Corporate Accounting Analysis: AMA Group vs. Adairs Limited

VerifiedAdded on 2021/01/02

|18

|4698

|388

Report

AI Summary

This report provides a detailed analysis of corporate accounting practices, focusing on two companies in the retailing industry: AMA Group Limited and Adairs Limited. The report begins with an examination of owners' equity, including a comparative analysis of the capital structure and changes in equity components over time. It then delves into the cash flow statements of both companies, comparing operating, investing, and financing activities, along with their respective changes. The analysis extends to the other comprehensive income (OCI) statements, exploring the items included, reasons for their exclusion from the income statement, and their significance in performance evaluation. Finally, the report addresses accounting for corporate income tax, covering effective tax rates, deferred tax assets and liabilities, cash tax rates, and the differences between cash and book tax rates, providing a comprehensive overview of the financial performance and accounting practices of the selected companies.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Corporate accounting helps for specific events of organization such as absorption,

amalgamation and preparation of consolidated financial statements. The present report had

considered retailing industry as AMA Group Limited and Adairs Limited with its different

elements of corporate accounting. Initially, it will discuss about owner's equity and comparative

analysis of capital structure of both selected organizations. In the similar aspect, it has shown

importance of other comprehensive income which are necessary for performance evaluation.

Further, it is conculded by stating effective tax rate and difference among cash and book tax rate.

Corporate accounting helps for specific events of organization such as absorption,

amalgamation and preparation of consolidated financial statements. The present report had

considered retailing industry as AMA Group Limited and Adairs Limited with its different

elements of corporate accounting. Initially, it will discuss about owner's equity and comparative

analysis of capital structure of both selected organizations. In the similar aspect, it has shown

importance of other comprehensive income which are necessary for performance evaluation.

Further, it is conculded by stating effective tax rate and difference among cash and book tax rate.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

OWNERS EQUITY.........................................................................................................................1

1. Presenting each item of equity with its changes from past years............................................1

2. Presenting debt equity position of both organizations............................................................2

CASH FLOW STATEMENT..........................................................................................................4

3.Presenting items of Cash flow with its changes from past year...............................................4

4. Presenting comparative analysis of broad categories of cash flow.........................................5

5. Presenting insights about comparative analysis of both companies.......................................6

OTHER COMPREHENSIVE INCOME STATEMENT................................................................7

6. Presenting items related to other comprehensive income statement.......................................7

7. Presenting reason for not stating these items in income statement ........................................7

8. Presenting comparative analysis of other comprehensive income statements........................7

9. Presenting importance of OCI in performance evaluation......................................................9

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................9

10. Represent tax expenses in the latest financial statements of both companies.......................9

11. Presenting effective tax rate................................................................................................10

12. Interpreting deferred tax assets and liabilities with reference of balance sheet..................10

13. Presenting change in deferred tax asset and liability..........................................................10

14. Presenting cash tax amount with application of book tax, DTA and DTL.........................11

15. Presenting cash tax rate.......................................................................................................12

16. Presenting difference between cash tax and book tax rate..................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

OWNERS EQUITY.........................................................................................................................1

1. Presenting each item of equity with its changes from past years............................................1

2. Presenting debt equity position of both organizations............................................................2

CASH FLOW STATEMENT..........................................................................................................4

3.Presenting items of Cash flow with its changes from past year...............................................4

4. Presenting comparative analysis of broad categories of cash flow.........................................5

5. Presenting insights about comparative analysis of both companies.......................................6

OTHER COMPREHENSIVE INCOME STATEMENT................................................................7

6. Presenting items related to other comprehensive income statement.......................................7

7. Presenting reason for not stating these items in income statement ........................................7

8. Presenting comparative analysis of other comprehensive income statements........................7

9. Presenting importance of OCI in performance evaluation......................................................9

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................9

10. Represent tax expenses in the latest financial statements of both companies.......................9

11. Presenting effective tax rate................................................................................................10

12. Interpreting deferred tax assets and liabilities with reference of balance sheet..................10

13. Presenting change in deferred tax asset and liability..........................................................10

14. Presenting cash tax amount with application of book tax, DTA and DTL.........................11

15. Presenting cash tax rate.......................................................................................................12

16. Presenting difference between cash tax and book tax rate..................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate accounting is a specialised accounting branch which deals with business entity

for preparing cash flow and financial statements, accounting with appropriate interpretation and

analysis of its outcomes. It also provides help for particular events such as absorption,

amalgamation and preparation of consolidated financial statements. The present report will

discuss about retailing industry as AMA Group Limited and Adairs Limited on basis of different

components of corporate accounting. Initially, it will articulate about owner's equity and

comparative analysis of debt equity position of both selected organizations. In the same series, it

will show comparative analysis of cash flow statement with each item and alterations from past

three consecutive years. This report will discuss about other comprehensive income statements

(OCI) and items which are included in this statement. In this context, movements from year 2015

to 2017 will be discussed and reasons for not including items of OCI in profit and loss account.

Further, this report will present accounting for corporate income tax which consists of effective

tax rate, cash tax rate and book tax rate with its differences.

OWNERS EQUITY

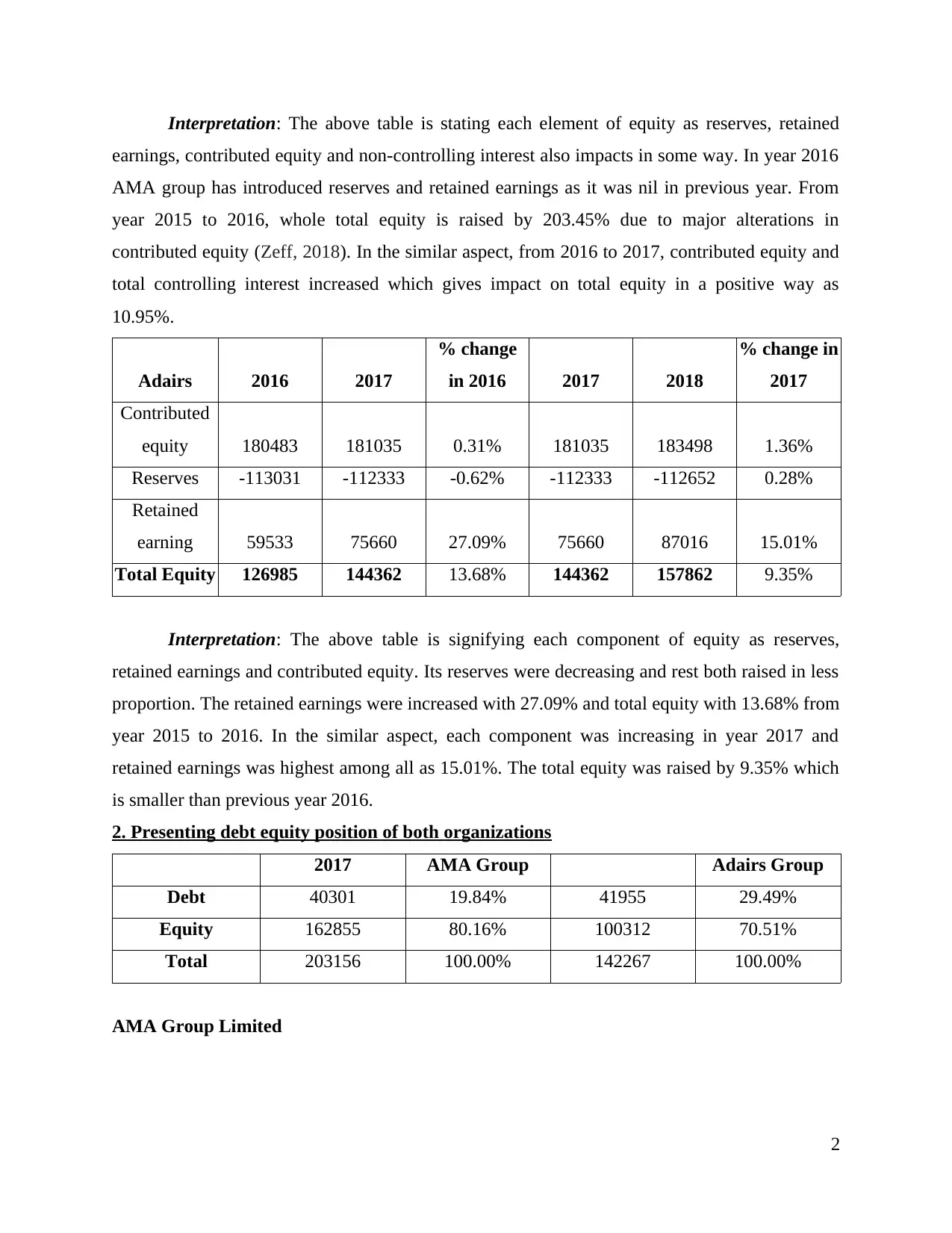

1. Presenting each item of equity with its changes from past years

AMA Group Limited

2015 2016

% change

in 2016 2016 2017

% change in

2017

Contributed

equity 74904 172149 129.83% 172149 181691 5.54%

Reserves 0 3059 0.00% 3059 3054 -0.16%

Retained

earning -26534 -28626 7.88% -28626 -22122 -22.72%

Total Group

Interest 48370 146582 203.04% 146582 162623 10.94%

Non-

Controlling

interest 0 197 0.00% 197 232 17.77%

Total Equity 48370 146779 203.45% 146779 162855 10.95%

1

Corporate accounting is a specialised accounting branch which deals with business entity

for preparing cash flow and financial statements, accounting with appropriate interpretation and

analysis of its outcomes. It also provides help for particular events such as absorption,

amalgamation and preparation of consolidated financial statements. The present report will

discuss about retailing industry as AMA Group Limited and Adairs Limited on basis of different

components of corporate accounting. Initially, it will articulate about owner's equity and

comparative analysis of debt equity position of both selected organizations. In the same series, it

will show comparative analysis of cash flow statement with each item and alterations from past

three consecutive years. This report will discuss about other comprehensive income statements

(OCI) and items which are included in this statement. In this context, movements from year 2015

to 2017 will be discussed and reasons for not including items of OCI in profit and loss account.

Further, this report will present accounting for corporate income tax which consists of effective

tax rate, cash tax rate and book tax rate with its differences.

OWNERS EQUITY

1. Presenting each item of equity with its changes from past years

AMA Group Limited

2015 2016

% change

in 2016 2016 2017

% change in

2017

Contributed

equity 74904 172149 129.83% 172149 181691 5.54%

Reserves 0 3059 0.00% 3059 3054 -0.16%

Retained

earning -26534 -28626 7.88% -28626 -22122 -22.72%

Total Group

Interest 48370 146582 203.04% 146582 162623 10.94%

Non-

Controlling

interest 0 197 0.00% 197 232 17.77%

Total Equity 48370 146779 203.45% 146779 162855 10.95%

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: The above table is stating each element of equity as reserves, retained

earnings, contributed equity and non-controlling interest also impacts in some way. In year 2016

AMA group has introduced reserves and retained earnings as it was nil in previous year. From

year 2015 to 2016, whole total equity is raised by 203.45% due to major alterations in

contributed equity (Zeff, 2018). In the similar aspect, from 2016 to 2017, contributed equity and

total controlling interest increased which gives impact on total equity in a positive way as

10.95%.

Adairs 2016 2017

% change

in 2016 2017 2018

% change in

2017

Contributed

equity 180483 181035 0.31% 181035 183498 1.36%

Reserves -113031 -112333 -0.62% -112333 -112652 0.28%

Retained

earning 59533 75660 27.09% 75660 87016 15.01%

Total Equity 126985 144362 13.68% 144362 157862 9.35%

Interpretation: The above table is signifying each component of equity as reserves,

retained earnings and contributed equity. Its reserves were decreasing and rest both raised in less

proportion. The retained earnings were increased with 27.09% and total equity with 13.68% from

year 2015 to 2016. In the similar aspect, each component was increasing in year 2017 and

retained earnings was highest among all as 15.01%. The total equity was raised by 9.35% which

is smaller than previous year 2016.

2. Presenting debt equity position of both organizations

2017 AMA Group Adairs Group

Debt 40301 19.84% 41955 29.49%

Equity 162855 80.16% 100312 70.51%

Total 203156 100.00% 142267 100.00%

AMA Group Limited

2

earnings, contributed equity and non-controlling interest also impacts in some way. In year 2016

AMA group has introduced reserves and retained earnings as it was nil in previous year. From

year 2015 to 2016, whole total equity is raised by 203.45% due to major alterations in

contributed equity (Zeff, 2018). In the similar aspect, from 2016 to 2017, contributed equity and

total controlling interest increased which gives impact on total equity in a positive way as

10.95%.

Adairs 2016 2017

% change

in 2016 2017 2018

% change in

2017

Contributed

equity 180483 181035 0.31% 181035 183498 1.36%

Reserves -113031 -112333 -0.62% -112333 -112652 0.28%

Retained

earning 59533 75660 27.09% 75660 87016 15.01%

Total Equity 126985 144362 13.68% 144362 157862 9.35%

Interpretation: The above table is signifying each component of equity as reserves,

retained earnings and contributed equity. Its reserves were decreasing and rest both raised in less

proportion. The retained earnings were increased with 27.09% and total equity with 13.68% from

year 2015 to 2016. In the similar aspect, each component was increasing in year 2017 and

retained earnings was highest among all as 15.01%. The total equity was raised by 9.35% which

is smaller than previous year 2016.

2. Presenting debt equity position of both organizations

2017 AMA Group Adairs Group

Debt 40301 19.84% 41955 29.49%

Equity 162855 80.16% 100312 70.51%

Total 203156 100.00% 142267 100.00%

AMA Group Limited

2

19.84%

80.16%

Debt

Equity

Interpretation: The above pie chart is depicting capital structure of AMA Group Limited

as it is highly financing through equity. The optimal capital structure of every firm is of 40:60

but this organization is not matching with this as it has debt of 19.84% and equity of 80.16%.

Adairs Limited

29.49%

70.51%

Debt

Equity

3

80.16%

Debt

Equity

Interpretation: The above pie chart is depicting capital structure of AMA Group Limited

as it is highly financing through equity. The optimal capital structure of every firm is of 40:60

but this organization is not matching with this as it has debt of 19.84% and equity of 80.16%.

Adairs Limited

29.49%

70.51%

Debt

Equity

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

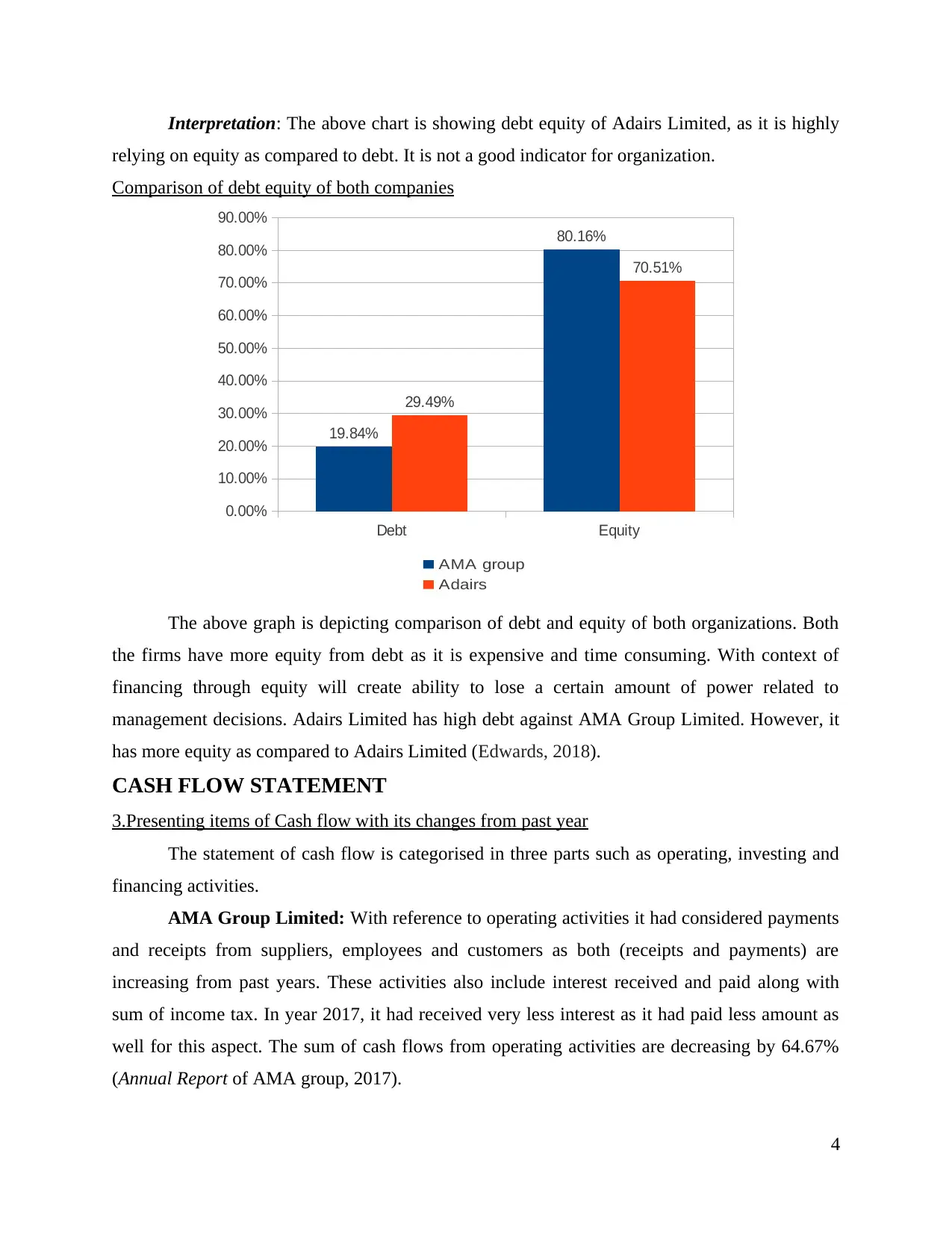

Interpretation: The above chart is showing debt equity of Adairs Limited, as it is highly

relying on equity as compared to debt. It is not a good indicator for organization.

Comparison of debt equity of both companies

Debt Equity

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

19.84%

80.16%

29.49%

70.51%

AMA group

Adairs

The above graph is depicting comparison of debt and equity of both organizations. Both

the firms have more equity from debt as it is expensive and time consuming. With context of

financing through equity will create ability to lose a certain amount of power related to

management decisions. Adairs Limited has high debt against AMA Group Limited. However, it

has more equity as compared to Adairs Limited (Edwards, 2018).

CASH FLOW STATEMENT

3.Presenting items of Cash flow with its changes from past year

The statement of cash flow is categorised in three parts such as operating, investing and

financing activities.

AMA Group Limited: With reference to operating activities it had considered payments

and receipts from suppliers, employees and customers as both (receipts and payments) are

increasing from past years. These activities also include interest received and paid along with

sum of income tax. In year 2017, it had received very less interest as it had paid less amount as

well for this aspect. The sum of cash flows from operating activities are decreasing by 64.67%

(Annual Report of AMA group, 2017).

4

relying on equity as compared to debt. It is not a good indicator for organization.

Comparison of debt equity of both companies

Debt Equity

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

19.84%

80.16%

29.49%

70.51%

AMA group

Adairs

The above graph is depicting comparison of debt and equity of both organizations. Both

the firms have more equity from debt as it is expensive and time consuming. With context of

financing through equity will create ability to lose a certain amount of power related to

management decisions. Adairs Limited has high debt against AMA Group Limited. However, it

has more equity as compared to Adairs Limited (Edwards, 2018).

CASH FLOW STATEMENT

3.Presenting items of Cash flow with its changes from past year

The statement of cash flow is categorised in three parts such as operating, investing and

financing activities.

AMA Group Limited: With reference to operating activities it had considered payments

and receipts from suppliers, employees and customers as both (receipts and payments) are

increasing from past years. These activities also include interest received and paid along with

sum of income tax. In year 2017, it had received very less interest as it had paid less amount as

well for this aspect. The sum of cash flows from operating activities are decreasing by 64.67%

(Annual Report of AMA group, 2017).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The cash used with context of investing activity reduced by 40.62% because of ridding

proceeds from business disposals and payments for intangible assets. These elements has not

given major impact on this variation as payments for purchasing equipment, property and plant

increased. It has huge reduction in amount for acquiring business. In the similar aspect, loans

from other investments remained positive in 2016 and vice versa in 2017.

The last category of cash flow is financing activity which plays important role in this

statement, as equity was raising in year 2016 but in 2017 it was NIL. The proceeds from

borrowing is increased in a high proportion and its repayments decreased massively. It has also

considered payments of dividend to its shareholders along with non-controlling shareholders.

Aggregately it was reduced by 93.02% from year 2016 to 2017.

Adairs Limited: The operating activity of this organization is increasing with 15.87%

because of positive change in receipts and payments to suppliers, customers and employees. The

major impact was due to increment in income tax payment from previous year. Simultaneously,

it had fully ridden payment of IPO transaction cost (Annual Report of Adairs, 2017).

In this organization, cash used with context of investing activity is only related to plant,

equipment and property's acquisition which is increasing from year 2016 to 2017 by 9.74%.

With context of financing activity, it had introduced payments of borrowing cost in year

2017 which was NIL in 2016. Further, Adairs Limited had paid approx. double dividend in

present year. The sum of both are giving more than 100% change in 2017.

4. Presenting comparative analysis of broad categories of cash flow

AMA Group Limited

2015 (base

year) 2016 %

2016 (base

year) 2017 %

Cash flow

from

operating

activity 7820 36761 370.09% 36761 12987 -64.67%

Cash flow

from

investing

10693 38207 257.31% 38207 22687 -40.62%

5

proceeds from business disposals and payments for intangible assets. These elements has not

given major impact on this variation as payments for purchasing equipment, property and plant

increased. It has huge reduction in amount for acquiring business. In the similar aspect, loans

from other investments remained positive in 2016 and vice versa in 2017.

The last category of cash flow is financing activity which plays important role in this

statement, as equity was raising in year 2016 but in 2017 it was NIL. The proceeds from

borrowing is increased in a high proportion and its repayments decreased massively. It has also

considered payments of dividend to its shareholders along with non-controlling shareholders.

Aggregately it was reduced by 93.02% from year 2016 to 2017.

Adairs Limited: The operating activity of this organization is increasing with 15.87%

because of positive change in receipts and payments to suppliers, customers and employees. The

major impact was due to increment in income tax payment from previous year. Simultaneously,

it had fully ridden payment of IPO transaction cost (Annual Report of Adairs, 2017).

In this organization, cash used with context of investing activity is only related to plant,

equipment and property's acquisition which is increasing from year 2016 to 2017 by 9.74%.

With context of financing activity, it had introduced payments of borrowing cost in year

2017 which was NIL in 2016. Further, Adairs Limited had paid approx. double dividend in

present year. The sum of both are giving more than 100% change in 2017.

4. Presenting comparative analysis of broad categories of cash flow

AMA Group Limited

2015 (base

year) 2016 %

2016 (base

year) 2017 %

Cash flow

from

operating

activity 7820 36761 370.09% 36761 12987 -64.67%

Cash flow

from

investing

10693 38207 257.31% 38207 22687 -40.62%

5

activity

Cash flow

from

financing

activity 2972 22126 644.48% 22126 1545 -93.02%

Adairs Limited

2015 (base

year) 2016 %

2016 (base

year) 2017 %

Cash flow

from

operating

activity 31952 23857 -25.33% 23857 27644 15.87%

Cash flow

from

investing

activity 15296 10324 -32.51% 10324 11330 9.74%

Cash flow

from

financing

activity 31596 8294 -73.75% 8294 16677 101.07%

5. Presenting insights about comparative analysis of both companies

Particulars % 2016 (AMA) % 2016 (Adairs) % 2017 (AMA) % 2017 (Adairs)

Cash flow from

operating activity 370.09% -25.33% -64.67% 15.87%

Cash flow from

investing activity 257.31% -32.51% -40.62% 9.74%

Cash flow from

financing activity 644.48% -73.75% -93.02% 101.07%

6

Cash flow

from

financing

activity 2972 22126 644.48% 22126 1545 -93.02%

Adairs Limited

2015 (base

year) 2016 %

2016 (base

year) 2017 %

Cash flow

from

operating

activity 31952 23857 -25.33% 23857 27644 15.87%

Cash flow

from

investing

activity 15296 10324 -32.51% 10324 11330 9.74%

Cash flow

from

financing

activity 31596 8294 -73.75% 8294 16677 101.07%

5. Presenting insights about comparative analysis of both companies

Particulars % 2016 (AMA) % 2016 (Adairs) % 2017 (AMA) % 2017 (Adairs)

Cash flow from

operating activity 370.09% -25.33% -64.67% 15.87%

Cash flow from

investing activity 257.31% -32.51% -40.62% 9.74%

Cash flow from

financing activity 644.48% -73.75% -93.02% 101.07%

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: The above table is providing comparison among each category of cash

flow with both organizations. In year 2016, each category was increased by huge proportion in

AMA Group Limited. However, all categories of cash flow are decreasing by small proportion as

compared to AMA Group Limited in Adairs Limited. In the year 2017, situation was contrasting

previous year. Each activity was decreasing in AMA Limited and vice versa in Adairs Limited.

OTHER COMPREHENSIVE INCOME STATEMENT

6. Presenting items related to other comprehensive income statement (OCI)

AMA Group Limited: The items are categorised to profit OCI such as exchange

differences on translation of foreign operation (Annual Report of AMA group, 2016).

Adairs Limited: It has presence of items which are reclassified subsequently to loss or

profit which are movement with context of cash flow hedge. It has also stated income tax related

to other comprehensive income (OCI). Further, the most common element is of exchange

difference for foreign operation translation.

7. Presenting reason for not stating these items in income statement

The items of other comprehensive income statement are referred as very expansive view

of net income. The changes in net income are deemed with reference to its core operations.

These items are allowed and volatile for cash flow for context of shareholder's equity. Generally,

it considers losses, gains, expenses which are not realized in this aspect. The items which alters

equity of organization without involving owner's investment and creation of distribution. It does

not provide impact on net income and organization's retained earnings. The current year's item

will impact on changes for accumulating OCI which are referred as another component of

stockholder's equity.

8. Presenting comparative analysis of other comprehensive income statements

Adairs Limited

Year 2015 (Base) 2016

% change in

2016 2016 (base) 2017

% change in

2017

Profit 745 27172 3547.25% 27172 21017 -22.65%

Items classified for loss or profit

OCI from continuing operations

7

flow with both organizations. In year 2016, each category was increased by huge proportion in

AMA Group Limited. However, all categories of cash flow are decreasing by small proportion as

compared to AMA Group Limited in Adairs Limited. In the year 2017, situation was contrasting

previous year. Each activity was decreasing in AMA Limited and vice versa in Adairs Limited.

OTHER COMPREHENSIVE INCOME STATEMENT

6. Presenting items related to other comprehensive income statement (OCI)

AMA Group Limited: The items are categorised to profit OCI such as exchange

differences on translation of foreign operation (Annual Report of AMA group, 2016).

Adairs Limited: It has presence of items which are reclassified subsequently to loss or

profit which are movement with context of cash flow hedge. It has also stated income tax related

to other comprehensive income (OCI). Further, the most common element is of exchange

difference for foreign operation translation.

7. Presenting reason for not stating these items in income statement

The items of other comprehensive income statement are referred as very expansive view

of net income. The changes in net income are deemed with reference to its core operations.

These items are allowed and volatile for cash flow for context of shareholder's equity. Generally,

it considers losses, gains, expenses which are not realized in this aspect. The items which alters

equity of organization without involving owner's investment and creation of distribution. It does

not provide impact on net income and organization's retained earnings. The current year's item

will impact on changes for accumulating OCI which are referred as another component of

stockholder's equity.

8. Presenting comparative analysis of other comprehensive income statements

Adairs Limited

Year 2015 (Base) 2016

% change in

2016 2016 (base) 2017

% change in

2017

Profit 745 27172 3547.25% 27172 21017 -22.65%

Items classified for loss or profit

OCI from continuing operations

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

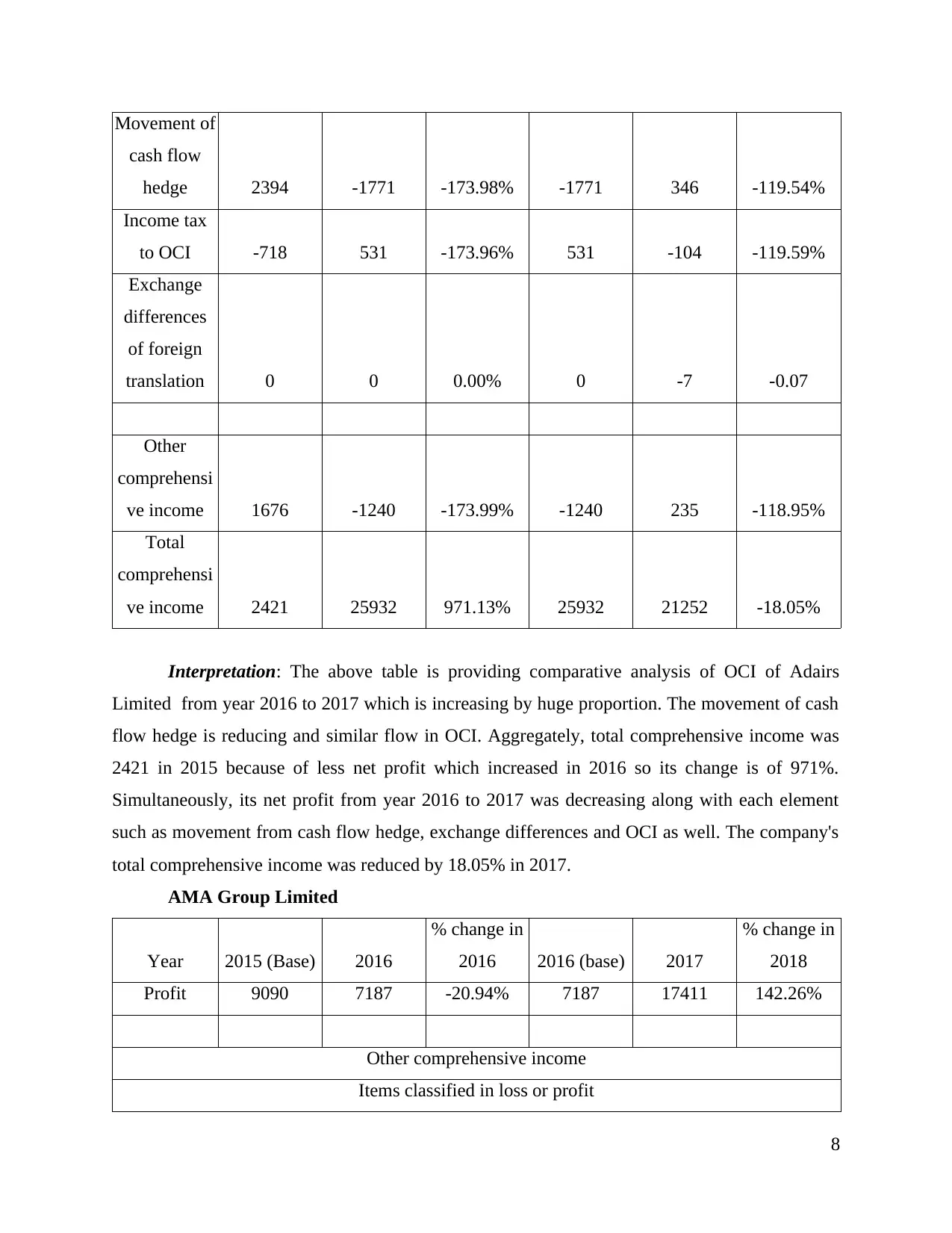

Movement of

cash flow

hedge 2394 -1771 -173.98% -1771 346 -119.54%

Income tax

to OCI -718 531 -173.96% 531 -104 -119.59%

Exchange

differences

of foreign

translation 0 0 0.00% 0 -7 -0.07

Other

comprehensi

ve income 1676 -1240 -173.99% -1240 235 -118.95%

Total

comprehensi

ve income 2421 25932 971.13% 25932 21252 -18.05%

Interpretation: The above table is providing comparative analysis of OCI of Adairs

Limited from year 2016 to 2017 which is increasing by huge proportion. The movement of cash

flow hedge is reducing and similar flow in OCI. Aggregately, total comprehensive income was

2421 in 2015 because of less net profit which increased in 2016 so its change is of 971%.

Simultaneously, its net profit from year 2016 to 2017 was decreasing along with each element

such as movement from cash flow hedge, exchange differences and OCI as well. The company's

total comprehensive income was reduced by 18.05% in 2017.

AMA Group Limited

Year 2015 (Base) 2016

% change in

2016 2016 (base) 2017

% change in

2018

Profit 9090 7187 -20.94% 7187 17411 142.26%

Other comprehensive income

Items classified in loss or profit

8

cash flow

hedge 2394 -1771 -173.98% -1771 346 -119.54%

Income tax

to OCI -718 531 -173.96% 531 -104 -119.59%

Exchange

differences

of foreign

translation 0 0 0.00% 0 -7 -0.07

Other

comprehensi

ve income 1676 -1240 -173.99% -1240 235 -118.95%

Total

comprehensi

ve income 2421 25932 971.13% 25932 21252 -18.05%

Interpretation: The above table is providing comparative analysis of OCI of Adairs

Limited from year 2016 to 2017 which is increasing by huge proportion. The movement of cash

flow hedge is reducing and similar flow in OCI. Aggregately, total comprehensive income was

2421 in 2015 because of less net profit which increased in 2016 so its change is of 971%.

Simultaneously, its net profit from year 2016 to 2017 was decreasing along with each element

such as movement from cash flow hedge, exchange differences and OCI as well. The company's

total comprehensive income was reduced by 18.05% in 2017.

AMA Group Limited

Year 2015 (Base) 2016

% change in

2016 2016 (base) 2017

% change in

2018

Profit 9090 7187 -20.94% 7187 17411 142.26%

Other comprehensive income

Items classified in loss or profit

8

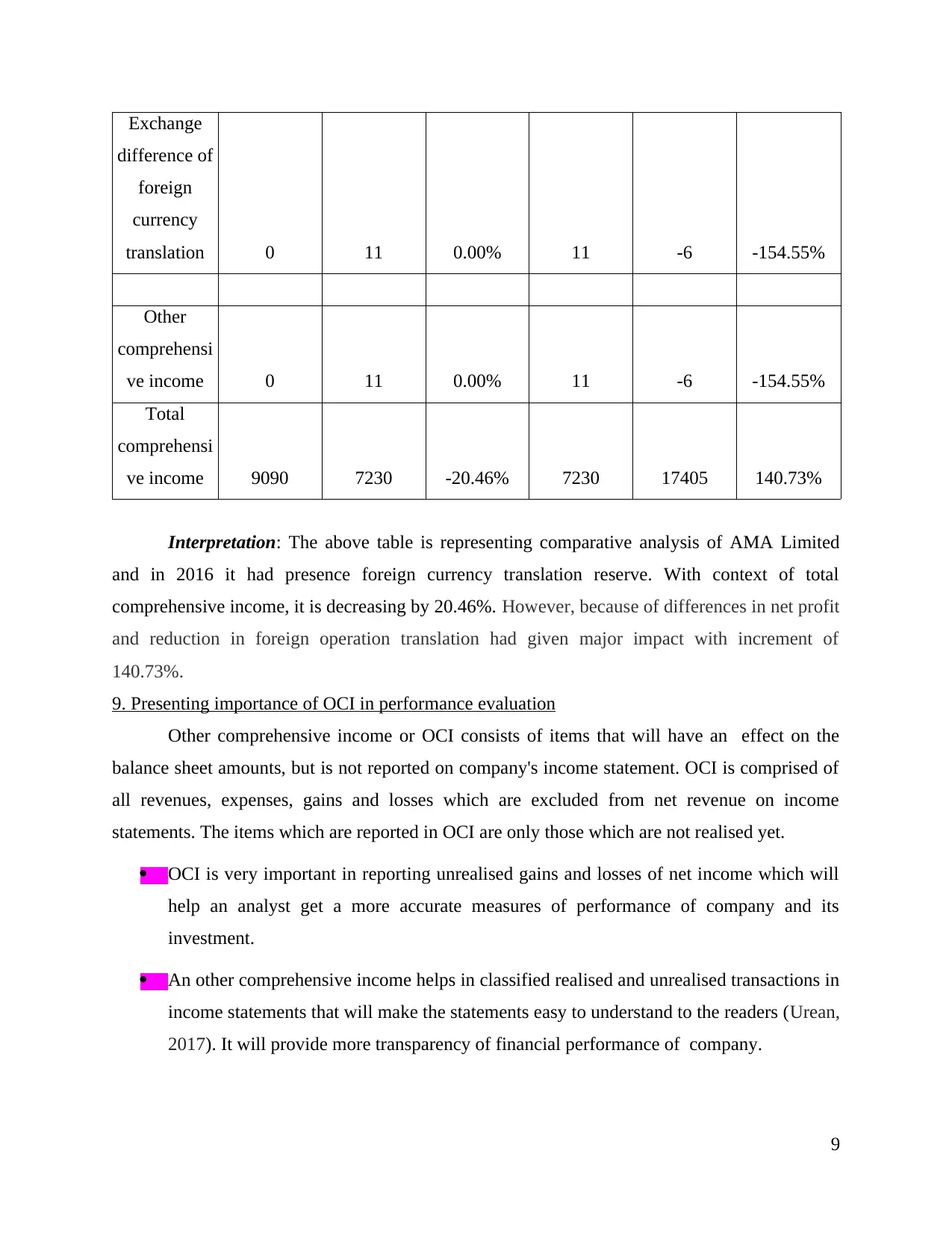

Exchange

difference of

foreign

currency

translation 0 11 0.00% 11 -6 -154.55%

Other

comprehensi

ve income 0 11 0.00% 11 -6 -154.55%

Total

comprehensi

ve income 9090 7230 -20.46% 7230 17405 140.73%

Interpretation: The above table is representing comparative analysis of AMA Limited

and in 2016 it had presence foreign currency translation reserve. With context of total

comprehensive income, it is decreasing by 20.46%. However, because of differences in net profit

and reduction in foreign operation translation had given major impact with increment of

140.73%.

9. Presenting importance of OCI in performance evaluation

Other comprehensive income or OCI consists of items that will have an effect on the

balance sheet amounts, but is not reported on company's income statement. OCI is comprised of

all revenues, expenses, gains and losses which are excluded from net revenue on income

statements. The items which are reported in OCI are only those which are not realised yet.

OCI is very important in reporting unrealised gains and losses of net income which will

help an analyst get a more accurate measures of performance of company and its

investment.

An other comprehensive income helps in classified realised and unrealised transactions in

income statements that will make the statements easy to understand to the readers (Urean,

2017). It will provide more transparency of financial performance of company.

9

difference of

foreign

currency

translation 0 11 0.00% 11 -6 -154.55%

Other

comprehensi

ve income 0 11 0.00% 11 -6 -154.55%

Total

comprehensi

ve income 9090 7230 -20.46% 7230 17405 140.73%

Interpretation: The above table is representing comparative analysis of AMA Limited

and in 2016 it had presence foreign currency translation reserve. With context of total

comprehensive income, it is decreasing by 20.46%. However, because of differences in net profit

and reduction in foreign operation translation had given major impact with increment of

140.73%.

9. Presenting importance of OCI in performance evaluation

Other comprehensive income or OCI consists of items that will have an effect on the

balance sheet amounts, but is not reported on company's income statement. OCI is comprised of

all revenues, expenses, gains and losses which are excluded from net revenue on income

statements. The items which are reported in OCI are only those which are not realised yet.

OCI is very important in reporting unrealised gains and losses of net income which will

help an analyst get a more accurate measures of performance of company and its

investment.

An other comprehensive income helps in classified realised and unrealised transactions in

income statements that will make the statements easy to understand to the readers (Urean,

2017). It will provide more transparency of financial performance of company.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.