HI5020 Corporate Accounting: Analysis of Cooper Energy's Tax Expense

VerifiedAdded on 2024/04/17

|16

|3285

|139

Report

AI Summary

This report provides a comprehensive analysis of Cooper Energy Limited's financial statements, focusing on equity and tax-related aspects. It examines various equity items, including contributed equity, reserves, and accumulated losses, detailing changes and their underlying reasons. The report identifies the firm's tax expense, reconciles it with the accounting income, and explains discrepancies arising from non-deductible expenses and prior-period adjustments. It also discusses deferred tax assets and liabilities, outlining potential reasons for their recording, such as temporary differences between accounting and taxable income. Furthermore, the analysis clarifies the differences between income tax expense and income tax payable, as well as between income tax expense and the actual cash outflow for tax payments. The report concludes by reflecting on the complexities and insights gained from examining the company's tax treatment.

HI5020- Corporate accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:....................................................................................................................................3

1. From your firm’s financial statement, list each item of equity and write your understanding

of each item. Discuss any changes in each item of equity for your firm over the past year

articulating the reasons for the change.........................................................................................4

2. What is your firm’s tax expense in its latest financial statements?.........................................7

3. Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm...................................................................8

4. Comment on deferred tax assets/liabilities that are reported in the balance sheet articulating

the possible reasons why they have been recorded......................................................................9

5. Is there any current tax assets or income tax payable recorded by your company? Why is the

income tax payable not the same as income tax expense?.........................................................11

6. Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?..............................................12

7. What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s tax

expense in its accounts?.............................................................................................................13

Conclusion:....................................................................................................................................15

References:....................................................................................................................................16

2

Introduction:....................................................................................................................................3

1. From your firm’s financial statement, list each item of equity and write your understanding

of each item. Discuss any changes in each item of equity for your firm over the past year

articulating the reasons for the change.........................................................................................4

2. What is your firm’s tax expense in its latest financial statements?.........................................7

3. Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm...................................................................8

4. Comment on deferred tax assets/liabilities that are reported in the balance sheet articulating

the possible reasons why they have been recorded......................................................................9

5. Is there any current tax assets or income tax payable recorded by your company? Why is the

income tax payable not the same as income tax expense?.........................................................11

6. Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?..............................................12

7. What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s tax

expense in its accounts?.............................................................................................................13

Conclusion:....................................................................................................................................15

References:....................................................................................................................................16

2

Introduction:

The following report is related to corporate accounting and the concepts related to this

accounting. In order to understand the basic concepts of corporate accounting a company has

been chosen named Cooper Energy limited. The company has been engaged in finding,

developing and commercializing oil and gas. The financial statement of the company will be

recognized and analysed for the purpose of corporate governance. The information will be

presented about the tax liability of the company and analysis will be made about the deferred tax

asset and liability created by the company in the concerned year. An explanation will be given of

the understanding created for the tax liability of the company.

3

The following report is related to corporate accounting and the concepts related to this

accounting. In order to understand the basic concepts of corporate accounting a company has

been chosen named Cooper Energy limited. The company has been engaged in finding,

developing and commercializing oil and gas. The financial statement of the company will be

recognized and analysed for the purpose of corporate governance. The information will be

presented about the tax liability of the company and analysis will be made about the deferred tax

asset and liability created by the company in the concerned year. An explanation will be given of

the understanding created for the tax liability of the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. From your firm’s financial statement, list each item of equity and write your

understanding of each item. Discuss any changes in each item of equity for your firm over

the past year articulating the reasons for the change.

As per the latest annual report extracted for the company for the year ended 2017, the equity

portion of the company includes items such as contributed equity with a share of $343161000,

reserves of $6777000 and accumulated losses of the company amounting to ($64891000).

Therefore the total equity of the company comes out to be $285047000 (Cooper Energy Limited,

2017). The items of the equity are explained in brief as below:

Equity share capital – The equity share capital of the company represents the funds raised

by the company in exchange of the ordinary as well as preferred shares. The equity

capital of the company can fluctuate over the number of years based on the amount of

share capital issued by the company. However they bear a kind of cost of capital to be

incurred in the form of dividend and expectation of the shareholders of the company.

Reserves – The reserves of the company represents the retained profits of the company

which have not been distributed to the shareholders of the company and can be utilized

for future investment and capital purposes. There are certain rules and regulations as

prescribe d by the laws applicable to the company for determining the amount of reserves

that can be transferred for the net profit achieved by the company. The transfer to various

reserves should be carefully analysed as the decision will directly influence the wealth of

the shareholders of the company (Beekes, et. al., 2015).

Accumulated losses – The losses of the previous year’s which have been carried forward

for setting off from the future earnings are defined as accumulated losses. These losses of

the previous year’s results in decrease of the equity portion of the company. The

accumulated losses should be recognized after proper investigation and they should be

adequately presented in the annual reports and financial statements of the company.

4

understanding of each item. Discuss any changes in each item of equity for your firm over

the past year articulating the reasons for the change.

As per the latest annual report extracted for the company for the year ended 2017, the equity

portion of the company includes items such as contributed equity with a share of $343161000,

reserves of $6777000 and accumulated losses of the company amounting to ($64891000).

Therefore the total equity of the company comes out to be $285047000 (Cooper Energy Limited,

2017). The items of the equity are explained in brief as below:

Equity share capital – The equity share capital of the company represents the funds raised

by the company in exchange of the ordinary as well as preferred shares. The equity

capital of the company can fluctuate over the number of years based on the amount of

share capital issued by the company. However they bear a kind of cost of capital to be

incurred in the form of dividend and expectation of the shareholders of the company.

Reserves – The reserves of the company represents the retained profits of the company

which have not been distributed to the shareholders of the company and can be utilized

for future investment and capital purposes. There are certain rules and regulations as

prescribe d by the laws applicable to the company for determining the amount of reserves

that can be transferred for the net profit achieved by the company. The transfer to various

reserves should be carefully analysed as the decision will directly influence the wealth of

the shareholders of the company (Beekes, et. al., 2015).

Accumulated losses – The losses of the previous year’s which have been carried forward

for setting off from the future earnings are defined as accumulated losses. These losses of

the previous year’s results in decrease of the equity portion of the company. The

accumulated losses should be recognized after proper investigation and they should be

adequately presented in the annual reports and financial statements of the company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The statement of changes in equity is presented below in order to give a proper

understanding:

(Source: Cooper Energy Limited, 2017)

The above statement shows that the reason for the change in equity is issue of share capital in the

form of equity shares issued by the company. The issued share capital in the current year of 2017

is $203940000. The change in the reserves of the company has been due to the comprehensive

expenditure of the company (Ali, 2016). Also there has been loss for the company in the current

year which amounted to ($12312000) which resulted in increase in the accumulated losses of the

5

understanding:

(Source: Cooper Energy Limited, 2017)

The above statement shows that the reason for the change in equity is issue of share capital in the

form of equity shares issued by the company. The issued share capital in the current year of 2017

is $203940000. The change in the reserves of the company has been due to the comprehensive

expenditure of the company (Ali, 2016). Also there has been loss for the company in the current

year which amounted to ($12312000) which resulted in increase in the accumulated losses of the

5

company. The reserves have also been increased due to share based payments and there has been

a transfer to the issued share capital of the company.

6

a transfer to the issued share capital of the company.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. What is your firm’s tax expense in its latest financial statements?

The income tax expense as per the latest income statement of the company presented in the year

2017 has been ($2812000) for the year ending 2017. The major component contributing to the

income tax expense of the company is Petroleum resource rent tax expense which is amounting

to ($7598000) for the concerned year and also there has been a tax benefit arising to the

company for the amount of $4786000. The current year royalty tax of the company has been

($6117000). The current tax amounts of the company are measured and recognized in a manner

which is consistent with the principles of AASB 112 Income Taxes (Cooper Energy Limited,

2017). The tax rates applicable to the company are in respect of the domestic corporation tax rate

of 30%.

7

The income tax expense as per the latest income statement of the company presented in the year

2017 has been ($2812000) for the year ending 2017. The major component contributing to the

income tax expense of the company is Petroleum resource rent tax expense which is amounting

to ($7598000) for the concerned year and also there has been a tax benefit arising to the

company for the amount of $4786000. The current year royalty tax of the company has been

($6117000). The current tax amounts of the company are measured and recognized in a manner

which is consistent with the principles of AASB 112 Income Taxes (Cooper Energy Limited,

2017). The tax rates applicable to the company are in respect of the domestic corporation tax rate

of 30%.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

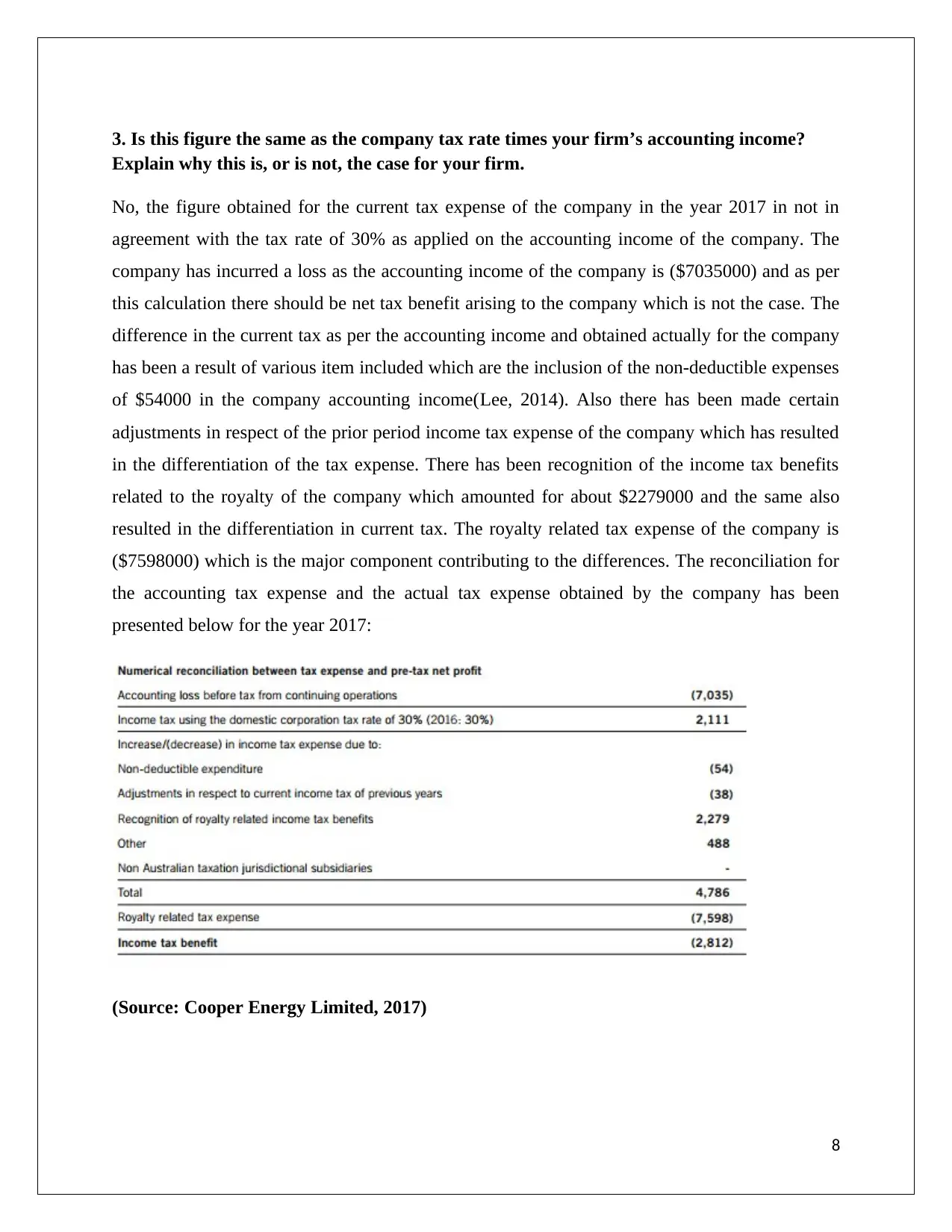

3. Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

No, the figure obtained for the current tax expense of the company in the year 2017 in not in

agreement with the tax rate of 30% as applied on the accounting income of the company. The

company has incurred a loss as the accounting income of the company is ($7035000) and as per

this calculation there should be net tax benefit arising to the company which is not the case. The

difference in the current tax as per the accounting income and obtained actually for the company

has been a result of various item included which are the inclusion of the non-deductible expenses

of $54000 in the company accounting income(Lee, 2014). Also there has been made certain

adjustments in respect of the prior period income tax expense of the company which has resulted

in the differentiation of the tax expense. There has been recognition of the income tax benefits

related to the royalty of the company which amounted for about $2279000 and the same also

resulted in the differentiation in current tax. The royalty related tax expense of the company is

($7598000) which is the major component contributing to the differences. The reconciliation for

the accounting tax expense and the actual tax expense obtained by the company has been

presented below for the year 2017:

(Source: Cooper Energy Limited, 2017)

8

Explain why this is, or is not, the case for your firm.

No, the figure obtained for the current tax expense of the company in the year 2017 in not in

agreement with the tax rate of 30% as applied on the accounting income of the company. The

company has incurred a loss as the accounting income of the company is ($7035000) and as per

this calculation there should be net tax benefit arising to the company which is not the case. The

difference in the current tax as per the accounting income and obtained actually for the company

has been a result of various item included which are the inclusion of the non-deductible expenses

of $54000 in the company accounting income(Lee, 2014). Also there has been made certain

adjustments in respect of the prior period income tax expense of the company which has resulted

in the differentiation of the tax expense. There has been recognition of the income tax benefits

related to the royalty of the company which amounted for about $2279000 and the same also

resulted in the differentiation in current tax. The royalty related tax expense of the company is

($7598000) which is the major component contributing to the differences. The reconciliation for

the accounting tax expense and the actual tax expense obtained by the company has been

presented below for the year 2017:

(Source: Cooper Energy Limited, 2017)

8

4. Comment on deferred tax assets/liabilities that are reported in the balance sheet

articulating the possible reasons why they have been recorded.

Deferred tax assets – Deferred tax assets arises in the case where the firm has paid taxes in

advance or overpaid taxes which are due to temporary differences recognized due to accounting

treatment and tax treatment of the company.

Deferred tax liability – Deferred tax liability can be represented as the future liability arising to

the company which have been recognized in the current year due to temporary differences in the

accounting income and taxable income of the company (Lee, 2014).

The deferred tax liabilities which have been recorded and created by the company in ten current

year consists of the amounts elated to trade and other receivables, oils and gas assets of the

company, related to exploration and evaluation, related to various provisions which are not

allowed as tax expenses in the current year and will be allowed in the year of occurrence, others

and in respect of unrealized currency translation gains. The whole of the above items resulted in

a deferred tax liability of $18740000.

Reason - The possible reasons for which they have been reported can be the reason that these

items would have resulted in decrease in the taxable income of the company as per the taxation

rules because the tax corporation has allowed in excess of what should be allowed to the

company. Therefore the tax related to these items will be paid in the future years when the same

become due according to the taxation rules applicable to the company.

The deferred tax assets as created by the company in the concerned year consists of items related

to trade and other payables, provisions created from various employee entitlements, provisions,

others, capital raising cost in equity and due to tax losses incurred in the current year but the

benefit will be received in the year when there will be recognized positive income by the

company (Lee, 2014). The total deferred tax asset created by the company for the concerned year

is $23054.

Reason – The reason for creating these deferred tax assets is that the company is anticipating a

lower taxable income as per its accounting records but the taxation authority is not allowing the

concerned items for allowable tax expenses and therefore the benefits of these expenses will be

9

articulating the possible reasons why they have been recorded.

Deferred tax assets – Deferred tax assets arises in the case where the firm has paid taxes in

advance or overpaid taxes which are due to temporary differences recognized due to accounting

treatment and tax treatment of the company.

Deferred tax liability – Deferred tax liability can be represented as the future liability arising to

the company which have been recognized in the current year due to temporary differences in the

accounting income and taxable income of the company (Lee, 2014).

The deferred tax liabilities which have been recorded and created by the company in ten current

year consists of the amounts elated to trade and other receivables, oils and gas assets of the

company, related to exploration and evaluation, related to various provisions which are not

allowed as tax expenses in the current year and will be allowed in the year of occurrence, others

and in respect of unrealized currency translation gains. The whole of the above items resulted in

a deferred tax liability of $18740000.

Reason - The possible reasons for which they have been reported can be the reason that these

items would have resulted in decrease in the taxable income of the company as per the taxation

rules because the tax corporation has allowed in excess of what should be allowed to the

company. Therefore the tax related to these items will be paid in the future years when the same

become due according to the taxation rules applicable to the company.

The deferred tax assets as created by the company in the concerned year consists of items related

to trade and other payables, provisions created from various employee entitlements, provisions,

others, capital raising cost in equity and due to tax losses incurred in the current year but the

benefit will be received in the year when there will be recognized positive income by the

company (Lee, 2014). The total deferred tax asset created by the company for the concerned year

is $23054.

Reason – The reason for creating these deferred tax assets is that the company is anticipating a

lower taxable income as per its accounting records but the taxation authority is not allowing the

concerned items for allowable tax expenses and therefore the benefits of these expenses will be

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

obtained in the future years when the conditions related to their allow ability will be fulfilled by

the company.

10

the company.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Is there any current tax assets or income tax payable recorded by your company? Why is

the income tax payable not the same as income tax expense?

By referring to the financial statements of the company it can be observed that there exists no

current tax assets for the company for the concerned year and also there has been no income tax

payable recorded by the company in the current year. The income tax expense represents the

actual tax liability of the company for the year which is recognized after considering all the

incomes and expenses of the current year and applying the concerned tax rate of the company.

However income tax payable represents the total amount consisting of the current tax liability

and the amounts of prior period including certain adjustments which are considered to be payable

by the company to the concerned taxation authority of the country. Therefore the amount of both

the items can be different for the company as the current tax liability can be different and the

income tax payable can include the prior period adjustments of the tax liability of the company

(Henderson, et. al., 2015).

11

the income tax payable not the same as income tax expense?

By referring to the financial statements of the company it can be observed that there exists no

current tax assets for the company for the concerned year and also there has been no income tax

payable recorded by the company in the current year. The income tax expense represents the

actual tax liability of the company for the year which is recognized after considering all the

incomes and expenses of the current year and applying the concerned tax rate of the company.

However income tax payable represents the total amount consisting of the current tax liability

and the amounts of prior period including certain adjustments which are considered to be payable

by the company to the concerned taxation authority of the country. Therefore the amount of both

the items can be different for the company as the current tax liability can be different and the

income tax payable can include the prior period adjustments of the tax liability of the company

(Henderson, et. al., 2015).

11

6. Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?

The income tax expenses shown in the income statement of the company Cooper energy Limited

is $2812000 whereas the income tax paid by the company in the current year of 2017 as per the

cash flow statements of the company is NIL. Therefore it shows that there is a difference in the

income tax liability ascertained for the company and the actual cash outflow incurred for the tax

liability of the company. The reason behind this is the liability created for the further years which

can be adjusted in the future income tax benefits or liability to be paid by the company. The tax

liability of the company represents the premium resource tax to be paid for the current year after

considering the tax benefit and the same has been $2812000 but the actual payment made for the

same is $2785000 which is due to the adjustment of the prior period tax expense already paid by

the company (Cooper Energy Limited, 2017).

12

shown in the cash flow statement? If not why is the difference?

The income tax expenses shown in the income statement of the company Cooper energy Limited

is $2812000 whereas the income tax paid by the company in the current year of 2017 as per the

cash flow statements of the company is NIL. Therefore it shows that there is a difference in the

income tax liability ascertained for the company and the actual cash outflow incurred for the tax

liability of the company. The reason behind this is the liability created for the further years which

can be adjusted in the future income tax benefits or liability to be paid by the company. The tax

liability of the company represents the premium resource tax to be paid for the current year after

considering the tax benefit and the same has been $2812000 but the actual payment made for the

same is $2785000 which is due to the adjustment of the prior period tax expense already paid by

the company (Cooper Energy Limited, 2017).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.