HI5020: Corporate Accounting Analysis of AGL and Beach Energy Limited

VerifiedAdded on 2023/06/04

|20

|3634

|222

Report

AI Summary

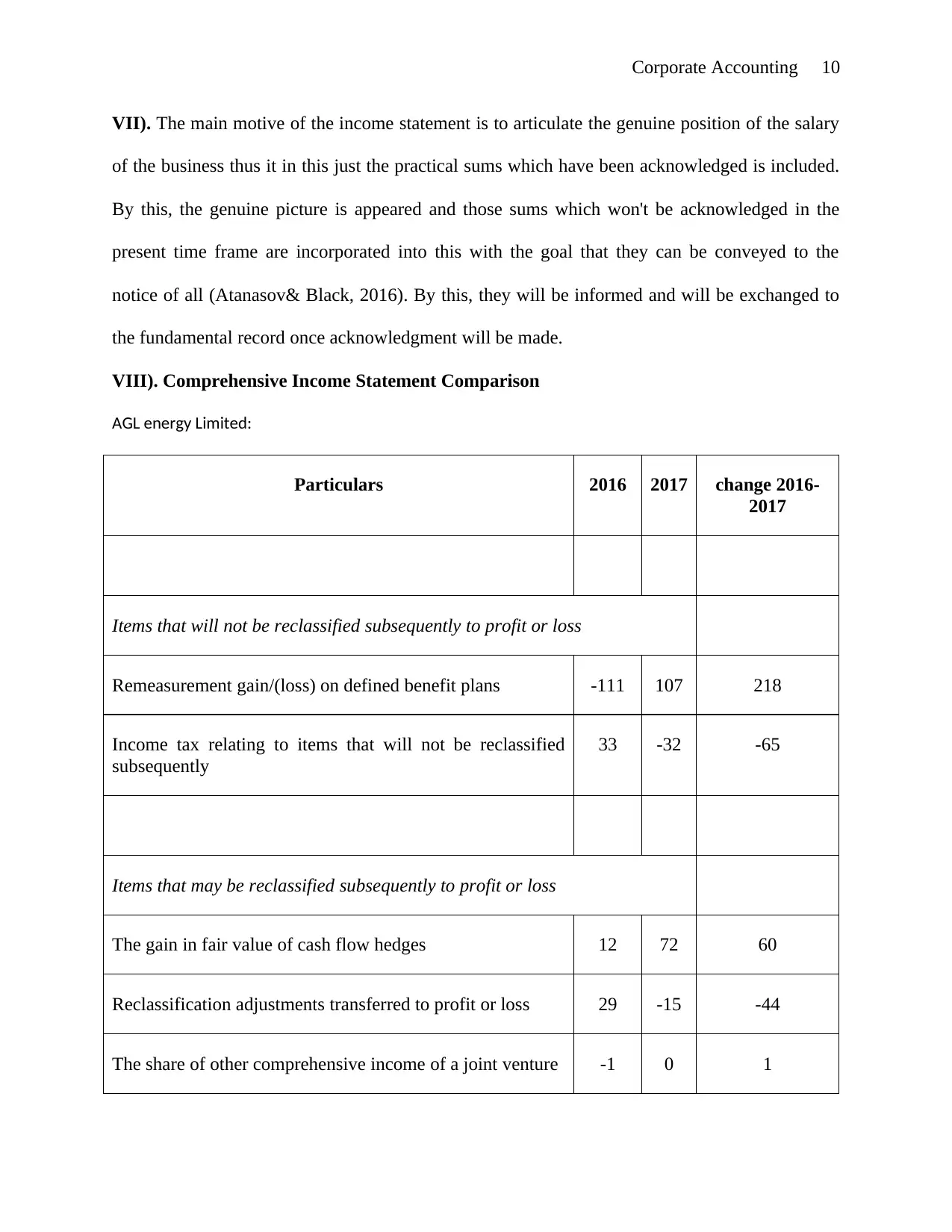

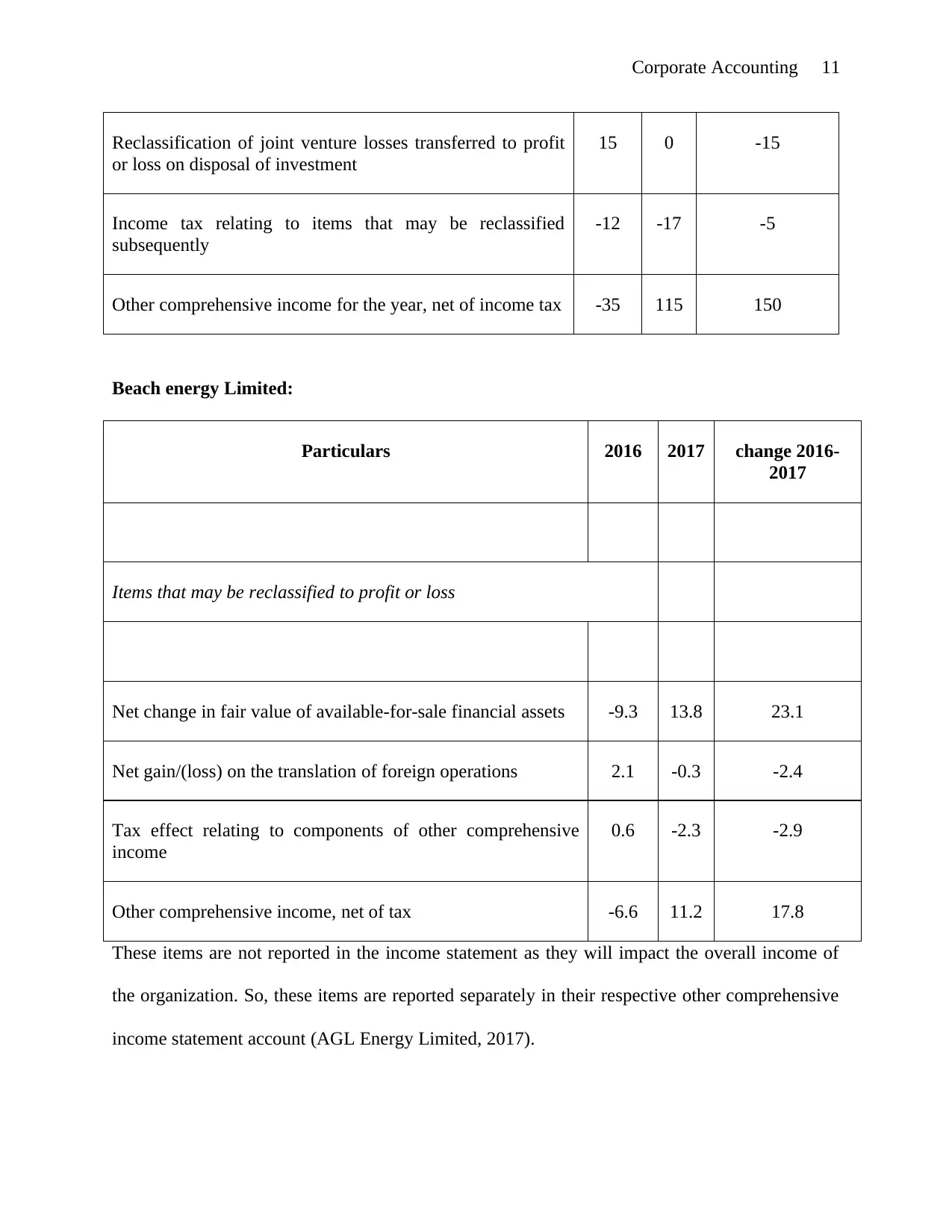

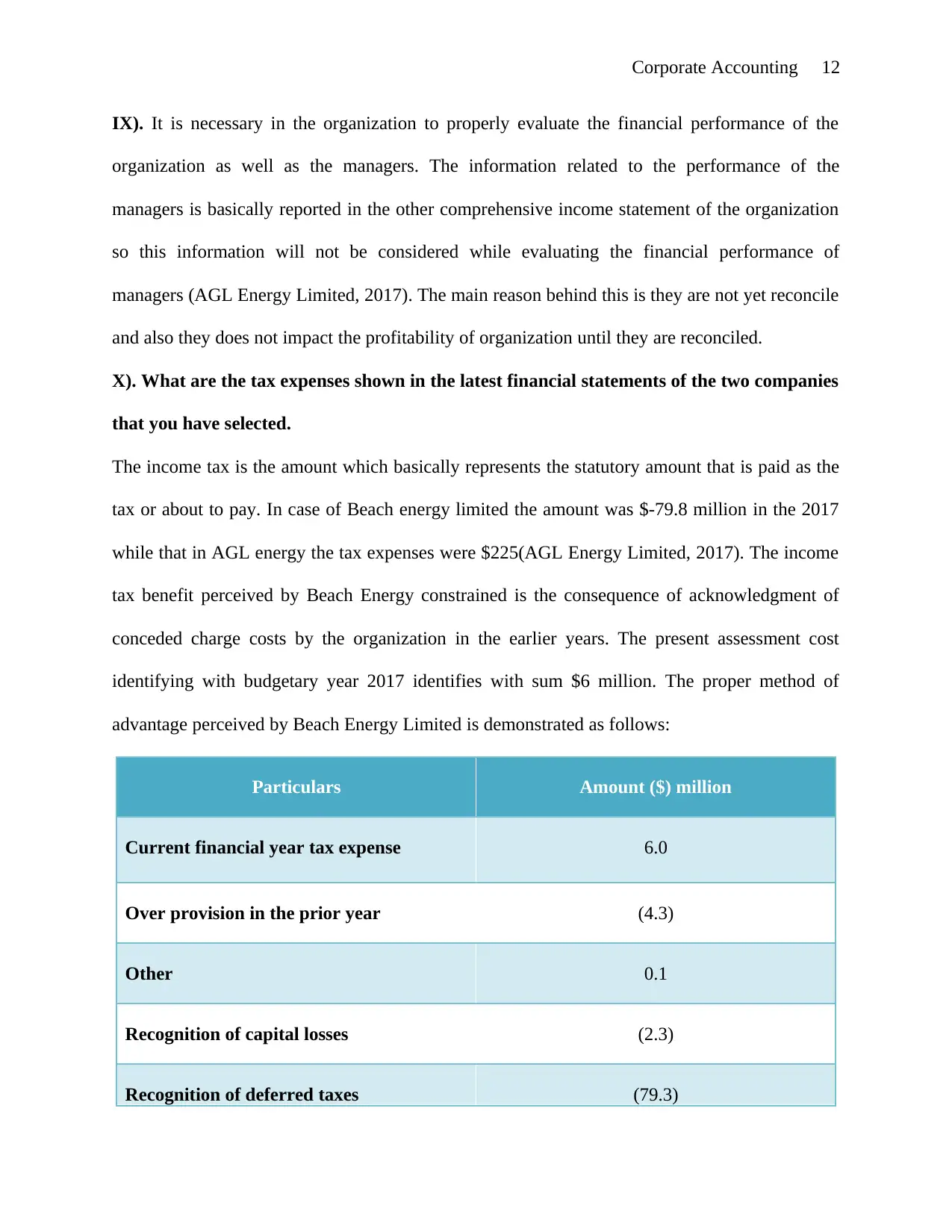

This report provides a comprehensive analysis of the corporate accounting practices of AGL Energy Limited and Beach Energy Limited, both listed on the Australian Securities Exchange (ASX). The analysis begins with an executive summary and an introduction that highlights the importance of accurate financial reporting for strategic decision-making. The report then delves into the owners' equity sections of the balance sheets for both companies, detailing contributed equity, reserves, retained earnings, and issued capital. A comparative analysis of the debt and equity financing strategies of both companies over a three-year period is also included. The cash flow statements of AGL Energy and Beach Energy are examined, focusing on operating, investing, and financing activities, with comparisons made across the three years. The report further explores the other comprehensive income statements, differentiating between items that may or may not be reclassified to profit or loss, and assesses the impact of these items on the overall financial performance of the companies. Finally, the report provides insights into the tax expenses reported in the latest financial statements of both companies, providing a well-rounded overview of their corporate accounting practices.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.