Woolworths Limited: An In-depth Corporate Accounting and Tax Analysis

VerifiedAdded on 2024/04/25

|14

|2636

|239

Report

AI Summary

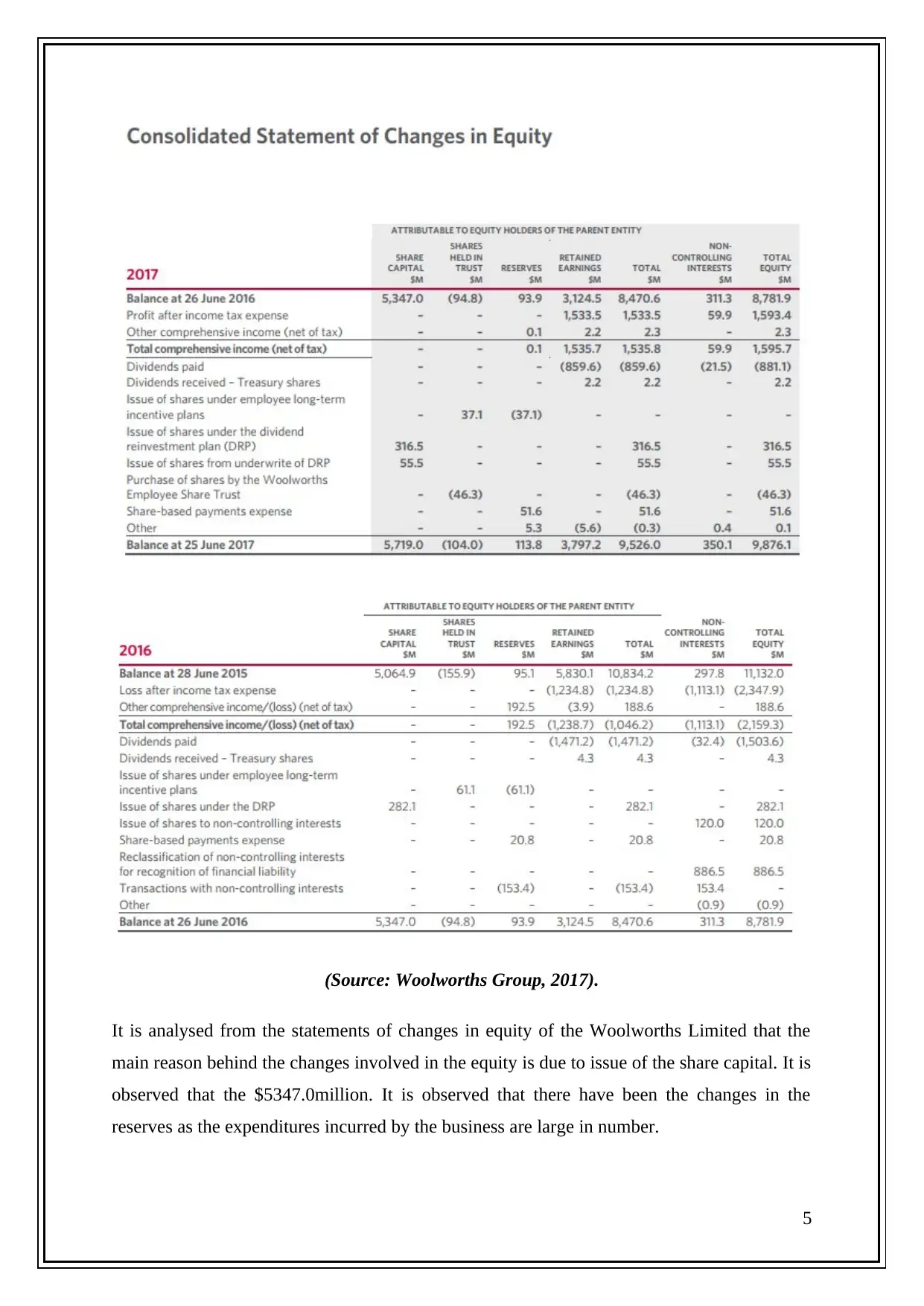

This report offers a detailed analysis of Woolworths Limited's corporate accounting practices, focusing on equity, tax expenses, and deferred tax assets and liabilities as reported in the company's 2017 annual report. It examines the components of equity, including contributed equity, reserves, retained earnings, and non-controlling interests, and explains the changes in these items over the past year. The report also investigates Woolworths' tax expenses, comparing the reported figures with the expected tax rate based on accounting income, and explores the reasons for any discrepancies. Furthermore, it discusses deferred tax assets and liabilities, providing insights into their potential impact on the company's future taxable income. The analysis extends to a comparison of income tax expenses reported in the income statement with the income tax paid as shown in the cash flow statement, highlighting the factors contributing to any differences. Finally, the report reflects on interesting, confusing, or surprising aspects of Woolworths' tax treatment, offering new insights into how companies account for income tax. Desklib provides access to similar solved assignments for students.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.