Corporate Accounting Report: Spark Infrastructure Tax and Equity

VerifiedAdded on 2020/04/01

|12

|2707

|65

Report

AI Summary

This report provides a comprehensive analysis of Spark Infrastructure's corporate accounting practices, focusing on the company's financial statements for the year ended June 30, 2016. The report begins by examining the items of equity, including issued capital, reserves, and retained earnings, and explains the changes in each item. It then delves into the company's tax expenses, comparing the effective tax rate to the statutory rate and explaining the reasons for any differences. The report also addresses deferred tax assets and liabilities, current tax or income tax payable, and the discrepancies between income tax expenses and income tax paid. Furthermore, the report highlights a confusing aspect regarding deferred tax and provides new insights into the company's income tax treatment. The analysis references the annual report to support its findings, offering a detailed understanding of Spark Infrastructure's financial position and tax strategies.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Author note

Corporate accounting

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

(i) Item of equity and explanation........................................................................................2

(i) Tax expenses of the company.........................................................................................4

(ii) Difference in company tax rate and tax expenses...........................................................5

(iii) Deferred tax assets or liabilities......................................................................................5

(iv) Current tax or income tax payable..................................................................................6

(v) Difference in income tax expenses and income tax paid................................................7

(vi) Confusing, interesting, difficult or surprising fact with regard to tax treatment of the

company.....................................................................................................................................8

Reference..................................................................................................................................10

Table of Contents

(i) Item of equity and explanation........................................................................................2

(i) Tax expenses of the company.........................................................................................4

(ii) Difference in company tax rate and tax expenses...........................................................5

(iii) Deferred tax assets or liabilities......................................................................................5

(iv) Current tax or income tax payable..................................................................................6

(v) Difference in income tax expenses and income tax paid................................................7

(vi) Confusing, interesting, difficult or surprising fact with regard to tax treatment of the

company.....................................................................................................................................8

Reference..................................................................................................................................10

2CORPORATE ACCOUNTING

Spark Infrastructure is the fund for specialist infrastructure and the main objective of

the company is investing in the regulated utility infrastructure within Australia as well as in

overseas. The products and services of the company includes the gas and electricity

transmission and distribution, sewerage assets, regulated water that offers stable cash flows

and comparatively low risks and it facilitates payment to the investors along with the

potential long-term growth. The vision of the company is to offer long-term, stable and

attractive returns complied with the market expectations and risk profile (Spark Infrastructure

2018). Further, it seeks to establish the diversified portfolio with regard to regulated utility

infrastructure assets and continuing to be in the lead position under the Australian

infrastructure investment fund. Further, the values upon which the company is maintaining its

growth are fairness, honesty, maximising the value of the security holder and maintenance of

the high standards for corporate governance.

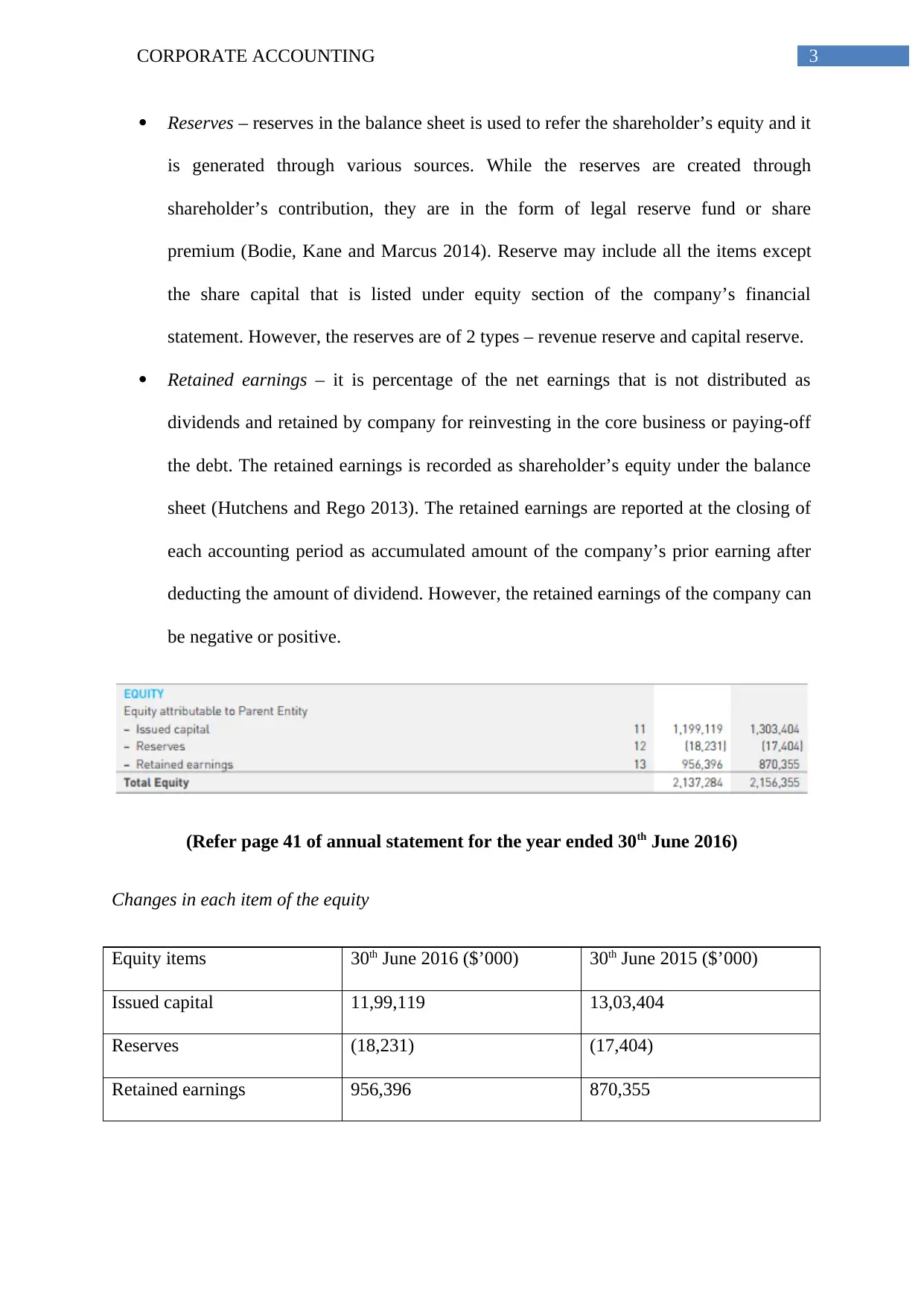

(i) Item of equity and explanation

From the annual report of the company for the year ended 30th June 2016, it has been

recognized that the equity of the company has the following items –

Issued capital – issued capital is the number of shares capital that is issued to the

shareholders. The issued capital is the authorised capital of the company and the

unused part is known as unissued capital. Further it is face value of shares that is

issued to the shareholders. The share premium and issued share capital represent the

invested capital of the shareholders (Dhaliwal et al. 2016). The issued capital is also

known as the subscribed share capital or subscribed capital. The share capital value

changes with the issuance of new shares to new or existing shareholders. Further, the

company has the option of redeeming or purchasing the shares that will result into the

changes in the value of subscribed capital.

Spark Infrastructure is the fund for specialist infrastructure and the main objective of

the company is investing in the regulated utility infrastructure within Australia as well as in

overseas. The products and services of the company includes the gas and electricity

transmission and distribution, sewerage assets, regulated water that offers stable cash flows

and comparatively low risks and it facilitates payment to the investors along with the

potential long-term growth. The vision of the company is to offer long-term, stable and

attractive returns complied with the market expectations and risk profile (Spark Infrastructure

2018). Further, it seeks to establish the diversified portfolio with regard to regulated utility

infrastructure assets and continuing to be in the lead position under the Australian

infrastructure investment fund. Further, the values upon which the company is maintaining its

growth are fairness, honesty, maximising the value of the security holder and maintenance of

the high standards for corporate governance.

(i) Item of equity and explanation

From the annual report of the company for the year ended 30th June 2016, it has been

recognized that the equity of the company has the following items –

Issued capital – issued capital is the number of shares capital that is issued to the

shareholders. The issued capital is the authorised capital of the company and the

unused part is known as unissued capital. Further it is face value of shares that is

issued to the shareholders. The share premium and issued share capital represent the

invested capital of the shareholders (Dhaliwal et al. 2016). The issued capital is also

known as the subscribed share capital or subscribed capital. The share capital value

changes with the issuance of new shares to new or existing shareholders. Further, the

company has the option of redeeming or purchasing the shares that will result into the

changes in the value of subscribed capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Reserves – reserves in the balance sheet is used to refer the shareholder’s equity and it

is generated through various sources. While the reserves are created through

shareholder’s contribution, they are in the form of legal reserve fund or share

premium (Bodie, Kane and Marcus 2014). Reserve may include all the items except

the share capital that is listed under equity section of the company’s financial

statement. However, the reserves are of 2 types – revenue reserve and capital reserve.

Retained earnings – it is percentage of the net earnings that is not distributed as

dividends and retained by company for reinvesting in the core business or paying-off

the debt. The retained earnings is recorded as shareholder’s equity under the balance

sheet (Hutchens and Rego 2013). The retained earnings are reported at the closing of

each accounting period as accumulated amount of the company’s prior earning after

deducting the amount of dividend. However, the retained earnings of the company can

be negative or positive.

(Refer page 41 of annual statement for the year ended 30th June 2016)

Changes in each item of the equity

Equity items 30th June 2016 ($’000) 30th June 2015 ($’000)

Issued capital 11,99,119 13,03,404

Reserves (18,231) (17,404)

Retained earnings 956,396 870,355

Reserves – reserves in the balance sheet is used to refer the shareholder’s equity and it

is generated through various sources. While the reserves are created through

shareholder’s contribution, they are in the form of legal reserve fund or share

premium (Bodie, Kane and Marcus 2014). Reserve may include all the items except

the share capital that is listed under equity section of the company’s financial

statement. However, the reserves are of 2 types – revenue reserve and capital reserve.

Retained earnings – it is percentage of the net earnings that is not distributed as

dividends and retained by company for reinvesting in the core business or paying-off

the debt. The retained earnings is recorded as shareholder’s equity under the balance

sheet (Hutchens and Rego 2013). The retained earnings are reported at the closing of

each accounting period as accumulated amount of the company’s prior earning after

deducting the amount of dividend. However, the retained earnings of the company can

be negative or positive.

(Refer page 41 of annual statement for the year ended 30th June 2016)

Changes in each item of the equity

Equity items 30th June 2016 ($’000) 30th June 2015 ($’000)

Issued capital 11,99,119 13,03,404

Reserves (18,231) (17,404)

Retained earnings 956,396 870,355

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

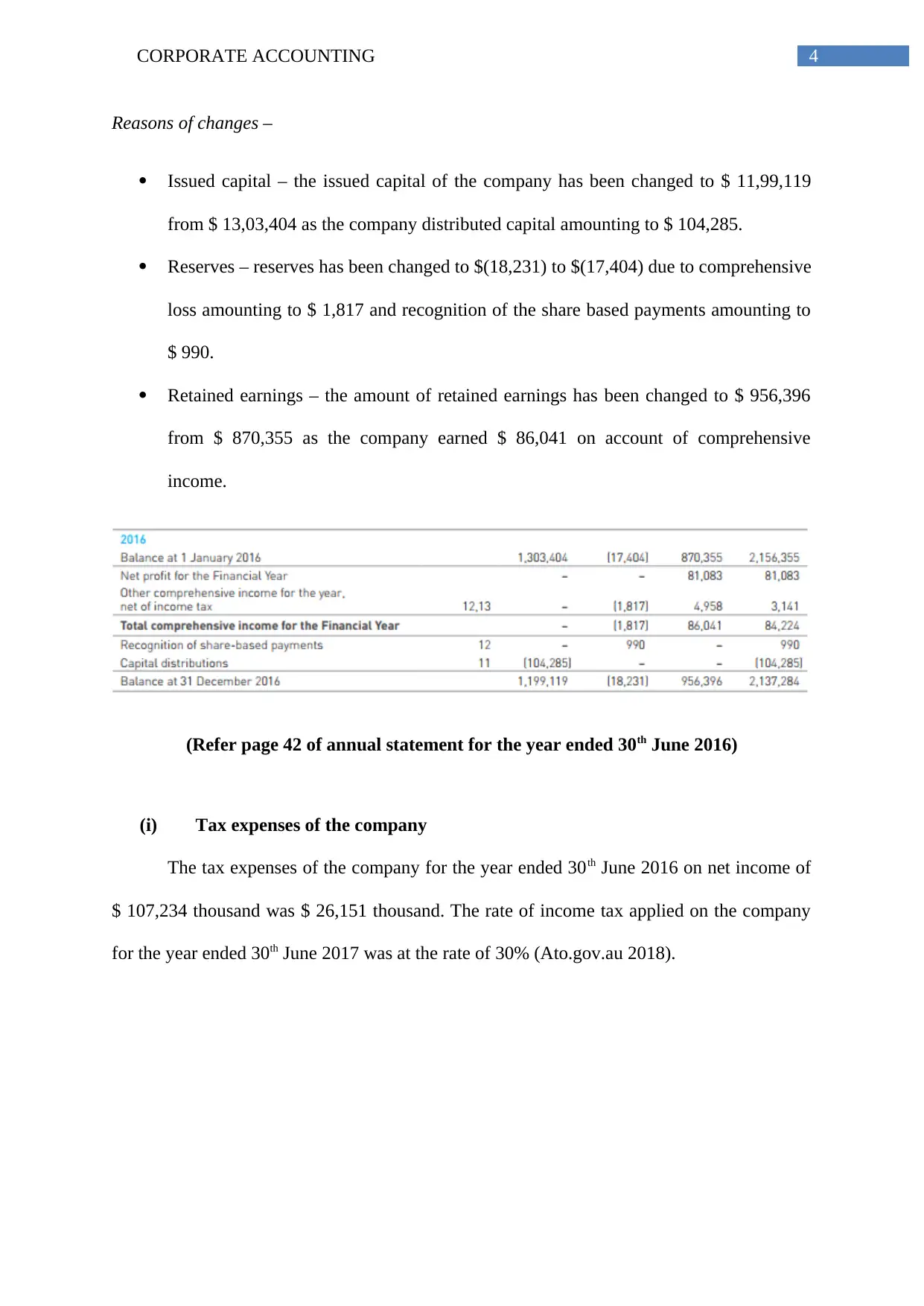

Reasons of changes –

Issued capital – the issued capital of the company has been changed to $ 11,99,119

from $ 13,03,404 as the company distributed capital amounting to $ 104,285.

Reserves – reserves has been changed to $(18,231) to $(17,404) due to comprehensive

loss amounting to $ 1,817 and recognition of the share based payments amounting to

$ 990.

Retained earnings – the amount of retained earnings has been changed to $ 956,396

from $ 870,355 as the company earned $ 86,041 on account of comprehensive

income.

(Refer page 42 of annual statement for the year ended 30th June 2016)

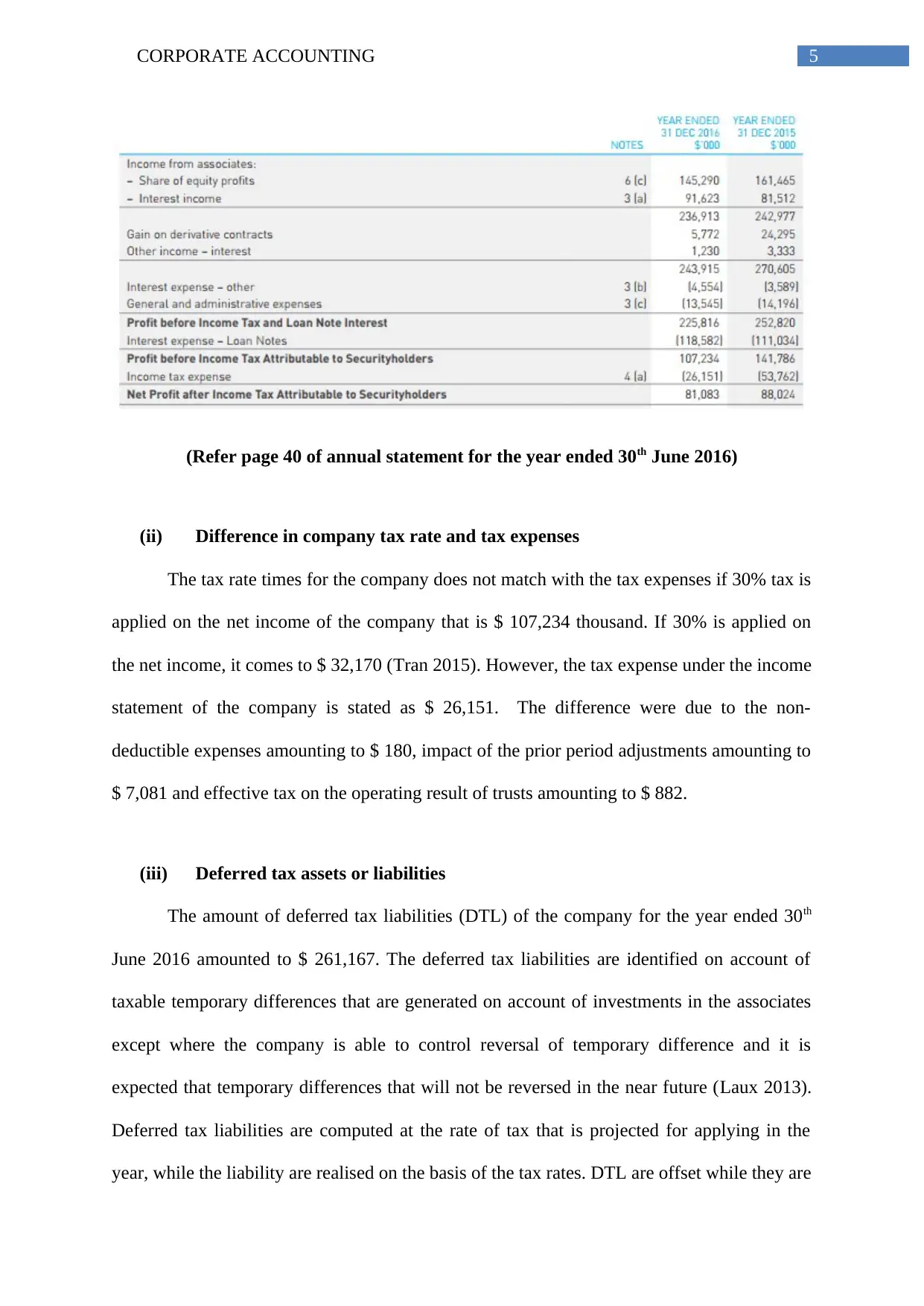

(i) Tax expenses of the company

The tax expenses of the company for the year ended 30th June 2016 on net income of

$ 107,234 thousand was $ 26,151 thousand. The rate of income tax applied on the company

for the year ended 30th June 2017 was at the rate of 30% (Ato.gov.au 2018).

Reasons of changes –

Issued capital – the issued capital of the company has been changed to $ 11,99,119

from $ 13,03,404 as the company distributed capital amounting to $ 104,285.

Reserves – reserves has been changed to $(18,231) to $(17,404) due to comprehensive

loss amounting to $ 1,817 and recognition of the share based payments amounting to

$ 990.

Retained earnings – the amount of retained earnings has been changed to $ 956,396

from $ 870,355 as the company earned $ 86,041 on account of comprehensive

income.

(Refer page 42 of annual statement for the year ended 30th June 2016)

(i) Tax expenses of the company

The tax expenses of the company for the year ended 30th June 2016 on net income of

$ 107,234 thousand was $ 26,151 thousand. The rate of income tax applied on the company

for the year ended 30th June 2017 was at the rate of 30% (Ato.gov.au 2018).

5CORPORATE ACCOUNTING

(Refer page 40 of annual statement for the year ended 30th June 2016)

(ii) Difference in company tax rate and tax expenses

The tax rate times for the company does not match with the tax expenses if 30% tax is

applied on the net income of the company that is $ 107,234 thousand. If 30% is applied on

the net income, it comes to $ 32,170 (Tran 2015). However, the tax expense under the income

statement of the company is stated as $ 26,151. The difference were due to the non-

deductible expenses amounting to $ 180, impact of the prior period adjustments amounting to

$ 7,081 and effective tax on the operating result of trusts amounting to $ 882.

(iii) Deferred tax assets or liabilities

The amount of deferred tax liabilities (DTL) of the company for the year ended 30th

June 2016 amounted to $ 261,167. The deferred tax liabilities are identified on account of

taxable temporary differences that are generated on account of investments in the associates

except where the company is able to control reversal of temporary difference and it is

expected that temporary differences that will not be reversed in the near future (Laux 2013).

Deferred tax liabilities are computed at the rate of tax that is projected for applying in the

year, while the liability are realised on the basis of the tax rates. DTL are offset while they are

(Refer page 40 of annual statement for the year ended 30th June 2016)

(ii) Difference in company tax rate and tax expenses

The tax rate times for the company does not match with the tax expenses if 30% tax is

applied on the net income of the company that is $ 107,234 thousand. If 30% is applied on

the net income, it comes to $ 32,170 (Tran 2015). However, the tax expense under the income

statement of the company is stated as $ 26,151. The difference were due to the non-

deductible expenses amounting to $ 180, impact of the prior period adjustments amounting to

$ 7,081 and effective tax on the operating result of trusts amounting to $ 882.

(iii) Deferred tax assets or liabilities

The amount of deferred tax liabilities (DTL) of the company for the year ended 30th

June 2016 amounted to $ 261,167. The deferred tax liabilities are identified on account of

taxable temporary differences that are generated on account of investments in the associates

except where the company is able to control reversal of temporary difference and it is

expected that temporary differences that will not be reversed in the near future (Laux 2013).

Deferred tax liabilities are computed at the rate of tax that is projected for applying in the

year, while the liability are realised on the basis of the tax rates. DTL are offset while they are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

related to the income taxes applied by the same authority for taxation and the group that is

intended for settling the current tax liabilities on the net basis (Mullinova and Simonyants

2016).

(Refer page 41 of annual statement for the year ended 30th June 2016)

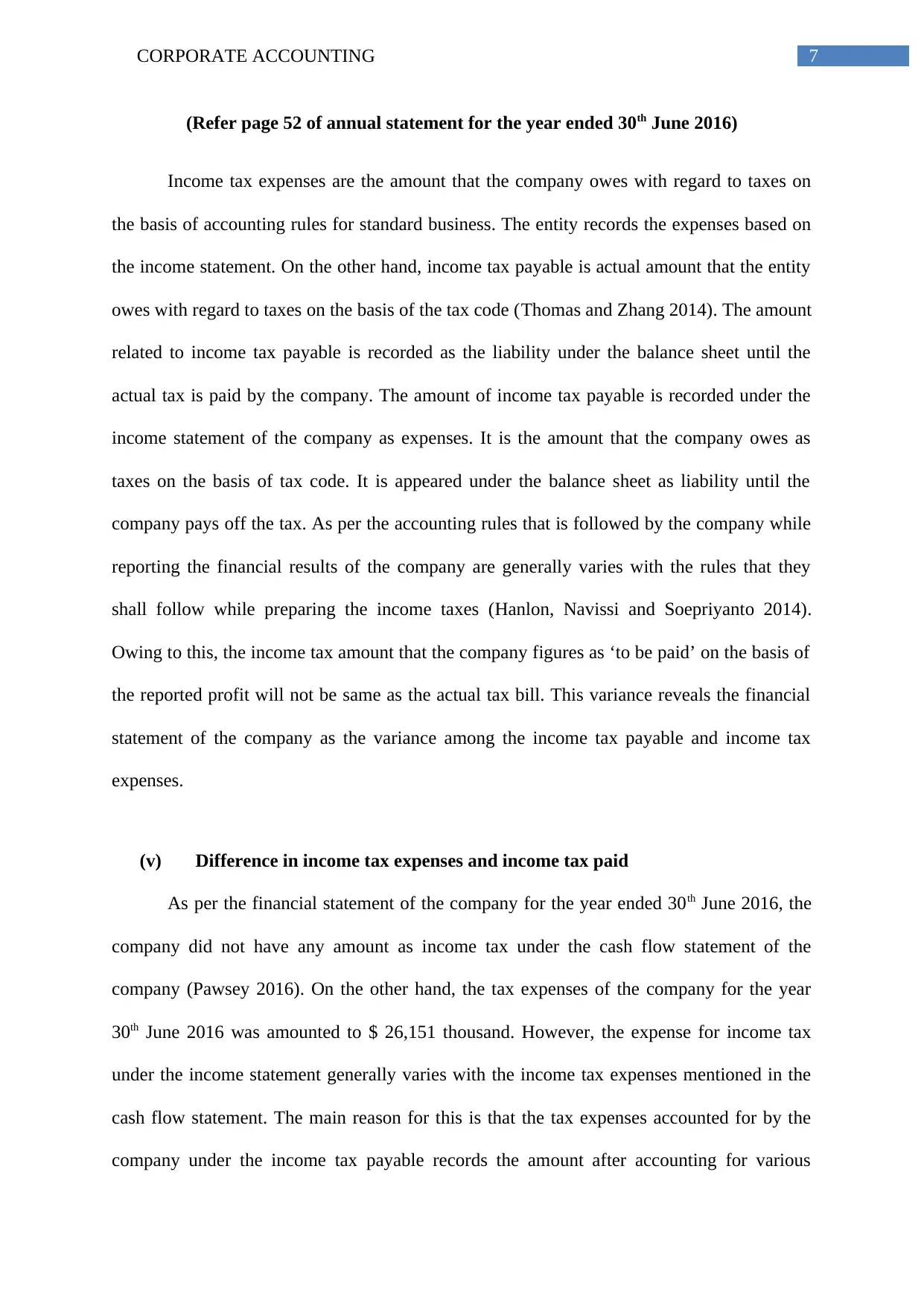

(iv) Current tax or income tax payable

Current tax is measured by referencing the income tax payable amount or recoverable

amount with regard to the tax loss or taxable profit for the accounting year. It is computed

through using the tax laws and tax rates that is the substantively enacted or enacted at the

reporting date. For the prior period or current period the current tax is identified as the

liability or as the asset to the extent of the refundable or unpaid amount. Current tax is

recognised as the income or expenses under the profit and loss statement except where it is

associated with the debited or credited items that is directly debited or credited to equity. The

current tax of the company for the year ended 30th June 2016 amounted to $ 104,409

thousand. Out of the total amount of current tax, the amount of current tax with regard to the

current year was $ 241 thousand whereas, the amount of adjustments that was recognized

with regard to the income tax for the prior years were amounted to $ 104,409.

related to the income taxes applied by the same authority for taxation and the group that is

intended for settling the current tax liabilities on the net basis (Mullinova and Simonyants

2016).

(Refer page 41 of annual statement for the year ended 30th June 2016)

(iv) Current tax or income tax payable

Current tax is measured by referencing the income tax payable amount or recoverable

amount with regard to the tax loss or taxable profit for the accounting year. It is computed

through using the tax laws and tax rates that is the substantively enacted or enacted at the

reporting date. For the prior period or current period the current tax is identified as the

liability or as the asset to the extent of the refundable or unpaid amount. Current tax is

recognised as the income or expenses under the profit and loss statement except where it is

associated with the debited or credited items that is directly debited or credited to equity. The

current tax of the company for the year ended 30th June 2016 amounted to $ 104,409

thousand. Out of the total amount of current tax, the amount of current tax with regard to the

current year was $ 241 thousand whereas, the amount of adjustments that was recognized

with regard to the income tax for the prior years were amounted to $ 104,409.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

(Refer page 52 of annual statement for the year ended 30th June 2016)

Income tax expenses are the amount that the company owes with regard to taxes on

the basis of accounting rules for standard business. The entity records the expenses based on

the income statement. On the other hand, income tax payable is actual amount that the entity

owes with regard to taxes on the basis of the tax code (Thomas and Zhang 2014). The amount

related to income tax payable is recorded as the liability under the balance sheet until the

actual tax is paid by the company. The amount of income tax payable is recorded under the

income statement of the company as expenses. It is the amount that the company owes as

taxes on the basis of tax code. It is appeared under the balance sheet as liability until the

company pays off the tax. As per the accounting rules that is followed by the company while

reporting the financial results of the company are generally varies with the rules that they

shall follow while preparing the income taxes (Hanlon, Navissi and Soepriyanto 2014).

Owing to this, the income tax amount that the company figures as ‘to be paid’ on the basis of

the reported profit will not be same as the actual tax bill. This variance reveals the financial

statement of the company as the variance among the income tax payable and income tax

expenses.

(v) Difference in income tax expenses and income tax paid

As per the financial statement of the company for the year ended 30th June 2016, the

company did not have any amount as income tax under the cash flow statement of the

company (Pawsey 2016). On the other hand, the tax expenses of the company for the year

30th June 2016 was amounted to $ 26,151 thousand. However, the expense for income tax

under the income statement generally varies with the income tax expenses mentioned in the

cash flow statement. The main reason for this is that the tax expenses accounted for by the

company under the income tax payable records the amount after accounting for various

(Refer page 52 of annual statement for the year ended 30th June 2016)

Income tax expenses are the amount that the company owes with regard to taxes on

the basis of accounting rules for standard business. The entity records the expenses based on

the income statement. On the other hand, income tax payable is actual amount that the entity

owes with regard to taxes on the basis of the tax code (Thomas and Zhang 2014). The amount

related to income tax payable is recorded as the liability under the balance sheet until the

actual tax is paid by the company. The amount of income tax payable is recorded under the

income statement of the company as expenses. It is the amount that the company owes as

taxes on the basis of tax code. It is appeared under the balance sheet as liability until the

company pays off the tax. As per the accounting rules that is followed by the company while

reporting the financial results of the company are generally varies with the rules that they

shall follow while preparing the income taxes (Hanlon, Navissi and Soepriyanto 2014).

Owing to this, the income tax amount that the company figures as ‘to be paid’ on the basis of

the reported profit will not be same as the actual tax bill. This variance reveals the financial

statement of the company as the variance among the income tax payable and income tax

expenses.

(v) Difference in income tax expenses and income tax paid

As per the financial statement of the company for the year ended 30th June 2016, the

company did not have any amount as income tax under the cash flow statement of the

company (Pawsey 2016). On the other hand, the tax expenses of the company for the year

30th June 2016 was amounted to $ 26,151 thousand. However, the expense for income tax

under the income statement generally varies with the income tax expenses mentioned in the

cash flow statement. The main reason for this is that the tax expenses accounted for by the

company under the income tax payable records the amount after accounting for various

8CORPORATE ACCOUNTING

expenses like, operating expenses, administrative expenses, selling expenses, financing

charges and various other expenses, if any (Gitman, Juchau and Flanagan 2015). The income

left after meeting all these expenses are taxed at the rate of 30% as per the Australian tax

code. On the other hand, the income tax recorded under the cash flow statement is the taxes

applicable on the operating activities of the company.

(vi) Confusing, interesting, difficult or surprising fact with regard to tax

treatment of the company

Confusing and difficult fact – while going through the annual report of the company for the

year ended 30th June 2016 was that the concept of deferred tax liabilities and deferred tax

assets. The deferred tax liabilities are identified on account of taxable temporary differences

that are generated on account of investments in the associates except where the company is

able to control reversal of temporary difference and it is expected that temporary differences

that will not be reversed in the near future. However, there are many controversies regarding

the ability to control reversal of temporary difference. There are no specified indication that

based on which it can be expected that the company will be able to control the reversal of

temporary differences. Further, the deferred tax liabilities or assets are computed at the rate of

tax that is projected for applying in the year, while the liability are realised on the basis of the

tax rates. Therefore, if the DTL or DTA is accounted for in one period and it is reversed in

another period then there will be difference in the applicable tax rate at which it is accounted

and at which it is reversed.

New insights – the new insights gained with regard to the income tax treatment by Spark

infrastructure is that all the revenues of the company are disclosed at top of the income

statement. All the expenses are then deducted from the revenues of the company to get the

operating income. From the operating income, the finance costs of the company are deducted

expenses like, operating expenses, administrative expenses, selling expenses, financing

charges and various other expenses, if any (Gitman, Juchau and Flanagan 2015). The income

left after meeting all these expenses are taxed at the rate of 30% as per the Australian tax

code. On the other hand, the income tax recorded under the cash flow statement is the taxes

applicable on the operating activities of the company.

(vi) Confusing, interesting, difficult or surprising fact with regard to tax

treatment of the company

Confusing and difficult fact – while going through the annual report of the company for the

year ended 30th June 2016 was that the concept of deferred tax liabilities and deferred tax

assets. The deferred tax liabilities are identified on account of taxable temporary differences

that are generated on account of investments in the associates except where the company is

able to control reversal of temporary difference and it is expected that temporary differences

that will not be reversed in the near future. However, there are many controversies regarding

the ability to control reversal of temporary difference. There are no specified indication that

based on which it can be expected that the company will be able to control the reversal of

temporary differences. Further, the deferred tax liabilities or assets are computed at the rate of

tax that is projected for applying in the year, while the liability are realised on the basis of the

tax rates. Therefore, if the DTL or DTA is accounted for in one period and it is reversed in

another period then there will be difference in the applicable tax rate at which it is accounted

and at which it is reversed.

New insights – the new insights gained with regard to the income tax treatment by Spark

infrastructure is that all the revenues of the company are disclosed at top of the income

statement. All the expenses are then deducted from the revenues of the company to get the

operating income. From the operating income, the finance costs of the company are deducted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

to obtain the amount of taxable income. On the taxable income the tax is deducted at the

prescribed rate to get the net income after tax. The income tax expenses are recorded as the

deduction under the income statement as income tax expense. One more insight gained is that

the expense amount owing to the accrual accounting rules that varies with the rules needed

for filing the returns on tax. In other words, the expenses associated with the income tax are

matched with the revenues that generate the expenses irrespective of the amount of tax paid

or returned.

Therefore, it is concluded from the above discussion that the company follows the

requirement of Australian Tax Office (ATO) for applying the tax rate and treating the tax on

various aspects. Further, the company disclosed proper justification and details regarding all

the tax treatments through notes to the financial statements. The tax matters of the company

are reviewed as the part of audits. Further, the company records the assets, expenses and

revenues after deducting the applicable goods and services tax (GST). Moreover, the current

tax is measured by referencing the income tax payable amount or recoverable amount with

regard to the tax loss or taxable profit for the accounting year. It is computed through using

the tax laws and tax rates that is the substantively enacted or enacted at the reporting date.

Therefore, the company follows all the requirements of ATO while treating various taxes

under the financial statement.

to obtain the amount of taxable income. On the taxable income the tax is deducted at the

prescribed rate to get the net income after tax. The income tax expenses are recorded as the

deduction under the income statement as income tax expense. One more insight gained is that

the expense amount owing to the accrual accounting rules that varies with the rules needed

for filing the returns on tax. In other words, the expenses associated with the income tax are

matched with the revenues that generate the expenses irrespective of the amount of tax paid

or returned.

Therefore, it is concluded from the above discussion that the company follows the

requirement of Australian Tax Office (ATO) for applying the tax rate and treating the tax on

various aspects. Further, the company disclosed proper justification and details regarding all

the tax treatments through notes to the financial statements. The tax matters of the company

are reviewed as the part of audits. Further, the company records the assets, expenses and

revenues after deducting the applicable goods and services tax (GST). Moreover, the current

tax is measured by referencing the income tax payable amount or recoverable amount with

regard to the tax loss or taxable profit for the accounting year. It is computed through using

the tax laws and tax rates that is the substantively enacted or enacted at the reporting date.

Therefore, the company follows all the requirements of ATO while treating various taxes

under the financial statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Reference

Ato.gov.au., 2018. Home page. [online] Available at: https://www.ato.gov.au/ [Accessed 22

Jan. 2018].

Bodie, Z., Kane, A. and Marcus, A.J., 2014. Investments, 10e. McGraw-Hill Education.

Dhaliwal, D., Judd, J.S., Serfling, M. and Shaikh, S., 2016. Customer concentration risk and

the cost of equity capital. Journal of Accounting and Economics, 61(1), pp.23-48.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hanlon, D., Navissi, F. and Soepriyanto, G., 2014. The value relevance of deferred tax

attributed to asset revaluations. Journal of Contemporary Accounting & Economics, 10(2),

pp.87-99.

Hutchens, M. and Rego, S., 2013. Tax risk and the cost of equity capital. Available at SSRN9.

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), pp.1357-1383.

Mullinova, S. and Simonyants, N., 2016. Reflection of a deferred tax liability in the credit

union reporting according to IFRS (IAS) 12 “Income taxes”. Modern European Researches,

(1), pp.83-88.

Pawsey, N., 2016. Project: Review of IFRS adoption in Australia.

Spark Infrastructure., 2018. Spark Infrastructure. [online] Available at:

https://www.sparkinfrastructure.com/ [Accessed 22 Jan. 2018].

Reference

Ato.gov.au., 2018. Home page. [online] Available at: https://www.ato.gov.au/ [Accessed 22

Jan. 2018].

Bodie, Z., Kane, A. and Marcus, A.J., 2014. Investments, 10e. McGraw-Hill Education.

Dhaliwal, D., Judd, J.S., Serfling, M. and Shaikh, S., 2016. Customer concentration risk and

the cost of equity capital. Journal of Accounting and Economics, 61(1), pp.23-48.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hanlon, D., Navissi, F. and Soepriyanto, G., 2014. The value relevance of deferred tax

attributed to asset revaluations. Journal of Contemporary Accounting & Economics, 10(2),

pp.87-99.

Hutchens, M. and Rego, S., 2013. Tax risk and the cost of equity capital. Available at SSRN9.

Laux, R.C., 2013. The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), pp.1357-1383.

Mullinova, S. and Simonyants, N., 2016. Reflection of a deferred tax liability in the credit

union reporting according to IFRS (IAS) 12 “Income taxes”. Modern European Researches,

(1), pp.83-88.

Pawsey, N., 2016. Project: Review of IFRS adoption in Australia.

Spark Infrastructure., 2018. Spark Infrastructure. [online] Available at:

https://www.sparkinfrastructure.com/ [Accessed 22 Jan. 2018].

11CORPORATE ACCOUNTING

Thomas, J. and Zhang, F., 2014. Valuation of tax expense. Review of Accounting

Studies, 19(4), pp.1436-1467.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia?. Browser Download This Paper.

Thomas, J. and Zhang, F., 2014. Valuation of tax expense. Review of Accounting

Studies, 19(4), pp.1436-1467.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia?. Browser Download This Paper.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.