Corporate Accounting: Cash Flow, Income, and Tax Analysis

VerifiedAdded on 2021/06/17

|13

|2782

|401

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices, specifically focusing on the cash flow statement, income statement, and tax implications for a listed company operating internationally, likely JB HI-FI. The report examines the classification of cash flows into operating, investing, and financing activities, highlighting the impact of non-cash items and dividend payments. It compares the income statement and cash flow statement, differentiating between items recognized in each. The analysis also delves into tax payments, deferred tax liabilities, and the reasons for differences between accounting profit and taxable income, referencing AASB 112. The report concludes with an examination of deferred tax assets and liabilities, providing insights into the company's financial performance and tax planning strategies. The report also highlights the differences between income tax payable and income tax payment and the treatment of tax as per AASB 112.

Corporate Accounting

Name of the student-

Topic- Corporate Accounting

University name

Name of the student-

Topic- Corporate Accounting

University name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

Table of Contents

Introduction...........................................................................................................................................3

Answer to question-1.............................................................................................................................3

Answer to question-2.............................................................................................................................4

Comparative analysis of the all three main flow of activities............................................................4

Answer to question no-3.......................................................................................................................4

Answer to question no-4.......................................................................................................................5

Answer to question no-5.......................................................................................................................5

Answer to question no-6.......................................................................................................................5

Answer to question no-7........................................................................................................................6

Explain, why this is with reason.............................................................................................................6

Answer to question no-8........................................................................................................................7

Answer to question no-9........................................................................................................................9

Why the income tax payment is not same with the income tax payable..........................................9

Answer to question no-10......................................................................................................................9

Answer to question no-11....................................................................................................................10

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

.

Table of Contents

Introduction...........................................................................................................................................3

Answer to question-1.............................................................................................................................3

Answer to question-2.............................................................................................................................4

Comparative analysis of the all three main flow of activities............................................................4

Answer to question no-3.......................................................................................................................4

Answer to question no-4.......................................................................................................................5

Answer to question no-5.......................................................................................................................5

Answer to question no-6.......................................................................................................................5

Answer to question no-7........................................................................................................................6

Explain, why this is with reason.............................................................................................................6

Answer to question no-8........................................................................................................................7

Answer to question no-9........................................................................................................................9

Why the income tax payment is not same with the income tax payable..........................................9

Answer to question no-10......................................................................................................................9

Answer to question no-11....................................................................................................................10

Conclusion...........................................................................................................................................11

References...........................................................................................................................................12

.

Corporate Accounting

Introduction

With the ramified economic changes and complex business structure, each and every

company is operating in the international market are following international financial

reporting framework. As this International rules and regulation has very complex structure

which require from company or entity to establish a separate compliance function like

internal audit department or audit committee and foam a policy to define role and

responsibility of such function or department. This report focuses on the analysing the cash

flow statement and recording of accounts as per the accounting rules and taxation rules. It is a

listed company operating in the international field which make it obligated to compliance

with domestic as well as international financial reporting framework.

Answer to question-1

Analysis of the Cash flow statement

Cash flow statement show the flow of the cash whether it is inflow or outflow , It include

the cash flow of current year as well as cash flow of the year as well as cash flow of the year

which is not related to relevant previous year. Cash flow statement classifies its activity in

three phases:-

Operating Activity which includes the flows of the cash which generate from operational

activity.

Investment activity includes the flow of cash from sale or purchases of any Immovable

property.

Financial activity includes the cash flow from financial activity like loan taken or repayment,

issue of security or redemption of debenture etc.

Introduction

With the ramified economic changes and complex business structure, each and every

company is operating in the international market are following international financial

reporting framework. As this International rules and regulation has very complex structure

which require from company or entity to establish a separate compliance function like

internal audit department or audit committee and foam a policy to define role and

responsibility of such function or department. This report focuses on the analysing the cash

flow statement and recording of accounts as per the accounting rules and taxation rules. It is a

listed company operating in the international field which make it obligated to compliance

with domestic as well as international financial reporting framework.

Answer to question-1

Analysis of the Cash flow statement

Cash flow statement show the flow of the cash whether it is inflow or outflow , It include

the cash flow of current year as well as cash flow of the year as well as cash flow of the year

which is not related to relevant previous year. Cash flow statement classifies its activity in

three phases:-

Operating Activity which includes the flows of the cash which generate from operational

activity.

Investment activity includes the flow of cash from sale or purchases of any Immovable

property.

Financial activity includes the cash flow from financial activity like loan taken or repayment,

issue of security or redemption of debenture etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

The non- cash items if company is AUD $ 34 million which have increased by 22% since

last one year.

The company has also acquired the new machinery and assets of AUD $886 million which

has been shown in investment activity.

The cash outflow from the financial activities have reflected the cash outflow of AUD $ 396

in 2017 that is 12% higher as compared to last year data.

The company has also declared the dividend on its share capital which is AUD$119

million .It is 10% higher than the previous year.

After assessing the cash flow of JB HI-FI Company it is concluded that company has

increased its free cash flow to AUD$ 21 million. Since last years.

Answer to question-2

Comparative analysis of the all three main flow of activities

JB HI FI LTD (JBH) Statement of CASH FLOW

Fiscal year ends in June. AUD in millions

except per share data.

2017-

06

2016-

06

2015-

06

2014-

06

2013-

06

Net cash provided by operating activities 191 185 180 41 156

Net cash used for investing activities -886 -52 -44 -38 -38

Net cash provided by (used for) financing

activities 716 -131 -130 -28 -91

Free cash flow 142 133 137 5 121

As company is operating on a large scale so it is reasonable to have higher amount of

operating activity therefore all of its free cash flow is accompanied with the increasing and

decreasing of cash. Company is having positive cash flow in the business as reflect from free

cash flow amounting AUD $ 142 million. If company want to sustain its capital for long run

than it needs to focus on increasing the value of its business then they needs to increase the

overall output and efficiency of the business.

The non- cash items if company is AUD $ 34 million which have increased by 22% since

last one year.

The company has also acquired the new machinery and assets of AUD $886 million which

has been shown in investment activity.

The cash outflow from the financial activities have reflected the cash outflow of AUD $ 396

in 2017 that is 12% higher as compared to last year data.

The company has also declared the dividend on its share capital which is AUD$119

million .It is 10% higher than the previous year.

After assessing the cash flow of JB HI-FI Company it is concluded that company has

increased its free cash flow to AUD$ 21 million. Since last years.

Answer to question-2

Comparative analysis of the all three main flow of activities

JB HI FI LTD (JBH) Statement of CASH FLOW

Fiscal year ends in June. AUD in millions

except per share data.

2017-

06

2016-

06

2015-

06

2014-

06

2013-

06

Net cash provided by operating activities 191 185 180 41 156

Net cash used for investing activities -886 -52 -44 -38 -38

Net cash provided by (used for) financing

activities 716 -131 -130 -28 -91

Free cash flow 142 133 137 5 121

As company is operating on a large scale so it is reasonable to have higher amount of

operating activity therefore all of its free cash flow is accompanied with the increasing and

decreasing of cash. Company is having positive cash flow in the business as reflect from free

cash flow amounting AUD $ 142 million. If company want to sustain its capital for long run

than it needs to focus on increasing the value of its business then they needs to increase the

overall output and efficiency of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

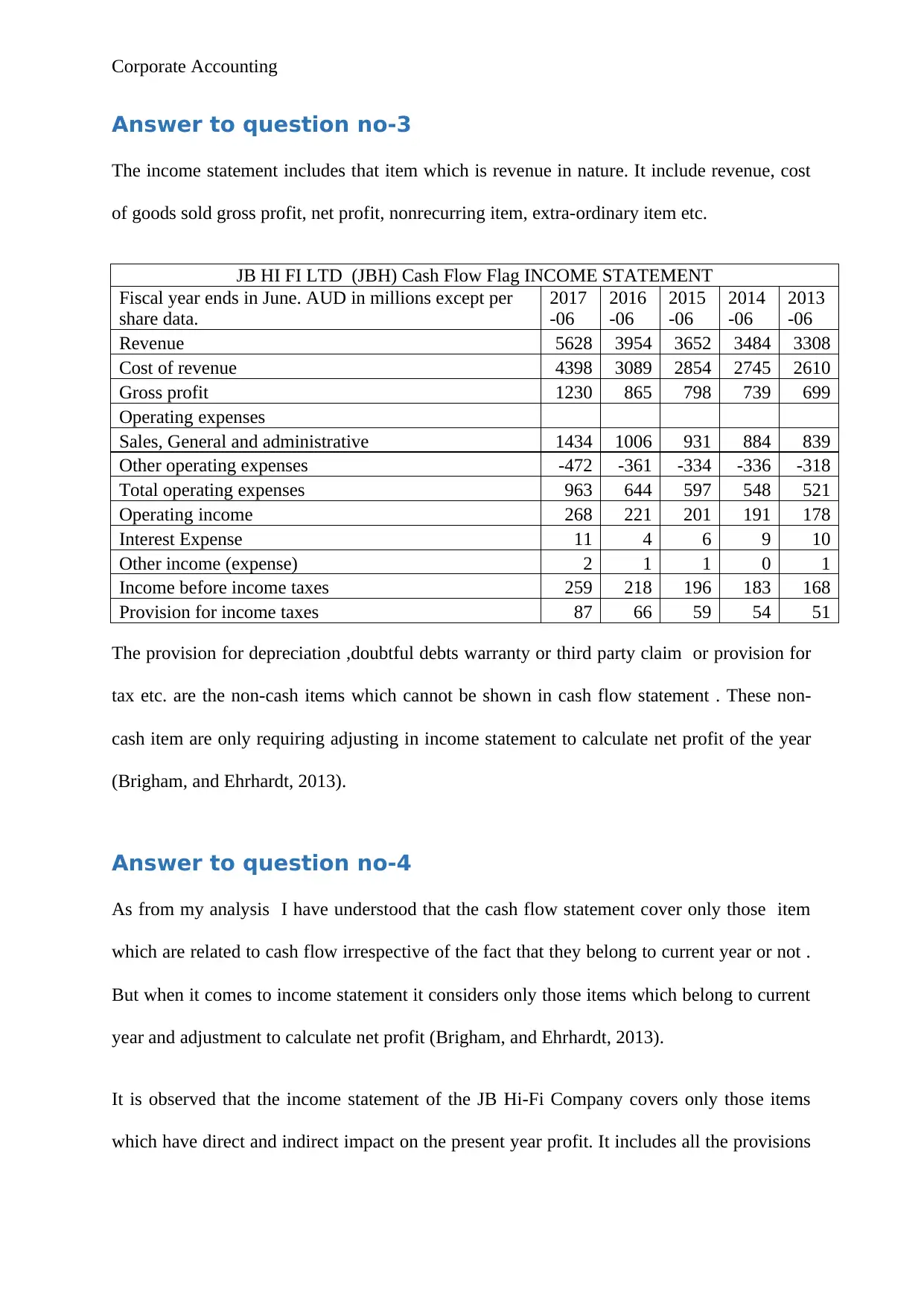

Answer to question no-3

The income statement includes that item which is revenue in nature. It include revenue, cost

of goods sold gross profit, net profit, nonrecurring item, extra-ordinary item etc.

JB HI FI LTD (JBH) Cash Flow Flag INCOME STATEMENT

Fiscal year ends in June. AUD in millions except per

share data.

2017

-06

2016

-06

2015

-06

2014

-06

2013

-06

Revenue 5628 3954 3652 3484 3308

Cost of revenue 4398 3089 2854 2745 2610

Gross profit 1230 865 798 739 699

Operating expenses

Sales, General and administrative 1434 1006 931 884 839

Other operating expenses -472 -361 -334 -336 -318

Total operating expenses 963 644 597 548 521

Operating income 268 221 201 191 178

Interest Expense 11 4 6 9 10

Other income (expense) 2 1 1 0 1

Income before income taxes 259 218 196 183 168

Provision for income taxes 87 66 59 54 51

The provision for depreciation ,doubtful debts warranty or third party claim or provision for

tax etc. are the non-cash items which cannot be shown in cash flow statement . These non-

cash item are only requiring adjusting in income statement to calculate net profit of the year

(Brigham, and Ehrhardt, 2013).

Answer to question no-4

As from my analysis I have understood that the cash flow statement cover only those item

which are related to cash flow irrespective of the fact that they belong to current year or not .

But when it comes to income statement it considers only those items which belong to current

year and adjustment to calculate net profit (Brigham, and Ehrhardt, 2013).

It is observed that the income statement of the JB Hi-Fi Company covers only those items

which have direct and indirect impact on the present year profit. It includes all the provisions

Answer to question no-3

The income statement includes that item which is revenue in nature. It include revenue, cost

of goods sold gross profit, net profit, nonrecurring item, extra-ordinary item etc.

JB HI FI LTD (JBH) Cash Flow Flag INCOME STATEMENT

Fiscal year ends in June. AUD in millions except per

share data.

2017

-06

2016

-06

2015

-06

2014

-06

2013

-06

Revenue 5628 3954 3652 3484 3308

Cost of revenue 4398 3089 2854 2745 2610

Gross profit 1230 865 798 739 699

Operating expenses

Sales, General and administrative 1434 1006 931 884 839

Other operating expenses -472 -361 -334 -336 -318

Total operating expenses 963 644 597 548 521

Operating income 268 221 201 191 178

Interest Expense 11 4 6 9 10

Other income (expense) 2 1 1 0 1

Income before income taxes 259 218 196 183 168

Provision for income taxes 87 66 59 54 51

The provision for depreciation ,doubtful debts warranty or third party claim or provision for

tax etc. are the non-cash items which cannot be shown in cash flow statement . These non-

cash item are only requiring adjusting in income statement to calculate net profit of the year

(Brigham, and Ehrhardt, 2013).

Answer to question no-4

As from my analysis I have understood that the cash flow statement cover only those item

which are related to cash flow irrespective of the fact that they belong to current year or not .

But when it comes to income statement it considers only those items which belong to current

year and adjustment to calculate net profit (Brigham, and Ehrhardt, 2013).

It is observed that the income statement of the JB Hi-Fi Company covers only those items

which have direct and indirect impact on the present year profit. It includes all the provisions

Corporate Accounting

and taxes which will be required to pay or provisions for the income tax made. The cash flwo

statement covers all the tax payment of company in the present year.

Answer to question no-5

Income statement is prepared to calculate net profit available for shareholder after

considering revenue item relented to relevant previous year. Advance made to sappier or

advance received from customer will not be shown to income statement as it does not belong

to relevant previous year. This is done to show the true and fair view of income statement so

that the economic decision of user of such statement does not affect. The true and fair view

of the income statement is based on the recording framework and accounting rules for

identifying the profit and loss of Company.

Answer to question no-6

Tax payment is required to be paid as tax obligation by Company. This amount of tax

calculate as per the rules and regulation related to income tax act applicable to the company

in the country in which it is operating. AUD $ 65.65 has been paid by the company in

current year as compared to last year data which shows the payment of tax AUD $ 86.8

(Brigham, and Ehrhardt, 2013).

Particular(AUD $ in million) 2016 2017

Income tax expenses 86.8 65.6

However, company is having high financial leverage due to which it reduces the amount of

tax. The higher interest expenses payment in the books of account will be used by JB Hi-Fi

and taxes which will be required to pay or provisions for the income tax made. The cash flwo

statement covers all the tax payment of company in the present year.

Answer to question no-5

Income statement is prepared to calculate net profit available for shareholder after

considering revenue item relented to relevant previous year. Advance made to sappier or

advance received from customer will not be shown to income statement as it does not belong

to relevant previous year. This is done to show the true and fair view of income statement so

that the economic decision of user of such statement does not affect. The true and fair view

of the income statement is based on the recording framework and accounting rules for

identifying the profit and loss of Company.

Answer to question no-6

Tax payment is required to be paid as tax obligation by Company. This amount of tax

calculate as per the rules and regulation related to income tax act applicable to the company

in the country in which it is operating. AUD $ 65.65 has been paid by the company in

current year as compared to last year data which shows the payment of tax AUD $ 86.8

(Brigham, and Ehrhardt, 2013).

Particular(AUD $ in million) 2016 2017

Income tax expenses 86.8 65.6

However, company is having high financial leverage due to which it reduces the amount of

tax. The higher interest expenses payment in the books of account will be used by JB Hi-Fi

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

Company to reduce the tax payment on long term basis. It is ideally used as tax planning of

the organization.

Answer to question no-7

It is analyzed that the tax amount paid by company is done by following the taxation rules

and standards. The income tax rate computed based on the accounting income differ from the

tax paid by company in its books of accounts.

Explain, why there is difference between both and

reasons

The income tax payment made by company is AUD $ 65.6 million in 2017 .The tax rate

applicable to the company is 30 %.

It would be around 259*30%.

The amount of tax should be 77.7 million.

The accounting profit is calculated on the basis of financial reporting framework but

the profit for taxation matter is calculated on the basis of income tax rule after

considering the relevant provision and deferred tax arise due to timing difference

between accounting profit or income tax profit .

Two reason for the changes in this tax payment

1. Some expenditure is not allowed as per income tax rule but this expenditure is

deductible as per accounting standard so that it will lead to temporary difference.

2. Rate applicable to fixed assets for the purpose of calculation of depreciation are

applied as per company act rather than the rate as per income tax rule.

Company to reduce the tax payment on long term basis. It is ideally used as tax planning of

the organization.

Answer to question no-7

It is analyzed that the tax amount paid by company is done by following the taxation rules

and standards. The income tax rate computed based on the accounting income differ from the

tax paid by company in its books of accounts.

Explain, why there is difference between both and

reasons

The income tax payment made by company is AUD $ 65.6 million in 2017 .The tax rate

applicable to the company is 30 %.

It would be around 259*30%.

The amount of tax should be 77.7 million.

The accounting profit is calculated on the basis of financial reporting framework but

the profit for taxation matter is calculated on the basis of income tax rule after

considering the relevant provision and deferred tax arise due to timing difference

between accounting profit or income tax profit .

Two reason for the changes in this tax payment

1. Some expenditure is not allowed as per income tax rule but this expenditure is

deductible as per accounting standard so that it will lead to temporary difference.

2. Rate applicable to fixed assets for the purpose of calculation of depreciation are

applied as per company act rather than the rate as per income tax rule.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

Answer to question no-8

The deferred tax liabilities recorded is amounting to $ 8.2 million. It is evaluated that JB Hi-

Fi Company could recognize and carried forward its deferred tax libiliteis to the extent to

which it could set off with its tax payment. It has deferred tax liabilities in its books of

account t (Brigham, and Ehrhardt, 2013).

It is evaluated that the recording of the tax payment in the books of account is different as per

the accounting rules and regulation and taxation rules and regulation given under AASB 112.

Recording of the deferred tax assets is done when the tax payment is higher as compared too

accounting taxation rules (Robinson, Stomberg, & Towery, 2015).

On the other hand, tax payment is lower as per the computation made under the income tax

rules and regulation as compared to the tax computed as per the accounting rules then the

higher tax will be considered as deferred tax assets (JB HI-FI, 2017).

The deferred tax liabilities in the books of accounts shown are given below given table

(Towery, 2017).

Particular (AUD $ million) 2017 2016

Deferred tax liabilities 8.2 0

Answer to question no-8

The deferred tax liabilities recorded is amounting to $ 8.2 million. It is evaluated that JB Hi-

Fi Company could recognize and carried forward its deferred tax libiliteis to the extent to

which it could set off with its tax payment. It has deferred tax liabilities in its books of

account t (Brigham, and Ehrhardt, 2013).

It is evaluated that the recording of the tax payment in the books of account is different as per

the accounting rules and regulation and taxation rules and regulation given under AASB 112.

Recording of the deferred tax assets is done when the tax payment is higher as compared too

accounting taxation rules (Robinson, Stomberg, & Towery, 2015).

On the other hand, tax payment is lower as per the computation made under the income tax

rules and regulation as compared to the tax computed as per the accounting rules then the

higher tax will be considered as deferred tax assets (JB HI-FI, 2017).

The deferred tax liabilities in the books of accounts shown are given below given table

(Towery, 2017).

Particular (AUD $ million) 2017 2016

Deferred tax liabilities 8.2 0

Corporate Accounting

Answer to question no-9

Income tax payable and current tax assets as recorded by the company disclose as follows:-

JB HI Fi Company Had paid AUD $ 4.9 million in the year 2016 which have gone up to

AUD $ 9 million in 2017 (JB HI-FI, 2017).

Income tax paid by the company has been calculated as per accounting profit but this amount

should be calculated on the basis of income tax provision and rule.

AUD $ 8.5 million has been shown as deferred tax payment by JB Hi-Fi Company

(Mullinova, &Simonyants, 2016).

Particular(AUD $ in million) 2016 2017

Income tax payable 4.9 9

Why the income tax payment is not same with the income

tax payable

It is evaluated that the income tax payment shown in the books of account is the amount of

tax charged on the profit earned by the company. It is considered that thee the income tax

payable is the total amount of tax including outstanding of the previous years (Watson, 2018).

The recording of the income tax payment is done in the profit and loss accounts and the

recording of the income tax payment is done in the liabilities side of the balance sheet

(Reinstein, & Ahlers, 2018).

Answer to question no-9

Income tax payable and current tax assets as recorded by the company disclose as follows:-

JB HI Fi Company Had paid AUD $ 4.9 million in the year 2016 which have gone up to

AUD $ 9 million in 2017 (JB HI-FI, 2017).

Income tax paid by the company has been calculated as per accounting profit but this amount

should be calculated on the basis of income tax provision and rule.

AUD $ 8.5 million has been shown as deferred tax payment by JB Hi-Fi Company

(Mullinova, &Simonyants, 2016).

Particular(AUD $ in million) 2016 2017

Income tax payable 4.9 9

Why the income tax payment is not same with the income

tax payable

It is evaluated that the income tax payment shown in the books of account is the amount of

tax charged on the profit earned by the company. It is considered that thee the income tax

payable is the total amount of tax including outstanding of the previous years (Watson, 2018).

The recording of the income tax payment is done in the profit and loss accounts and the

recording of the income tax payment is done in the liabilities side of the balance sheet

(Reinstein, & Ahlers, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

Answer to question no-10

It is evaluated that the cash flow statement is accompanied with the inflow and outflow of the

cash in the business (Farrell, Greig, and Hamoudi2018).

The cash flow statement shows the amount of tax payment which company made in the

present year i.e. $98.5 million. It covers all the tax payment.

The income tax recorded in the profit and loss account is not equal to the amount of the tax

payment shown in the cash flow statement of company (Ayers,., Call, & Schwab, 2018).

Reason

The cash flow statement covers all the tax payment in the present year whether it relates to

present year or not. The tax payment is charged on the current year profit and recorded as tax

amount charged as well.

On the other hand, tax charged on the profit is shown in the profit and loss account as per the

AASB 112 (Phillips, et al. , 2014).

Answer to question no-11

Treatment of the Tax

Interesting thing

The tax payment as per the AASB 112 is not certain so it blocks high amount of cash or

capital in business.

Surprising thing

Answer to question no-10

It is evaluated that the cash flow statement is accompanied with the inflow and outflow of the

cash in the business (Farrell, Greig, and Hamoudi2018).

The cash flow statement shows the amount of tax payment which company made in the

present year i.e. $98.5 million. It covers all the tax payment.

The income tax recorded in the profit and loss account is not equal to the amount of the tax

payment shown in the cash flow statement of company (Ayers,., Call, & Schwab, 2018).

Reason

The cash flow statement covers all the tax payment in the present year whether it relates to

present year or not. The tax payment is charged on the current year profit and recorded as tax

amount charged as well.

On the other hand, tax charged on the profit is shown in the profit and loss account as per the

AASB 112 (Phillips, et al. , 2014).

Answer to question no-11

Treatment of the Tax

Interesting thing

The tax payment as per the AASB 112 is not certain so it blocks high amount of cash or

capital in business.

Surprising thing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

Company can never has deferred tax assets and deferred tax libiliteis in the books of accounts

at the same time (Akomeah, Kong., & Antwi, 2018).

Difficulty in recorded the entire tax amount

The main difficulty in the recording of the tax amount arise due to the change in the taxation

rules and difference between the accounting rules and taxation rules and regulations (Brabete,

Drăgan., & Dindiri, 2018).

Conclusion

After analysing all the details and taxation rules, it could be inferred that the deferred

tax asset and deferred tax liabilities is recorded in the balance sheet which reflects the excess

tax payment and short amount of tax payment made by the company. After analysing all the

facts, it could be inferred that the computation of the tax amount is done by following proper

taxation rules and regulations. if in case the tax payment is higher as compared to accounting

rules and regulation then the same will be recorded as deferred tax assets in the books of

account of company.

Company can never has deferred tax assets and deferred tax libiliteis in the books of accounts

at the same time (Akomeah, Kong., & Antwi, 2018).

Difficulty in recorded the entire tax amount

The main difficulty in the recording of the tax amount arise due to the change in the taxation

rules and difference between the accounting rules and taxation rules and regulations (Brabete,

Drăgan., & Dindiri, 2018).

Conclusion

After analysing all the details and taxation rules, it could be inferred that the deferred

tax asset and deferred tax liabilities is recorded in the balance sheet which reflects the excess

tax payment and short amount of tax payment made by the company. After analysing all the

facts, it could be inferred that the computation of the tax amount is done by following proper

taxation rules and regulations. if in case the tax payment is higher as compared to accounting

rules and regulation then the same will be recorded as deferred tax assets in the books of

account of company.

Corporate Accounting

References

Akomeah, M.O., Kong, Y. and Antwi, H.A., (2018). Effect of Tax-Deferred Assets on

Mutual Fund Strategies of the Mutual Funds. European Journal of Contemporary

Research, 7(1).

Ayers, B.C., Call, A.C. & Schwab, C.M., (2018). Do Analysts' Cash Flow Forecasts

Encourage Managers to Improve the Firm's Cash Flows? Evidence from Tax

Planning. Contemporary Accounting Research.

Brabete, V., Drăgan, C. & Dindiri, C.M., (2018). Public Interest Satisfaction and

Accounting's Assuming of Social Responsibility. Accounting Data on Profit Tax in

the Context of Corporate Social Responsibility. In Current Issues in Corporate Social

Responsibility (pp. 217-235). Springer, Cham.

Brigham, E.F. & Ehrhardt, M.C., (2013). Financial management: Theory and practice.

Cengage Learning.

Farrell, D., Greig, F. and Hamoudi, A., (2018). Deferred Care: How Tax Refunds Enable

Healthcare Spending.

JB HI-FI, (2017). Annual report., [Online]., retrieved from

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_JBH_2016.pdf

Mullinova, S. & Simonyants, N., (2016). Reflection of a deferred tax liability in the credit

union reporting according to IFRS (IAS) 12" Income taxes". Modern European

Researches, (1), pp.83-88.

Phillips, J.D., Pincus, M., Rego, S.O. and Wan, H., (2014). Decomposing changes in deferred

tax assets and liabilities to isolate earnings management activities. Journal of the

American Taxation Association, 26(s-1), pp.43-66.

Reinstein, T., & Ahlers, A. (2018). Effective NOL Planning in Light of Tax Reform. Tax

Executive, 70, 33.

References

Akomeah, M.O., Kong, Y. and Antwi, H.A., (2018). Effect of Tax-Deferred Assets on

Mutual Fund Strategies of the Mutual Funds. European Journal of Contemporary

Research, 7(1).

Ayers, B.C., Call, A.C. & Schwab, C.M., (2018). Do Analysts' Cash Flow Forecasts

Encourage Managers to Improve the Firm's Cash Flows? Evidence from Tax

Planning. Contemporary Accounting Research.

Brabete, V., Drăgan, C. & Dindiri, C.M., (2018). Public Interest Satisfaction and

Accounting's Assuming of Social Responsibility. Accounting Data on Profit Tax in

the Context of Corporate Social Responsibility. In Current Issues in Corporate Social

Responsibility (pp. 217-235). Springer, Cham.

Brigham, E.F. & Ehrhardt, M.C., (2013). Financial management: Theory and practice.

Cengage Learning.

Farrell, D., Greig, F. and Hamoudi, A., (2018). Deferred Care: How Tax Refunds Enable

Healthcare Spending.

JB HI-FI, (2017). Annual report., [Online]., retrieved from

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_JBH_2016.pdf

Mullinova, S. & Simonyants, N., (2016). Reflection of a deferred tax liability in the credit

union reporting according to IFRS (IAS) 12" Income taxes". Modern European

Researches, (1), pp.83-88.

Phillips, J.D., Pincus, M., Rego, S.O. and Wan, H., (2014). Decomposing changes in deferred

tax assets and liabilities to isolate earnings management activities. Journal of the

American Taxation Association, 26(s-1), pp.43-66.

Reinstein, T., & Ahlers, A. (2018). Effective NOL Planning in Light of Tax Reform. Tax

Executive, 70, 33.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.