FINC20019: Contemporary Issues in Australian Payday Lending Market

VerifiedAdded on 2023/06/13

|15

|3130

|190

Report

AI Summary

This report provides an analysis of the payday loan market in Australia, examining the opportunities and risks inherent for investors. It begins with an overview of cash advance lending, highlighting its role in meeting financial emergencies. The report then delves into the growth of the payday loan market in Australia, comparing it to trends in countries like Canada, the UK, and the USA. It explores the mechanics of payday loans, including the fees and lending processes involved. A significant portion of the report is dedicated to analyzing the payday loan market in the USA as a benchmark, discussing its adoption by small businesses and entrepreneurs. The report also considers the regulatory environment, including the federal truth in lending act, and reflects on the impact of market volatility on investment decisions. Finally, it discusses the importance of investors carefully evaluating the return on capital employed versus the cost of raising funds, while also mentioning that Desklib provides students access to similar solved assignments and past papers.

RUNNING Head: Financial: money and capital market analysis

0

Financial: money and capital market analysis

Research Report

0

Financial: money and capital market analysis

Research Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial: money and capital market analysis 1

Table of Contents

Introduction...........................................................................................................................................1

Objective of the report.......................................................................................................................1

Overview of the Cash Advance Lending...........................................................................................1

Risk and opportunity in the Payday loan market...................................................................................2

Analysis of Payday loan market in USA...............................................................................................2

Reflection on the pay day loan..............................................................................................................6

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Appendix...............................................................................................................................................9

Table of Contents

Introduction...........................................................................................................................................1

Objective of the report.......................................................................................................................1

Overview of the Cash Advance Lending...........................................................................................1

Risk and opportunity in the Payday loan market...................................................................................2

Analysis of Payday loan market in USA...............................................................................................2

Reflection on the pay day loan..............................................................................................................6

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Appendix...............................................................................................................................................9

Financial: money and capital market analysis 2

Introduction

There are several factors which influence the investment decision of the investors.

The economics of Australia has been changing with the drastic rate and capital market is

highly volatile. In this research report, opportunity and risks inherent in the financial market

for the investors have been analysed. After that, contemporary issues impacting on the

investment decisions and the sustainability of the financial market have been analysed.

Objective of the report

The main objective of the report is to analyse the Payday / Cash Advance Lending

Industry in Australia.

Purpose of the report

The main purpose of this research report is to analysis the opportunity and risk

inherent in the financial market of the Australia in context with the Payday / Cash Advance

Lending Industry in Australia (Higgins, 2012).

Overview of the Cash Advance Lending

It is observed that cash advance lending is the process which assists in meeting the

financial emergencies if a person cannot wait until the payday to get the money they need.

However, in the ramified economic and highly volatile financial market, it would be easy to

go for Cash Advance Lending from the licensed or authorised body. Payday loans in

Australia have been described as part of the small loan market which valued around $ 400

million a year within 12 months (Crawford and Jin, 2014).

Introduction

There are several factors which influence the investment decision of the investors.

The economics of Australia has been changing with the drastic rate and capital market is

highly volatile. In this research report, opportunity and risks inherent in the financial market

for the investors have been analysed. After that, contemporary issues impacting on the

investment decisions and the sustainability of the financial market have been analysed.

Objective of the report

The main objective of the report is to analyse the Payday / Cash Advance Lending

Industry in Australia.

Purpose of the report

The main purpose of this research report is to analysis the opportunity and risk

inherent in the financial market of the Australia in context with the Payday / Cash Advance

Lending Industry in Australia (Higgins, 2012).

Overview of the Cash Advance Lending

It is observed that cash advance lending is the process which assists in meeting the

financial emergencies if a person cannot wait until the payday to get the money they need.

However, in the ramified economic and highly volatile financial market, it would be easy to

go for Cash Advance Lending from the licensed or authorised body. Payday loans in

Australia have been described as part of the small loan market which valued around $ 400

million a year within 12 months (Crawford and Jin, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial: money and capital market analysis 3

With the changes in economic factors, investors are more inclined towards investing

their money in many business sectors and attractive market opportunities to save their capital

value due to the market inflation rate. However, there are several ways which are used by

investors and people to arrange capital from the market such as pay day loan, capital

borrowing, applying for loan and lending from the banks and financial institutions by creating

charge on their assets. Payday loan market in Australia has been gaining momentum

throughout the time due to its easy availability of the loan and borrowings (Irvin, 2016). The

growth of the payday loan could be seen by evaluating the growth in the Canada, UK and

USA. In these countries, Payday loan market has shown average 22% average growth since

last three years. In Australia, there is increase of the short term and long term loan by

approximately by average 18% since last three years which shows that people are more

inclined towards raising funds from the financial market (Flannery, 2016).

Risk and opportunity in the Payday loan market

There is the proper work process which is followed while raising capital from the

Payday loan market. In order to raise the capital from the Payday loan market, applicant or

borrower needs to write a personal check payable to lender for the amount of capital which

wants to borrow accompanied by the fees of the borrowing. After that lending company gives

the amount of capital which he wrote in the favour of company (lender) deducting the fees

amount into the borrowers account. This is the lending process which is mostly used by the

borrowers to raise the funds. In Australia, there are several companies and body corporate

which have undertaken this business plan to earn profit and lend capital to borrowers.

However, the cash pay day lenders are approaching the borrowers by keeping the fees as low

as bank rate. Although, new standards set for capping the overall cost of payday loans, high-

cost credit remains a serious issue (Fontoynont, et al. 2016).

Analysis of Payday loan market in USA

The loan amount is due to be deducted or debited the next payday. The fees

determined on the loan amount are determined on the basis of the percentage of the face

value of the check. The success of Payday loan market in USA is the perfect benchmark

which reflects the positive increment of high growth of this loan raising methods for the

borrowers. In USA, small business organizations and investors uses Payday / Cash Advance

With the changes in economic factors, investors are more inclined towards investing

their money in many business sectors and attractive market opportunities to save their capital

value due to the market inflation rate. However, there are several ways which are used by

investors and people to arrange capital from the market such as pay day loan, capital

borrowing, applying for loan and lending from the banks and financial institutions by creating

charge on their assets. Payday loan market in Australia has been gaining momentum

throughout the time due to its easy availability of the loan and borrowings (Irvin, 2016). The

growth of the payday loan could be seen by evaluating the growth in the Canada, UK and

USA. In these countries, Payday loan market has shown average 22% average growth since

last three years. In Australia, there is increase of the short term and long term loan by

approximately by average 18% since last three years which shows that people are more

inclined towards raising funds from the financial market (Flannery, 2016).

Risk and opportunity in the Payday loan market

There is the proper work process which is followed while raising capital from the

Payday loan market. In order to raise the capital from the Payday loan market, applicant or

borrower needs to write a personal check payable to lender for the amount of capital which

wants to borrow accompanied by the fees of the borrowing. After that lending company gives

the amount of capital which he wrote in the favour of company (lender) deducting the fees

amount into the borrowers account. This is the lending process which is mostly used by the

borrowers to raise the funds. In Australia, there are several companies and body corporate

which have undertaken this business plan to earn profit and lend capital to borrowers.

However, the cash pay day lenders are approaching the borrowers by keeping the fees as low

as bank rate. Although, new standards set for capping the overall cost of payday loans, high-

cost credit remains a serious issue (Fontoynont, et al. 2016).

Analysis of Payday loan market in USA

The loan amount is due to be deducted or debited the next payday. The fees

determined on the loan amount are determined on the basis of the percentage of the face

value of the check. The success of Payday loan market in USA is the perfect benchmark

which reflects the positive increment of high growth of this loan raising methods for the

borrowers. In USA, small business organizations and investors uses Payday / Cash Advance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial: money and capital market analysis 4

lenders to raise capital instantly to grab the opportunity available in the market (Gorshkov,

Murgul, and Oliynyk, 2016).

Source: https://www.statcan.gc.ca/pub/75-001-x/10407/9617-eng.htm

With the increased use of Payday / Cash Advance lenders in USA, many entrepreneur

and companies have also adopted this Payday / Cash Advance lenders as their business

working chain to earn profit. However, Payday loan market is easy to tap but due to its high

fees charges, it is least liked by the other borrowers to raise funds in market if they have other

available capital lending options (Kidwell, et al. 2016).

As per the financial rules and regulations, the federal truth in the lending act treats

payday loans like other types of credit in the financial market. It is analysed that there are

several risk and opportunities for the investors in the financial market due to its high

volatility. The main risk for the investors is related to the equity capital investment (Magni,

2016). It is the type of investment in which investor’s buys stocks and share of the particular

company for the return on equity share. There is certain requirement of the pay day loan

which needs be filled by the borrowers before raising funds from this method such as

principle loan cannot exceed AUD $ 1500, minimum fees charges is around 15% and payday

lenders do not perform credit checks who do not report to credit information services

(Bourke, 2018). They need to have employment record and bank account on which they write

lenders to raise capital instantly to grab the opportunity available in the market (Gorshkov,

Murgul, and Oliynyk, 2016).

Source: https://www.statcan.gc.ca/pub/75-001-x/10407/9617-eng.htm

With the increased use of Payday / Cash Advance lenders in USA, many entrepreneur

and companies have also adopted this Payday / Cash Advance lenders as their business

working chain to earn profit. However, Payday loan market is easy to tap but due to its high

fees charges, it is least liked by the other borrowers to raise funds in market if they have other

available capital lending options (Kidwell, et al. 2016).

As per the financial rules and regulations, the federal truth in the lending act treats

payday loans like other types of credit in the financial market. It is analysed that there are

several risk and opportunities for the investors in the financial market due to its high

volatility. The main risk for the investors is related to the equity capital investment (Magni,

2016). It is the type of investment in which investor’s buys stocks and share of the particular

company for the return on equity share. There is certain requirement of the pay day loan

which needs be filled by the borrowers before raising funds from this method such as

principle loan cannot exceed AUD $ 1500, minimum fees charges is around 15% and payday

lenders do not perform credit checks who do not report to credit information services

(Bourke, 2018). They need to have employment record and bank account on which they write

Financial: money and capital market analysis 5

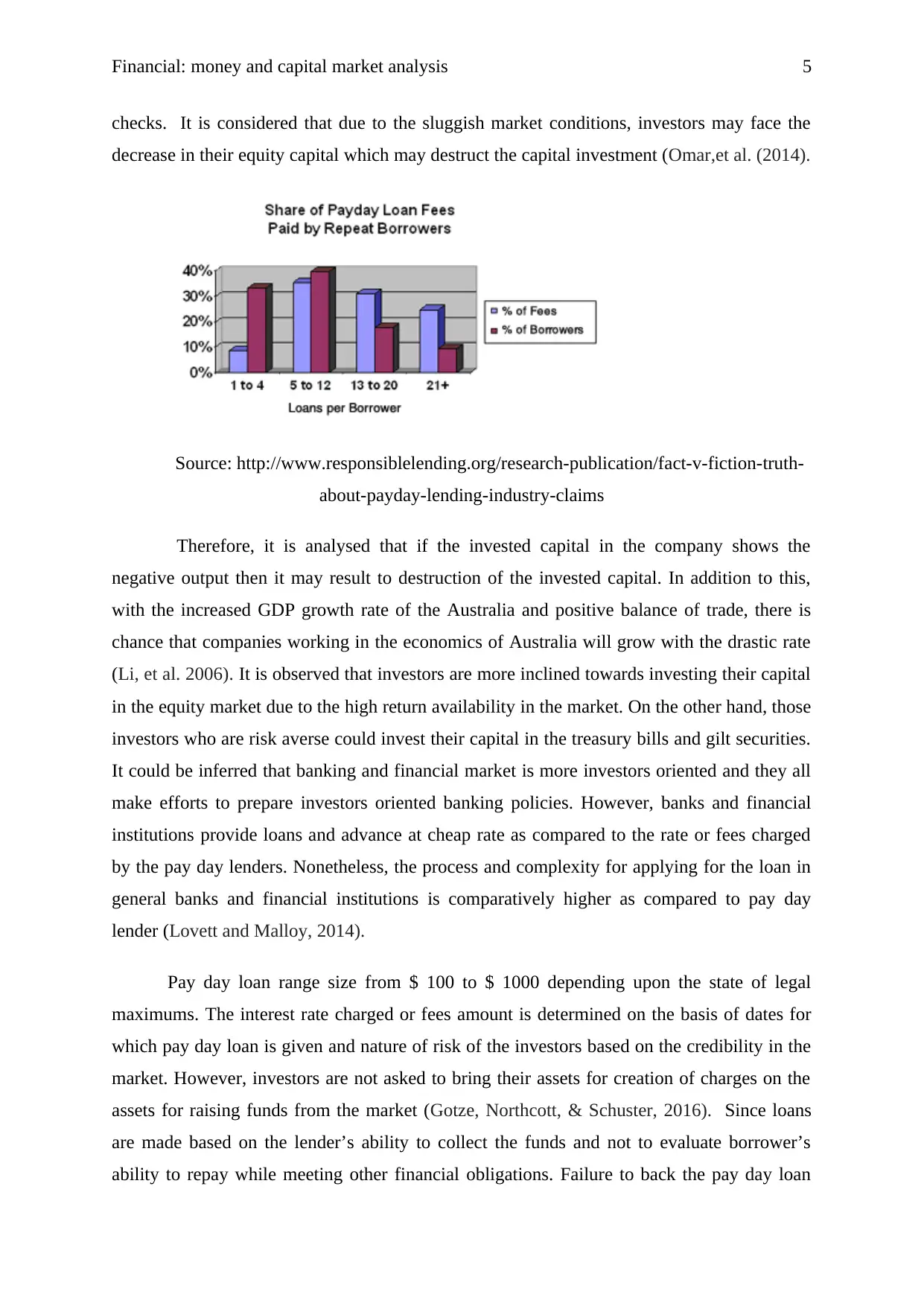

checks. It is considered that due to the sluggish market conditions, investors may face the

decrease in their equity capital which may destruct the capital investment (Omar,et al. (2014).

Source: http://www.responsiblelending.org/research-publication/fact-v-fiction-truth-

about-payday-lending-industry-claims

Therefore, it is analysed that if the invested capital in the company shows the

negative output then it may result to destruction of the invested capital. In addition to this,

with the increased GDP growth rate of the Australia and positive balance of trade, there is

chance that companies working in the economics of Australia will grow with the drastic rate

(Li, et al. 2006). It is observed that investors are more inclined towards investing their capital

in the equity market due to the high return availability in the market. On the other hand, those

investors who are risk averse could invest their capital in the treasury bills and gilt securities.

It could be inferred that banking and financial market is more investors oriented and they all

make efforts to prepare investors oriented banking policies. However, banks and financial

institutions provide loans and advance at cheap rate as compared to the rate or fees charged

by the pay day lenders. Nonetheless, the process and complexity for applying for the loan in

general banks and financial institutions is comparatively higher as compared to pay day

lender (Lovett and Malloy, 2014).

Pay day loan range size from $ 100 to $ 1000 depending upon the state of legal

maximums. The interest rate charged or fees amount is determined on the basis of dates for

which pay day loan is given and nature of risk of the investors based on the credibility in the

market. However, investors are not asked to bring their assets for creation of charges on the

assets for raising funds from the market (Gotze, Northcott, & Schuster, 2016). Since loans

are made based on the lender’s ability to collect the funds and not to evaluate borrower’s

ability to repay while meeting other financial obligations. Failure to back the pay day loan

checks. It is considered that due to the sluggish market conditions, investors may face the

decrease in their equity capital which may destruct the capital investment (Omar,et al. (2014).

Source: http://www.responsiblelending.org/research-publication/fact-v-fiction-truth-

about-payday-lending-industry-claims

Therefore, it is analysed that if the invested capital in the company shows the

negative output then it may result to destruction of the invested capital. In addition to this,

with the increased GDP growth rate of the Australia and positive balance of trade, there is

chance that companies working in the economics of Australia will grow with the drastic rate

(Li, et al. 2006). It is observed that investors are more inclined towards investing their capital

in the equity market due to the high return availability in the market. On the other hand, those

investors who are risk averse could invest their capital in the treasury bills and gilt securities.

It could be inferred that banking and financial market is more investors oriented and they all

make efforts to prepare investors oriented banking policies. However, banks and financial

institutions provide loans and advance at cheap rate as compared to the rate or fees charged

by the pay day lenders. Nonetheless, the process and complexity for applying for the loan in

general banks and financial institutions is comparatively higher as compared to pay day

lender (Lovett and Malloy, 2014).

Pay day loan range size from $ 100 to $ 1000 depending upon the state of legal

maximums. The interest rate charged or fees amount is determined on the basis of dates for

which pay day loan is given and nature of risk of the investors based on the credibility in the

market. However, investors are not asked to bring their assets for creation of charges on the

assets for raising funds from the market (Gotze, Northcott, & Schuster, 2016). Since loans

are made based on the lender’s ability to collect the funds and not to evaluate borrower’s

ability to repay while meeting other financial obligations. Failure to back the pay day loan

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial: money and capital market analysis 6

may result to legal penalties and jail as per the banking rules and regulation (Allen, et al.

2017).

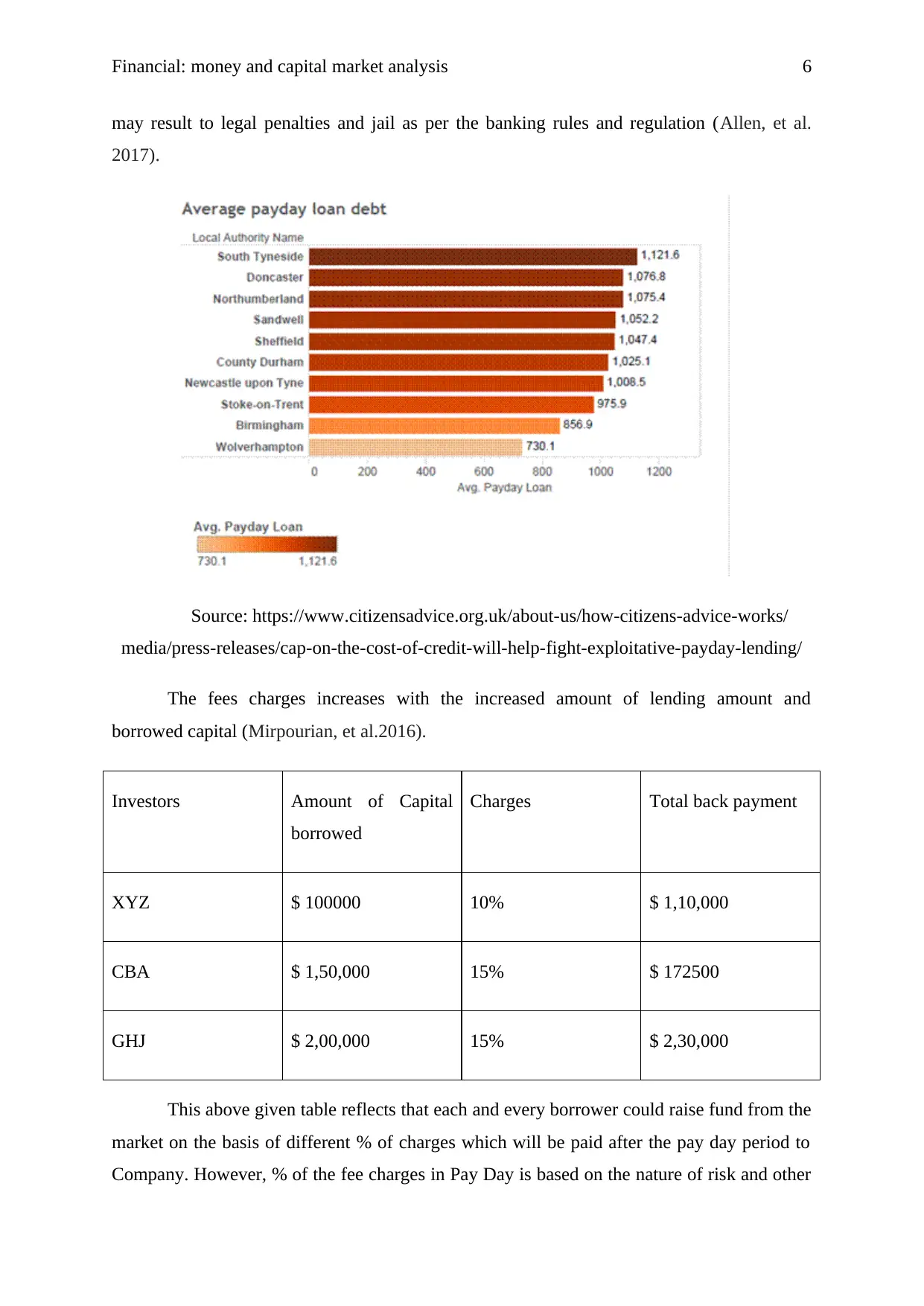

Source: https://www.citizensadvice.org.uk/about-us/how-citizens-advice-works/

media/press-releases/cap-on-the-cost-of-credit-will-help-fight-exploitative-payday-lending/

The fees charges increases with the increased amount of lending amount and

borrowed capital (Mirpourian, et al.2016).

Investors Amount of Capital

borrowed

Charges Total back payment

XYZ $ 100000 10% $ 1,10,000

CBA $ 1,50,000 15% $ 172500

GHJ $ 2,00,000 15% $ 2,30,000

This above given table reflects that each and every borrower could raise fund from the

market on the basis of different % of charges which will be paid after the pay day period to

Company. However, % of the fee charges in Pay Day is based on the nature of risk and other

may result to legal penalties and jail as per the banking rules and regulation (Allen, et al.

2017).

Source: https://www.citizensadvice.org.uk/about-us/how-citizens-advice-works/

media/press-releases/cap-on-the-cost-of-credit-will-help-fight-exploitative-payday-lending/

The fees charges increases with the increased amount of lending amount and

borrowed capital (Mirpourian, et al.2016).

Investors Amount of Capital

borrowed

Charges Total back payment

XYZ $ 100000 10% $ 1,10,000

CBA $ 1,50,000 15% $ 172500

GHJ $ 2,00,000 15% $ 2,30,000

This above given table reflects that each and every borrower could raise fund from the

market on the basis of different % of charges which will be paid after the pay day period to

Company. However, % of the fee charges in Pay Day is based on the nature of risk and other

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial: money and capital market analysis 7

factors which may shows the negative impact on the business functioning of organization

(Rizvi, and Khan, 2015).

After analysing the international financial factors, it could be inferred that the banking

and financial market of the Australia is comparatively stable as compared to other

organization (Beck, Demirgüç-Kunt, and Levine, 2009). The balance of trade of the

economics of Australia has increased by average 12% since last three year which reflects

high amount of inflow in the Australian economy. As per the banking and reserve bank of

Australia, the capital reserve and repo rate has been set low which eventually decrease the

bank interest rate for clients (Allen, et al., 2017). The flow of cash in the particular economy

is based on the open market operation. The development of the financial system and

increased security program works in concert to bring about the changes in the financial

investment structure of the banking and investment models of the Australia. The main issue

impacting the financial investment decisions is based on the investment opportunity in the

financial market, industry growth rate, remittance rules and regulation for the flow of cash

out of economy. For instance, if the interest rate and banking regulations are liberal and offer

high interest rate growth to investors then it will result to high flow of cash in the economy

(Mathuva, 2015). The open market operation is used by the Reserve Bank of Australia to

implement proper strategic program to maintain the flow of cash in the particular economy. It

is analysed that if the return offers on the treasury bills and securities are high then it will also

increase the lending of the borrowers from banks and financial institutions.

This could be understood with the simple illustration that if XAB investors is having AUD $

1, 00,000 capital to investment and he wants to buy mutual funds of AUD $ 3, 00,000 then it

could do so raising funds from the banks and financial institutions (Bourke, 2009). However,

investors needs to analysis whether the return on capital employed is more than the cost of

raising funds from the banks and financial institutions. The return on capital employed of the

invested capital is based on the companies chosen and return offered by these companies

(Woodbridge, 2017).

Reflection on the pay day loan

After analysing all the details, risk and market opportunity available in the market, it

could be inferred that Payday / Cash Advance lenders process has been gaining momentum

throughout the time. It is observed that in the fast moving economic, investors needs to

factors which may shows the negative impact on the business functioning of organization

(Rizvi, and Khan, 2015).

After analysing the international financial factors, it could be inferred that the banking

and financial market of the Australia is comparatively stable as compared to other

organization (Beck, Demirgüç-Kunt, and Levine, 2009). The balance of trade of the

economics of Australia has increased by average 12% since last three year which reflects

high amount of inflow in the Australian economy. As per the banking and reserve bank of

Australia, the capital reserve and repo rate has been set low which eventually decrease the

bank interest rate for clients (Allen, et al., 2017). The flow of cash in the particular economy

is based on the open market operation. The development of the financial system and

increased security program works in concert to bring about the changes in the financial

investment structure of the banking and investment models of the Australia. The main issue

impacting the financial investment decisions is based on the investment opportunity in the

financial market, industry growth rate, remittance rules and regulation for the flow of cash

out of economy. For instance, if the interest rate and banking regulations are liberal and offer

high interest rate growth to investors then it will result to high flow of cash in the economy

(Mathuva, 2015). The open market operation is used by the Reserve Bank of Australia to

implement proper strategic program to maintain the flow of cash in the particular economy. It

is analysed that if the return offers on the treasury bills and securities are high then it will also

increase the lending of the borrowers from banks and financial institutions.

This could be understood with the simple illustration that if XAB investors is having AUD $

1, 00,000 capital to investment and he wants to buy mutual funds of AUD $ 3, 00,000 then it

could do so raising funds from the banks and financial institutions (Bourke, 2009). However,

investors needs to analysis whether the return on capital employed is more than the cost of

raising funds from the banks and financial institutions. The return on capital employed of the

invested capital is based on the companies chosen and return offered by these companies

(Woodbridge, 2017).

Reflection on the pay day loan

After analysing all the details, risk and market opportunity available in the market, it

could be inferred that Payday / Cash Advance lenders process has been gaining momentum

throughout the time. It is observed that in the fast moving economic, investors needs to

Financial: money and capital market analysis 8

speedily grab the opportunity available in the market without any delay if they want to gain

profit on their investment due to sensitivity of the information available in the market.

Therefore, by using Payday / Cash Advance lenders, investors could easily raise capital from

the market which could be further used by investors to create value on their investment.

However, the longer the time period for the borrowed capital by using Payday / Cash

Advance lenders, the more % of fees would be charged. It is further analysed that if I will

find sudden growth in the market due to the high volatility and market premium factors then I

will go for Payday / Cash Advance lenders. It will not only provide easily availability of

funds but also provide speedy availability of cash for the investment.

Conclusion

There are several domestic and international factors which have been impacting the

Australian financial market. However, due to high volatility in the industries and high market

premium, investors may have to face high loss in their invested capital but at the same time, it

also offers high amount of opportunities for creating value on their invested capital. With the

increasing changes in economic conditions, there are several types of banks and financial

institutions have been developed which provides capital and lends money to borrowers. It is

evaluated that Payday / Cash Advance lenders is one of the best option for the borrowers to

instantly raise the funds from the market as per their investment needs and demand.

speedily grab the opportunity available in the market without any delay if they want to gain

profit on their investment due to sensitivity of the information available in the market.

Therefore, by using Payday / Cash Advance lenders, investors could easily raise capital from

the market which could be further used by investors to create value on their investment.

However, the longer the time period for the borrowed capital by using Payday / Cash

Advance lenders, the more % of fees would be charged. It is further analysed that if I will

find sudden growth in the market due to the high volatility and market premium factors then I

will go for Payday / Cash Advance lenders. It will not only provide easily availability of

funds but also provide speedy availability of cash for the investment.

Conclusion

There are several domestic and international factors which have been impacting the

Australian financial market. However, due to high volatility in the industries and high market

premium, investors may have to face high loss in their invested capital but at the same time, it

also offers high amount of opportunities for creating value on their invested capital. With the

increasing changes in economic conditions, there are several types of banks and financial

institutions have been developed which provides capital and lends money to borrowers. It is

evaluated that Payday / Cash Advance lenders is one of the best option for the borrowers to

instantly raise the funds from the market as per their investment needs and demand.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial: money and capital market analysis 9

References

Allen, F., Armour, J., Balling, M., Belchambers, A., Danielsson, J., Gnan, E., Grant, C.,

Haben, P., Jackson, P., Macrae, R. and Micheler, E., 2017. Central banking and monetary

policy: Which will be the post-crisis new normal?. SUERF Studies.

Beck, T., Demirgüç-Kunt, A. and Levine, R., 2009. Financial institutions and markets across

countries and over time-data and analysis.

Bourke, P., 2018. Concentration and other determinants of bank profitability in Europe,

North America and Australia. Journal of Banking & Finance, 13(1), pp.65-79.

Crawford, C. and Jin, W., 2014. Payback time? Student debt and loan repayments: what will

the 2012 reforms mean for graduates? (No. R93). IFS Reports, Institute for Fiscal Studies.

Flannery, M.J., 2016. Stabilizing large financial institutions with contingent capital

certificates. Quarterly Journal of Finance, 6(02), p.1650006.

Fontoynont, M., de Boer, J., Rötlander, J., Skov, K.G., Gudmandsen, N.S. and Koga, Y.,

2016. Global Economic Models: A Technical Report of IEA SHC Task 50: Advanced

Lighting Solutions for Retrofitting Buildings.

Gorshkov, A., Murgul, V. and Oliynyk, O., 2016. Forecasted Payback Period in the Case of

Energy-Efficient Activities. In MATEC Web of Conferences (Vol. 53). EDP Sciences.

Gotze, U., Northcott, D., & Schuster, P. (2016). INVESTMENT APPRAISAL. SPRINGER-

VERLAG BERLIN AN.

Higgins, R. C. (2012). Analysis for financial management. McGraw-Hill/Irwin.

Irvin, G. (2016). Modern cost-benefit methods: an introduction to financial, economic and

social appraisal of development projects. Macmillan Education Ltd..

Kidwell, D.S., Blackwell, D.W., Sias, R.W. and Whidbee, D.A., 2016. Financial institutions,

markets, and money. John Wiley & Sons.

Li, D., Moshirian, F., Pham, P.K. and Zein, J., 2006. When financial institutions are large

shareholders: The role of macro corporate governance environments. The Journal of

Finance, 61(6), pp.2975-3007.

Lovett, W. and Malloy, M., 2014. Banking and Financial Institutions Law in a Nutshell, 8th.

West Academic.

Magni, C. A. (2016). An average-based accounting approach to capital asset investments:

The case of project finance. European Accounting Review, 25(2), 275-286.

Mathuva, D. (2015). The Influence of working capital management components on corporate

profitability.

References

Allen, F., Armour, J., Balling, M., Belchambers, A., Danielsson, J., Gnan, E., Grant, C.,

Haben, P., Jackson, P., Macrae, R. and Micheler, E., 2017. Central banking and monetary

policy: Which will be the post-crisis new normal?. SUERF Studies.

Beck, T., Demirgüç-Kunt, A. and Levine, R., 2009. Financial institutions and markets across

countries and over time-data and analysis.

Bourke, P., 2018. Concentration and other determinants of bank profitability in Europe,

North America and Australia. Journal of Banking & Finance, 13(1), pp.65-79.

Crawford, C. and Jin, W., 2014. Payback time? Student debt and loan repayments: what will

the 2012 reforms mean for graduates? (No. R93). IFS Reports, Institute for Fiscal Studies.

Flannery, M.J., 2016. Stabilizing large financial institutions with contingent capital

certificates. Quarterly Journal of Finance, 6(02), p.1650006.

Fontoynont, M., de Boer, J., Rötlander, J., Skov, K.G., Gudmandsen, N.S. and Koga, Y.,

2016. Global Economic Models: A Technical Report of IEA SHC Task 50: Advanced

Lighting Solutions for Retrofitting Buildings.

Gorshkov, A., Murgul, V. and Oliynyk, O., 2016. Forecasted Payback Period in the Case of

Energy-Efficient Activities. In MATEC Web of Conferences (Vol. 53). EDP Sciences.

Gotze, U., Northcott, D., & Schuster, P. (2016). INVESTMENT APPRAISAL. SPRINGER-

VERLAG BERLIN AN.

Higgins, R. C. (2012). Analysis for financial management. McGraw-Hill/Irwin.

Irvin, G. (2016). Modern cost-benefit methods: an introduction to financial, economic and

social appraisal of development projects. Macmillan Education Ltd..

Kidwell, D.S., Blackwell, D.W., Sias, R.W. and Whidbee, D.A., 2016. Financial institutions,

markets, and money. John Wiley & Sons.

Li, D., Moshirian, F., Pham, P.K. and Zein, J., 2006. When financial institutions are large

shareholders: The role of macro corporate governance environments. The Journal of

Finance, 61(6), pp.2975-3007.

Lovett, W. and Malloy, M., 2014. Banking and Financial Institutions Law in a Nutshell, 8th.

West Academic.

Magni, C. A. (2016). An average-based accounting approach to capital asset investments:

The case of project finance. European Accounting Review, 25(2), 275-286.

Mathuva, D. (2015). The Influence of working capital management components on corporate

profitability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial: money and capital market analysis 10

Mirpourian, S., Caragliu, A., Di Maio, G., Landoni, P. and Rusinà, E., 2016. Determinants of

loan repayment performance among borrowers of microfinance institutions: Evidence from

India. World Development Perspectives, 1, pp.49-52.

Omar, N., Koya, R. K., Sanusi, Z. M., & Shafie, N. A. (2014). Financial statement fraud: A

case examination using Beneish Model and ratio analysis. International Journal of Trade,

Economics and Finance, 5(2), 184.

Rizvi, W. and Khan, M.M.S., 2015. The Impact Of Inflation On Loan Default: A Study On

Pakistan. Australian Journal of Business and Economic Studies, 1 (1).

Woodbridge, L., 2017. Payback Time: On the Economic Rhetoric of Revenge in The

Merchant of Venice. In Shakespeare and the Cultures of Performance (pp. 43-54).

Routledge.

Mirpourian, S., Caragliu, A., Di Maio, G., Landoni, P. and Rusinà, E., 2016. Determinants of

loan repayment performance among borrowers of microfinance institutions: Evidence from

India. World Development Perspectives, 1, pp.49-52.

Omar, N., Koya, R. K., Sanusi, Z. M., & Shafie, N. A. (2014). Financial statement fraud: A

case examination using Beneish Model and ratio analysis. International Journal of Trade,

Economics and Finance, 5(2), 184.

Rizvi, W. and Khan, M.M.S., 2015. The Impact Of Inflation On Loan Default: A Study On

Pakistan. Australian Journal of Business and Economic Studies, 1 (1).

Woodbridge, L., 2017. Payback Time: On the Economic Rhetoric of Revenge in The

Merchant of Venice. In Shakespeare and the Cultures of Performance (pp. 43-54).

Routledge.

Financial: money and capital market analysis 11

Appendix

Appendix

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.