Corporate Accounting Homework Solution - Semester 1, University Name

VerifiedAdded on 2023/01/06

|10

|1139

|32

Homework Assignment

AI Summary

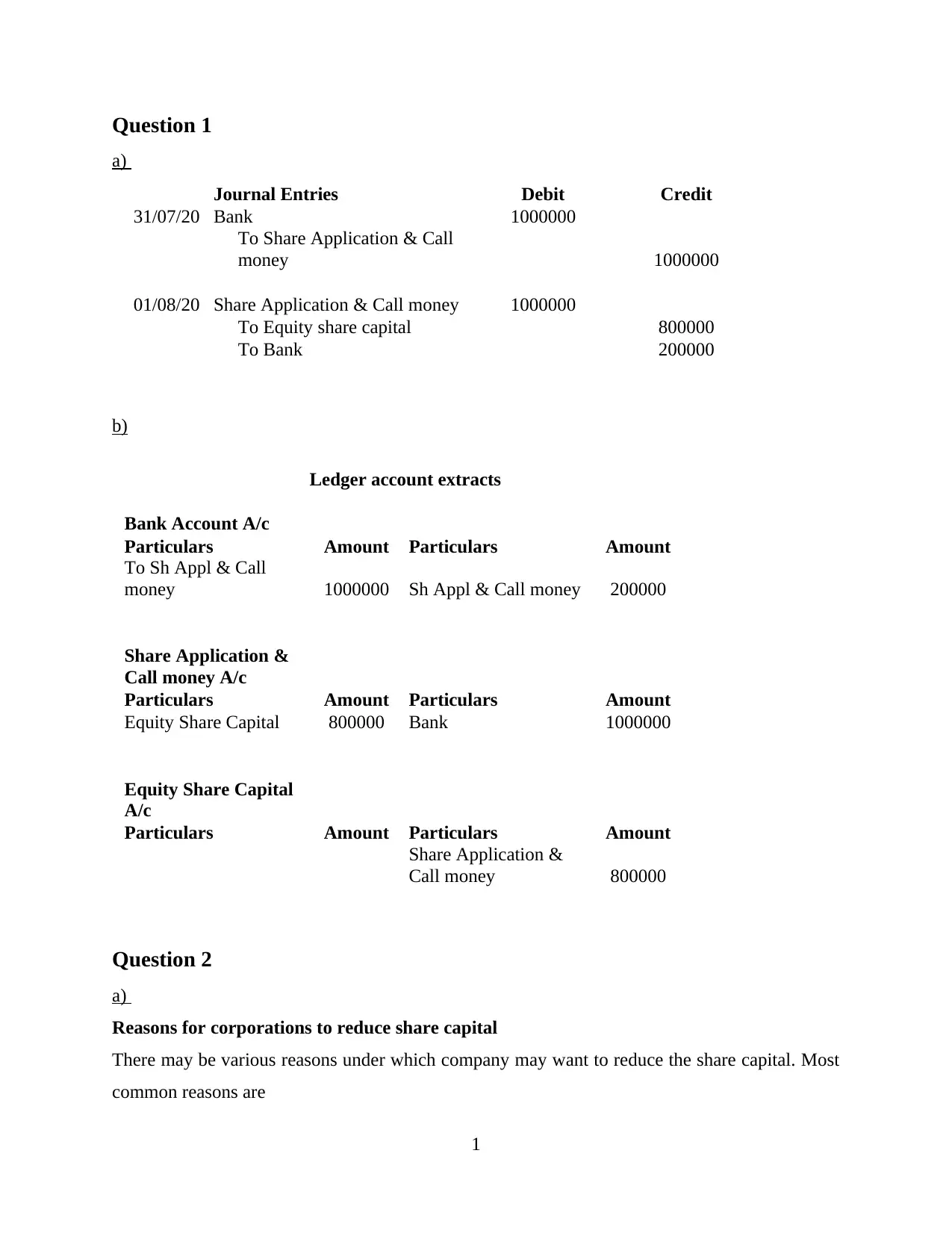

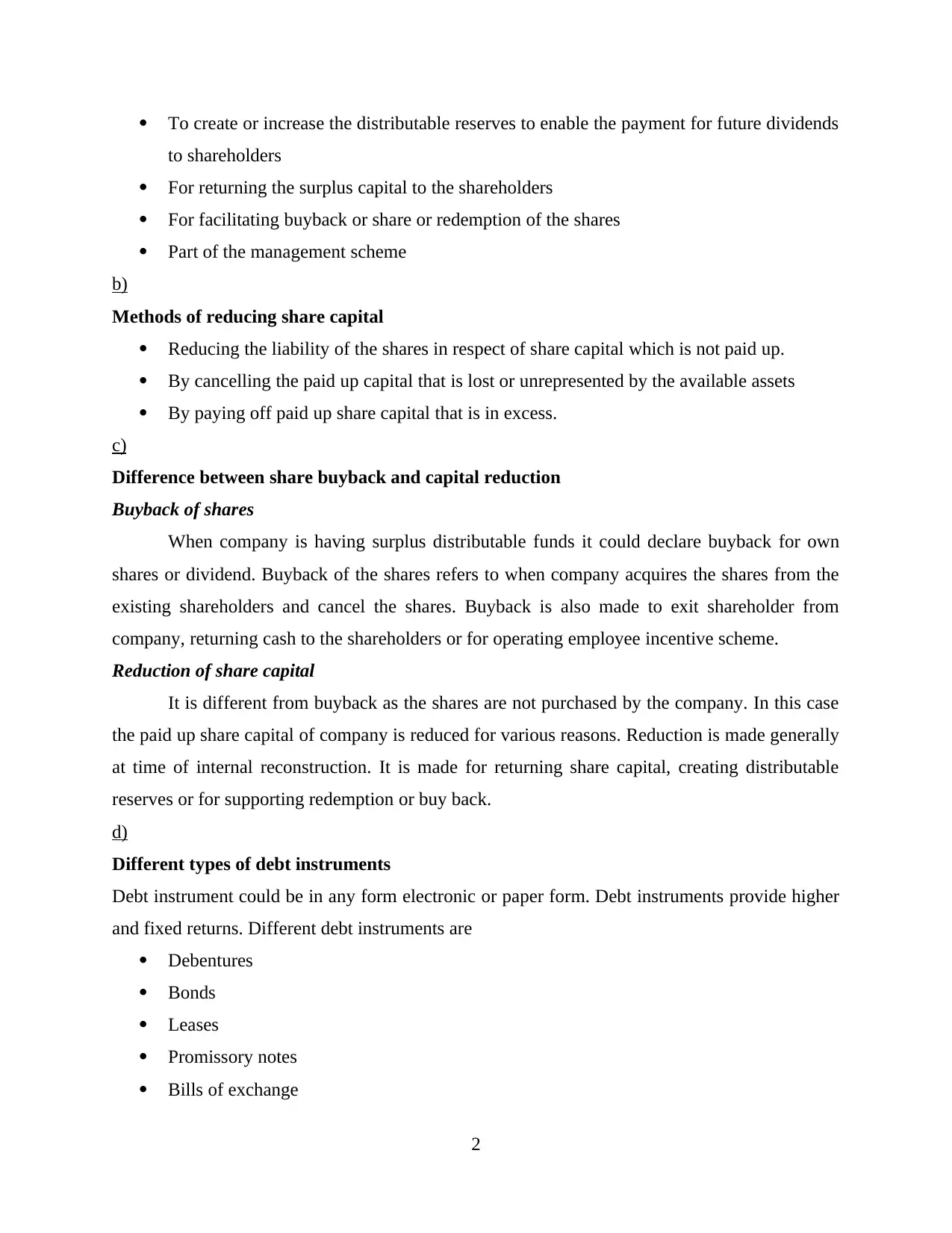

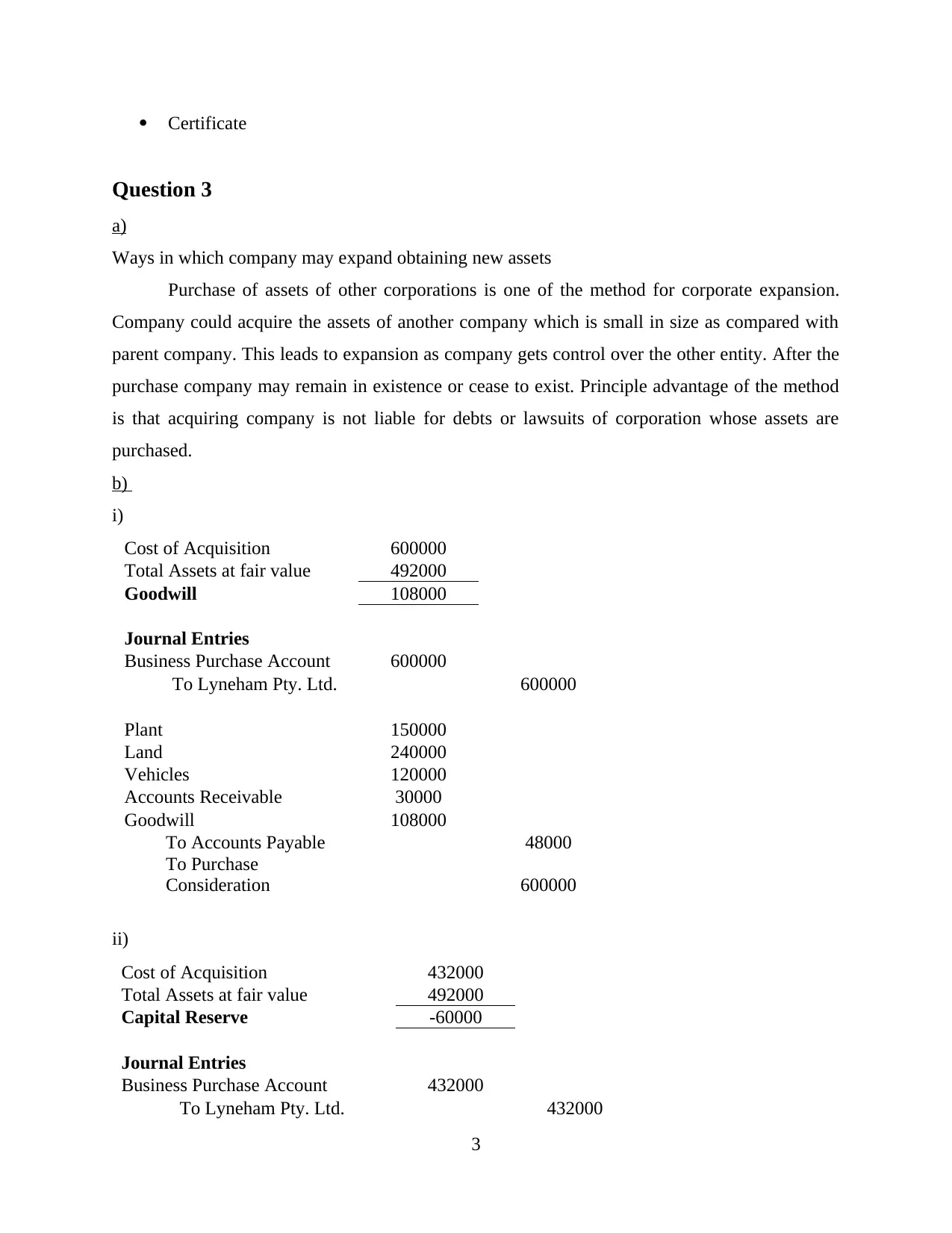

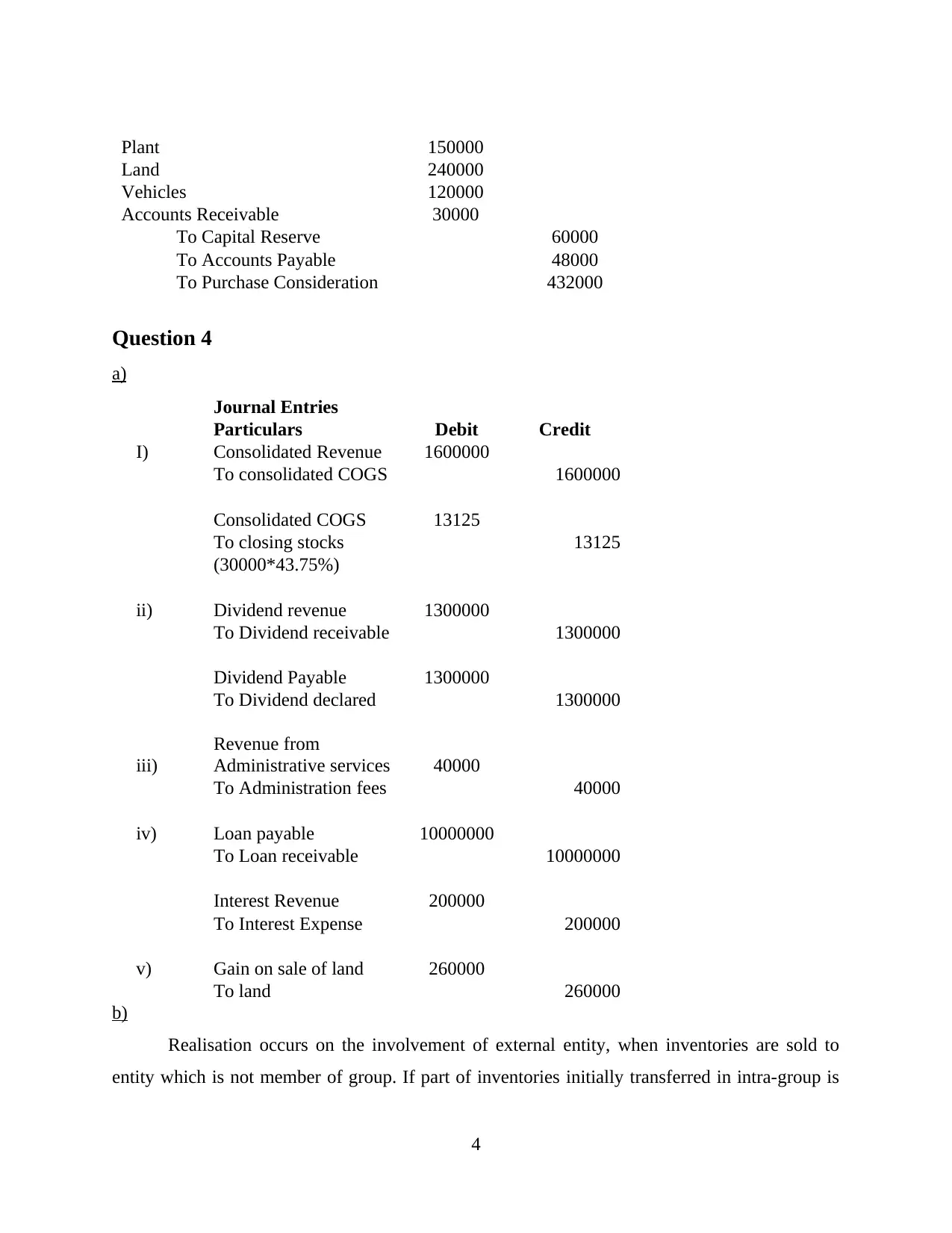

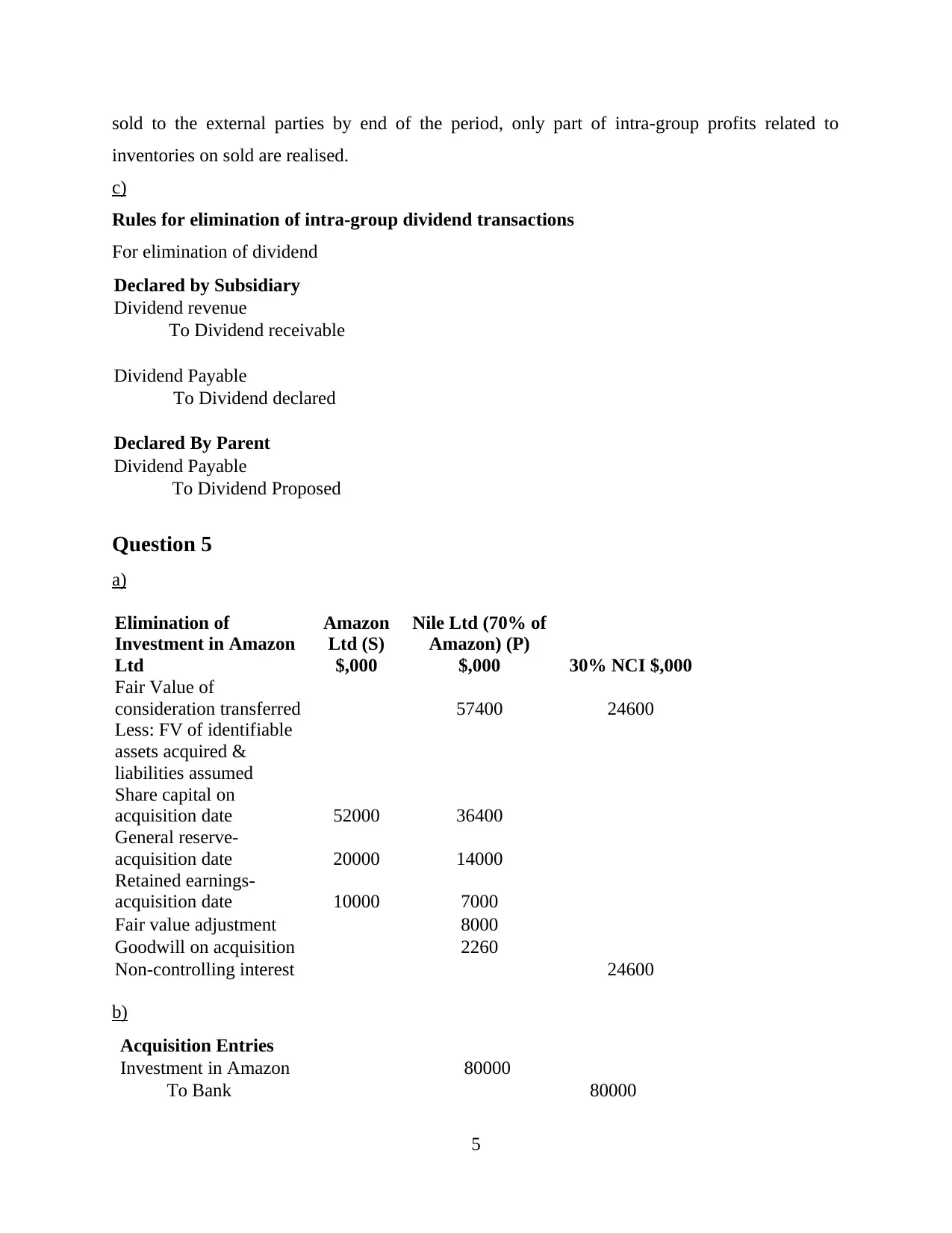

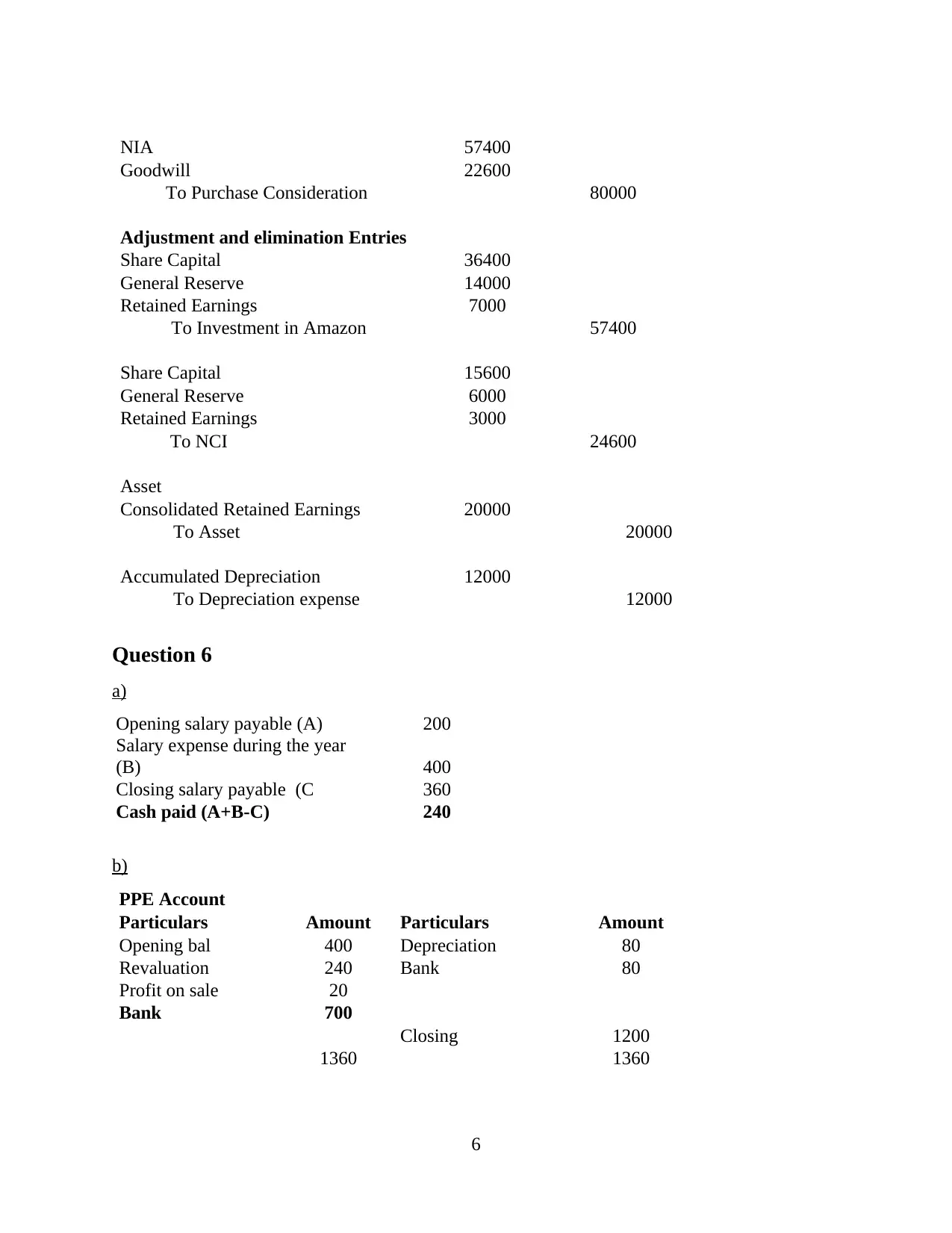

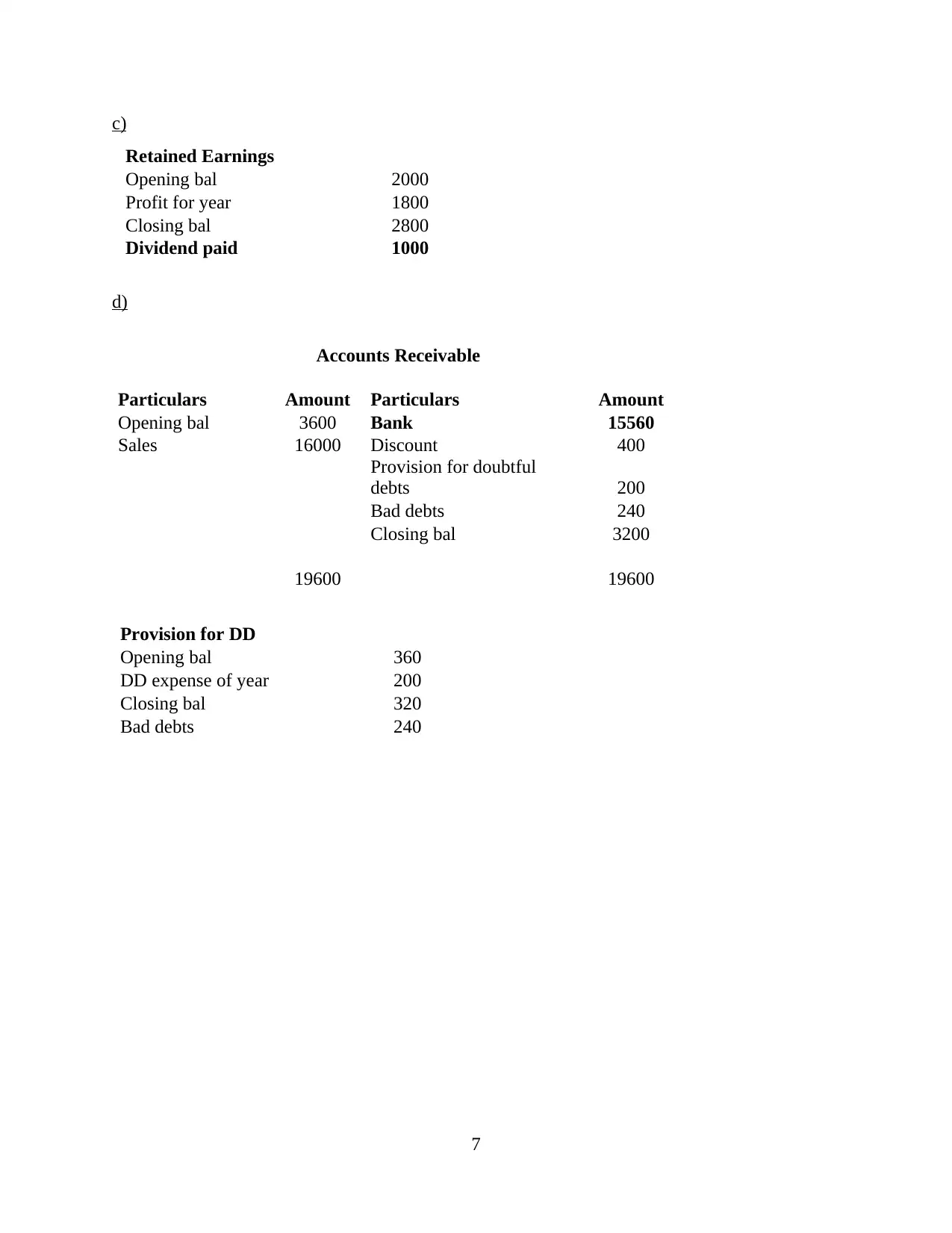

This document presents a comprehensive solution to a corporate accounting homework assignment, covering a range of topics. The solution begins with journal entries and ledger accounts related to share applications and equity share capital. It then delves into the reasons and methods for reducing share capital, differentiating between share buybacks and capital reduction, and outlining different types of debt instruments. The assignment continues with an analysis of corporate expansion through asset acquisition, including journal entries for business purchase and the calculation of goodwill. It also addresses consolidated financial statements, including the elimination of intra-group transactions such as dividends and unrealized profits. The solution provides entries for eliminating investment in subsidiaries, including the calculation of non-controlling interest and acquisition entries. It also addresses financial statement analysis, including salary expense, PPE, retained earnings, and accounts receivable. The assignment concludes with the preparation of relevant journal entries and account extracts.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.