Corporate Accounting Assignment: Gali Ltd. Journal Entries & Analysis

VerifiedAdded on 2020/04/01

|9

|1600

|72

Homework Assignment

AI Summary

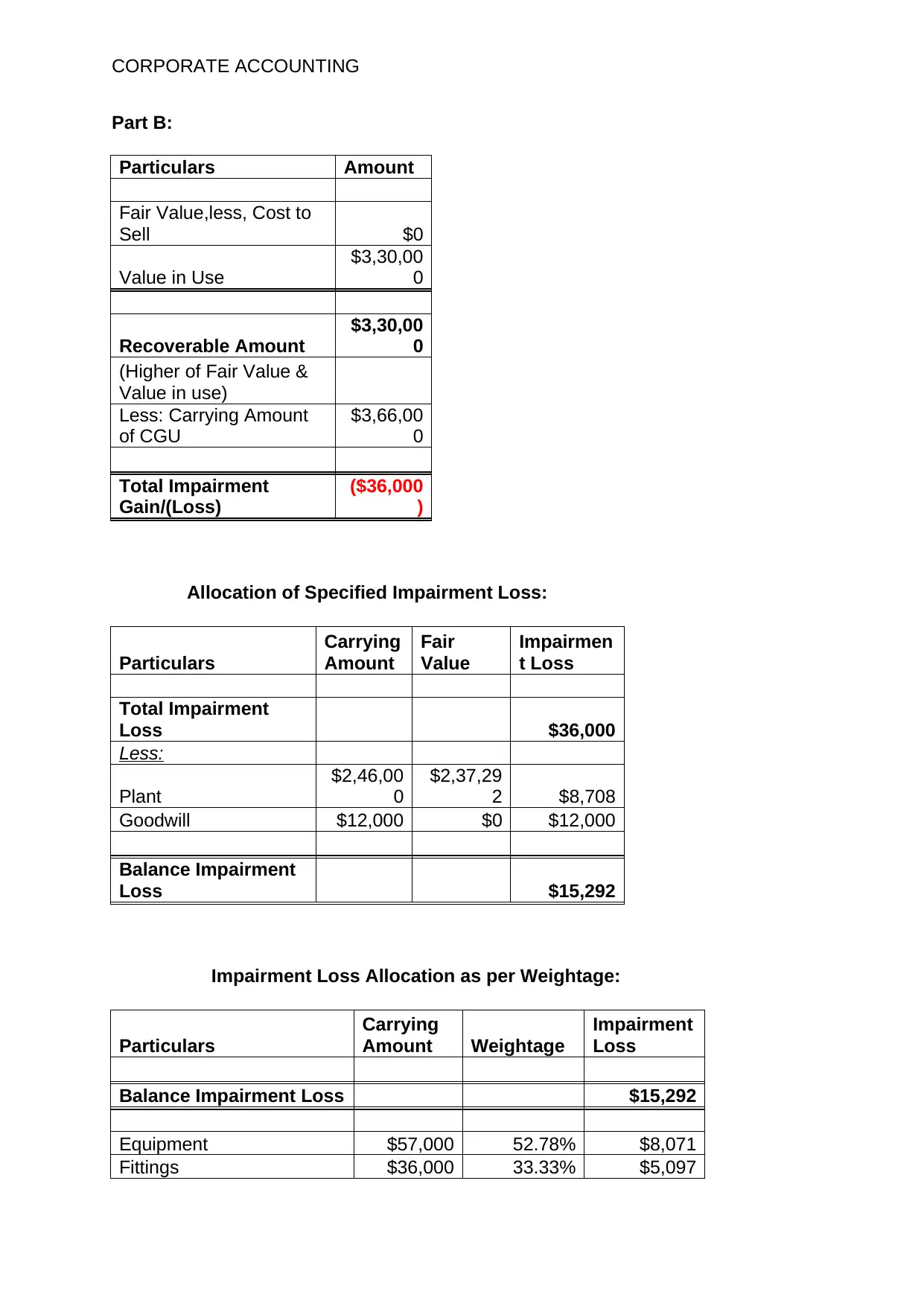

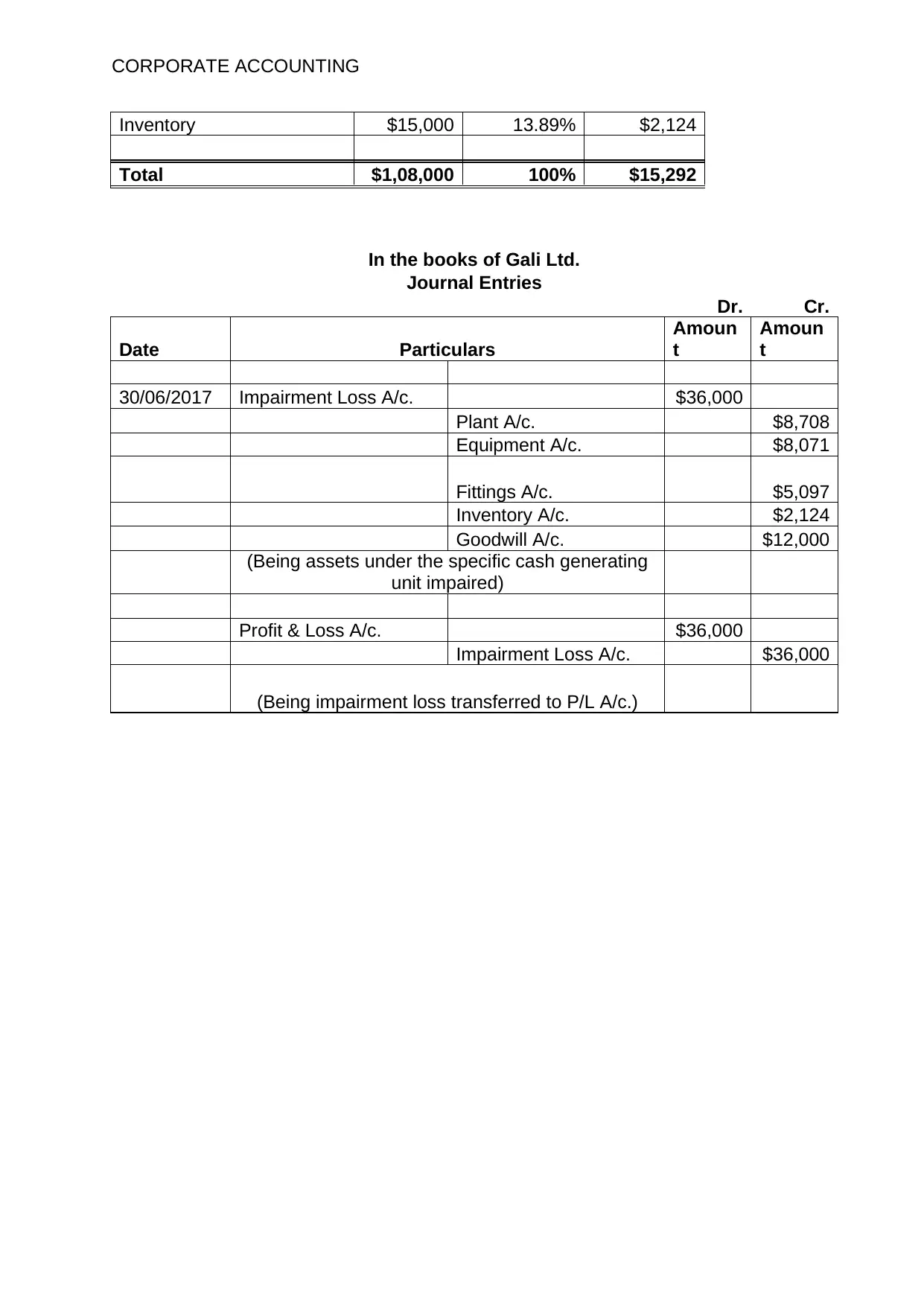

This assignment delves into the intricacies of corporate accounting, specifically addressing the reversal of impairment loss for individual assets under International Accounting Standard 136 (IAS 136). The solution outlines the standard's objective, which is to ensure assets are not carried above their recoverable amount, and its applicability to financial reporting. It details the assessment of impairment indicators from internal and external sources, the assets covered, and the assets excluded. The assignment also explains the reversal of impairment losses, the calculation of recoverable amounts, and the treatment of impairment losses for goodwill. Part B of the assignment provides a practical example with calculations for recoverable amounts, carrying amounts, and impairment loss allocation, including journal entries for Gali Ltd., with relevant references.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.