Corporate Accounting Assignment Solution: Questions 3-6 Analysis

VerifiedAdded on 2022/12/27

|7

|829

|22

Homework Assignment

AI Summary

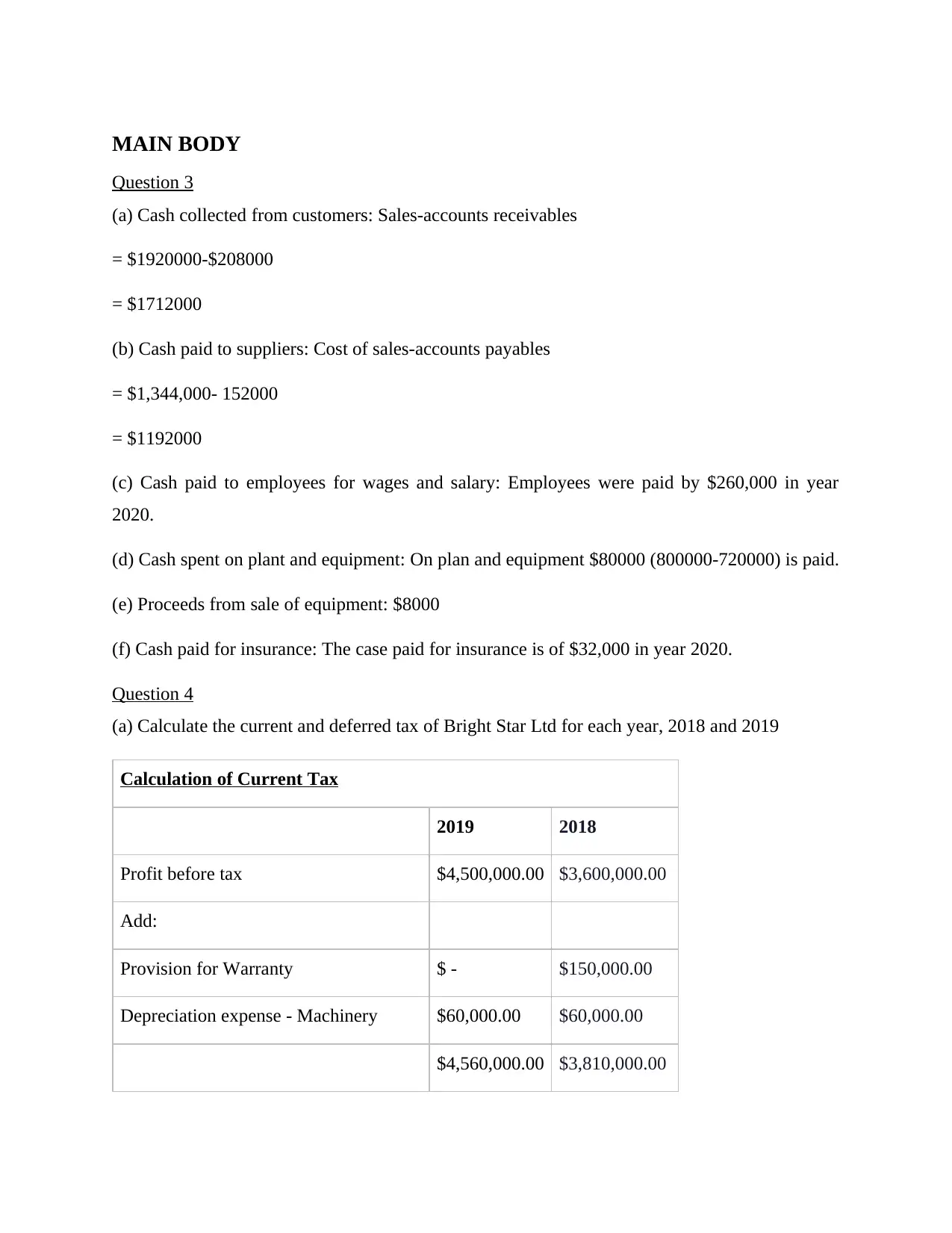

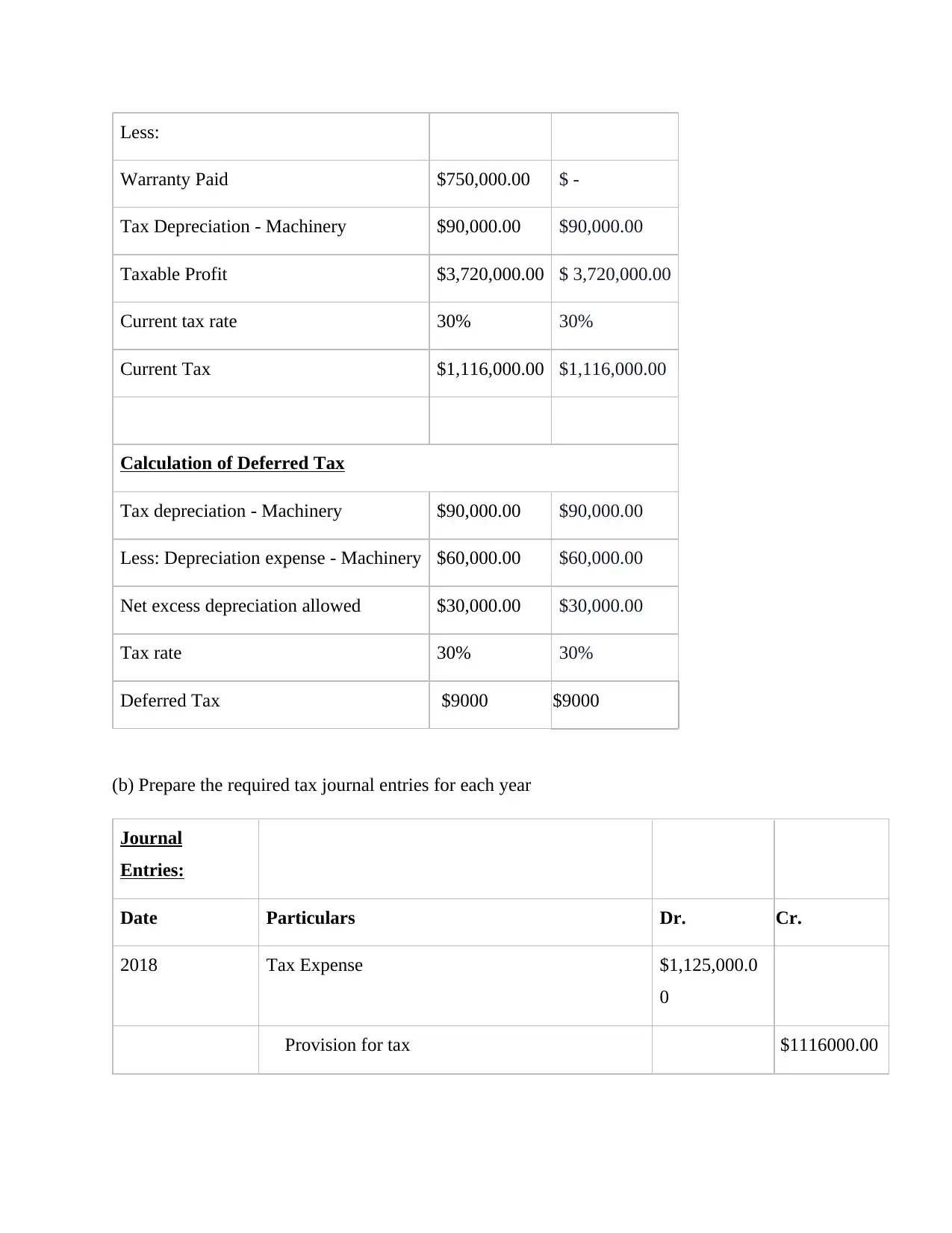

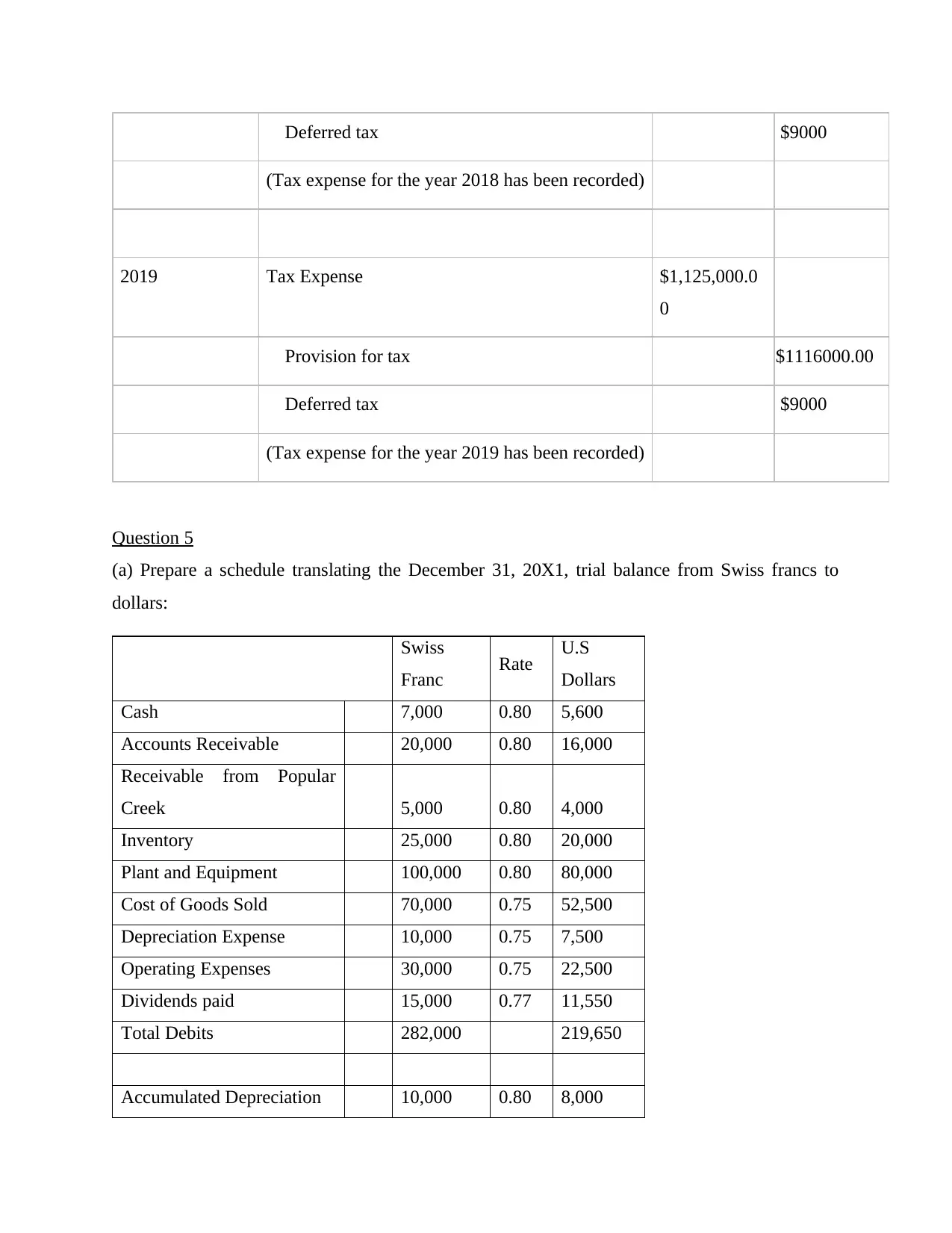

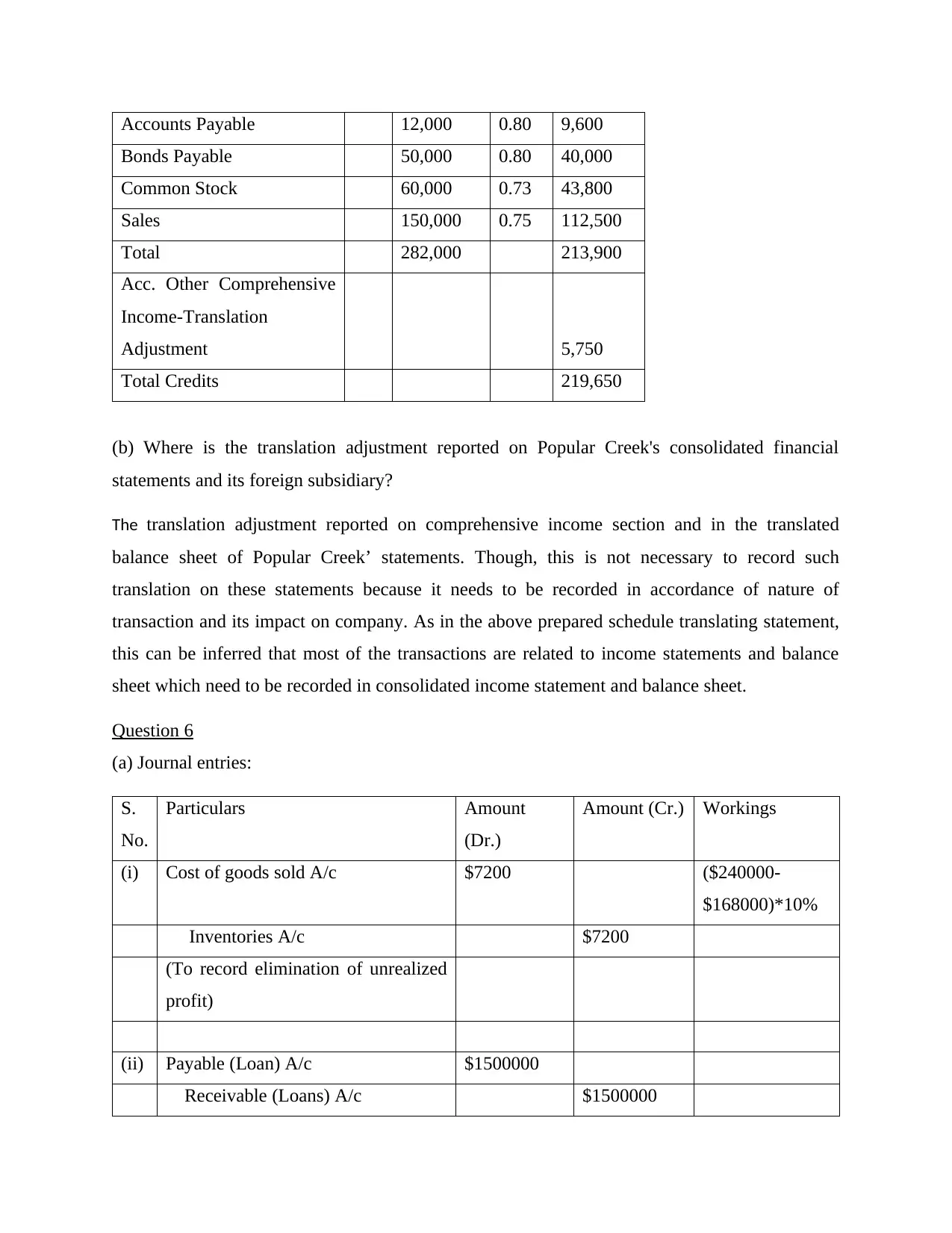

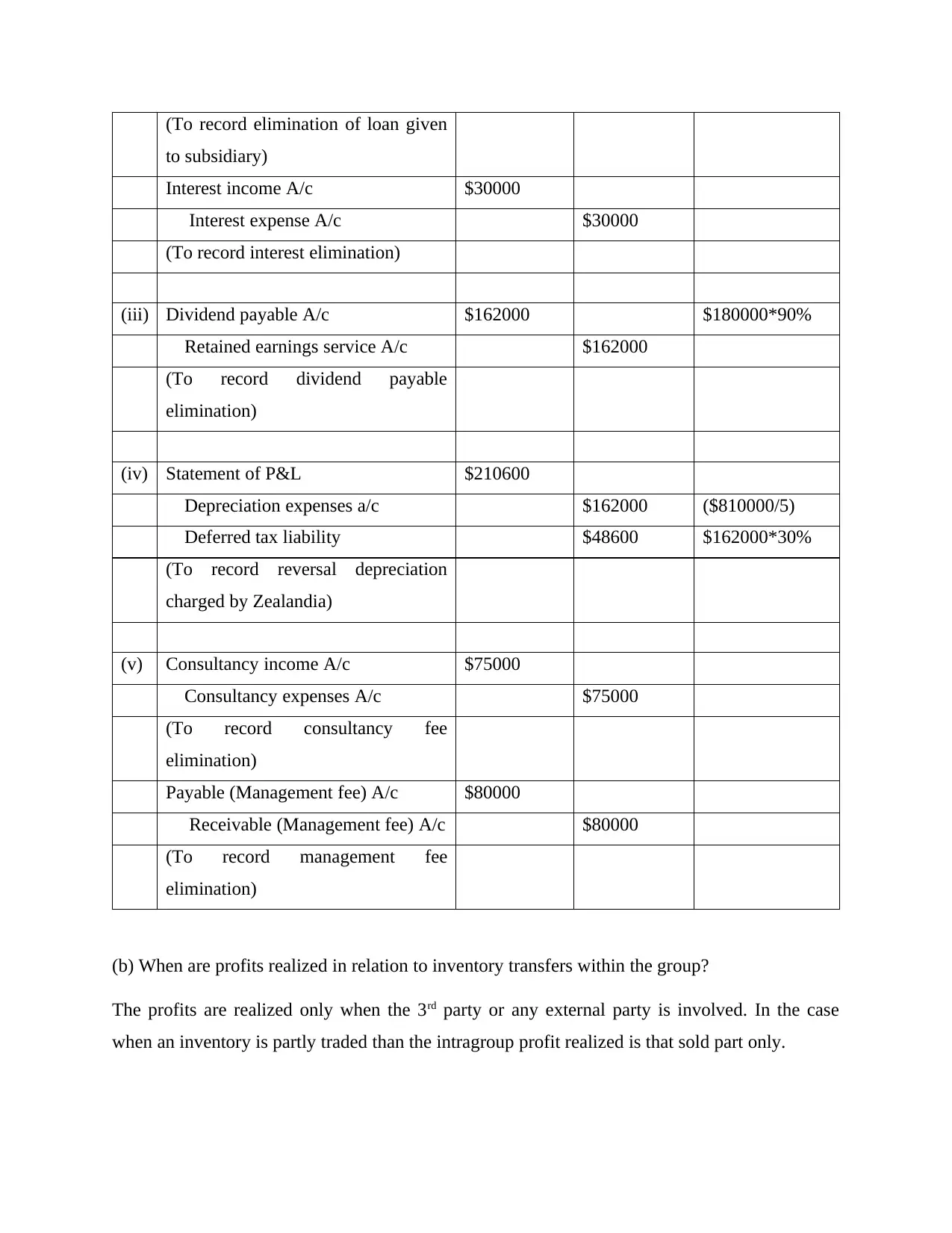

This document provides a comprehensive solution to a corporate accounting assignment, addressing key concepts and calculations. The solution includes detailed answers to questions 3 through 6, covering topics such as cash flow statements, deferred tax calculations and journal entries, foreign currency translation, and consolidation accounting. The assignment demonstrates the calculation of cash collected from customers and cash paid to suppliers, current and deferred tax calculations, and preparation of journal entries. It also includes a schedule for translating a trial balance from Swiss francs to dollars, and explains the reporting of translation adjustments in consolidated financial statements. Finally, the solution offers journal entries for eliminating intercompany transactions, including unrealized profits on inventory, intercompany loans, and dividends, as well as the reversal of depreciation expense and elimination of consultancy fees.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.