Detailed Analysis of Corporate Accounting and Reporting Issues

VerifiedAdded on 2021/05/31

|13

|2743

|24

Report

AI Summary

This report comprehensively examines corporate accounting and reporting, focusing on share forfeiture and impairment of assets. It begins with an introduction to the advantages of issuing shares in installments and the procedures for accounting for share forfeiture and reissue, including the necessary notices and journal entries. The report details the accounting treatment for forfeited shares, including the impact on share capital and the issuance of shares at a premium. Part B of the report then presents an analysis of an impairment loss, including calculations and journal entries. The report provides insights into the Corporations Act 2001 and the importance of financial reporting in the Australian context. It also includes journal entries for recording the applications received and assets' carrying amount. The report concludes with a summary of the key findings and implications of the analysis.

Running head: CORPORATE ACCOUNTING AND REPORTING

Corporate Accounting and Reporting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting and Reporting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING AND REPORTING

Table of Contents

Answer to Part A:...............................................................................................................2

Introduction:...................................................................................................................2

Accounting for forfeiture and reissue of shares:............................................................2

Conclusion:.....................................................................................................................8

Answer to Part B:...............................................................................................................8

References:......................................................................................................................12

Table of Contents

Answer to Part A:...............................................................................................................2

Introduction:...................................................................................................................2

Accounting for forfeiture and reissue of shares:............................................................2

Conclusion:.....................................................................................................................8

Answer to Part B:...............................................................................................................8

References:......................................................................................................................12

2CORPORATE ACCOUNTING AND REPORTING

Answer to Part A:

Introduction:

There are certain advantages of issuing shares in the form of instalments. One of

them is that it is possible for the investors to purchase many shares by not paying the

lump sum amount at once like certain number of instalments made for purchasing

assets. However, the organisations are deemed to have legally binding commitments

for making payment of the calls made (Jena, Mishra and Rajib 2016). In case, a

shareholder fails to pay allotted money or a part or call by the stipulated fixed amount

for payment, the board of directors of the organisation progress in forfeiting the shares

on which allotted money or call has been in-arrear.

Accounting for forfeiture and reissue of shares:

There are certain procedures related to accounting for forfeiture and reissue of

shares. In such instances, a notice needs to be provided to the defaulter by asking the

person to clear the unsettled amount along with the accrued interest at a certain point of

time. There is another significant aspect that needs to be mentioned in the notice as

well.

It needs to inform the defaulter that if the payment is not made within the

stipulated time before the due date, the shares for which the notice is served would be

forfeited (Beams, Brozovsky and Shoulders 2017). During the time of share forfeiture,

the name of the shareholder would be removed from the member register and the

amount incurred by the individual on shares is forfeited to the organisation. This could

be treated in the form of capital gain and the amount would be credited to the “Forfeited

Answer to Part A:

Introduction:

There are certain advantages of issuing shares in the form of instalments. One of

them is that it is possible for the investors to purchase many shares by not paying the

lump sum amount at once like certain number of instalments made for purchasing

assets. However, the organisations are deemed to have legally binding commitments

for making payment of the calls made (Jena, Mishra and Rajib 2016). In case, a

shareholder fails to pay allotted money or a part or call by the stipulated fixed amount

for payment, the board of directors of the organisation progress in forfeiting the shares

on which allotted money or call has been in-arrear.

Accounting for forfeiture and reissue of shares:

There are certain procedures related to accounting for forfeiture and reissue of

shares. In such instances, a notice needs to be provided to the defaulter by asking the

person to clear the unsettled amount along with the accrued interest at a certain point of

time. There is another significant aspect that needs to be mentioned in the notice as

well.

It needs to inform the defaulter that if the payment is not made within the

stipulated time before the due date, the shares for which the notice is served would be

forfeited (Beams, Brozovsky and Shoulders 2017). During the time of share forfeiture,

the name of the shareholder would be removed from the member register and the

amount incurred by the individual on shares is forfeited to the organisation. This could

be treated in the form of capital gain and the amount would be credited to the “Forfeited

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING AND REPORTING

Shares Account”. There is possibility of reissuing the forfeited shares at a loss.

However, the loss incurred on reissuance could not exceed the profit made on forfeiture

of the reissued shares. Moreover, it is necessary to consider certain provisions

associated with the forfeiture and reissue of shares and they are briefly discussed as

follows:

Firstly, if any shareholder could not pay any call or instalment related on or

before the stipulated date, the board of the organisation has the right to provide a notice

to the individual asking for payment (Carnegie and O’Connell 2014). In addition, the

individual is needed to make the interest payment as well, which is accrued on or before

the stipulated timeframe. Secondly, the notice to be sent to the defaulter would

comprise of certain components within the same. An additional date after the due date

would be provided on which the shareholders needs to make the overall outstanding

payment, as per the notice. In case, if the shareholder misses the due date again or

event of non-payment takes place, the shares in relation to which the call has been

made would be liable to be forfeited. If the defaulter does not meet any of the

requirements mentioned in the notice, the board would forfeit the shares of the defaulter

and the decision would come into effect (Collier 2015).

Once the decision of forfeiture is taken, the shares could be sold or disposed on

certain terms and conditions, as deemed appropriate by the board of the organisation.

However, it needs to be mentioned that before selling or disposing the shares, the

board has the full right of cancelling the forfeiture on certain terms as deemed fit. It

might sometimes happen that when a shareholder realises about the inability of paying

the calls made, the individual has an option of surrendering the shares voluntarily to the

Shares Account”. There is possibility of reissuing the forfeited shares at a loss.

However, the loss incurred on reissuance could not exceed the profit made on forfeiture

of the reissued shares. Moreover, it is necessary to consider certain provisions

associated with the forfeiture and reissue of shares and they are briefly discussed as

follows:

Firstly, if any shareholder could not pay any call or instalment related on or

before the stipulated date, the board of the organisation has the right to provide a notice

to the individual asking for payment (Carnegie and O’Connell 2014). In addition, the

individual is needed to make the interest payment as well, which is accrued on or before

the stipulated timeframe. Secondly, the notice to be sent to the defaulter would

comprise of certain components within the same. An additional date after the due date

would be provided on which the shareholders needs to make the overall outstanding

payment, as per the notice. In case, if the shareholder misses the due date again or

event of non-payment takes place, the shares in relation to which the call has been

made would be liable to be forfeited. If the defaulter does not meet any of the

requirements mentioned in the notice, the board would forfeit the shares of the defaulter

and the decision would come into effect (Collier 2015).

Once the decision of forfeiture is taken, the shares could be sold or disposed on

certain terms and conditions, as deemed appropriate by the board of the organisation.

However, it needs to be mentioned that before selling or disposing the shares, the

board has the full right of cancelling the forfeiture on certain terms as deemed fit. It

might sometimes happen that when a shareholder realises about the inability of paying

the calls made, the individual has an option of surrendering the shares voluntarily to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING AND REPORTING

organisation (Dagwell, Wines and Lambert 2015). The impact related to surrender of

shares is identical to that of forfeiture. The only difference is that at the time of

surrender, the shareholder undertakes the initiative and the organisation need not have

to make the formality of serving the notice and waiting until the end of the stipulated

period.

Even though it is possible for the organisation to cancel the forfeited shares, they

might intend to issue the shares again. The reissue accounting would be identical as in

the case for reissue. However, there would be difference in conditions between the two

situations. For instance, the shares forfeited on the part of an organisation might be

utilised for one-time payment, instead of instalments (Lyons 2018). At the time of

dealing with the issue of forfeited shares, it is necessary to take into account the overall

number of shares and the desired impact on share capital. As per the recent changes in

the Corporations Act 2001, all the Australian business organisations are needed to

disclose their overall capital amounts and its composition in respect of the number of

shares. This denotes the authorised capital of an organisation and it is restricted to

issue any further capital. This could be identified as the nominal or par share value and

it is the share amount at the incorporated date. The only funds that an organisation

obtains from issuance of shares include those from the initial issue. The owners of the

shares obtain considerable benefits with the increase in the share values.

Various journal entries are inherent related to forfeiture and reissue of shares. At

the time shares issued at par are forfeited, it is necessary to ascertain the amount with

which credit has been made to the Share Capital Account. This amount could be

divided into two portions. These include the amount obtained and the amount not

organisation (Dagwell, Wines and Lambert 2015). The impact related to surrender of

shares is identical to that of forfeiture. The only difference is that at the time of

surrender, the shareholder undertakes the initiative and the organisation need not have

to make the formality of serving the notice and waiting until the end of the stipulated

period.

Even though it is possible for the organisation to cancel the forfeited shares, they

might intend to issue the shares again. The reissue accounting would be identical as in

the case for reissue. However, there would be difference in conditions between the two

situations. For instance, the shares forfeited on the part of an organisation might be

utilised for one-time payment, instead of instalments (Lyons 2018). At the time of

dealing with the issue of forfeited shares, it is necessary to take into account the overall

number of shares and the desired impact on share capital. As per the recent changes in

the Corporations Act 2001, all the Australian business organisations are needed to

disclose their overall capital amounts and its composition in respect of the number of

shares. This denotes the authorised capital of an organisation and it is restricted to

issue any further capital. This could be identified as the nominal or par share value and

it is the share amount at the incorporated date. The only funds that an organisation

obtains from issuance of shares include those from the initial issue. The owners of the

shares obtain considerable benefits with the increase in the share values.

Various journal entries are inherent related to forfeiture and reissue of shares. At

the time shares issued at par are forfeited, it is necessary to ascertain the amount with

which credit has been made to the Share Capital Account. This amount could be

divided into two portions. These include the amount obtained and the amount not

5CORPORATE ACCOUNTING AND REPORTING

obtained due to which the forfeiture of shares is conducted. The received amount could

be considered as a capital gain for the organisation and it is to be credited to the Share

Forfeiture Account. The amount not obtained might fall in Calls-in-Arrear Account. In

case, the organisation does not have any Calls-in-Arrear Account, credit could be made

to share allotment accounts or other call accounts (Fogarty, Zimmerman and

Richardson 2016). For example, it is assumed that an organisation issues equity shares

of $10 each at par. An additional assumption is made that the allotted and applications

amounts are obtained at $2.50 per share each in relation to all the shares. However, the

first call and the second call are $3 per share and $2 per share respectively and they

are not obtained in relation to 500 shares, which are forfeited. If there is no Calls-in-

Arrear Account, the journal entry for forfeiting the shares is discussed as follows:

Equity Share Capital Account................................Dr $5,000

To Equity Share First Call Account $1,500

To Equity Share Second Call Account $1,000

To Forfeited Shares Account $2,500

The narration for the above-stated journal entry would be the receipt of

application and allotted amounts at $5 per share for not paying the first call at $3 per

share and the last two calls at $2 per share (Garrett 2018). If the amounts that are not

obtained on the non-repayment of the first two calls are transferred to Calls-in-Arrear

Account, there is no need for “Equity Share First Call Account” and “Equity Share

Second Call Account”. Instead, the Calls-in-Arrear Account could be used to replace

obtained due to which the forfeiture of shares is conducted. The received amount could

be considered as a capital gain for the organisation and it is to be credited to the Share

Forfeiture Account. The amount not obtained might fall in Calls-in-Arrear Account. In

case, the organisation does not have any Calls-in-Arrear Account, credit could be made

to share allotment accounts or other call accounts (Fogarty, Zimmerman and

Richardson 2016). For example, it is assumed that an organisation issues equity shares

of $10 each at par. An additional assumption is made that the allotted and applications

amounts are obtained at $2.50 per share each in relation to all the shares. However, the

first call and the second call are $3 per share and $2 per share respectively and they

are not obtained in relation to 500 shares, which are forfeited. If there is no Calls-in-

Arrear Account, the journal entry for forfeiting the shares is discussed as follows:

Equity Share Capital Account................................Dr $5,000

To Equity Share First Call Account $1,500

To Equity Share Second Call Account $1,000

To Forfeited Shares Account $2,500

The narration for the above-stated journal entry would be the receipt of

application and allotted amounts at $5 per share for not paying the first call at $3 per

share and the last two calls at $2 per share (Garrett 2018). If the amounts that are not

obtained on the non-repayment of the first two calls are transferred to Calls-in-Arrear

Account, there is no need for “Equity Share First Call Account” and “Equity Share

Second Call Account”. Instead, the Calls-in-Arrear Account could be used to replace

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING AND REPORTING

them. For this scenario, a change in the journal entry is obvious, which is depicted as

follows:

Equity Share Capital Account................................Dr $5,000

To Calls-in-Arrear Account $1,500

To Forfeited Shares Account $2,500

The journal entry would have the same narration as in the previous case.

Alternatively, the call amount in relation to forfeited shares is credited to Forfeited

Shares Account and debit would be made to Share Capital Account (Jain 2014).

In case, the market price of the shares is greater in contrast to their par value, it

is quite obvious that the organisation would intend to seek advantage of the situation.

As a result, it might issue shares at a price, which is more than the par value. This

situation could be defined as issuing shares at premium (Rani 2014). However, the

current Australian law does not require the ASX listed business organisations to have

authorised capital or par value shares. If they seek permission from the constitutions,

they are allowed to issue additional shares in the market at a bearable price. However,

the legal changes are not retrospective, as there are a number of business

organisations having amounts in their books of accounts, which could be considered as

share premium reserve or share premium account. These are the additional amounts

obtained in excess of par values, which the organisations have obtained from issuing

shares. Moreover, they need to keep aside this amount from share and issued capital

(Saini 2015). Since there are no par values of the shares, the amount obtained from

share issues for future would raise the overall share capital.

them. For this scenario, a change in the journal entry is obvious, which is depicted as

follows:

Equity Share Capital Account................................Dr $5,000

To Calls-in-Arrear Account $1,500

To Forfeited Shares Account $2,500

The journal entry would have the same narration as in the previous case.

Alternatively, the call amount in relation to forfeited shares is credited to Forfeited

Shares Account and debit would be made to Share Capital Account (Jain 2014).

In case, the market price of the shares is greater in contrast to their par value, it

is quite obvious that the organisation would intend to seek advantage of the situation.

As a result, it might issue shares at a price, which is more than the par value. This

situation could be defined as issuing shares at premium (Rani 2014). However, the

current Australian law does not require the ASX listed business organisations to have

authorised capital or par value shares. If they seek permission from the constitutions,

they are allowed to issue additional shares in the market at a bearable price. However,

the legal changes are not retrospective, as there are a number of business

organisations having amounts in their books of accounts, which could be considered as

share premium reserve or share premium account. These are the additional amounts

obtained in excess of par values, which the organisations have obtained from issuing

shares. Moreover, they need to keep aside this amount from share and issued capital

(Saini 2015). Since there are no par values of the shares, the amount obtained from

share issues for future would raise the overall share capital.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING AND REPORTING

An illustration could be considered here, in which a business organisation had

issued shares at $1 each in the past. However, at present, it is planning to issue

1,000,000 new ordinary shares for $1.50 each. The amounts are to be incurred entirely

on application and anyone having plans to make investments would have to pay $1.50

for every share. If it is assumed that the shares are subscribed fully, the journal entries

for recording the applications received would be the following:

Bank Trust Account...........................................Dr $1,500,000

To Application Account $1,500,000

(Amount obtained for share application)

Application Account...........................................Dr $1,500,000

To Share Capital Account $1,500,000

(Shares issued at $1.50 per share)

Bank Account...........................................Dr $1,500,000

To Bank Trust Account $1,500,000

(Amounts obtained transferred on issuance of shares)

On the other hand, according to the Australian regulations, the proprietary firms

are not allowed to provide shares to the public. This is because they are considered as

private issues and they could be sold to certain group of purchasers only. However, a

public listed entity could sell shares privately, if it obtains the necessary permission from

the Australian constitution. The large institutional investors could purchase the shares

An illustration could be considered here, in which a business organisation had

issued shares at $1 each in the past. However, at present, it is planning to issue

1,000,000 new ordinary shares for $1.50 each. The amounts are to be incurred entirely

on application and anyone having plans to make investments would have to pay $1.50

for every share. If it is assumed that the shares are subscribed fully, the journal entries

for recording the applications received would be the following:

Bank Trust Account...........................................Dr $1,500,000

To Application Account $1,500,000

(Amount obtained for share application)

Application Account...........................................Dr $1,500,000

To Share Capital Account $1,500,000

(Shares issued at $1.50 per share)

Bank Account...........................................Dr $1,500,000

To Bank Trust Account $1,500,000

(Amounts obtained transferred on issuance of shares)

On the other hand, according to the Australian regulations, the proprietary firms

are not allowed to provide shares to the public. This is because they are considered as

private issues and they could be sold to certain group of purchasers only. However, a

public listed entity could sell shares privately, if it obtains the necessary permission from

the Australian constitution. The large institutional investors could purchase the shares

8CORPORATE ACCOUNTING AND REPORTING

for avoiding the cost and time taken in an overall public issue. However, there are

restrictions on the part of ASX regarding the share percentage, which the listed public

organisations could issue privately.

An organisation might sell the right of purchasing a number of shares in the

organisation at a later point of time in future. Such right could be termed as the

company-issued call option. At the time an organisation is involved in issuing options for

few useful considerations, the equity of the shareholders would be increased from the

amount obtained (Thornton 2018).

Conclusion:

Based on the above discussion, it could be evaluated that In case, a shareholder

fails to pay allotted money or a part or call by the stipulated fixed amount for payment,

the board of directors of the organisation progress in forfeiting the shares on which

allotted money or call has been in-arrear. In case, the market price of the shares is

greater in contrast to their par value, it is quite obvious that the organisation would

intend to seek advantage of the situation. As a result, it might issue shares at a price,

which is more than the par value. This situation could be defined as issuing shares at

premium.

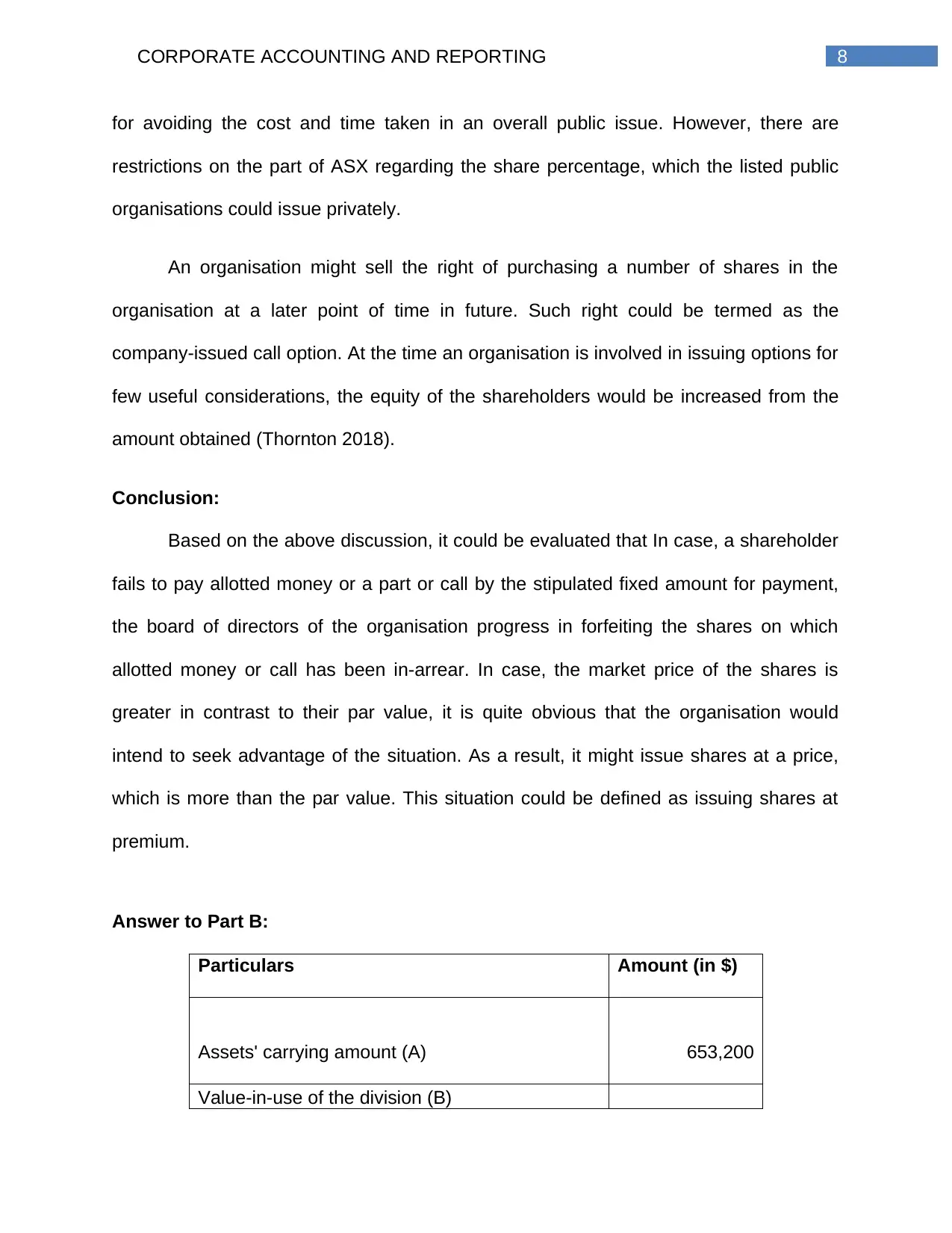

Answer to Part B:

Particulars Amount (in $)

Assets' carrying amount (A) 653,200

Value-in-use of the division (B)

for avoiding the cost and time taken in an overall public issue. However, there are

restrictions on the part of ASX regarding the share percentage, which the listed public

organisations could issue privately.

An organisation might sell the right of purchasing a number of shares in the

organisation at a later point of time in future. Such right could be termed as the

company-issued call option. At the time an organisation is involved in issuing options for

few useful considerations, the equity of the shareholders would be increased from the

amount obtained (Thornton 2018).

Conclusion:

Based on the above discussion, it could be evaluated that In case, a shareholder

fails to pay allotted money or a part or call by the stipulated fixed amount for payment,

the board of directors of the organisation progress in forfeiting the shares on which

allotted money or call has been in-arrear. In case, the market price of the shares is

greater in contrast to their par value, it is quite obvious that the organisation would

intend to seek advantage of the situation. As a result, it might issue shares at a price,

which is more than the par value. This situation could be defined as issuing shares at

premium.

Answer to Part B:

Particulars Amount (in $)

Assets' carrying amount (A) 653,200

Value-in-use of the division (B)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

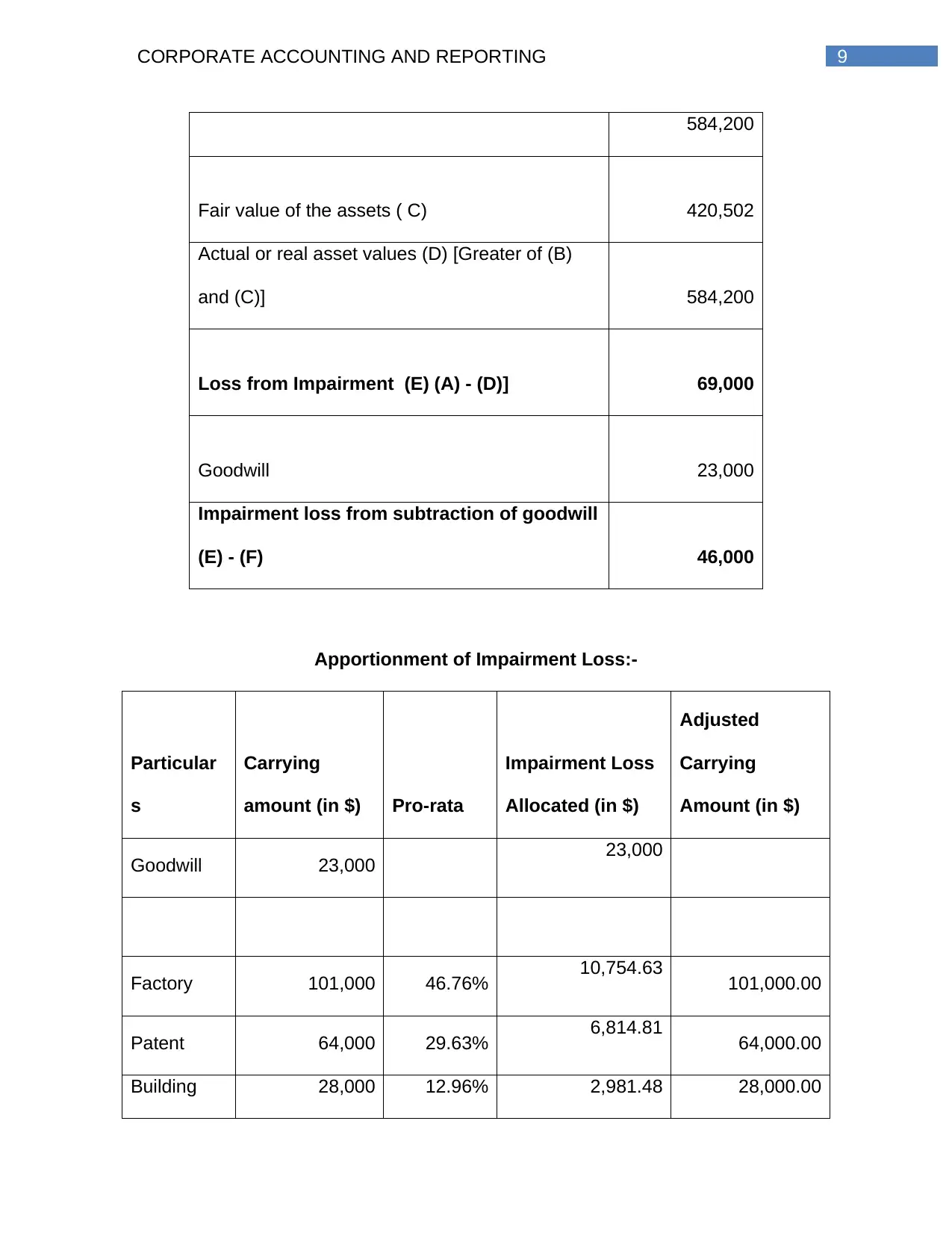

9CORPORATE ACCOUNTING AND REPORTING

584,200

Fair value of the assets ( C) 420,502

Actual or real asset values (D) [Greater of (B)

and (C)] 584,200

Loss from Impairment (E) (A) - (D)] 69,000

Goodwill 23,000

Impairment loss from subtraction of goodwill

(E) - (F) 46,000

Apportionment of Impairment Loss:-

Particular

s

Carrying

amount (in $) Pro-rata

Impairment Loss

Allocated (in $)

Adjusted

Carrying

Amount (in $)

Goodwill 23,000 23,000

Factory 101,000 46.76% 10,754.63 101,000.00

Patent 64,000 29.63% 6,814.81 64,000.00

Building 28,000 12.96% 2,981.48 28,000.00

584,200

Fair value of the assets ( C) 420,502

Actual or real asset values (D) [Greater of (B)

and (C)] 584,200

Loss from Impairment (E) (A) - (D)] 69,000

Goodwill 23,000

Impairment loss from subtraction of goodwill

(E) - (F) 46,000

Apportionment of Impairment Loss:-

Particular

s

Carrying

amount (in $) Pro-rata

Impairment Loss

Allocated (in $)

Adjusted

Carrying

Amount (in $)

Goodwill 23,000 23,000

Factory 101,000 46.76% 10,754.63 101,000.00

Patent 64,000 29.63% 6,814.81 64,000.00

Building 28,000 12.96% 2,981.48 28,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

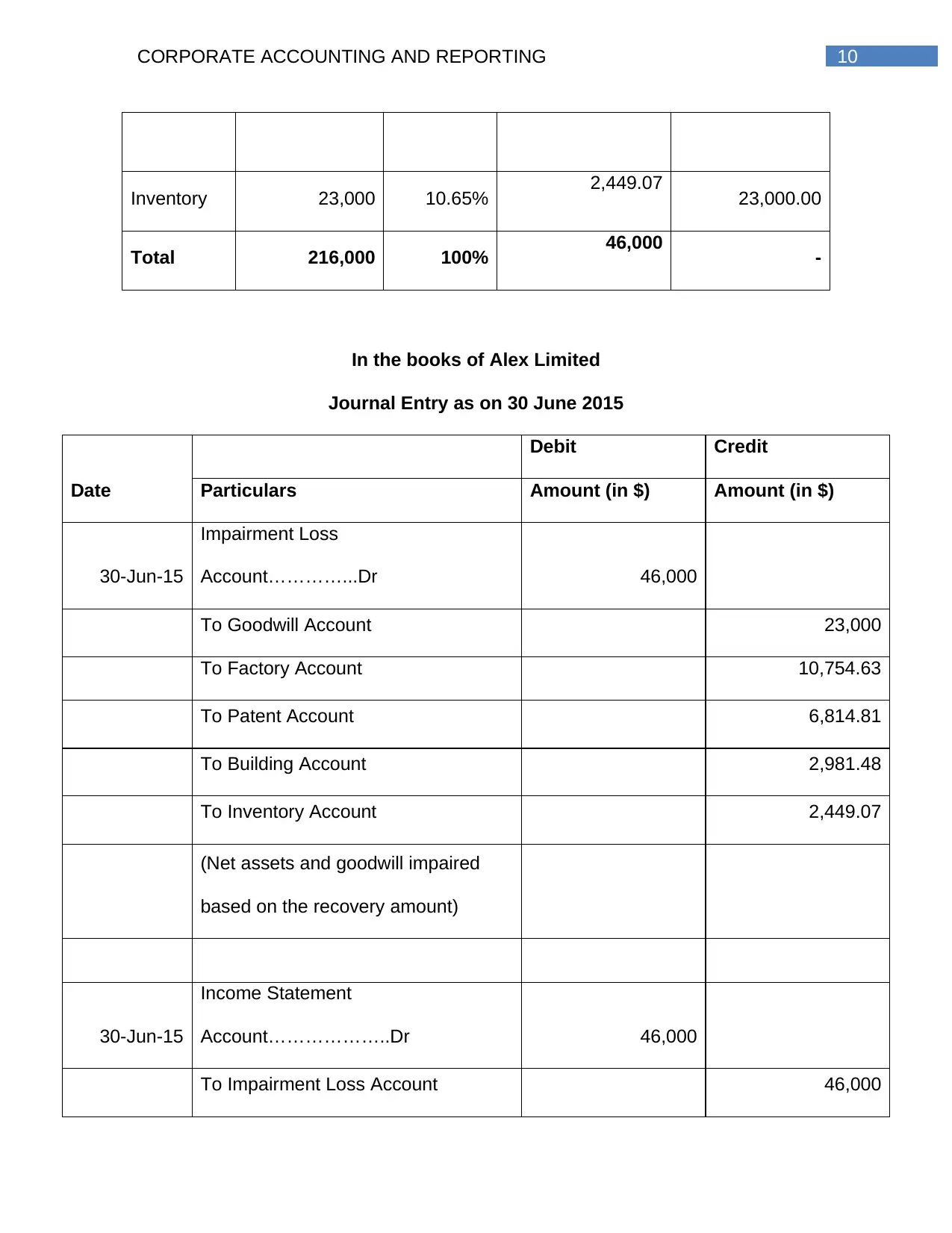

10CORPORATE ACCOUNTING AND REPORTING

Inventory 23,000 10.65% 2,449.07 23,000.00

Total 216,000 100% 46,000 -

In the books of Alex Limited

Journal Entry as on 30 June 2015

Date

Debit Credit

Particulars Amount (in $) Amount (in $)

30-Jun-15

Impairment Loss

Account…………...Dr 46,000

To Goodwill Account 23,000

To Factory Account 10,754.63

To Patent Account 6,814.81

To Building Account 2,981.48

To Inventory Account 2,449.07

(Net assets and goodwill impaired

based on the recovery amount)

30-Jun-15

Income Statement

Account………………..Dr 46,000

To Impairment Loss Account 46,000

Inventory 23,000 10.65% 2,449.07 23,000.00

Total 216,000 100% 46,000 -

In the books of Alex Limited

Journal Entry as on 30 June 2015

Date

Debit Credit

Particulars Amount (in $) Amount (in $)

30-Jun-15

Impairment Loss

Account…………...Dr 46,000

To Goodwill Account 23,000

To Factory Account 10,754.63

To Patent Account 6,814.81

To Building Account 2,981.48

To Inventory Account 2,449.07

(Net assets and goodwill impaired

based on the recovery amount)

30-Jun-15

Income Statement

Account………………..Dr 46,000

To Impairment Loss Account 46,000

11CORPORATE ACCOUNTING AND REPORTING

(Value of impairment loss reallocated

to the income statement)

(Value of impairment loss reallocated

to the income statement)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.