Corporate Accounting Analysis of Wesfarmers' Financial Statements

VerifiedAdded on 2021/05/31

|9

|866

|14

Report

AI Summary

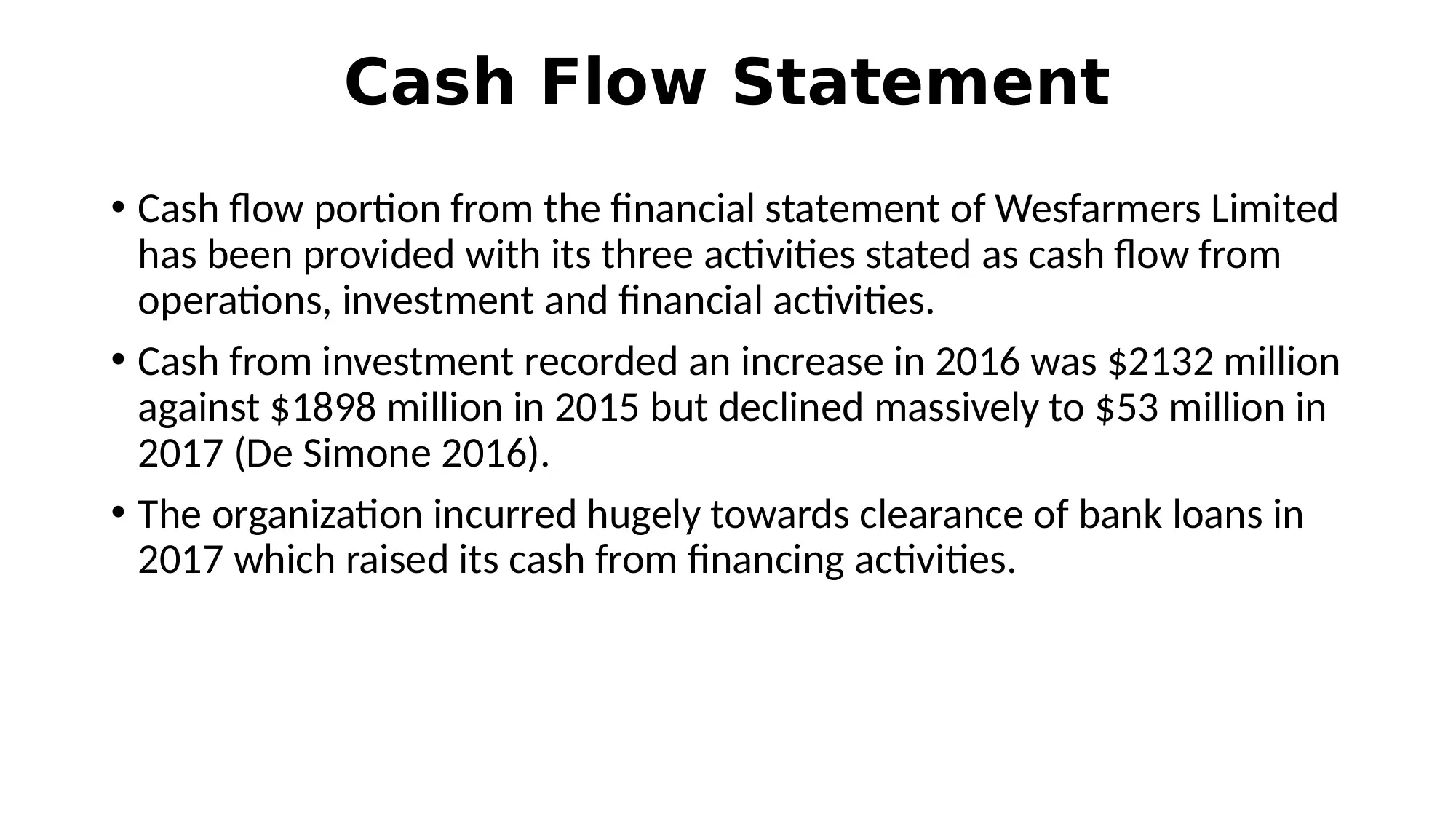

This report provides a detailed analysis of Wesfarmers Limited's corporate accounting practices. It begins with an examination of the cash flow statement, highlighting the company's activities in operations, investment, and financing. The analysis notes changes in investment activities due to asset sales and discusses the impact of loan terms on borrowing transactions. The report then delves into the other comprehensive income statement, outlining components such as foreign currency translation and retained earnings. It further explores the accounting for corporate income tax, including Wesfarmers' tax rate, tax assets, and liabilities, with a comparison of figures from income and cash flow statements. The report references the company's adherence to Australian tax regulations and identifies key dynamics influencing its tax treatment. References to relevant academic literature are included to support the analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.