HI5020 Corporate Accounting: Ausdrill & Rio Tinto Financial Comparison

VerifiedAdded on 2023/06/08

|19

|4875

|228

Report

AI Summary

This report provides a comprehensive financial analysis of Ausdrill Ltd and Rio Tinto Ltd, two companies in the mining industry listed on the Australian Securities Exchange (ASX). The analysis covers a three-year period, focusing on key elements of their financial statements, including owner's equity, capital structure, cash flow statements, other comprehensive income, and income tax accounting. A comparative analysis is conducted to highlight the differences in financial reporting and performance between the two companies, particularly in areas such as debt and equity capital usage, cash flow management, and effective tax rates. The report also includes calculations and explanations of deferred tax assets and liabilities, as well as a comparison of cash tax rates and book tax rates for both companies.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive Summary

The main purpose of this assessment is to analyze the financial statements of two companies for

a period of three years. The companies which are selected for this assessment are Ausdrill ltd and

Rio Tinto Ltd. The assessment analyzes different elements which are disclosed in the annual

report such as Income tax expenses. The assessment analyzes in dept the cash flow statement of

both the companies in order to under the cash flows of the business during the year. The

assessment conducts a comparative analysis of the cash flow statement between Ausdrill ltd and

Rio Tinto Ltd. The assessment also contains calculations of Effective tax rate and Cash and Book

tax rates and also an explanation of the tax expenses and tax structure of both the companies.

CORPORATE ACCOUNTING

Executive Summary

The main purpose of this assessment is to analyze the financial statements of two companies for

a period of three years. The companies which are selected for this assessment are Ausdrill ltd and

Rio Tinto Ltd. The assessment analyzes different elements which are disclosed in the annual

report such as Income tax expenses. The assessment analyzes in dept the cash flow statement of

both the companies in order to under the cash flows of the business during the year. The

assessment conducts a comparative analysis of the cash flow statement between Ausdrill ltd and

Rio Tinto Ltd. The assessment also contains calculations of Effective tax rate and Cash and Book

tax rates and also an explanation of the tax expenses and tax structure of both the companies.

2

CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Owner’s Equity............................................................................................................................4

Capital Structure Position of Both the Companies......................................................................5

Cash Flow Statement Analysis....................................................................................................7

Comparative Analysis of Three Components of Cash Flow Statement....................................10

Insight of Cash flow Statement..................................................................................................11

Analysis of Other Comprehensive Income Statement...................................................................11

Reporting of Comprehensive Items...........................................................................................12

Comparative Analysis of Comprehensive Items.......................................................................12

Accounting for Income Tax.......................................................................................................13

Effective Tax Rate.....................................................................................................................13

Deferred Tax Assets and Liabilities..........................................................................................14

Cash Tax Amount and Rate of Both Company.........................................................................15

Difference Between Cash Tax Rate and Book Tax Rate...........................................................15

Reference.......................................................................................................................................16

CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Owner’s Equity............................................................................................................................4

Capital Structure Position of Both the Companies......................................................................5

Cash Flow Statement Analysis....................................................................................................7

Comparative Analysis of Three Components of Cash Flow Statement....................................10

Insight of Cash flow Statement..................................................................................................11

Analysis of Other Comprehensive Income Statement...................................................................11

Reporting of Comprehensive Items...........................................................................................12

Comparative Analysis of Comprehensive Items.......................................................................12

Accounting for Income Tax.......................................................................................................13

Effective Tax Rate.....................................................................................................................13

Deferred Tax Assets and Liabilities..........................................................................................14

Cash Tax Amount and Rate of Both Company.........................................................................15

Difference Between Cash Tax Rate and Book Tax Rate...........................................................15

Reference.......................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction

The main purpose of this assessment is to analyze the financial statements of two

companies which belong to the same industry and has similar level of operations. The two

companies which are selected for this assessment are Ausdrill Ltd and Rio Tinto Ltd which are

both engaged in engaged in mining and extraction of mineral resources business. The assessment

considers annual reports of both the company for the purpose of analyzing different elements of

the financial statements and also make a comparative analysis between the two companies as to

which has a better reporting of such elements of the annual reports.

Ausdrill Ltd is engaged in the business of extracting minerals and mining business in

Australia. The primary operations of the company are in Australia however, the business has also

expanded to certain areas of Africa and United Kingdom. The company specializes in mining

services, grade control, drill and blast exploration projects (Ausdrill.com.au. 2018). The

company also employ significant number of employees in the business and the revenues of the

business are constantly improving.

Rio Tinto Ltd is regarded as one of the leading businesses in Mining industry and has its

origin as an Anglo-Australian company which has a majority of its operations in Australia. The

company is known for its mining activities and is a leading producer for metals in Australia

(Riotinto.com. 2018). The company produces coal, iron ores, uranium, copper and diamonds. In

addition to this, the company is also engaged in the business of refining for products like bauxite

and some other minerals.

The main focus of the assessment will be to analyze the annual reports of both the

companies for a period of last three consecutive years starting from 2017. The assessment also

CORPORATE ACCOUNTING

Introduction

The main purpose of this assessment is to analyze the financial statements of two

companies which belong to the same industry and has similar level of operations. The two

companies which are selected for this assessment are Ausdrill Ltd and Rio Tinto Ltd which are

both engaged in engaged in mining and extraction of mineral resources business. The assessment

considers annual reports of both the company for the purpose of analyzing different elements of

the financial statements and also make a comparative analysis between the two companies as to

which has a better reporting of such elements of the annual reports.

Ausdrill Ltd is engaged in the business of extracting minerals and mining business in

Australia. The primary operations of the company are in Australia however, the business has also

expanded to certain areas of Africa and United Kingdom. The company specializes in mining

services, grade control, drill and blast exploration projects (Ausdrill.com.au. 2018). The

company also employ significant number of employees in the business and the revenues of the

business are constantly improving.

Rio Tinto Ltd is regarded as one of the leading businesses in Mining industry and has its

origin as an Anglo-Australian company which has a majority of its operations in Australia. The

company is known for its mining activities and is a leading producer for metals in Australia

(Riotinto.com. 2018). The company produces coal, iron ores, uranium, copper and diamonds. In

addition to this, the company is also engaged in the business of refining for products like bauxite

and some other minerals.

The main focus of the assessment will be to analyze the annual reports of both the

companies for a period of last three consecutive years starting from 2017. The assessment also

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

shows analysis and comparative analysis of the elements which are shown in the annual reports

of the business. Some of the significant areas which are considered in the annual reports of both

the companies are cash flow statements, equity capital used, tax treatments and disclosures. In

addition to this, the assessment will also be containing calculations regarding effective tax rate

and other tax computations.

Discussion

Owner’s Equity

The owner’s equity represents the equity capital and retain earnings of the business which

is used for financing the activities of the business. The annual report of 2017 is considered for

both the companies for the purpose of analyzing the owner’s equity of the business. As per the

annual report of 2017 for the Ausdrill Ltd, the owner’s equity is shown in the balance sheet. The

owner’s equity comprises of contributed equity, retained earnings and other reserves. The

contributed equity relates to the share capital which the company has accumulated by issues of

shares to the public. The contributed equity of the business for the year 2017 is shown to be $

546,447,000 which is same as the figure which was shown for previous year (Needles, Powers

and Crosson 2013). There have been no changes in the figure of equity as per previous year

estimates and also as per 2015 estimates. The retained earnings of the business reflect a part of

the profits which are kept aside either for reinvesting the same in the business or meeting certain

future obligations of the business. The retained earnings of the business for the year 2017 has

significantly increased in comparison to previous year analysis and the same is shown to be $

121,444,000. The estimate which is shown for 2015 is $ 38,027,000. Therefore, there is a general

trend which shows increase in the retained earnings of the business. This may be due to the

improvement in profitability of the business and also due to improvement in the operating

CORPORATE ACCOUNTING

shows analysis and comparative analysis of the elements which are shown in the annual reports

of the business. Some of the significant areas which are considered in the annual reports of both

the companies are cash flow statements, equity capital used, tax treatments and disclosures. In

addition to this, the assessment will also be containing calculations regarding effective tax rate

and other tax computations.

Discussion

Owner’s Equity

The owner’s equity represents the equity capital and retain earnings of the business which

is used for financing the activities of the business. The annual report of 2017 is considered for

both the companies for the purpose of analyzing the owner’s equity of the business. As per the

annual report of 2017 for the Ausdrill Ltd, the owner’s equity is shown in the balance sheet. The

owner’s equity comprises of contributed equity, retained earnings and other reserves. The

contributed equity relates to the share capital which the company has accumulated by issues of

shares to the public. The contributed equity of the business for the year 2017 is shown to be $

546,447,000 which is same as the figure which was shown for previous year (Needles, Powers

and Crosson 2013). There have been no changes in the figure of equity as per previous year

estimates and also as per 2015 estimates. The retained earnings of the business reflect a part of

the profits which are kept aside either for reinvesting the same in the business or meeting certain

future obligations of the business. The retained earnings of the business for the year 2017 has

significantly increased in comparison to previous year analysis and the same is shown to be $

121,444,000. The estimate which is shown for 2015 is $ 38,027,000. Therefore, there is a general

trend which shows increase in the retained earnings of the business. This may be due to the

improvement in profitability of the business and also due to improvement in the operating

5

CORPORATE ACCOUNTING

structure of the business. The reserves of the business are shown in negative which represents

accumulated losses of the business which are from previous year.

On the other hand, the components of owner’s equity which is shown in the annual report

of the business for 2017 is shown to be equity share capital of the business, share premium,

retained earnings and reserves. The equity share capital which is shown for the business for 2017

comprises of equity capital of Rio Tinto Plc and Rio Tinto Limited. The equity capital represents

the funds which are used by the business for the purpose of meeting the obligations of the

business. The reserves figure which is shown in the balance sheet of the business is shown to be

positive which represents that the business has accumulated parts of earnings which the

management of the company can use in any manner possible (Chambers 2014). The share capital

of the business is shown to be US$ 4,140 million which has significantly improved in

comparison to previous year. This is due to the fact that the company has issued certain number

of shares during the year in order to draw capital from the same (Warren, Reeve and Duchac

2013). The retained earnings of the business are shown to be US$ 23,761 million. The retained

earnings of the business have also increased which is due to increase in profit generating

capability of the business. The annual report further shows that the reserves of profits of the

business are appropriate for meeting any obligations of the business.

Capital Structure Position of Both the Companies

The capital structure of Ausdrill ltd as per the balance of the business for the year 2017 is

shown to be more relying on equity capital rather than debt capital of the business. The debt

capital is shown to be $ 385,815,000 for the year 2017 and the same was $ 395,019,000 in 2016

as shown in the balance sheet of the company for 2016 which shows that the management of

company repaid a part of the loan during the current year. In case of equity share capital, the

CORPORATE ACCOUNTING

structure of the business. The reserves of the business are shown in negative which represents

accumulated losses of the business which are from previous year.

On the other hand, the components of owner’s equity which is shown in the annual report

of the business for 2017 is shown to be equity share capital of the business, share premium,

retained earnings and reserves. The equity share capital which is shown for the business for 2017

comprises of equity capital of Rio Tinto Plc and Rio Tinto Limited. The equity capital represents

the funds which are used by the business for the purpose of meeting the obligations of the

business. The reserves figure which is shown in the balance sheet of the business is shown to be

positive which represents that the business has accumulated parts of earnings which the

management of the company can use in any manner possible (Chambers 2014). The share capital

of the business is shown to be US$ 4,140 million which has significantly improved in

comparison to previous year. This is due to the fact that the company has issued certain number

of shares during the year in order to draw capital from the same (Warren, Reeve and Duchac

2013). The retained earnings of the business are shown to be US$ 23,761 million. The retained

earnings of the business have also increased which is due to increase in profit generating

capability of the business. The annual report further shows that the reserves of profits of the

business are appropriate for meeting any obligations of the business.

Capital Structure Position of Both the Companies

The capital structure of Ausdrill ltd as per the balance of the business for the year 2017 is

shown to be more relying on equity capital rather than debt capital of the business. The debt

capital is shown to be $ 385,815,000 for the year 2017 and the same was $ 395,019,000 in 2016

as shown in the balance sheet of the company for 2016 which shows that the management of

company repaid a part of the loan during the current year. In case of equity share capital, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

business has increased equity capital of the business during the year as shown in the balance

sheet of the business. The borrowings of the business for the year 2015 is shown to be $

407,307,000 which is higher than 2016 estimate. The analysis for 3 years reveals that the

management is systematically reducing the debts of the business and thereby focusing on

application of more equity capital of the business.

In the case of Rio Tinto Ltd, the balance sheet of the company for the year 2017 shows

that the borrowings of the business are US$ 15,148 million which is lower than the estimate

which is shown for the year 2016 which is US$ 17,470 million. The borrowings of the business

for the year 2015 is shown to be US$ 21,140 million which is more than debt capital which is

shown for 2016. This shows that the management of the company is trying to reduce the debt

capital of the business on year by year basis (Ampenberger et al. 2013). The company has also

equity capital which is shown in the annual reports of the business during the year which is

shown to be US$ 4,140 million for 2017 and the same was US$ 3,950 million in 2015 which

shows that the management of the company is trying to increase the equity capital in the capital

structure of the business. The management of Rio Tinto Ltd is trying to increase the equity

capital of the business and is relying more on debt capital of the business.

Therefore, the analysis of the debt and equity capital which is used by both the

companies, it is revealed that the business of Ausdrill ltd is more reliant on using debt capital to

finance the activities of the business while on the other hand the management of Rio Tinto ltd is

relying more on equity capital as the business is trying to reduce the debt capital which is used

by the business. However, in current scenario, the management of Rio Tinto ltd is still using

much more debt capital than equity capital of the business.

CORPORATE ACCOUNTING

business has increased equity capital of the business during the year as shown in the balance

sheet of the business. The borrowings of the business for the year 2015 is shown to be $

407,307,000 which is higher than 2016 estimate. The analysis for 3 years reveals that the

management is systematically reducing the debts of the business and thereby focusing on

application of more equity capital of the business.

In the case of Rio Tinto Ltd, the balance sheet of the company for the year 2017 shows

that the borrowings of the business are US$ 15,148 million which is lower than the estimate

which is shown for the year 2016 which is US$ 17,470 million. The borrowings of the business

for the year 2015 is shown to be US$ 21,140 million which is more than debt capital which is

shown for 2016. This shows that the management of the company is trying to reduce the debt

capital of the business on year by year basis (Ampenberger et al. 2013). The company has also

equity capital which is shown in the annual reports of the business during the year which is

shown to be US$ 4,140 million for 2017 and the same was US$ 3,950 million in 2015 which

shows that the management of the company is trying to increase the equity capital in the capital

structure of the business. The management of Rio Tinto Ltd is trying to increase the equity

capital of the business and is relying more on debt capital of the business.

Therefore, the analysis of the debt and equity capital which is used by both the

companies, it is revealed that the business of Ausdrill ltd is more reliant on using debt capital to

finance the activities of the business while on the other hand the management of Rio Tinto ltd is

relying more on equity capital as the business is trying to reduce the debt capital which is used

by the business. However, in current scenario, the management of Rio Tinto ltd is still using

much more debt capital than equity capital of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

Cash Flow Statement Analysis

The cash flow statement represents the cash position of the business and demonstrates

each activity which is either a cash inflow and cash outflow for the business. The cash flow

statement of Ausdrill ltd shows cash from operating activities which mainly comprises of cash

receipts which the business receives from operating activities of the business and also cash

payments which are made by the business to suppliers (Nurnberg 2015). Another significant item

which is included ion the cash flow statement is income tax paid by the business during the year.

The net cash flow for the year 2017 is shown to be $ 94,613,000 which has increased from 2016

estimates which is shown to be $ 91,006,000. The receipts from customers and also the payments

which are made to the suppliers of the business have increased on the basis of estimates of 2016

which shows that the level of operations of the business has increased significantly. The cash

from investing activities of the business effectively shows that main cash flow during the year is

from purchase of property, plant and equipment during the year which is shown to be $

147,418,000. The cash outflow suggest that the management has made significant investments in

assets during the year (Pavlović and Bogdanović 2013). The cash flow from financing activities

include various repayments which are undertaken by the business during the year such as

repayment of borrowings, repayment of Hire purchase and also dividend paid to the shareholders

of the company (Sayari and Mugan 2013). The net cash equivalents which is shown for the year

2017 is shown to be $ 166,710,000 and the same is shown to be $ 181,157,000 for the year 2016.

Therefore, the cash balance of the business has slightly fallen in comparison to previous year

results.

CORPORATE ACCOUNTING

Cash Flow Statement Analysis

The cash flow statement represents the cash position of the business and demonstrates

each activity which is either a cash inflow and cash outflow for the business. The cash flow

statement of Ausdrill ltd shows cash from operating activities which mainly comprises of cash

receipts which the business receives from operating activities of the business and also cash

payments which are made by the business to suppliers (Nurnberg 2015). Another significant item

which is included ion the cash flow statement is income tax paid by the business during the year.

The net cash flow for the year 2017 is shown to be $ 94,613,000 which has increased from 2016

estimates which is shown to be $ 91,006,000. The receipts from customers and also the payments

which are made to the suppliers of the business have increased on the basis of estimates of 2016

which shows that the level of operations of the business has increased significantly. The cash

from investing activities of the business effectively shows that main cash flow during the year is

from purchase of property, plant and equipment during the year which is shown to be $

147,418,000. The cash outflow suggest that the management has made significant investments in

assets during the year (Pavlović and Bogdanović 2013). The cash flow from financing activities

include various repayments which are undertaken by the business during the year such as

repayment of borrowings, repayment of Hire purchase and also dividend paid to the shareholders

of the company (Sayari and Mugan 2013). The net cash equivalents which is shown for the year

2017 is shown to be $ 166,710,000 and the same is shown to be $ 181,157,000 for the year 2016.

Therefore, the cash balance of the business has slightly fallen in comparison to previous year

results.

8

CORPORATE ACCOUNTING

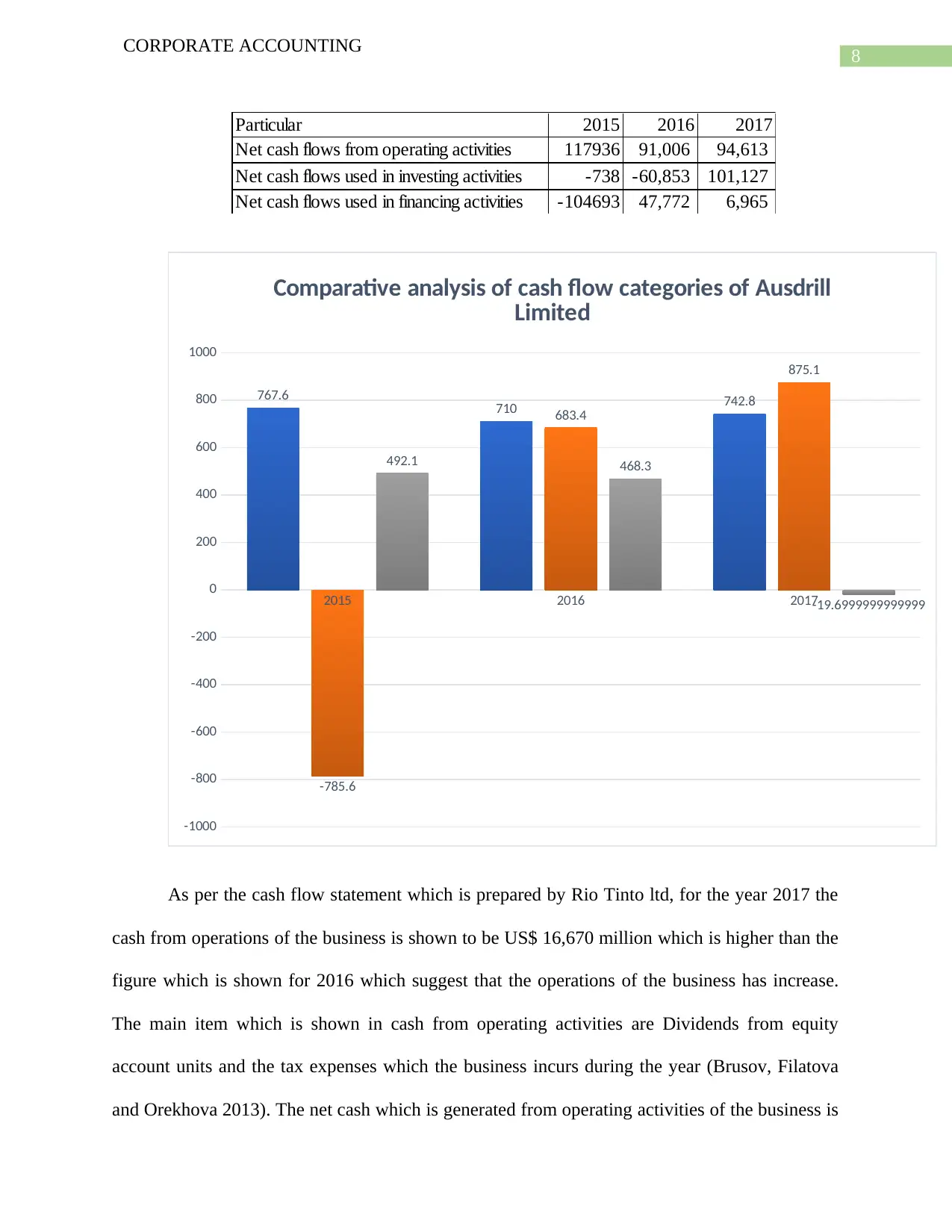

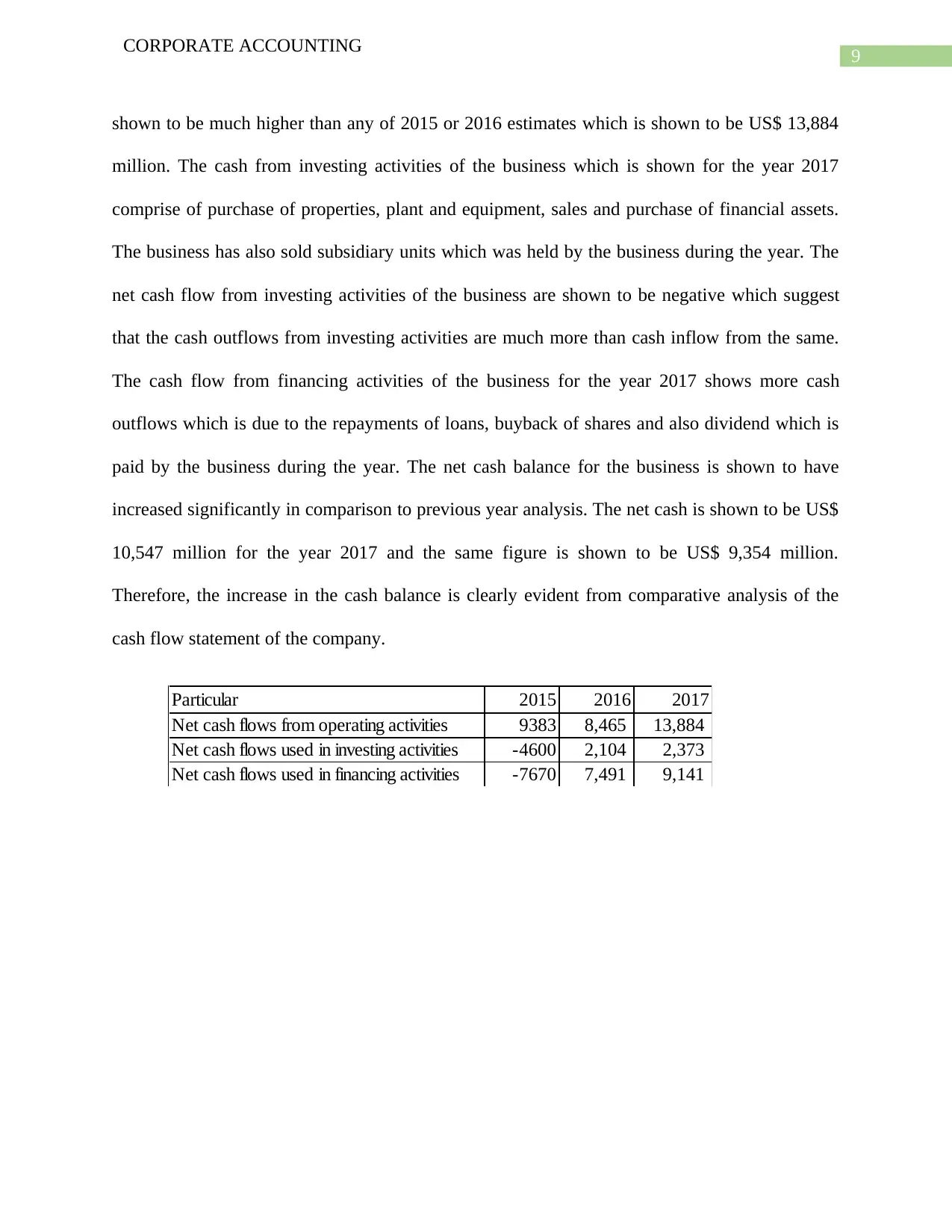

Particular 2015 2016 2017

Net cash flows from operating activities 117936 91,006 94,613

Net cash flows used in investing activities -738 -60,853 101,127

Net cash flows used in financing activities -104693 47,772 6,965

2015 2016 2017

-1000

-800

-600

-400

-200

0

200

400

600

800

1000

767.6 710 742.8

-785.6

683.4

875.1

492.1 468.3

-19.6999999999999

Comparative analysis of cash flow categories of Ausdrill

Limited

As per the cash flow statement which is prepared by Rio Tinto ltd, for the year 2017 the

cash from operations of the business is shown to be US$ 16,670 million which is higher than the

figure which is shown for 2016 which suggest that the operations of the business has increase.

The main item which is shown in cash from operating activities are Dividends from equity

account units and the tax expenses which the business incurs during the year (Brusov, Filatova

and Orekhova 2013). The net cash which is generated from operating activities of the business is

CORPORATE ACCOUNTING

Particular 2015 2016 2017

Net cash flows from operating activities 117936 91,006 94,613

Net cash flows used in investing activities -738 -60,853 101,127

Net cash flows used in financing activities -104693 47,772 6,965

2015 2016 2017

-1000

-800

-600

-400

-200

0

200

400

600

800

1000

767.6 710 742.8

-785.6

683.4

875.1

492.1 468.3

-19.6999999999999

Comparative analysis of cash flow categories of Ausdrill

Limited

As per the cash flow statement which is prepared by Rio Tinto ltd, for the year 2017 the

cash from operations of the business is shown to be US$ 16,670 million which is higher than the

figure which is shown for 2016 which suggest that the operations of the business has increase.

The main item which is shown in cash from operating activities are Dividends from equity

account units and the tax expenses which the business incurs during the year (Brusov, Filatova

and Orekhova 2013). The net cash which is generated from operating activities of the business is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

shown to be much higher than any of 2015 or 2016 estimates which is shown to be US$ 13,884

million. The cash from investing activities of the business which is shown for the year 2017

comprise of purchase of properties, plant and equipment, sales and purchase of financial assets.

The business has also sold subsidiary units which was held by the business during the year. The

net cash flow from investing activities of the business are shown to be negative which suggest

that the cash outflows from investing activities are much more than cash inflow from the same.

The cash flow from financing activities of the business for the year 2017 shows more cash

outflows which is due to the repayments of loans, buyback of shares and also dividend which is

paid by the business during the year. The net cash balance for the business is shown to have

increased significantly in comparison to previous year analysis. The net cash is shown to be US$

10,547 million for the year 2017 and the same figure is shown to be US$ 9,354 million.

Therefore, the increase in the cash balance is clearly evident from comparative analysis of the

cash flow statement of the company.

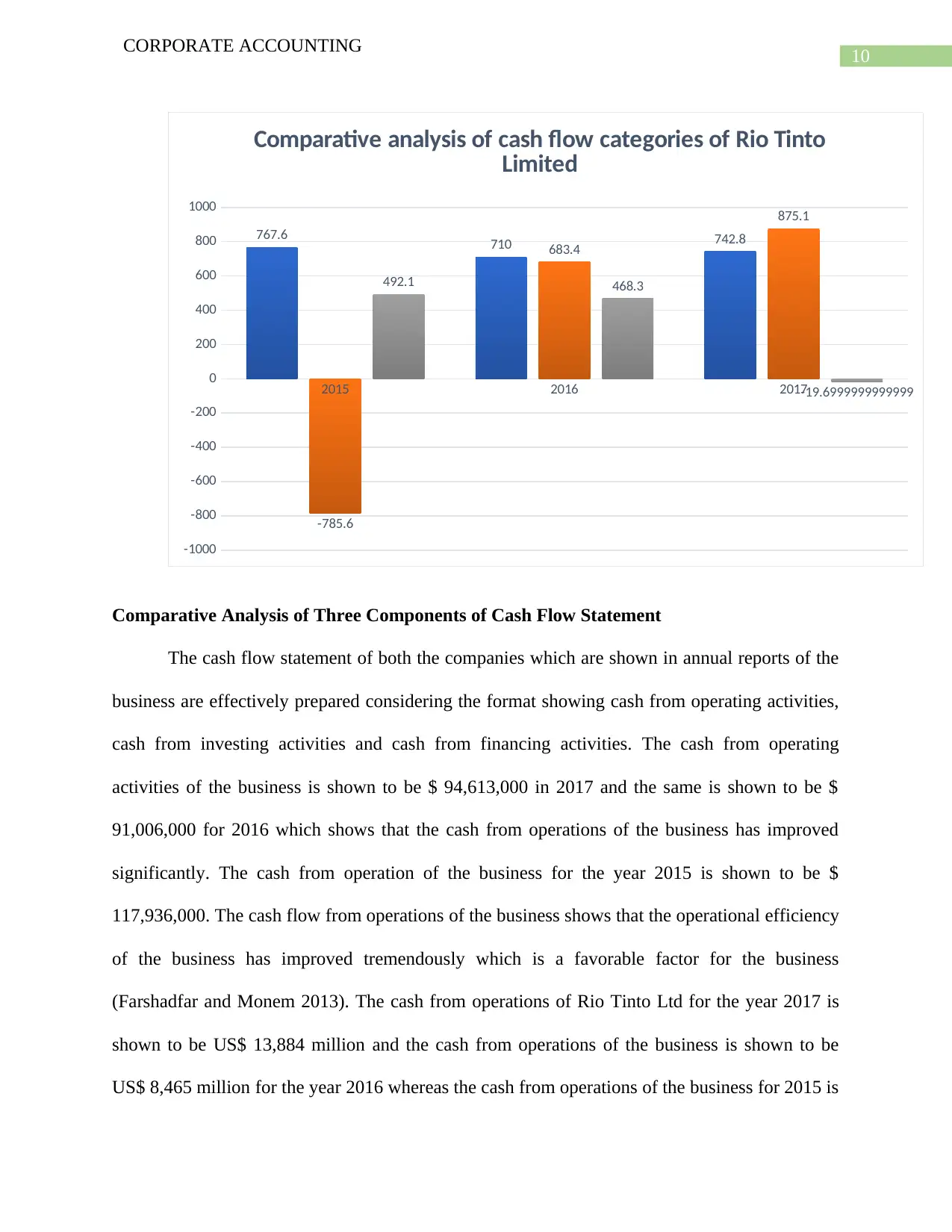

Particular 2015 2016 2017

Net cash flows from operating activities 9383 8,465 13,884

Net cash flows used in investing activities -4600 2,104 2,373

Net cash flows used in financing activities -7670 7,491 9,141

CORPORATE ACCOUNTING

shown to be much higher than any of 2015 or 2016 estimates which is shown to be US$ 13,884

million. The cash from investing activities of the business which is shown for the year 2017

comprise of purchase of properties, plant and equipment, sales and purchase of financial assets.

The business has also sold subsidiary units which was held by the business during the year. The

net cash flow from investing activities of the business are shown to be negative which suggest

that the cash outflows from investing activities are much more than cash inflow from the same.

The cash flow from financing activities of the business for the year 2017 shows more cash

outflows which is due to the repayments of loans, buyback of shares and also dividend which is

paid by the business during the year. The net cash balance for the business is shown to have

increased significantly in comparison to previous year analysis. The net cash is shown to be US$

10,547 million for the year 2017 and the same figure is shown to be US$ 9,354 million.

Therefore, the increase in the cash balance is clearly evident from comparative analysis of the

cash flow statement of the company.

Particular 2015 2016 2017

Net cash flows from operating activities 9383 8,465 13,884

Net cash flows used in investing activities -4600 2,104 2,373

Net cash flows used in financing activities -7670 7,491 9,141

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

2015 2016 2017

-1000

-800

-600

-400

-200

0

200

400

600

800

1000

767.6 710 742.8

-785.6

683.4

875.1

492.1 468.3

-19.6999999999999

Comparative analysis of cash flow categories of Rio Tinto

Limited

Comparative Analysis of Three Components of Cash Flow Statement

The cash flow statement of both the companies which are shown in annual reports of the

business are effectively prepared considering the format showing cash from operating activities,

cash from investing activities and cash from financing activities. The cash from operating

activities of the business is shown to be $ 94,613,000 in 2017 and the same is shown to be $

91,006,000 for 2016 which shows that the cash from operations of the business has improved

significantly. The cash from operation of the business for the year 2015 is shown to be $

117,936,000. The cash flow from operations of the business shows that the operational efficiency

of the business has improved tremendously which is a favorable factor for the business

(Farshadfar and Monem 2013). The cash from operations of Rio Tinto Ltd for the year 2017 is

shown to be US$ 13,884 million and the cash from operations of the business is shown to be

US$ 8,465 million for the year 2016 whereas the cash from operations of the business for 2015 is

CORPORATE ACCOUNTING

2015 2016 2017

-1000

-800

-600

-400

-200

0

200

400

600

800

1000

767.6 710 742.8

-785.6

683.4

875.1

492.1 468.3

-19.6999999999999

Comparative analysis of cash flow categories of Rio Tinto

Limited

Comparative Analysis of Three Components of Cash Flow Statement

The cash flow statement of both the companies which are shown in annual reports of the

business are effectively prepared considering the format showing cash from operating activities,

cash from investing activities and cash from financing activities. The cash from operating

activities of the business is shown to be $ 94,613,000 in 2017 and the same is shown to be $

91,006,000 for 2016 which shows that the cash from operations of the business has improved

significantly. The cash from operation of the business for the year 2015 is shown to be $

117,936,000. The cash flow from operations of the business shows that the operational efficiency

of the business has improved tremendously which is a favorable factor for the business

(Farshadfar and Monem 2013). The cash from operations of Rio Tinto Ltd for the year 2017 is

shown to be US$ 13,884 million and the cash from operations of the business is shown to be

US$ 8,465 million for the year 2016 whereas the cash from operations of the business for 2015 is

11

CORPORATE ACCOUNTING

shown to be $ 9,383,000. The cash from operating activities shows that the figure shown for

2017 is more for Rio Tinto Ltd in comparison to Ausdrill Ltd. This may be due to the higher

scale of operations of the business. The cash from investing activities of Ausdrill Ltd for the year

2017 is shown to be negative and the figure is shown to be $ 101,127,000 which is mainly due to

the payments which has undertaken for purchase of assets, purchase of financial assets

(Farshadfar and Monem 2013). The cash flow for Rio Tinto ltd for the year 2017 is also shown

to be negative which is also due to the increasing amount of payments which are related to

purchases which are undertaken by the business. The cash flow from investing activities of the

business is shown to be better in case of Ausdrill Ltd. The cash from financing activities of the

business mainly comprise of repayments of loans and hire purchase agreements and the proceeds

includes loans which are taken by the business during the period. The cash flow from financing

activities is shown to be in negative which is $ 6,965 million for the year and the same has

improved from last year analysis. In the case of Rio Tinto ltd, the financing cash from operations

is shown to more which means that the company has made quite a few cash payments during the

year.

Insight of Cash flow Statement

The cash from operations of the both the companies shows rise in cash from operations of

the business which suggest that the operational efficiency of the business is appropriate, however

the cash which is generated from operations of the business is shown to be more appropriate for

Rio Tinto ltd as the figure is comparatively much more than the results of Ausdrill ltd. The cash

from investing activities of both the companies are shown to be to same as both the companies

has undertaken significant amount of cash flows which is related to purchases of property, plant

and equipment and also repayment of loans of the business (Gupta et al. 2014). The net cash

CORPORATE ACCOUNTING

shown to be $ 9,383,000. The cash from operating activities shows that the figure shown for

2017 is more for Rio Tinto Ltd in comparison to Ausdrill Ltd. This may be due to the higher

scale of operations of the business. The cash from investing activities of Ausdrill Ltd for the year

2017 is shown to be negative and the figure is shown to be $ 101,127,000 which is mainly due to

the payments which has undertaken for purchase of assets, purchase of financial assets

(Farshadfar and Monem 2013). The cash flow for Rio Tinto ltd for the year 2017 is also shown

to be negative which is also due to the increasing amount of payments which are related to

purchases which are undertaken by the business. The cash flow from investing activities of the

business is shown to be better in case of Ausdrill Ltd. The cash from financing activities of the

business mainly comprise of repayments of loans and hire purchase agreements and the proceeds

includes loans which are taken by the business during the period. The cash flow from financing

activities is shown to be in negative which is $ 6,965 million for the year and the same has

improved from last year analysis. In the case of Rio Tinto ltd, the financing cash from operations

is shown to more which means that the company has made quite a few cash payments during the

year.

Insight of Cash flow Statement

The cash from operations of the both the companies shows rise in cash from operations of

the business which suggest that the operational efficiency of the business is appropriate, however

the cash which is generated from operations of the business is shown to be more appropriate for

Rio Tinto ltd as the figure is comparatively much more than the results of Ausdrill ltd. The cash

from investing activities of both the companies are shown to be to same as both the companies

has undertaken significant amount of cash flows which is related to purchases of property, plant

and equipment and also repayment of loans of the business (Gupta et al. 2014). The net cash

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.