the premises to be returned to the lessor as per of their initial condition. It needs to be

further discerned that the operating lease payments does not include repairs and overhauls.

Cochlear is identified to lease property under “noncancelable operating leases” expiring over 15

years. The leases are generally provided with the right of renewal at which the terms are

renegotiated. The future noncancelable leases for not later than one year is seen as $ 22142 in

2017 and $ 22372 in 2016. In addition to this, future noncancelable leases later than one year but

not later than five years is depicted to be $ 70016 in 2017 and $ 82528 in 2016. The lease is later

2016 2015 2016 2015

0%

5%

10%

15%

20%

25%

30%

35%

40% 37%

27%

12% 12%

Composition of Intangible Assets

Cochlear Limited

CSL Limited

Figure: Comparison of Composition of Intangible Assets in Cochlear Limited and CSL

Limited

(Source: Cochlear.com. 2018)

Leases

The various types of payments made under the operating leases are expensed as per

straight-line method over the lease term for Cochlear Limited. This however follows the

exception where alternative basis is more representable with the pattern of benefits which are

derived from leased property. The minimum lease payments consist of fixed-rate interests. The

company has been further depicted with number of operating leases over its offices which

requires the premises to be returned to the lessor as per of their initial condition. It needs to be

further discerned that the operating lease payments does not include repairs and overhauls.

Cochlear is identified to lease property under “noncancelable operating leases” expiring over 15

years. The leases are generally provided with the right of renewal at which the terms are

renegotiated. The future noncancelable leases for not later than one year is seen as $ 22142 in

2017 and $ 22372 in 2016. In addition to this, future noncancelable leases later than one year but

not later than five years is depicted to be $ 70016 in 2017 and $ 82528 in 2016. The lease is later

8CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

than five years is determined as $ 58897 in 2017 and 65312 in 2016. The total operating lease

commitments for Cochlear is seen to be $ 151055 in 2017 and 170212 in 2016. Some of the new

standards which are yet to be adopted for leases includes the adoption AASB 16 leases which is

mandated for the company to follow in 2020 (Warren and Jones2018).

Figure: Disclosure on Lease Assets

(Source: Cochlear.com. 2018)

The total lease improvement cost is depicted as $ 275.9 million in 2017 and 223.3 million

in 2016 for CSL Limited. The total lease “property, plant and equipment” is determined to be $

35.4 million in 2017 and 32.8 million in 2016. The lease of the “property, plant and equipment”

in which the group is determined with substantial risk and reward of ownership are segregated as

financial leases. Finance lease is capitalized at the leases inception at “fair value of the minimum

lease payments”. Each of the lease payment is depicted to be allocated between liability and

finance cost. The finance cost is further seen to be charged to the statement of comprehensive

income over the lease period in order to produce a constant periodic rate of interest on the

remaining balance of the needs for each period. The various types of “property, plant and

equipment” acquired as per the finance lease is depreciated over the shorter assets useful life and

leased term. Used to be further understood that the cost of improvement for the leasehold

properties are amortized over the unexpired cost ranging for the lease or estimated useful life of

improvement whichever is depicted to be shorter in nature. The financial instruments comprise

of the “cash and cash equivalents, receivables, payables, lease liabilities and other derivative

instrument”. The operating lease are determined to have a varying for renewal rights. The

different types of rental payments under the leases are predominantly fixed however they are

generally consist of inflation escalation clauses. It needs to be understood that no operating or

than five years is determined as $ 58897 in 2017 and 65312 in 2016. The total operating lease

commitments for Cochlear is seen to be $ 151055 in 2017 and 170212 in 2016. Some of the new

standards which are yet to be adopted for leases includes the adoption AASB 16 leases which is

mandated for the company to follow in 2020 (Warren and Jones2018).

Figure: Disclosure on Lease Assets

(Source: Cochlear.com. 2018)

The total lease improvement cost is depicted as $ 275.9 million in 2017 and 223.3 million

in 2016 for CSL Limited. The total lease “property, plant and equipment” is determined to be $

35.4 million in 2017 and 32.8 million in 2016. The lease of the “property, plant and equipment”

in which the group is determined with substantial risk and reward of ownership are segregated as

financial leases. Finance lease is capitalized at the leases inception at “fair value of the minimum

lease payments”. Each of the lease payment is depicted to be allocated between liability and

finance cost. The finance cost is further seen to be charged to the statement of comprehensive

income over the lease period in order to produce a constant periodic rate of interest on the

remaining balance of the needs for each period. The various types of “property, plant and

equipment” acquired as per the finance lease is depreciated over the shorter assets useful life and

leased term. Used to be further understood that the cost of improvement for the leasehold

properties are amortized over the unexpired cost ranging for the lease or estimated useful life of

improvement whichever is depicted to be shorter in nature. The financial instruments comprise

of the “cash and cash equivalents, receivables, payables, lease liabilities and other derivative

instrument”. The operating lease are determined to have a varying for renewal rights. The

different types of rental payments under the leases are predominantly fixed however they are

generally consist of inflation escalation clauses. It needs to be understood that no operating or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

financier lease consists of restrictions over leasing activities for the company. Similar to

Cochlear Limited, some of the new standards which are yet to be adopted for leases includes the

adoption AASB 16 leases which is mandated for the company to follow in 2020 (Henderson et

al. 2015).

Figure: Lease treatment for CSL

(Source: Csl.com. 2018)

Voluntary Disclosures

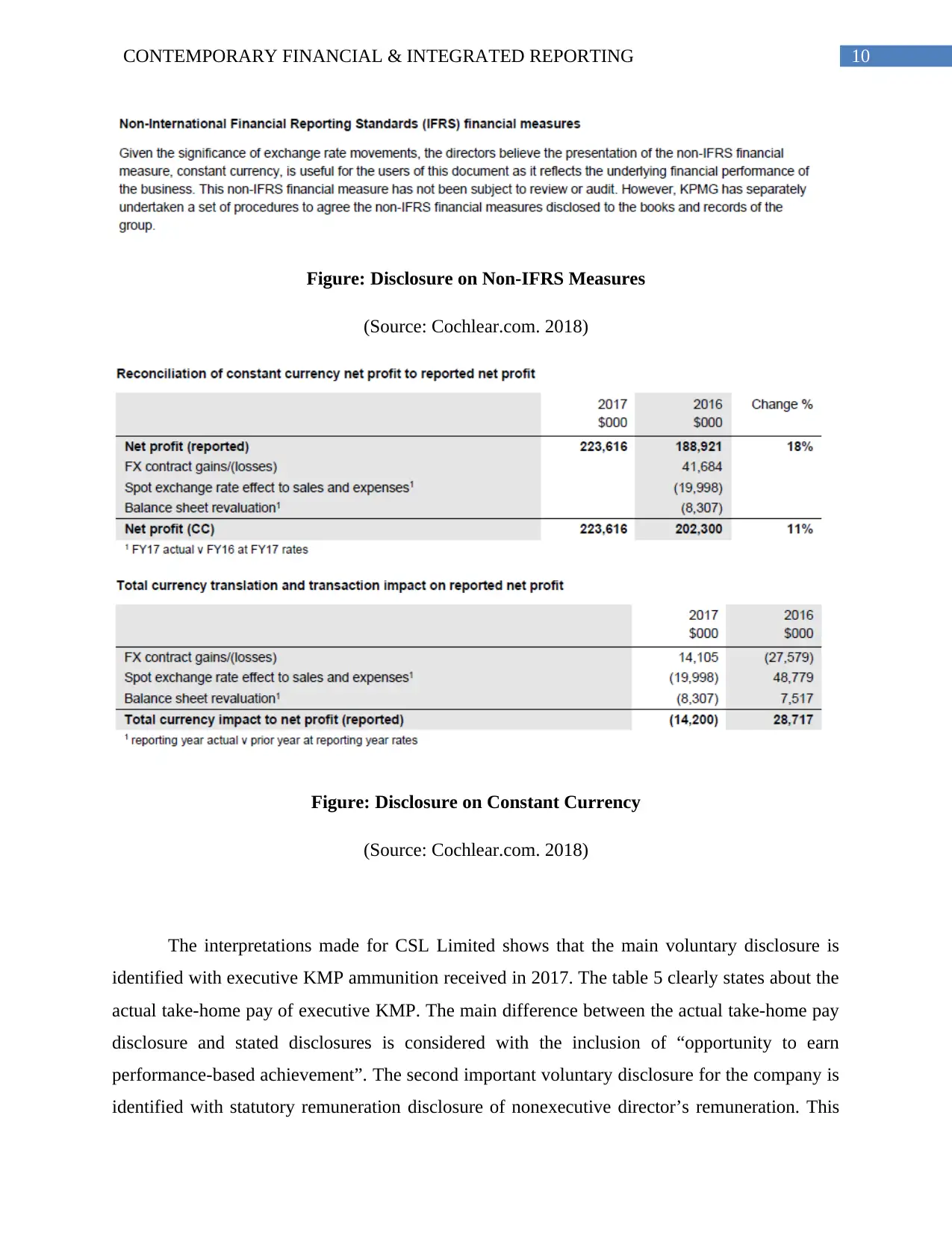

Based on the significance of the exchange rate movements, the directors of Cochlear

Limited decided to present the non-IFRS financial measure which is applied to the underlying

financial performance of the business. The non-IFRS financial disclosure is completely voluntary

nature and are not subject to review our audit. The first disclosure is identified with constant

currency. The constant currency eliminates the impact of any sort of exchange rate movements

which is required to facilitate comparability of the operational excellence for Cochlear. This is

applied with converting the prior comparable period net profit of entities with the use of currency

other than Australian dollar (Bartlett and Beamish 2018). The company is further depicted to

make voluntary disclosure in area of key management personal. This is in particular has been

maintained with disclosing the short-term employee benefits, postemployment benefits, other

long-term benefits, director retirement benefits and share-based payments. The information

associated to the individual KMP remuneration is considered to be plummeted by section 300A

of the “Corporation’s Act 2001”. It needs to be also understood that KMP has not received any

loans from Cochlear and there has been no related party transaction with the company (McGuire,

Wang and Wilson 2014).

financier lease consists of restrictions over leasing activities for the company. Similar to

Cochlear Limited, some of the new standards which are yet to be adopted for leases includes the

adoption AASB 16 leases which is mandated for the company to follow in 2020 (Henderson et

al. 2015).

Figure: Lease treatment for CSL

(Source: Csl.com. 2018)

Voluntary Disclosures

Based on the significance of the exchange rate movements, the directors of Cochlear

Limited decided to present the non-IFRS financial measure which is applied to the underlying

financial performance of the business. The non-IFRS financial disclosure is completely voluntary

nature and are not subject to review our audit. The first disclosure is identified with constant

currency. The constant currency eliminates the impact of any sort of exchange rate movements

which is required to facilitate comparability of the operational excellence for Cochlear. This is

applied with converting the prior comparable period net profit of entities with the use of currency

other than Australian dollar (Bartlett and Beamish 2018). The company is further depicted to

make voluntary disclosure in area of key management personal. This is in particular has been

maintained with disclosing the short-term employee benefits, postemployment benefits, other

long-term benefits, director retirement benefits and share-based payments. The information

associated to the individual KMP remuneration is considered to be plummeted by section 300A

of the “Corporation’s Act 2001”. It needs to be also understood that KMP has not received any

loans from Cochlear and there has been no related party transaction with the company (McGuire,

Wang and Wilson 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

Figure: Disclosure on Non-IFRS Measures

(Source: Cochlear.com. 2018)

Figure: Disclosure on Constant Currency

(Source: Cochlear.com. 2018)

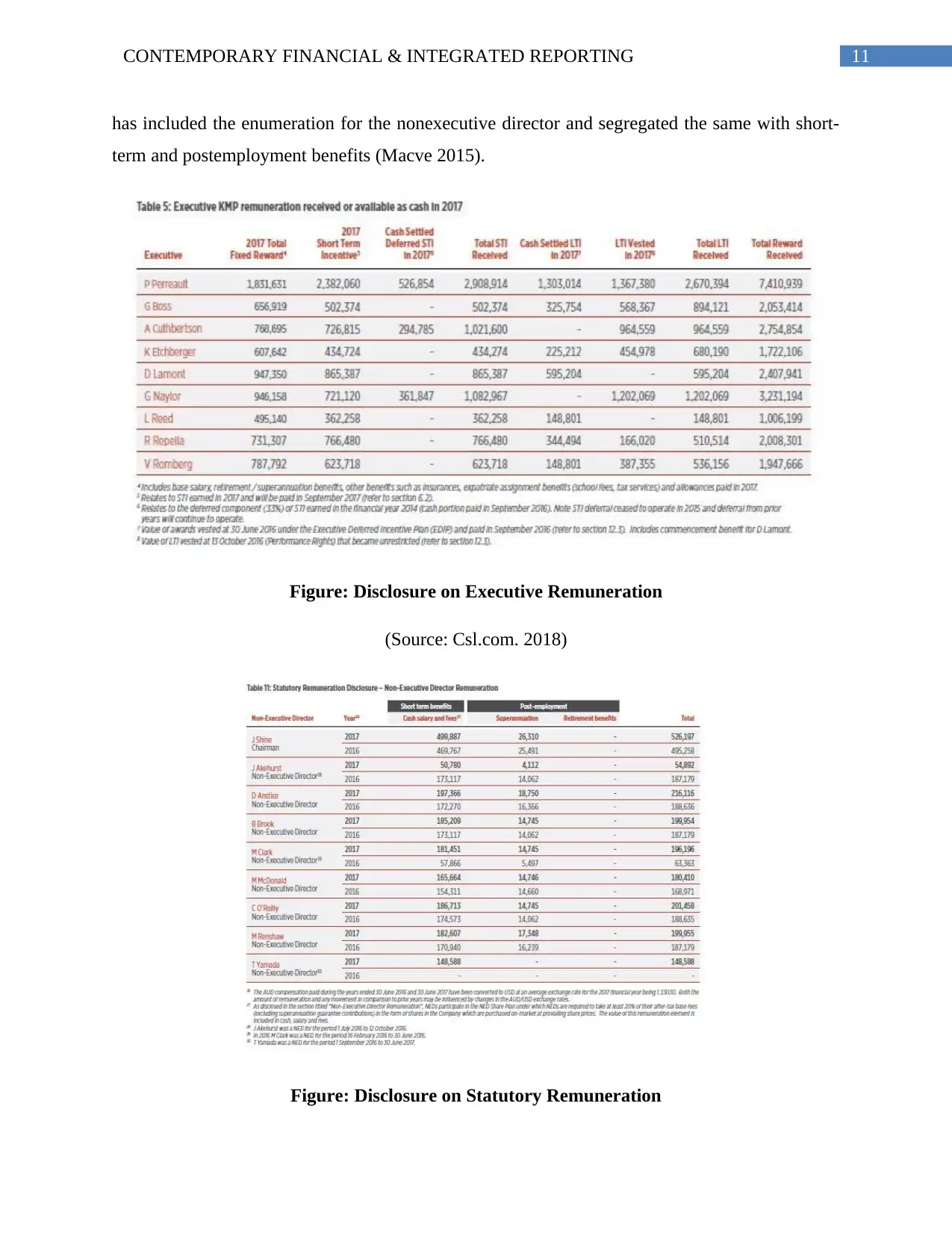

The interpretations made for CSL Limited shows that the main voluntary disclosure is

identified with executive KMP ammunition received in 2017. The table 5 clearly states about the

actual take-home pay of executive KMP. The main difference between the actual take-home pay

disclosure and stated disclosures is considered with the inclusion of “opportunity to earn

performance-based achievement”. The second important voluntary disclosure for the company is

identified with statutory remuneration disclosure of nonexecutive director’s remuneration. This

Figure: Disclosure on Non-IFRS Measures

(Source: Cochlear.com. 2018)

Figure: Disclosure on Constant Currency

(Source: Cochlear.com. 2018)

The interpretations made for CSL Limited shows that the main voluntary disclosure is

identified with executive KMP ammunition received in 2017. The table 5 clearly states about the

actual take-home pay of executive KMP. The main difference between the actual take-home pay

disclosure and stated disclosures is considered with the inclusion of “opportunity to earn

performance-based achievement”. The second important voluntary disclosure for the company is

identified with statutory remuneration disclosure of nonexecutive director’s remuneration. This

11CONTEMPORARY FINANCIAL & INTEGRATED REPORTING

has included the enumeration for the nonexecutive director and segregated the same with short-

term and postemployment benefits (Macve 2015).

Figure: Disclosure on Executive Remuneration

(Source: Csl.com. 2018)

Figure: Disclosure on Statutory Remuneration

has included the enumeration for the nonexecutive director and segregated the same with short-

term and postemployment benefits (Macve 2015).

Figure: Disclosure on Executive Remuneration

(Source: Csl.com. 2018)

Figure: Disclosure on Statutory Remuneration

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.