Comprehensive Financial Analysis: Business Plan for Contracting School

VerifiedAdded on 2023/06/12

|13

|1986

|322

Report

AI Summary

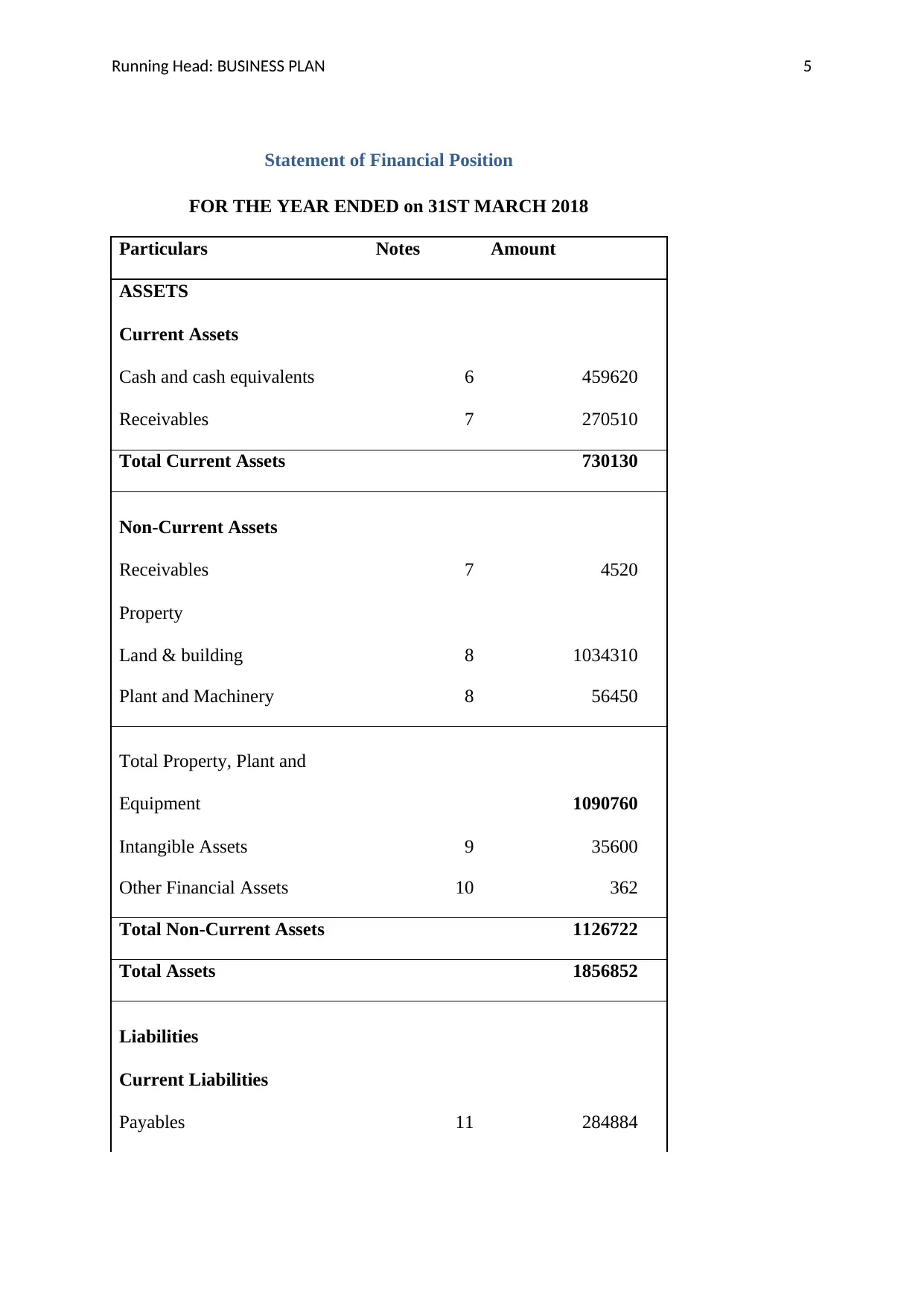

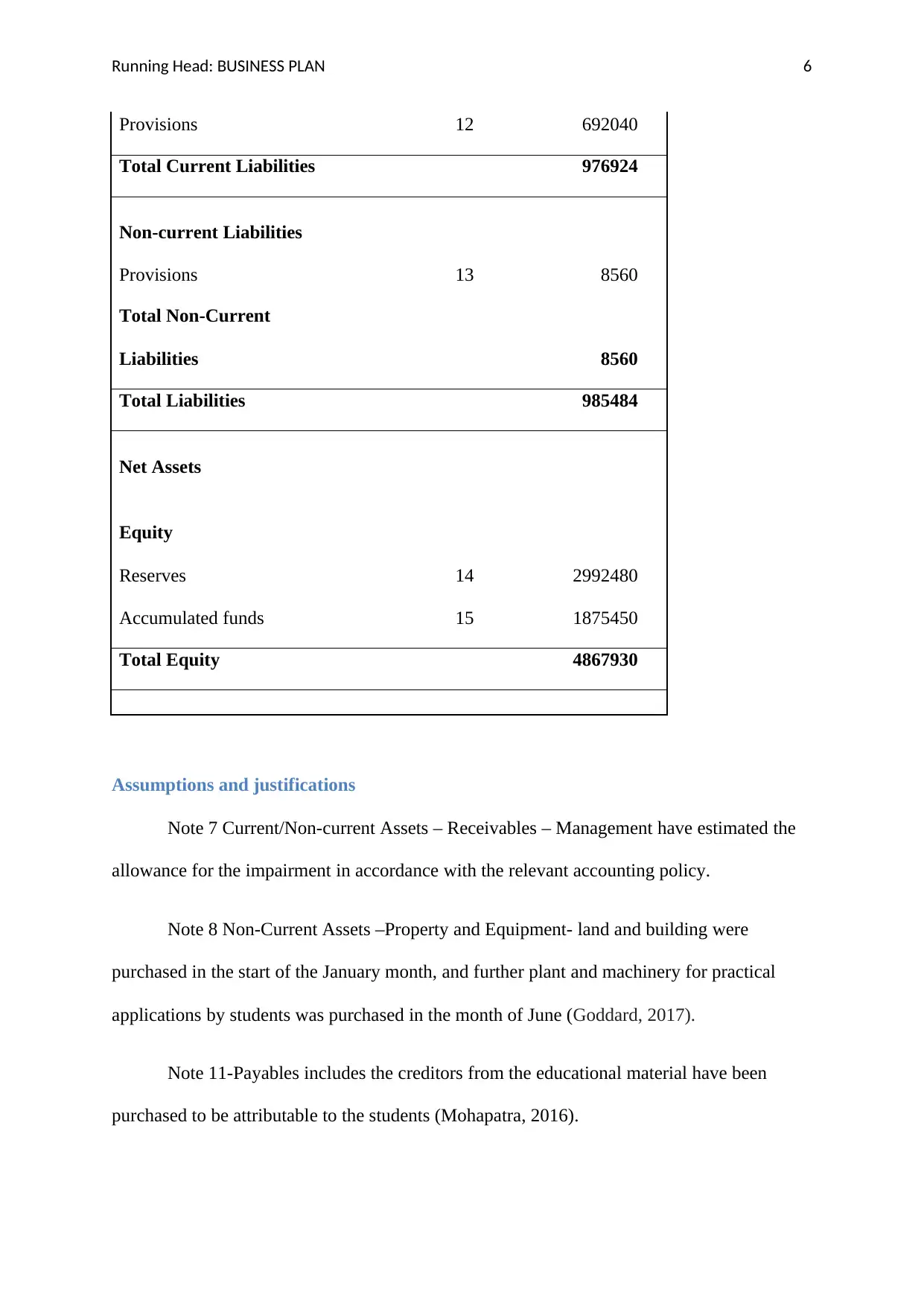

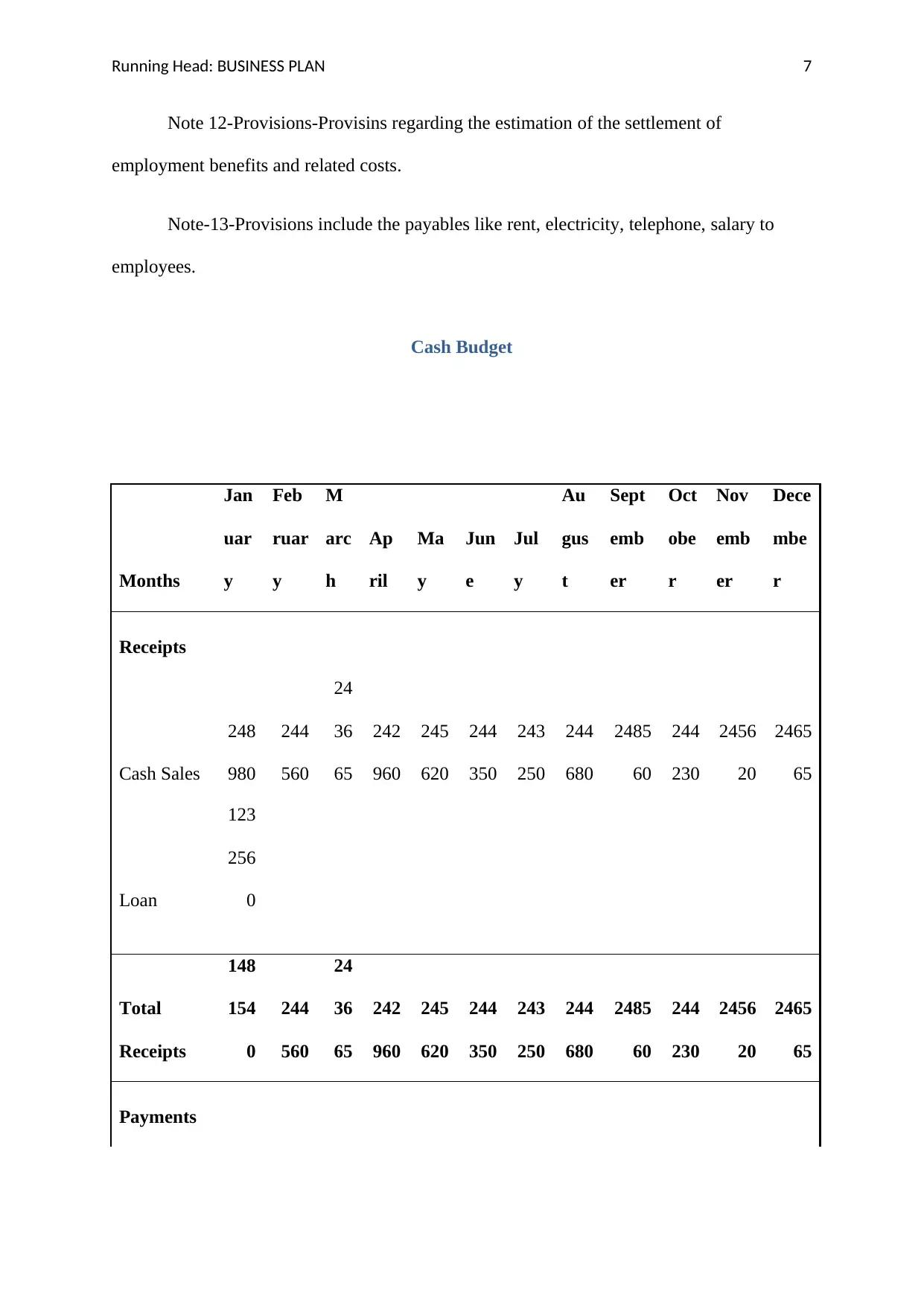

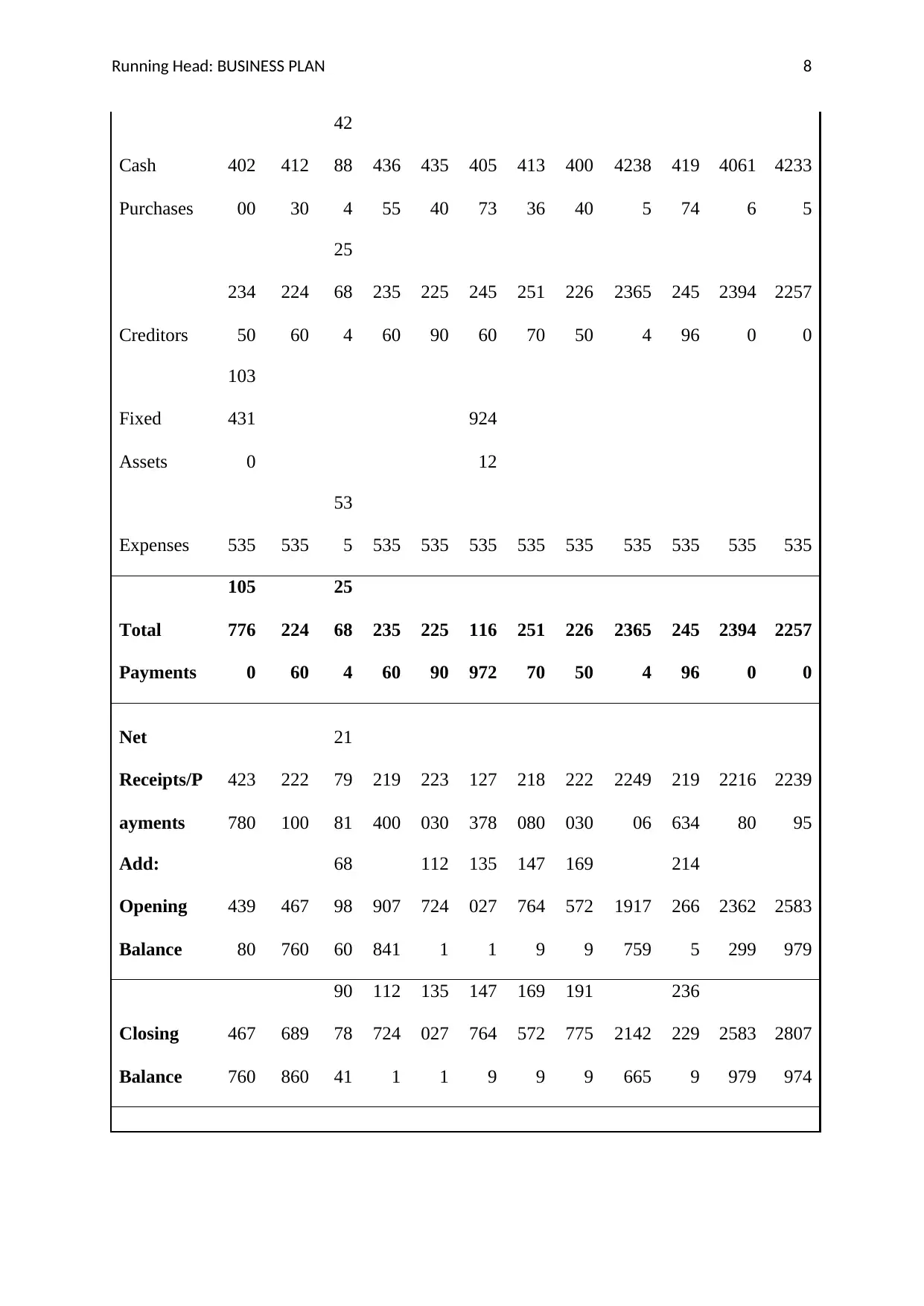

This document presents a detailed financial analysis for a contracting school business plan, including a pro forma income statement, balance sheet, and cash budget. Key assumptions and justifications are provided for each financial statement component, such as revenue recognition, grant contributions, and employee benefits. The analysis also includes a scrutiny of tangible and intangible assets, focusing on land, buildings, plant, and machinery. Furthermore, the report discusses equity valuation methods, emphasizing discounted cash flow, cost approach, and comparable approach. The conclusion highlights the importance of a solid business plan for the startup's survival and future growth. Desklib offers this document along with a wide array of solved assignments and past papers to aid students in their studies.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.