Corporate Accounting Assignment - Finance Module: Alma vs Davis

VerifiedAdded on 2022/11/15

|6

|579

|261

Homework Assignment

AI Summary

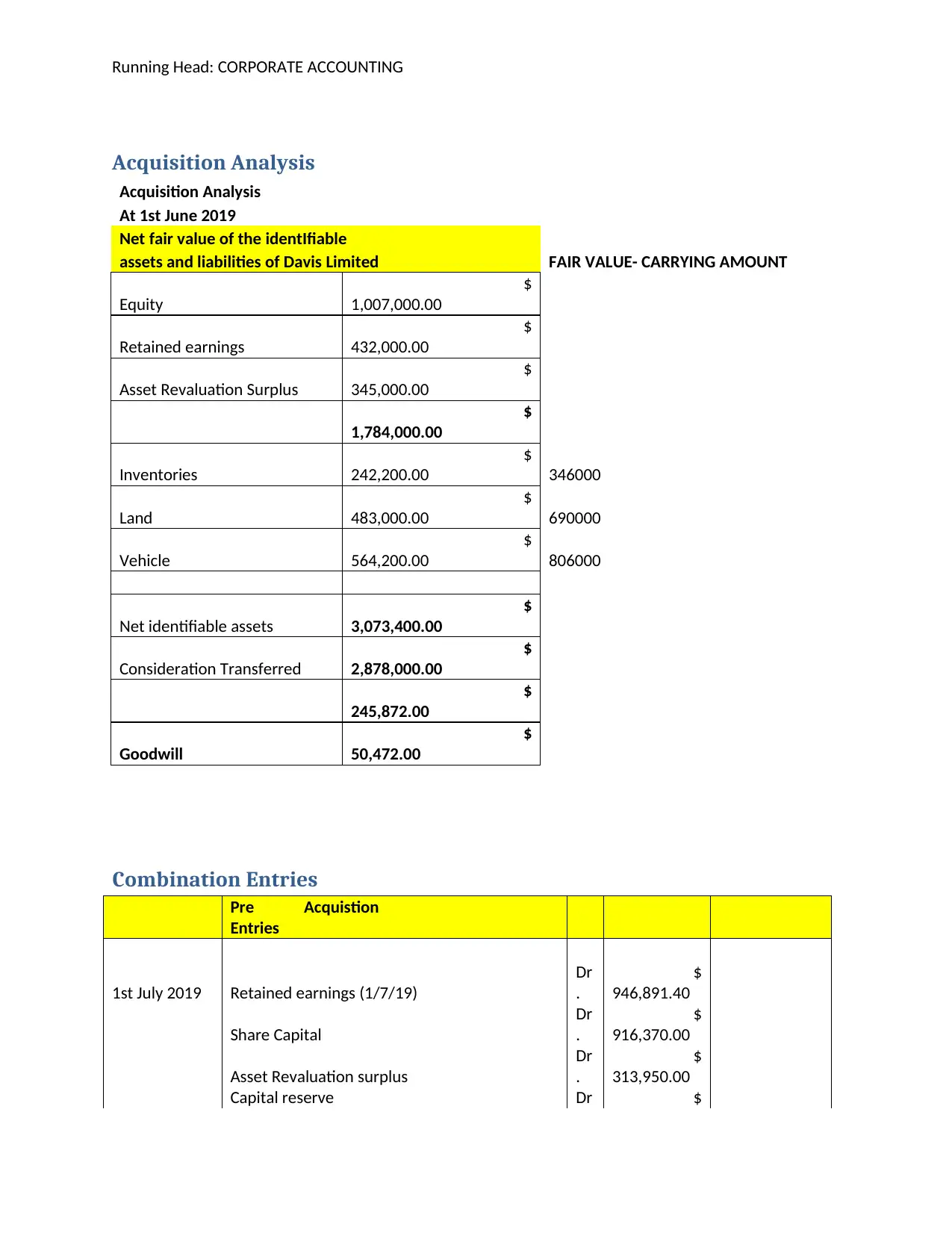

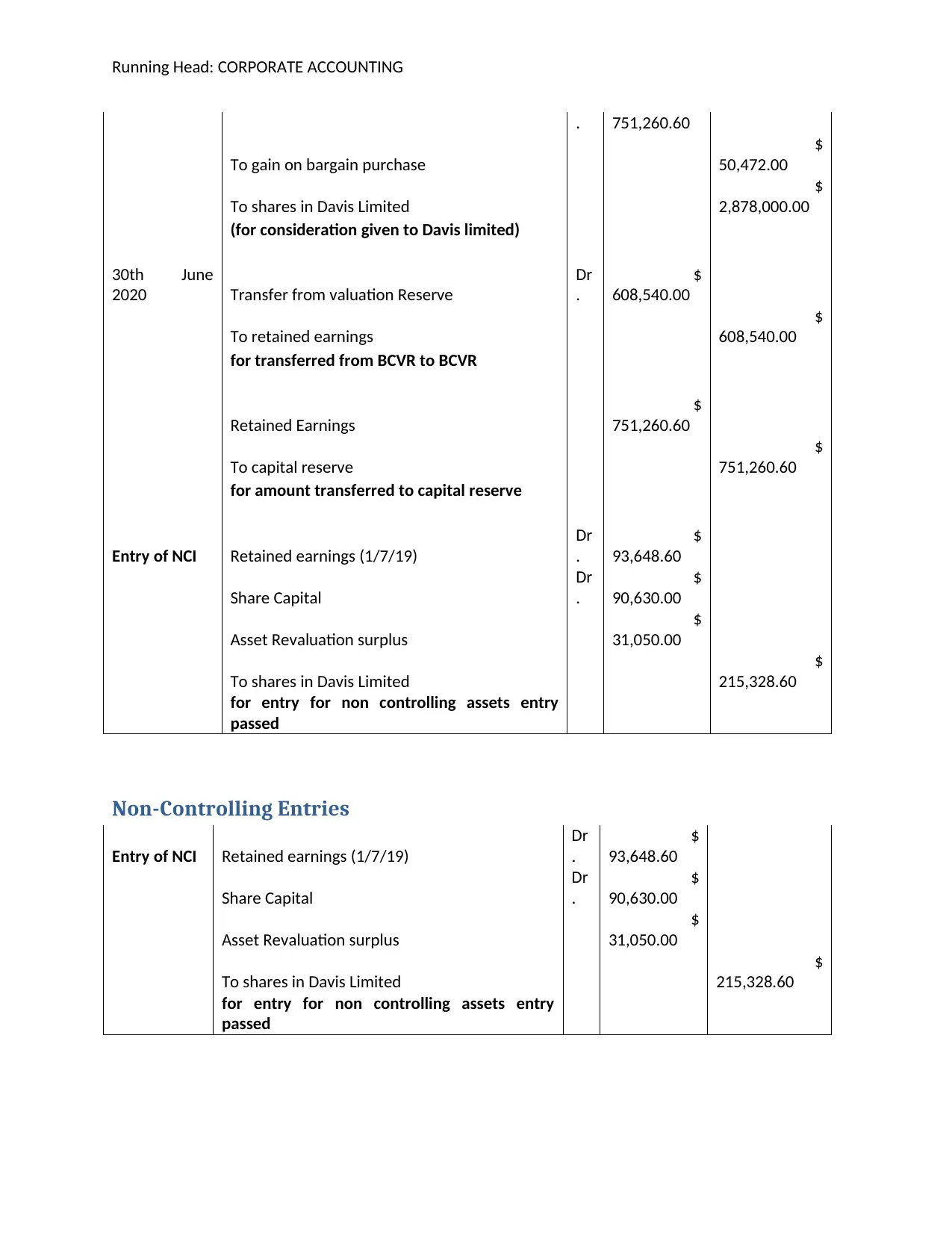

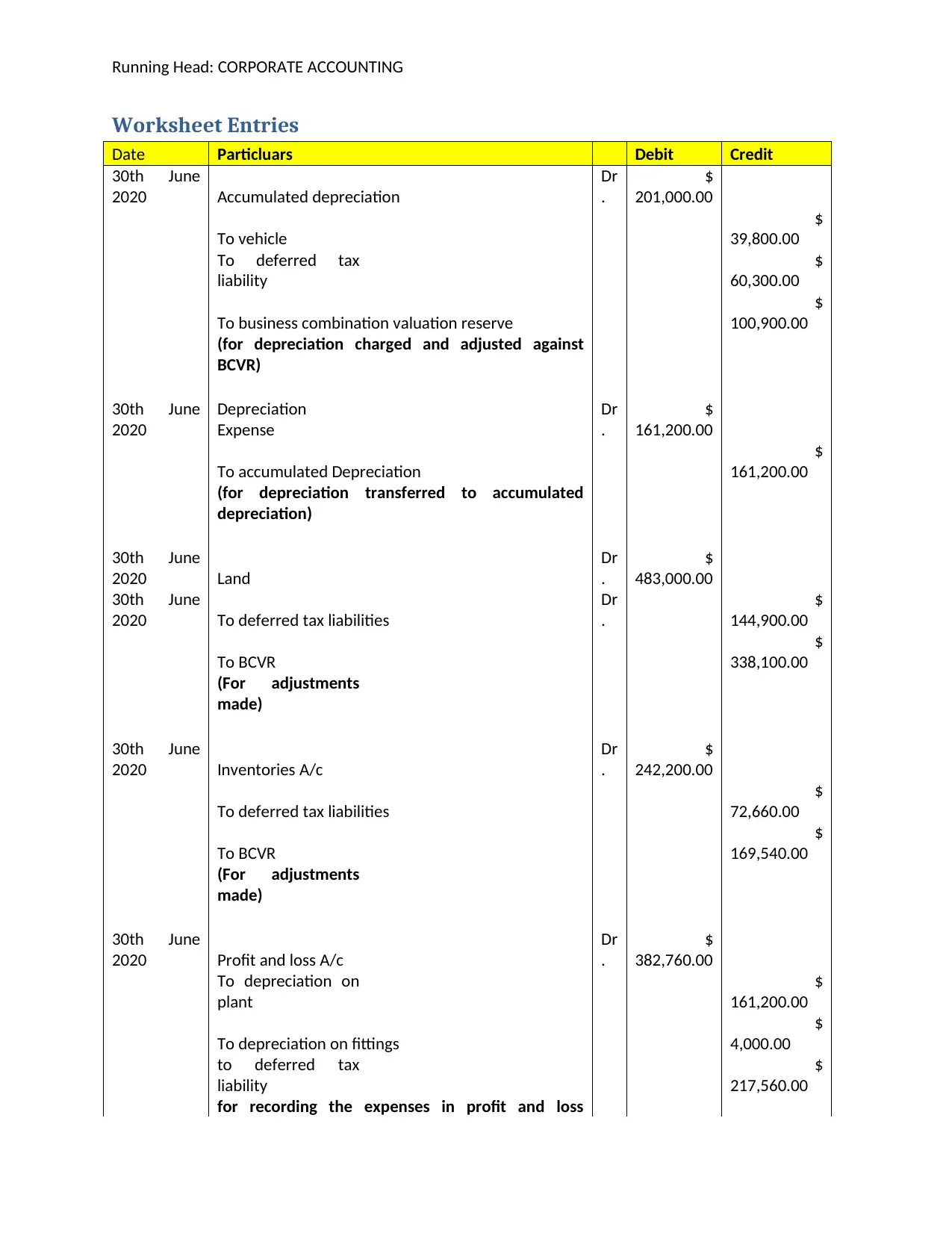

This assignment analyzes the acquisition of Davis Ltd by Alma Ltd, focusing on corporate accounting principles. It includes a detailed acquisition analysis, examining the fair value of identifiable assets and liabilities, and calculating goodwill. The solution provides combination entries, including pre-acquisition entries and entries for non-controlling interests (NCI). Worksheet entries are presented to adjust for depreciation, land, and inventories. The assignment also discusses the changes in the full goodwill method versus the partial goodwill method, highlighting the impact on goodwill calculation and profit sharing. Relevant journal entries are provided to illustrate the accounting treatment of the acquisition and consolidation process, offering a comprehensive understanding of the financial implications.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.