Master Budget Report: Context Ltd's Financial Performance Analysis

VerifiedAdded on 2021/02/20

|8

|1958

|234

Report

AI Summary

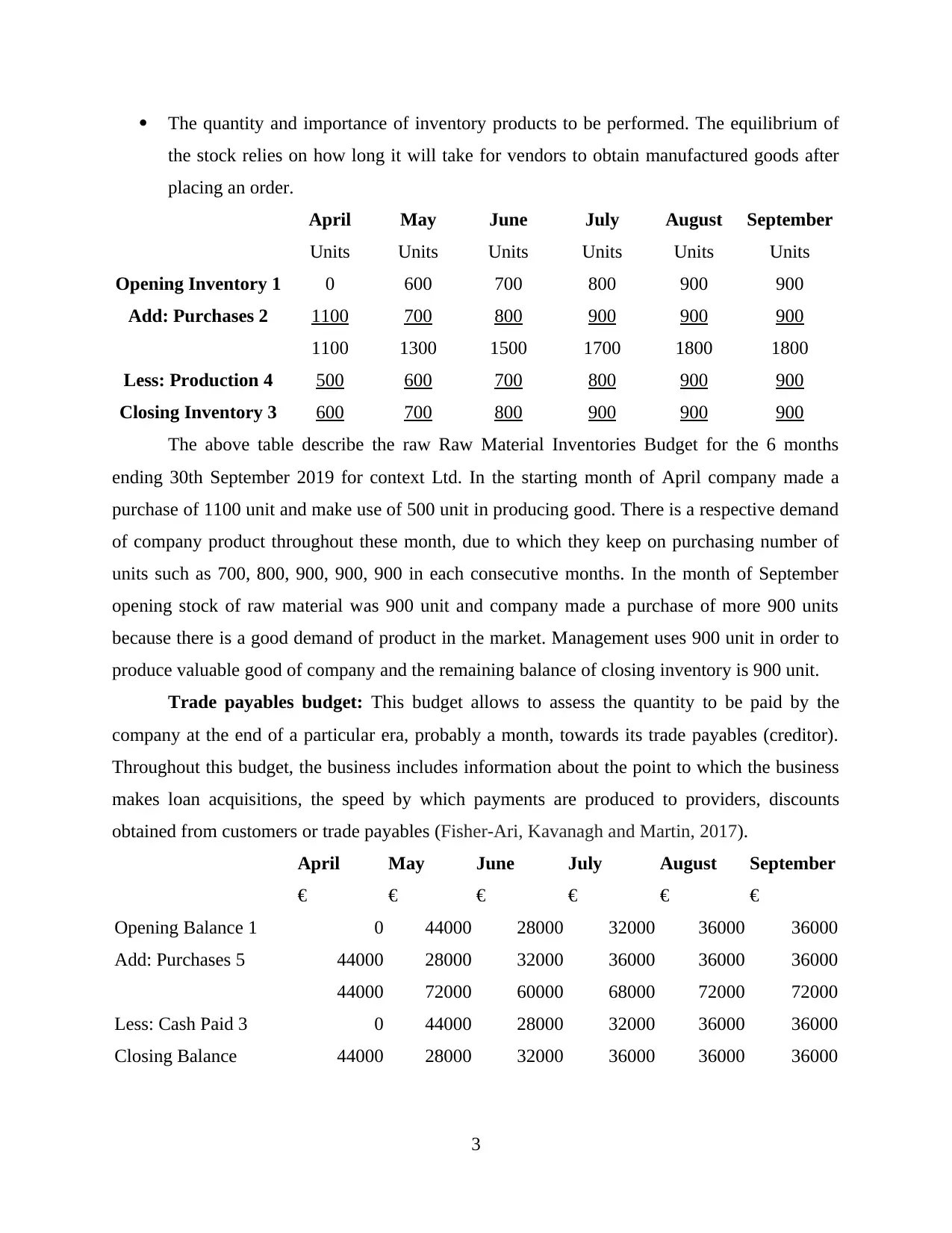

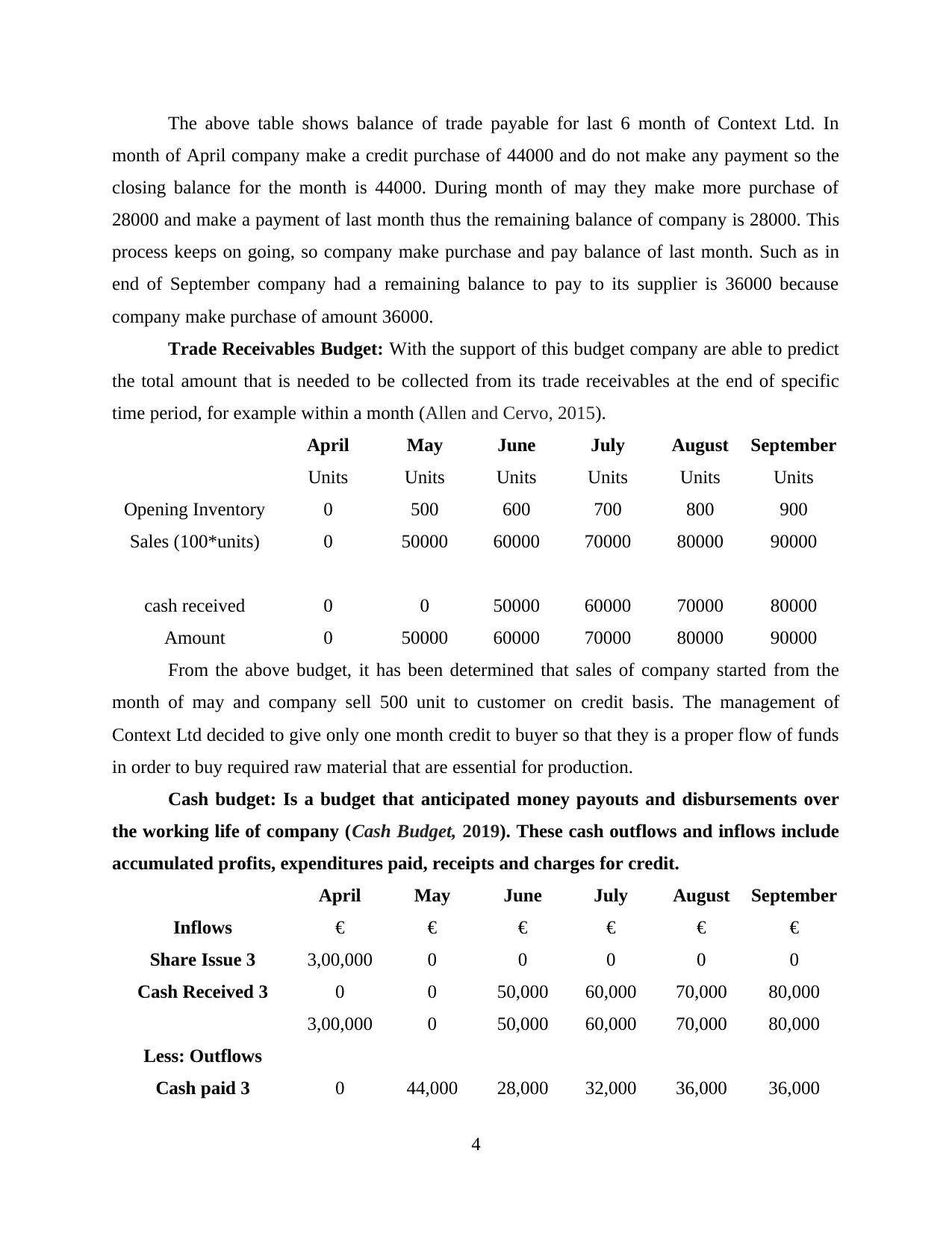

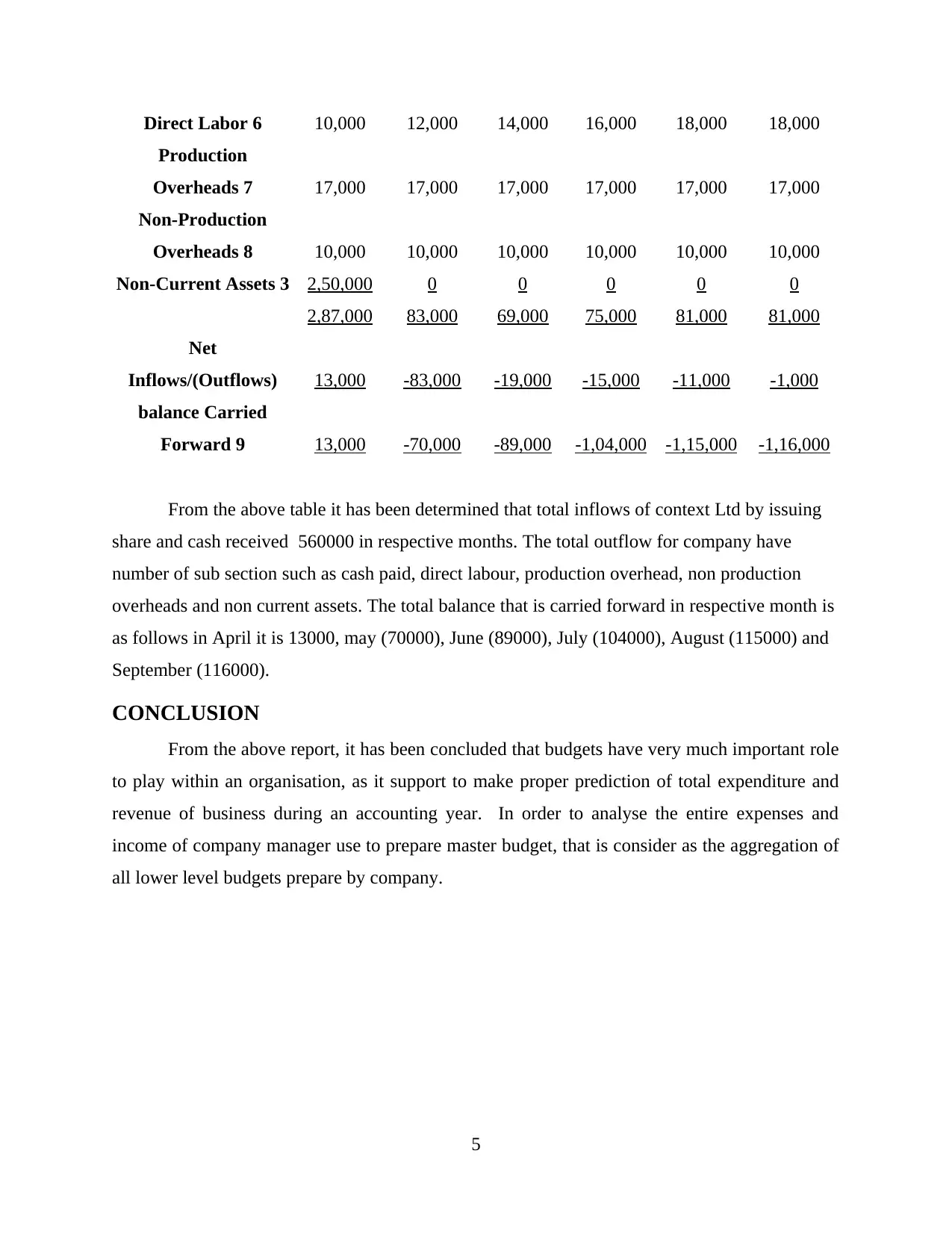

This report provides a comprehensive analysis of a master budget, focusing on Context Ltd, a company planning to start a new business. The report delves into appropriate budgetary targets, the creation of a master budget, and a comparison of actual expenditure and income. It examines various budgets, including finished inventory, raw material inventory, trade payables, trade receivables, and cash budgets. The report details the processes involved in creating these budgets and compares actual financial data against the budgeted figures. Furthermore, the report evaluates budgetary monitoring processes, illustrating how to ensure that financial, functional, and investment plans are executed effectively. The analysis includes detailed tables and calculations to support the findings, offering insights into the company's financial performance and planning.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.