Corporate Accounting: Regulations, Standards, Equity of Mining Firms

VerifiedAdded on 2023/06/05

|16

|2923

|200

Report

AI Summary

This report provides an analysis of corporate accounting regulations, accounting standard settings, and owner’s equity within the context of the Australian mining industry. It discusses the importance of proper financial reporting and disclosure, highlighting the roles of IFRS and AASB standards. The report examines key components of owner's equity, including retained earnings, contributed equity, and various reserves, and their impact on financial statements. A comparative analysis of BHP Billiton, Rio Tinto, Fortescue Metals Group, and Orica Limited is presented, focusing on their equity components and financial performance. The report also touches on the evaluation of debt and equity, aiming to provide insights into the financial health and reporting practices of these companies. Desklib provides a platform to explore similar solved assignments.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The following assignment contains a brief discussion on corporate regulation, accounting

standards and a discussion on owner’s equity of four listed company belonging to mining

industry in Australia. This will help us have an insight into the need for proper reporting by

the corporate.

2

The following assignment contains a brief discussion on corporate regulation, accounting

standards and a discussion on owner’s equity of four listed company belonging to mining

industry in Australia. This will help us have an insight into the need for proper reporting by

the corporate.

2

Contents

Introduction................................................................................................................................4

Corporate regulations.................................................................................................................5

Accounting Standard Setting......................................................................................................6

Owner’s equity...........................................................................................................................7

Item of equity.........................................................................................................................7

Equity and Debt evaluation..................................................................................................10

Conclusion................................................................................................................................12

Bibliography.............................................................................................................................13

3

Introduction................................................................................................................................4

Corporate regulations.................................................................................................................5

Accounting Standard Setting......................................................................................................6

Owner’s equity...........................................................................................................................7

Item of equity.........................................................................................................................7

Equity and Debt evaluation..................................................................................................10

Conclusion................................................................................................................................12

Bibliography.............................................................................................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Nowadays, the importance of a proper financial reporting system has increased a lot for an

organization to conduct its business successfully in the market. Also, the organization is

needed to provide the public with proper disclosure of the information that is reliable in

nature (Alvarez, 2013). This report will be based on the major emphasis that is experienced in

a business if proper disclosure and discussion may or may not have been made. A discussion

on the IFRS and AASB standards will also be done which will be accompanied with

evaluation of debt and equity for four public companies.

4

Nowadays, the importance of a proper financial reporting system has increased a lot for an

organization to conduct its business successfully in the market. Also, the organization is

needed to provide the public with proper disclosure of the information that is reliable in

nature (Alvarez, 2013). This report will be based on the major emphasis that is experienced in

a business if proper disclosure and discussion may or may not have been made. A discussion

on the IFRS and AASB standards will also be done which will be accompanied with

evaluation of debt and equity for four public companies.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate regulations

It is very important for the organizations to evaluate the requirement of the customers before

making any type of disclosure of information. The current system has not proved to be

successful in providing the different users with appropriate financial reporting data. The users

are divided between two groups among which half-hour happy with the data while the other

half requires more information for the process of decision making (Easton, 2010). Therefore

a regulation should be conducted on the financial reporting so that the manager can ascertain

the level of information that is to be disclosed by him. The manager should also keep in mind

that no information is lived on a voluntary basis. The financial statements of an organization

are not public documents because of which if they are lived in any way, the organization may

suffer a huge loss (Elaine, 2015). Therefore, the manager should try and disclose only

essential information that is needed to be conveyed and not each and every financial aspect of

the organization should be disclosed.

There should be a presence of a common approach which can be followed by different

companies in various jurisdictions in order to make the task of comparison easy. It is the duty

of positive to restrict the manager from disclosing any data that is relevant in nature or may

cause harm to the organizations business (Fridson & Alvarez, 2012). If the managers release

any information voluntarily then innumerable misstatements can take place. Hence, this states

the importance of regulation of financial reporting and accounting in an organization. If there

is an absence of regulations in an organization, the manager of the organization may disclose

unnecessary information which may further cause unnecessary problems in the task of

comparison (Girard, 2014). Therefore it can be clearly stated that the task of regulation in the

financial reporting is important as it helps to build reliability and credibility commitment

towards the disclosure. Making disclosures using the proper regulatory controls is much more

convenient than voluntarily providing it to the public. Making disclosures on the basis of

regulatory regimes will be more cost-beneficial also (Ittelson, 2009). The major concern of

financial reporting is to provide transparent data which can be used in an idealistic nature by

the public in order to conduct the decision-making process. However, it should also be noted

that transparency doesn't mean to reveal all information of the organization, where it is meant

to provide all necessary information that is needed by the investors and shareholders of the

organization to conduct the process of decision making. Too much information in the

financial reports may lead the report to look vague (McLaney & Adril, 2016).

5

It is very important for the organizations to evaluate the requirement of the customers before

making any type of disclosure of information. The current system has not proved to be

successful in providing the different users with appropriate financial reporting data. The users

are divided between two groups among which half-hour happy with the data while the other

half requires more information for the process of decision making (Easton, 2010). Therefore

a regulation should be conducted on the financial reporting so that the manager can ascertain

the level of information that is to be disclosed by him. The manager should also keep in mind

that no information is lived on a voluntary basis. The financial statements of an organization

are not public documents because of which if they are lived in any way, the organization may

suffer a huge loss (Elaine, 2015). Therefore, the manager should try and disclose only

essential information that is needed to be conveyed and not each and every financial aspect of

the organization should be disclosed.

There should be a presence of a common approach which can be followed by different

companies in various jurisdictions in order to make the task of comparison easy. It is the duty

of positive to restrict the manager from disclosing any data that is relevant in nature or may

cause harm to the organizations business (Fridson & Alvarez, 2012). If the managers release

any information voluntarily then innumerable misstatements can take place. Hence, this states

the importance of regulation of financial reporting and accounting in an organization. If there

is an absence of regulations in an organization, the manager of the organization may disclose

unnecessary information which may further cause unnecessary problems in the task of

comparison (Girard, 2014). Therefore it can be clearly stated that the task of regulation in the

financial reporting is important as it helps to build reliability and credibility commitment

towards the disclosure. Making disclosures using the proper regulatory controls is much more

convenient than voluntarily providing it to the public. Making disclosures on the basis of

regulatory regimes will be more cost-beneficial also (Ittelson, 2009). The major concern of

financial reporting is to provide transparent data which can be used in an idealistic nature by

the public in order to conduct the decision-making process. However, it should also be noted

that transparency doesn't mean to reveal all information of the organization, where it is meant

to provide all necessary information that is needed by the investors and shareholders of the

organization to conduct the process of decision making. Too much information in the

financial reports may lead the report to look vague (McLaney & Adril, 2016).

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Standard Setting

The international financial reporting system can be defined as a set of systems that are needed

to be procured by an organization while preparation of accounts and Audit reports. According

to the AASB, the adoption of IFRS has been made in order to fulfil the purpose of financial

reporting on an annual basis under the obligations of the Corporations Act, 2001. These

regulations are being conducted in order to ensure that all the statements are prepared in

accordance to the accounting standards and a neutral policy have been adopted in order to

record the transaction so that comparison for the different companies in the same industry can

be made easier (Menifield, 2014). All the companies, irrespective of the fact that they work

as a profit or a non-profit organization should record their transactions in accordance with

these principles. The AASB clearly states the importance of the international financial

reporting system in the preparation of accounts of public and private sector firms (Parrino,

2013).

It has been observed that AASB has accounted for the standards of Australian auditing and

accounting. This will be a continuous process that will be needed by the organizations to be

fulfilled according to the principles of IFRS (Penman, 2012). The companies that play

important role in the international capital markets should also try to maintain their statements

in accordance to the IFRS so that the capital costs can be decreased (Seitz & Ellison, 2009).

The principles of IFRS stated by IASB are not compulsory for other member countries to be

followed because the compulsion of this principle in the accounting process will need a lot of

convergence and change in the systems. The application of these principles in the accounts of

the firm is not always easy because of the various challenges present wild adoption of this

framework (Siciliano, 2015). However, the benefits that will be gained by the organization

after the implementation of this framework will be very useful for the flourishing of the

economy of both the company and the industry. The other countries following different

accounting systems are not compelled to follow this method for the preparation of financial

accounts. However, if uniformity is maintained in the principle used for recording the

financial data, the task of comparison will be made easy between the organizations of the

same industry (Simpson, 2012).

7

The international financial reporting system can be defined as a set of systems that are needed

to be procured by an organization while preparation of accounts and Audit reports. According

to the AASB, the adoption of IFRS has been made in order to fulfil the purpose of financial

reporting on an annual basis under the obligations of the Corporations Act, 2001. These

regulations are being conducted in order to ensure that all the statements are prepared in

accordance to the accounting standards and a neutral policy have been adopted in order to

record the transaction so that comparison for the different companies in the same industry can

be made easier (Menifield, 2014). All the companies, irrespective of the fact that they work

as a profit or a non-profit organization should record their transactions in accordance with

these principles. The AASB clearly states the importance of the international financial

reporting system in the preparation of accounts of public and private sector firms (Parrino,

2013).

It has been observed that AASB has accounted for the standards of Australian auditing and

accounting. This will be a continuous process that will be needed by the organizations to be

fulfilled according to the principles of IFRS (Penman, 2012). The companies that play

important role in the international capital markets should also try to maintain their statements

in accordance to the IFRS so that the capital costs can be decreased (Seitz & Ellison, 2009).

The principles of IFRS stated by IASB are not compulsory for other member countries to be

followed because the compulsion of this principle in the accounting process will need a lot of

convergence and change in the systems. The application of these principles in the accounts of

the firm is not always easy because of the various challenges present wild adoption of this

framework (Siciliano, 2015). However, the benefits that will be gained by the organization

after the implementation of this framework will be very useful for the flourishing of the

economy of both the company and the industry. The other countries following different

accounting systems are not compelled to follow this method for the preparation of financial

accounts. However, if uniformity is maintained in the principle used for recording the

financial data, the task of comparison will be made easy between the organizations of the

same industry (Simpson, 2012).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Owner’s equity

Item of equity

The major components of equity are as follows:

• Retained earnings: retained earnings are the excess revenue of the organization that is

kept aside in order to support the future cash flows and fulfils the liabilities of the

organization in future so that operations can be carried out successfully and without any

problems. Retained earnings are also referred to as ploughing back of profits because they are

excess profit that is kept aside by the organization for future use (Skonieczny, 2012). The

retained earnings after the question to the organisation because they help the organisation to

meet contingencies in future that maybe come hazardous for the business. The shareholders

and the investors are also provided incentive using the retained earnings in the case of

emergencies.

• Contributed equity: the contributed equity capital consists of the equity share capital of

the organization and also the shares that are held in a trust. All these find the provided to the

owners of the organization in order to conduct business successfully. Shareholders can also

be stated as the owners of the organization as they have contributed or bought a small share

of the company by purchasing small equity holdings in the company (Taillard, 2013). The

shareholders are also provided with incentives or interest from time to time in terms of cash

or shares termed as bonus issue. Shares are issued in compliance with the policies of the

company towards the public.

• Reserves: there is a different type of reserves that is to be maintained by an organization

in order to make the future more predictable. Reserves like remuneration reserve, translation

Reserve of foreign currency, hedging reserve, equity reserve, and general reserve are created

in order to ensure the future safety of the organization. Hedging reserves are made in order to

fulfil particular losses against on a derivative instrument. The translation reserve for foreign

currency is made in order to face the losses against that have been incurred by the

organization while conducting international business. The remuneration Reserves are used to

pay the employees and auditors without any delay. The remuneration reserve is not evaluated

on an accurate basis because of the changes that take place in the incentives provided to the

9

Item of equity

The major components of equity are as follows:

• Retained earnings: retained earnings are the excess revenue of the organization that is

kept aside in order to support the future cash flows and fulfils the liabilities of the

organization in future so that operations can be carried out successfully and without any

problems. Retained earnings are also referred to as ploughing back of profits because they are

excess profit that is kept aside by the organization for future use (Skonieczny, 2012). The

retained earnings after the question to the organisation because they help the organisation to

meet contingencies in future that maybe come hazardous for the business. The shareholders

and the investors are also provided incentive using the retained earnings in the case of

emergencies.

• Contributed equity: the contributed equity capital consists of the equity share capital of

the organization and also the shares that are held in a trust. All these find the provided to the

owners of the organization in order to conduct business successfully. Shareholders can also

be stated as the owners of the organization as they have contributed or bought a small share

of the company by purchasing small equity holdings in the company (Taillard, 2013). The

shareholders are also provided with incentives or interest from time to time in terms of cash

or shares termed as bonus issue. Shares are issued in compliance with the policies of the

company towards the public.

• Reserves: there is a different type of reserves that is to be maintained by an organization

in order to make the future more predictable. Reserves like remuneration reserve, translation

Reserve of foreign currency, hedging reserve, equity reserve, and general reserve are created

in order to ensure the future safety of the organization. Hedging reserves are made in order to

fulfil particular losses against on a derivative instrument. The translation reserve for foreign

currency is made in order to face the losses against that have been incurred by the

organization while conducting international business. The remuneration Reserves are used to

pay the employees and auditors without any delay. The remuneration reserve is not evaluated

on an accurate basis because of the changes that take place in the incentives provided to the

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

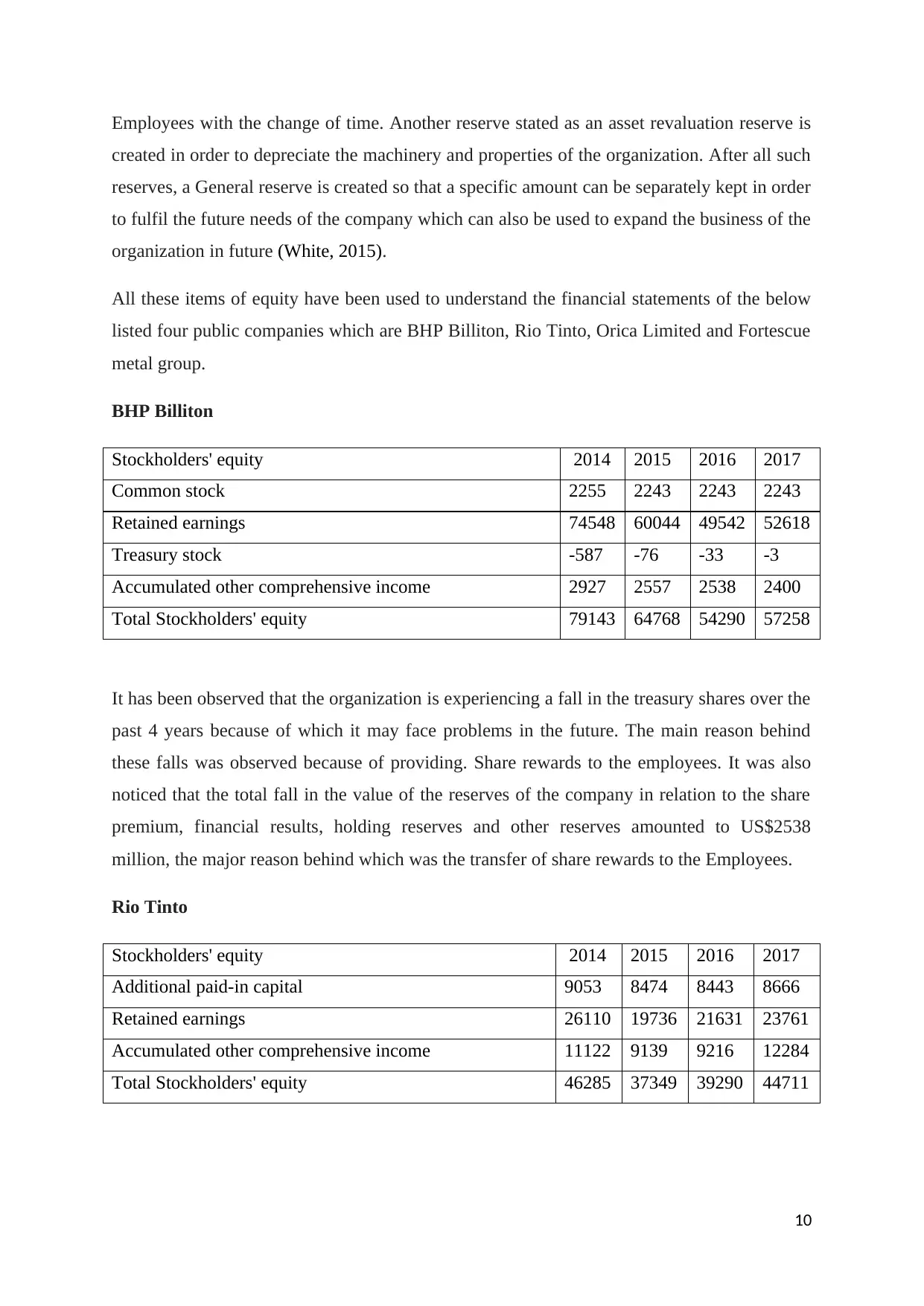

Employees with the change of time. Another reserve stated as an asset revaluation reserve is

created in order to depreciate the machinery and properties of the organization. After all such

reserves, a General reserve is created so that a specific amount can be separately kept in order

to fulfil the future needs of the company which can also be used to expand the business of the

organization in future (White, 2015).

All these items of equity have been used to understand the financial statements of the below

listed four public companies which are BHP Billiton, Rio Tinto, Orica Limited and Fortescue

metal group.

BHP Billiton

Stockholders' equity 2014 2015 2016 2017

Common stock 2255 2243 2243 2243

Retained earnings 74548 60044 49542 52618

Treasury stock -587 -76 -33 -3

Accumulated other comprehensive income 2927 2557 2538 2400

Total Stockholders' equity 79143 64768 54290 57258

It has been observed that the organization is experiencing a fall in the treasury shares over the

past 4 years because of which it may face problems in the future. The main reason behind

these falls was observed because of providing. Share rewards to the employees. It was also

noticed that the total fall in the value of the reserves of the company in relation to the share

premium, financial results, holding reserves and other reserves amounted to US$2538

million, the major reason behind which was the transfer of share rewards to the Employees.

Rio Tinto

Stockholders' equity 2014 2015 2016 2017

Additional paid-in capital 9053 8474 8443 8666

Retained earnings 26110 19736 21631 23761

Accumulated other comprehensive income 11122 9139 9216 12284

Total Stockholders' equity 46285 37349 39290 44711

10

created in order to depreciate the machinery and properties of the organization. After all such

reserves, a General reserve is created so that a specific amount can be separately kept in order

to fulfil the future needs of the company which can also be used to expand the business of the

organization in future (White, 2015).

All these items of equity have been used to understand the financial statements of the below

listed four public companies which are BHP Billiton, Rio Tinto, Orica Limited and Fortescue

metal group.

BHP Billiton

Stockholders' equity 2014 2015 2016 2017

Common stock 2255 2243 2243 2243

Retained earnings 74548 60044 49542 52618

Treasury stock -587 -76 -33 -3

Accumulated other comprehensive income 2927 2557 2538 2400

Total Stockholders' equity 79143 64768 54290 57258

It has been observed that the organization is experiencing a fall in the treasury shares over the

past 4 years because of which it may face problems in the future. The main reason behind

these falls was observed because of providing. Share rewards to the employees. It was also

noticed that the total fall in the value of the reserves of the company in relation to the share

premium, financial results, holding reserves and other reserves amounted to US$2538

million, the major reason behind which was the transfer of share rewards to the Employees.

Rio Tinto

Stockholders' equity 2014 2015 2016 2017

Additional paid-in capital 9053 8474 8443 8666

Retained earnings 26110 19736 21631 23761

Accumulated other comprehensive income 11122 9139 9216 12284

Total Stockholders' equity 46285 37349 39290 44711

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It was observed that the organization was having a very good and structured equity and

retained earnings value present in their financial accounts which were comprehensive in

nature. The retained earnings of the organization were also high because of the huge profits

earned by it in the past years. Therefore, this portrays that the company is able to plough back

its profit in the terms of retained earnings. The accumulated funds and the comprehensive

income of the organization were also observed to grow at an increasing rate because of the

incremental business and high earnings made by the organization.

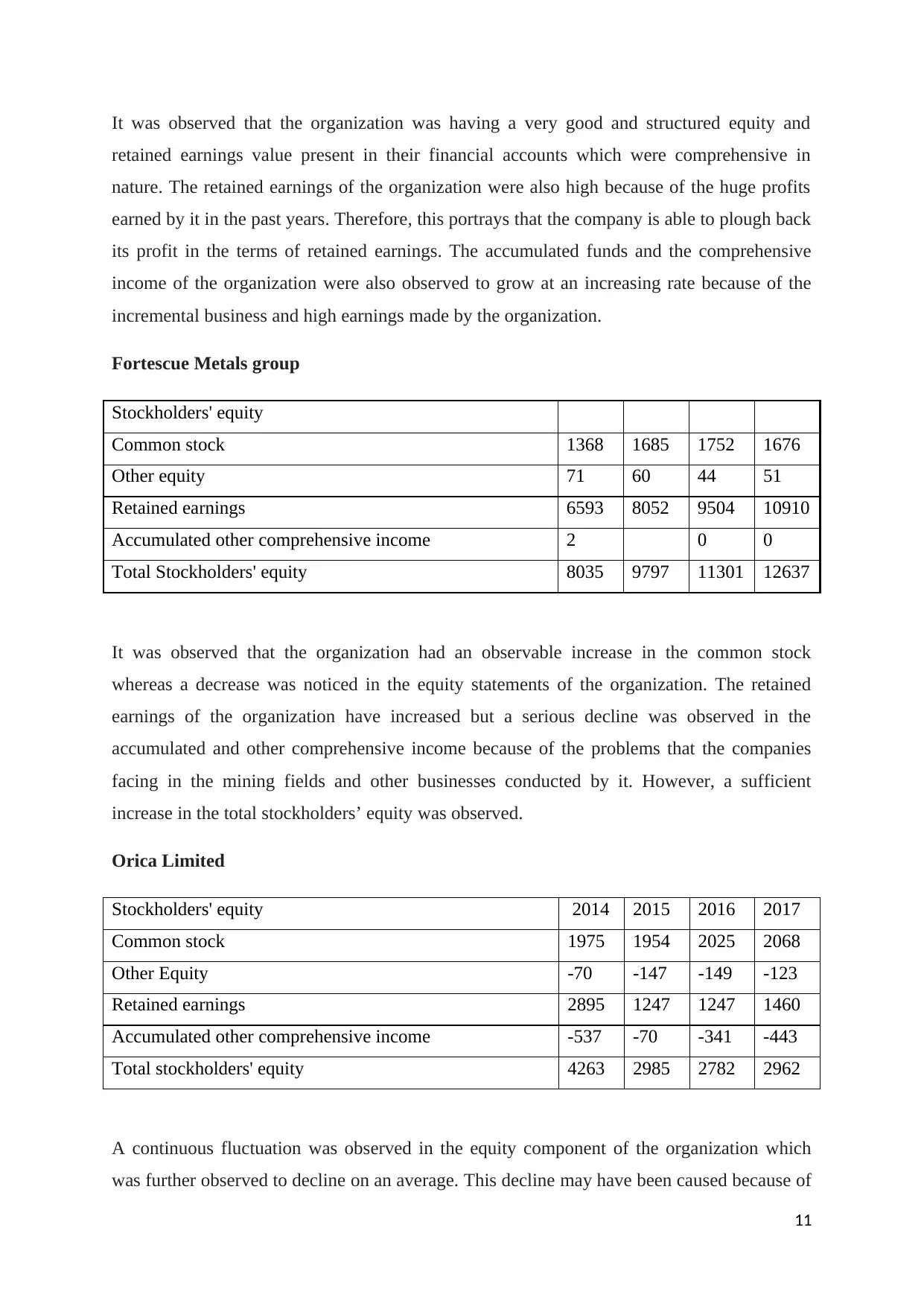

Fortescue Metals group

Stockholders' equity

Common stock 1368 1685 1752 1676

Other equity 71 60 44 51

Retained earnings 6593 8052 9504 10910

Accumulated other comprehensive income 2 0 0

Total Stockholders' equity 8035 9797 11301 12637

It was observed that the organization had an observable increase in the common stock

whereas a decrease was noticed in the equity statements of the organization. The retained

earnings of the organization have increased but a serious decline was observed in the

accumulated and other comprehensive income because of the problems that the companies

facing in the mining fields and other businesses conducted by it. However, a sufficient

increase in the total stockholders’ equity was observed.

Orica Limited

Stockholders' equity 2014 2015 2016 2017

Common stock 1975 1954 2025 2068

Other Equity -70 -147 -149 -123

Retained earnings 2895 1247 1247 1460

Accumulated other comprehensive income -537 -70 -341 -443

Total stockholders' equity 4263 2985 2782 2962

A continuous fluctuation was observed in the equity component of the organization which

was further observed to decline on an average. This decline may have been caused because of

11

retained earnings value present in their financial accounts which were comprehensive in

nature. The retained earnings of the organization were also high because of the huge profits

earned by it in the past years. Therefore, this portrays that the company is able to plough back

its profit in the terms of retained earnings. The accumulated funds and the comprehensive

income of the organization were also observed to grow at an increasing rate because of the

incremental business and high earnings made by the organization.

Fortescue Metals group

Stockholders' equity

Common stock 1368 1685 1752 1676

Other equity 71 60 44 51

Retained earnings 6593 8052 9504 10910

Accumulated other comprehensive income 2 0 0

Total Stockholders' equity 8035 9797 11301 12637

It was observed that the organization had an observable increase in the common stock

whereas a decrease was noticed in the equity statements of the organization. The retained

earnings of the organization have increased but a serious decline was observed in the

accumulated and other comprehensive income because of the problems that the companies

facing in the mining fields and other businesses conducted by it. However, a sufficient

increase in the total stockholders’ equity was observed.

Orica Limited

Stockholders' equity 2014 2015 2016 2017

Common stock 1975 1954 2025 2068

Other Equity -70 -147 -149 -123

Retained earnings 2895 1247 1247 1460

Accumulated other comprehensive income -537 -70 -341 -443

Total stockholders' equity 4263 2985 2782 2962

A continuous fluctuation was observed in the equity component of the organization which

was further observed to decline on an average. This decline may have been caused because of

11

the increase in the material cost that has been incurred by the organization to fulfil the terms

of contracts in which it has indulged. The retained earnings of the organization were stated to

be positive because of the enhancement of business in the future course of action.

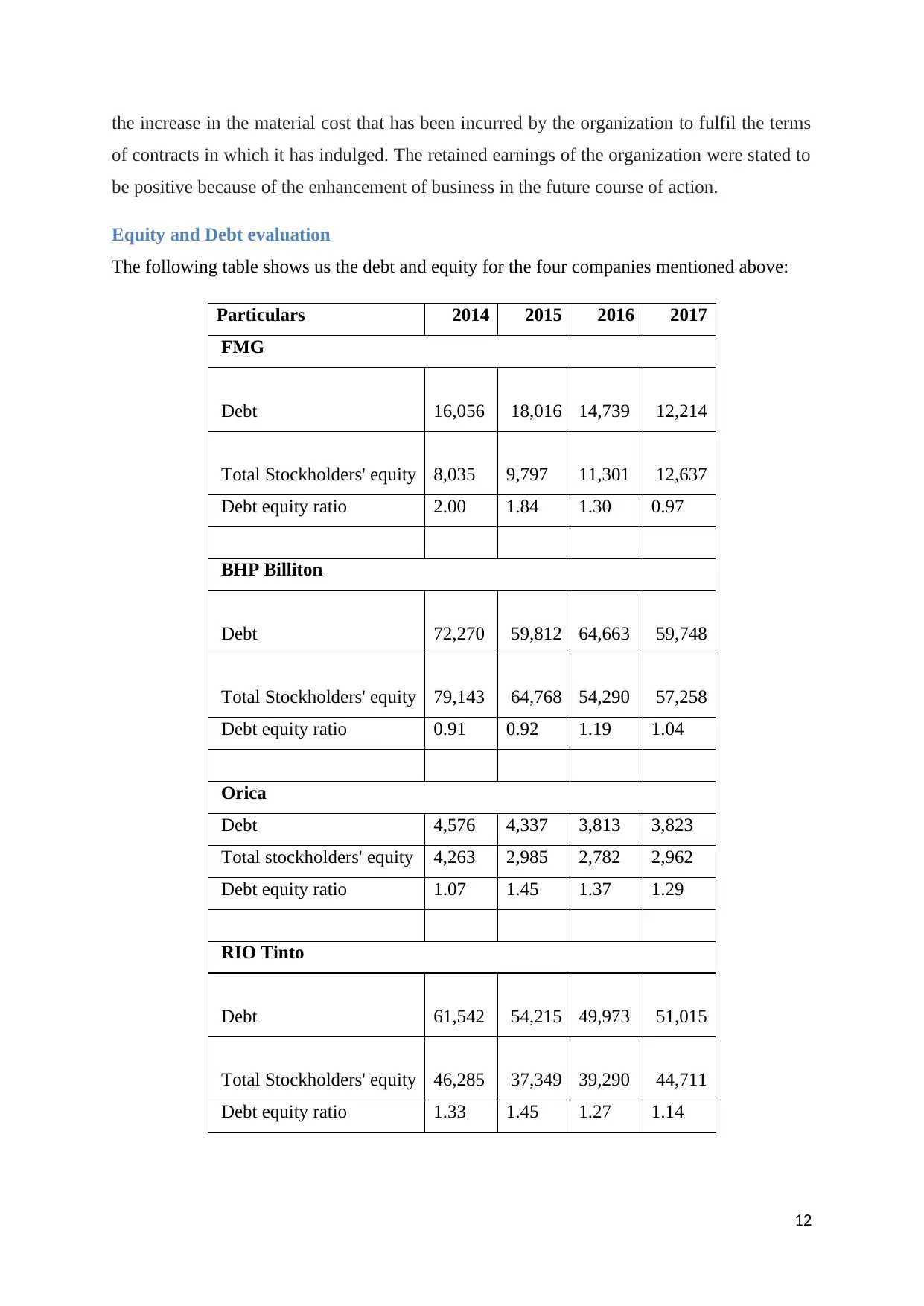

Equity and Debt evaluation

The following table shows us the debt and equity for the four companies mentioned above:

Particulars 2014 2015 2016 2017

FMG

Debt 16,056 18,016 14,739 12,214

Total Stockholders' equity 8,035 9,797 11,301 12,637

Debt equity ratio 2.00 1.84 1.30 0.97

BHP Billiton

Debt 72,270 59,812 64,663 59,748

Total Stockholders' equity 79,143 64,768 54,290 57,258

Debt equity ratio 0.91 0.92 1.19 1.04

Orica

Debt 4,576 4,337 3,813 3,823

Total stockholders' equity 4,263 2,985 2,782 2,962

Debt equity ratio 1.07 1.45 1.37 1.29

RIO Tinto

Debt 61,542 54,215 49,973 51,015

Total Stockholders' equity 46,285 37,349 39,290 44,711

Debt equity ratio 1.33 1.45 1.27 1.14

12

of contracts in which it has indulged. The retained earnings of the organization were stated to

be positive because of the enhancement of business in the future course of action.

Equity and Debt evaluation

The following table shows us the debt and equity for the four companies mentioned above:

Particulars 2014 2015 2016 2017

FMG

Debt 16,056 18,016 14,739 12,214

Total Stockholders' equity 8,035 9,797 11,301 12,637

Debt equity ratio 2.00 1.84 1.30 0.97

BHP Billiton

Debt 72,270 59,812 64,663 59,748

Total Stockholders' equity 79,143 64,768 54,290 57,258

Debt equity ratio 0.91 0.92 1.19 1.04

Orica

Debt 4,576 4,337 3,813 3,823

Total stockholders' equity 4,263 2,985 2,782 2,962

Debt equity ratio 1.07 1.45 1.37 1.29

RIO Tinto

Debt 61,542 54,215 49,973 51,015

Total Stockholders' equity 46,285 37,349 39,290 44,711

Debt equity ratio 1.33 1.45 1.27 1.14

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.