Corporate Accounting Report: Avjennings and Mirvac Group Analysis

VerifiedAdded on 2020/11/23

|18

|4736

|49

Report

AI Summary

This report provides a comprehensive analysis of the corporate accounting practices of two ASX-listed real estate companies, Avjennings Limited and Mirvac Group. It begins with an introduction to corporate accounting and its relevance to financial statement analysis, particularly focusing on absorption, amalgamation, and consolidated financial statements. The report then delves into the owner's equity of both companies, presenting changes over a three-year period and conducting a comparative analysis of their debt and equity positions. The cash flow statements are examined, including the presentation of changes in items related to cash flow, comparative analysis of broad categories (operating, investing, and financing), and interpretation of the comparative analysis. The report also explores the other comprehensive income statement, outlining items related to the comparative income statement of each company, reasons for the absence of certain items in the income statement, and a comparative analysis with the impact of profit to its shareholders. Finally, the report addresses accounting for corporate income tax, presenting tax expenses, calculating effective tax rates, commenting on deferred tax assets/liabilities, calculating cash tax rates, and presenting reasons for different cash tax rates from book tax rates. The conclusion summarizes the key findings and insights gained from the analysis.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Corporate accounting helps in accounting for particular events such as absorption,

amalgamation and for preparing consolidated financial statements. The present report will

discuss about two real state companies which are listed from ASX are Avjennings Limited and

Mirvac group. Avjennings is involved in residential development business in Australia. Mirvac

Group is engaged in Australian development and construction industry as it manages and

develop property and capital asset throughout Australia. Further it could be elaborated that other

comprehensive income statement plays major role in assessing its actual profit. It could be

summed by stating that corporate income tax has very important function in its financial

statements.

Corporate accounting helps in accounting for particular events such as absorption,

amalgamation and for preparing consolidated financial statements. The present report will

discuss about two real state companies which are listed from ASX are Avjennings Limited and

Mirvac group. Avjennings is involved in residential development business in Australia. Mirvac

Group is engaged in Australian development and construction industry as it manages and

develop property and capital asset throughout Australia. Further it could be elaborated that other

comprehensive income statement plays major role in assessing its actual profit. It could be

summed by stating that corporate income tax has very important function in its financial

statements.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

OWNERS EQUITY.........................................................................................................................1

1. Presenting change in equity from last three years...................................................................1

2. Comparative analysis of debt and equity position of both firms............................................2

CASH FLOW STATEMENT..........................................................................................................4

3. Presenting changes in items related to cash flow statement...................................................4

4. Comparative analysis of its broads categories........................................................................5

5. Interpreting comparative analysis of both organization..........................................................5

OTHER COMPREHENSIVE INCOME STATEMENT................................................................6

6. Stating items related to comparative income statement of each company..............................6

7. Reason for absence of these items in income statement.........................................................7

8. Comparative analysis of both company with impact of profit to its shareholders..................7

9. Reason for including other comprehensive income for performance evaluation...................8

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................9

10. Presenting tax expenses of both company............................................................................9

11. Calculating effective tax rate................................................................................................9

12. Commenting on deferred tax asset/liabilities in balance sheet...........................................10

13. Change in deferred tax asset/liabilities...............................................................................10

14. Calculating cash tax with book tax amount and change in deferred tax asset/liabilities....11

15. Calculate cash tax rate.........................................................................................................12

16. Presenting reason for different cash tax rate from book tax rate........................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

OWNERS EQUITY.........................................................................................................................1

1. Presenting change in equity from last three years...................................................................1

2. Comparative analysis of debt and equity position of both firms............................................2

CASH FLOW STATEMENT..........................................................................................................4

3. Presenting changes in items related to cash flow statement...................................................4

4. Comparative analysis of its broads categories........................................................................5

5. Interpreting comparative analysis of both organization..........................................................5

OTHER COMPREHENSIVE INCOME STATEMENT................................................................6

6. Stating items related to comparative income statement of each company..............................6

7. Reason for absence of these items in income statement.........................................................7

8. Comparative analysis of both company with impact of profit to its shareholders..................7

9. Reason for including other comprehensive income for performance evaluation...................8

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................9

10. Presenting tax expenses of both company............................................................................9

11. Calculating effective tax rate................................................................................................9

12. Commenting on deferred tax asset/liabilities in balance sheet...........................................10

13. Change in deferred tax asset/liabilities...............................................................................10

14. Calculating cash tax with book tax amount and change in deferred tax asset/liabilities....11

15. Calculate cash tax rate.........................................................................................................12

16. Presenting reason for different cash tax rate from book tax rate........................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate accounting is referred as special accounting branch which helps in dealing with

company's accounting and for preparing final accounts, analysing cash flow and for interpreting

financial outcome of organization. In the similar aspect, it helps in accounting for particular

events such as absorption, amalgamation and for preparing consolidated financial statements.

The present report will discuss about two real state companies which are listed from ASX are

Avjennings Limited and Mirvac group. Avjennings is involved in residential development

business in Australia. Mirvac Group is engaged in Australian development and construction

industry as it manages and develop property and capital asset throughout Australia. This report is

reflecting owner's equity with comparative analysis of debt equity position. It will articulate

about cash flow statement with its appropriate classification of its broad categories. This report

will indicate other comprehensive income statement with performance evaluation of managers of

organization. Further, it will state accounting on basis of corporate income tax with effective

cash and book tax rate.

OWNERS EQUITY

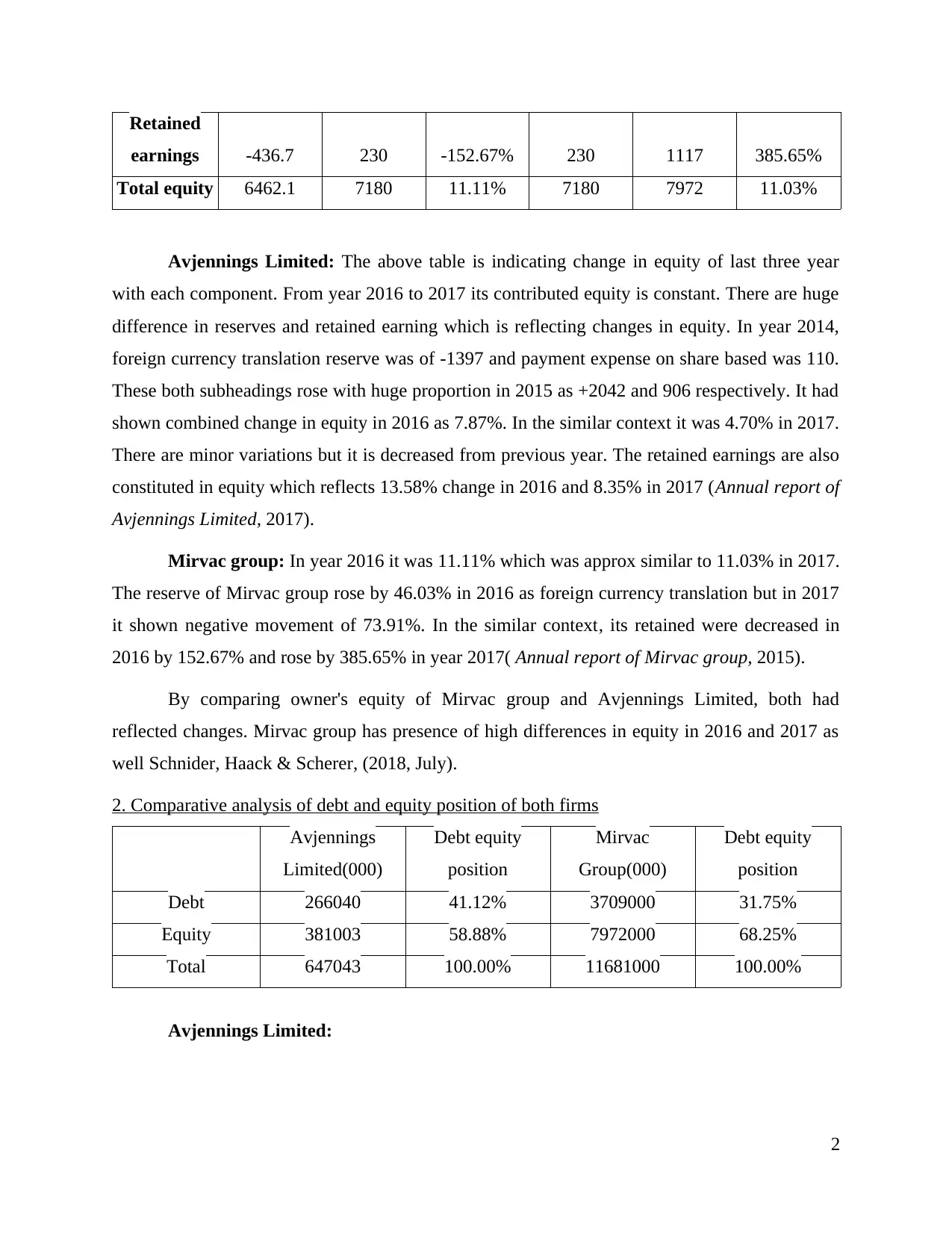

1. Presenting change in equity from last three years

2015 2016

% change

in 2016 2016 2017

% change in

2017

Avjennings Limited

Contributed

equity 160436 160436 0.00% 160436 160436 0.00%

Reserves 3074 6022 95.90% 6022 6622 9.96%

Retained

earnings 173836 197449 13.58% 197449 213945 8.35%

Total equity 337346 363907 7.87% 363907 381003 4.70%

Mirvac Group

Contributed

equity 6804.3 6812 0.11% 6812 6819 0.10%

Reserves 94.5 138 46.03% 138 36 -73.91%

1

Corporate accounting is referred as special accounting branch which helps in dealing with

company's accounting and for preparing final accounts, analysing cash flow and for interpreting

financial outcome of organization. In the similar aspect, it helps in accounting for particular

events such as absorption, amalgamation and for preparing consolidated financial statements.

The present report will discuss about two real state companies which are listed from ASX are

Avjennings Limited and Mirvac group. Avjennings is involved in residential development

business in Australia. Mirvac Group is engaged in Australian development and construction

industry as it manages and develop property and capital asset throughout Australia. This report is

reflecting owner's equity with comparative analysis of debt equity position. It will articulate

about cash flow statement with its appropriate classification of its broad categories. This report

will indicate other comprehensive income statement with performance evaluation of managers of

organization. Further, it will state accounting on basis of corporate income tax with effective

cash and book tax rate.

OWNERS EQUITY

1. Presenting change in equity from last three years

2015 2016

% change

in 2016 2016 2017

% change in

2017

Avjennings Limited

Contributed

equity 160436 160436 0.00% 160436 160436 0.00%

Reserves 3074 6022 95.90% 6022 6622 9.96%

Retained

earnings 173836 197449 13.58% 197449 213945 8.35%

Total equity 337346 363907 7.87% 363907 381003 4.70%

Mirvac Group

Contributed

equity 6804.3 6812 0.11% 6812 6819 0.10%

Reserves 94.5 138 46.03% 138 36 -73.91%

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Retained

earnings -436.7 230 -152.67% 230 1117 385.65%

Total equity 6462.1 7180 11.11% 7180 7972 11.03%

Avjennings Limited: The above table is indicating change in equity of last three year

with each component. From year 2016 to 2017 its contributed equity is constant. There are huge

difference in reserves and retained earning which is reflecting changes in equity. In year 2014,

foreign currency translation reserve was of -1397 and payment expense on share based was 110.

These both subheadings rose with huge proportion in 2015 as +2042 and 906 respectively. It had

shown combined change in equity in 2016 as 7.87%. In the similar context it was 4.70% in 2017.

There are minor variations but it is decreased from previous year. The retained earnings are also

constituted in equity which reflects 13.58% change in 2016 and 8.35% in 2017 (Annual report of

Avjennings Limited, 2017).

Mirvac group: In year 2016 it was 11.11% which was approx similar to 11.03% in 2017.

The reserve of Mirvac group rose by 46.03% in 2016 as foreign currency translation but in 2017

it shown negative movement of 73.91%. In the similar context, its retained were decreased in

2016 by 152.67% and rose by 385.65% in year 2017( Annual report of Mirvac group, 2015).

By comparing owner's equity of Mirvac group and Avjennings Limited, both had

reflected changes. Mirvac group has presence of high differences in equity in 2016 and 2017 as

well Schnider, Haack & Scherer, (2018, July).

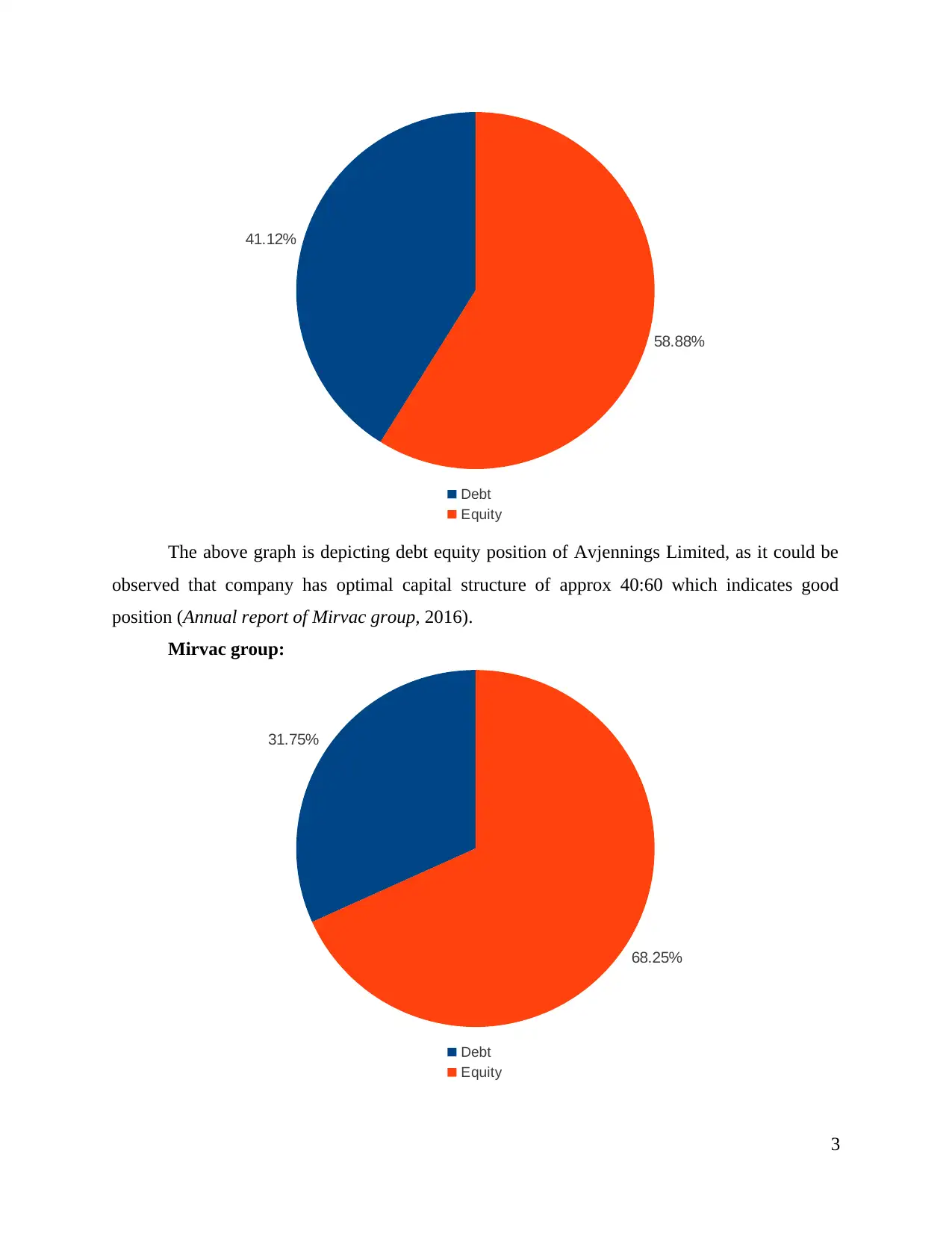

2. Comparative analysis of debt and equity position of both firms

Avjennings

Limited(000)

Debt equity

position

Mirvac

Group(000)

Debt equity

position

Debt 266040 41.12% 3709000 31.75%

Equity 381003 58.88% 7972000 68.25%

Total 647043 100.00% 11681000 100.00%

Avjennings Limited:

2

earnings -436.7 230 -152.67% 230 1117 385.65%

Total equity 6462.1 7180 11.11% 7180 7972 11.03%

Avjennings Limited: The above table is indicating change in equity of last three year

with each component. From year 2016 to 2017 its contributed equity is constant. There are huge

difference in reserves and retained earning which is reflecting changes in equity. In year 2014,

foreign currency translation reserve was of -1397 and payment expense on share based was 110.

These both subheadings rose with huge proportion in 2015 as +2042 and 906 respectively. It had

shown combined change in equity in 2016 as 7.87%. In the similar context it was 4.70% in 2017.

There are minor variations but it is decreased from previous year. The retained earnings are also

constituted in equity which reflects 13.58% change in 2016 and 8.35% in 2017 (Annual report of

Avjennings Limited, 2017).

Mirvac group: In year 2016 it was 11.11% which was approx similar to 11.03% in 2017.

The reserve of Mirvac group rose by 46.03% in 2016 as foreign currency translation but in 2017

it shown negative movement of 73.91%. In the similar context, its retained were decreased in

2016 by 152.67% and rose by 385.65% in year 2017( Annual report of Mirvac group, 2015).

By comparing owner's equity of Mirvac group and Avjennings Limited, both had

reflected changes. Mirvac group has presence of high differences in equity in 2016 and 2017 as

well Schnider, Haack & Scherer, (2018, July).

2. Comparative analysis of debt and equity position of both firms

Avjennings

Limited(000)

Debt equity

position

Mirvac

Group(000)

Debt equity

position

Debt 266040 41.12% 3709000 31.75%

Equity 381003 58.88% 7972000 68.25%

Total 647043 100.00% 11681000 100.00%

Avjennings Limited:

2

41.12%

58.88%

Debt

Equity

The above graph is depicting debt equity position of Avjennings Limited, as it could be

observed that company has optimal capital structure of approx 40:60 which indicates good

position (Annual report of Mirvac group, 2016).

Mirvac group:

31.75%

68.25%

Debt

Equity

3

58.88%

Debt

Equity

The above graph is depicting debt equity position of Avjennings Limited, as it could be

observed that company has optimal capital structure of approx 40:60 which indicates good

position (Annual report of Mirvac group, 2016).

Mirvac group:

31.75%

68.25%

Debt

Equity

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above graph is showing capital structure of Mirvac group which reflects that

company is highly relying on equity as compared to debt. It has equity of 68.25% and debt of

31.75%. The major risk faced due to high equity is about dilution of existing holdings of

shareholder due to division of net income in huge number of shares Murtala & et.al., (2018).

CASH FLOW STATEMENT

3. Presenting changes in items related to cash flow statement

There is presence of three broad categories in cash flow statement which are operating,

investing and financing activity in both organization.

Operating activity: With reference to Mirvac group, all the items which are related to

cash operation of business entity. The receipts which are collected through customer and

payment from its employees and supplier are considered in this. Further, it includes cash which

is received on basis of interest and along with this, it deducts interest and tax payment as well.

In the similar aspect, distribution gained is replicated in operating activities. From year 2016 to

2017, it does not have huge variation. With reference to Avjenning Limited, it had considered

receipts and payments via customers, suppliers and employees. It has also stated finance cost

with interest paid. Income tax payment also belongs to operating activity.

Investing activity: This category considers cash related to long and short term

investments such as payments for property, plant, equipment and investment properties. In the

similar aspect, it shows proceeds from joint venture and sale of property of investment. It has

shown repayments related to loan and payments for investment and intangibles. From year 2016

to 2017, it had reflected major change in Mirvac group because there was presence of high

amount related to proceeds from sale of investment properties. By considering Avjennings

Limited, its unique item is dividend received via joint venture entity which is decreasing from

2016 to 2017 in huge proportion Larkin, Ng & Zhu, (2018).

Financing activity: Finance plays major role in every business entity as it had

considered proceed and repayments for borrowings which is doubling from previous year. It

consists of distributions payments which is approx. to stable amount with minor changes in

Mirvac group. In cash flow statement of Avjennings limited had also paid dividends which are

comprised in financing activity.

4

company is highly relying on equity as compared to debt. It has equity of 68.25% and debt of

31.75%. The major risk faced due to high equity is about dilution of existing holdings of

shareholder due to division of net income in huge number of shares Murtala & et.al., (2018).

CASH FLOW STATEMENT

3. Presenting changes in items related to cash flow statement

There is presence of three broad categories in cash flow statement which are operating,

investing and financing activity in both organization.

Operating activity: With reference to Mirvac group, all the items which are related to

cash operation of business entity. The receipts which are collected through customer and

payment from its employees and supplier are considered in this. Further, it includes cash which

is received on basis of interest and along with this, it deducts interest and tax payment as well.

In the similar aspect, distribution gained is replicated in operating activities. From year 2016 to

2017, it does not have huge variation. With reference to Avjenning Limited, it had considered

receipts and payments via customers, suppliers and employees. It has also stated finance cost

with interest paid. Income tax payment also belongs to operating activity.

Investing activity: This category considers cash related to long and short term

investments such as payments for property, plant, equipment and investment properties. In the

similar aspect, it shows proceeds from joint venture and sale of property of investment. It has

shown repayments related to loan and payments for investment and intangibles. From year 2016

to 2017, it had reflected major change in Mirvac group because there was presence of high

amount related to proceeds from sale of investment properties. By considering Avjennings

Limited, its unique item is dividend received via joint venture entity which is decreasing from

2016 to 2017 in huge proportion Larkin, Ng & Zhu, (2018).

Financing activity: Finance plays major role in every business entity as it had

considered proceed and repayments for borrowings which is doubling from previous year. It

consists of distributions payments which is approx. to stable amount with minor changes in

Mirvac group. In cash flow statement of Avjennings limited had also paid dividends which are

comprised in financing activity.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

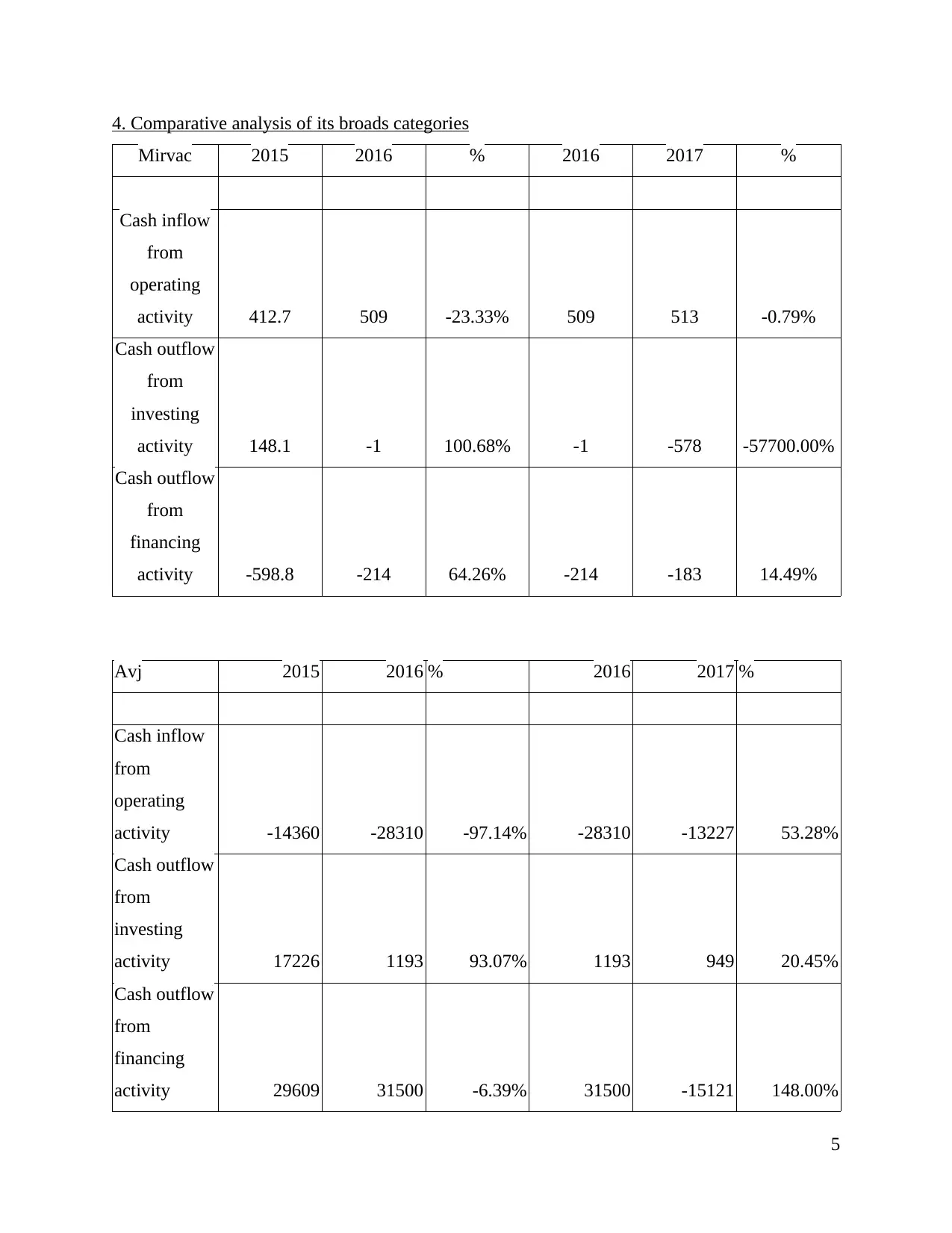

4. Comparative analysis of its broads categories

Mirvac 2015 2016 % 2016 2017 %

Cash inflow

from

operating

activity 412.7 509 -23.33% 509 513 -0.79%

Cash outflow

from

investing

activity 148.1 -1 100.68% -1 -578 -57700.00%

Cash outflow

from

financing

activity -598.8 -214 64.26% -214 -183 14.49%

Avj 2015 2016 % 2016 2017 %

Cash inflow

from

operating

activity -14360 -28310 -97.14% -28310 -13227 53.28%

Cash outflow

from

investing

activity 17226 1193 93.07% 1193 949 20.45%

Cash outflow

from

financing

activity 29609 31500 -6.39% 31500 -15121 148.00%

5

Mirvac 2015 2016 % 2016 2017 %

Cash inflow

from

operating

activity 412.7 509 -23.33% 509 513 -0.79%

Cash outflow

from

investing

activity 148.1 -1 100.68% -1 -578 -57700.00%

Cash outflow

from

financing

activity -598.8 -214 64.26% -214 -183 14.49%

Avj 2015 2016 % 2016 2017 %

Cash inflow

from

operating

activity -14360 -28310 -97.14% -28310 -13227 53.28%

Cash outflow

from

investing

activity 17226 1193 93.07% 1193 949 20.45%

Cash outflow

from

financing

activity 29609 31500 -6.39% 31500 -15121 148.00%

5

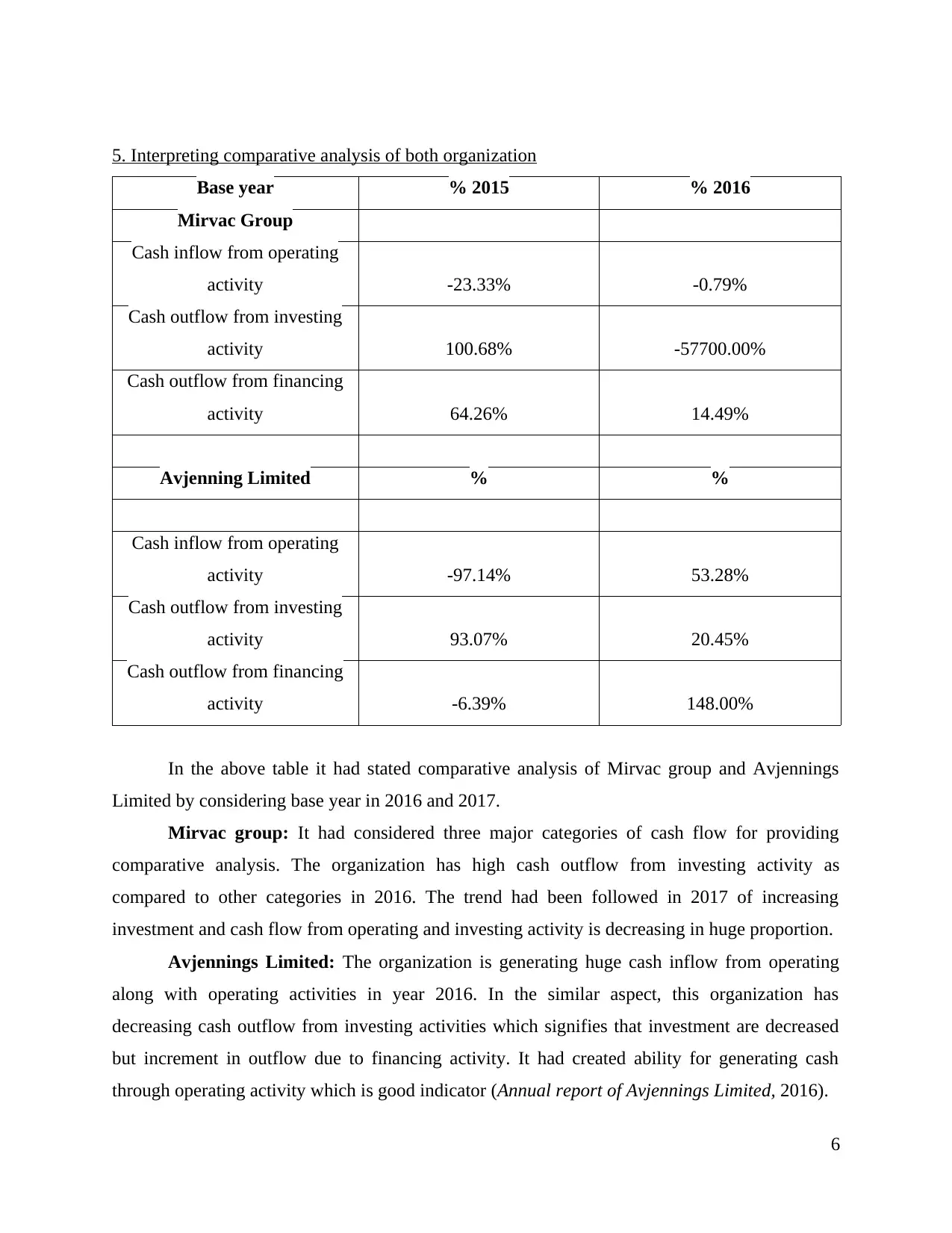

5. Interpreting comparative analysis of both organization

Base year % 2015 % 2016

Mirvac Group

Cash inflow from operating

activity -23.33% -0.79%

Cash outflow from investing

activity 100.68% -57700.00%

Cash outflow from financing

activity 64.26% 14.49%

Avjenning Limited % %

Cash inflow from operating

activity -97.14% 53.28%

Cash outflow from investing

activity 93.07% 20.45%

Cash outflow from financing

activity -6.39% 148.00%

In the above table it had stated comparative analysis of Mirvac group and Avjennings

Limited by considering base year in 2016 and 2017.

Mirvac group: It had considered three major categories of cash flow for providing

comparative analysis. The organization has high cash outflow from investing activity as

compared to other categories in 2016. The trend had been followed in 2017 of increasing

investment and cash flow from operating and investing activity is decreasing in huge proportion.

Avjennings Limited: The organization is generating huge cash inflow from operating

along with operating activities in year 2016. In the similar aspect, this organization has

decreasing cash outflow from investing activities which signifies that investment are decreased

but increment in outflow due to financing activity. It had created ability for generating cash

through operating activity which is good indicator (Annual report of Avjennings Limited, 2016).

6

Base year % 2015 % 2016

Mirvac Group

Cash inflow from operating

activity -23.33% -0.79%

Cash outflow from investing

activity 100.68% -57700.00%

Cash outflow from financing

activity 64.26% 14.49%

Avjenning Limited % %

Cash inflow from operating

activity -97.14% 53.28%

Cash outflow from investing

activity 93.07% 20.45%

Cash outflow from financing

activity -6.39% 148.00%

In the above table it had stated comparative analysis of Mirvac group and Avjennings

Limited by considering base year in 2016 and 2017.

Mirvac group: It had considered three major categories of cash flow for providing

comparative analysis. The organization has high cash outflow from investing activity as

compared to other categories in 2016. The trend had been followed in 2017 of increasing

investment and cash flow from operating and investing activity is decreasing in huge proportion.

Avjennings Limited: The organization is generating huge cash inflow from operating

along with operating activities in year 2016. In the similar aspect, this organization has

decreasing cash outflow from investing activities which signifies that investment are decreased

but increment in outflow due to financing activity. It had created ability for generating cash

through operating activity which is good indicator (Annual report of Avjennings Limited, 2016).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

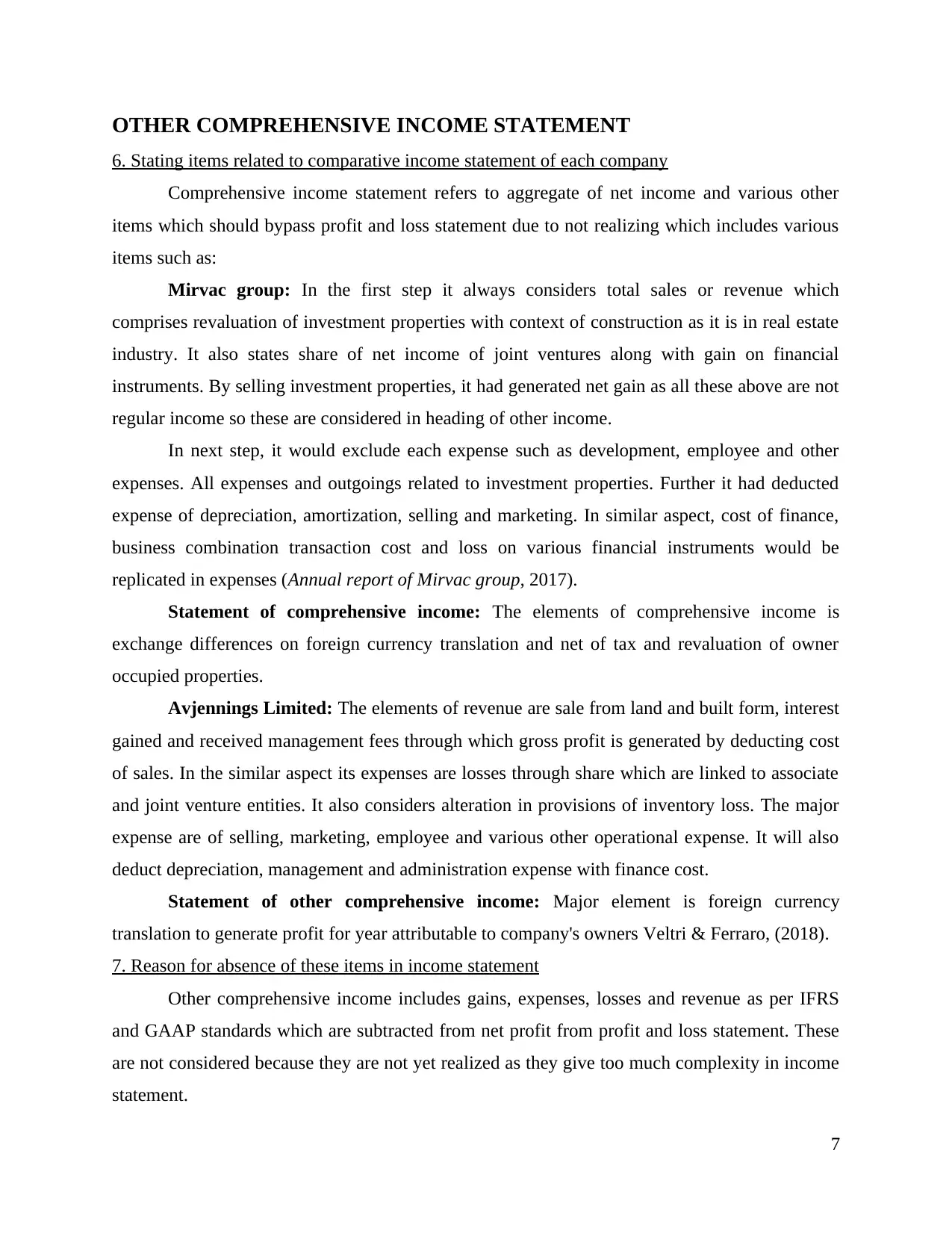

OTHER COMPREHENSIVE INCOME STATEMENT

6. Stating items related to comparative income statement of each company

Comprehensive income statement refers to aggregate of net income and various other

items which should bypass profit and loss statement due to not realizing which includes various

items such as:

Mirvac group: In the first step it always considers total sales or revenue which

comprises revaluation of investment properties with context of construction as it is in real estate

industry. It also states share of net income of joint ventures along with gain on financial

instruments. By selling investment properties, it had generated net gain as all these above are not

regular income so these are considered in heading of other income.

In next step, it would exclude each expense such as development, employee and other

expenses. All expenses and outgoings related to investment properties. Further it had deducted

expense of depreciation, amortization, selling and marketing. In similar aspect, cost of finance,

business combination transaction cost and loss on various financial instruments would be

replicated in expenses (Annual report of Mirvac group, 2017).

Statement of comprehensive income: The elements of comprehensive income is

exchange differences on foreign currency translation and net of tax and revaluation of owner

occupied properties.

Avjennings Limited: The elements of revenue are sale from land and built form, interest

gained and received management fees through which gross profit is generated by deducting cost

of sales. In the similar aspect its expenses are losses through share which are linked to associate

and joint venture entities. It also considers alteration in provisions of inventory loss. The major

expense are of selling, marketing, employee and various other operational expense. It will also

deduct depreciation, management and administration expense with finance cost.

Statement of other comprehensive income: Major element is foreign currency

translation to generate profit for year attributable to company's owners Veltri & Ferraro, (2018).

7. Reason for absence of these items in income statement

Other comprehensive income includes gains, expenses, losses and revenue as per IFRS

and GAAP standards which are subtracted from net profit from profit and loss statement. These

are not considered because they are not yet realized as they give too much complexity in income

statement.

7

6. Stating items related to comparative income statement of each company

Comprehensive income statement refers to aggregate of net income and various other

items which should bypass profit and loss statement due to not realizing which includes various

items such as:

Mirvac group: In the first step it always considers total sales or revenue which

comprises revaluation of investment properties with context of construction as it is in real estate

industry. It also states share of net income of joint ventures along with gain on financial

instruments. By selling investment properties, it had generated net gain as all these above are not

regular income so these are considered in heading of other income.

In next step, it would exclude each expense such as development, employee and other

expenses. All expenses and outgoings related to investment properties. Further it had deducted

expense of depreciation, amortization, selling and marketing. In similar aspect, cost of finance,

business combination transaction cost and loss on various financial instruments would be

replicated in expenses (Annual report of Mirvac group, 2017).

Statement of comprehensive income: The elements of comprehensive income is

exchange differences on foreign currency translation and net of tax and revaluation of owner

occupied properties.

Avjennings Limited: The elements of revenue are sale from land and built form, interest

gained and received management fees through which gross profit is generated by deducting cost

of sales. In the similar aspect its expenses are losses through share which are linked to associate

and joint venture entities. It also considers alteration in provisions of inventory loss. The major

expense are of selling, marketing, employee and various other operational expense. It will also

deduct depreciation, management and administration expense with finance cost.

Statement of other comprehensive income: Major element is foreign currency

translation to generate profit for year attributable to company's owners Veltri & Ferraro, (2018).

7. Reason for absence of these items in income statement

Other comprehensive income includes gains, expenses, losses and revenue as per IFRS

and GAAP standards which are subtracted from net profit from profit and loss statement. These

are not considered because they are not yet realized as they give too much complexity in income

statement.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

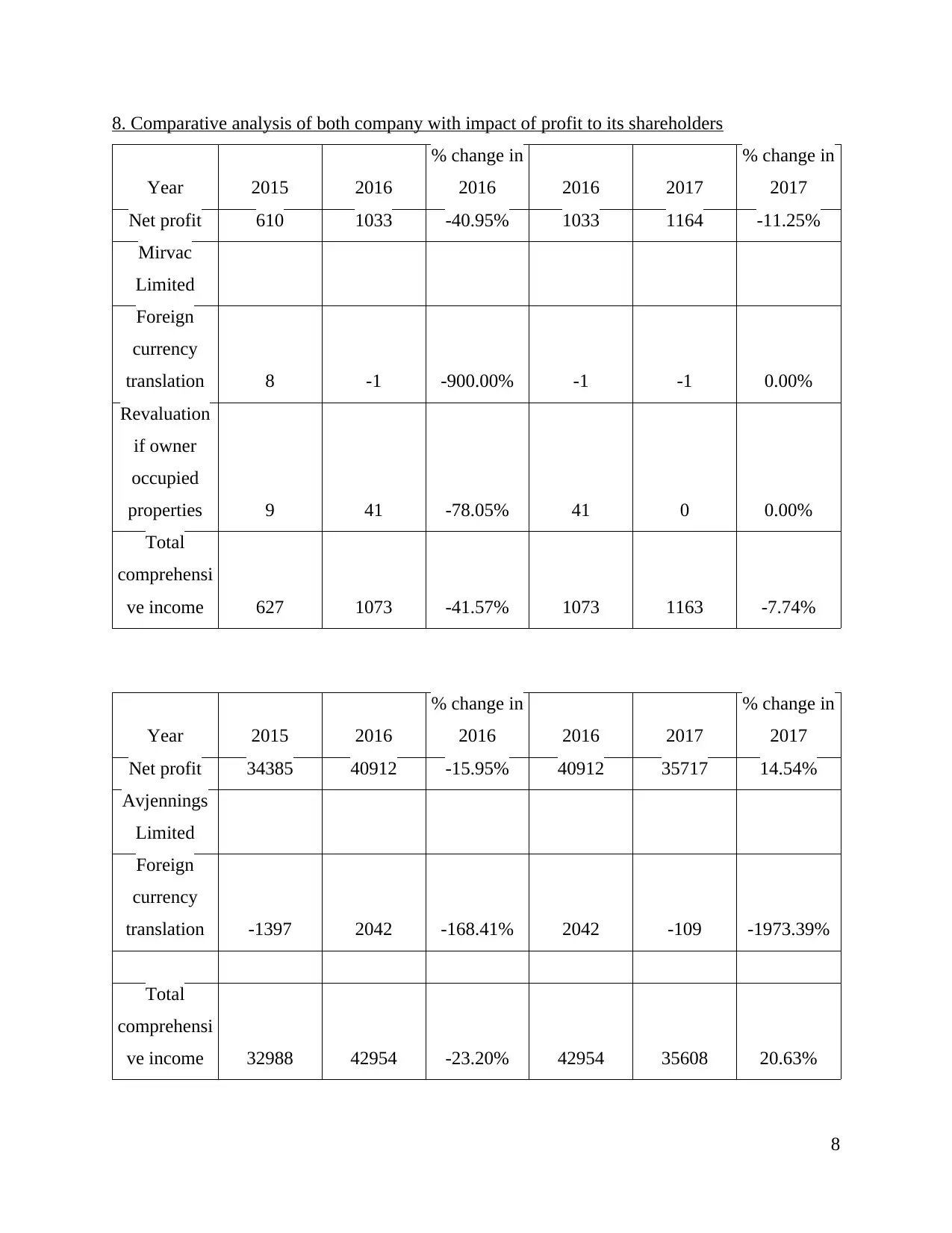

8. Comparative analysis of both company with impact of profit to its shareholders

Year 2015 2016

% change in

2016 2016 2017

% change in

2017

Net profit 610 1033 -40.95% 1033 1164 -11.25%

Mirvac

Limited

Foreign

currency

translation 8 -1 -900.00% -1 -1 0.00%

Revaluation

if owner

occupied

properties 9 41 -78.05% 41 0 0.00%

Total

comprehensi

ve income 627 1073 -41.57% 1073 1163 -7.74%

Year 2015 2016

% change in

2016 2016 2017

% change in

2017

Net profit 34385 40912 -15.95% 40912 35717 14.54%

Avjennings

Limited

Foreign

currency

translation -1397 2042 -168.41% 2042 -109 -1973.39%

Total

comprehensi

ve income 32988 42954 -23.20% 42954 35608 20.63%

8

Year 2015 2016

% change in

2016 2016 2017

% change in

2017

Net profit 610 1033 -40.95% 1033 1164 -11.25%

Mirvac

Limited

Foreign

currency

translation 8 -1 -900.00% -1 -1 0.00%

Revaluation

if owner

occupied

properties 9 41 -78.05% 41 0 0.00%

Total

comprehensi

ve income 627 1073 -41.57% 1073 1163 -7.74%

Year 2015 2016

% change in

2016 2016 2017

% change in

2017

Net profit 34385 40912 -15.95% 40912 35717 14.54%

Avjennings

Limited

Foreign

currency

translation -1397 2042 -168.41% 2042 -109 -1973.39%

Total

comprehensi

ve income 32988 42954 -23.20% 42954 35608 20.63%

8

9. Reason for including other comprehensive income for performance evaluation

The other comprehensive income must be included as it could be observed as expansive

aspect of net profit. It helps for understanding organization's drivers with its day to day

operations. Generally, realized losses and gains are always attained through net income due to

very important concern but unrealized equation assists for demonstrating investment

management. From the past scenario, alterations in profit of organization are deemed outside

from its core operations and allowed to flow via total shareholder's equity. It provides perfect

measure of investment of company with its fair value.

It provides analysing and better understanding of OCI which improves financial analysis

majorly for fiscal organizations. It exists disclosures with detailed comprehensive income along

with its components of income statement.

ACCOUNTING FOR CORPORATE INCOME TAX

10. Presenting tax expenses of both company

Mirvac Group: It has adopted Taxation's tax transparency code, where it had published

tax governance statement which had detailed corporate structure and system of tax corporate

governance. The expense of income tax is calculated at specific applicable tax rate which was

30% in Australia in 2017 along with recognising profit of year which is related to comprehensive

transaction or income which is directly paired in equity. It comprises both deferred and current

tax. Current tax represents amount which is paid or must be payable for present year. The

account of deferred tax reflects temporary differences of tax. These temporary variations occur

for recognising income and expenses through tax authorities for objective of accounting in

different duration.

Avjennings Limited: It had calculated income tax expense with appropriate tax rate

which was recognised in profit and loss statement of year as it is related to comprehensive

transactions or income with context of equity. Tax expense is combination of deferred and

current tax. Current tax signify paid tax expense or payable for present year Faulkender, Hankins

& Petersen, (2018).

9

The other comprehensive income must be included as it could be observed as expansive

aspect of net profit. It helps for understanding organization's drivers with its day to day

operations. Generally, realized losses and gains are always attained through net income due to

very important concern but unrealized equation assists for demonstrating investment

management. From the past scenario, alterations in profit of organization are deemed outside

from its core operations and allowed to flow via total shareholder's equity. It provides perfect

measure of investment of company with its fair value.

It provides analysing and better understanding of OCI which improves financial analysis

majorly for fiscal organizations. It exists disclosures with detailed comprehensive income along

with its components of income statement.

ACCOUNTING FOR CORPORATE INCOME TAX

10. Presenting tax expenses of both company

Mirvac Group: It has adopted Taxation's tax transparency code, where it had published

tax governance statement which had detailed corporate structure and system of tax corporate

governance. The expense of income tax is calculated at specific applicable tax rate which was

30% in Australia in 2017 along with recognising profit of year which is related to comprehensive

transaction or income which is directly paired in equity. It comprises both deferred and current

tax. Current tax represents amount which is paid or must be payable for present year. The

account of deferred tax reflects temporary differences of tax. These temporary variations occur

for recognising income and expenses through tax authorities for objective of accounting in

different duration.

Avjennings Limited: It had calculated income tax expense with appropriate tax rate

which was recognised in profit and loss statement of year as it is related to comprehensive

transactions or income with context of equity. Tax expense is combination of deferred and

current tax. Current tax signify paid tax expense or payable for present year Faulkender, Hankins

& Petersen, (2018).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.