Corporate Accounting Assignment: Consolidation, NCI, and Liquidation

VerifiedAdded on 2022/09/27

|17

|1474

|30

Homework Assignment

AI Summary

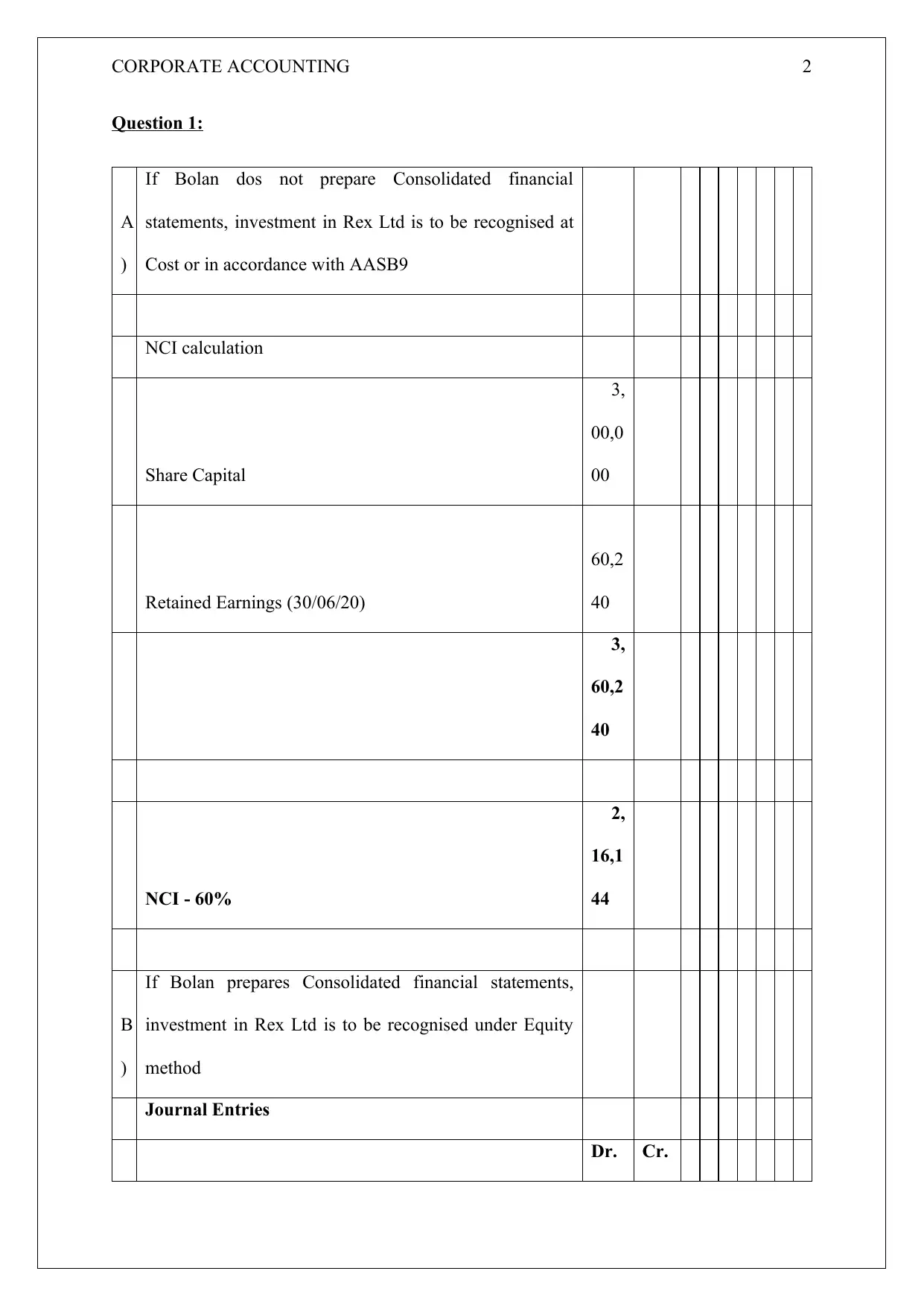

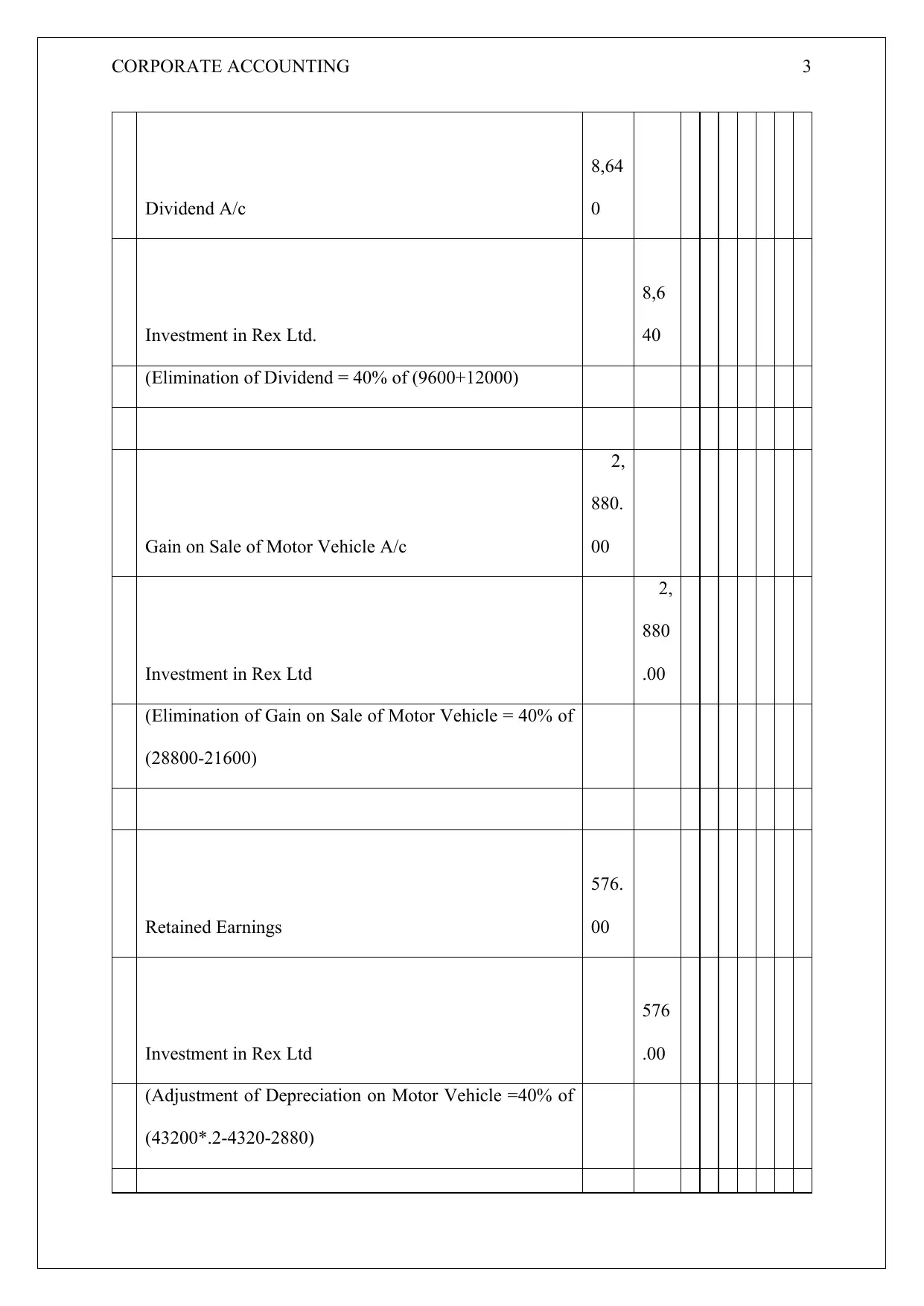

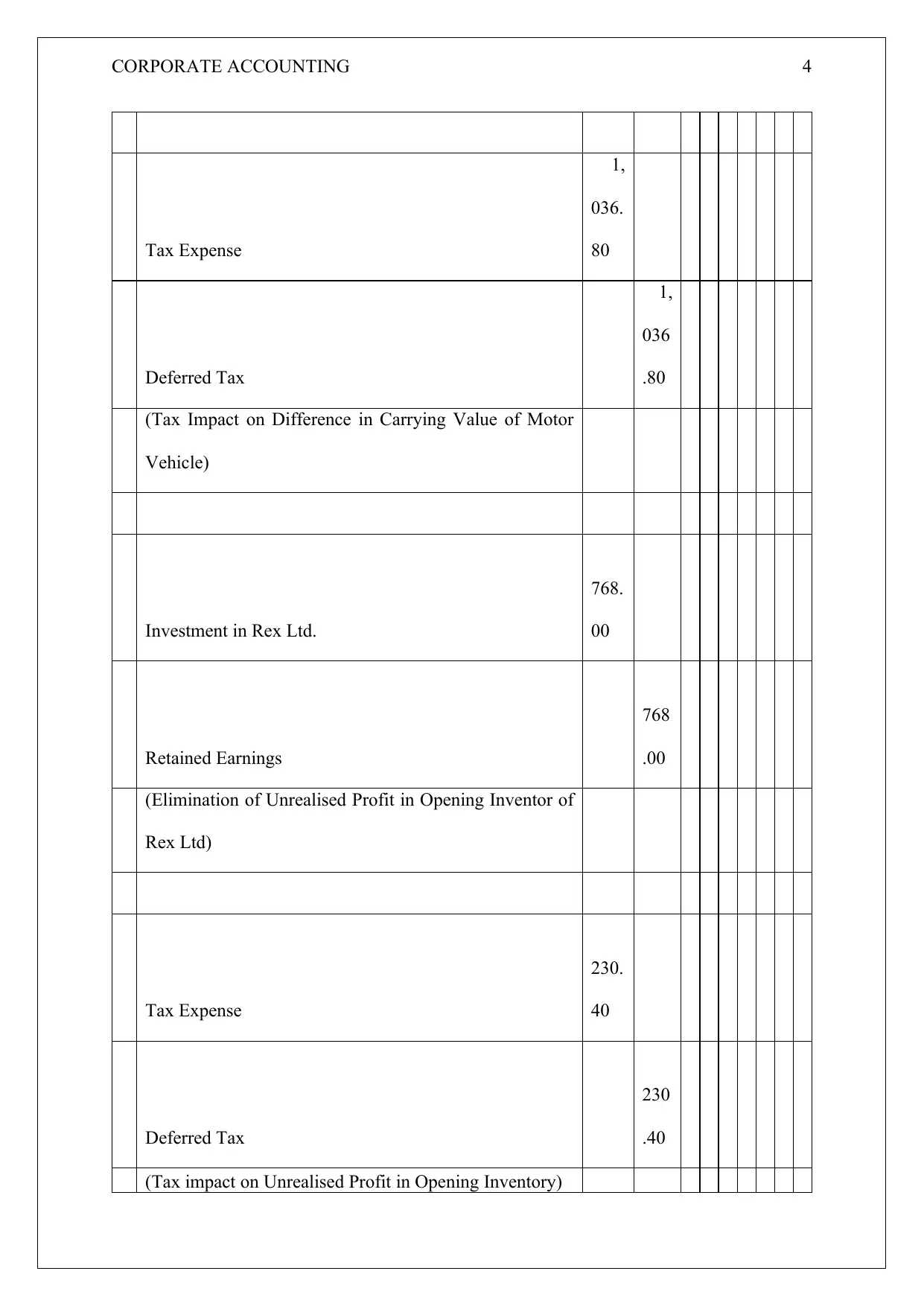

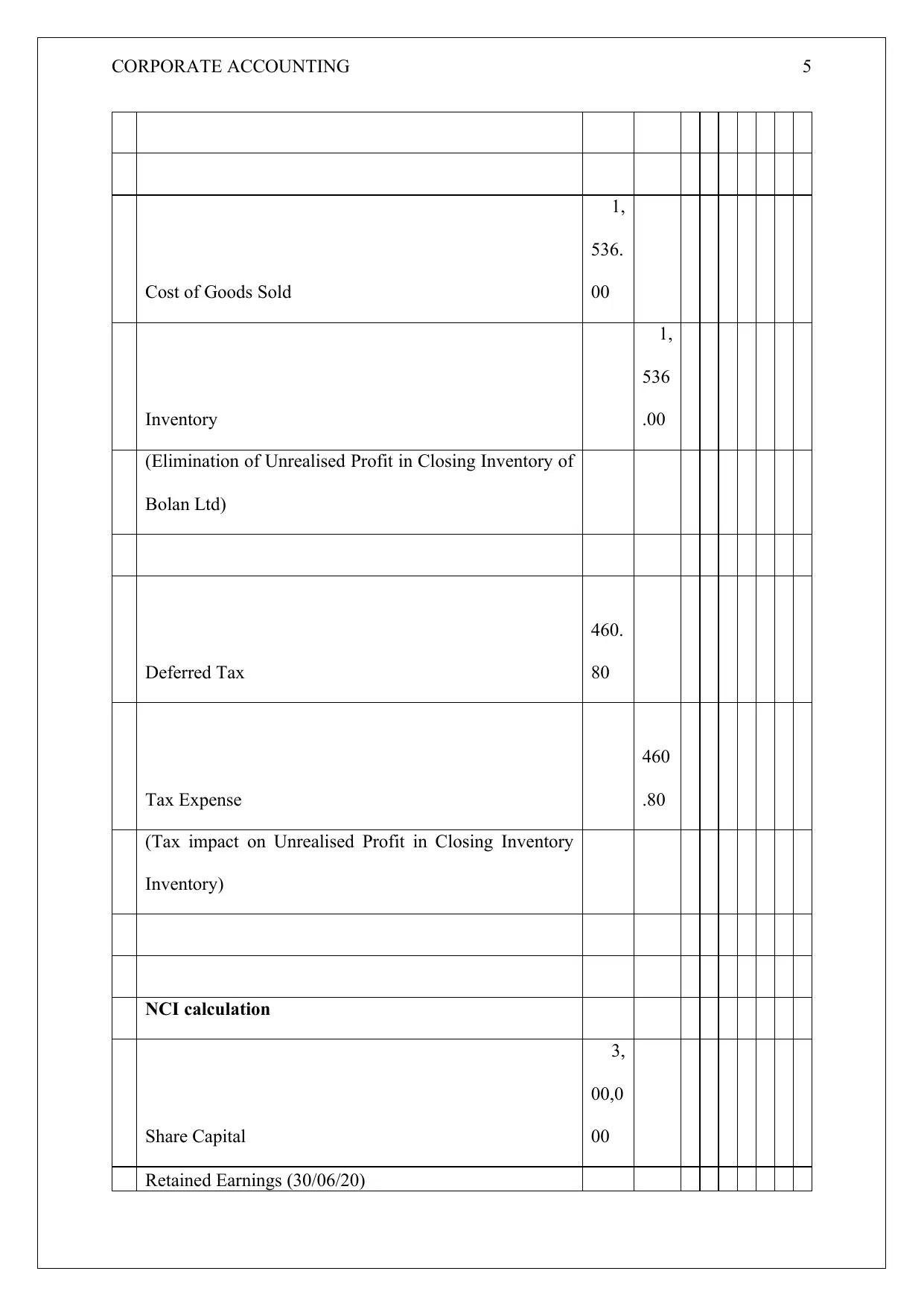

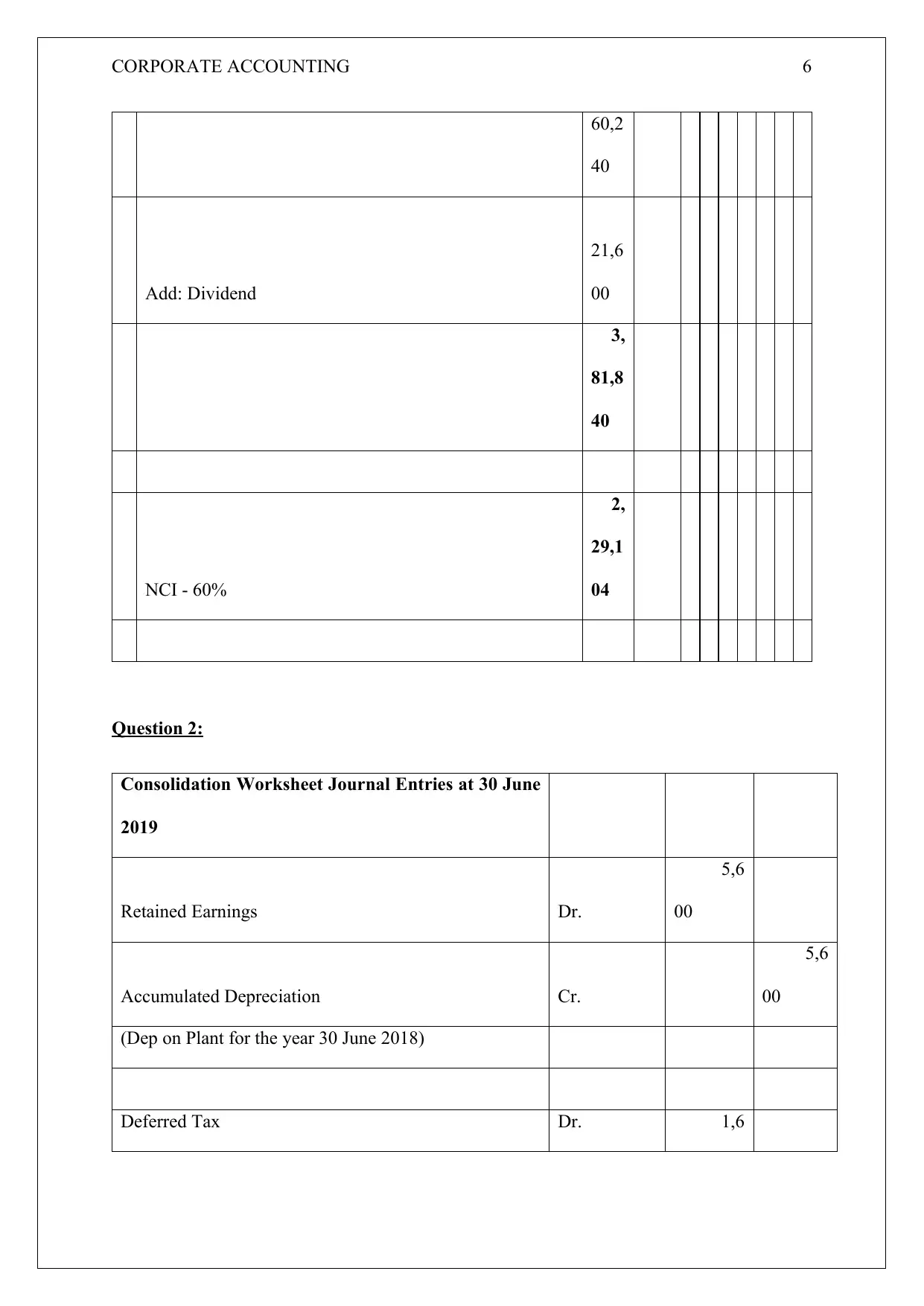

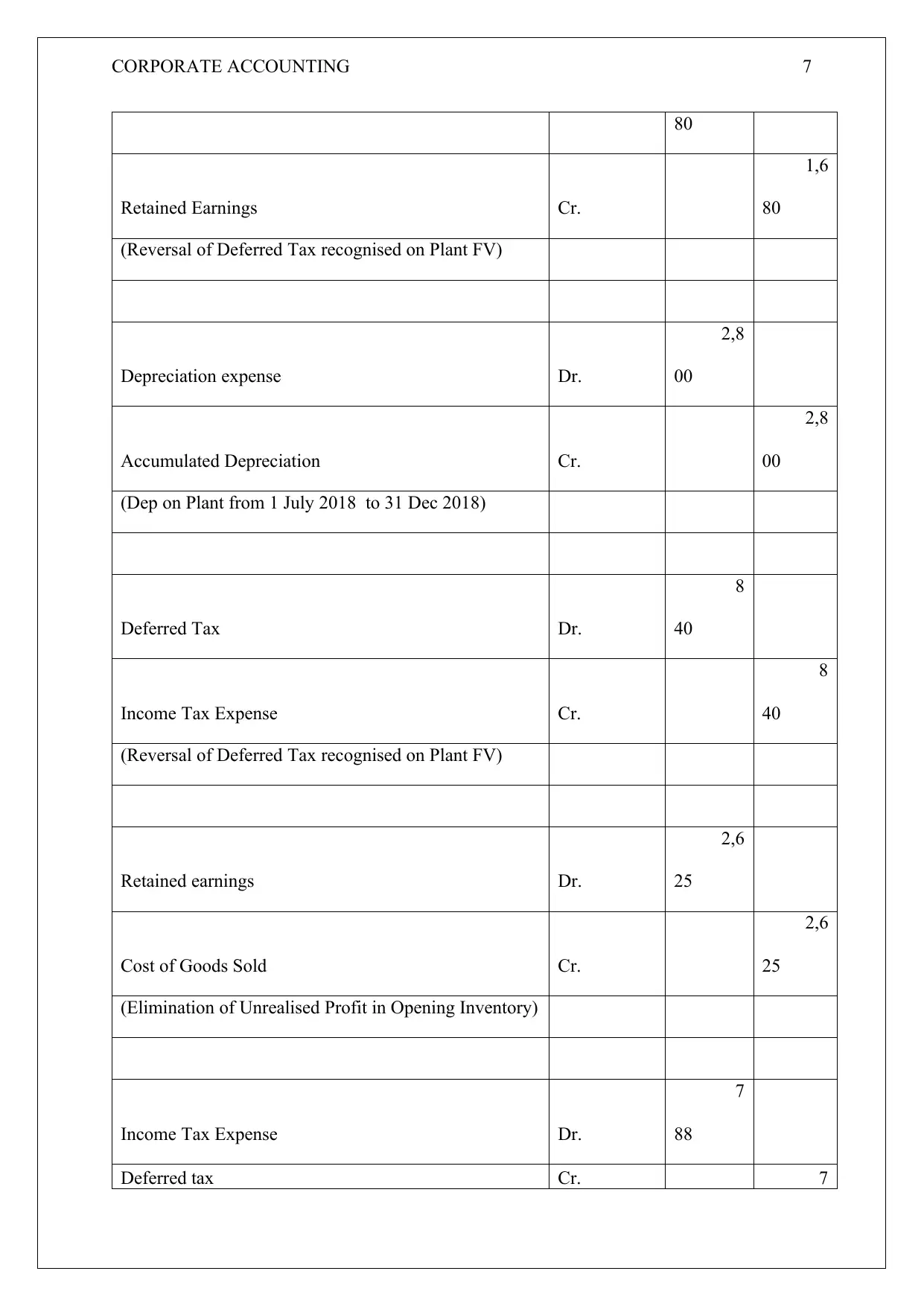

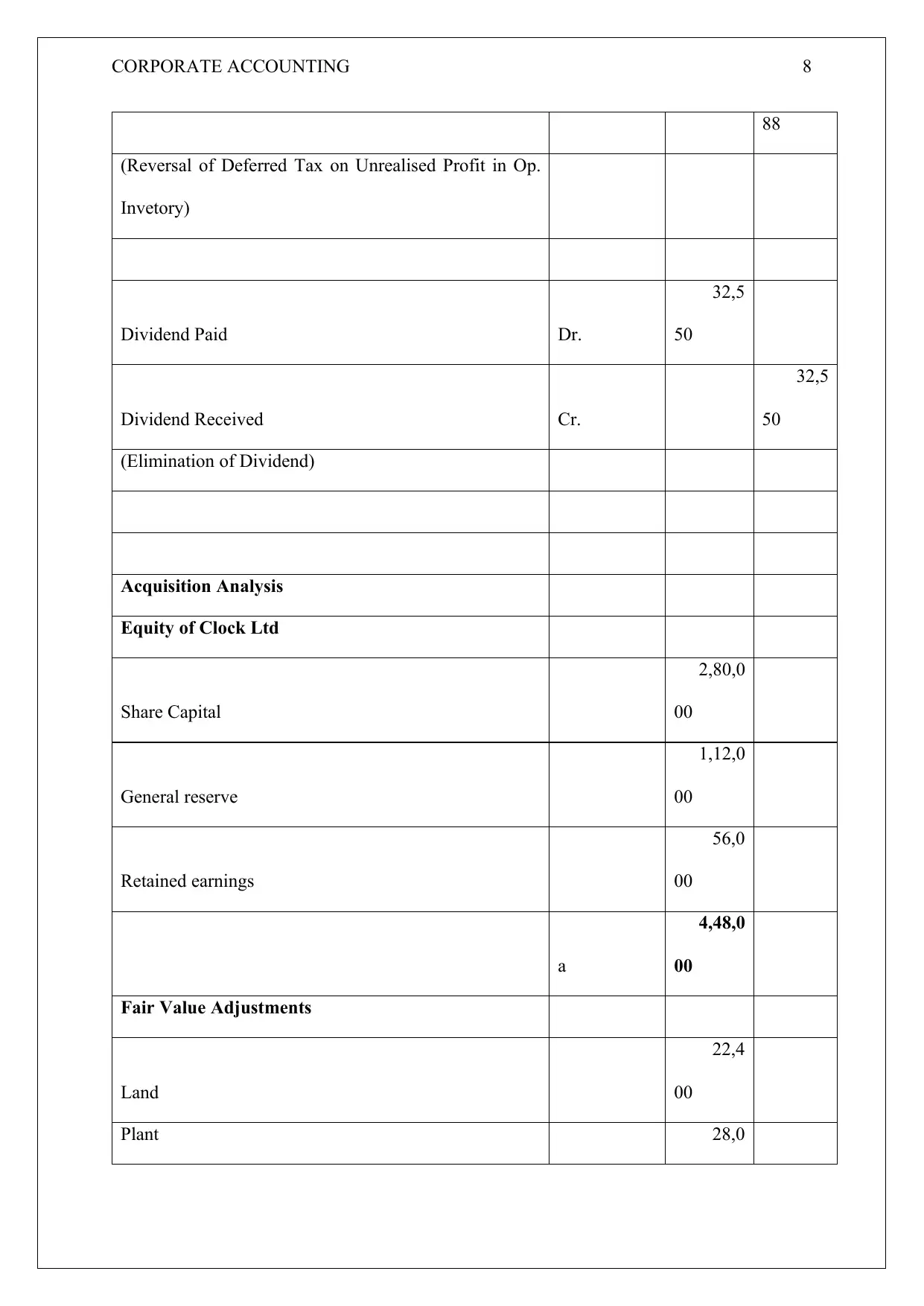

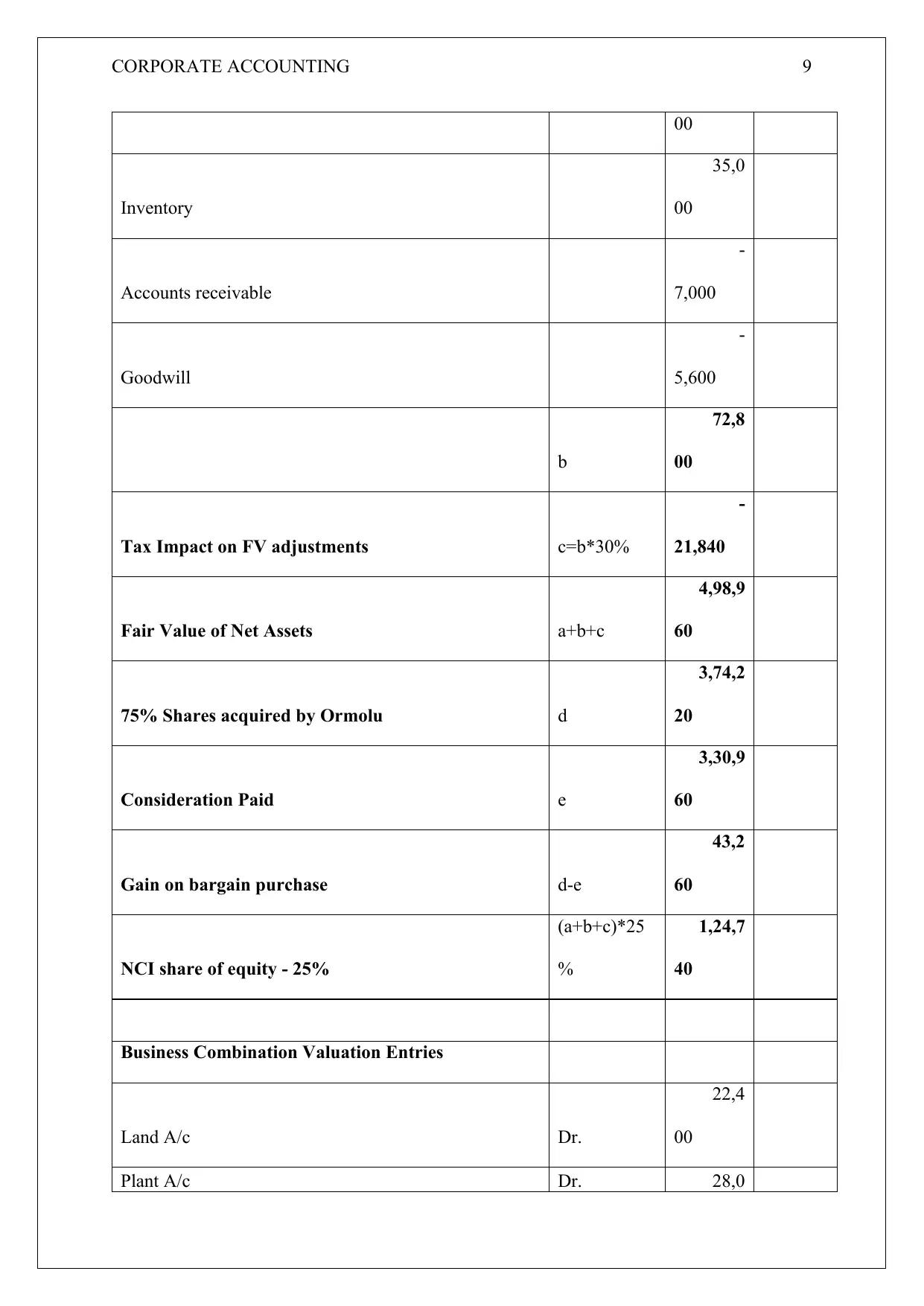

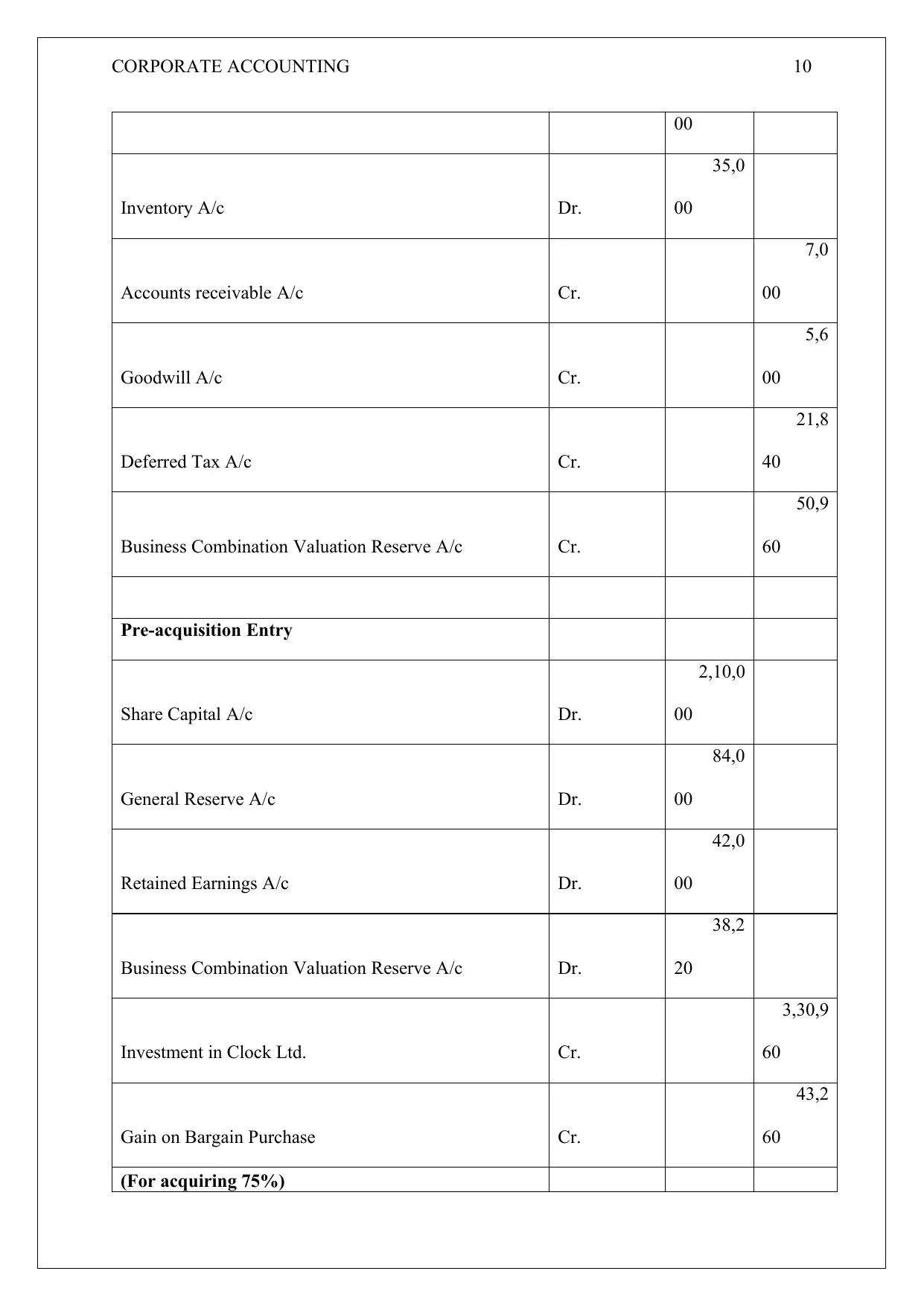

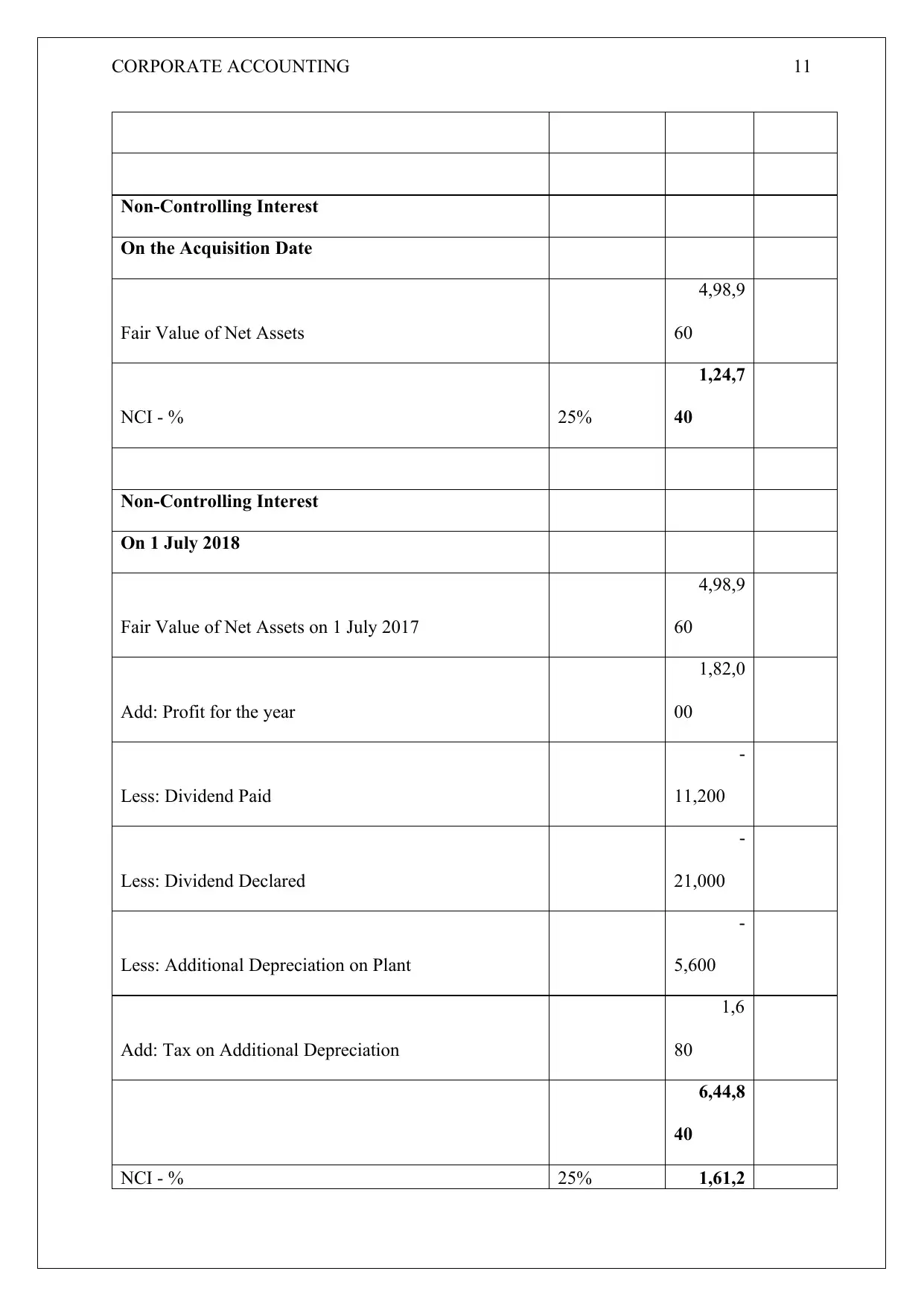

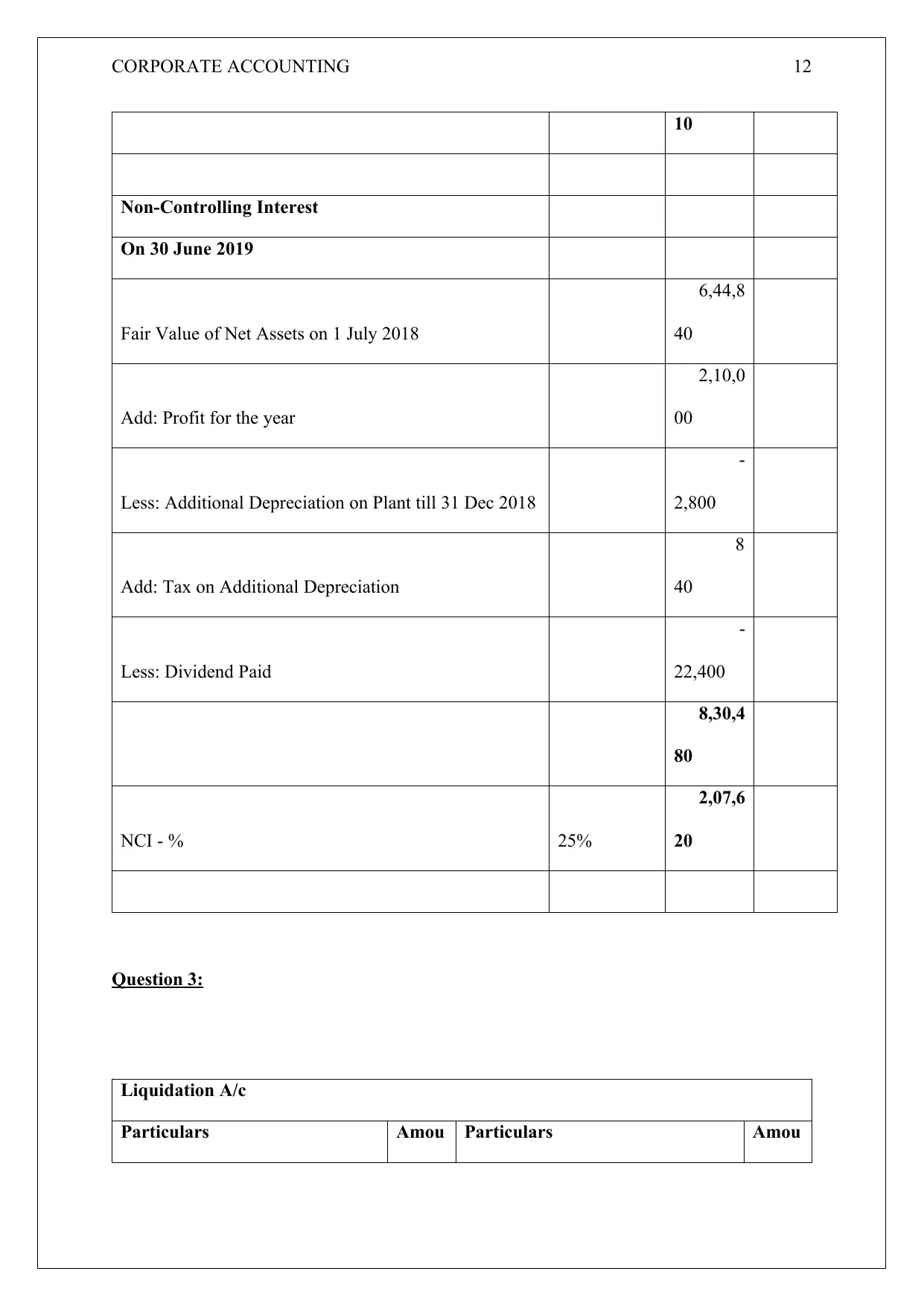

This document presents a comprehensive solution to a corporate accounting assignment, addressing key concepts such as consolidation, non-controlling interest (NCI), and liquidation. The assignment begins by exploring the accounting treatment of an investment in a subsidiary, comparing the cost method and the equity method. It then delves into the preparation of consolidated financial statements, including detailed journal entries for adjustments related to dividends, gain on sale of motor vehicles, depreciation, unrealized profits in inventory, and deferred tax implications. A consolidation worksheet is provided, along with acquisition analysis and the calculation of NCI at different points in time. The solution also covers a business combination valuation, including fair value adjustments, goodwill calculation, and the pre-acquisition entry. Furthermore, the assignment includes a liquidation scenario, presenting a liquidation account, a liquidator's statement of receipts and payments, and a shareholders' distribution account. Finally, the document provides a detailed explanation of non-controlling interest, its calculation, and its presentation in consolidated financial statements, referencing relevant accounting standards and resources.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.