Corporate Accounting Report: Equity, Cash Flow, and Debt Analysis

VerifiedAdded on 2020/11/23

|20

|3613

|350

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting, focusing on the financial statements of two real estate companies, Abacus Property Group and LandMark White Limited. The executive summary highlights the importance of financial statements in understanding a company's equity, debt, and cash flow positions, as well as tax liabilities. The report delves into the equity items, including issued capital, reserves, and retained earnings, and their changes over a three-year period, offering a comparative analysis of the two companies. It also examines the debt-equity ratio and its implications. Furthermore, the report analyzes the cash flow statements, detailing items such as interest received, income tax paid, purchase of investments, and repayment of borrowings. It provides a comparative analysis of operating, investing, and financing activities for both companies over three years, offering insights into their financial performance and management strategies. The report concludes with a comparative analysis of the two companies, summarizing their financial strengths and weaknesses based on the data presented.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report contains information about corporate accounting which is used to create and

analyse the financial statement of a company which can be either a business entity or lawful

business. In this project, description about companies which are selected is mentioned along with

their equity items and cash flow items. It also describes about the importance of financial

statement of a company. By using financial statements one can identify the debt as well as equity

position of the company. It also help in identifying the amount of cash inflow and cash outflows

transactions performed by an organisation throughout the year. Further using financial statement

tax expenses can also be listed which includes current tax liabilities.

This report contains information about corporate accounting which is used to create and

analyse the financial statement of a company which can be either a business entity or lawful

business. In this project, description about companies which are selected is mentioned along with

their equity items and cash flow items. It also describes about the importance of financial

statement of a company. By using financial statements one can identify the debt as well as equity

position of the company. It also help in identifying the amount of cash inflow and cash outflows

transactions performed by an organisation throughout the year. Further using financial statement

tax expenses can also be listed which includes current tax liabilities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate accounting is that branch of accounting which is focused to preparation of

financial statements of companies. These corporations include any business entity which runs a

lawful business. In this project report, two companies are chosen in order to better understand

this topic. These companies are Abacus Property Group and LandMark White Limited. Both of

these companies operates in real estate industry and deals with property construction. In this

project report, annual reports of these two organisations are analysed and interpreted with the

aim of ascertaining their equity and debt position, cash flow performance and taxation position

of the organisation. Financial reports and accounts which are prepared by the accountants of a

company includes income statement, balance sheet and cash flow which are further analysed by

management of the company (Bennett, 2013).

TASK 1: OWNERS EQUITY

Listing equity items and their changes

Owner's equity is the amount of investment which is contributed by the owner in the

business. Owner's equity of an organisation can be ascertained by deducting the total assets from

total liabilities. Changes in equity items is mentioned below of the past three years:

Issued capital – This capital is the amount or value which is obtained through sale of

company's shares. When a company issues shares and earn a amount from it, that value is known

as issued capital (Epstein, 2018). In the case of LandMark White Limited, issued capital is in

increasing trend. In the year of 2015, this capital was amounting 6008000, 6050000 in 2016 and

33773000 dollars in 2017. Reason of this change is fluctuations in the share price and issuance of

shares by the company every year. According to the annual reports of Abacus Property Group,

shares amounting 1581156 issued in the year of 2017, 1523878 in 2016 and 1514015 in 2015.

From this data it can be said that this company is consistent when it comes to share capital

because of issuing a similar number of shares every year.

Reserves – These are the funds which are reserved by the company in order to save them

for future contingencies and plans (Reserves, 2018). The amount in reserves is considered as the

net worth of the organisation which is earned from the sale of shares. In the case of LandMark

White Limited, there are no reserves in the year of 2017. But in the year of 2016 and 2015,

company managed to save a amount in reserves and the value of these reserve were recorded as

1

Corporate accounting is that branch of accounting which is focused to preparation of

financial statements of companies. These corporations include any business entity which runs a

lawful business. In this project report, two companies are chosen in order to better understand

this topic. These companies are Abacus Property Group and LandMark White Limited. Both of

these companies operates in real estate industry and deals with property construction. In this

project report, annual reports of these two organisations are analysed and interpreted with the

aim of ascertaining their equity and debt position, cash flow performance and taxation position

of the organisation. Financial reports and accounts which are prepared by the accountants of a

company includes income statement, balance sheet and cash flow which are further analysed by

management of the company (Bennett, 2013).

TASK 1: OWNERS EQUITY

Listing equity items and their changes

Owner's equity is the amount of investment which is contributed by the owner in the

business. Owner's equity of an organisation can be ascertained by deducting the total assets from

total liabilities. Changes in equity items is mentioned below of the past three years:

Issued capital – This capital is the amount or value which is obtained through sale of

company's shares. When a company issues shares and earn a amount from it, that value is known

as issued capital (Epstein, 2018). In the case of LandMark White Limited, issued capital is in

increasing trend. In the year of 2015, this capital was amounting 6008000, 6050000 in 2016 and

33773000 dollars in 2017. Reason of this change is fluctuations in the share price and issuance of

shares by the company every year. According to the annual reports of Abacus Property Group,

shares amounting 1581156 issued in the year of 2017, 1523878 in 2016 and 1514015 in 2015.

From this data it can be said that this company is consistent when it comes to share capital

because of issuing a similar number of shares every year.

Reserves – These are the funds which are reserved by the company in order to save them

for future contingencies and plans (Reserves, 2018). The amount in reserves is considered as the

net worth of the organisation which is earned from the sale of shares. In the case of LandMark

White Limited, there are no reserves in the year of 2017. But in the year of 2016 and 2015,

company managed to save a amount in reserves and the value of these reserve were recorded as

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

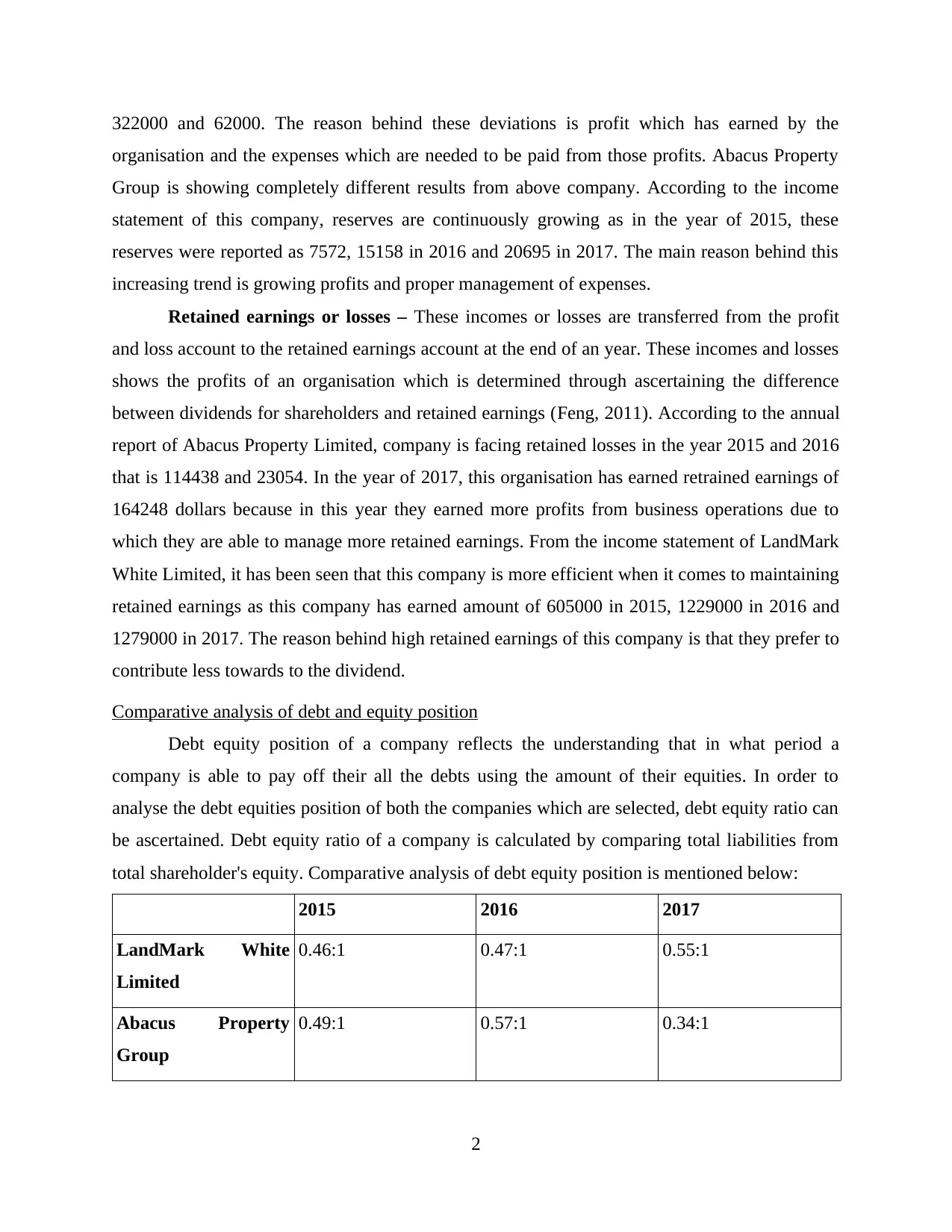

322000 and 62000. The reason behind these deviations is profit which has earned by the

organisation and the expenses which are needed to be paid from those profits. Abacus Property

Group is showing completely different results from above company. According to the income

statement of this company, reserves are continuously growing as in the year of 2015, these

reserves were reported as 7572, 15158 in 2016 and 20695 in 2017. The main reason behind this

increasing trend is growing profits and proper management of expenses.

Retained earnings or losses – These incomes or losses are transferred from the profit

and loss account to the retained earnings account at the end of an year. These incomes and losses

shows the profits of an organisation which is determined through ascertaining the difference

between dividends for shareholders and retained earnings (Feng, 2011). According to the annual

report of Abacus Property Limited, company is facing retained losses in the year 2015 and 2016

that is 114438 and 23054. In the year of 2017, this organisation has earned retrained earnings of

164248 dollars because in this year they earned more profits from business operations due to

which they are able to manage more retained earnings. From the income statement of LandMark

White Limited, it has been seen that this company is more efficient when it comes to maintaining

retained earnings as this company has earned amount of 605000 in 2015, 1229000 in 2016 and

1279000 in 2017. The reason behind high retained earnings of this company is that they prefer to

contribute less towards to the dividend.

Comparative analysis of debt and equity position

Debt equity position of a company reflects the understanding that in what period a

company is able to pay off their all the debts using the amount of their equities. In order to

analyse the debt equities position of both the companies which are selected, debt equity ratio can

be ascertained. Debt equity ratio of a company is calculated by comparing total liabilities from

total shareholder's equity. Comparative analysis of debt equity position is mentioned below:

2015 2016 2017

LandMark White

Limited

0.46:1 0.47:1 0.55:1

Abacus Property

Group

0.49:1 0.57:1 0.34:1

2

organisation and the expenses which are needed to be paid from those profits. Abacus Property

Group is showing completely different results from above company. According to the income

statement of this company, reserves are continuously growing as in the year of 2015, these

reserves were reported as 7572, 15158 in 2016 and 20695 in 2017. The main reason behind this

increasing trend is growing profits and proper management of expenses.

Retained earnings or losses – These incomes or losses are transferred from the profit

and loss account to the retained earnings account at the end of an year. These incomes and losses

shows the profits of an organisation which is determined through ascertaining the difference

between dividends for shareholders and retained earnings (Feng, 2011). According to the annual

report of Abacus Property Limited, company is facing retained losses in the year 2015 and 2016

that is 114438 and 23054. In the year of 2017, this organisation has earned retrained earnings of

164248 dollars because in this year they earned more profits from business operations due to

which they are able to manage more retained earnings. From the income statement of LandMark

White Limited, it has been seen that this company is more efficient when it comes to maintaining

retained earnings as this company has earned amount of 605000 in 2015, 1229000 in 2016 and

1279000 in 2017. The reason behind high retained earnings of this company is that they prefer to

contribute less towards to the dividend.

Comparative analysis of debt and equity position

Debt equity position of a company reflects the understanding that in what period a

company is able to pay off their all the debts using the amount of their equities. In order to

analyse the debt equities position of both the companies which are selected, debt equity ratio can

be ascertained. Debt equity ratio of a company is calculated by comparing total liabilities from

total shareholder's equity. Comparative analysis of debt equity position is mentioned below:

2015 2016 2017

LandMark White

Limited

0.46:1 0.47:1 0.55:1

Abacus Property

Group

0.49:1 0.57:1 0.34:1

2

Ideal debt equity ratio for this industry is considered to be 2:1. By analysing position of

both the companies it has been seen that there is no much difference when it comes to debt

equity ratio. From the point of financial position, it can be said that LandMark White Limited has

better debt equity position than Abacus property group. The reason behind this above statement

is that LandMark White Limited has increasing trend in debt equity ratio that means they are

putting efforts in order to increase their debt equity ratio. On the other hand Abacus property

group has fluctuated debt equity ratio.

TASK 2: CASH FLOW STATEMENTS

Listing items of cash flow statements and their changes

Cash flow statement is a financial statement which has all cash inflows and outflows for

an accounting period (Zadek, 2013). Items present in cash flow statement of both the companies

are mentioned below:

Interest received – This item is included in the operating activities of both the

companies (Fisher, 2012). According to this item, interest is a cash inflow which is needed to be

received by an organisation which are due to from credit amount. From the cash flow statement

of Abacus Property Group, interest valued at 2502000 is received in 2015, 642000 in 2016 and

1329 in 2017. The amount of interest fluctuates due to credit sales amount which is provided by

the company to their debtors. In the case of LandMark White Limited, 21000 was received in

2015, 8000 in 2016 and 15000 in 2017. These deviations are the result of credit sales.

Income tax paid – Income tax is an expense which is required to be paid by an

organisation against the income earned by the company. It is recorded as a cash outflow in the

operating activity of CFS. In the case of LandMark White Limited, liability of income tax was

recorded as 486000 in 2015, 555000 in 2016 and 822000 in 2017. From the CFS of Abacus

Property Group, it has determined that 11122 paid as income tax expense in the year of 2015,

8524 in 2016 and 2944 in 2017. The reason behind the fluctuations in CFS of both the companies

are the value of income which is earned as income tax expense is directly related with income of

a company.

Purchase of investments – This item is a capital expense which is faced by an

organisation when they purchase new investments such as properties, stocks and many more.

These investments helps an organisation to attain profit. Purchase of investments are recorded as

3

both the companies it has been seen that there is no much difference when it comes to debt

equity ratio. From the point of financial position, it can be said that LandMark White Limited has

better debt equity position than Abacus property group. The reason behind this above statement

is that LandMark White Limited has increasing trend in debt equity ratio that means they are

putting efforts in order to increase their debt equity ratio. On the other hand Abacus property

group has fluctuated debt equity ratio.

TASK 2: CASH FLOW STATEMENTS

Listing items of cash flow statements and their changes

Cash flow statement is a financial statement which has all cash inflows and outflows for

an accounting period (Zadek, 2013). Items present in cash flow statement of both the companies

are mentioned below:

Interest received – This item is included in the operating activities of both the

companies (Fisher, 2012). According to this item, interest is a cash inflow which is needed to be

received by an organisation which are due to from credit amount. From the cash flow statement

of Abacus Property Group, interest valued at 2502000 is received in 2015, 642000 in 2016 and

1329 in 2017. The amount of interest fluctuates due to credit sales amount which is provided by

the company to their debtors. In the case of LandMark White Limited, 21000 was received in

2015, 8000 in 2016 and 15000 in 2017. These deviations are the result of credit sales.

Income tax paid – Income tax is an expense which is required to be paid by an

organisation against the income earned by the company. It is recorded as a cash outflow in the

operating activity of CFS. In the case of LandMark White Limited, liability of income tax was

recorded as 486000 in 2015, 555000 in 2016 and 822000 in 2017. From the CFS of Abacus

Property Group, it has determined that 11122 paid as income tax expense in the year of 2015,

8524 in 2016 and 2944 in 2017. The reason behind the fluctuations in CFS of both the companies

are the value of income which is earned as income tax expense is directly related with income of

a company.

Purchase of investments – This item is a capital expense which is faced by an

organisation when they purchase new investments such as properties, stocks and many more.

These investments helps an organisation to attain profit. Purchase of investments are recorded as

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a cash outflow in investing activity. From the CFS of Abacus Property group, it has been

observed that this expense is valued as 210821 in 2015, 158637 in 2016 and 141049 in 2017.

According to the CFS of LandMark White Limited, purchase of investments are valued as

575000 in 2015, 140000 in 2016 and 14215000 in 2017. The reason behind this varied amounts

is fluctuated amount of profit which is available for purchase of investments.

Repayment of borrowings – This item is also a cash outflow but is recorded in

financing activity in CFS (Gallhofer, 2011). The fluctuations in its value over the years is the

result of requirement of additional value which can be used in organisational operations. From

the cash flow statement of Abacus Property Group, it has been observed that this expense is

valued as 238150 in 2015, 43107 in 2016 and 260130 in 2017. Whereas from the annual reports

of LandMark White Limited, it has been seen that there was no such expense in 2015 and 2016

but in 2017, a expense of 7000 was recorded as in this year there were more requirements of

borrowings.

Comparative analysis of activities of cash flow statements

CFS is an accounting statement which reflects all cash inflows and cash outflows which

occurs in a company. These cash flows are classified into operating, investing and financing.

Comparative analysis of these companies on the basis of all three activities is conducted below:

Operating activities Investing activities Financing activity

2015 These activities are the

operations which are

conducted for the normal

course of business. It

includes certain items such

as interest, cash receipts and

many more. From the CFS

of LandMark White Limited,

it has been seen that

company has earned 324000

in 2015. Whereas in the case

of Abacus, these activities

These are the operations

which are conducted by the

company to increase the

value of their amount. In the

case of LandMark White

Limited, this activity has to

bear amount of 788000.

From the CFS of Abacus,

this investing activities

results in major expenses of

31178.

Financing activity are the

operations which are

conducted in order to pay

capital expenses. LandMark

White Limited, has

transacted this expense as

1034000 and Abacus Group

has recorded this expense as

111264.

4

observed that this expense is valued as 210821 in 2015, 158637 in 2016 and 141049 in 2017.

According to the CFS of LandMark White Limited, purchase of investments are valued as

575000 in 2015, 140000 in 2016 and 14215000 in 2017. The reason behind this varied amounts

is fluctuated amount of profit which is available for purchase of investments.

Repayment of borrowings – This item is also a cash outflow but is recorded in

financing activity in CFS (Gallhofer, 2011). The fluctuations in its value over the years is the

result of requirement of additional value which can be used in organisational operations. From

the cash flow statement of Abacus Property Group, it has been observed that this expense is

valued as 238150 in 2015, 43107 in 2016 and 260130 in 2017. Whereas from the annual reports

of LandMark White Limited, it has been seen that there was no such expense in 2015 and 2016

but in 2017, a expense of 7000 was recorded as in this year there were more requirements of

borrowings.

Comparative analysis of activities of cash flow statements

CFS is an accounting statement which reflects all cash inflows and cash outflows which

occurs in a company. These cash flows are classified into operating, investing and financing.

Comparative analysis of these companies on the basis of all three activities is conducted below:

Operating activities Investing activities Financing activity

2015 These activities are the

operations which are

conducted for the normal

course of business. It

includes certain items such

as interest, cash receipts and

many more. From the CFS

of LandMark White Limited,

it has been seen that

company has earned 324000

in 2015. Whereas in the case

of Abacus, these activities

These are the operations

which are conducted by the

company to increase the

value of their amount. In the

case of LandMark White

Limited, this activity has to

bear amount of 788000.

From the CFS of Abacus,

this investing activities

results in major expenses of

31178.

Financing activity are the

operations which are

conducted in order to pay

capital expenses. LandMark

White Limited, has

transacted this expense as

1034000 and Abacus Group

has recorded this expense as

111264.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

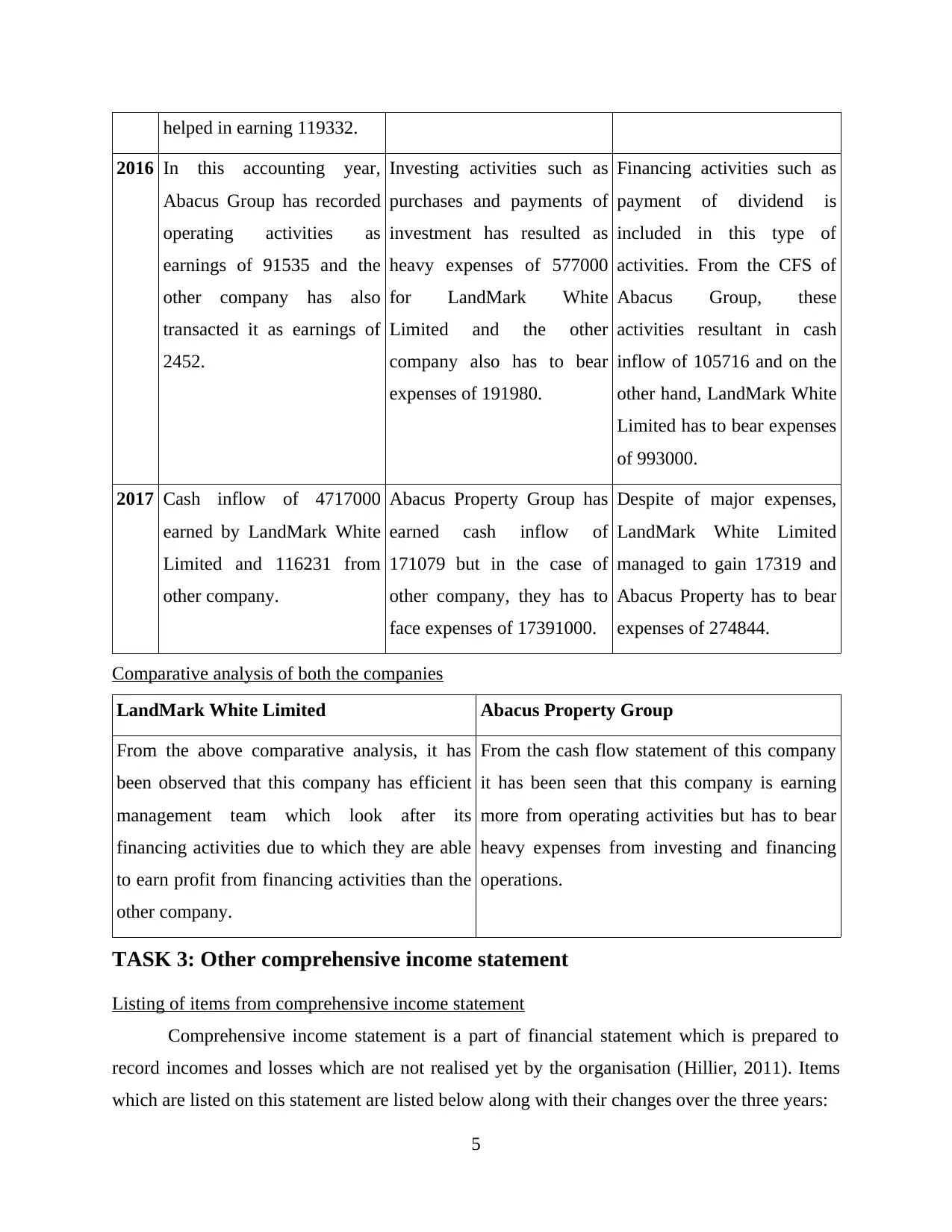

helped in earning 119332.

2016 In this accounting year,

Abacus Group has recorded

operating activities as

earnings of 91535 and the

other company has also

transacted it as earnings of

2452.

Investing activities such as

purchases and payments of

investment has resulted as

heavy expenses of 577000

for LandMark White

Limited and the other

company also has to bear

expenses of 191980.

Financing activities such as

payment of dividend is

included in this type of

activities. From the CFS of

Abacus Group, these

activities resultant in cash

inflow of 105716 and on the

other hand, LandMark White

Limited has to bear expenses

of 993000.

2017 Cash inflow of 4717000

earned by LandMark White

Limited and 116231 from

other company.

Abacus Property Group has

earned cash inflow of

171079 but in the case of

other company, they has to

face expenses of 17391000.

Despite of major expenses,

LandMark White Limited

managed to gain 17319 and

Abacus Property has to bear

expenses of 274844.

Comparative analysis of both the companies

LandMark White Limited Abacus Property Group

From the above comparative analysis, it has

been observed that this company has efficient

management team which look after its

financing activities due to which they are able

to earn profit from financing activities than the

other company.

From the cash flow statement of this company

it has been seen that this company is earning

more from operating activities but has to bear

heavy expenses from investing and financing

operations.

TASK 3: Other comprehensive income statement

Listing of items from comprehensive income statement

Comprehensive income statement is a part of financial statement which is prepared to

record incomes and losses which are not realised yet by the organisation (Hillier, 2011). Items

which are listed on this statement are listed below along with their changes over the three years:

5

2016 In this accounting year,

Abacus Group has recorded

operating activities as

earnings of 91535 and the

other company has also

transacted it as earnings of

2452.

Investing activities such as

purchases and payments of

investment has resulted as

heavy expenses of 577000

for LandMark White

Limited and the other

company also has to bear

expenses of 191980.

Financing activities such as

payment of dividend is

included in this type of

activities. From the CFS of

Abacus Group, these

activities resultant in cash

inflow of 105716 and on the

other hand, LandMark White

Limited has to bear expenses

of 993000.

2017 Cash inflow of 4717000

earned by LandMark White

Limited and 116231 from

other company.

Abacus Property Group has

earned cash inflow of

171079 but in the case of

other company, they has to

face expenses of 17391000.

Despite of major expenses,

LandMark White Limited

managed to gain 17319 and

Abacus Property has to bear

expenses of 274844.

Comparative analysis of both the companies

LandMark White Limited Abacus Property Group

From the above comparative analysis, it has

been observed that this company has efficient

management team which look after its

financing activities due to which they are able

to earn profit from financing activities than the

other company.

From the cash flow statement of this company

it has been seen that this company is earning

more from operating activities but has to bear

heavy expenses from investing and financing

operations.

TASK 3: Other comprehensive income statement

Listing of items from comprehensive income statement

Comprehensive income statement is a part of financial statement which is prepared to

record incomes and losses which are not realised yet by the organisation (Hillier, 2011). Items

which are listed on this statement are listed below along with their changes over the three years:

5

Comprehensive income – After evaluating annual reports items of comprehensive

income statement are mentioned below of both the companies. The only item which is

mentioned in the comprehensive income statements is net comprehensive income of an year.

After analysing comprehensive statement of LandMark White Limited, it has been seen that in

the year of 2015, comprehensive income of 779000 is received. 1659000 in 2016 and 1626000 in

2017 is received. The reason behind the fluctuations of this amount is increase in the value of

non realised income.

From the comprehensive statement of Abacus property Group, it has been analysed that

this company has also a considerable amount of comprehensive income. Total comprehensive

income determined from revaluation of assets and foreign exchange translation adjustment items

in the year of 2015 is 130079, 201567 in 2016 and 302611 in 2017. The reason behind the

variations in the amount of comprehensive income is the fluctuations in the income which is

earned by realising the assets and revaluation of assets.

Rationale of comprehensive income statement

Comprehensive income statement refers to a accounting statement which has items which

are not realised by the company yet. These items are unrealized which generally holds losses or

gains for available security over its sales. The items of comprehensive income statement are

generally not included in income statement of a company as it includes items which are not exist

in real. This statement includes various items such as derivatives, foreign currency, pension plan

etc. These items are based on assumptions, therefore they are not beneficial for company (Jones,

2011).

Comparative analysis

LandMark White Limited Abacus Property Group

From the comprehensive income statement of

this company it has been analysed that a huge

amount is received from this statement which

is more than the other company. The reason

behind ample of this amount is huge value of

non realisable assets.

In the case of this organisation, there is less but

considerable amount is earned from the

comprehensive income statement. This amount

is earned due to revaluation of their capital

assets.

6

income statement are mentioned below of both the companies. The only item which is

mentioned in the comprehensive income statements is net comprehensive income of an year.

After analysing comprehensive statement of LandMark White Limited, it has been seen that in

the year of 2015, comprehensive income of 779000 is received. 1659000 in 2016 and 1626000 in

2017 is received. The reason behind the fluctuations of this amount is increase in the value of

non realised income.

From the comprehensive statement of Abacus property Group, it has been analysed that

this company has also a considerable amount of comprehensive income. Total comprehensive

income determined from revaluation of assets and foreign exchange translation adjustment items

in the year of 2015 is 130079, 201567 in 2016 and 302611 in 2017. The reason behind the

variations in the amount of comprehensive income is the fluctuations in the income which is

earned by realising the assets and revaluation of assets.

Rationale of comprehensive income statement

Comprehensive income statement refers to a accounting statement which has items which

are not realised by the company yet. These items are unrealized which generally holds losses or

gains for available security over its sales. The items of comprehensive income statement are

generally not included in income statement of a company as it includes items which are not exist

in real. This statement includes various items such as derivatives, foreign currency, pension plan

etc. These items are based on assumptions, therefore they are not beneficial for company (Jones,

2011).

Comparative analysis

LandMark White Limited Abacus Property Group

From the comprehensive income statement of

this company it has been analysed that a huge

amount is received from this statement which

is more than the other company. The reason

behind ample of this amount is huge value of

non realisable assets.

In the case of this organisation, there is less but

considerable amount is earned from the

comprehensive income statement. This amount

is earned due to revaluation of their capital

assets.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above comparative analyses, it has been evaluated that if comprehensive

statement income is mentioned in typical income statement, then the value of profit attributable

will be increased which can reflect misstatements in the financial reporting of an organisation.

Evaluation

Managers of the company are their personnel assets which helps in achieving the

organisational objectives such as profit maximisation. Amount which is mentioned in

comprehensive income statement is not reflecting any usual incomes but the incomes which are

not realised by the organisation yet. This items are recorded and reported in annual report as

these items helps in evaluating performance of managers and management. Main aim behind

including these incomes and expenditures in the form of comprehensive income statement is to

determine efficiency of management and its employees.

TASK 4: Accounting for corporate income tax

Listing tax expenses from financial statements

Tax expenses of an organisation includes current tax liabilities (Kim, 2012). From the

income statement of LandMark White Limited current tax liabilities which are recorded valued

as 159000 in 2015, 397000 in 2016 and 1367000 in 2017. These tax liabilities are the income tax

expenses which are needed to be paid by an organisation. These expenses are directly related

with the income of the company.

From the income statement of Abacus Property Group, it has been observed that this

company has gained income tax rebate of 1684000 in 2016. Besides this year, they has paid

income tax expense amounting 6644000 in 2015 and 10140 in 2016. The reason behind earning

the rebate for income tax in the year of 2016 is payment of advance income tax.

Calculation of effective tax rate

Effective tax rate is the rate which should be adopt by an organisation so that they can

pay their tax liability effectively (Leventis, , 2013). The rate which is ascertained can be

calculated by comparing total income and tax expense which is incurred by the company. This

determination is mentioned below:

7

statement income is mentioned in typical income statement, then the value of profit attributable

will be increased which can reflect misstatements in the financial reporting of an organisation.

Evaluation

Managers of the company are their personnel assets which helps in achieving the

organisational objectives such as profit maximisation. Amount which is mentioned in

comprehensive income statement is not reflecting any usual incomes but the incomes which are

not realised by the organisation yet. This items are recorded and reported in annual report as

these items helps in evaluating performance of managers and management. Main aim behind

including these incomes and expenditures in the form of comprehensive income statement is to

determine efficiency of management and its employees.

TASK 4: Accounting for corporate income tax

Listing tax expenses from financial statements

Tax expenses of an organisation includes current tax liabilities (Kim, 2012). From the

income statement of LandMark White Limited current tax liabilities which are recorded valued

as 159000 in 2015, 397000 in 2016 and 1367000 in 2017. These tax liabilities are the income tax

expenses which are needed to be paid by an organisation. These expenses are directly related

with the income of the company.

From the income statement of Abacus Property Group, it has been observed that this

company has gained income tax rebate of 1684000 in 2016. Besides this year, they has paid

income tax expense amounting 6644000 in 2015 and 10140 in 2016. The reason behind earning

the rebate for income tax in the year of 2016 is payment of advance income tax.

Calculation of effective tax rate

Effective tax rate is the rate which should be adopt by an organisation so that they can

pay their tax liability effectively (Leventis, , 2013). The rate which is ascertained can be

calculated by comparing total income and tax expense which is incurred by the company. This

determination is mentioned below:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

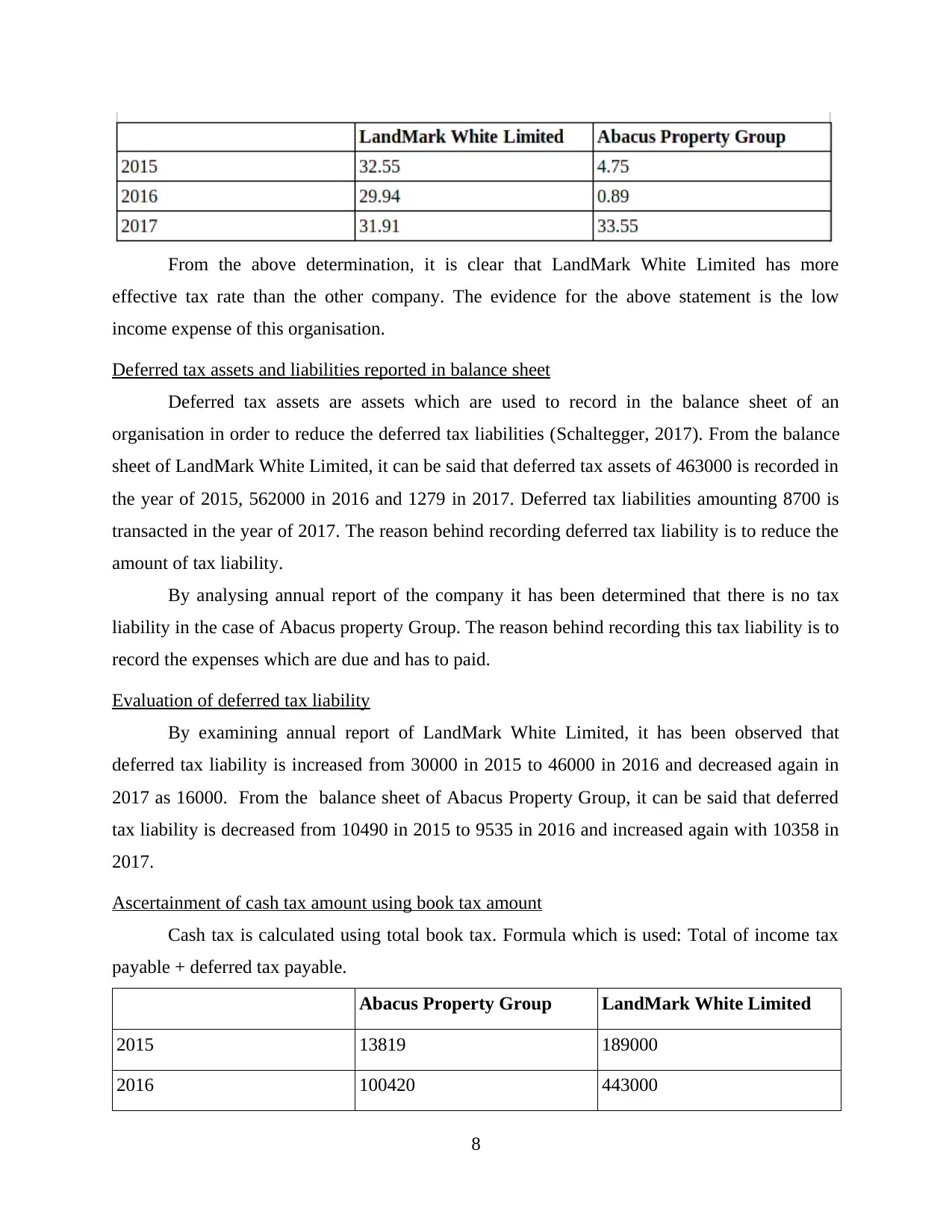

From the above determination, it is clear that LandMark White Limited has more

effective tax rate than the other company. The evidence for the above statement is the low

income expense of this organisation.

Deferred tax assets and liabilities reported in balance sheet

Deferred tax assets are assets which are used to record in the balance sheet of an

organisation in order to reduce the deferred tax liabilities (Schaltegger, 2017). From the balance

sheet of LandMark White Limited, it can be said that deferred tax assets of 463000 is recorded in

the year of 2015, 562000 in 2016 and 1279 in 2017. Deferred tax liabilities amounting 8700 is

transacted in the year of 2017. The reason behind recording deferred tax liability is to reduce the

amount of tax liability.

By analysing annual report of the company it has been determined that there is no tax

liability in the case of Abacus property Group. The reason behind recording this tax liability is to

record the expenses which are due and has to paid.

Evaluation of deferred tax liability

By examining annual report of LandMark White Limited, it has been observed that

deferred tax liability is increased from 30000 in 2015 to 46000 in 2016 and decreased again in

2017 as 16000. From the balance sheet of Abacus Property Group, it can be said that deferred

tax liability is decreased from 10490 in 2015 to 9535 in 2016 and increased again with 10358 in

2017.

Ascertainment of cash tax amount using book tax amount

Cash tax is calculated using total book tax. Formula which is used: Total of income tax

payable + deferred tax payable.

Abacus Property Group LandMark White Limited

2015 13819 189000

2016 100420 443000

8

effective tax rate than the other company. The evidence for the above statement is the low

income expense of this organisation.

Deferred tax assets and liabilities reported in balance sheet

Deferred tax assets are assets which are used to record in the balance sheet of an

organisation in order to reduce the deferred tax liabilities (Schaltegger, 2017). From the balance

sheet of LandMark White Limited, it can be said that deferred tax assets of 463000 is recorded in

the year of 2015, 562000 in 2016 and 1279 in 2017. Deferred tax liabilities amounting 8700 is

transacted in the year of 2017. The reason behind recording deferred tax liability is to reduce the

amount of tax liability.

By analysing annual report of the company it has been determined that there is no tax

liability in the case of Abacus property Group. The reason behind recording this tax liability is to

record the expenses which are due and has to paid.

Evaluation of deferred tax liability

By examining annual report of LandMark White Limited, it has been observed that

deferred tax liability is increased from 30000 in 2015 to 46000 in 2016 and decreased again in

2017 as 16000. From the balance sheet of Abacus Property Group, it can be said that deferred

tax liability is decreased from 10490 in 2015 to 9535 in 2016 and increased again with 10358 in

2017.

Ascertainment of cash tax amount using book tax amount

Cash tax is calculated using total book tax. Formula which is used: Total of income tax

payable + deferred tax payable.

Abacus Property Group LandMark White Limited

2015 13819 189000

2016 100420 443000

8

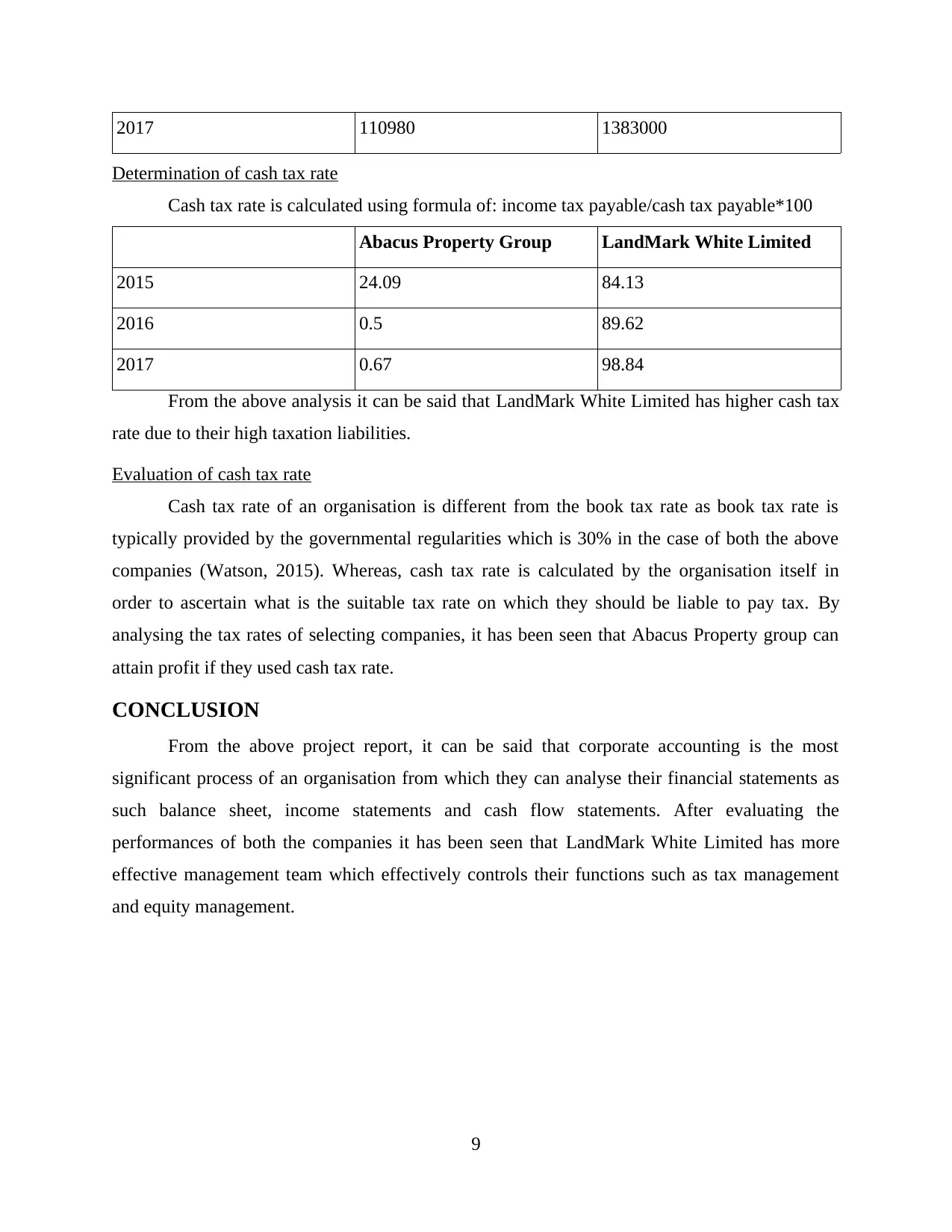

2017 110980 1383000

Determination of cash tax rate

Cash tax rate is calculated using formula of: income tax payable/cash tax payable*100

Abacus Property Group LandMark White Limited

2015 24.09 84.13

2016 0.5 89.62

2017 0.67 98.84

From the above analysis it can be said that LandMark White Limited has higher cash tax

rate due to their high taxation liabilities.

Evaluation of cash tax rate

Cash tax rate of an organisation is different from the book tax rate as book tax rate is

typically provided by the governmental regularities which is 30% in the case of both the above

companies (Watson, 2015). Whereas, cash tax rate is calculated by the organisation itself in

order to ascertain what is the suitable tax rate on which they should be liable to pay tax. By

analysing the tax rates of selecting companies, it has been seen that Abacus Property group can

attain profit if they used cash tax rate.

CONCLUSION

From the above project report, it can be said that corporate accounting is the most

significant process of an organisation from which they can analyse their financial statements as

such balance sheet, income statements and cash flow statements. After evaluating the

performances of both the companies it has been seen that LandMark White Limited has more

effective management team which effectively controls their functions such as tax management

and equity management.

9

Determination of cash tax rate

Cash tax rate is calculated using formula of: income tax payable/cash tax payable*100

Abacus Property Group LandMark White Limited

2015 24.09 84.13

2016 0.5 89.62

2017 0.67 98.84

From the above analysis it can be said that LandMark White Limited has higher cash tax

rate due to their high taxation liabilities.

Evaluation of cash tax rate

Cash tax rate of an organisation is different from the book tax rate as book tax rate is

typically provided by the governmental regularities which is 30% in the case of both the above

companies (Watson, 2015). Whereas, cash tax rate is calculated by the organisation itself in

order to ascertain what is the suitable tax rate on which they should be liable to pay tax. By

analysing the tax rates of selecting companies, it has been seen that Abacus Property group can

attain profit if they used cash tax rate.

CONCLUSION

From the above project report, it can be said that corporate accounting is the most

significant process of an organisation from which they can analyse their financial statements as

such balance sheet, income statements and cash flow statements. After evaluating the

performances of both the companies it has been seen that LandMark White Limited has more

effective management team which effectively controls their functions such as tax management

and equity management.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.