MAA363 Corporate Accounting: Financial Statements and AASB 16 Impact

VerifiedAdded on 2022/09/07

|9

|1480

|17

Report

AI Summary

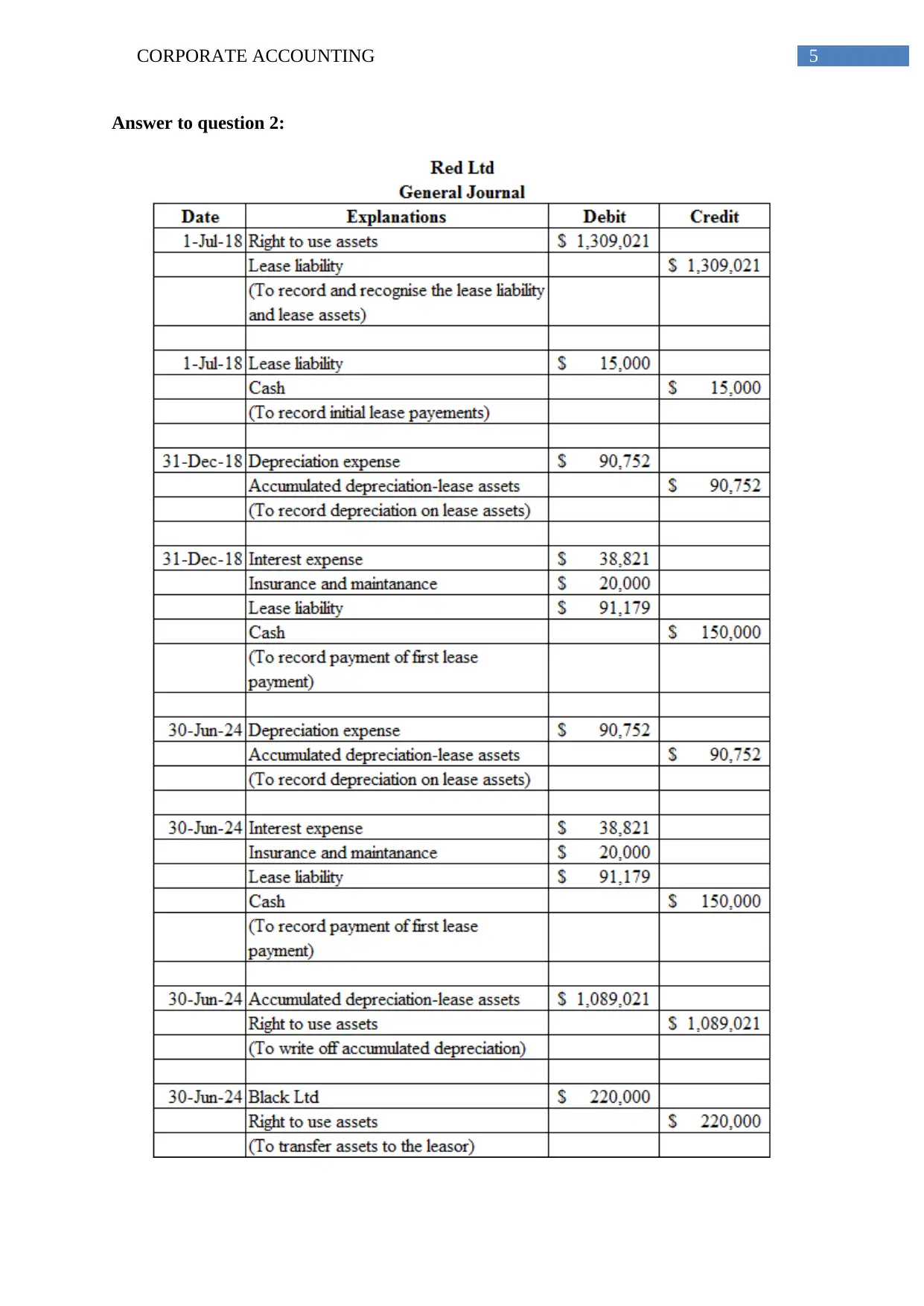

This report delves into corporate accounting, focusing on the implications of AASB 16 on lease accounting and the concept of a 'true and fair view' in financial statements. It discusses the recognition of lease liabilities and assets, highlighting how AASB 16 impacts the solvency and transparency of businesses. The report also addresses the challenges of implementing new accounting standards and the importance of uniform global reporting. Furthermore, it explores the role of financial statements in reflecting a company's financial performance and the ethical considerations for directors in ensuring accurate and fair representation. The analysis includes a discussion on the need for comparability in financial reporting and the efforts to establish consistent accounting standards worldwide.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.