Corporate Accounting Assignment (ACT305): Financial Reporting Analysis

VerifiedAdded on 2023/06/05

|9

|1859

|147

Homework Assignment

AI Summary

This corporate accounting assignment solution addresses several key areas of financial accounting. It begins with journal entries and consolidation worksheet entries related to an investment in Fry Ltd. The solution then delves into a liquidation analysis of Rock Bottom Pty Ltd, outlining asset realization, creditor payments, and proportions. Next, the assignment analyzes the acquisition of Seven Ltd by Blake Ltd, including goodwill calculations and consolidation journal entries. Finally, it explores the application of AASB 10, discussing the consolidation of investments in Struggle Ltd, Very Big Company Ltd, and Medium Sized Company Ltd, as well as the control and consolidation of CrocsRUs, providing a comprehensive overview of financial reporting and investment accounting principles.

Unit Code: ACT305

Unit Name: Corporate Accounting

Name of the Student

Name of the University

Unit Name: Corporate Accounting

Name of the Student

Name of the University

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Answer to question 1:.................................................................................................................3

Part [a] Journal entries related to investment in Fry ltd.........................................................3

Part [b] Consolidation worksheet entries...............................................................................3

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................7

Introduction............................................................................................................................7

Discussion..............................................................................................................................7

Conclusion..............................................................................................................................8

Reference:..................................................................................................................................9

Answer to question 1:.................................................................................................................3

Part [a] Journal entries related to investment in Fry ltd.........................................................3

Part [b] Consolidation worksheet entries...............................................................................3

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................7

Introduction............................................................................................................................7

Discussion..............................................................................................................................7

Conclusion..............................................................................................................................8

Reference:..................................................................................................................................9

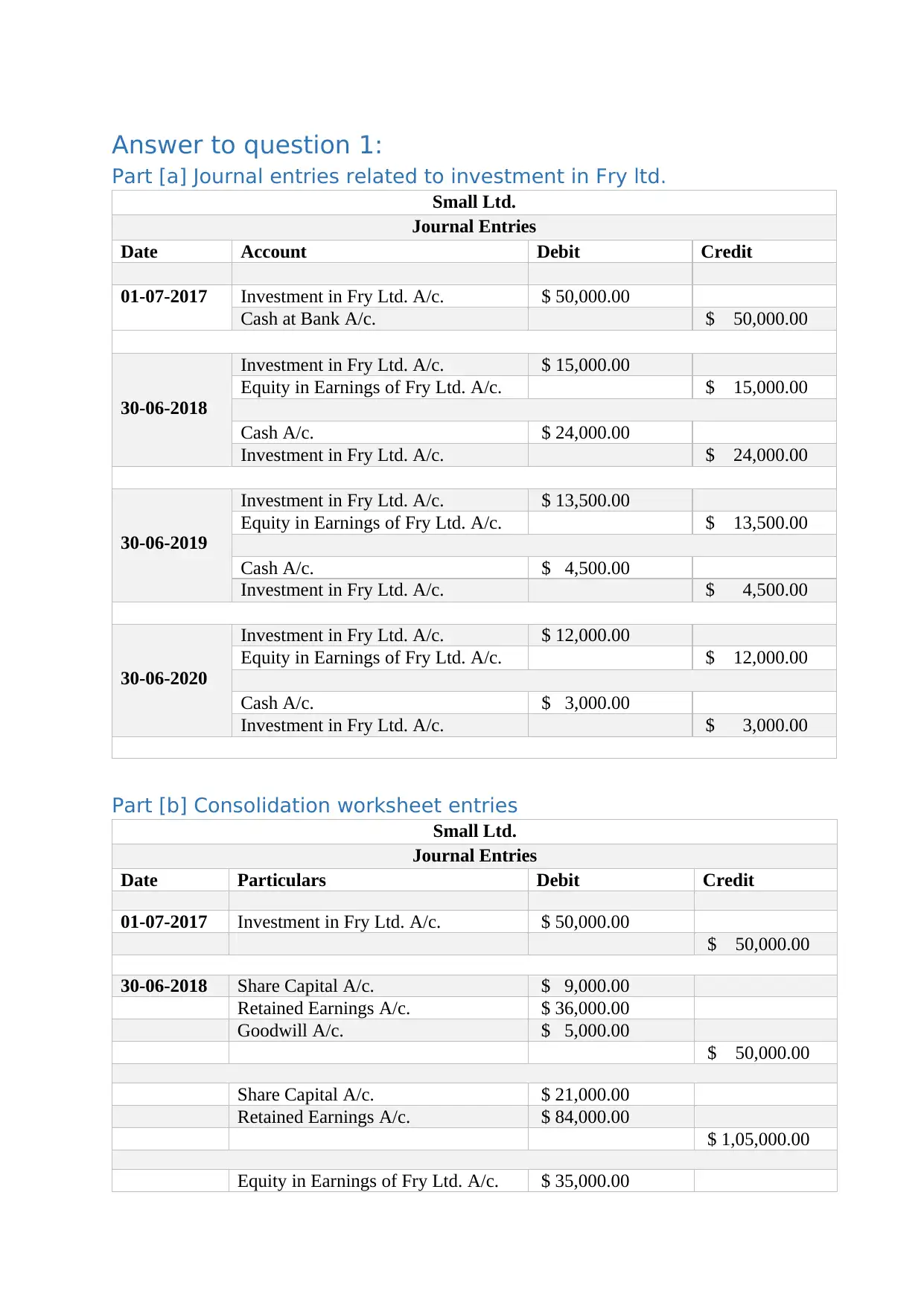

Answer to question 1:

Part [a] Journal entries related to investment in Fry ltd.

Small Ltd.

Journal Entries

Date Account Debit Credit

01-07-2017 Investment in Fry Ltd. A/c. $ 50,000.00

Cash at Bank A/c. $ 50,000.00

30-06-2018

Investment in Fry Ltd. A/c. $ 15,000.00

Equity in Earnings of Fry Ltd. A/c. $ 15,000.00

Cash A/c. $ 24,000.00

Investment in Fry Ltd. A/c. $ 24,000.00

30-06-2019

Investment in Fry Ltd. A/c. $ 13,500.00

Equity in Earnings of Fry Ltd. A/c. $ 13,500.00

Cash A/c. $ 4,500.00

Investment in Fry Ltd. A/c. $ 4,500.00

30-06-2020

Investment in Fry Ltd. A/c. $ 12,000.00

Equity in Earnings of Fry Ltd. A/c. $ 12,000.00

Cash A/c. $ 3,000.00

Investment in Fry Ltd. A/c. $ 3,000.00

Part [b] Consolidation worksheet entries

Small Ltd.

Journal Entries

Date Particulars Debit Credit

01-07-2017 Investment in Fry Ltd. A/c. $ 50,000.00

$ 50,000.00

30-06-2018 Share Capital A/c. $ 9,000.00

Retained Earnings A/c. $ 36,000.00

Goodwill A/c. $ 5,000.00

$ 50,000.00

Share Capital A/c. $ 21,000.00

Retained Earnings A/c. $ 84,000.00

$ 1,05,000.00

Equity in Earnings of Fry Ltd. A/c. $ 35,000.00

Part [a] Journal entries related to investment in Fry ltd.

Small Ltd.

Journal Entries

Date Account Debit Credit

01-07-2017 Investment in Fry Ltd. A/c. $ 50,000.00

Cash at Bank A/c. $ 50,000.00

30-06-2018

Investment in Fry Ltd. A/c. $ 15,000.00

Equity in Earnings of Fry Ltd. A/c. $ 15,000.00

Cash A/c. $ 24,000.00

Investment in Fry Ltd. A/c. $ 24,000.00

30-06-2019

Investment in Fry Ltd. A/c. $ 13,500.00

Equity in Earnings of Fry Ltd. A/c. $ 13,500.00

Cash A/c. $ 4,500.00

Investment in Fry Ltd. A/c. $ 4,500.00

30-06-2020

Investment in Fry Ltd. A/c. $ 12,000.00

Equity in Earnings of Fry Ltd. A/c. $ 12,000.00

Cash A/c. $ 3,000.00

Investment in Fry Ltd. A/c. $ 3,000.00

Part [b] Consolidation worksheet entries

Small Ltd.

Journal Entries

Date Particulars Debit Credit

01-07-2017 Investment in Fry Ltd. A/c. $ 50,000.00

$ 50,000.00

30-06-2018 Share Capital A/c. $ 9,000.00

Retained Earnings A/c. $ 36,000.00

Goodwill A/c. $ 5,000.00

$ 50,000.00

Share Capital A/c. $ 21,000.00

Retained Earnings A/c. $ 84,000.00

$ 1,05,000.00

Equity in Earnings of Fry Ltd. A/c. $ 35,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

$ 35,000.00

Dividend Revenue A/c. $ 24,000.00

Non-Controlling Interest A/c. $ 56,000.00

$ 80,000.00

30-06-2019 Equity in Earnings of Fry Ltd. A/c. $ 31,500.00

$ 31,500.00

Dividend Revenue A/c. $ 4,500.00

Non-Controlling Interest A/c. $ 10,500.00

$ 15,000.00

30-06-2020 Equity in Earnings of Fry Ltd. A/c. $ 28,000.00

$ 28,000.00

Dividend Revenue A/c. $ 3,000.00

Non-Controlling Interest A/c. $ 7,000.00

$ 10,000.00

Answer to question 2:

Creditors Ranking

Schedule 1 Receiver's Cost when realising secured assets

Schedule 2 Liquidator's Expenses

Schedule 3 Secured Creditors

Schedule 4 Staff Wages Payable

Schedule 5 Staff Leave Entitlements

Schedule 6 Unsecured Bank Overdraft

Schedule 7 Tax Payable

Schedule 8 Local Government Rates

Schedule 9 Unsecured Trade Payables

Schedule 10 Executive Directors' Wages Payable

Schedule 11 Executive Directors' Leave Entitlements

Schedule 12 Dividend Payable

Liquidation Rock Bottom Pty Ltd:

Total Realised Assets = Secured land and buildings + other assets

= $75,00,000.00 + $67,50,000.00 = $1,42,50,000.00

The creditors totalled = $1,63,50,000.00

Therefore, Proportion of creditor would be paid = Total Realised Assets / The creditors

totalled

= $1,42,50,000.00 / $1,63,50,000.00

Dividend Revenue A/c. $ 24,000.00

Non-Controlling Interest A/c. $ 56,000.00

$ 80,000.00

30-06-2019 Equity in Earnings of Fry Ltd. A/c. $ 31,500.00

$ 31,500.00

Dividend Revenue A/c. $ 4,500.00

Non-Controlling Interest A/c. $ 10,500.00

$ 15,000.00

30-06-2020 Equity in Earnings of Fry Ltd. A/c. $ 28,000.00

$ 28,000.00

Dividend Revenue A/c. $ 3,000.00

Non-Controlling Interest A/c. $ 7,000.00

$ 10,000.00

Answer to question 2:

Creditors Ranking

Schedule 1 Receiver's Cost when realising secured assets

Schedule 2 Liquidator's Expenses

Schedule 3 Secured Creditors

Schedule 4 Staff Wages Payable

Schedule 5 Staff Leave Entitlements

Schedule 6 Unsecured Bank Overdraft

Schedule 7 Tax Payable

Schedule 8 Local Government Rates

Schedule 9 Unsecured Trade Payables

Schedule 10 Executive Directors' Wages Payable

Schedule 11 Executive Directors' Leave Entitlements

Schedule 12 Dividend Payable

Liquidation Rock Bottom Pty Ltd:

Total Realised Assets = Secured land and buildings + other assets

= $75,00,000.00 + $67,50,000.00 = $1,42,50,000.00

The creditors totalled = $1,63,50,000.00

Therefore, Proportion of creditor would be paid = Total Realised Assets / The creditors

totalled

= $1,42,50,000.00 / $1,63,50,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

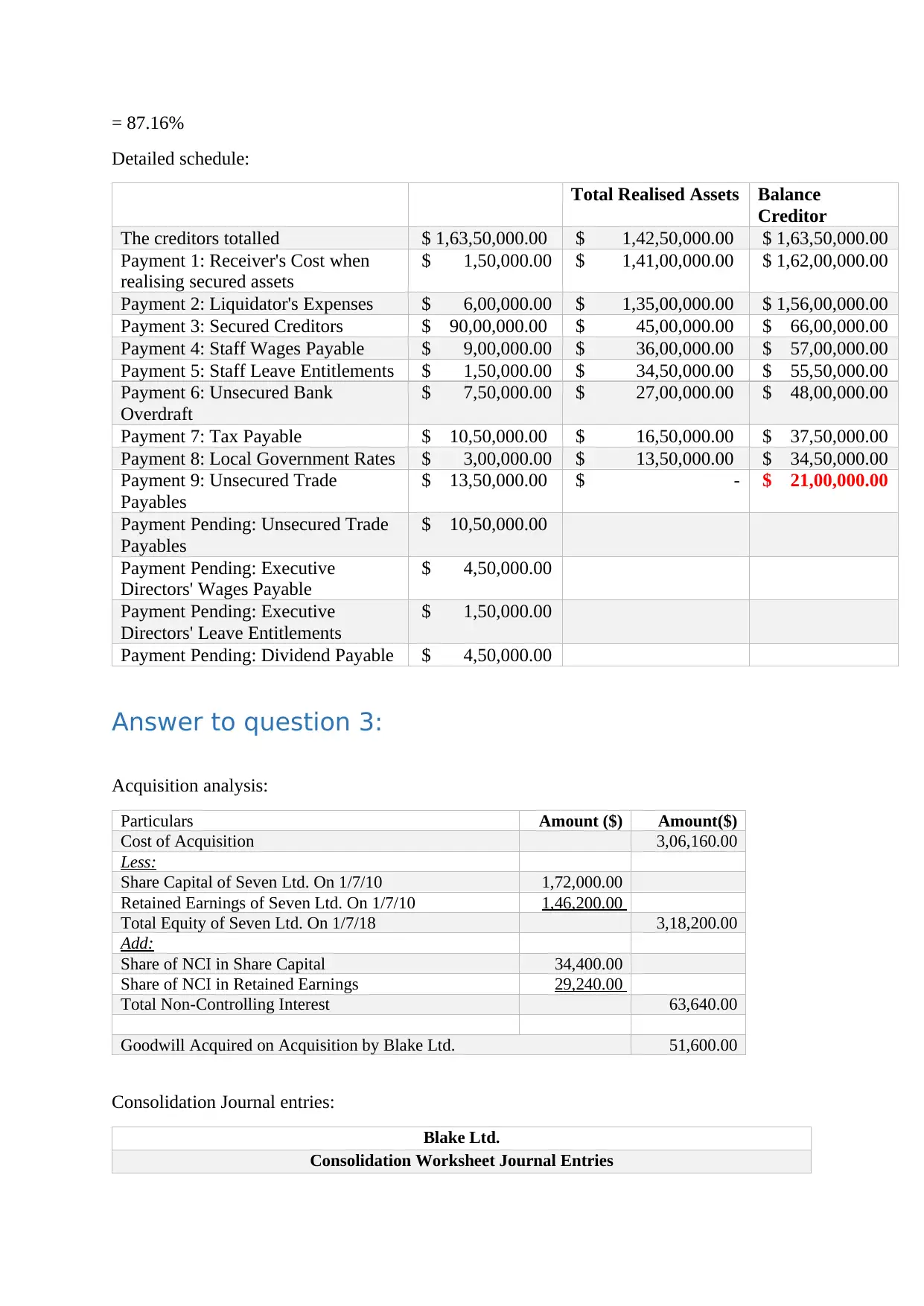

= 87.16%

Detailed schedule:

Total Realised Assets Balance

Creditor

The creditors totalled $ 1,63,50,000.00 $ 1,42,50,000.00 $ 1,63,50,000.00

Payment 1: Receiver's Cost when

realising secured assets

$ 1,50,000.00 $ 1,41,00,000.00 $ 1,62,00,000.00

Payment 2: Liquidator's Expenses $ 6,00,000.00 $ 1,35,00,000.00 $ 1,56,00,000.00

Payment 3: Secured Creditors $ 90,00,000.00 $ 45,00,000.00 $ 66,00,000.00

Payment 4: Staff Wages Payable $ 9,00,000.00 $ 36,00,000.00 $ 57,00,000.00

Payment 5: Staff Leave Entitlements $ 1,50,000.00 $ 34,50,000.00 $ 55,50,000.00

Payment 6: Unsecured Bank

Overdraft

$ 7,50,000.00 $ 27,00,000.00 $ 48,00,000.00

Payment 7: Tax Payable $ 10,50,000.00 $ 16,50,000.00 $ 37,50,000.00

Payment 8: Local Government Rates $ 3,00,000.00 $ 13,50,000.00 $ 34,50,000.00

Payment 9: Unsecured Trade

Payables

$ 13,50,000.00 $ - $ 21,00,000.00

Payment Pending: Unsecured Trade

Payables

$ 10,50,000.00

Payment Pending: Executive

Directors' Wages Payable

$ 4,50,000.00

Payment Pending: Executive

Directors' Leave Entitlements

$ 1,50,000.00

Payment Pending: Dividend Payable $ 4,50,000.00

Answer to question 3:

Acquisition analysis:

Particulars Amount ($) Amount($)

Cost of Acquisition 3,06,160.00

Less:

Share Capital of Seven Ltd. On 1/7/10 1,72,000.00

Retained Earnings of Seven Ltd. On 1/7/10 1,46,200.00

Total Equity of Seven Ltd. On 1/7/18 3,18,200.00

Add:

Share of NCI in Share Capital 34,400.00

Share of NCI in Retained Earnings 29,240.00

Total Non-Controlling Interest 63,640.00

Goodwill Acquired on Acquisition by Blake Ltd. 51,600.00

Consolidation Journal entries:

Blake Ltd.

Consolidation Worksheet Journal Entries

Detailed schedule:

Total Realised Assets Balance

Creditor

The creditors totalled $ 1,63,50,000.00 $ 1,42,50,000.00 $ 1,63,50,000.00

Payment 1: Receiver's Cost when

realising secured assets

$ 1,50,000.00 $ 1,41,00,000.00 $ 1,62,00,000.00

Payment 2: Liquidator's Expenses $ 6,00,000.00 $ 1,35,00,000.00 $ 1,56,00,000.00

Payment 3: Secured Creditors $ 90,00,000.00 $ 45,00,000.00 $ 66,00,000.00

Payment 4: Staff Wages Payable $ 9,00,000.00 $ 36,00,000.00 $ 57,00,000.00

Payment 5: Staff Leave Entitlements $ 1,50,000.00 $ 34,50,000.00 $ 55,50,000.00

Payment 6: Unsecured Bank

Overdraft

$ 7,50,000.00 $ 27,00,000.00 $ 48,00,000.00

Payment 7: Tax Payable $ 10,50,000.00 $ 16,50,000.00 $ 37,50,000.00

Payment 8: Local Government Rates $ 3,00,000.00 $ 13,50,000.00 $ 34,50,000.00

Payment 9: Unsecured Trade

Payables

$ 13,50,000.00 $ - $ 21,00,000.00

Payment Pending: Unsecured Trade

Payables

$ 10,50,000.00

Payment Pending: Executive

Directors' Wages Payable

$ 4,50,000.00

Payment Pending: Executive

Directors' Leave Entitlements

$ 1,50,000.00

Payment Pending: Dividend Payable $ 4,50,000.00

Answer to question 3:

Acquisition analysis:

Particulars Amount ($) Amount($)

Cost of Acquisition 3,06,160.00

Less:

Share Capital of Seven Ltd. On 1/7/10 1,72,000.00

Retained Earnings of Seven Ltd. On 1/7/10 1,46,200.00

Total Equity of Seven Ltd. On 1/7/18 3,18,200.00

Add:

Share of NCI in Share Capital 34,400.00

Share of NCI in Retained Earnings 29,240.00

Total Non-Controlling Interest 63,640.00

Goodwill Acquired on Acquisition by Blake Ltd. 51,600.00

Consolidation Journal entries:

Blake Ltd.

Consolidation Worksheet Journal Entries

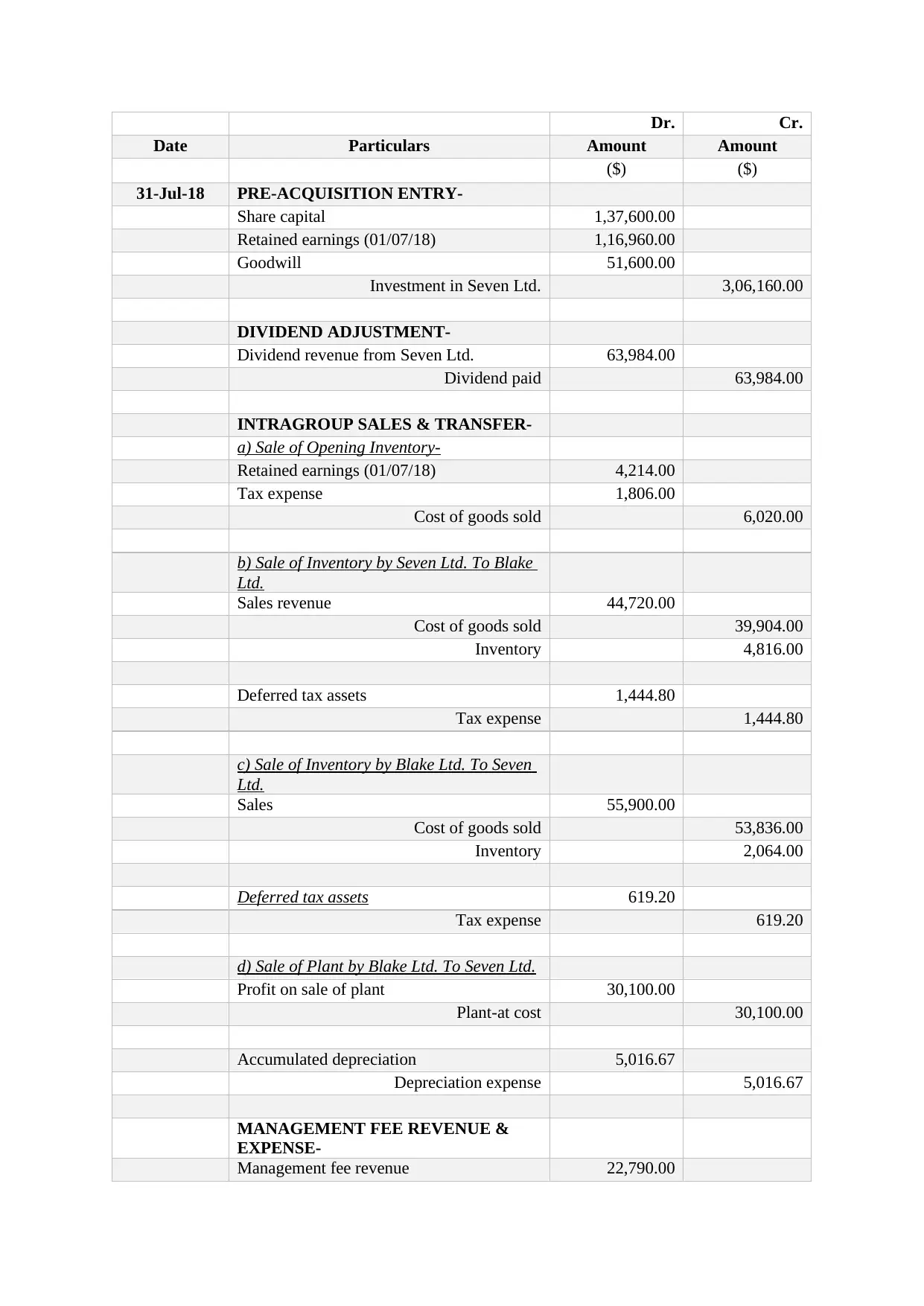

Dr. Cr.

Date Particulars Amount Amount

($) ($)

31-Jul-18 PRE-ACQUISITION ENTRY-

Share capital 1,37,600.00

Retained earnings (01/07/18) 1,16,960.00

Goodwill 51,600.00

Investment in Seven Ltd. 3,06,160.00

DIVIDEND ADJUSTMENT-

Dividend revenue from Seven Ltd. 63,984.00

Dividend paid 63,984.00

INTRAGROUP SALES & TRANSFER-

a) Sale of Opening Inventory-

Retained earnings (01/07/18) 4,214.00

Tax expense 1,806.00

Cost of goods sold 6,020.00

b) Sale of Inventory by Seven Ltd. To Blake

Ltd.

Sales revenue 44,720.00

Cost of goods sold 39,904.00

Inventory 4,816.00

Deferred tax assets 1,444.80

Tax expense 1,444.80

c) Sale of Inventory by Blake Ltd. To Seven

Ltd.

Sales 55,900.00

Cost of goods sold 53,836.00

Inventory 2,064.00

Deferred tax assets 619.20

Tax expense 619.20

d) Sale of Plant by Blake Ltd. To Seven Ltd.

Profit on sale of plant 30,100.00

Plant-at cost 30,100.00

Accumulated depreciation 5,016.67

Depreciation expense 5,016.67

MANAGEMENT FEE REVENUE &

EXPENSE-

Management fee revenue 22,790.00

Date Particulars Amount Amount

($) ($)

31-Jul-18 PRE-ACQUISITION ENTRY-

Share capital 1,37,600.00

Retained earnings (01/07/18) 1,16,960.00

Goodwill 51,600.00

Investment in Seven Ltd. 3,06,160.00

DIVIDEND ADJUSTMENT-

Dividend revenue from Seven Ltd. 63,984.00

Dividend paid 63,984.00

INTRAGROUP SALES & TRANSFER-

a) Sale of Opening Inventory-

Retained earnings (01/07/18) 4,214.00

Tax expense 1,806.00

Cost of goods sold 6,020.00

b) Sale of Inventory by Seven Ltd. To Blake

Ltd.

Sales revenue 44,720.00

Cost of goods sold 39,904.00

Inventory 4,816.00

Deferred tax assets 1,444.80

Tax expense 1,444.80

c) Sale of Inventory by Blake Ltd. To Seven

Ltd.

Sales 55,900.00

Cost of goods sold 53,836.00

Inventory 2,064.00

Deferred tax assets 619.20

Tax expense 619.20

d) Sale of Plant by Blake Ltd. To Seven Ltd.

Profit on sale of plant 30,100.00

Plant-at cost 30,100.00

Accumulated depreciation 5,016.67

Depreciation expense 5,016.67

MANAGEMENT FEE REVENUE &

EXPENSE-

Management fee revenue 22,790.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management fee expense 22,790.00

IMPAIRMENT OF GOODWILL-

Loss on goodwill impairment 2,580.00

Accumulated loss on impairment-Goodwill 2,580.00

NON-CONTROLLING INTEREST-

a) NCI on Acquisition

Share capital 6,880.00

Retained earnings (01/07/18) 5,848.00

Non-controlling interest 12,728.00

a) Sale of Opening Inventory-

Non-Controlling Interest Share of Profit 842.80

Retained earnings (01/07/18) 842.80

b) Sale of Inventory by Seven Ltd. To Blake

Ltd.

Non-Controlling Interest 674.24

Non-Controlling Interest Share of Profit 674.24

c) Dividend Adjustment

Non-controlling interest 15,996.00

Dividend paid 15,996.00

Answer to question 4:

Introduction

The primary reason for this report is to investigate the arrangements of AASB 10 which is on

combined monetary proclamations of the given business situation. The appraisal means to

instruct the finance director of Northern Australia Global Investments Ltd (NAGIL) to deal

with investment decision (Aasb.gov.au. 2018). The different investment options are assessed

throughout this report based on the arrangements of AASB 10.

Discussion

According to the case, NAGIL ltd had given a credit to Struggle Ltd (SL) which was later on

changed over to value finance at the last was not able pay the equivalent. This gave the

organization a 70% holding in the matter of Struggle ltd. According to the arrangements of

Para 5 of AASB 10, financial specialist will decide if the equivalent is parent organization

based on control which the business have over the investee. According to Para 7, command

over a business is set up when every one of the conditions are met which are control over the

investee, introduction or rights to variable comes back from the contribution in the business,

the ability to influence the profits which are made by the investee (Aasb.gov.au. 2018). The

case demonstrates that NAGIL ltd isn't effectively associated with the everyday business of

the organization and furthermore not in choices of the business and in this way the

IMPAIRMENT OF GOODWILL-

Loss on goodwill impairment 2,580.00

Accumulated loss on impairment-Goodwill 2,580.00

NON-CONTROLLING INTEREST-

a) NCI on Acquisition

Share capital 6,880.00

Retained earnings (01/07/18) 5,848.00

Non-controlling interest 12,728.00

a) Sale of Opening Inventory-

Non-Controlling Interest Share of Profit 842.80

Retained earnings (01/07/18) 842.80

b) Sale of Inventory by Seven Ltd. To Blake

Ltd.

Non-Controlling Interest 674.24

Non-Controlling Interest Share of Profit 674.24

c) Dividend Adjustment

Non-controlling interest 15,996.00

Dividend paid 15,996.00

Answer to question 4:

Introduction

The primary reason for this report is to investigate the arrangements of AASB 10 which is on

combined monetary proclamations of the given business situation. The appraisal means to

instruct the finance director of Northern Australia Global Investments Ltd (NAGIL) to deal

with investment decision (Aasb.gov.au. 2018). The different investment options are assessed

throughout this report based on the arrangements of AASB 10.

Discussion

According to the case, NAGIL ltd had given a credit to Struggle Ltd (SL) which was later on

changed over to value finance at the last was not able pay the equivalent. This gave the

organization a 70% holding in the matter of Struggle ltd. According to the arrangements of

Para 5 of AASB 10, financial specialist will decide if the equivalent is parent organization

based on control which the business have over the investee. According to Para 7, command

over a business is set up when every one of the conditions are met which are control over the

investee, introduction or rights to variable comes back from the contribution in the business,

the ability to influence the profits which are made by the investee (Aasb.gov.au. 2018). The

case demonstrates that NAGIL ltd isn't effectively associated with the everyday business of

the organization and furthermore not in choices of the business and in this way the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

administration of the organization ought not include such interests in the combination of the

business.

According to the case which is gives, NAGIL has given credit to Very Big Company ltd

(VBCL) amid the period. The administration of NAGIL has not made an interest in the offers

of the organization of VBCL however has given a credit and VBCL has not possessed the

capacity to meet the installment necessities of the advance and along these lines a bailout

bundle is started according to the organization can't be make any installments except if the

equivalent is endorsed by NAGIL. This isn't an interest in the value offers of the business and

along these lines the equivalent can't be shrouded in AASB 10 as NAGIL can't be considered

as a parent organization of VBCL. Hence, the administration of NAGIL ought to think about

the equivalent as credit for the business.

The case which is given identifies with the organization of Medium Sized Company Ltd

(MSCL) which is a backup of both NAGIL and Sharp Players Ltd (SPL). Both the

organizations hold meet offer of proprietorship in the business and furthermore gives fund on

equivalent premise to the organization. According to the arrangements which is expressed in

ASSB 10, Para 9 expresses that on the off chance that an investee is controlled by two

financial specialists together than the equivalent can't be held to be controlled by any one

business and in this way both the organizations needs to represent the premium which it has

in the investee (Aasb.gov.au. 2018). On account of MSCL, the administration NAGIL needs

to just think about the enthusiasm on credits and the administration charges which is to be

paid on the off chance that the organization can produce benefits for the period. If there

should arise an occurrence of misfortunes, the administration of MSCL just needs to acquire

intrigue costs and not the administration charges to the business.

The case which is given in the appraisal demonstrates that the administration of NAGIL ltd

holds around 40% of possessions in the matter of CrocsRUs and the other 60% is held by the

proprietors. The case gives that the administration of the organization is dealt with by NAGIL

and furthermore all real choices are taken by them also. According to the arrangements of

ASSB 10, Para 7 gives that so as to a business to be responsible for the investee, the business

ought to have a control over the investee, ought to have variable rights on returns of the

business which is for dynamic exasperate in the business. Furthermore, the capacity to utilize

the control over the investee keeping in mind the end goal to influence the profits of the

business. Every one of the three conditions need to fulfill for the business to have control. On

account of CrocsRUs, the administration of NAGIL have the power over the business and

furthermore takes the significant choices and consequently they have to combine the interests

in a critical position sheet.

Conclusion

The above discourse demonstrates the different speculations and advances which are given to

various organizations amid the period. The evaluation demonstrates the utilization of the

arrangements of AASB 10 with a specific end goal to decide if the back executive should

fuse the exchange in the merged money related proclamation of the business. The evaluation

viably manages the revealing necessity of ventures made in different organizations.

business.

According to the case which is gives, NAGIL has given credit to Very Big Company ltd

(VBCL) amid the period. The administration of NAGIL has not made an interest in the offers

of the organization of VBCL however has given a credit and VBCL has not possessed the

capacity to meet the installment necessities of the advance and along these lines a bailout

bundle is started according to the organization can't be make any installments except if the

equivalent is endorsed by NAGIL. This isn't an interest in the value offers of the business and

along these lines the equivalent can't be shrouded in AASB 10 as NAGIL can't be considered

as a parent organization of VBCL. Hence, the administration of NAGIL ought to think about

the equivalent as credit for the business.

The case which is given identifies with the organization of Medium Sized Company Ltd

(MSCL) which is a backup of both NAGIL and Sharp Players Ltd (SPL). Both the

organizations hold meet offer of proprietorship in the business and furthermore gives fund on

equivalent premise to the organization. According to the arrangements which is expressed in

ASSB 10, Para 9 expresses that on the off chance that an investee is controlled by two

financial specialists together than the equivalent can't be held to be controlled by any one

business and in this way both the organizations needs to represent the premium which it has

in the investee (Aasb.gov.au. 2018). On account of MSCL, the administration NAGIL needs

to just think about the enthusiasm on credits and the administration charges which is to be

paid on the off chance that the organization can produce benefits for the period. If there

should arise an occurrence of misfortunes, the administration of MSCL just needs to acquire

intrigue costs and not the administration charges to the business.

The case which is given in the appraisal demonstrates that the administration of NAGIL ltd

holds around 40% of possessions in the matter of CrocsRUs and the other 60% is held by the

proprietors. The case gives that the administration of the organization is dealt with by NAGIL

and furthermore all real choices are taken by them also. According to the arrangements of

ASSB 10, Para 7 gives that so as to a business to be responsible for the investee, the business

ought to have a control over the investee, ought to have variable rights on returns of the

business which is for dynamic exasperate in the business. Furthermore, the capacity to utilize

the control over the investee keeping in mind the end goal to influence the profits of the

business. Every one of the three conditions need to fulfill for the business to have control. On

account of CrocsRUs, the administration of NAGIL have the power over the business and

furthermore takes the significant choices and consequently they have to combine the interests

in a critical position sheet.

Conclusion

The above discourse demonstrates the different speculations and advances which are given to

various organizations amid the period. The evaluation demonstrates the utilization of the

arrangements of AASB 10 with a specific end goal to decide if the back executive should

fuse the exchange in the merged money related proclamation of the business. The evaluation

viably manages the revealing necessity of ventures made in different organizations.

Reference:

Aasb.gov.au. 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 4th Oct.

2018].

Aasb.gov.au. 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 4th Oct.

2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.