HI5020 Corporate Accounting Assignment: Bank Performance Analysis

VerifiedAdded on 2023/06/04

|22

|4465

|56

Report

AI Summary

This report provides a comparative analysis of the corporate accounting practices of Commonwealth Bank and Westpac Bank, both listed on the Australian Securities Exchange (ASX). The analysis, conducted from an investor's perspective, examines various financial components, including equity, cash flow statements, comprehensive income statements, and corporate income tax. The equity section discusses share capital, retained earnings, and reserves, highlighting the debt-equity ratios of both banks. The cash flow statement analysis explores operating, investing, and financing activities, comparing trends and providing graphical representations. The comprehensive income statement section addresses items reported under other comprehensive income (OCI) and their implications. Finally, the report delves into corporate income tax, calculating effective tax rates, deferred tax assets and liabilities, and the difference between cash and book tax, concluding with an overview of the key findings.

Corporate accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

We get the industry overview by analyzing the performance of each company belonging to that

industry. The following discussion is the comparative analysis of two listed companies of

Australia operating within the same industry. For such an analysis, we have chosen

Commonwealth and Westpac banks. The analysis has been made from an investor's point of

view as such stakeholders have an interest in knowing about the internal environment of an

organization so that useful decisions can be made accordingly.

We get the industry overview by analyzing the performance of each company belonging to that

industry. The following discussion is the comparative analysis of two listed companies of

Australia operating within the same industry. For such an analysis, we have chosen

Commonwealth and Westpac banks. The analysis has been made from an investor's point of

view as such stakeholders have an interest in knowing about the internal environment of an

organization so that useful decisions can be made accordingly.

Contents

ANALYSIS OF EQUITY................................................................................................................6

Discussion on each item of equity for both the companies..........................................................6

Discussion regarding debt and equity of both the companies......................................................7

ANALYSIS OF CASH FLOW STATEMENT...............................................................................9

Discussion regarding Cash Flow Statement:...............................................................................9

Description of Analysis of Cash flow of both the companies....................................................13

ANALYSIS OF COMPREHENSIVE INCOME STATEMENT.................................................14

Items reported in other comprehensive income statement.........................................................14

Reasons for not reporting this item in income statement...........................................................14

Comparative Analysis of OCI statement items..........................................................................14

Use of OCI in evaluation of performance of managers.............................................................15

ANALYSIS OF CORPORATE INCOME TAX...........................................................................16

Tax expense for the companies for the current year..................................................................16

Effective income tax rate...........................................................................................................16

Deferred tax asset and liabilities................................................................................................16

Increase in DTA and DTL.........................................................................................................17

Calculation of cash tax using book tax......................................................................................17

Calculation of Tax rate...............................................................................................................19

Difference in cash tax and book tax...........................................................................................19

ANALYSIS OF EQUITY................................................................................................................6

Discussion on each item of equity for both the companies..........................................................6

Discussion regarding debt and equity of both the companies......................................................7

ANALYSIS OF CASH FLOW STATEMENT...............................................................................9

Discussion regarding Cash Flow Statement:...............................................................................9

Description of Analysis of Cash flow of both the companies....................................................13

ANALYSIS OF COMPREHENSIVE INCOME STATEMENT.................................................14

Items reported in other comprehensive income statement.........................................................14

Reasons for not reporting this item in income statement...........................................................14

Comparative Analysis of OCI statement items..........................................................................14

Use of OCI in evaluation of performance of managers.............................................................15

ANALYSIS OF CORPORATE INCOME TAX...........................................................................16

Tax expense for the companies for the current year..................................................................16

Effective income tax rate...........................................................................................................16

Deferred tax asset and liabilities................................................................................................16

Increase in DTA and DTL.........................................................................................................17

Calculation of cash tax using book tax......................................................................................17

Calculation of Tax rate...............................................................................................................19

Difference in cash tax and book tax...........................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION..............................................................................................................................20

Bibliography..................................................................................................................................21

Bibliography..................................................................................................................................21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The financial & non financial measures and statistics together sums up as various components of

the financial reports. Such components differ from each other in terms of characteristics and their

nature. The following discussion focuses on comparison of various such components between

Commonwealth group and Westpac group working under the same industry.

The Australian multinational bank, Commonwealth Bank, is engaged a number of activities such

as Institutional banking , retail and business management of funds, superannuation facilities,

investment, insurance and such other financial services such as brokerage services. It has its

businesses spread all over the world such as New Zealand, US, UK and Asia. As of 2015, this

company had turned out to be the largest listed company on Australian Securities Exchange

(ASX) with brands such as Commonwealth securities & insurance, ASB Bank, Bankwest, etc.

This company is also the Southern Hemisphere's largest bank (Armstrong, 2015).

Westpac Banking Corporation, also known as Westpac, having headquarters at Sydney is a

provider of financial services and is considered as one of the 'big four' banks of Australia. It's

name is formed by the combination of 'Western' and 'Pacific'. Considering its current status, it

has 14 million customers with 40,000 employees under it. It looks forward to prosper in terms of

growth, customers, communities and great service provider. It was consideded as one of the most

sustainable bank as per Dow Jones Sustainability Index in 2017 which was for the fourth time in

a row (Atkinson, 2012).

For a better picture of both the companies, we have discussed the following financial aspects of

both the companies’ along with a comparison analysis between the two.

The financial & non financial measures and statistics together sums up as various components of

the financial reports. Such components differ from each other in terms of characteristics and their

nature. The following discussion focuses on comparison of various such components between

Commonwealth group and Westpac group working under the same industry.

The Australian multinational bank, Commonwealth Bank, is engaged a number of activities such

as Institutional banking , retail and business management of funds, superannuation facilities,

investment, insurance and such other financial services such as brokerage services. It has its

businesses spread all over the world such as New Zealand, US, UK and Asia. As of 2015, this

company had turned out to be the largest listed company on Australian Securities Exchange

(ASX) with brands such as Commonwealth securities & insurance, ASB Bank, Bankwest, etc.

This company is also the Southern Hemisphere's largest bank (Armstrong, 2015).

Westpac Banking Corporation, also known as Westpac, having headquarters at Sydney is a

provider of financial services and is considered as one of the 'big four' banks of Australia. It's

name is formed by the combination of 'Western' and 'Pacific'. Considering its current status, it

has 14 million customers with 40,000 employees under it. It looks forward to prosper in terms of

growth, customers, communities and great service provider. It was consideded as one of the most

sustainable bank as per Dow Jones Sustainability Index in 2017 which was for the fourth time in

a row (Atkinson, 2012).

For a better picture of both the companies, we have discussed the following financial aspects of

both the companies’ along with a comparison analysis between the two.

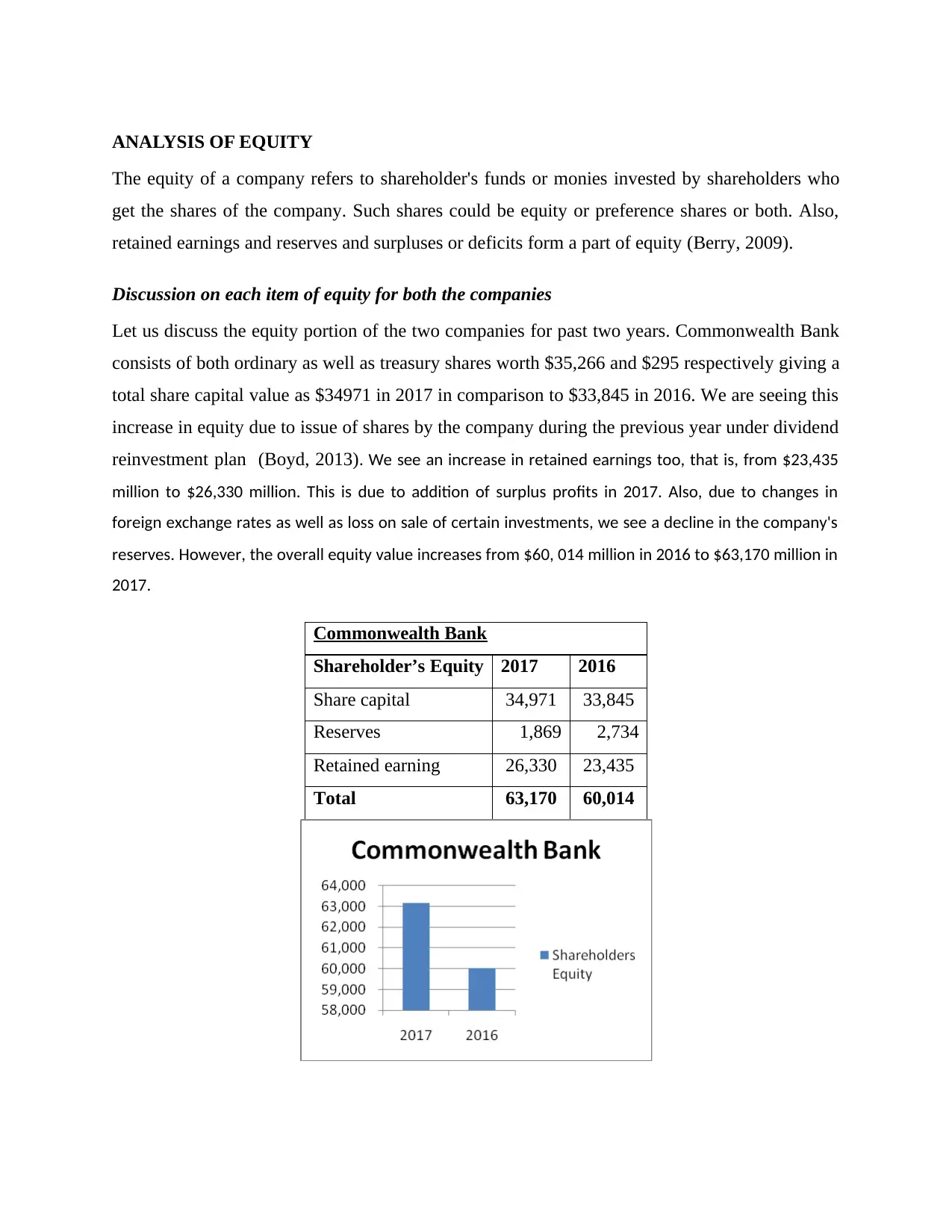

ANALYSIS OF EQUITY

The equity of a company refers to shareholder's funds or monies invested by shareholders who

get the shares of the company. Such shares could be equity or preference shares or both. Also,

retained earnings and reserves and surpluses or deficits form a part of equity (Berry, 2009).

Discussion on each item of equity for both the companies

Let us discuss the equity portion of the two companies for past two years. Commonwealth Bank

consists of both ordinary as well as treasury shares worth $35,266 and $295 respectively giving a

total share capital value as $34971 in 2017 in comparison to $33,845 in 2016. We are seeing this

increase in equity due to issue of shares by the company during the previous year under dividend

reinvestment plan (Boyd, 2013). We see an increase in retained earnings too, that is, from $23,435

million to $26,330 million. This is due to addition of surplus profits in 2017. Also, due to changes in

foreign exchange rates as well as loss on sale of certain investments, we see a decline in the company's

reserves. However, the overall equity value increases from $60, 014 million in 2016 to $63,170 million in

2017.

Commonwealth Bank

Shareholder’s Equity 2017 2016

Share capital 34,971 33,845

Reserves 1,869 2,734

Retained earning 26,330 23,435

Total 63,170 60,014

The equity of a company refers to shareholder's funds or monies invested by shareholders who

get the shares of the company. Such shares could be equity or preference shares or both. Also,

retained earnings and reserves and surpluses or deficits form a part of equity (Berry, 2009).

Discussion on each item of equity for both the companies

Let us discuss the equity portion of the two companies for past two years. Commonwealth Bank

consists of both ordinary as well as treasury shares worth $35,266 and $295 respectively giving a

total share capital value as $34971 in 2017 in comparison to $33,845 in 2016. We are seeing this

increase in equity due to issue of shares by the company during the previous year under dividend

reinvestment plan (Boyd, 2013). We see an increase in retained earnings too, that is, from $23,435

million to $26,330 million. This is due to addition of surplus profits in 2017. Also, due to changes in

foreign exchange rates as well as loss on sale of certain investments, we see a decline in the company's

reserves. However, the overall equity value increases from $60, 014 million in 2016 to $63,170 million in

2017.

Commonwealth Bank

Shareholder’s Equity 2017 2016

Share capital 34,971 33,845

Reserves 1,869 2,734

Retained earning 26,330 23,435

Total 63,170 60,014

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

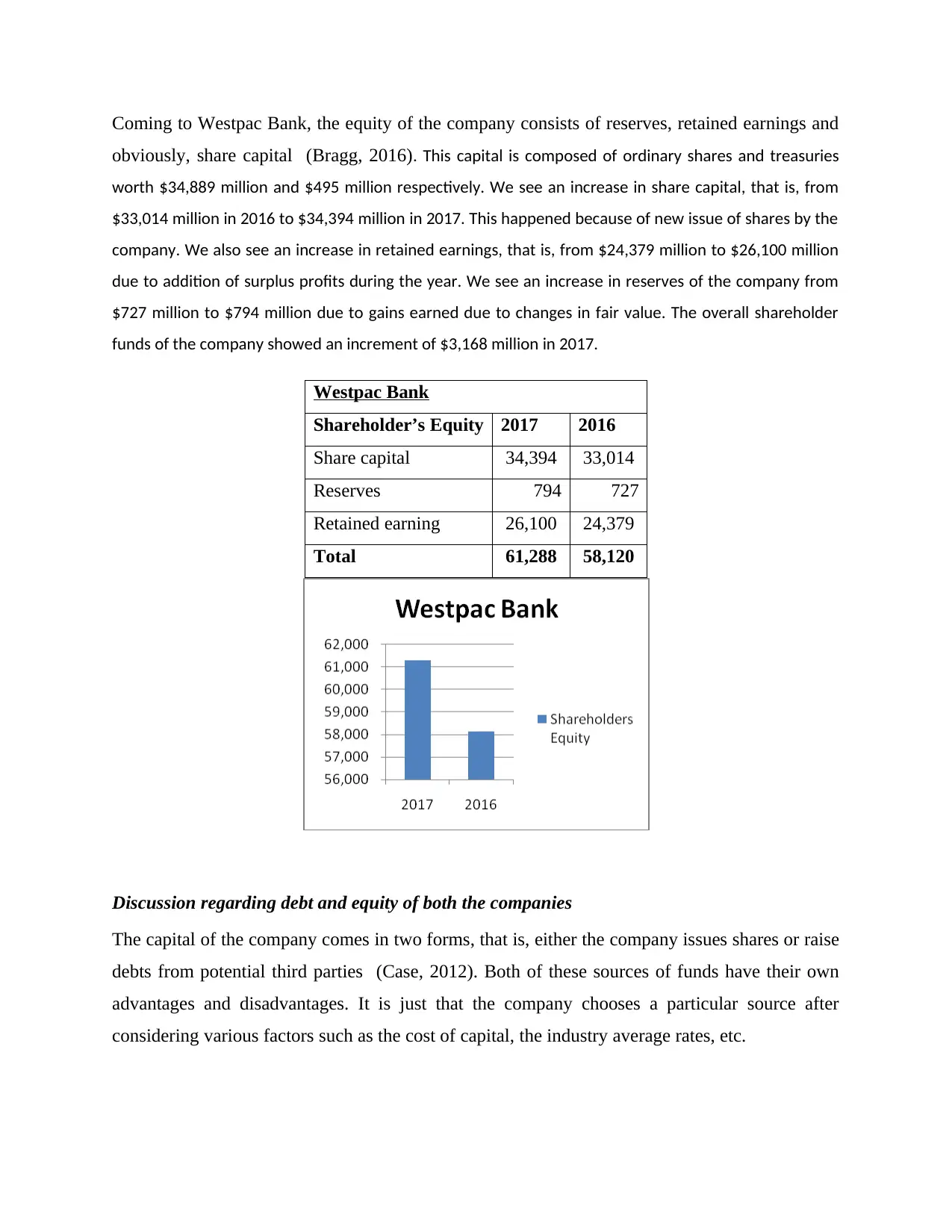

Coming to Westpac Bank, the equity of the company consists of reserves, retained earnings and

obviously, share capital (Bragg, 2016). This capital is composed of ordinary shares and treasuries

worth $34,889 million and $495 million respectively. We see an increase in share capital, that is, from

$33,014 million in 2016 to $34,394 million in 2017. This happened because of new issue of shares by the

company. We also see an increase in retained earnings, that is, from $24,379 million to $26,100 million

due to addition of surplus profits during the year. We see an increase in reserves of the company from

$727 million to $794 million due to gains earned due to changes in fair value. The overall shareholder

funds of the company showed an increment of $3,168 million in 2017.

Westpac Bank

Shareholder’s Equity 2017 2016

Share capital 34,394 33,014

Reserves 794 727

Retained earning 26,100 24,379

Total 61,288 58,120

Discussion regarding debt and equity of both the companies

The capital of the company comes in two forms, that is, either the company issues shares or raise

debts from potential third parties (Case, 2012). Both of these sources of funds have their own

advantages and disadvantages. It is just that the company chooses a particular source after

considering various factors such as the cost of capital, the industry average rates, etc.

obviously, share capital (Bragg, 2016). This capital is composed of ordinary shares and treasuries

worth $34,889 million and $495 million respectively. We see an increase in share capital, that is, from

$33,014 million in 2016 to $34,394 million in 2017. This happened because of new issue of shares by the

company. We also see an increase in retained earnings, that is, from $24,379 million to $26,100 million

due to addition of surplus profits during the year. We see an increase in reserves of the company from

$727 million to $794 million due to gains earned due to changes in fair value. The overall shareholder

funds of the company showed an increment of $3,168 million in 2017.

Westpac Bank

Shareholder’s Equity 2017 2016

Share capital 34,394 33,014

Reserves 794 727

Retained earning 26,100 24,379

Total 61,288 58,120

Discussion regarding debt and equity of both the companies

The capital of the company comes in two forms, that is, either the company issues shares or raise

debts from potential third parties (Case, 2012). Both of these sources of funds have their own

advantages and disadvantages. It is just that the company chooses a particular source after

considering various factors such as the cost of capital, the industry average rates, etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

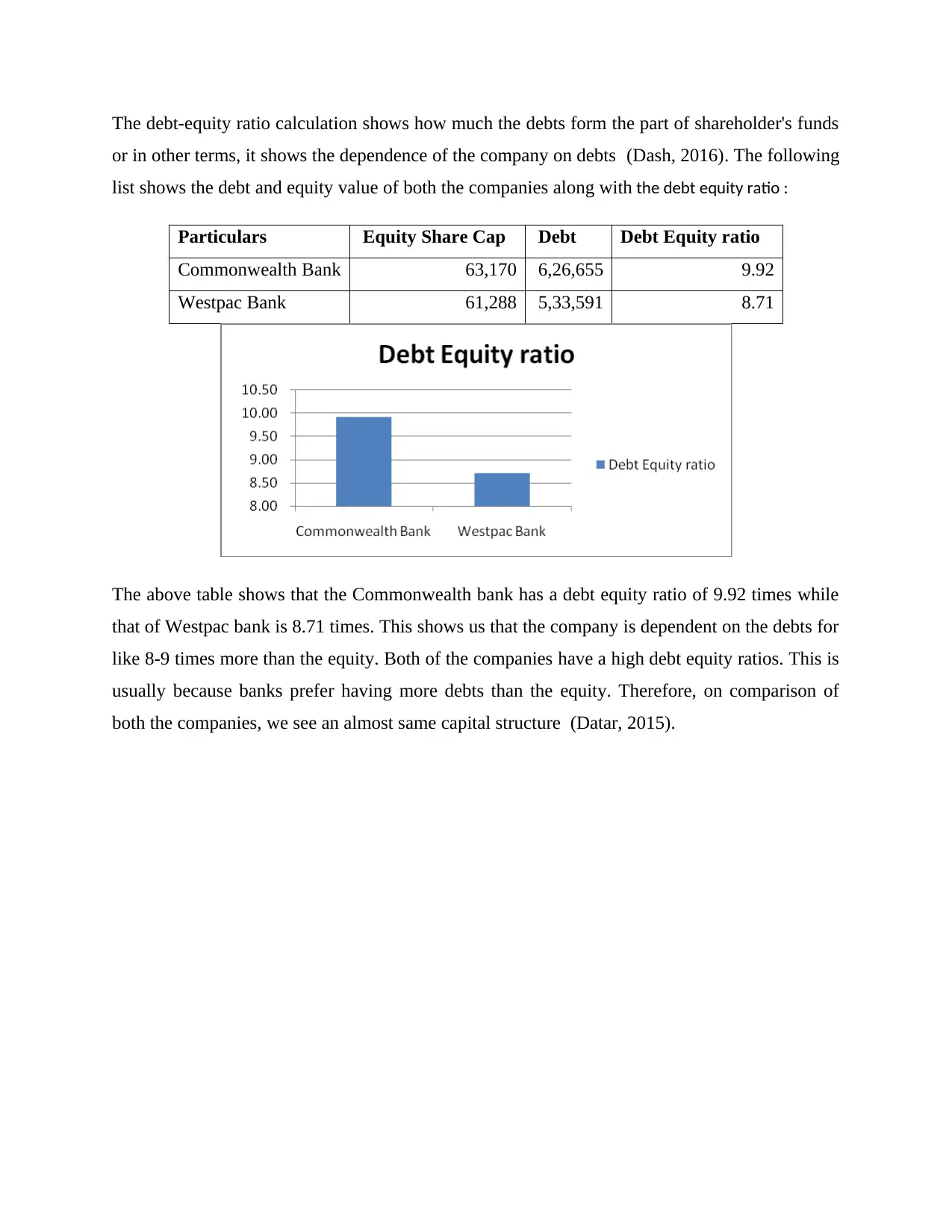

The debt-equity ratio calculation shows how much the debts form the part of shareholder's funds

or in other terms, it shows the dependence of the company on debts (Dash, 2016). The following

list shows the debt and equity value of both the companies along with the debt equity ratio :

Particulars Equity Share Cap Debt Debt Equity ratio

Commonwealth Bank 63,170 6,26,655 9.92

Westpac Bank 61,288 5,33,591 8.71

The above table shows that the Commonwealth bank has a debt equity ratio of 9.92 times while

that of Westpac bank is 8.71 times. This shows us that the company is dependent on the debts for

like 8-9 times more than the equity. Both of the companies have a high debt equity ratios. This is

usually because banks prefer having more debts than the equity. Therefore, on comparison of

both the companies, we see an almost same capital structure (Datar, 2015).

or in other terms, it shows the dependence of the company on debts (Dash, 2016). The following

list shows the debt and equity value of both the companies along with the debt equity ratio :

Particulars Equity Share Cap Debt Debt Equity ratio

Commonwealth Bank 63,170 6,26,655 9.92

Westpac Bank 61,288 5,33,591 8.71

The above table shows that the Commonwealth bank has a debt equity ratio of 9.92 times while

that of Westpac bank is 8.71 times. This shows us that the company is dependent on the debts for

like 8-9 times more than the equity. Both of the companies have a high debt equity ratios. This is

usually because banks prefer having more debts than the equity. Therefore, on comparison of

both the companies, we see an almost same capital structure (Datar, 2015).

ANALYSIS OF CASH FLOW STATEMENT

There are two bases to prepare the cash flow statement, either on the cash basis or the accrual

basis. The two companies prepare their cash flow statements on the accrual basis. It is important

for a company to prepare this statement to know the actual inflow or outflow of cash in the

company and thereby, let the users know about the liquidity status of the company (Donanldson,

2012).

Discussion regarding Cash Flow Statement:

In case of Commonwealth bank:

Operating activities consists of investment incomes and Interest payments as those are the

main activities of the business.

Investing activities consists of cash flows from sale and acquirement of associates or

subsidiaries, investments, fixed assets and investment incomes in the form of dividend.

Financing activities consists of repayments and proceeds of leverage funds (debts) and

equity.

The outflow of cash from the operating activities in $807 million in 2017 in comparison to

$4,561 million in 2016. Such a decline is visualized due to increase in inflow from interest

incomes and investments incomes. We see a decline in cash flowing out from investment

activities, that is, from $2,032 million in 2016 to $677 million in 2017. This decline took place

due to non payments for acquiring of certain entities that are under control, less purchases of

property, plant and equipment & intangible assets. We see an increment in cash inflows in case

of financing activities which is due to lesser outflow from redemption of debt instruments.

On an overall basis, we see a positive result as there is an increase from the negative balance of

$4,973 million in 2016 to the positive balance of $8,988 million in 2017.

In case of Westpac bank :

Operating activities consists of cash flowing from proceeds of insurance, interest and

income tax.

There are two bases to prepare the cash flow statement, either on the cash basis or the accrual

basis. The two companies prepare their cash flow statements on the accrual basis. It is important

for a company to prepare this statement to know the actual inflow or outflow of cash in the

company and thereby, let the users know about the liquidity status of the company (Donanldson,

2012).

Discussion regarding Cash Flow Statement:

In case of Commonwealth bank:

Operating activities consists of investment incomes and Interest payments as those are the

main activities of the business.

Investing activities consists of cash flows from sale and acquirement of associates or

subsidiaries, investments, fixed assets and investment incomes in the form of dividend.

Financing activities consists of repayments and proceeds of leverage funds (debts) and

equity.

The outflow of cash from the operating activities in $807 million in 2017 in comparison to

$4,561 million in 2016. Such a decline is visualized due to increase in inflow from interest

incomes and investments incomes. We see a decline in cash flowing out from investment

activities, that is, from $2,032 million in 2016 to $677 million in 2017. This decline took place

due to non payments for acquiring of certain entities that are under control, less purchases of

property, plant and equipment & intangible assets. We see an increment in cash inflows in case

of financing activities which is due to lesser outflow from redemption of debt instruments.

On an overall basis, we see a positive result as there is an increase from the negative balance of

$4,973 million in 2016 to the positive balance of $8,988 million in 2017.

In case of Westpac bank :

Operating activities consists of cash flowing from proceeds of insurance, interest and

income tax.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Investing activities consists of cash flows from sale and acquirement of associates or

subsidiaries, investments, both intangible & tangible assets and various other securities.

Financing activities consists of repayments and proceeds of leverage funds (debts) and

equity.

As we can see, Westpac shows a decline in the cash flowing due to operating activities, that is,

from $5,497 million in 2016 to $2,820 million in 2017 which happened due to losses incurred

from valuations of the investments according to fair value method. It shows a decline in cash

outflows too from $7,245 million in 2016 to $1,698 million in 2017 which took place majorly

due to increase in proceeds from sale of associates and securities. Similarly, we again see a

decline in inflows in case of financing activities from $4,573 million to $552 million in 2017.

This took place due to increase in out flowing of cash in the form of redemption of loans and

issue of debts in lower proportions (Flood, 2017).

On an overall basis, we see a decline in net cash flow by approximately $1,151 million in the

current year 2017.

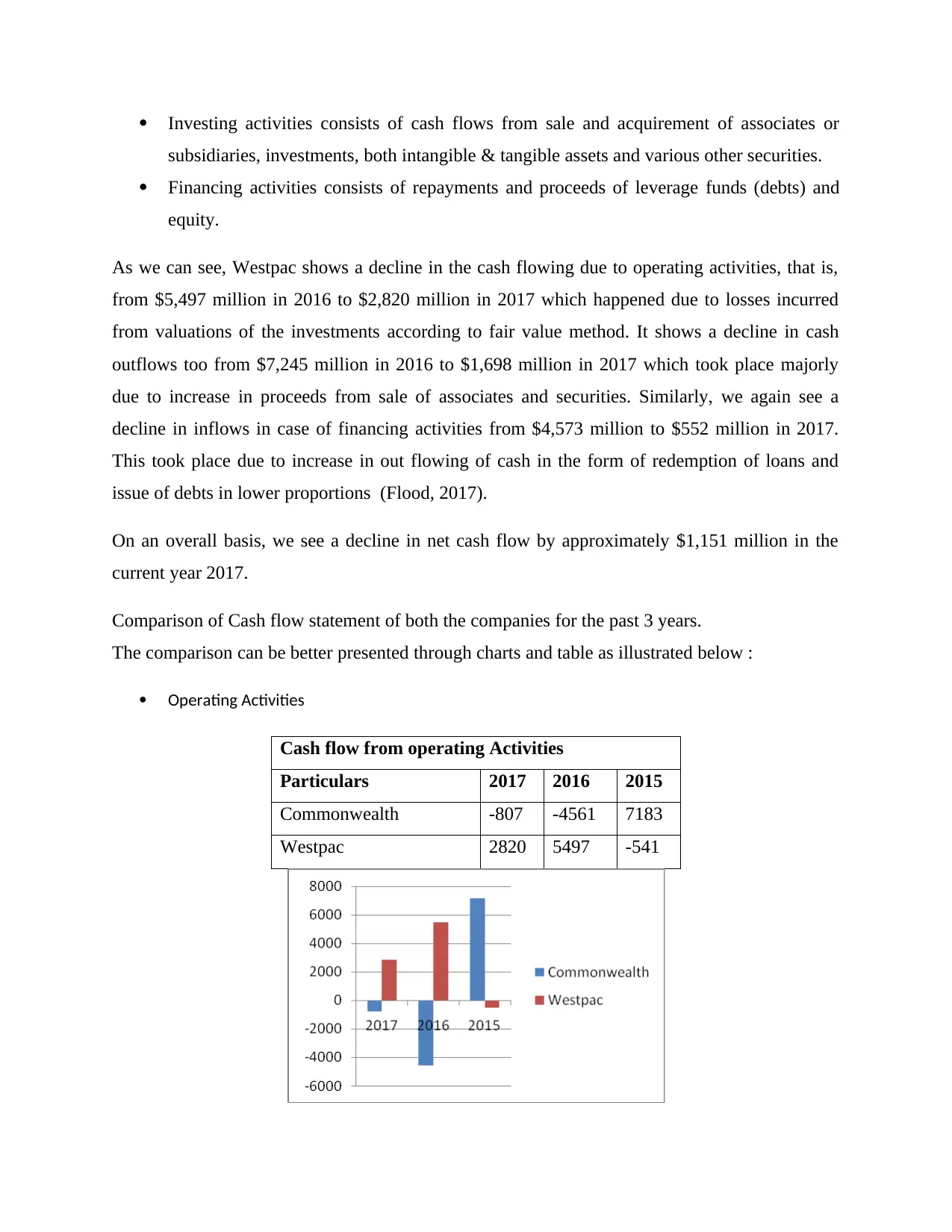

Comparison of Cash flow statement of both the companies for the past 3 years.

The comparison can be better presented through charts and table as illustrated below :

Operating Activities

Cash flow from operating Activities

Particulars 2017 2016 2015

Commonwealth -807 -4561 7183

Westpac 2820 5497 -541

subsidiaries, investments, both intangible & tangible assets and various other securities.

Financing activities consists of repayments and proceeds of leverage funds (debts) and

equity.

As we can see, Westpac shows a decline in the cash flowing due to operating activities, that is,

from $5,497 million in 2016 to $2,820 million in 2017 which happened due to losses incurred

from valuations of the investments according to fair value method. It shows a decline in cash

outflows too from $7,245 million in 2016 to $1,698 million in 2017 which took place majorly

due to increase in proceeds from sale of associates and securities. Similarly, we again see a

decline in inflows in case of financing activities from $4,573 million to $552 million in 2017.

This took place due to increase in out flowing of cash in the form of redemption of loans and

issue of debts in lower proportions (Flood, 2017).

On an overall basis, we see a decline in net cash flow by approximately $1,151 million in the

current year 2017.

Comparison of Cash flow statement of both the companies for the past 3 years.

The comparison can be better presented through charts and table as illustrated below :

Operating Activities

Cash flow from operating Activities

Particulars 2017 2016 2015

Commonwealth -807 -4561 7183

Westpac 2820 5497 -541

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

We do not see any trend being followed in case of operating activities of both the companies.

Investing activities

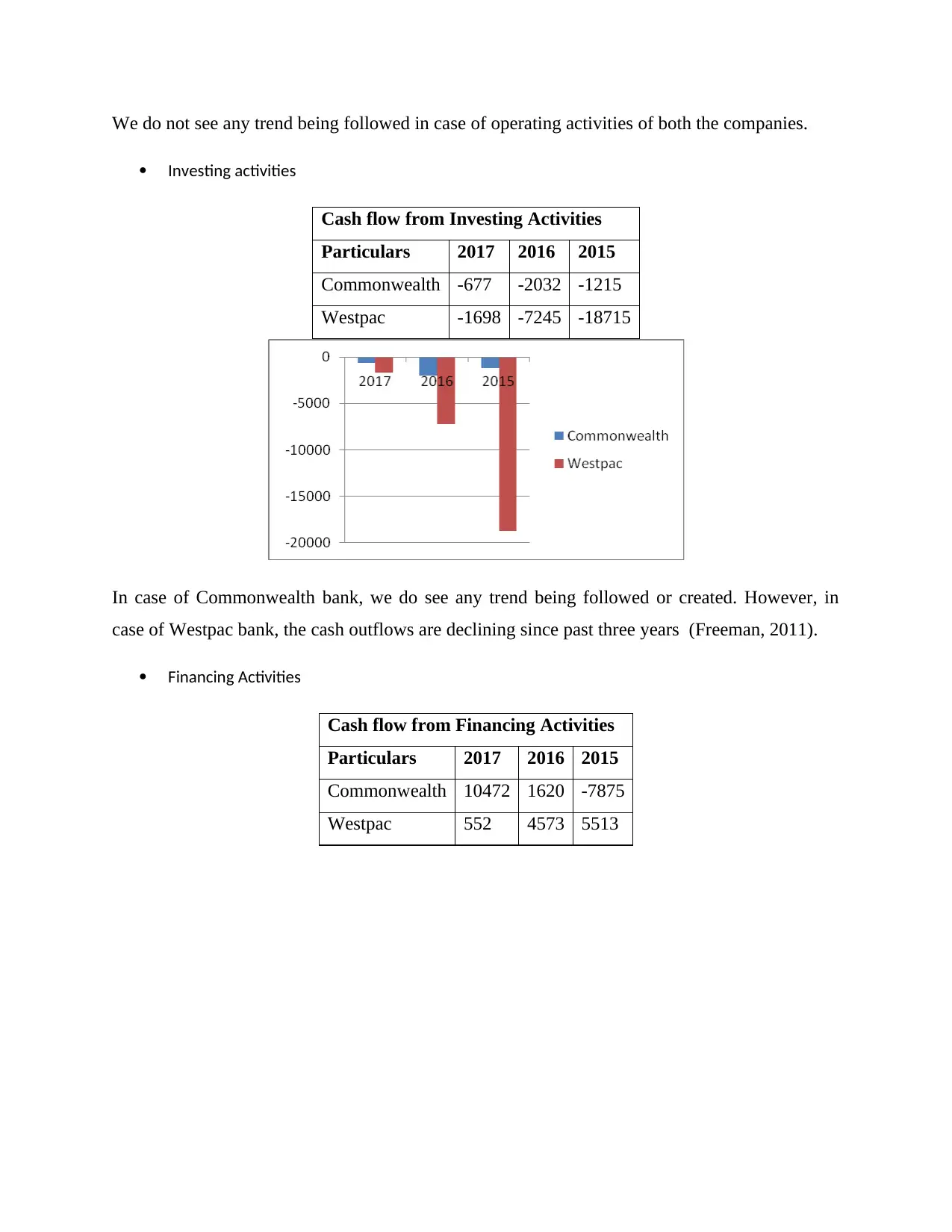

Cash flow from Investing Activities

Particulars 2017 2016 2015

Commonwealth -677 -2032 -1215

Westpac -1698 -7245 -18715

In case of Commonwealth bank, we do see any trend being followed or created. However, in

case of Westpac bank, the cash outflows are declining since past three years (Freeman, 2011).

Financing Activities

Cash flow from Financing Activities

Particulars 2017 2016 2015

Commonwealth 10472 1620 -7875

Westpac 552 4573 5513

Investing activities

Cash flow from Investing Activities

Particulars 2017 2016 2015

Commonwealth -677 -2032 -1215

Westpac -1698 -7245 -18715

In case of Commonwealth bank, we do see any trend being followed or created. However, in

case of Westpac bank, the cash outflows are declining since past three years (Freeman, 2011).

Financing Activities

Cash flow from Financing Activities

Particulars 2017 2016 2015

Commonwealth 10472 1620 -7875

Westpac 552 4573 5513

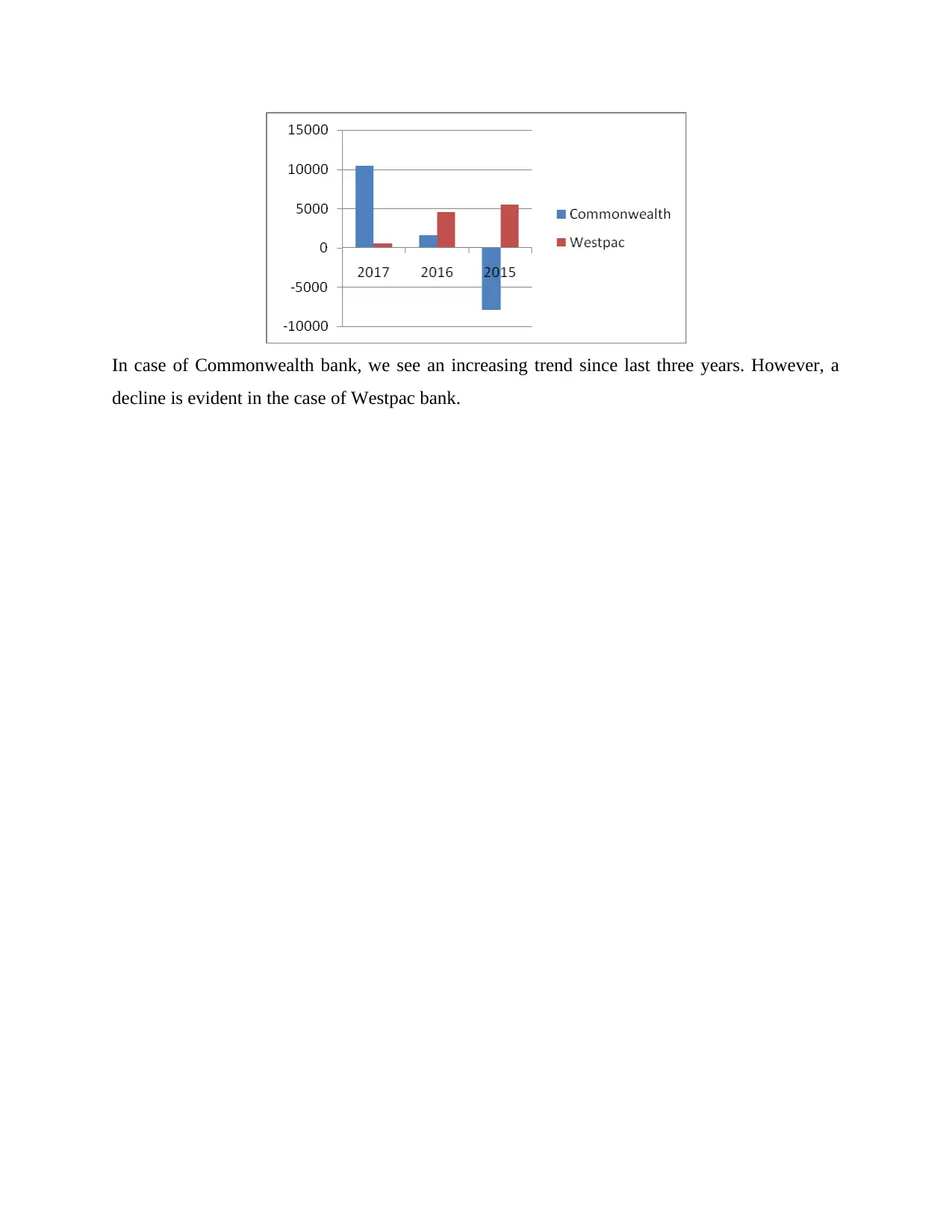

In case of Commonwealth bank, we see an increasing trend since last three years. However, a

decline is evident in the case of Westpac bank.

decline is evident in the case of Westpac bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.