Corporate Accounting Report: AASB3/IFRS3 Acquisition Method Analysis

VerifiedAdded on 2022/10/09

|12

|2435

|403

Report

AI Summary

This report provides a comprehensive analysis of the acquisition method in corporate accounting, specifically focusing on AASB3/IFRS3. It begins with an introduction to accounting standards and their role in ensuring proper financial reporting, particularly in the context of business acquisitions. The report delves into the purpose and content of AASB 3, emphasizing the valuation methods and disclosure requirements. It discusses the importance of properly reporting business acquisitions to stakeholders and the objectives of AASB 3 in measuring assets, liabilities, and non-controlling interests. The discussion covers key areas such as identifying the acquirer, determining the acquisition date, recognizing and measuring assets, liabilities, and goodwill, and the required disclosures. The report also examines the practical application of the acquisition method, including the steps involved and the recognition criteria for assets, liabilities, and non-controlling interests. It highlights the significance of fair value measurement and the recognition and measurement of goodwill. The report concludes by emphasizing the detailed requirements of AASB 3 and their implications for accounting professionals and the importance of adhering to disclosure requirements.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Part A: The acquisition method in AASB3/IFRS3

Introduction:

Accounting standards are guidelines which are issued by an accounting regulations body

for the purpose of ensuring that proper guideline is available in the market regarding the

treatment of key transactions of a business. The accounting standards not only shows different

methods which needs to be applied by an accountant but also the disclosures which the

accountant needs to provide so that the users can understand the transactions in better way.

AASB 3 Business Combinations is considered for discussion regarding the treatments which

needs to be followed by an accountant along with the disclosures which needs to be provided by

the corporate entity (Aasb.gov.au. 2019). The focus of the discussion would be on the valuation

method which is stated under the accounting standard and it would be assessed whether the same

is appropriate from a business perspective. The acquisition of a business needs to be properly

reported so that the business is able to reveal to the stakeholders whether the transactions which

have taken place are appropriate or not. The purpose for introducing AASB 3 was to ensure that

the assets and liabilities which arises at the time of acquisition of a business can be measured

appropriately and the same can be reported in the books of accounts which is formulated by the

business (Christensen, Cottrell and Baker 2013). Another complex aspect which needs to be

reported in respect of an acquisition is the amount of non-controlling interest present in the

acquiree company. In case of an acquisition of a business, the acquire company needs to present

all the information from both the entities in a consolidated format so that the users are able to get

a clear idea about the process and performance post acquisition.

CORPORATE ACCOUNTING

Part A: The acquisition method in AASB3/IFRS3

Introduction:

Accounting standards are guidelines which are issued by an accounting regulations body

for the purpose of ensuring that proper guideline is available in the market regarding the

treatment of key transactions of a business. The accounting standards not only shows different

methods which needs to be applied by an accountant but also the disclosures which the

accountant needs to provide so that the users can understand the transactions in better way.

AASB 3 Business Combinations is considered for discussion regarding the treatments which

needs to be followed by an accountant along with the disclosures which needs to be provided by

the corporate entity (Aasb.gov.au. 2019). The focus of the discussion would be on the valuation

method which is stated under the accounting standard and it would be assessed whether the same

is appropriate from a business perspective. The acquisition of a business needs to be properly

reported so that the business is able to reveal to the stakeholders whether the transactions which

have taken place are appropriate or not. The purpose for introducing AASB 3 was to ensure that

the assets and liabilities which arises at the time of acquisition of a business can be measured

appropriately and the same can be reported in the books of accounts which is formulated by the

business (Christensen, Cottrell and Baker 2013). Another complex aspect which needs to be

reported in respect of an acquisition is the amount of non-controlling interest present in the

acquiree company. In case of an acquisition of a business, the acquire company needs to present

all the information from both the entities in a consolidated format so that the users are able to get

a clear idea about the process and performance post acquisition.

2

CORPORATE ACCOUNTING

Discussion:

It is to be noted that accounting standards are implemented so that guidance can be

provided regarding complex areas of the business and proper treatments can be done for complex

transactions of the business. The reason due to which AASB 3 Business Combinations has been

implemented is to ensure that the reporting for acquisition of another business is shown in an

appropriate manner in the books of accounts of the business (Sedláček, Křížová and Hýblová

2013). The standard was introduced for the purpose of providing guideline to the accounting

professionals for proper maintenance of the financial information relating to acquisition of a

business. The standard was introduced with an objective so that relevant information relating to

business combinations can be given in the annual reports of the business. Some of the key areas

which would be the focus of this accounting standard are listed below in point form and the same

are:

The standard aims to recognise identifiable assets, liabilities and non-controlling interests

of the business which is being acquired.

The treatment and recognition of goodwill which is derived from the acquisition process

is also important which would be shown in the analysis of the financial reports.

Further the standard also discusses regarding the disclosure requirements which the

business needs to show in the books of accounts.

In today’s world, acquisition and mergers are common techniques which is used by the

business for the purpose of achieving growth in the organization and thereby also increasing the

productivity of the entity (Paugam, Astolfi and Ramond 2015). There is also the impact of

synergy which comes with acquisition of a corporate entity and the same results in improvement

of the productivity and lead the business to growth and development. In a process of acquisition,

CORPORATE ACCOUNTING

Discussion:

It is to be noted that accounting standards are implemented so that guidance can be

provided regarding complex areas of the business and proper treatments can be done for complex

transactions of the business. The reason due to which AASB 3 Business Combinations has been

implemented is to ensure that the reporting for acquisition of another business is shown in an

appropriate manner in the books of accounts of the business (Sedláček, Křížová and Hýblová

2013). The standard was introduced for the purpose of providing guideline to the accounting

professionals for proper maintenance of the financial information relating to acquisition of a

business. The standard was introduced with an objective so that relevant information relating to

business combinations can be given in the annual reports of the business. Some of the key areas

which would be the focus of this accounting standard are listed below in point form and the same

are:

The standard aims to recognise identifiable assets, liabilities and non-controlling interests

of the business which is being acquired.

The treatment and recognition of goodwill which is derived from the acquisition process

is also important which would be shown in the analysis of the financial reports.

Further the standard also discusses regarding the disclosure requirements which the

business needs to show in the books of accounts.

In today’s world, acquisition and mergers are common techniques which is used by the

business for the purpose of achieving growth in the organization and thereby also increasing the

productivity of the entity (Paugam, Astolfi and Ramond 2015). There is also the impact of

synergy which comes with acquisition of a corporate entity and the same results in improvement

of the productivity and lead the business to growth and development. In a process of acquisition,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

the acquirer company obtains all the assets of the company which is being acquired and the

former also needs to show all assets and liabilities in a consolidated format after acquisition is

completed. The business needs to show appropriate treatment for the takeover of the assets and

the same needs to be shown appropriately in the financial reports of an entity.

The method for acquisition for an entity which is specified by the accounting standard

enables the accounting professionals to follow a set of procedures so that the transactions can be

appropriately shown in the books of accounts relating to the company. As per “para 4 of AASB

3 Business Combinations”, an entity needs to account for business combinations by following a

proper acquisition method. The application of acquisition method requires the management of

the company to follow the steps which is prescribed below:

Identification of the acquirer business.

Identification of the date of acquisition of the business.

Recognition and measurement of assets which are acquired along with the liabilities of

the business. The business also needs to consider if there is any non-controlling interest

which needs to be reported.

Recognition and measurement of goodwill which has arisen due to acquisition of the

undertaking.

The steps which are discussed above are discussed in more details in the paragraph which is

shown below and the same deals with the reporting requirement which is applicable to a

business.

Identifying the Acquirer

CORPORATE ACCOUNTING

the acquirer company obtains all the assets of the company which is being acquired and the

former also needs to show all assets and liabilities in a consolidated format after acquisition is

completed. The business needs to show appropriate treatment for the takeover of the assets and

the same needs to be shown appropriately in the financial reports of an entity.

The method for acquisition for an entity which is specified by the accounting standard

enables the accounting professionals to follow a set of procedures so that the transactions can be

appropriately shown in the books of accounts relating to the company. As per “para 4 of AASB

3 Business Combinations”, an entity needs to account for business combinations by following a

proper acquisition method. The application of acquisition method requires the management of

the company to follow the steps which is prescribed below:

Identification of the acquirer business.

Identification of the date of acquisition of the business.

Recognition and measurement of assets which are acquired along with the liabilities of

the business. The business also needs to consider if there is any non-controlling interest

which needs to be reported.

Recognition and measurement of goodwill which has arisen due to acquisition of the

undertaking.

The steps which are discussed above are discussed in more details in the paragraph which is

shown below and the same deals with the reporting requirement which is applicable to a

business.

Identifying the Acquirer

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

The acquisition of the acquirer would be done as per the guidance which is provided in

AASB 10 which covers the acquisition of another business. The acquisition provides control to

acquirer business regarding the business which is actually being acquired (Wen and Moehrle

2016). In case a business combination has taken place but the same cannot be identified by

applying the guidance of the AASB 10 than the factors which are stated under the recognition

criteria is considered for the purpose of identification.

Determination of Acquisition Date

The date on which the acquirer attained control over the business which is acquired

would be considered as the date of acquisition for the purpose of reporting. This is the date on

which the purchase consideration for the business is transferred and all items of the balance sheet

is being transferred to the acquirer. This is also known as the closing date for the acquisition

where all requirements are settled by the business. However, it is to be noted that the acquirer

must attain control over the operations of the business either earlier or on the closing date for the

transaction.

Recognition Criteria for Assets, liabilities and Non- controlling interest of the Business

The provision which is specified under “para 10 of AASB 3 Business Combinations”,

the acquirer needs to recognise and account in a separate form for the goodwill, identifiable

assets and the liabilities which are assumed by the business along with any non-controlling

interest which is present in the acquire business (AASB 2014). However, it is to be noted that

there are certain conditions which needs to be met prior to the recognition criteria of a business.

One of the main conditions for the purpose of recognition as a part of the method of acquisition

of a business requires the recognizable assets and liabilities to meet the definitions of assets and

CORPORATE ACCOUNTING

The acquisition of the acquirer would be done as per the guidance which is provided in

AASB 10 which covers the acquisition of another business. The acquisition provides control to

acquirer business regarding the business which is actually being acquired (Wen and Moehrle

2016). In case a business combination has taken place but the same cannot be identified by

applying the guidance of the AASB 10 than the factors which are stated under the recognition

criteria is considered for the purpose of identification.

Determination of Acquisition Date

The date on which the acquirer attained control over the business which is acquired

would be considered as the date of acquisition for the purpose of reporting. This is the date on

which the purchase consideration for the business is transferred and all items of the balance sheet

is being transferred to the acquirer. This is also known as the closing date for the acquisition

where all requirements are settled by the business. However, it is to be noted that the acquirer

must attain control over the operations of the business either earlier or on the closing date for the

transaction.

Recognition Criteria for Assets, liabilities and Non- controlling interest of the Business

The provision which is specified under “para 10 of AASB 3 Business Combinations”,

the acquirer needs to recognise and account in a separate form for the goodwill, identifiable

assets and the liabilities which are assumed by the business along with any non-controlling

interest which is present in the acquire business (AASB 2014). However, it is to be noted that

there are certain conditions which needs to be met prior to the recognition criteria of a business.

One of the main conditions for the purpose of recognition as a part of the method of acquisition

of a business requires the recognizable assets and liabilities to meet the definitions of assets and

5

CORPORATE ACCOUNTING

liabilities which are set out in the framework of presentation and preparation of the financial

statements. Another major consideration is to meet the recognition standard of a corporate entity.

The acquisition of the assets of the business needs to be considered for all transactions which are

applicable to Australian Accounting Standards. In a similar fashion, the recognition criteria can

be applied to some of the assets and liabilities which are applicable to an asset or liability which

was not previously recognised by the acquirer company in the books of accounts maintained by

the business (Loyeung et al. 2016). Therefore, the recognition criteria effectively help in

identifying the assets and liabilities which have been missed out and ensure that the same can be

appropriately reported in the financial, statement of the business.

As per “para 15 of AASB 3 Business Combinations”, the acquirer can identify and

classify the assets and liabilities which are assumed to be necessary for application of other

accounting standards of the business. The acquirer would in such a case undertake the

classification on the bis of the terms of contracts, economic conditions and accounting policies as

per they exist on the acquisition date. However, there are exceptions to para 15 which is shown

above which are classification of lease contracts as per AASB 117 Leases and classification of

insurance contracts as per AASB 4 Insurance Contracts. The measurement principles which are

stated under “para 18 of AASB 3 Business Combinations”, reveals that the assets and liabilities

which are identified for the acquirer business must be assumed at their fair values which is

shown at their acquisition dates (Masadeh, Mansour and AL Salamat 2017). In the case of non-

controlling interest, the acquirer shall measure of the items considering either:

At its Fair value

The present possessed instruments proportionate share in the recognised amounts of the

identifiable assets of the business.

CORPORATE ACCOUNTING

liabilities which are set out in the framework of presentation and preparation of the financial

statements. Another major consideration is to meet the recognition standard of a corporate entity.

The acquisition of the assets of the business needs to be considered for all transactions which are

applicable to Australian Accounting Standards. In a similar fashion, the recognition criteria can

be applied to some of the assets and liabilities which are applicable to an asset or liability which

was not previously recognised by the acquirer company in the books of accounts maintained by

the business (Loyeung et al. 2016). Therefore, the recognition criteria effectively help in

identifying the assets and liabilities which have been missed out and ensure that the same can be

appropriately reported in the financial, statement of the business.

As per “para 15 of AASB 3 Business Combinations”, the acquirer can identify and

classify the assets and liabilities which are assumed to be necessary for application of other

accounting standards of the business. The acquirer would in such a case undertake the

classification on the bis of the terms of contracts, economic conditions and accounting policies as

per they exist on the acquisition date. However, there are exceptions to para 15 which is shown

above which are classification of lease contracts as per AASB 117 Leases and classification of

insurance contracts as per AASB 4 Insurance Contracts. The measurement principles which are

stated under “para 18 of AASB 3 Business Combinations”, reveals that the assets and liabilities

which are identified for the acquirer business must be assumed at their fair values which is

shown at their acquisition dates (Masadeh, Mansour and AL Salamat 2017). In the case of non-

controlling interest, the acquirer shall measure of the items considering either:

At its Fair value

The present possessed instruments proportionate share in the recognised amounts of the

identifiable assets of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

The measurement principle helps businesses to provide for appropriate values in the financial

statement of the business and ensures that proper disclosures are available for all items relating

to acquisition of a business.

Recognising and Measuring Goodwill

The recognition and measurement of goodwill of the business is important factor and the

same needs to be demonstrated in annual reports in an appropriate manner. The requirements

which are stated under “para 32 of AASB 3 Business Combinations”, reveals that goodwill shall

be recognised on the acquisition date as a measure of excess of either (a) or (b) which is stated

below:

a) The aggregate of the follow:

The purchase consideration which is transferred in respect of the acquisition and

generally requires considering fair value at the date of acquisition.

The amount of any non-controlling interest in the business of acquire which needs to

be measured according to the standard

In case of business acquisition which has been executed in stages then the acquisition

date fair value for the acquirer previously held equity in the business of acquiree is to

be considered.

b) The net of amounts at acquisition date for the assets and liabilities which are identifiable

considering the same which are measured according to the standard.

The above mentioned are the major criteria which are covered in an acquisition method of a

business and in accordance with the same appropriate reporting framework is to be applied for

the purpose of ensuring that the users are able to take decisions considering the information

CORPORATE ACCOUNTING

The measurement principle helps businesses to provide for appropriate values in the financial

statement of the business and ensures that proper disclosures are available for all items relating

to acquisition of a business.

Recognising and Measuring Goodwill

The recognition and measurement of goodwill of the business is important factor and the

same needs to be demonstrated in annual reports in an appropriate manner. The requirements

which are stated under “para 32 of AASB 3 Business Combinations”, reveals that goodwill shall

be recognised on the acquisition date as a measure of excess of either (a) or (b) which is stated

below:

a) The aggregate of the follow:

The purchase consideration which is transferred in respect of the acquisition and

generally requires considering fair value at the date of acquisition.

The amount of any non-controlling interest in the business of acquire which needs to

be measured according to the standard

In case of business acquisition which has been executed in stages then the acquisition

date fair value for the acquirer previously held equity in the business of acquiree is to

be considered.

b) The net of amounts at acquisition date for the assets and liabilities which are identifiable

considering the same which are measured according to the standard.

The above mentioned are the major criteria which are covered in an acquisition method of a

business and in accordance with the same appropriate reporting framework is to be applied for

the purpose of ensuring that the users are able to take decisions considering the information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

which is provided in the financial reports of the business. In addition to the treatments which is

specified in the accounting standard, there are certain disclosure requirements which the business

needs to follow while reporting business combinations and some of the information are

considered to be important for the users to judge the nature and financial effect of business

combinations on a business. The acquirer business needs to reveal the period in which business

combination had taken place during either the current reporting period or at the end of the

reporting period. The acquirer of the business needs to disclose information that enable the users

of the financial statements to evaluate the effects of adjustments which is recognised in the

current reporting period of the business or that which has taken place in previous reporting

periods.

Conclusion

The analysis of the reporting framework which is to be followed in case of acquisition of

a business shows that the accounting professionals needs to adhere to a lot of requirements.

These requirements are appropriately covered in the guidelines which is provided in AASB 3

business combinations. The standard shows various reporting requirements and identification

which is required to be followed by business so that the management of the company can

appropriately report financial information to the users of the financial statement. The standard

shows the measurement criteria and the importance of acquisition method which is required to be

followed when undertaking an acquisition of a business. The analysis of the Standard further

reveals how goodwill is to be identified in case of acquisition and measurement criteria relating

to the same. The accounting standard further provides disclosure requirements which the entity

needs to adhere to for reporting key financial information relating to acquisition of a business.

CORPORATE ACCOUNTING

which is provided in the financial reports of the business. In addition to the treatments which is

specified in the accounting standard, there are certain disclosure requirements which the business

needs to follow while reporting business combinations and some of the information are

considered to be important for the users to judge the nature and financial effect of business

combinations on a business. The acquirer business needs to reveal the period in which business

combination had taken place during either the current reporting period or at the end of the

reporting period. The acquirer of the business needs to disclose information that enable the users

of the financial statements to evaluate the effects of adjustments which is recognised in the

current reporting period of the business or that which has taken place in previous reporting

periods.

Conclusion

The analysis of the reporting framework which is to be followed in case of acquisition of

a business shows that the accounting professionals needs to adhere to a lot of requirements.

These requirements are appropriately covered in the guidelines which is provided in AASB 3

business combinations. The standard shows various reporting requirements and identification

which is required to be followed by business so that the management of the company can

appropriately report financial information to the users of the financial statement. The standard

shows the measurement criteria and the importance of acquisition method which is required to be

followed when undertaking an acquisition of a business. The analysis of the Standard further

reveals how goodwill is to be identified in case of acquisition and measurement criteria relating

to the same. The accounting standard further provides disclosure requirements which the entity

needs to adhere to for reporting key financial information relating to acquisition of a business.

8

CORPORATE ACCOUNTING

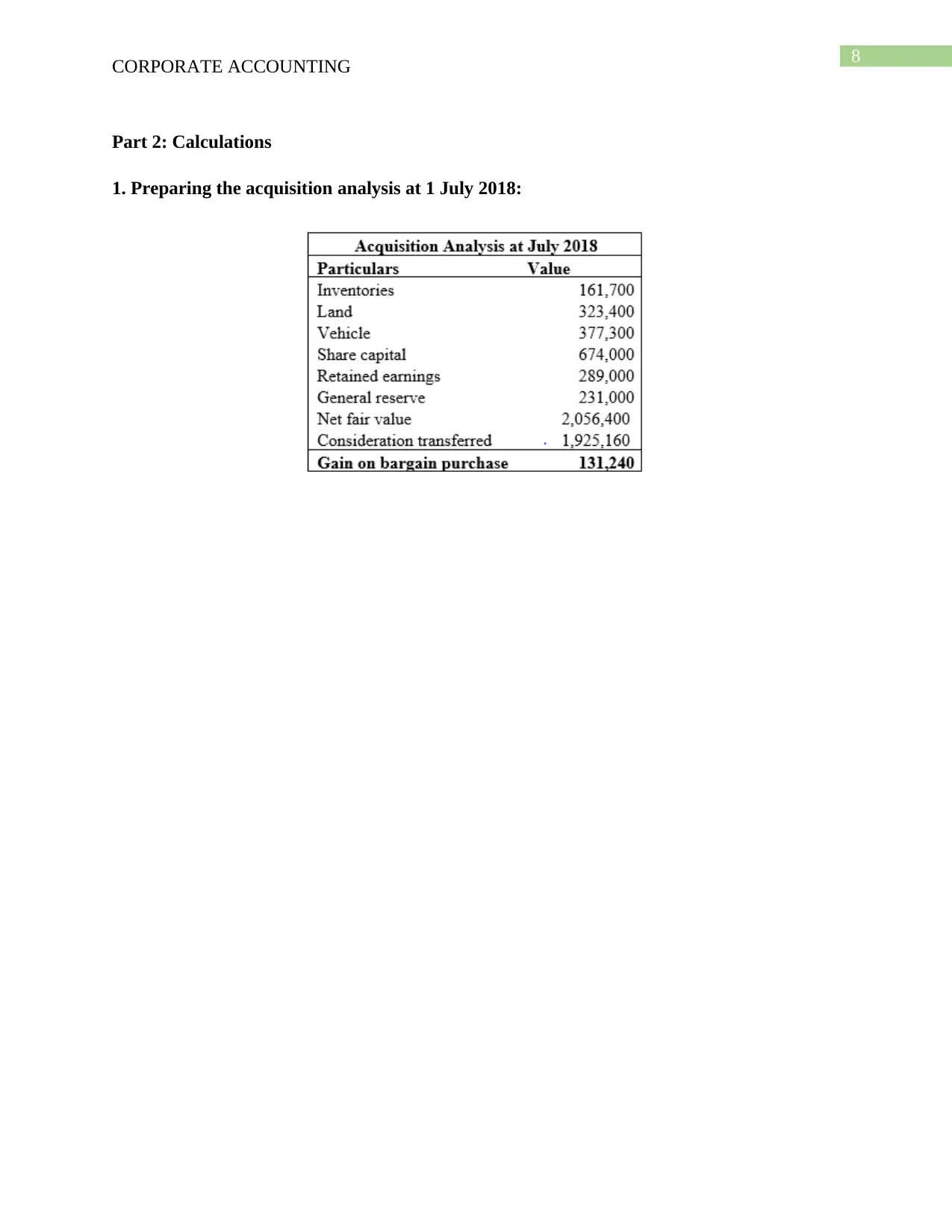

Part 2: Calculations

1. Preparing the acquisition analysis at 1 July 2018:

CORPORATE ACCOUNTING

Part 2: Calculations

1. Preparing the acquisition analysis at 1 July 2018:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

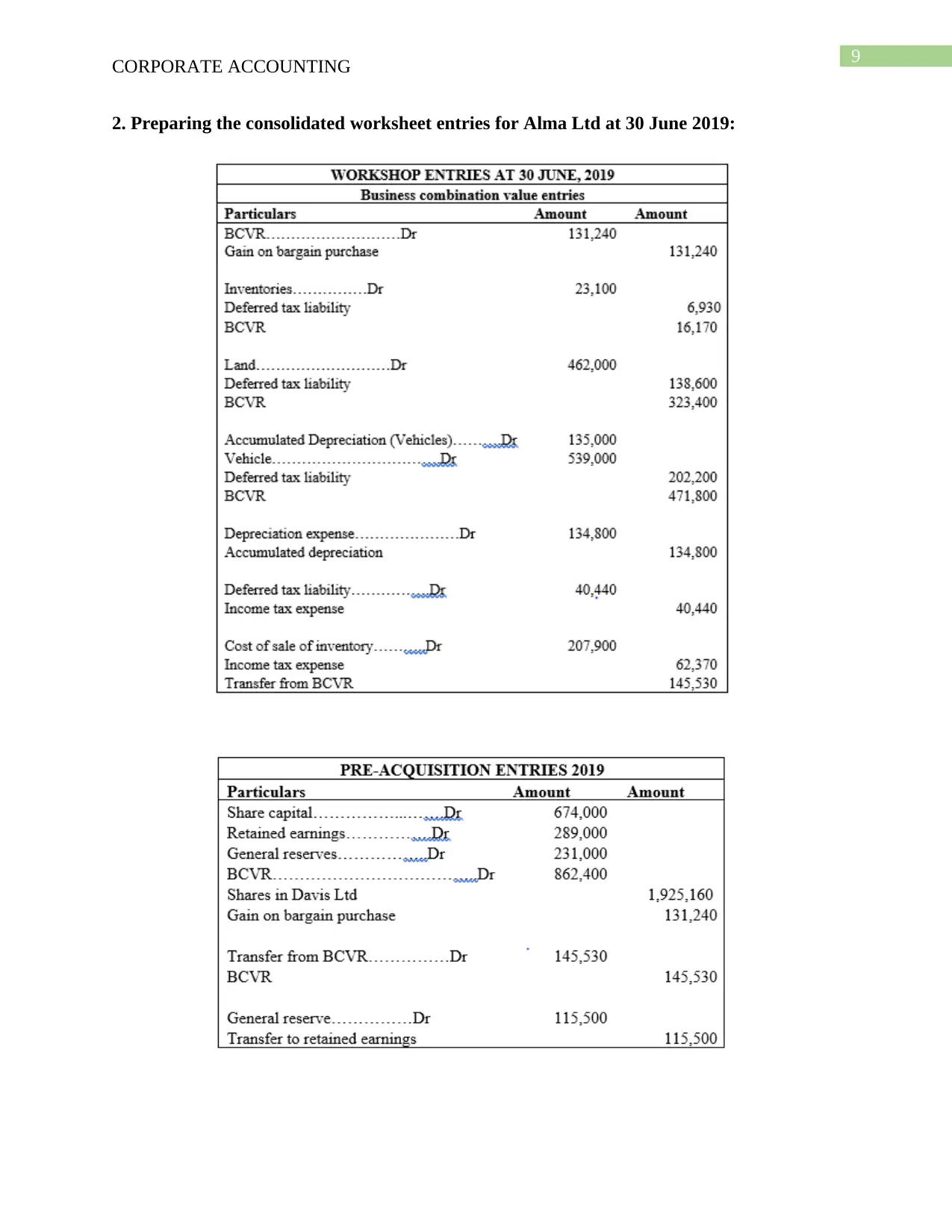

2. Preparing the consolidated worksheet entries for Alma Ltd at 30 June 2019:

CORPORATE ACCOUNTING

2. Preparing the consolidated worksheet entries for Alma Ltd at 30 June 2019:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

CORPORATE ACCOUNTING

11

CORPORATE ACCOUNTING

References:

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 28 Sep. 2019].

Christensen, T., Cottrell, D. and Baker, R., 2013. Advanced financial accounting. McGraw-Hill.

Loyeung, A., Matolcsy, Z., Weber, J. and Wells, P., 2016. The cost of implementing new

accounting standards: The case of IFRS adoption in Australia. Australian Journal of

Management, 41(4), pp.611-632.

Masadeh, W., Mansour, E. and AL Salamat, W., 2017. Changes in IFRS 3 accounting for

business combinations: a feedback and effects analysis. Global Journal of Business

Research, 11(1), pp.61-70.

Paugam, L., Astolfi, P. and Ramond, O., 2015. Accounting for business combinations: Do

purchase price allocations matter?. Journal of Accounting and Public Policy, 34(4), pp.362-391.

Sedláček, J., Křížová, Z. and Hýblová, E., 2013. Comparison of accounting methods for business

combinations. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 60(2),

pp.315-324.

Wen, H. and Moehrle, S.R., 2016. Accounting for goodwill: An academic literature review and

analysis to inform the debate. Research in Accounting Regulation, 28(1), pp.11-21.

CORPORATE ACCOUNTING

References:

AASB, C.A.S., 2014. Business Combinations. Disclosure, 66, p.77.

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 28 Sep. 2019].

Christensen, T., Cottrell, D. and Baker, R., 2013. Advanced financial accounting. McGraw-Hill.

Loyeung, A., Matolcsy, Z., Weber, J. and Wells, P., 2016. The cost of implementing new

accounting standards: The case of IFRS adoption in Australia. Australian Journal of

Management, 41(4), pp.611-632.

Masadeh, W., Mansour, E. and AL Salamat, W., 2017. Changes in IFRS 3 accounting for

business combinations: a feedback and effects analysis. Global Journal of Business

Research, 11(1), pp.61-70.

Paugam, L., Astolfi, P. and Ramond, O., 2015. Accounting for business combinations: Do

purchase price allocations matter?. Journal of Accounting and Public Policy, 34(4), pp.362-391.

Sedláček, J., Křížová, Z. and Hýblová, E., 2013. Comparison of accounting methods for business

combinations. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 60(2),

pp.315-324.

Wen, H. and Moehrle, S.R., 2016. Accounting for goodwill: An academic literature review and

analysis to inform the debate. Research in Accounting Regulation, 28(1), pp.11-21.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.