HI5020: Corporate Accounting Assignment on Funds, Liabilities, Assets

VerifiedAdded on 2022/09/07

|12

|4249

|19

Report

AI Summary

This report provides a comprehensive analysis of the financial aspects of two ASX-listed companies, Wesfarmers Limited and JB Hi-Fi Limited. It begins by examining the various sources of funds utilized by both companies, including interest-bearing loans, issued capital, reserves, retained earnings, and current liabilities, and traces the evolution of these funds over a three-year period. The report then delves into the advantages and disadvantages of each funding source, offering insights into the strategic financial decisions of the companies. A significant portion is dedicated to the provisions of AASB 137, exploring its application in the annual reports of the two companies, particularly concerning provisions, contingent liabilities, and contingent assets. Finally, the report identifies and analyzes the different categories of assets reported by Wesfarmers and JB Hi-Fi, along with the measurement bases employed for each asset class, providing a detailed understanding of their accounting practices.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Author’s Note

Corporate Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Abstract

Business organizations require funds in order to continue their business operation

along with facilitating certain expansion plans or business growth. Moreover.

Different types of assets and liabilities can be seen in the companies that require the

companies to adopt the appropriate measurement basis to measure and recognize

them. There are three different parts of the report. The first part discusses about the

internal and external sources of funds in Wesfarmers Limited and JB Hi-Fi Limited.

The second part discusses about description of liabilities along with the provisions of

the accounting standard of AASB 137 Provisions, Contingent Liabilities and

Contingent Assets. The last part discusses about the assets in these two companies

along with the adopted measurement basis by these two companies.

Abstract

Business organizations require funds in order to continue their business operation

along with facilitating certain expansion plans or business growth. Moreover.

Different types of assets and liabilities can be seen in the companies that require the

companies to adopt the appropriate measurement basis to measure and recognize

them. There are three different parts of the report. The first part discusses about the

internal and external sources of funds in Wesfarmers Limited and JB Hi-Fi Limited.

The second part discusses about description of liabilities along with the provisions of

the accounting standard of AASB 137 Provisions, Contingent Liabilities and

Contingent Assets. The last part discusses about the assets in these two companies

along with the adopted measurement basis by these two companies.

2CORPORATE ACCOUNTING

Table of Contents

Introduction...................................................................................................................3

Different Sources of Fund.............................................................................................3

Evolution of Funds........................................................................................................3

Percentage of Internally Generated and Externally Generated Funds........................4

Relative Merits and Shortcomings of Sources of Funds Used.....................................5

Types of Liabilities........................................................................................................6

Provisions under AASB 137.........................................................................................6

References to the Standard of AASB 137 in the Annual Report..................................7

Different Categories of Assets......................................................................................7

Measurement Basis of Assets used by the Companies...............................................7

Conclusion....................................................................................................................9

References.................................................................................................................10

Table of Contents

Introduction...................................................................................................................3

Different Sources of Fund.............................................................................................3

Evolution of Funds........................................................................................................3

Percentage of Internally Generated and Externally Generated Funds........................4

Relative Merits and Shortcomings of Sources of Funds Used.....................................5

Types of Liabilities........................................................................................................6

Provisions under AASB 137.........................................................................................6

References to the Standard of AASB 137 in the Annual Report..................................7

Different Categories of Assets......................................................................................7

Measurement Basis of Assets used by the Companies...............................................7

Conclusion....................................................................................................................9

References.................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Introduction

The key purpose of this report is the analysis and evaluation of some of the

major financial aspects of two ASX listed companies; they are Wesfarmers Limited

(Wesfarmers) and JB Hi-Fi Limited (JB Hi-Fi). This report discusses about different

types of funds used by these two companies and the evolution of these funds for the

last three years. This also discusses about the advantages and disadvantages of

sources of funds used by these firms. After that, this report sheds light on the

provisions of AASB 137 and the use of the same standard in the annual reports of

these two companies. Lastly, this report discusses about the types of assets

reported by these two companies. In addition, it shows the measurement bases

adopted by these two companies for the reported assets in the financial statements.

Different Sources of Fund

Wesfarmers – Wesfarmers has used four source of funds for the business. They are

interest bearing loans and borrowings, issued capital, reserves, retained earnings

and current liabilities (wesfarmers.com.au 2019). The company has used these

funds with the aim to fund its business operations.

JB Hi Fi – JB Hi-Fi has also used certain sources of funds for the business; they are

borrowings, contributed equity, reserves, retained earnings and current liabilities.

The management of JB Hi-Fi has used these sources of funds for the purpose of

financing its business operations (investors.jbhifi.com.au 2019).

Evolution of Funds

Wesfarmers – Wesfarmers has divided its interest bearing loans and borrowings

under current liabilities and non-current liabilities over the last three years

(wesfarmers.com.au 2019). Interest bearing loans and borrowings under current

liabilities have decreased from 2017 to 2019; that is $1347 million in 2017, $1159

million in 2018 and $356 million in 2019. The same trend can be seen in case of

interest bearing loans and borrowings under non-current liabilities; that is $4066

million, $2985 million and $2673 million (wesfarmers.com.au 2019). The main

reason for this decrease is the large repayment of borrowings. Issued capital has

decreased over the years that is $22268 million in 2017, $22277 million in 2018 and

$15809 million in 2019 (wesfarmers.com.au 2019). The reserves have also

decreased over the years and 2019 has registered negative reserve and this is

because of accumulated losses due to poor business performance. Wesfarmers has

also reported accumulated losses in 2019 after the reduction of retained earnings

from 2017 to 2018 (wesfarmers.com.au 2019).

JB Hi-Fi – In JB Hi-Fi, the borrowings have decreased over the last three years that

is $558.8 million in 2017, $469.4 million in 2018 and $439.1 million in 2019: and

continuous repayment of borrowings is the main reason for this reduction in the

source of fund (investors.jbhifi.com.au 2019). Contributed equity has increased from

$438.7 million in 2017 to $441.7 million in 2018 and then decreased in 2018 that is

$434.8 million (investors.jbhifi.com.au 2019). This is due to the deviation in the issue

of shares and share prices. JB Hi-Fi has increased its reserve from 2017 to 2019

continuously that is $33.2 million in 2017, $42.7 million in 2018 and $53.7 million in

2019. Like reserves, retained earnings of the company has also increased

continuously from 2017 to 2019; that is $381.6 million in 2017, $463.2 million in 2018

and $555.6 million in 2019 (investors.jbhifi.com.au 2019).

Introduction

The key purpose of this report is the analysis and evaluation of some of the

major financial aspects of two ASX listed companies; they are Wesfarmers Limited

(Wesfarmers) and JB Hi-Fi Limited (JB Hi-Fi). This report discusses about different

types of funds used by these two companies and the evolution of these funds for the

last three years. This also discusses about the advantages and disadvantages of

sources of funds used by these firms. After that, this report sheds light on the

provisions of AASB 137 and the use of the same standard in the annual reports of

these two companies. Lastly, this report discusses about the types of assets

reported by these two companies. In addition, it shows the measurement bases

adopted by these two companies for the reported assets in the financial statements.

Different Sources of Fund

Wesfarmers – Wesfarmers has used four source of funds for the business. They are

interest bearing loans and borrowings, issued capital, reserves, retained earnings

and current liabilities (wesfarmers.com.au 2019). The company has used these

funds with the aim to fund its business operations.

JB Hi Fi – JB Hi-Fi has also used certain sources of funds for the business; they are

borrowings, contributed equity, reserves, retained earnings and current liabilities.

The management of JB Hi-Fi has used these sources of funds for the purpose of

financing its business operations (investors.jbhifi.com.au 2019).

Evolution of Funds

Wesfarmers – Wesfarmers has divided its interest bearing loans and borrowings

under current liabilities and non-current liabilities over the last three years

(wesfarmers.com.au 2019). Interest bearing loans and borrowings under current

liabilities have decreased from 2017 to 2019; that is $1347 million in 2017, $1159

million in 2018 and $356 million in 2019. The same trend can be seen in case of

interest bearing loans and borrowings under non-current liabilities; that is $4066

million, $2985 million and $2673 million (wesfarmers.com.au 2019). The main

reason for this decrease is the large repayment of borrowings. Issued capital has

decreased over the years that is $22268 million in 2017, $22277 million in 2018 and

$15809 million in 2019 (wesfarmers.com.au 2019). The reserves have also

decreased over the years and 2019 has registered negative reserve and this is

because of accumulated losses due to poor business performance. Wesfarmers has

also reported accumulated losses in 2019 after the reduction of retained earnings

from 2017 to 2018 (wesfarmers.com.au 2019).

JB Hi-Fi – In JB Hi-Fi, the borrowings have decreased over the last three years that

is $558.8 million in 2017, $469.4 million in 2018 and $439.1 million in 2019: and

continuous repayment of borrowings is the main reason for this reduction in the

source of fund (investors.jbhifi.com.au 2019). Contributed equity has increased from

$438.7 million in 2017 to $441.7 million in 2018 and then decreased in 2018 that is

$434.8 million (investors.jbhifi.com.au 2019). This is due to the deviation in the issue

of shares and share prices. JB Hi-Fi has increased its reserve from 2017 to 2019

continuously that is $33.2 million in 2017, $42.7 million in 2018 and $53.7 million in

2019. Like reserves, retained earnings of the company has also increased

continuously from 2017 to 2019; that is $381.6 million in 2017, $463.2 million in 2018

and $555.6 million in 2019 (investors.jbhifi.com.au 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

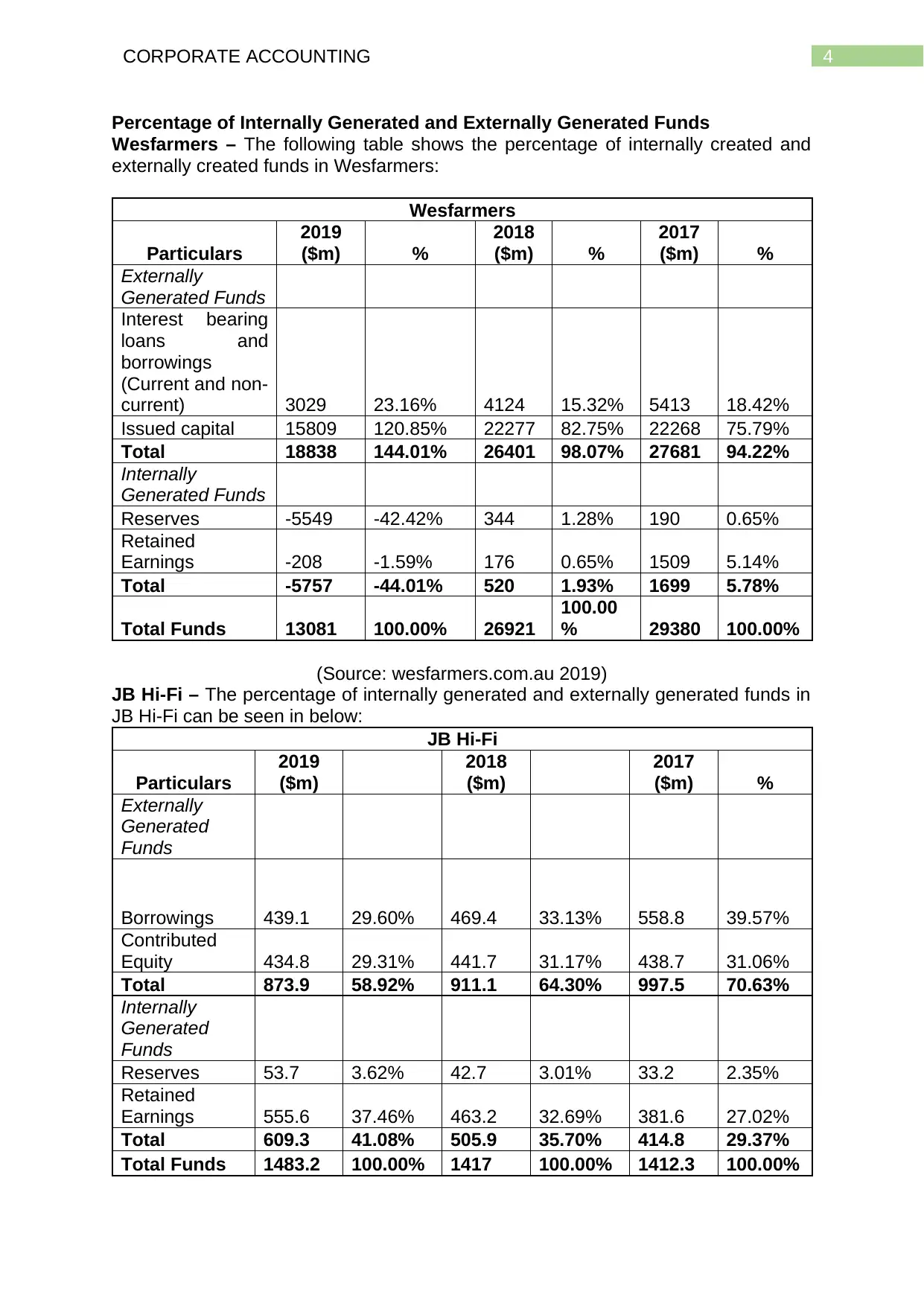

Percentage of Internally Generated and Externally Generated Funds

Wesfarmers – The following table shows the percentage of internally created and

externally created funds in Wesfarmers:

Wesfarmers

Particulars

2019

($m) %

2018

($m) %

2017

($m) %

Externally

Generated Funds

Interest bearing

loans and

borrowings

(Current and non-

current) 3029 23.16% 4124 15.32% 5413 18.42%

Issued capital 15809 120.85% 22277 82.75% 22268 75.79%

Total 18838 144.01% 26401 98.07% 27681 94.22%

Internally

Generated Funds

Reserves -5549 -42.42% 344 1.28% 190 0.65%

Retained

Earnings -208 -1.59% 176 0.65% 1509 5.14%

Total -5757 -44.01% 520 1.93% 1699 5.78%

Total Funds 13081 100.00% 26921

100.00

% 29380 100.00%

(Source: wesfarmers.com.au 2019)

JB Hi-Fi – The percentage of internally generated and externally generated funds in

JB Hi-Fi can be seen in below:

JB Hi-Fi

Particulars

2019

($m)

2018

($m)

2017

($m) %

Externally

Generated

Funds

Borrowings 439.1 29.60% 469.4 33.13% 558.8 39.57%

Contributed

Equity 434.8 29.31% 441.7 31.17% 438.7 31.06%

Total 873.9 58.92% 911.1 64.30% 997.5 70.63%

Internally

Generated

Funds

Reserves 53.7 3.62% 42.7 3.01% 33.2 2.35%

Retained

Earnings 555.6 37.46% 463.2 32.69% 381.6 27.02%

Total 609.3 41.08% 505.9 35.70% 414.8 29.37%

Total Funds 1483.2 100.00% 1417 100.00% 1412.3 100.00%

Percentage of Internally Generated and Externally Generated Funds

Wesfarmers – The following table shows the percentage of internally created and

externally created funds in Wesfarmers:

Wesfarmers

Particulars

2019

($m) %

2018

($m) %

2017

($m) %

Externally

Generated Funds

Interest bearing

loans and

borrowings

(Current and non-

current) 3029 23.16% 4124 15.32% 5413 18.42%

Issued capital 15809 120.85% 22277 82.75% 22268 75.79%

Total 18838 144.01% 26401 98.07% 27681 94.22%

Internally

Generated Funds

Reserves -5549 -42.42% 344 1.28% 190 0.65%

Retained

Earnings -208 -1.59% 176 0.65% 1509 5.14%

Total -5757 -44.01% 520 1.93% 1699 5.78%

Total Funds 13081 100.00% 26921

100.00

% 29380 100.00%

(Source: wesfarmers.com.au 2019)

JB Hi-Fi – The percentage of internally generated and externally generated funds in

JB Hi-Fi can be seen in below:

JB Hi-Fi

Particulars

2019

($m)

2018

($m)

2017

($m) %

Externally

Generated

Funds

Borrowings 439.1 29.60% 469.4 33.13% 558.8 39.57%

Contributed

Equity 434.8 29.31% 441.7 31.17% 438.7 31.06%

Total 873.9 58.92% 911.1 64.30% 997.5 70.63%

Internally

Generated

Funds

Reserves 53.7 3.62% 42.7 3.01% 33.2 2.35%

Retained

Earnings 555.6 37.46% 463.2 32.69% 381.6 27.02%

Total 609.3 41.08% 505.9 35.70% 414.8 29.37%

Total Funds 1483.2 100.00% 1417 100.00% 1412.3 100.00%

5CORPORATE ACCOUNTING

(Source: investors.jbhifi.com.au 2019)

In case of both of the companies, borrowings and issued capital are the

externally generated funds; and reserves and retained earnings are the internal

sources of funds.

Relative Merits and Shortcomings of Sources of Funds Used

Interest Bearing Debts or Borrowings

Merits – The main merits is that it allows the companies to keep the ownership of

the business unlike equity financing. After that, large amount of funds for the

purposes of large purchases or business expansion can be acquired by using this

source of fund. It provides flexibility to the companies along with providing the

opportunity to improve the credit ratings (Wang and Lin 2013).

Shortcomings – This source of fund creates key obligation on the companies to

make the repayment of the borrowed funds irrespective of the fact that whether the

company has made profit or not. In addition, this source of fund comes with high

interest rate. In addition, collaterals need to be maintained by the company in most

of the cases (Zhang 2016).

Issued Capital or Contributed Equity

Merits – Fund raised through issue of shares can be used for the business

operations as well as growth of the companies. Unlike debts, the companies are not

required to repay it. Companies can use the proceeds from the sales of shares

however they want in the absence of any obligation (Rossi 2014).

Shortcomings – Companies have to incur high costs in order to raise the required

fund by share issue. Most importantly, using shares in order to raise the required

money ends up in dividing ownership of the company among the shareholders by

providing the voting rights to them. This can make the corporations vulnerable

(Finnerty 2013).

Reserves

Merits – The main advantage is that this provides the companies with the ability to

meet the future losses and this ads stability to the whole financial position of the

companies. In addition, reserves can be used in the lean financial years in order to

cover the abnormal losses. It is a useful tool to the companies at the time of financial

crisis (Brief and Peasnell 2013).

Shortcomings – The main shortcoming associated with this is that the purpose of

audit cannot be achieved since the true and fair financial position of the company is

not possible to show. Sometimes, misuse of this kind of reserves can be seen that is

not good for companies (Maurer et al. 2016).

Retained Earnings

Merits – It is a powerful business strategy to fund a business by the use of retained

earnings since this does not contribute to the increase in the amount of debt of the

firms. In addition, the option of conservation allows the companies in maintaining full

control over the business. This provides the companies with the opportunity to fund

the business growth internally (Yusra, Hadya and Fatmasari 2019).

Shortcomings – The main shortcoming is that it is a slow process to fund the

business through retained earnings as the businesses can miss the crucial business

opportunities at the time of building up the required funds. Devoting large amount of

retained earnings for business growth can hamper the present business operations

of the companies (Royer 2017).

(Source: investors.jbhifi.com.au 2019)

In case of both of the companies, borrowings and issued capital are the

externally generated funds; and reserves and retained earnings are the internal

sources of funds.

Relative Merits and Shortcomings of Sources of Funds Used

Interest Bearing Debts or Borrowings

Merits – The main merits is that it allows the companies to keep the ownership of

the business unlike equity financing. After that, large amount of funds for the

purposes of large purchases or business expansion can be acquired by using this

source of fund. It provides flexibility to the companies along with providing the

opportunity to improve the credit ratings (Wang and Lin 2013).

Shortcomings – This source of fund creates key obligation on the companies to

make the repayment of the borrowed funds irrespective of the fact that whether the

company has made profit or not. In addition, this source of fund comes with high

interest rate. In addition, collaterals need to be maintained by the company in most

of the cases (Zhang 2016).

Issued Capital or Contributed Equity

Merits – Fund raised through issue of shares can be used for the business

operations as well as growth of the companies. Unlike debts, the companies are not

required to repay it. Companies can use the proceeds from the sales of shares

however they want in the absence of any obligation (Rossi 2014).

Shortcomings – Companies have to incur high costs in order to raise the required

fund by share issue. Most importantly, using shares in order to raise the required

money ends up in dividing ownership of the company among the shareholders by

providing the voting rights to them. This can make the corporations vulnerable

(Finnerty 2013).

Reserves

Merits – The main advantage is that this provides the companies with the ability to

meet the future losses and this ads stability to the whole financial position of the

companies. In addition, reserves can be used in the lean financial years in order to

cover the abnormal losses. It is a useful tool to the companies at the time of financial

crisis (Brief and Peasnell 2013).

Shortcomings – The main shortcoming associated with this is that the purpose of

audit cannot be achieved since the true and fair financial position of the company is

not possible to show. Sometimes, misuse of this kind of reserves can be seen that is

not good for companies (Maurer et al. 2016).

Retained Earnings

Merits – It is a powerful business strategy to fund a business by the use of retained

earnings since this does not contribute to the increase in the amount of debt of the

firms. In addition, the option of conservation allows the companies in maintaining full

control over the business. This provides the companies with the opportunity to fund

the business growth internally (Yusra, Hadya and Fatmasari 2019).

Shortcomings – The main shortcoming is that it is a slow process to fund the

business through retained earnings as the businesses can miss the crucial business

opportunities at the time of building up the required funds. Devoting large amount of

retained earnings for business growth can hamper the present business operations

of the companies (Royer 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

Types of Liabilities

Wesfarmers – Two categories of liabilities have been reported by Wesfarmers that

are current liabilities and non-current liabilities. Trade and other payable is a current

liability and this is the obligation of Wesfarmers to pay for goods and services.

Income tax payable is the amount that is owed to the government on the basis of

profitability (wesfarmers.com.au 2019). Provision is another liability of Wesfarmers

and there are five types of provisions in Wesfarmers; they are employee benefits,

provision for lease, off-market contracts, self-insured risks, mine rehabilitation and

restructuring and make good. Hedging is another liability of Wesfarmers that is a

portion of the company’s risk management strategy against the risk from movement

in foreign exchange. Among all these liabilities, interest-bearing loans and

borrowings are the only interest bearing liabilities and the rest are the non-interest

bearing liabilities. Interest-bearing loans and borrowings include bank debt and

capital market debt (wesfarmers.com.au 2019).

JB Hi-Fi – JB Hi-Fi has reported both current and non-current liabilities. Trade and

other payables is a major current asset that represent the liabilities for provided

goods and services that are unpaid. That includes goods and services tax payable

and other creditors and accruals (investors.jbhifi.com.au 2019). Deferred revenue is

considered under both current and non-current liabilities and this is associated the

unfulfilled services to be performed. Provision is another current and non-current

liability of JB Hi-Fi; and the company has two types of provisions that are employee

benefit provision and lease provision (investors.jbhifi.com.au 2019). Some of the

other liabilities are lease accruals, lease incentives and other financial liabilities

(investors.jbhifi.com.au 2019). Deferred tax is a current as well as non-current

liability that is generated from the provisional changes attributed to deferred tax

assets, inventories, provisions, deferred revenue and other. The only interest bearing

liability is borrowings which is bank loans (investors.jbhifi.com.au 2019).

Provisions under AASB 137

AASB 137 Provisions, Contingent Liabilities and Contingent Assets provides

the Australian listed companies with the techniques and procedures to recognize and

measure the provisions, contingent liabilities and contingent assets (aasb.gov.au

2019).

As per AASB 137, Paragraph 14, provision needs to be recognized by an

entity when it has a present commitment because of a past incident which probable

the outflow of resources associated with the economic benefit for settling the

commitment and it is possible to estimate it properly (Moerman and van der Laan

2013).

As per Paragraph 27 and 31 of AASB 137, it is not required for an entity to

report the contingent liabilities and contingent assets. As per Paragraph 28 of AASB

137, a contingent liability is required to be disclosed, but it cannot be disclosed when

there is a remote possibility of the outflow of economic resources associated with the

economic benefit. As per Paragraph 34 of AASB 137, a company needs to disclose

the contingent assets where there is a probability of the outflow of economic benefits

(Hudson 2016).

According to Paragraph 36 of AASB 137, the amount recognized as a

provision needs to be the finest estimate of the required outflow for settling the

present obligation. Paragraph 42 of AASB 137 puts the obligation on the companies

to consider the risks and uncertainties surrounded many events and circumstance at

the time to reach to the best estimation of a provision. As per Paragraph 84 of AASB

Types of Liabilities

Wesfarmers – Two categories of liabilities have been reported by Wesfarmers that

are current liabilities and non-current liabilities. Trade and other payable is a current

liability and this is the obligation of Wesfarmers to pay for goods and services.

Income tax payable is the amount that is owed to the government on the basis of

profitability (wesfarmers.com.au 2019). Provision is another liability of Wesfarmers

and there are five types of provisions in Wesfarmers; they are employee benefits,

provision for lease, off-market contracts, self-insured risks, mine rehabilitation and

restructuring and make good. Hedging is another liability of Wesfarmers that is a

portion of the company’s risk management strategy against the risk from movement

in foreign exchange. Among all these liabilities, interest-bearing loans and

borrowings are the only interest bearing liabilities and the rest are the non-interest

bearing liabilities. Interest-bearing loans and borrowings include bank debt and

capital market debt (wesfarmers.com.au 2019).

JB Hi-Fi – JB Hi-Fi has reported both current and non-current liabilities. Trade and

other payables is a major current asset that represent the liabilities for provided

goods and services that are unpaid. That includes goods and services tax payable

and other creditors and accruals (investors.jbhifi.com.au 2019). Deferred revenue is

considered under both current and non-current liabilities and this is associated the

unfulfilled services to be performed. Provision is another current and non-current

liability of JB Hi-Fi; and the company has two types of provisions that are employee

benefit provision and lease provision (investors.jbhifi.com.au 2019). Some of the

other liabilities are lease accruals, lease incentives and other financial liabilities

(investors.jbhifi.com.au 2019). Deferred tax is a current as well as non-current

liability that is generated from the provisional changes attributed to deferred tax

assets, inventories, provisions, deferred revenue and other. The only interest bearing

liability is borrowings which is bank loans (investors.jbhifi.com.au 2019).

Provisions under AASB 137

AASB 137 Provisions, Contingent Liabilities and Contingent Assets provides

the Australian listed companies with the techniques and procedures to recognize and

measure the provisions, contingent liabilities and contingent assets (aasb.gov.au

2019).

As per AASB 137, Paragraph 14, provision needs to be recognized by an

entity when it has a present commitment because of a past incident which probable

the outflow of resources associated with the economic benefit for settling the

commitment and it is possible to estimate it properly (Moerman and van der Laan

2013).

As per Paragraph 27 and 31 of AASB 137, it is not required for an entity to

report the contingent liabilities and contingent assets. As per Paragraph 28 of AASB

137, a contingent liability is required to be disclosed, but it cannot be disclosed when

there is a remote possibility of the outflow of economic resources associated with the

economic benefit. As per Paragraph 34 of AASB 137, a company needs to disclose

the contingent assets where there is a probability of the outflow of economic benefits

(Hudson 2016).

According to Paragraph 36 of AASB 137, the amount recognized as a

provision needs to be the finest estimate of the required outflow for settling the

present obligation. Paragraph 42 of AASB 137 puts the obligation on the companies

to consider the risks and uncertainties surrounded many events and circumstance at

the time to reach to the best estimation of a provision. As per Paragraph 84 of AASB

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

137, a company needs to disclose certain aspects related to provision; they are end

of the period carrying amount, additional provision made, amount used during the

period, reversal of the amount of unused provision, increase in provision during the

year. As per Paragraph 85 of AASB 137, the disclosures associated with each type

of provision include short explanation of the provision, indication of the uncertainties

and any amount of expected reimbursement (Wardani et al. 2019).

References to the Standard of AASB 137 in the Annual Report

The annual reports of both Wesfarmers and JB Hi-Fi demonstrate that these

companies have not mentioned about AASB 137 in their annual reports. However,

these companies have accounted for provision, contingent liabilities and contingent

assets by complying with the provisions of AASB 137 (Tran 2015). Both Wesfarmers

and JB Hi-Fi have disclosed every element of their business provisions by complying

with the relevant paragraphs of AASB 137. For example, by complying with the

paragraphs 84 and 85 of AASB 137, both the companies have disclosed the opening

balance of provision, development of new provision, utilized provision, reversal of

provision and carrying amount at the accounting period end. After that, by complying

with the Paragraphs of 36 and 42, both the companies have taken into consideration

the necessary risk and uncertainty factors for the estimation of provision.

Wesfarmers has disclosed the information on its contingent liabilities associated with

trading guarantees in the notes to the financial reports. The main reason of the

company behind the disclosure of information on contingent liabilities is the high

probability that there could be outflow of economic resources due to the presence of

these liabilities (Richardson, Taylor and Lanis 2013). However, it needs to be

mentioned that JB Hi-Fi has not reported any contingent liabilities and contingent

assets because of the remote probability of outflow of economic resources for the

presence of these contingencies.

Different Categories of Assets

The annual reports of Wesfarmers and JB Hi-Fi have shown that both the

companies have reported certain assets in the balance sheet and they are discussed

below.

Wesfarmers – The firm has reported two categories of assets in its balance sheet;

they are current assets and non-current assets. The assets reported under the

current assets are cash and cash equivalent, trade and other receivables,

inventories, derivatives and others (wesfarmers.com.au 2019). The assets that

Wesfarmers has shown in the list of non-current assets are investment in associated

and joint ventures, deferred tax assets, property, plant and equipment, goodwill,

intangible assets, derivatives and other. These are all the assets reported by the

company in the financial statements (wesfarmers.com.au 2019).

JB Hi-Fi – The management of JB Hi-Fi has also categorized all of their assets in

two categories; they are current assets and non-current assets. The assets under

current assets are cash and cash equivalent, trade and other receivables,

inventories and other current assets. The assets under non-current assets are plant

and equipment, deferred tax assets, intangible assets and other non-current assets.

The management of the company has reported all these assets in the financial

statements (investors.jbhifi.com.au 2019).

137, a company needs to disclose certain aspects related to provision; they are end

of the period carrying amount, additional provision made, amount used during the

period, reversal of the amount of unused provision, increase in provision during the

year. As per Paragraph 85 of AASB 137, the disclosures associated with each type

of provision include short explanation of the provision, indication of the uncertainties

and any amount of expected reimbursement (Wardani et al. 2019).

References to the Standard of AASB 137 in the Annual Report

The annual reports of both Wesfarmers and JB Hi-Fi demonstrate that these

companies have not mentioned about AASB 137 in their annual reports. However,

these companies have accounted for provision, contingent liabilities and contingent

assets by complying with the provisions of AASB 137 (Tran 2015). Both Wesfarmers

and JB Hi-Fi have disclosed every element of their business provisions by complying

with the relevant paragraphs of AASB 137. For example, by complying with the

paragraphs 84 and 85 of AASB 137, both the companies have disclosed the opening

balance of provision, development of new provision, utilized provision, reversal of

provision and carrying amount at the accounting period end. After that, by complying

with the Paragraphs of 36 and 42, both the companies have taken into consideration

the necessary risk and uncertainty factors for the estimation of provision.

Wesfarmers has disclosed the information on its contingent liabilities associated with

trading guarantees in the notes to the financial reports. The main reason of the

company behind the disclosure of information on contingent liabilities is the high

probability that there could be outflow of economic resources due to the presence of

these liabilities (Richardson, Taylor and Lanis 2013). However, it needs to be

mentioned that JB Hi-Fi has not reported any contingent liabilities and contingent

assets because of the remote probability of outflow of economic resources for the

presence of these contingencies.

Different Categories of Assets

The annual reports of Wesfarmers and JB Hi-Fi have shown that both the

companies have reported certain assets in the balance sheet and they are discussed

below.

Wesfarmers – The firm has reported two categories of assets in its balance sheet;

they are current assets and non-current assets. The assets reported under the

current assets are cash and cash equivalent, trade and other receivables,

inventories, derivatives and others (wesfarmers.com.au 2019). The assets that

Wesfarmers has shown in the list of non-current assets are investment in associated

and joint ventures, deferred tax assets, property, plant and equipment, goodwill,

intangible assets, derivatives and other. These are all the assets reported by the

company in the financial statements (wesfarmers.com.au 2019).

JB Hi-Fi – The management of JB Hi-Fi has also categorized all of their assets in

two categories; they are current assets and non-current assets. The assets under

current assets are cash and cash equivalent, trade and other receivables,

inventories and other current assets. The assets under non-current assets are plant

and equipment, deferred tax assets, intangible assets and other non-current assets.

The management of the company has reported all these assets in the financial

statements (investors.jbhifi.com.au 2019).

8CORPORATE ACCOUNTING

Measurement Basis of Assets used by the Companies

Both Wesfarmers and JB Hi-Fi have used certain measurement bases for all

of their assets in the balance sheet; these are discussed below:

Wesfarmers

The classification of Cash on deposit is done as financial assets that are held

at amortized costs. Interests on cash at bank are earned at floating rate on

the basis of daily bank deposit rates (wesfarmers.com.au 2019).

Trade receivables are of terms of up to thirty days and the company initially

recognizes them as per its revenue policy and then, their measurement is

done at amortized costs utilizing actual interest method.

The valuation of inventories is undertaken at the lower of cost and net

realizable value. The company a key estimation associated with the realizable

value.

The company measures the derivative financial instruments at fair value on

the date of entering into the contracts. The classification of hedge accounting

is done as fair value hedges and cash flows hedges by the company

(wesfarmers.com.au 2019).

Investments in the associated by the company are carried in the balance

sheet at cost plus any post-acquisition changes in the company’s shares of

the net assets of the associated.

Wesfarmers measure the current tax assets at the amount that is anticipated

to be recovered from the authorities at the tax rates (wesfarmers.com.au

2019).

The company measures the carrying value associated with property, plant

and equipment as the cost of the assets less accumulated depreciation and

impairment. The depreciation is charged in accordance with the straight-line

method of depreciation.

The company measures acquired goodwill from business combination at cost.

The company separately acquires the intangible assets and their

measurement is done at cost less impairment losses and amortization

(wesfarmers.com.au 2019).

JB Hi-Fi

Trade receivables have a credit period of 30 days and no interest is

chargeable on it. JB Hi-Fi recognizes the trade receivables at amortized cost

less allowance for predictable credit loss. The company has made an

allowance for the expected credit losses through the use of matrix based

historical credit loss rates (investors.jbhifi.com.au 2019).

The company has stated its inventories at the lower of cost and net realisable

value. The assignment of costs is done to the individual inventory terms

based on weighted average cost. Management judgment is required in order

to ascertain the inventory’s net realisable value.

JB Hi-Fi accounts for the deferred tax through the use of balance sheet

liability technique providing for provisional difference between the carrying

amount of assets and liabilities under the purposes of financial reporting and

taxation. The company recognizes them in the presence of this temporary

difference (investors.jbhifi.com.au 2019).

The company states the property and equipment along with the leasehold

improvements at cost minus depreciation and impairment, if any. These

assets are subject to depreciation on straight-line method. The company tests

these assets for impairment in the presence of any change in circumstances.

Measurement Basis of Assets used by the Companies

Both Wesfarmers and JB Hi-Fi have used certain measurement bases for all

of their assets in the balance sheet; these are discussed below:

Wesfarmers

The classification of Cash on deposit is done as financial assets that are held

at amortized costs. Interests on cash at bank are earned at floating rate on

the basis of daily bank deposit rates (wesfarmers.com.au 2019).

Trade receivables are of terms of up to thirty days and the company initially

recognizes them as per its revenue policy and then, their measurement is

done at amortized costs utilizing actual interest method.

The valuation of inventories is undertaken at the lower of cost and net

realizable value. The company a key estimation associated with the realizable

value.

The company measures the derivative financial instruments at fair value on

the date of entering into the contracts. The classification of hedge accounting

is done as fair value hedges and cash flows hedges by the company

(wesfarmers.com.au 2019).

Investments in the associated by the company are carried in the balance

sheet at cost plus any post-acquisition changes in the company’s shares of

the net assets of the associated.

Wesfarmers measure the current tax assets at the amount that is anticipated

to be recovered from the authorities at the tax rates (wesfarmers.com.au

2019).

The company measures the carrying value associated with property, plant

and equipment as the cost of the assets less accumulated depreciation and

impairment. The depreciation is charged in accordance with the straight-line

method of depreciation.

The company measures acquired goodwill from business combination at cost.

The company separately acquires the intangible assets and their

measurement is done at cost less impairment losses and amortization

(wesfarmers.com.au 2019).

JB Hi-Fi

Trade receivables have a credit period of 30 days and no interest is

chargeable on it. JB Hi-Fi recognizes the trade receivables at amortized cost

less allowance for predictable credit loss. The company has made an

allowance for the expected credit losses through the use of matrix based

historical credit loss rates (investors.jbhifi.com.au 2019).

The company has stated its inventories at the lower of cost and net realisable

value. The assignment of costs is done to the individual inventory terms

based on weighted average cost. Management judgment is required in order

to ascertain the inventory’s net realisable value.

JB Hi-Fi accounts for the deferred tax through the use of balance sheet

liability technique providing for provisional difference between the carrying

amount of assets and liabilities under the purposes of financial reporting and

taxation. The company recognizes them in the presence of this temporary

difference (investors.jbhifi.com.au 2019).

The company states the property and equipment along with the leasehold

improvements at cost minus depreciation and impairment, if any. These

assets are subject to depreciation on straight-line method. The company tests

these assets for impairment in the presence of any change in circumstances.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

JB Hi-Fi carries the intangible assets with indefinite useful life at cost less

accumulated impairment losses. Goodwill is the surplus of the acquisition cost

over the fair value of the firm’s share of the net identifiable assets acquitted at

the acquisition date. The company has adopted the accounting strategy to

charge impairment on assets with identifiable life (investors.jbhifi.com.au

2019).

Conclusion

The main sources of fund used by Wesfarmers and JB Hi-Fi are interest-

bearing borrowings, equity capital, reserves and retained earnings. Both the

companies have made continuous debt payments which contributes to the decrease

in the percentage of debt. However, the merits and limitations of each of the sources

of finance are crucial which much be considered by the managements of the firms

before adopting them. It can also be seen from the analysis that both the companies

have reported current assets, current liabilities, non-current assets and non-current

liabilities. In both Wesfarmers and JB Hi-Fi, interest bearing term borrowing is the

only interest bearing liability reported. It can also be observed that the companies

have complied with the standards and requirements of AASB 137 in order to account

for provision, contingent assets and contingent liabilities. Lastly, both Wesfarmers

and JB Hi-Fi have used the appropriate measurement based for each class of

assets.

JB Hi-Fi carries the intangible assets with indefinite useful life at cost less

accumulated impairment losses. Goodwill is the surplus of the acquisition cost

over the fair value of the firm’s share of the net identifiable assets acquitted at

the acquisition date. The company has adopted the accounting strategy to

charge impairment on assets with identifiable life (investors.jbhifi.com.au

2019).

Conclusion

The main sources of fund used by Wesfarmers and JB Hi-Fi are interest-

bearing borrowings, equity capital, reserves and retained earnings. Both the

companies have made continuous debt payments which contributes to the decrease

in the percentage of debt. However, the merits and limitations of each of the sources

of finance are crucial which much be considered by the managements of the firms

before adopting them. It can also be seen from the analysis that both the companies

have reported current assets, current liabilities, non-current assets and non-current

liabilities. In both Wesfarmers and JB Hi-Fi, interest bearing term borrowing is the

only interest bearing liability reported. It can also be observed that the companies

have complied with the standards and requirements of AASB 137 in order to account

for provision, contingent assets and contingent liabilities. Lastly, both Wesfarmers

and JB Hi-Fi have used the appropriate measurement based for each class of

assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

References

Aasb.gov.au. 2019. Provisions, Contingent Liabilities and Contingent Assets. [online]

Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB137_08-

15_COMPdec16_01-19.pdf [Accessed 20 Dec. 2019].

Brief, R.P. and Peasnell, K.V. eds., 2013. Clean surplus: A link between accounting

and finance. Routledge.

Finnerty, J.D., 2013. Project financing: Asset-based financial engineering. John

Wiley & Sons.

Hudson, M., 2016. No setting off unfair preferences. Australian Restructuring

Insolvency & Turnaround Association Journal, 28(3), p.34.

Investors.jbhifi.com.au. 2019. ANNUAL REPORT 2017. [online] Available at:

https://investors.jbhifi.com.au/wp-content/uploads/2019/11/2017-Annual-Report.pdf

[Accessed 20 Dec. 2019].

Investors.jbhifi.com.au. 2019. ANNUAL REPORT 2018. [online] Available at:

https://investors.jbhifi.com.au/wp-content/uploads/2018/10/Annual-Report-2018-with-

Chairmans-CEOs-Report.pdf [Accessed 20 Dec. 2019].

Investors.jbhifi.com.au. 2019. ANNUAL REPORT 2019. [online] Available at:

https://investors.jbhifi.com.au/wp-content/uploads/2019/10/Annual-Report-2019-with-

Chairmans-CEOs-Report.pdf [Accessed 20 Dec. 2019].

Maurer, R., Mitchell, O.S., Rogalla, R. and Siegelin, I., 2016. Accounting and

actuarial smoothing of retirement payouts in participating life annuities. Insurance:

mathematics and Economics, 71, pp.268-283.

Moerman, L.C. and van der Laan, S.L., 2013. Long-tail liabilities: weaving accounting

constructs into an'intertextual'web.

Richardson, G., Taylor, G. and Lanis, R., 2013. The impact of board of director

oversight characteristics on corporate tax aggressiveness: An empirical

analysis. Journal of Accounting and Public Policy, 32(3), pp.68-88.

Rossi, M., 2014. SMEs’ access to finance: An overview from Southern

Italy. European Journal of Business and Social Sciences, 2(11), pp.155-164.

Royer, J., 2017. Financing agricultural cooperatives with retained

earnings. Agricultural Finance Review, 77(3), pp.393-411.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed

companies in Australia. Austl. Tax F., 30, p.569.

Wang, H.D. and Lin, C.J., 2013. Debt financing and earnings management: An

internal capital market perspective. Journal of Business Finance & Accounting, 40(7-

8), pp.842-868.

Wardani, L., Viverita, V., Husodo, Z.A. and Sunaryo, S., 2019. Contingent Claim

Approach for Pricing of Sovereign Sukuk for R&D Financing in Indonesia. Emerging

Markets Finance and Trade, pp.1-13.

Wesfarmers.com.au. 2019. 2017 Annual Report. [online] Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/j000901-

ar17_interactive_final.pdf?sfvrsn=4 [Accessed 20 Dec. 2019].

Wesfarmers.com.au. 2019. 2019 WESFARMERS ANNUAL REPOR. [online]

Available at: https://www.wesfarmers.com.au/docs/default-source/asx-

announcements/2019-annual-report.pdf?sfvrsn=0 [Accessed 20 Dec. 2019].

Wesfarmers.com.au. 2019. WESFARMERS ANNUAL REPORT 2018. [online]

Available at: https://www.wesfarmers.com.au/docs/default-source/reports/wes18-

044-2018-annual-report.pdf?sfvrsn=6 [Accessed 20 Dec. 2019].

References

Aasb.gov.au. 2019. Provisions, Contingent Liabilities and Contingent Assets. [online]

Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB137_08-

15_COMPdec16_01-19.pdf [Accessed 20 Dec. 2019].

Brief, R.P. and Peasnell, K.V. eds., 2013. Clean surplus: A link between accounting

and finance. Routledge.

Finnerty, J.D., 2013. Project financing: Asset-based financial engineering. John

Wiley & Sons.

Hudson, M., 2016. No setting off unfair preferences. Australian Restructuring

Insolvency & Turnaround Association Journal, 28(3), p.34.

Investors.jbhifi.com.au. 2019. ANNUAL REPORT 2017. [online] Available at:

https://investors.jbhifi.com.au/wp-content/uploads/2019/11/2017-Annual-Report.pdf

[Accessed 20 Dec. 2019].

Investors.jbhifi.com.au. 2019. ANNUAL REPORT 2018. [online] Available at:

https://investors.jbhifi.com.au/wp-content/uploads/2018/10/Annual-Report-2018-with-

Chairmans-CEOs-Report.pdf [Accessed 20 Dec. 2019].

Investors.jbhifi.com.au. 2019. ANNUAL REPORT 2019. [online] Available at:

https://investors.jbhifi.com.au/wp-content/uploads/2019/10/Annual-Report-2019-with-

Chairmans-CEOs-Report.pdf [Accessed 20 Dec. 2019].

Maurer, R., Mitchell, O.S., Rogalla, R. and Siegelin, I., 2016. Accounting and

actuarial smoothing of retirement payouts in participating life annuities. Insurance:

mathematics and Economics, 71, pp.268-283.

Moerman, L.C. and van der Laan, S.L., 2013. Long-tail liabilities: weaving accounting

constructs into an'intertextual'web.

Richardson, G., Taylor, G. and Lanis, R., 2013. The impact of board of director

oversight characteristics on corporate tax aggressiveness: An empirical

analysis. Journal of Accounting and Public Policy, 32(3), pp.68-88.

Rossi, M., 2014. SMEs’ access to finance: An overview from Southern

Italy. European Journal of Business and Social Sciences, 2(11), pp.155-164.

Royer, J., 2017. Financing agricultural cooperatives with retained

earnings. Agricultural Finance Review, 77(3), pp.393-411.

Tran, A., 2015. Can taxable income be estimated from financial reports of listed

companies in Australia. Austl. Tax F., 30, p.569.

Wang, H.D. and Lin, C.J., 2013. Debt financing and earnings management: An

internal capital market perspective. Journal of Business Finance & Accounting, 40(7-

8), pp.842-868.

Wardani, L., Viverita, V., Husodo, Z.A. and Sunaryo, S., 2019. Contingent Claim

Approach for Pricing of Sovereign Sukuk for R&D Financing in Indonesia. Emerging

Markets Finance and Trade, pp.1-13.

Wesfarmers.com.au. 2019. 2017 Annual Report. [online] Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/j000901-

ar17_interactive_final.pdf?sfvrsn=4 [Accessed 20 Dec. 2019].

Wesfarmers.com.au. 2019. 2019 WESFARMERS ANNUAL REPOR. [online]

Available at: https://www.wesfarmers.com.au/docs/default-source/asx-

announcements/2019-annual-report.pdf?sfvrsn=0 [Accessed 20 Dec. 2019].

Wesfarmers.com.au. 2019. WESFARMERS ANNUAL REPORT 2018. [online]

Available at: https://www.wesfarmers.com.au/docs/default-source/reports/wes18-

044-2018-annual-report.pdf?sfvrsn=6 [Accessed 20 Dec. 2019].

11CORPORATE ACCOUNTING

Yusra, I., Hadya, R. and Fatmasari, R., 2019, July. The Effect of Retained Earnings

on Dividend Policy from the Perspective of Life Cycle. In 1st International

Conference on Life, Innovation, Change and Knowledge (ICLICK 2018). Atlantis

Press.

Zhang, S., 2016. Institutional arrangements and debt financing. Research in

International Business and Finance, 36, pp.362-372.

Yusra, I., Hadya, R. and Fatmasari, R., 2019, July. The Effect of Retained Earnings

on Dividend Policy from the Perspective of Life Cycle. In 1st International

Conference on Life, Innovation, Change and Knowledge (ICLICK 2018). Atlantis

Press.

Zhang, S., 2016. Institutional arrangements and debt financing. Research in

International Business and Finance, 36, pp.362-372.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.