ACC321 Audit Planning: Financial Statement Analysis Coral Enterprise

VerifiedAdded on 2023/06/08

|10

|2015

|135

Report

AI Summary

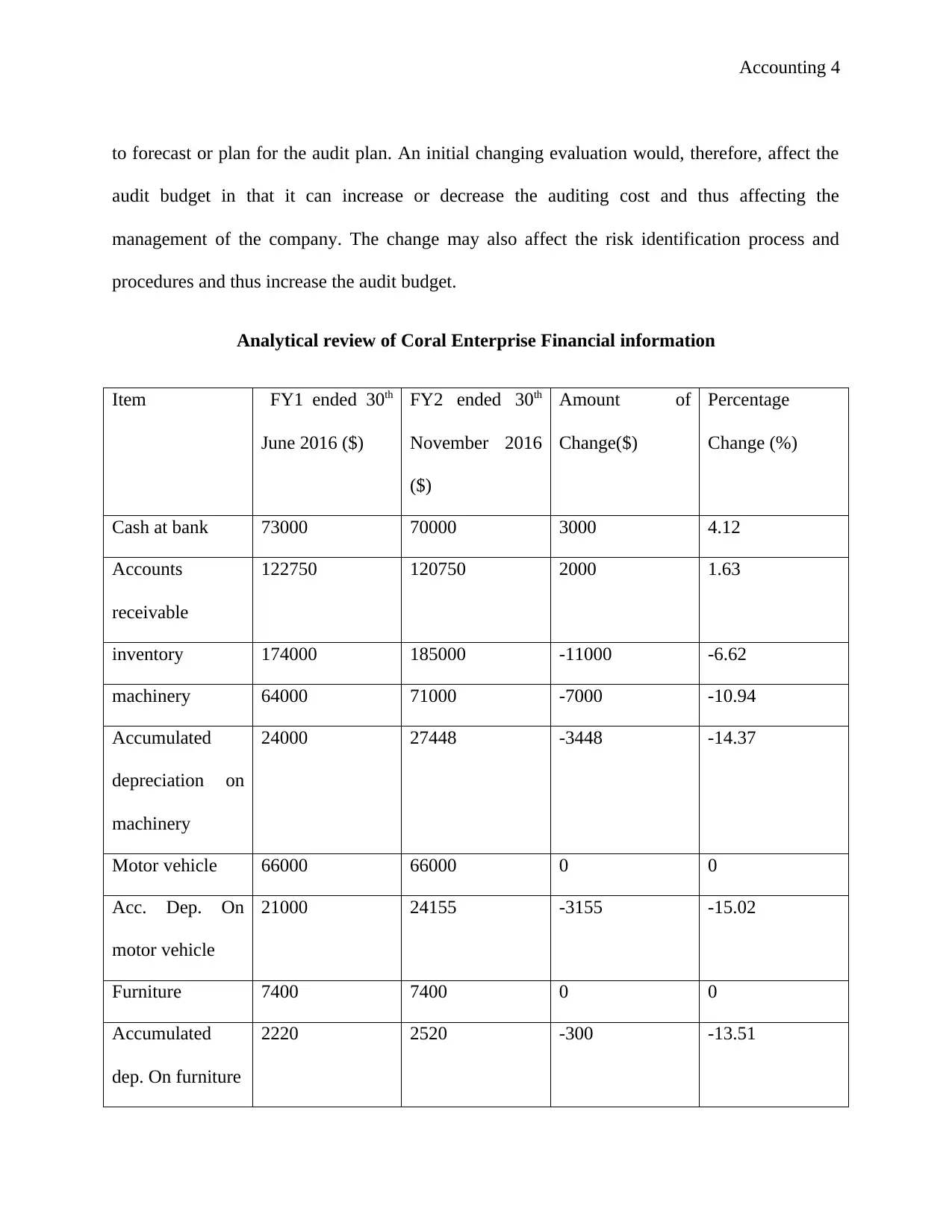

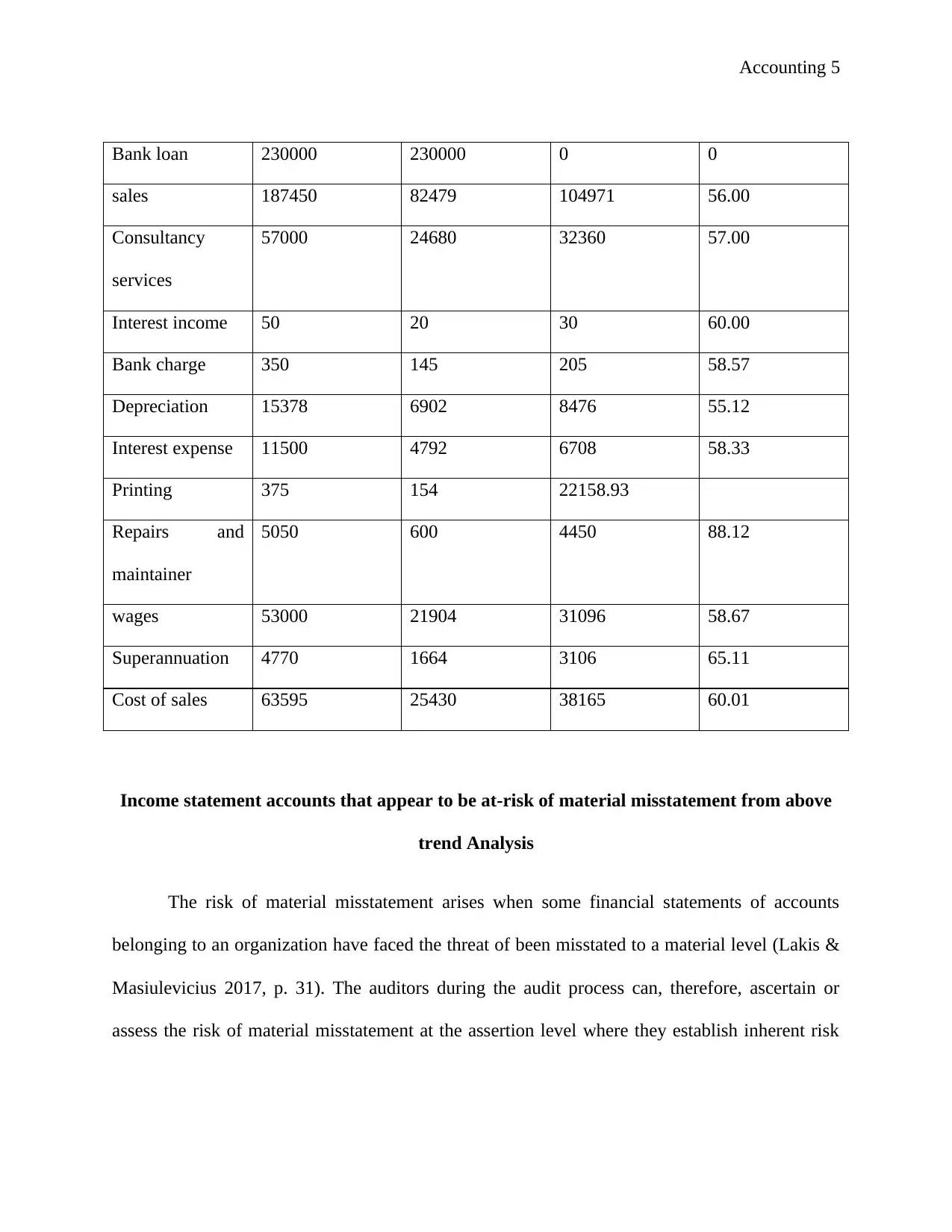

This report presents an audit plan for Coral Enterprise, focusing on the critical analysis of its financial statements to ensure an accurate and fair reflection of business performance. The plan includes a discussion of materiality, analytical review of financial information, selection and justification of key accounts and assertions, and the design of appropriate audit procedures. Materiality is assessed using the constant percentage method, and analytical review identifies accounts at risk of material misstatement, such as inventory, wages, and sales. Relevant audit procedures are outlined for each account, addressing assertions like existence, accuracy, and cut-off. The report also critiques the partner's suggestion to disregard fraud risk assessment based on staff trustworthiness, emphasizing the importance of considering fraud risk in any auditing process. Ultimately, the audit plan aims to provide a preliminary assessment to guide the senior auditor in establishing the reliability and validity of the financial information, forecasting the audit budget, and disclosing any financial misstatements.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.