Corporate Accounting Analysis Report: LandMark White & Land & Homes

VerifiedAdded on 2020/12/24

|26

|4200

|426

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting, focusing on the financial statements of LandMark White Limited and Land & Homes Group, both operating in the real estate sector. The report delves into owner's equity, examining equity items like share capital and retained earnings, and conducts a comparative analysis of their debt and equity positions using debt-equity ratios. It further explores cash flow statements, detailing items like interest received and property payments, and provides a comparative analysis of the companies' cash flows across operating, investing, and financing activities. The study also touches upon other comprehensive income statements, explaining their rationale and offering comparative analyses. Additionally, it investigates accounting for corporate income tax, analyzing tax expenses, effective tax rates, and deferred tax assets/liabilities. The report concludes with a comparative evaluation of the financial performance of both companies, providing valuable insights into their accounting practices and financial health.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1: OWNER'S EQUITY........................................................................................................1

Listing equity items and their changes........................................................................................1

Comparative analysis of debt and equity position of both the companies..................................2

TASK 2: CASH FLOW STATEMENTS........................................................................................3

Listing the items of cash flow statements and its changes..........................................................3

Comparative analyses of CFS of both the companies using three activities...............................4

Comparative analysis of selected companies along with insights..............................................5

TASK 3: Other Comprehensive income statement..........................................................................5

Items in comprehensive income statement.................................................................................5

Rationale for comprehensive income statement.........................................................................6

Comparative analyses..................................................................................................................6

Comprehensive income in evaluating performance of managers of a company.........................7

TASK 4: Accounting for Corporate income tax..............................................................................7

Tax expenses shown in financial statements of both the companies..........................................7

Effective tax rate.........................................................................................................................7

Deferred tax assets/liabilities......................................................................................................8

Evaluation on Deferred tax liability............................................................................................8

Cash tax amount using book tax amount....................................................................................8

Determination of cash tax rate and its evaluation.......................................................................9

Reasons of variation in cash tax rate and book tax rate..............................................................9

CONCLUSION................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1: OWNER'S EQUITY........................................................................................................1

Listing equity items and their changes........................................................................................1

Comparative analysis of debt and equity position of both the companies..................................2

TASK 2: CASH FLOW STATEMENTS........................................................................................3

Listing the items of cash flow statements and its changes..........................................................3

Comparative analyses of CFS of both the companies using three activities...............................4

Comparative analysis of selected companies along with insights..............................................5

TASK 3: Other Comprehensive income statement..........................................................................5

Items in comprehensive income statement.................................................................................5

Rationale for comprehensive income statement.........................................................................6

Comparative analyses..................................................................................................................6

Comprehensive income in evaluating performance of managers of a company.........................7

TASK 4: Accounting for Corporate income tax..............................................................................7

Tax expenses shown in financial statements of both the companies..........................................7

Effective tax rate.........................................................................................................................7

Deferred tax assets/liabilities......................................................................................................8

Evaluation on Deferred tax liability............................................................................................8

Cash tax amount using book tax amount....................................................................................8

Determination of cash tax rate and its evaluation.......................................................................9

Reasons of variation in cash tax rate and book tax rate..............................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

APPENDIX....................................................................................................................................11

APPENDIX....................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EXECUTIVE SUMMARY

This project summarises that corporate accounting is a process of developing financial

statements and interpreting them in order to perform comparative analyses. Two companies

which are listed on ASX are selected named as LandMark White Limited and Land & Homes

Group operating in real estate. In order to better understand this project financial statements of

both the countries are analysed. Tax revenue and liabilities are analysed to determine tax assets

of both the companies.

This project summarises that corporate accounting is a process of developing financial

statements and interpreting them in order to perform comparative analyses. Two companies

which are listed on ASX are selected named as LandMark White Limited and Land & Homes

Group operating in real estate. In order to better understand this project financial statements of

both the countries are analysed. Tax revenue and liabilities are analysed to determine tax assets

of both the companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Corporate accounting is a process of preparation and analysing the financial statements of

a corporate. Corporate includes various business entities which are formed with an objective to

run a lawful business. In order to understand this company, two companies are chosen in this

organisation which operates in same industry and that is real estate. LandMark White Limited

and Land & Homes Group are two companies which are chosen and analysed by evaluating their

annual reports in order to evaluate owner's equity, cash flow statements and tax liabilities of both

the companies (Dhaliwal and et. al., 2012).

TASK 1: OWNER'S EQUITY

Listing equity items and their changes

In terms of financing and accounting, equity refers to ownership or stocks. Equity items

are those units of ownership which includes equity shares. These items represents capital

contributed by the owners or the difference between a company's total assets and its total

liabilities (Edwards, 2013). In this project, two companies dealing in real estate are selected and

they are LandMark White Limited and Land & Homes Group. Equity items of these two

companies are listed below along with their reasons of change which are sourced from equity

position statement of both the companies :

Share capital/Ordinary shares – Share capital is the fund which is earned by an

organisation by selling their ordinary shares in public. This amount of equity shares is changes

over time and company wishes to increase this amount in order to increase their capital (Epstein,

2018). From the statement of changes in equity of both the companies, various changes are seen.

In case of Land & Homes Group limited, ordinary shares are reflecting an increasing trend. In

the year 2015, these shares were 52163223, 60541493 in 2016 and 69078509 in 2017. The

reason for its increasing trend is issuance of new shares in market. This increase is beneficial for

the company but not for the investors as it shows that there is less proportion of ownership of

investors in firm's capital. In the case of LandMark White Limited, there is also an increasing

trend like the other company. Share capital of this company in 2015 was 6008000, 6050000 in

2016 and 33773000 in 2017. The main reason of its change is that this company is successful in

paying their debts and new capital is supplied to them by new issue.

1

Corporate accounting is a process of preparation and analysing the financial statements of

a corporate. Corporate includes various business entities which are formed with an objective to

run a lawful business. In order to understand this company, two companies are chosen in this

organisation which operates in same industry and that is real estate. LandMark White Limited

and Land & Homes Group are two companies which are chosen and analysed by evaluating their

annual reports in order to evaluate owner's equity, cash flow statements and tax liabilities of both

the companies (Dhaliwal and et. al., 2012).

TASK 1: OWNER'S EQUITY

Listing equity items and their changes

In terms of financing and accounting, equity refers to ownership or stocks. Equity items

are those units of ownership which includes equity shares. These items represents capital

contributed by the owners or the difference between a company's total assets and its total

liabilities (Edwards, 2013). In this project, two companies dealing in real estate are selected and

they are LandMark White Limited and Land & Homes Group. Equity items of these two

companies are listed below along with their reasons of change which are sourced from equity

position statement of both the companies :

Share capital/Ordinary shares – Share capital is the fund which is earned by an

organisation by selling their ordinary shares in public. This amount of equity shares is changes

over time and company wishes to increase this amount in order to increase their capital (Epstein,

2018). From the statement of changes in equity of both the companies, various changes are seen.

In case of Land & Homes Group limited, ordinary shares are reflecting an increasing trend. In

the year 2015, these shares were 52163223, 60541493 in 2016 and 69078509 in 2017. The

reason for its increasing trend is issuance of new shares in market. This increase is beneficial for

the company but not for the investors as it shows that there is less proportion of ownership of

investors in firm's capital. In the case of LandMark White Limited, there is also an increasing

trend like the other company. Share capital of this company in 2015 was 6008000, 6050000 in

2016 and 33773000 in 2017. The main reason of its change is that this company is successful in

paying their debts and new capital is supplied to them by new issue.

1

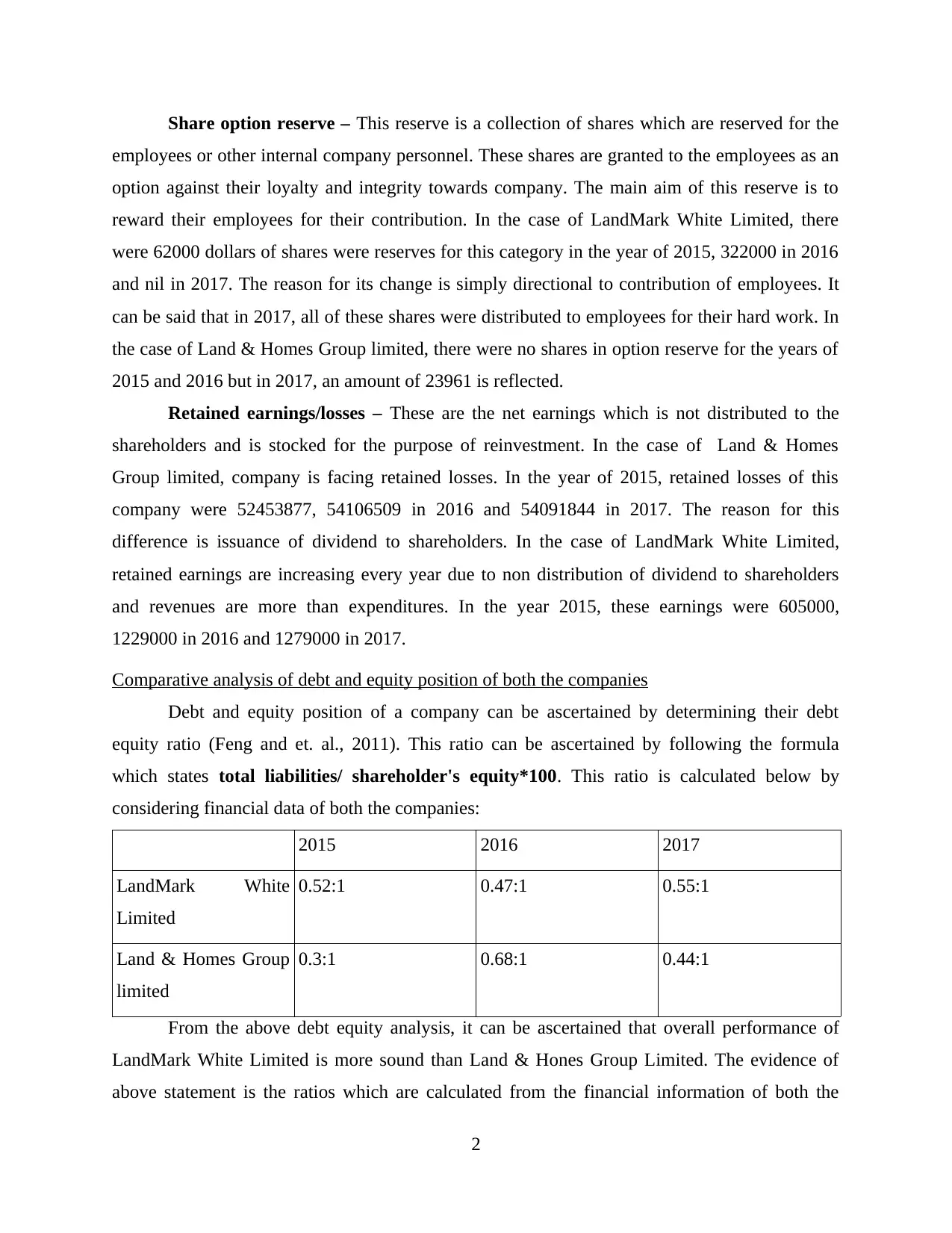

Share option reserve – This reserve is a collection of shares which are reserved for the

employees or other internal company personnel. These shares are granted to the employees as an

option against their loyalty and integrity towards company. The main aim of this reserve is to

reward their employees for their contribution. In the case of LandMark White Limited, there

were 62000 dollars of shares were reserves for this category in the year of 2015, 322000 in 2016

and nil in 2017. The reason for its change is simply directional to contribution of employees. It

can be said that in 2017, all of these shares were distributed to employees for their hard work. In

the case of Land & Homes Group limited, there were no shares in option reserve for the years of

2015 and 2016 but in 2017, an amount of 23961 is reflected.

Retained earnings/losses – These are the net earnings which is not distributed to the

shareholders and is stocked for the purpose of reinvestment. In the case of Land & Homes

Group limited, company is facing retained losses. In the year of 2015, retained losses of this

company were 52453877, 54106509 in 2016 and 54091844 in 2017. The reason for this

difference is issuance of dividend to shareholders. In the case of LandMark White Limited,

retained earnings are increasing every year due to non distribution of dividend to shareholders

and revenues are more than expenditures. In the year 2015, these earnings were 605000,

1229000 in 2016 and 1279000 in 2017.

Comparative analysis of debt and equity position of both the companies

Debt and equity position of a company can be ascertained by determining their debt

equity ratio (Feng and et. al., 2011). This ratio can be ascertained by following the formula

which states total liabilities/ shareholder's equity*100. This ratio is calculated below by

considering financial data of both the companies:

2015 2016 2017

LandMark White

Limited

0.52:1 0.47:1 0.55:1

Land & Homes Group

limited

0.3:1 0.68:1 0.44:1

From the above debt equity analysis, it can be ascertained that overall performance of

LandMark White Limited is more sound than Land & Hones Group Limited. The evidence of

above statement is the ratios which are calculated from the financial information of both the

2

employees or other internal company personnel. These shares are granted to the employees as an

option against their loyalty and integrity towards company. The main aim of this reserve is to

reward their employees for their contribution. In the case of LandMark White Limited, there

were 62000 dollars of shares were reserves for this category in the year of 2015, 322000 in 2016

and nil in 2017. The reason for its change is simply directional to contribution of employees. It

can be said that in 2017, all of these shares were distributed to employees for their hard work. In

the case of Land & Homes Group limited, there were no shares in option reserve for the years of

2015 and 2016 but in 2017, an amount of 23961 is reflected.

Retained earnings/losses – These are the net earnings which is not distributed to the

shareholders and is stocked for the purpose of reinvestment. In the case of Land & Homes

Group limited, company is facing retained losses. In the year of 2015, retained losses of this

company were 52453877, 54106509 in 2016 and 54091844 in 2017. The reason for this

difference is issuance of dividend to shareholders. In the case of LandMark White Limited,

retained earnings are increasing every year due to non distribution of dividend to shareholders

and revenues are more than expenditures. In the year 2015, these earnings were 605000,

1229000 in 2016 and 1279000 in 2017.

Comparative analysis of debt and equity position of both the companies

Debt and equity position of a company can be ascertained by determining their debt

equity ratio (Feng and et. al., 2011). This ratio can be ascertained by following the formula

which states total liabilities/ shareholder's equity*100. This ratio is calculated below by

considering financial data of both the companies:

2015 2016 2017

LandMark White

Limited

0.52:1 0.47:1 0.55:1

Land & Homes Group

limited

0.3:1 0.68:1 0.44:1

From the above debt equity analysis, it can be ascertained that overall performance of

LandMark White Limited is more sound than Land & Hones Group Limited. The evidence of

above statement is the ratios which are calculated from the financial information of both the

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

companies. In the case of LandMark White Limited, debt equity ratio was 0.52:1 in 2015, 0.47:1

in 2016 and 0.55:1 in 2017. This ratio shows that this company procures less debt capital when

compared to equity capital.

In the case of Land & Homes Group Limited, debt equity ratios are comparatively lower

than the other company. In the year of 2015, this ratio was reflected as 0.3:1, 0.68:1 in 2016 and

0.44:1 in 2017. The reason of these changes are this company prefers to increase their capital by

issuing shares in public rather than lending amount in order to increase the capital. Debt capital

of this company is lower than equity capital which shows that company is paying extra cost for

obtaining equity capital as debt capital funding is considered as cheaper to procure.

TASK 2: CASH FLOW STATEMENTS

Listing the items of cash flow statements and its changes

Cash flow statement is a kind of financial statement which shows all cash inflows and

outflows of a company. These inflows and outflows are divided into three categories and that is

operating, investing and financing. The main aim of this statement is to record items of cash and

cash equivalents (Fisher and Krumwiede, 2012). Some of these items are discussed below which

are shown in the CFS of both the selected companies.

Interest received – This is considered as cash inflow which is received from the deposits

which are deposited in banks and other financial institutions. This interest is considered a income

by the organisation from operating activities. According to the cash flow statement of LandMark

White Limited, it has been seen that in year 2015 this income was amounting 21000, 8000 in

2016 and 15000 in 2017. These fluctuations are the result of unbalanced deposits in the bank due

to which its interest is also fluctuates. According to the CFS of Land & Homes Group Limited,

there is no interest received in 2015. But in the year of 2016, interest amounting 33752 is

received and 12565 is received in 2017. These changes in the value of interest are the result of

unbalanced deposits by this company due to which they are earning non proportionate amount of

interest.

Payments for property – This item is recorded in investing activities head of both the

company. This item is concerned with paying the due amount against the property which is

acquired by an organisation, it is a cash outflow. From the cash flow statement of LandMark

White Limited, there is an outflow of cash amounting 198000 in 2015, 242000 in 2016 and

3

in 2016 and 0.55:1 in 2017. This ratio shows that this company procures less debt capital when

compared to equity capital.

In the case of Land & Homes Group Limited, debt equity ratios are comparatively lower

than the other company. In the year of 2015, this ratio was reflected as 0.3:1, 0.68:1 in 2016 and

0.44:1 in 2017. The reason of these changes are this company prefers to increase their capital by

issuing shares in public rather than lending amount in order to increase the capital. Debt capital

of this company is lower than equity capital which shows that company is paying extra cost for

obtaining equity capital as debt capital funding is considered as cheaper to procure.

TASK 2: CASH FLOW STATEMENTS

Listing the items of cash flow statements and its changes

Cash flow statement is a kind of financial statement which shows all cash inflows and

outflows of a company. These inflows and outflows are divided into three categories and that is

operating, investing and financing. The main aim of this statement is to record items of cash and

cash equivalents (Fisher and Krumwiede, 2012). Some of these items are discussed below which

are shown in the CFS of both the selected companies.

Interest received – This is considered as cash inflow which is received from the deposits

which are deposited in banks and other financial institutions. This interest is considered a income

by the organisation from operating activities. According to the cash flow statement of LandMark

White Limited, it has been seen that in year 2015 this income was amounting 21000, 8000 in

2016 and 15000 in 2017. These fluctuations are the result of unbalanced deposits in the bank due

to which its interest is also fluctuates. According to the CFS of Land & Homes Group Limited,

there is no interest received in 2015. But in the year of 2016, interest amounting 33752 is

received and 12565 is received in 2017. These changes in the value of interest are the result of

unbalanced deposits by this company due to which they are earning non proportionate amount of

interest.

Payments for property – This item is recorded in investing activities head of both the

company. This item is concerned with paying the due amount against the property which is

acquired by an organisation, it is a cash outflow. From the cash flow statement of LandMark

White Limited, there is an outflow of cash amounting 198000 in 2015, 242000 in 2016 and

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

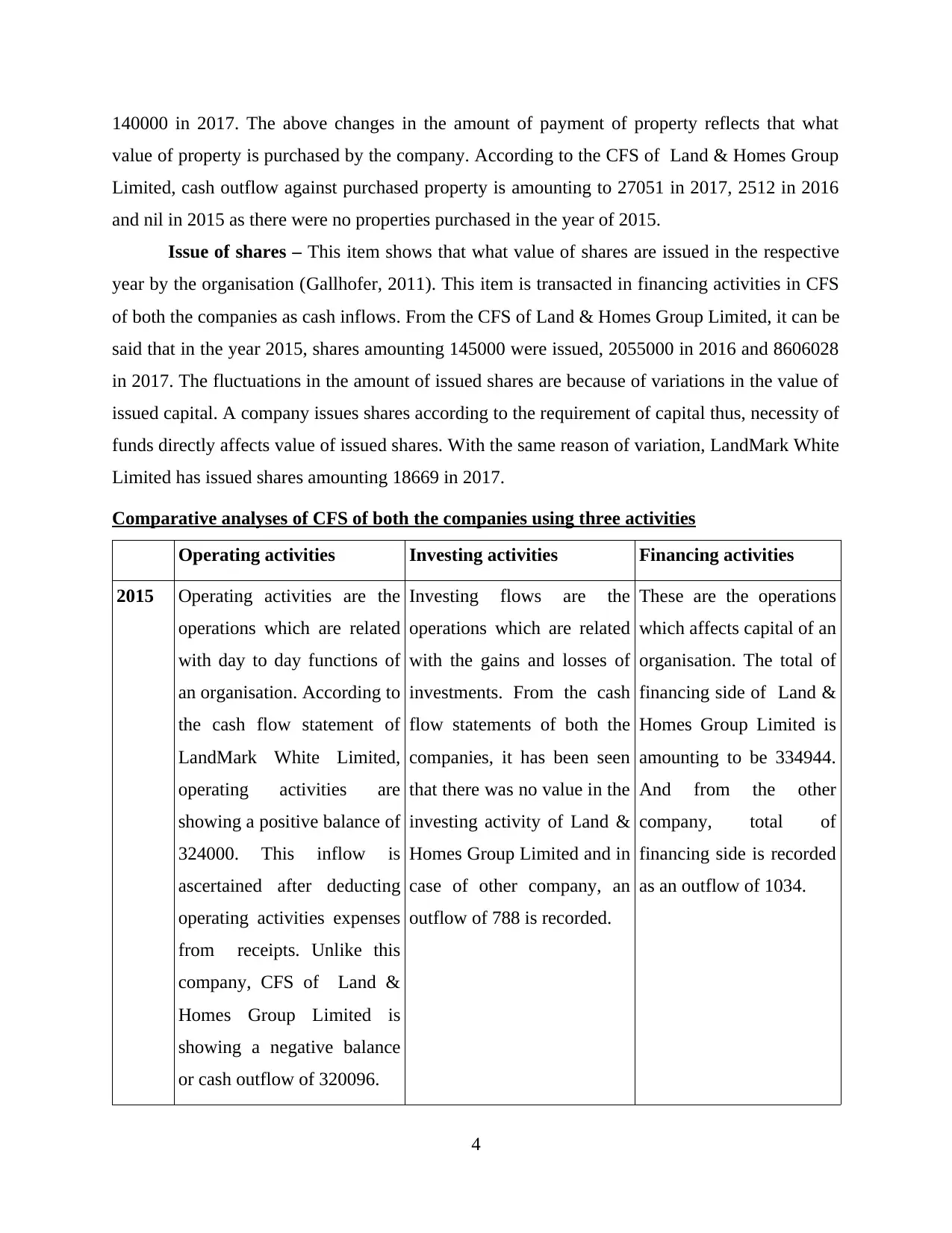

140000 in 2017. The above changes in the amount of payment of property reflects that what

value of property is purchased by the company. According to the CFS of Land & Homes Group

Limited, cash outflow against purchased property is amounting to 27051 in 2017, 2512 in 2016

and nil in 2015 as there were no properties purchased in the year of 2015.

Issue of shares – This item shows that what value of shares are issued in the respective

year by the organisation (Gallhofer, 2011). This item is transacted in financing activities in CFS

of both the companies as cash inflows. From the CFS of Land & Homes Group Limited, it can be

said that in the year 2015, shares amounting 145000 were issued, 2055000 in 2016 and 8606028

in 2017. The fluctuations in the amount of issued shares are because of variations in the value of

issued capital. A company issues shares according to the requirement of capital thus, necessity of

funds directly affects value of issued shares. With the same reason of variation, LandMark White

Limited has issued shares amounting 18669 in 2017.

Comparative analyses of CFS of both the companies using three activities

Operating activities Investing activities Financing activities

2015 Operating activities are the

operations which are related

with day to day functions of

an organisation. According to

the cash flow statement of

LandMark White Limited,

operating activities are

showing a positive balance of

324000. This inflow is

ascertained after deducting

operating activities expenses

from receipts. Unlike this

company, CFS of Land &

Homes Group Limited is

showing a negative balance

or cash outflow of 320096.

Investing flows are the

operations which are related

with the gains and losses of

investments. From the cash

flow statements of both the

companies, it has been seen

that there was no value in the

investing activity of Land &

Homes Group Limited and in

case of other company, an

outflow of 788 is recorded.

These are the operations

which affects capital of an

organisation. The total of

financing side of Land &

Homes Group Limited is

amounting to be 334944.

And from the other

company, total of

financing side is recorded

as an outflow of 1034.

4

value of property is purchased by the company. According to the CFS of Land & Homes Group

Limited, cash outflow against purchased property is amounting to 27051 in 2017, 2512 in 2016

and nil in 2015 as there were no properties purchased in the year of 2015.

Issue of shares – This item shows that what value of shares are issued in the respective

year by the organisation (Gallhofer, 2011). This item is transacted in financing activities in CFS

of both the companies as cash inflows. From the CFS of Land & Homes Group Limited, it can be

said that in the year 2015, shares amounting 145000 were issued, 2055000 in 2016 and 8606028

in 2017. The fluctuations in the amount of issued shares are because of variations in the value of

issued capital. A company issues shares according to the requirement of capital thus, necessity of

funds directly affects value of issued shares. With the same reason of variation, LandMark White

Limited has issued shares amounting 18669 in 2017.

Comparative analyses of CFS of both the companies using three activities

Operating activities Investing activities Financing activities

2015 Operating activities are the

operations which are related

with day to day functions of

an organisation. According to

the cash flow statement of

LandMark White Limited,

operating activities are

showing a positive balance of

324000. This inflow is

ascertained after deducting

operating activities expenses

from receipts. Unlike this

company, CFS of Land &

Homes Group Limited is

showing a negative balance

or cash outflow of 320096.

Investing flows are the

operations which are related

with the gains and losses of

investments. From the cash

flow statements of both the

companies, it has been seen

that there was no value in the

investing activity of Land &

Homes Group Limited and in

case of other company, an

outflow of 788 is recorded.

These are the operations

which affects capital of an

organisation. The total of

financing side of Land &

Homes Group Limited is

amounting to be 334944.

And from the other

company, total of

financing side is recorded

as an outflow of 1034.

4

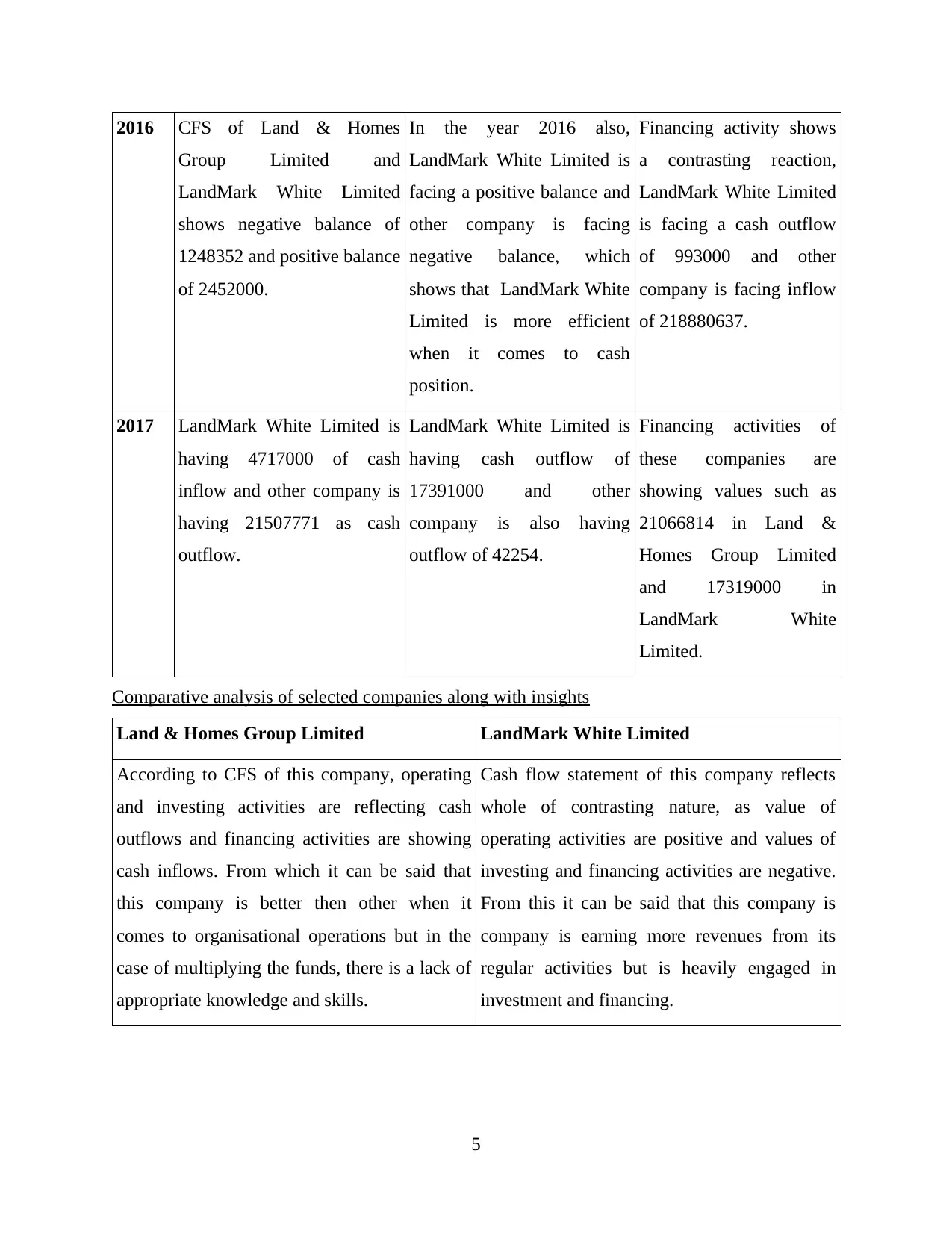

2016 CFS of Land & Homes

Group Limited and

LandMark White Limited

shows negative balance of

1248352 and positive balance

of 2452000.

In the year 2016 also,

LandMark White Limited is

facing a positive balance and

other company is facing

negative balance, which

shows that LandMark White

Limited is more efficient

when it comes to cash

position.

Financing activity shows

a contrasting reaction,

LandMark White Limited

is facing a cash outflow

of 993000 and other

company is facing inflow

of 218880637.

2017 LandMark White Limited is

having 4717000 of cash

inflow and other company is

having 21507771 as cash

outflow.

LandMark White Limited is

having cash outflow of

17391000 and other

company is also having

outflow of 42254.

Financing activities of

these companies are

showing values such as

21066814 in Land &

Homes Group Limited

and 17319000 in

LandMark White

Limited.

Comparative analysis of selected companies along with insights

Land & Homes Group Limited LandMark White Limited

According to CFS of this company, operating

and investing activities are reflecting cash

outflows and financing activities are showing

cash inflows. From which it can be said that

this company is better then other when it

comes to organisational operations but in the

case of multiplying the funds, there is a lack of

appropriate knowledge and skills.

Cash flow statement of this company reflects

whole of contrasting nature, as value of

operating activities are positive and values of

investing and financing activities are negative.

From this it can be said that this company is

company is earning more revenues from its

regular activities but is heavily engaged in

investment and financing.

5

Group Limited and

LandMark White Limited

shows negative balance of

1248352 and positive balance

of 2452000.

In the year 2016 also,

LandMark White Limited is

facing a positive balance and

other company is facing

negative balance, which

shows that LandMark White

Limited is more efficient

when it comes to cash

position.

Financing activity shows

a contrasting reaction,

LandMark White Limited

is facing a cash outflow

of 993000 and other

company is facing inflow

of 218880637.

2017 LandMark White Limited is

having 4717000 of cash

inflow and other company is

having 21507771 as cash

outflow.

LandMark White Limited is

having cash outflow of

17391000 and other

company is also having

outflow of 42254.

Financing activities of

these companies are

showing values such as

21066814 in Land &

Homes Group Limited

and 17319000 in

LandMark White

Limited.

Comparative analysis of selected companies along with insights

Land & Homes Group Limited LandMark White Limited

According to CFS of this company, operating

and investing activities are reflecting cash

outflows and financing activities are showing

cash inflows. From which it can be said that

this company is better then other when it

comes to organisational operations but in the

case of multiplying the funds, there is a lack of

appropriate knowledge and skills.

Cash flow statement of this company reflects

whole of contrasting nature, as value of

operating activities are positive and values of

investing and financing activities are negative.

From this it can be said that this company is

company is earning more revenues from its

regular activities but is heavily engaged in

investment and financing.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

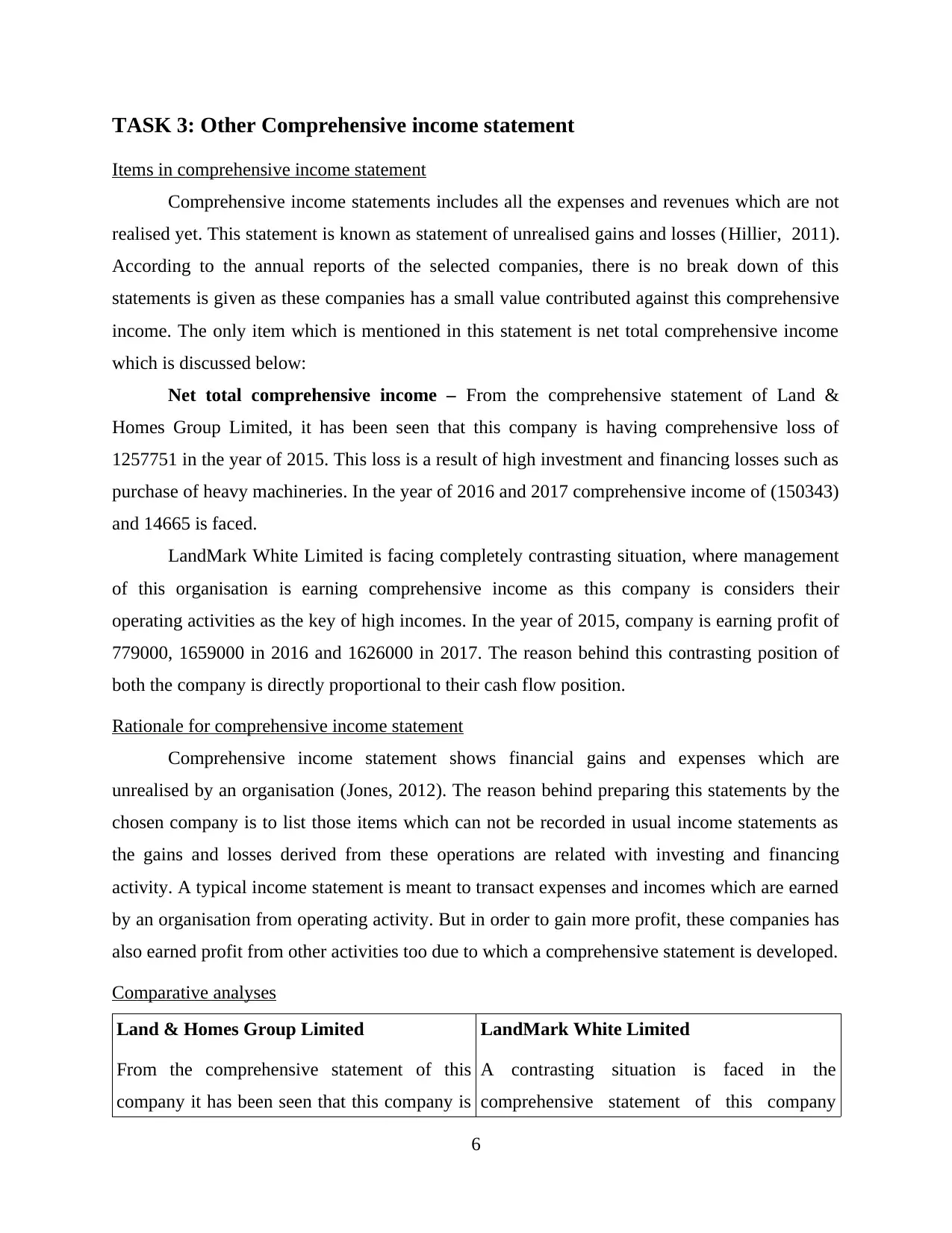

TASK 3: Other Comprehensive income statement

Items in comprehensive income statement

Comprehensive income statements includes all the expenses and revenues which are not

realised yet. This statement is known as statement of unrealised gains and losses (Hillier, 2011).

According to the annual reports of the selected companies, there is no break down of this

statements is given as these companies has a small value contributed against this comprehensive

income. The only item which is mentioned in this statement is net total comprehensive income

which is discussed below:

Net total comprehensive income – From the comprehensive statement of Land &

Homes Group Limited, it has been seen that this company is having comprehensive loss of

1257751 in the year of 2015. This loss is a result of high investment and financing losses such as

purchase of heavy machineries. In the year of 2016 and 2017 comprehensive income of (150343)

and 14665 is faced.

LandMark White Limited is facing completely contrasting situation, where management

of this organisation is earning comprehensive income as this company is considers their

operating activities as the key of high incomes. In the year of 2015, company is earning profit of

779000, 1659000 in 2016 and 1626000 in 2017. The reason behind this contrasting position of

both the company is directly proportional to their cash flow position.

Rationale for comprehensive income statement

Comprehensive income statement shows financial gains and expenses which are

unrealised by an organisation (Jones, 2012). The reason behind preparing this statements by the

chosen company is to list those items which can not be recorded in usual income statements as

the gains and losses derived from these operations are related with investing and financing

activity. A typical income statement is meant to transact expenses and incomes which are earned

by an organisation from operating activity. But in order to gain more profit, these companies has

also earned profit from other activities too due to which a comprehensive statement is developed.

Comparative analyses

Land & Homes Group Limited LandMark White Limited

From the comprehensive statement of this

company it has been seen that this company is

A contrasting situation is faced in the

comprehensive statement of this company

6

Items in comprehensive income statement

Comprehensive income statements includes all the expenses and revenues which are not

realised yet. This statement is known as statement of unrealised gains and losses (Hillier, 2011).

According to the annual reports of the selected companies, there is no break down of this

statements is given as these companies has a small value contributed against this comprehensive

income. The only item which is mentioned in this statement is net total comprehensive income

which is discussed below:

Net total comprehensive income – From the comprehensive statement of Land &

Homes Group Limited, it has been seen that this company is having comprehensive loss of

1257751 in the year of 2015. This loss is a result of high investment and financing losses such as

purchase of heavy machineries. In the year of 2016 and 2017 comprehensive income of (150343)

and 14665 is faced.

LandMark White Limited is facing completely contrasting situation, where management

of this organisation is earning comprehensive income as this company is considers their

operating activities as the key of high incomes. In the year of 2015, company is earning profit of

779000, 1659000 in 2016 and 1626000 in 2017. The reason behind this contrasting position of

both the company is directly proportional to their cash flow position.

Rationale for comprehensive income statement

Comprehensive income statement shows financial gains and expenses which are

unrealised by an organisation (Jones, 2012). The reason behind preparing this statements by the

chosen company is to list those items which can not be recorded in usual income statements as

the gains and losses derived from these operations are related with investing and financing

activity. A typical income statement is meant to transact expenses and incomes which are earned

by an organisation from operating activity. But in order to gain more profit, these companies has

also earned profit from other activities too due to which a comprehensive statement is developed.

Comparative analyses

Land & Homes Group Limited LandMark White Limited

From the comprehensive statement of this

company it has been seen that this company is

A contrasting situation is faced in the

comprehensive statement of this company

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investing a lot in capital assets due to which

they are facing comprehensive losses despite if

the year of 2017.

according to which this company is facilitated

by comprehensive incomes due to which high

profits from investing and financing activities.

If comprehensive income and loss is recorded in typical income statement, then company

has to face issues regarding classifying profits and losses earned and incurred by various

activities such as operating, investing and financing. Profit which is attributable to shareholders

is derived from both income statement and comprehensive statement due to which both of these

statements are equally important for them.

Comprehensive income in evaluating performance of managers of a company

Comprehensive incomes such as gains from investing and financing activities should be

considered by the managers of an organisation while evaluating the performance of their

company (Kim, 2012). Both the companies which are selected in this report should consider their

comprehensive statement while analysing position of their companies. The reason behind above

statement is that income which is recorded in this statement is earned from investing and

financing activities and these activities are also a part of an organisation.

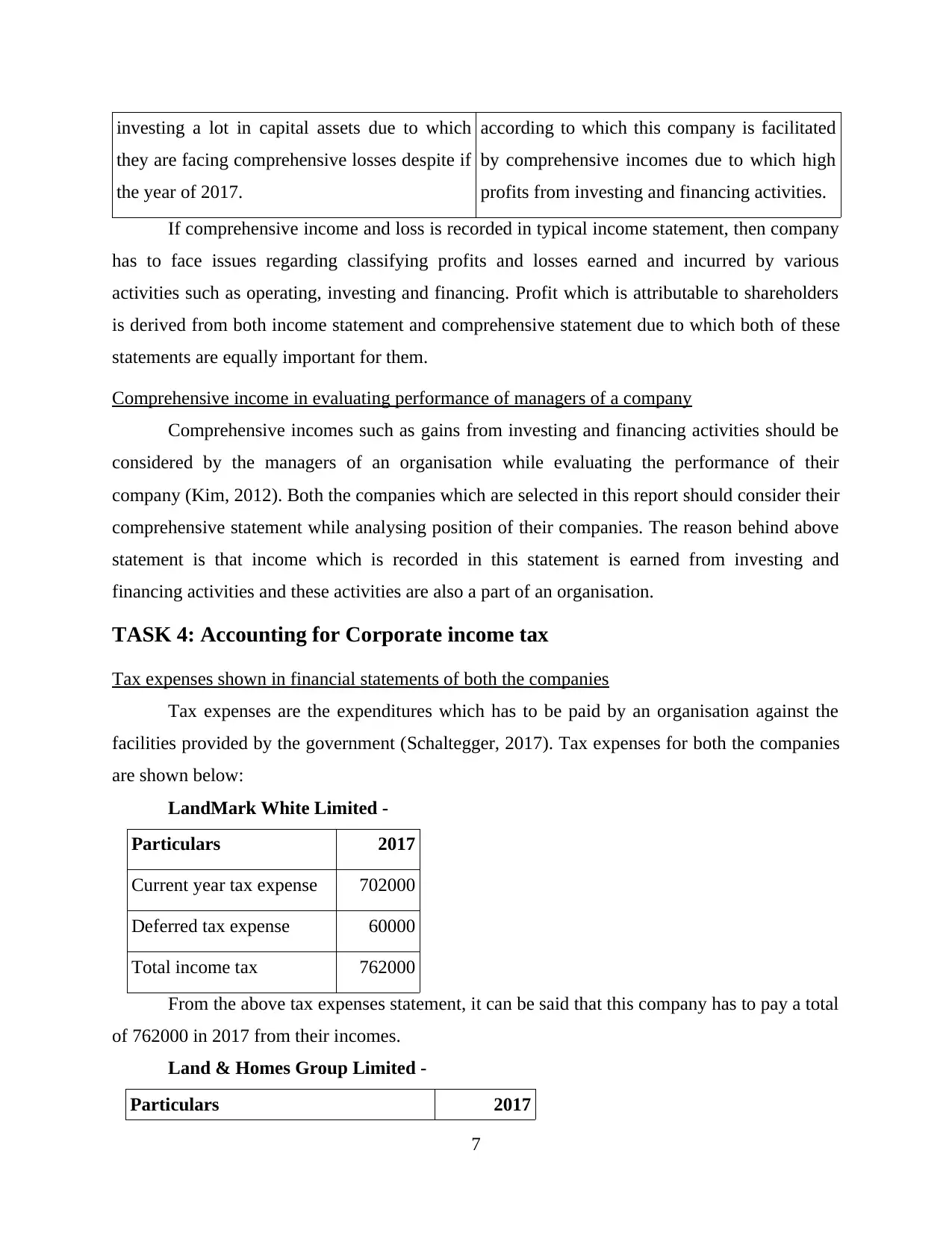

TASK 4: Accounting for Corporate income tax

Tax expenses shown in financial statements of both the companies

Tax expenses are the expenditures which has to be paid by an organisation against the

facilities provided by the government (Schaltegger, 2017). Tax expenses for both the companies

are shown below:

LandMark White Limited -

Particulars 2017

Current year tax expense 702000

Deferred tax expense 60000

Total income tax 762000

From the above tax expenses statement, it can be said that this company has to pay a total

of 762000 in 2017 from their incomes.

Land & Homes Group Limited -

Particulars 2017

7

they are facing comprehensive losses despite if

the year of 2017.

according to which this company is facilitated

by comprehensive incomes due to which high

profits from investing and financing activities.

If comprehensive income and loss is recorded in typical income statement, then company

has to face issues regarding classifying profits and losses earned and incurred by various

activities such as operating, investing and financing. Profit which is attributable to shareholders

is derived from both income statement and comprehensive statement due to which both of these

statements are equally important for them.

Comprehensive income in evaluating performance of managers of a company

Comprehensive incomes such as gains from investing and financing activities should be

considered by the managers of an organisation while evaluating the performance of their

company (Kim, 2012). Both the companies which are selected in this report should consider their

comprehensive statement while analysing position of their companies. The reason behind above

statement is that income which is recorded in this statement is earned from investing and

financing activities and these activities are also a part of an organisation.

TASK 4: Accounting for Corporate income tax

Tax expenses shown in financial statements of both the companies

Tax expenses are the expenditures which has to be paid by an organisation against the

facilities provided by the government (Schaltegger, 2017). Tax expenses for both the companies

are shown below:

LandMark White Limited -

Particulars 2017

Current year tax expense 702000

Deferred tax expense 60000

Total income tax 762000

From the above tax expenses statement, it can be said that this company has to pay a total

of 762000 in 2017 from their incomes.

Land & Homes Group Limited -

Particulars 2017

7

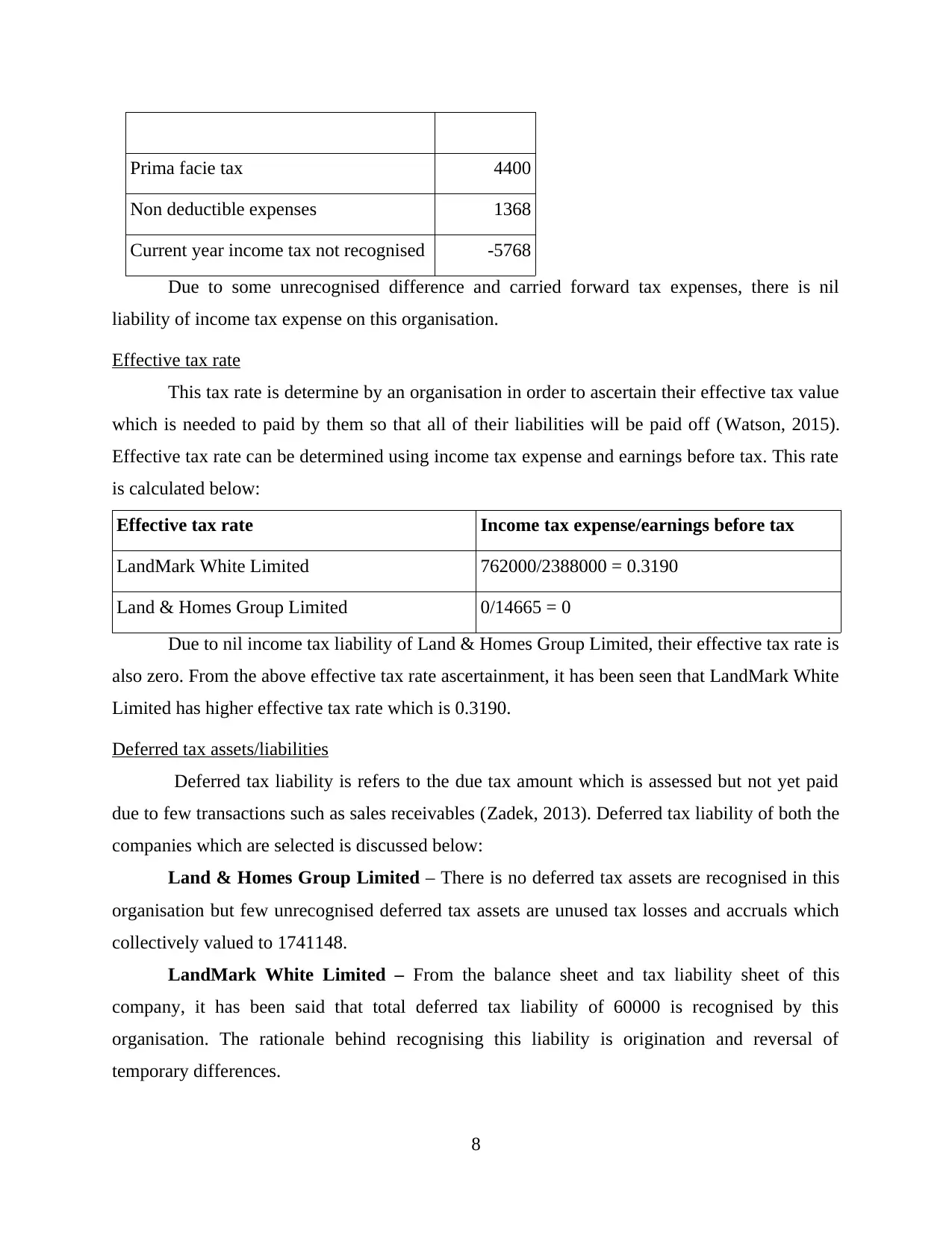

Prima facie tax 4400

Non deductible expenses 1368

Current year income tax not recognised -5768

Due to some unrecognised difference and carried forward tax expenses, there is nil

liability of income tax expense on this organisation.

Effective tax rate

This tax rate is determine by an organisation in order to ascertain their effective tax value

which is needed to paid by them so that all of their liabilities will be paid off (Watson, 2015).

Effective tax rate can be determined using income tax expense and earnings before tax. This rate

is calculated below:

Effective tax rate Income tax expense/earnings before tax

LandMark White Limited 762000/2388000 = 0.3190

Land & Homes Group Limited 0/14665 = 0

Due to nil income tax liability of Land & Homes Group Limited, their effective tax rate is

also zero. From the above effective tax rate ascertainment, it has been seen that LandMark White

Limited has higher effective tax rate which is 0.3190.

Deferred tax assets/liabilities

Deferred tax liability is refers to the due tax amount which is assessed but not yet paid

due to few transactions such as sales receivables (Zadek, 2013). Deferred tax liability of both the

companies which are selected is discussed below:

Land & Homes Group Limited – There is no deferred tax assets are recognised in this

organisation but few unrecognised deferred tax assets are unused tax losses and accruals which

collectively valued to 1741148.

LandMark White Limited – From the balance sheet and tax liability sheet of this

company, it has been said that total deferred tax liability of 60000 is recognised by this

organisation. The rationale behind recognising this liability is origination and reversal of

temporary differences.

8

Non deductible expenses 1368

Current year income tax not recognised -5768

Due to some unrecognised difference and carried forward tax expenses, there is nil

liability of income tax expense on this organisation.

Effective tax rate

This tax rate is determine by an organisation in order to ascertain their effective tax value

which is needed to paid by them so that all of their liabilities will be paid off (Watson, 2015).

Effective tax rate can be determined using income tax expense and earnings before tax. This rate

is calculated below:

Effective tax rate Income tax expense/earnings before tax

LandMark White Limited 762000/2388000 = 0.3190

Land & Homes Group Limited 0/14665 = 0

Due to nil income tax liability of Land & Homes Group Limited, their effective tax rate is

also zero. From the above effective tax rate ascertainment, it has been seen that LandMark White

Limited has higher effective tax rate which is 0.3190.

Deferred tax assets/liabilities

Deferred tax liability is refers to the due tax amount which is assessed but not yet paid

due to few transactions such as sales receivables (Zadek, 2013). Deferred tax liability of both the

companies which are selected is discussed below:

Land & Homes Group Limited – There is no deferred tax assets are recognised in this

organisation but few unrecognised deferred tax assets are unused tax losses and accruals which

collectively valued to 1741148.

LandMark White Limited – From the balance sheet and tax liability sheet of this

company, it has been said that total deferred tax liability of 60000 is recognised by this

organisation. The rationale behind recognising this liability is origination and reversal of

temporary differences.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.