Corporate Accounting Assignment: Theory and Application

VerifiedAdded on 2023/04/24

|9

|1639

|428

Homework Assignment

AI Summary

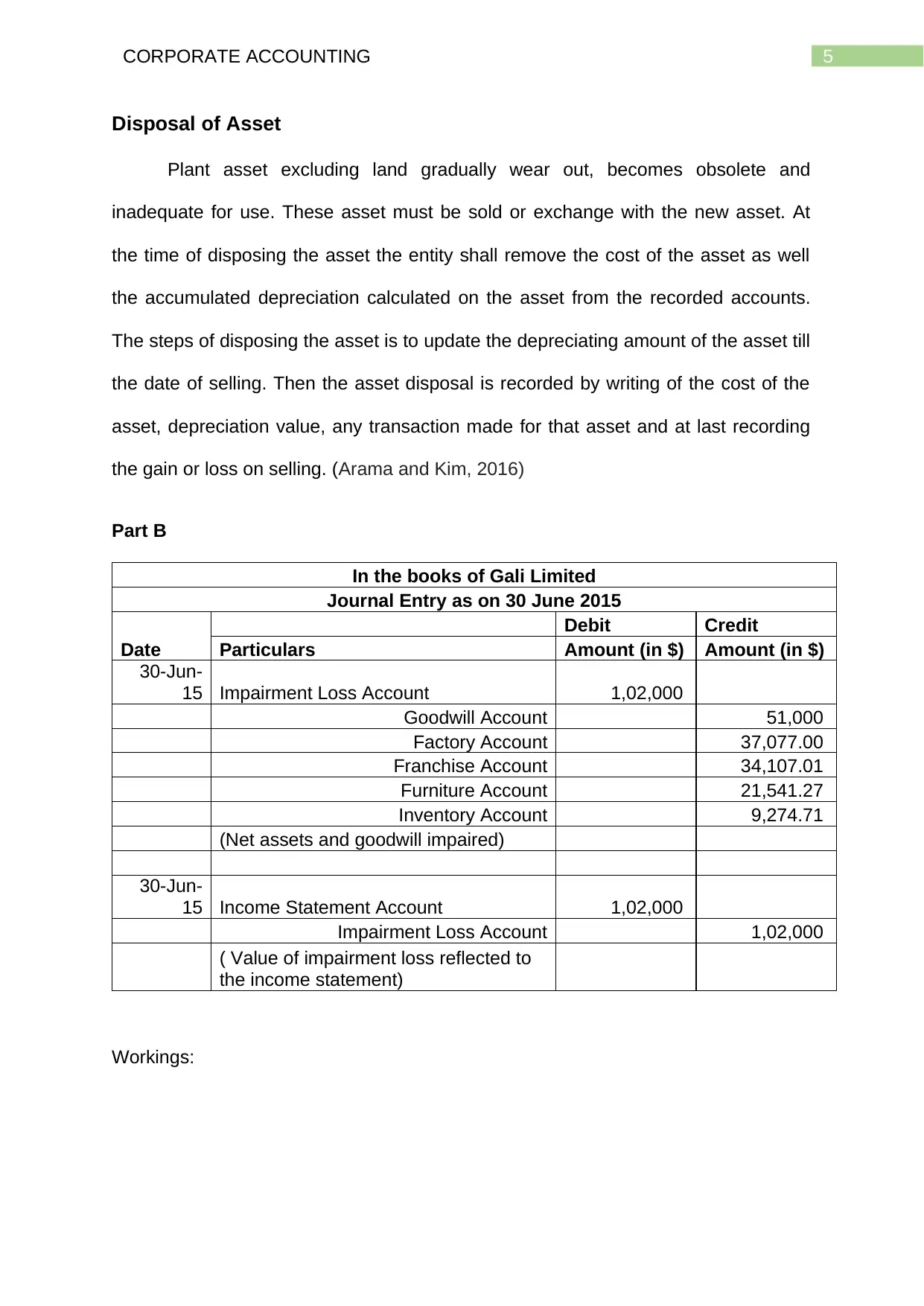

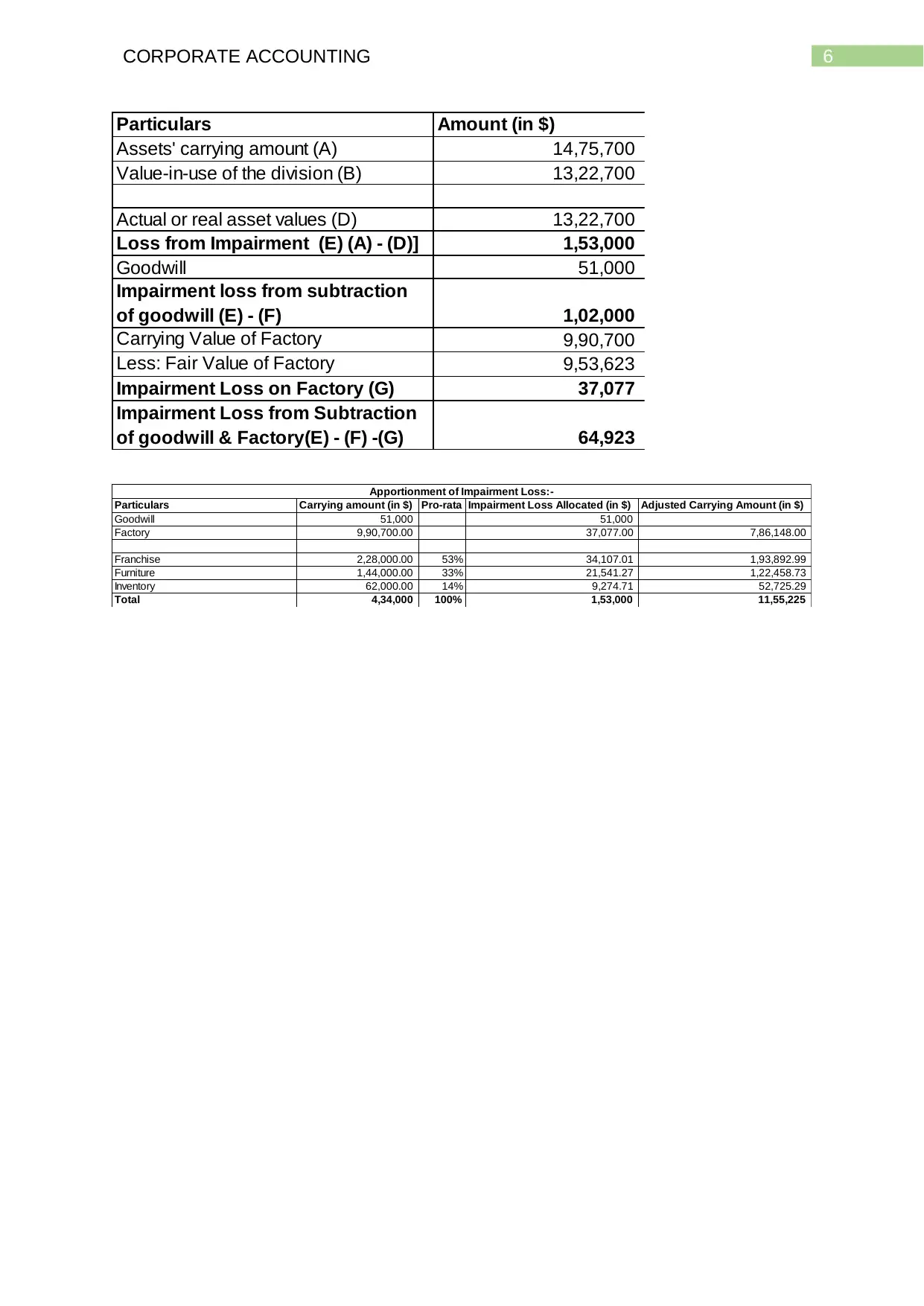

This assignment solution addresses corporate accounting principles, specifically focusing on impairment of assets and their disposal. Part A presents a 1000-word essay explaining recoverable amounts, value in use, and the process of asset disposal according to International Accounting Standard 36. It covers the calculation of recoverable amounts, the significance of impairment loss, and the conditions under which an entity should recognize and reverse an impairment loss, including the concept of Cash Generating Units (CGUs). Part B provides a practical application of the theory, including journal entries for Gali Limited, detailing the impairment loss allocation across various asset accounts, calculations of impairment loss, and the apportionment of the loss. The solution includes workings demonstrating how the impairment loss is calculated based on the carrying amount and the value in use of the division. The assignment is thoroughly referenced, citing various accounting standards and academic sources.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.