Corporate Accounting Analysis

VerifiedAdded on 2020/11/12

|11

|3553

|69

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices at Wesfarmers Ltd, detailing equity items, tax expenses, and the interpretation of financial statements. It highlights the importance of corporate accounting in decision-making and financial reporting, showcasing the company's performance and tax obligations over the years.

Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1) Listing of each items of equity................................................................................................1

2) Firm’s tax expense in its latest financial statements...............................................................3

3) Company tax rate times your firm’s accounting income........................................................3

4) Deferred tax assets/liabilities..................................................................................................4

5) Current tax assets or income tax payable recorded by company.............................................6

6) Income statement same as the income tax paid shown in the cash flow statement................6

7) Interpretation...........................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDEX.....................................................................................................................................9

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1) Listing of each items of equity................................................................................................1

2) Firm’s tax expense in its latest financial statements...............................................................3

3) Company tax rate times your firm’s accounting income........................................................3

4) Deferred tax assets/liabilities..................................................................................................4

5) Current tax assets or income tax payable recorded by company.............................................6

6) Income statement same as the income tax paid shown in the cash flow statement................6

7) Interpretation...........................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

APPENDEX.....................................................................................................................................9

INTRODUCTION

Corporate accounting deals with the processes like preparation of balance sheet, financial

reports and records, cash flow statements etc. In present time accountant of companies uses

special concept of accounting that help them to prepare financial accounts, cash flow statements,

analysis and interpretation of financial result and accounting. This help them in making effective

decision such as amalgamation, absorption, preparation of consolidated statements. To

understand the importance of corporate accounting the company selected is “Wesfarmer Ltd”

that is listed on ASX.

In this project, identification and interpretation of each item of equity is done. Firm tax

expense in latest financial statements, comment on deferred tax assets liabilities is reported and

reason for their reporting is analysed. This report also shows current tax assets or income tax

payable recorded by company, reason why the income tax expenses shown in the income

statements are the same as in the cash flow statements.

MAIN BODY

1) Listing of each items of equity

Equity items:

The item that are listed on equity are consider to be owner capital worth that is being

derived from the total liabilities and assets that they carry them within company. In general,

these types of account and their description shows the amount actual owner's equity that depend

on the nature of firm’s operation. From the annual report of “Wesfarmers Ltd” the data is taken

from which following information is collected. Thus there are assorted types of equity account

that are combined together in order to make total shareholder equity. Some examples of equity

are common stock, issued capital, contributing surplus, retained earnings, reserved share and

additional paid-up capital. These items are discussed below as per the annual statements

maintained by company (Wesfarmers Ltd.):

Issued capital: It refers to the actual number of shares that have been issued by the entity

to its shareholder (DeBusk, 2012). In accounting terms, the allotted share or share

subsequently held by the existing shareholder are known as issued capital. From the

annual report 2017-18 of “Wesfarmers Ltd” it has been observed that issued capital for

year 2017 was $22268 that had grown up to $22277 in year 2018. There is an increase in

1

Corporate accounting deals with the processes like preparation of balance sheet, financial

reports and records, cash flow statements etc. In present time accountant of companies uses

special concept of accounting that help them to prepare financial accounts, cash flow statements,

analysis and interpretation of financial result and accounting. This help them in making effective

decision such as amalgamation, absorption, preparation of consolidated statements. To

understand the importance of corporate accounting the company selected is “Wesfarmer Ltd”

that is listed on ASX.

In this project, identification and interpretation of each item of equity is done. Firm tax

expense in latest financial statements, comment on deferred tax assets liabilities is reported and

reason for their reporting is analysed. This report also shows current tax assets or income tax

payable recorded by company, reason why the income tax expenses shown in the income

statements are the same as in the cash flow statements.

MAIN BODY

1) Listing of each items of equity

Equity items:

The item that are listed on equity are consider to be owner capital worth that is being

derived from the total liabilities and assets that they carry them within company. In general,

these types of account and their description shows the amount actual owner's equity that depend

on the nature of firm’s operation. From the annual report of “Wesfarmers Ltd” the data is taken

from which following information is collected. Thus there are assorted types of equity account

that are combined together in order to make total shareholder equity. Some examples of equity

are common stock, issued capital, contributing surplus, retained earnings, reserved share and

additional paid-up capital. These items are discussed below as per the annual statements

maintained by company (Wesfarmers Ltd.):

Issued capital: It refers to the actual number of shares that have been issued by the entity

to its shareholder (DeBusk, 2012). In accounting terms, the allotted share or share

subsequently held by the existing shareholder are known as issued capital. From the

annual report 2017-18 of “Wesfarmers Ltd” it has been observed that issued capital for

year 2017 was $22268 that had grown up to $22277 in year 2018. There is an increase in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

number of shareholders during the year of 2018 because respective company is growing

at a fast pace and give better result on investment to following shareholder. “Wesfarmers

Ltd” is one of the leading company thus it holds good market share and generate huge

profit throughout the year. Thus, board of director also decide to increase the rate of

return on investment that has also increased the issued capital.

Reserved share or common stock: This is considered to be the security of share an

entity has set aside for a particular administrative reason that shows the ownership.

Reserved share consists of bonds, debenture, securities etc. From the balance sheet of

“Wesfarmers Ltd” the amount of common stock increase form ($26) in year 2017 to

($43) in year 2018. The primary reason of fluctuation among the value of common stock

is basically due to the changes in amount of dividend and interest income obtained by the

company during an accounting year (Edgerton, 2012).

Retained earnings: These are termed as the profit that a company has earned to date

after deducting any dividend or any other distribution that have been paid to investor

during an accounting year. Manager hold this in order to reinvest in company business or

to write off any outstanding debts. From the annual report of “Wesfarmers Ltd” 2017-18

it has been observed that balance of retained earning has decreased from $1509 to $176.

The main reason for the reduction in retained earnings is that company may have

repurchase of company stock, paid some loans form retained amount or there has been

loss for the company during an accounting year.

Reserve: These are considered to be the types of gains that have been incurred by

company in order to meet any kind of future contingencies. It is observed that capital

under this account is being procured either from selling price of fixed assets or from total

shareholder equity. The balance sheet of “Wesfarmers Ltd” shows the balance of reserve

during year 2018 $344 and in year 2017 it was $190. There is increase in the balance

because company is doing well in the market and earning huge profit. Therefore, they

maintain sufficient amount into reserve to handle unexpected situation.

Items Year Wesfarmers Ltd

Issued capital 2017 22,268

201822,277

2

at a fast pace and give better result on investment to following shareholder. “Wesfarmers

Ltd” is one of the leading company thus it holds good market share and generate huge

profit throughout the year. Thus, board of director also decide to increase the rate of

return on investment that has also increased the issued capital.

Reserved share or common stock: This is considered to be the security of share an

entity has set aside for a particular administrative reason that shows the ownership.

Reserved share consists of bonds, debenture, securities etc. From the balance sheet of

“Wesfarmers Ltd” the amount of common stock increase form ($26) in year 2017 to

($43) in year 2018. The primary reason of fluctuation among the value of common stock

is basically due to the changes in amount of dividend and interest income obtained by the

company during an accounting year (Edgerton, 2012).

Retained earnings: These are termed as the profit that a company has earned to date

after deducting any dividend or any other distribution that have been paid to investor

during an accounting year. Manager hold this in order to reinvest in company business or

to write off any outstanding debts. From the annual report of “Wesfarmers Ltd” 2017-18

it has been observed that balance of retained earning has decreased from $1509 to $176.

The main reason for the reduction in retained earnings is that company may have

repurchase of company stock, paid some loans form retained amount or there has been

loss for the company during an accounting year.

Reserve: These are considered to be the types of gains that have been incurred by

company in order to meet any kind of future contingencies. It is observed that capital

under this account is being procured either from selling price of fixed assets or from total

shareholder equity. The balance sheet of “Wesfarmers Ltd” shows the balance of reserve

during year 2018 $344 and in year 2017 it was $190. There is increase in the balance

because company is doing well in the market and earning huge profit. Therefore, they

maintain sufficient amount into reserve to handle unexpected situation.

Items Year Wesfarmers Ltd

Issued capital 2017 22,268

201822,277

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

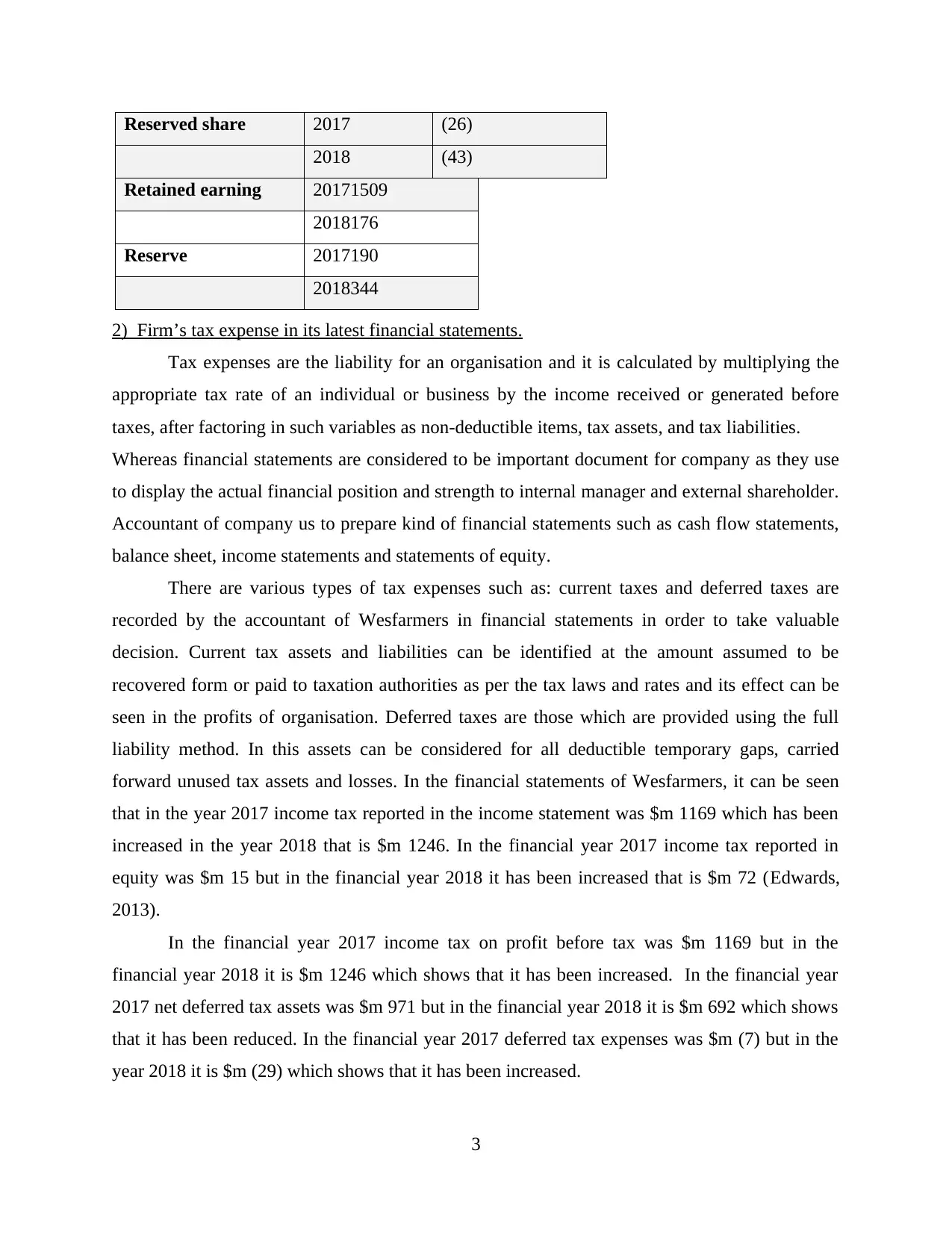

Reserved share 2017 (26)

2018 (43)

Retained earning 20171509

2018176

Reserve 2017190

2018344

2) Firm’s tax expense in its latest financial statements.

Tax expenses are the liability for an organisation and it is calculated by multiplying the

appropriate tax rate of an individual or business by the income received or generated before

taxes, after factoring in such variables as non-deductible items, tax assets, and tax liabilities.

Whereas financial statements are considered to be important document for company as they use

to display the actual financial position and strength to internal manager and external shareholder.

Accountant of company us to prepare kind of financial statements such as cash flow statements,

balance sheet, income statements and statements of equity.

There are various types of tax expenses such as: current taxes and deferred taxes are

recorded by the accountant of Wesfarmers in financial statements in order to take valuable

decision. Current tax assets and liabilities can be identified at the amount assumed to be

recovered form or paid to taxation authorities as per the tax laws and rates and its effect can be

seen in the profits of organisation. Deferred taxes are those which are provided using the full

liability method. In this assets can be considered for all deductible temporary gaps, carried

forward unused tax assets and losses. In the financial statements of Wesfarmers, it can be seen

that in the year 2017 income tax reported in the income statement was $m 1169 which has been

increased in the year 2018 that is $m 1246. In the financial year 2017 income tax reported in

equity was $m 15 but in the financial year 2018 it has been increased that is $m 72 (Edwards,

2013).

In the financial year 2017 income tax on profit before tax was $m 1169 but in the

financial year 2018 it is $m 1246 which shows that it has been increased. In the financial year

2017 net deferred tax assets was $m 971 but in the financial year 2018 it is $m 692 which shows

that it has been reduced. In the financial year 2017 deferred tax expenses was $m (7) but in the

year 2018 it is $m (29) which shows that it has been increased.

3

2018 (43)

Retained earning 20171509

2018176

Reserve 2017190

2018344

2) Firm’s tax expense in its latest financial statements.

Tax expenses are the liability for an organisation and it is calculated by multiplying the

appropriate tax rate of an individual or business by the income received or generated before

taxes, after factoring in such variables as non-deductible items, tax assets, and tax liabilities.

Whereas financial statements are considered to be important document for company as they use

to display the actual financial position and strength to internal manager and external shareholder.

Accountant of company us to prepare kind of financial statements such as cash flow statements,

balance sheet, income statements and statements of equity.

There are various types of tax expenses such as: current taxes and deferred taxes are

recorded by the accountant of Wesfarmers in financial statements in order to take valuable

decision. Current tax assets and liabilities can be identified at the amount assumed to be

recovered form or paid to taxation authorities as per the tax laws and rates and its effect can be

seen in the profits of organisation. Deferred taxes are those which are provided using the full

liability method. In this assets can be considered for all deductible temporary gaps, carried

forward unused tax assets and losses. In the financial statements of Wesfarmers, it can be seen

that in the year 2017 income tax reported in the income statement was $m 1169 which has been

increased in the year 2018 that is $m 1246. In the financial year 2017 income tax reported in

equity was $m 15 but in the financial year 2018 it has been increased that is $m 72 (Edwards,

2013).

In the financial year 2017 income tax on profit before tax was $m 1169 but in the

financial year 2018 it is $m 1246 which shows that it has been increased. In the financial year

2017 net deferred tax assets was $m 971 but in the financial year 2018 it is $m 692 which shows

that it has been reduced. In the financial year 2017 deferred tax expenses was $m (7) but in the

year 2018 it is $m (29) which shows that it has been increased.

3

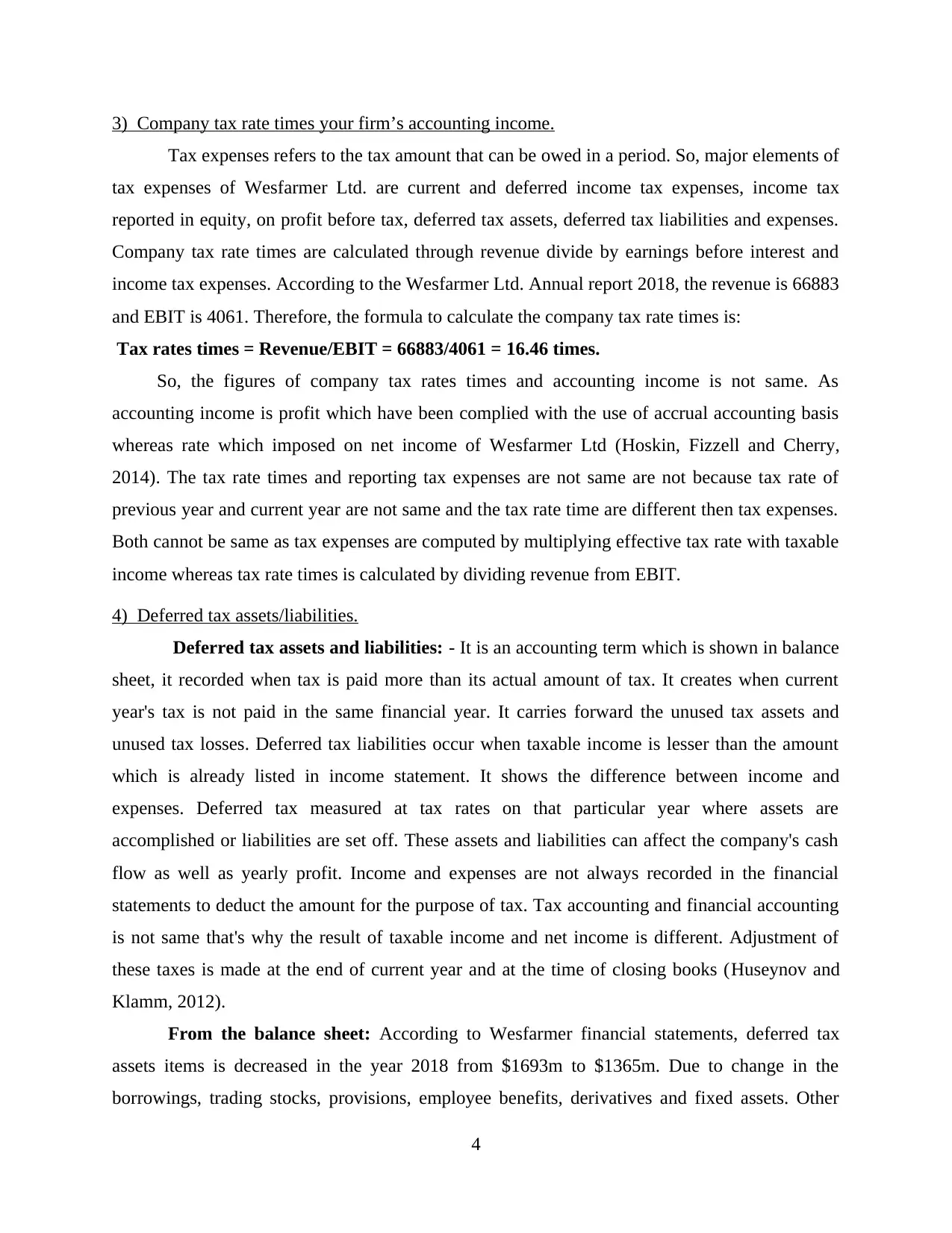

3) Company tax rate times your firm’s accounting income.

Tax expenses refers to the tax amount that can be owed in a period. So, major elements of

tax expenses of Wesfarmer Ltd. are current and deferred income tax expenses, income tax

reported in equity, on profit before tax, deferred tax assets, deferred tax liabilities and expenses.

Company tax rate times are calculated through revenue divide by earnings before interest and

income tax expenses. According to the Wesfarmer Ltd. Annual report 2018, the revenue is 66883

and EBIT is 4061. Therefore, the formula to calculate the company tax rate times is:

Tax rates times = Revenue/EBIT = 66883/4061 = 16.46 times.

So, the figures of company tax rates times and accounting income is not same. As

accounting income is profit which have been complied with the use of accrual accounting basis

whereas rate which imposed on net income of Wesfarmer Ltd (Hoskin, Fizzell and Cherry,

2014). The tax rate times and reporting tax expenses are not same are not because tax rate of

previous year and current year are not same and the tax rate time are different then tax expenses.

Both cannot be same as tax expenses are computed by multiplying effective tax rate with taxable

income whereas tax rate times is calculated by dividing revenue from EBIT.

4) Deferred tax assets/liabilities.

Deferred tax assets and liabilities: - It is an accounting term which is shown in balance

sheet, it recorded when tax is paid more than its actual amount of tax. It creates when current

year's tax is not paid in the same financial year. It carries forward the unused tax assets and

unused tax losses. Deferred tax liabilities occur when taxable income is lesser than the amount

which is already listed in income statement. It shows the difference between income and

expenses. Deferred tax measured at tax rates on that particular year where assets are

accomplished or liabilities are set off. These assets and liabilities can affect the company's cash

flow as well as yearly profit. Income and expenses are not always recorded in the financial

statements to deduct the amount for the purpose of tax. Tax accounting and financial accounting

is not same that's why the result of taxable income and net income is different. Adjustment of

these taxes is made at the end of current year and at the time of closing books (Huseynov and

Klamm, 2012).

From the balance sheet: According to Wesfarmer financial statements, deferred tax

assets items is decreased in the year 2018 from $1693m to $1365m. Due to change in the

borrowings, trading stocks, provisions, employee benefits, derivatives and fixed assets. Other

4

Tax expenses refers to the tax amount that can be owed in a period. So, major elements of

tax expenses of Wesfarmer Ltd. are current and deferred income tax expenses, income tax

reported in equity, on profit before tax, deferred tax assets, deferred tax liabilities and expenses.

Company tax rate times are calculated through revenue divide by earnings before interest and

income tax expenses. According to the Wesfarmer Ltd. Annual report 2018, the revenue is 66883

and EBIT is 4061. Therefore, the formula to calculate the company tax rate times is:

Tax rates times = Revenue/EBIT = 66883/4061 = 16.46 times.

So, the figures of company tax rates times and accounting income is not same. As

accounting income is profit which have been complied with the use of accrual accounting basis

whereas rate which imposed on net income of Wesfarmer Ltd (Hoskin, Fizzell and Cherry,

2014). The tax rate times and reporting tax expenses are not same are not because tax rate of

previous year and current year are not same and the tax rate time are different then tax expenses.

Both cannot be same as tax expenses are computed by multiplying effective tax rate with taxable

income whereas tax rate times is calculated by dividing revenue from EBIT.

4) Deferred tax assets/liabilities.

Deferred tax assets and liabilities: - It is an accounting term which is shown in balance

sheet, it recorded when tax is paid more than its actual amount of tax. It creates when current

year's tax is not paid in the same financial year. It carries forward the unused tax assets and

unused tax losses. Deferred tax liabilities occur when taxable income is lesser than the amount

which is already listed in income statement. It shows the difference between income and

expenses. Deferred tax measured at tax rates on that particular year where assets are

accomplished or liabilities are set off. These assets and liabilities can affect the company's cash

flow as well as yearly profit. Income and expenses are not always recorded in the financial

statements to deduct the amount for the purpose of tax. Tax accounting and financial accounting

is not same that's why the result of taxable income and net income is different. Adjustment of

these taxes is made at the end of current year and at the time of closing books (Huseynov and

Klamm, 2012).

From the balance sheet: According to Wesfarmer financial statements, deferred tax

assets items is decreased in the year 2018 from $1693m to $1365m. Due to change in the

borrowings, trading stocks, provisions, employee benefits, derivatives and fixed assets. Other

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

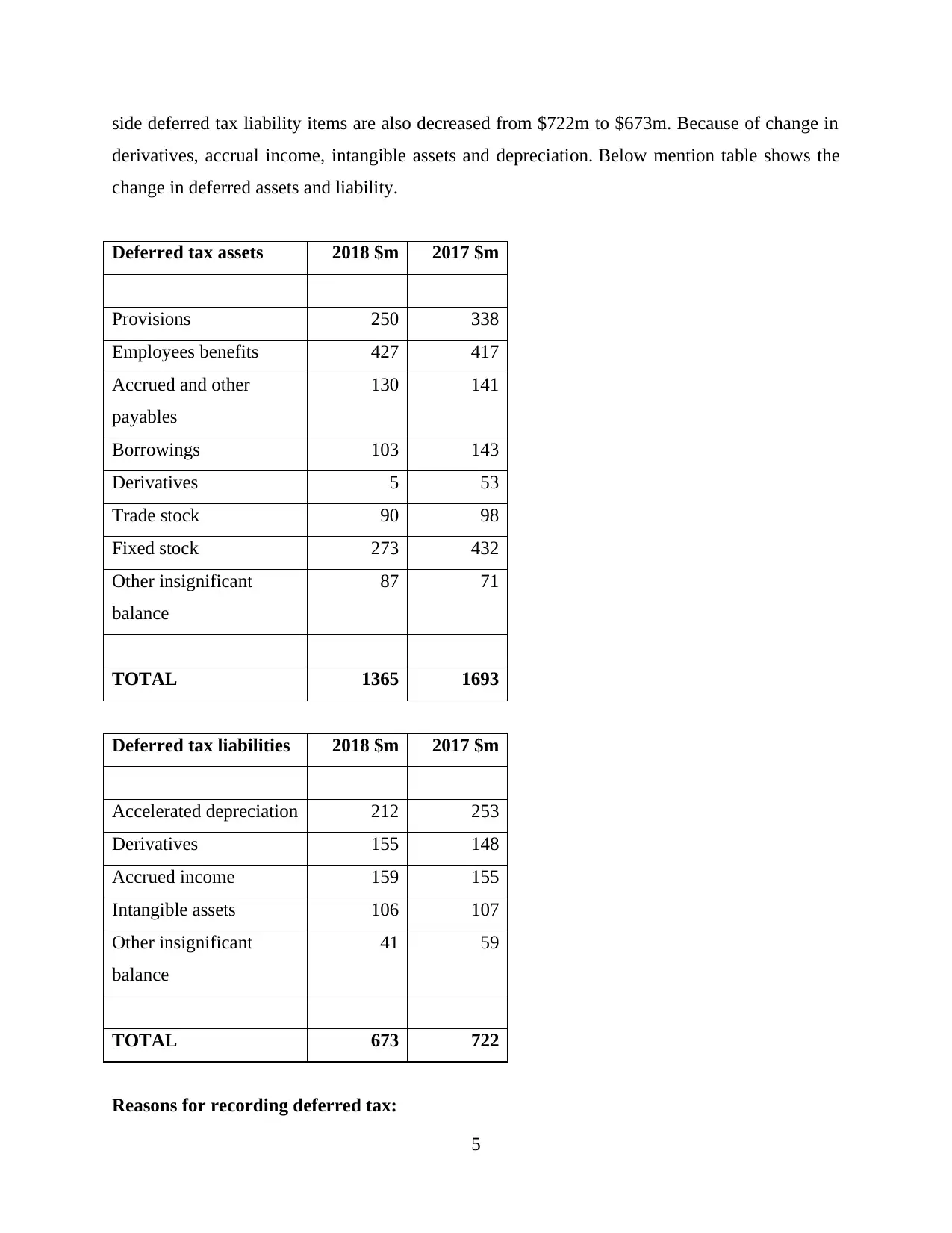

side deferred tax liability items are also decreased from $722m to $673m. Because of change in

derivatives, accrual income, intangible assets and depreciation. Below mention table shows the

change in deferred assets and liability.

Deferred tax assets 2018 $m 2017 $m

Provisions 250 338

Employees benefits 427 417

Accrued and other

payables

130 141

Borrowings 103 143

Derivatives 5 53

Trade stock 90 98

Fixed stock 273 432

Other insignificant

balance

87 71

TOTAL 1365 1693

Deferred tax liabilities 2018 $m 2017 $m

Accelerated depreciation 212 253

Derivatives 155 148

Accrued income 159 155

Intangible assets 106 107

Other insignificant

balance

41 59

TOTAL 673 722

Reasons for recording deferred tax:

5

derivatives, accrual income, intangible assets and depreciation. Below mention table shows the

change in deferred assets and liability.

Deferred tax assets 2018 $m 2017 $m

Provisions 250 338

Employees benefits 427 417

Accrued and other

payables

130 141

Borrowings 103 143

Derivatives 5 53

Trade stock 90 98

Fixed stock 273 432

Other insignificant

balance

87 71

TOTAL 1365 1693

Deferred tax liabilities 2018 $m 2017 $m

Accelerated depreciation 212 253

Derivatives 155 148

Accrued income 159 155

Intangible assets 106 107

Other insignificant

balance

41 59

TOTAL 673 722

Reasons for recording deferred tax:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Deferred tax recorded due to the timing difference between book profit and taxable profit.

Some items are allowed and disallowed to apply for tax purpose. These differences called timing

difference and it is classified into two parts. First one is temporary and another one is permanent.

Temporary includes the difference between book income and taxable income which is

compensate in next year. Permanent includes those difference which in not able to compensate in

next consequent year. It will generate temporary difference in the company's accounts and create

deferred tax liability. If book profit is higher than taxable profit so company can pay less tax in

current year and pay higher tax in future. Because of that difference, accountant have to create

deferred tax liability account. On the other hand, if book profit is less than taxable profit so

company pay high tax in current year and in future, they pay low tax (Schaltegger, Burritt and

Petersen, 2017). Due to this reason organisation have to create deferred tax assets account.

Timing difference also includes carry forward losses and un-reflected depreciation.

Another reason to create deferred tax liability is that, when an organisation sale it's

product on credit bases. In that case amount is received in the future but due to the accounting

rules, company acknowledge as full income. But according to tax laws, it recognizes full income

when instalment is fully made. It will generate temporary difference in the Wesfarmer company's

accounts and create deferred tax liability.

5) Current tax assets or income tax payable recorded by company.

Current tax assets are measured at that amount which is expected to be recovered from

authorities of taxation at tax laws and rates are enacted by balance sheet date. Yes, income tax

payable is recorded in 2018 annual report of Wesfarmer Ltd. Income tax payable is recorded in

balance sheet of company under current liabilities. Income tax expenses refers to an income

statement accounts which firm utilise to record state and federal costs of income tax. Income tax

payable is considered as a liability account which is shown in balance sheet and Wesfarmer Ltd.

Utilise it to record amount of income tax which is owe by company owe but but still not paid to

suitable taxing authority. According to the 2018 annual report of Wesfarmer Ltd. Income tax

payable is 299 and income tax expenses is (1246) and this is the amount which is not paid really

considered as an expected amount (Schaltegger, Etxeberria and Ortas, 2017).

Company need to give a full disclosure about this both the amount of tax expenses and

tax payable are not same because tax expenses is that amount which company expect to pay

whereas tax payable are real amount that is decided by government. This is shown in the income

6

Some items are allowed and disallowed to apply for tax purpose. These differences called timing

difference and it is classified into two parts. First one is temporary and another one is permanent.

Temporary includes the difference between book income and taxable income which is

compensate in next year. Permanent includes those difference which in not able to compensate in

next consequent year. It will generate temporary difference in the company's accounts and create

deferred tax liability. If book profit is higher than taxable profit so company can pay less tax in

current year and pay higher tax in future. Because of that difference, accountant have to create

deferred tax liability account. On the other hand, if book profit is less than taxable profit so

company pay high tax in current year and in future, they pay low tax (Schaltegger, Burritt and

Petersen, 2017). Due to this reason organisation have to create deferred tax assets account.

Timing difference also includes carry forward losses and un-reflected depreciation.

Another reason to create deferred tax liability is that, when an organisation sale it's

product on credit bases. In that case amount is received in the future but due to the accounting

rules, company acknowledge as full income. But according to tax laws, it recognizes full income

when instalment is fully made. It will generate temporary difference in the Wesfarmer company's

accounts and create deferred tax liability.

5) Current tax assets or income tax payable recorded by company.

Current tax assets are measured at that amount which is expected to be recovered from

authorities of taxation at tax laws and rates are enacted by balance sheet date. Yes, income tax

payable is recorded in 2018 annual report of Wesfarmer Ltd. Income tax payable is recorded in

balance sheet of company under current liabilities. Income tax expenses refers to an income

statement accounts which firm utilise to record state and federal costs of income tax. Income tax

payable is considered as a liability account which is shown in balance sheet and Wesfarmer Ltd.

Utilise it to record amount of income tax which is owe by company owe but but still not paid to

suitable taxing authority. According to the 2018 annual report of Wesfarmer Ltd. Income tax

payable is 299 and income tax expenses is (1246) and this is the amount which is not paid really

considered as an expected amount (Schaltegger, Etxeberria and Ortas, 2017).

Company need to give a full disclosure about this both the amount of tax expenses and

tax payable are not same because tax expenses is that amount which company expect to pay

whereas tax payable are real amount that is decided by government. This is shown in the income

6

statement and tax payable is recorded under liability account in balance sheet. It is use to record

that amount of income tax which is owe but as yet not paid to the authority of tax.

6) Income statement same as the income tax paid shown in the cash flow statement.

Income statement that is used for reporting financial performance of company upon a

particular accounting periods. It is essential for every company to prepare this statement as it

shows the profitability of firm. Cash flow statement shows the changes occurred in balance sheet

accounts and also effects of cash and cash equivalents. Income tax is which government imposed

on income produced by people or businesses with their legal power. In Wesfarmer Ltd. income

statement of 2018, the income tax expenses are (1246) and in cash flow statement, income tax

paid is 1308. Income tax is included in both the statements that is income statement as well as

cash flow statements. Income tax amount is not same in both the statements because in income

statement, expenses of income tax is included. In this those amount is mentioned which is not

actually been paid. It is an estimated amount which have been formed to cover what firm require

to pay. But in cash flow statement paid income tax is considered which is the actual or real

amount that Wesfarmer Ltd. owes in taxes. Whether it is of any periods previous or present. In

income statement only the current periods amount is included that's why their amount is different

is both the statements (Raiborn and Sivitanides, 2015).

7) Interpretation

After observing the financial statements of Wesfarmer Ltd, it is clearly stated that the

income to the company increases at a faster rate, this can be seen through the difference between

year 2017 and 2018 of the income tax reportable. Also, it can be verified by income tax payable

on the profit before tax by the company in these two year which is $ 1169m and $ 1246m

respectively. This is interesting to see that there is decrement in deferred tax assets, this shows

that either company received the refund of excess amount paid in previous year or it may set off

through deferred tax liabilities. This is very surprising to see that there is a vast decreasing in

borrowings of company, derivatives in one year period. This is also surprising that how fixed

assets are decreasing suddenly, which is $ 432m in year 2017 and $ 272m in year 2018. there

should be need to evaluate certain area to make company more profitable such as fixed assets,

deferred assets and deferred expenses and others important area. There is necessary to evaluate

those amount that is mentioned and which is not actually been paid. It is an estimated amount

which have been formed to cover what firm require to pay.

7

that amount of income tax which is owe but as yet not paid to the authority of tax.

6) Income statement same as the income tax paid shown in the cash flow statement.

Income statement that is used for reporting financial performance of company upon a

particular accounting periods. It is essential for every company to prepare this statement as it

shows the profitability of firm. Cash flow statement shows the changes occurred in balance sheet

accounts and also effects of cash and cash equivalents. Income tax is which government imposed

on income produced by people or businesses with their legal power. In Wesfarmer Ltd. income

statement of 2018, the income tax expenses are (1246) and in cash flow statement, income tax

paid is 1308. Income tax is included in both the statements that is income statement as well as

cash flow statements. Income tax amount is not same in both the statements because in income

statement, expenses of income tax is included. In this those amount is mentioned which is not

actually been paid. It is an estimated amount which have been formed to cover what firm require

to pay. But in cash flow statement paid income tax is considered which is the actual or real

amount that Wesfarmer Ltd. owes in taxes. Whether it is of any periods previous or present. In

income statement only the current periods amount is included that's why their amount is different

is both the statements (Raiborn and Sivitanides, 2015).

7) Interpretation

After observing the financial statements of Wesfarmer Ltd, it is clearly stated that the

income to the company increases at a faster rate, this can be seen through the difference between

year 2017 and 2018 of the income tax reportable. Also, it can be verified by income tax payable

on the profit before tax by the company in these two year which is $ 1169m and $ 1246m

respectively. This is interesting to see that there is decrement in deferred tax assets, this shows

that either company received the refund of excess amount paid in previous year or it may set off

through deferred tax liabilities. This is very surprising to see that there is a vast decreasing in

borrowings of company, derivatives in one year period. This is also surprising that how fixed

assets are decreasing suddenly, which is $ 432m in year 2017 and $ 272m in year 2018. there

should be need to evaluate certain area to make company more profitable such as fixed assets,

deferred assets and deferred expenses and others important area. There is necessary to evaluate

those amount that is mentioned and which is not actually been paid. It is an estimated amount

which have been formed to cover what firm require to pay.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the above project report, it has been articulated that corporate accounting is used by

an organisation in order to analyse the financial strength of the company. Company Wesfarmers

are profitable and earn sufficient amount of profit during the time that help to maintain, capture

large market share at global level. After making proper analysis, it has been said that Wesfarmers

ltd is more reliable and efficient when it comes to managing tax obligations. Form the annual

different items have been interpreted that help to determine the actual current position of

respective company. Company is doing well in market and capture good market share that help

to attract large number of customer and external stakeholder.

8

From the above project report, it has been articulated that corporate accounting is used by

an organisation in order to analyse the financial strength of the company. Company Wesfarmers

are profitable and earn sufficient amount of profit during the time that help to maintain, capture

large market share at global level. After making proper analysis, it has been said that Wesfarmers

ltd is more reliable and efficient when it comes to managing tax obligations. Form the annual

different items have been interpreted that help to determine the actual current position of

respective company. Company is doing well in market and capture good market share that help

to attract large number of customer and external stakeholder.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journal:

DeBusk, G. K., 2012. Use lean accounting to add value to the organization. Journal of Corporate

Accounting & Finance. 23(3). pp.35-41.

Edgerton, J., 2012. Investment, accounting, and the salience of the corporate income tax (No.

w18472). National Bureau of Economic Research.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Hoskin, R. E., Fizzell, M. R. and Cherry, D. C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

Huseynov, F. and Klamm, B.K., 2012. Tax avoidance, tax management and corporate social

responsibility. Journal of Corporate Finance. 18(4). pp.804-827.

Raiborn, C. and Sivitanides, M., 2015. Accounting issues related to Bitcoins. Journal of

Corporate Accounting & Finance. 26(2). pp.25-34.

Rogoff, K. S., 2017. The Curse of Cash: How Large-Denomination Bills Aid Crime and Tax

Evasion and Constrain Monetary Policy. Princeton University Press.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Schaltegger, S., Etxeberria, I. Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development. 25(2).

pp.113-122.

Uyar, A., 2016. Evolution of corporate reporting and emerging trends. Journal of Corporate

Accounting & Finance. 27(4). pp.27-30.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of Accounting

Literature. 34. pp.1-16.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building corporate accountability: Emerging practice

in social and ethical accounting and auditing. Routledge.

Online

Annual reports of Wesfarmers. 2018. [Online] Avaliable Through:<

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-annual-

report.pdf?sfvrsn>.

9

Books and Journal:

DeBusk, G. K., 2012. Use lean accounting to add value to the organization. Journal of Corporate

Accounting & Finance. 23(3). pp.35-41.

Edgerton, J., 2012. Investment, accounting, and the salience of the corporate income tax (No.

w18472). National Bureau of Economic Research.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Hoskin, R. E., Fizzell, M. R. and Cherry, D. C., 2014. Financial Accounting: a user perspective.

Wiley Global Education.

Huseynov, F. and Klamm, B.K., 2012. Tax avoidance, tax management and corporate social

responsibility. Journal of Corporate Finance. 18(4). pp.804-827.

Raiborn, C. and Sivitanides, M., 2015. Accounting issues related to Bitcoins. Journal of

Corporate Accounting & Finance. 26(2). pp.25-34.

Rogoff, K. S., 2017. The Curse of Cash: How Large-Denomination Bills Aid Crime and Tax

Evasion and Constrain Monetary Policy. Princeton University Press.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Schaltegger, S., Etxeberria, I. Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development. 25(2).

pp.113-122.

Uyar, A., 2016. Evolution of corporate reporting and emerging trends. Journal of Corporate

Accounting & Finance. 27(4). pp.27-30.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of Accounting

Literature. 34. pp.1-16.

Zadek, S., Evans, R. and Pruzan, P., 2013. Building corporate accountability: Emerging practice

in social and ethical accounting and auditing. Routledge.

Online

Annual reports of Wesfarmers. 2018. [Online] Avaliable Through:<

https://www.wesfarmers.com.au/docs/default-source/asx-announcements/2018-annual-

report.pdf?sfvrsn>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.