HI5020 Corporate Accounting: Comparative Analysis of ASX Companies

VerifiedAdded on 2023/06/04

|22

|3726

|147

Report

AI Summary

This report provides a comprehensive analysis of two ASX-listed companies, Perpetual Resources Ltd and Hill End Gold Ltd, focusing on their corporate accounting practices. It delves into the owners' equity, comparing contributed equity, retained earnings/accumulated loss, and reserves for both companies across different years. The report also examines the cash flow statements, explaining each item and the reasons for changes in cash flows from operating, investing, and financing activities. A comparative analysis of the companies based on their cash flow statements is presented, followed by a discussion on other comprehensive income. Finally, the report touches upon accounting for corporate income tax, providing a thorough overview of the financial reporting of these two companies. Desklib provides access to similar solved assignments and past papers for students.

CORPORATE ACCOUNTING 1

CORPORATE ACCOUNTING

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING 2

Contents

Executive summary:............................................................................................................................3

Introduction:........................................................................................................................................3

Owners’ equity:...................................................................................................................................3

Part I:...............................................................................................................................................3

Part ii:...............................................................................................................................................6

Cash flow statement:...........................................................................................................................6

Part iii:..............................................................................................................................................6

Part IV:...........................................................................................................................................13

Part v:.............................................................................................................................................14

Other comprehensive income statement:.........................................................................................14

Part VI:...........................................................................................................................................14

Part vii:...........................................................................................................................................15

Part viii:..........................................................................................................................................15

Part ix:............................................................................................................................................15

Accounting for corporate income tax:.............................................................................................15

Part x:.............................................................................................................................................15

Part xi:............................................................................................................................................15

Part xii:...........................................................................................................................................16

Part xiii:..........................................................................................................................................16

Part xiv:..........................................................................................................................................16

Part xv:...........................................................................................................................................17

Part xvi:..........................................................................................................................................18

References:.....................................................................................................................................19

Contents

Executive summary:............................................................................................................................3

Introduction:........................................................................................................................................3

Owners’ equity:...................................................................................................................................3

Part I:...............................................................................................................................................3

Part ii:...............................................................................................................................................6

Cash flow statement:...........................................................................................................................6

Part iii:..............................................................................................................................................6

Part IV:...........................................................................................................................................13

Part v:.............................................................................................................................................14

Other comprehensive income statement:.........................................................................................14

Part VI:...........................................................................................................................................14

Part vii:...........................................................................................................................................15

Part viii:..........................................................................................................................................15

Part ix:............................................................................................................................................15

Accounting for corporate income tax:.............................................................................................15

Part x:.............................................................................................................................................15

Part xi:............................................................................................................................................15

Part xii:...........................................................................................................................................16

Part xiii:..........................................................................................................................................16

Part xiv:..........................................................................................................................................16

Part xv:...........................................................................................................................................17

Part xvi:..........................................................................................................................................18

References:.....................................................................................................................................19

CORPORATE ACCOUNTING 3

Executive summary:

This assignment has been prepared to make a brief analysis of two ASX listed companies

belongs to the same industry. The selected companies are Perpetual Resources Ltd and Hill

End Gold Ltd. In this report, we will discuss the cash flow statement, owner’s equity,

effective tax rate etc. On the basis of the annual report of the selected companies, we have

analyzed the transaction reported by the company.

Executive summary:

This assignment has been prepared to make a brief analysis of two ASX listed companies

belongs to the same industry. The selected companies are Perpetual Resources Ltd and Hill

End Gold Ltd. In this report, we will discuss the cash flow statement, owner’s equity,

effective tax rate etc. On the basis of the annual report of the selected companies, we have

analyzed the transaction reported by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING 4

Introduction:

In the present era there is huge improvement in the reporting of the financial transaction of

the company. The users of the financial statement through reading and analysing of the

financial statement can obtain the insight of the business. In the report we will analyse the

reporting of the shareholder equity of the Perpetual Resource limited and Hill End Gold Ltd

and changes in the item over the past. It also analysis changes in the debt position of the

company in the recent past. Further the report discusses the items of the cash flow and the

way liquidity position of the company can be identified through analysing each item of the

equity. The report also states the reporting of the other comprehensive statement of both the

company and the reason why the items are not reported as regular operation. The reporting of

the taxation of the both the company can also be understood in the report.

Perpetual Resources Ltd

Perpetual Resources Limited was founded in the year 2011 with headquarter situated at

NSW, Australia. The company as nagged in the business of exploration of the gold project.

The main purpose or focus of the company is to implement the exploration and development

of a program for A to Z project.

Hill End Gold Ltd

The company has been founded in the year 1996 with headquartered situated at Sydney,

Australia. Hill End Gold Ltd is also spread geographically with their subsidiaries such as

Pure Alumina Pty Ltd, Hegel Investments Pty Ltd. The company has mainly been engaged in

the exploration of gold across Australia (Hillendgold.com.au. 2018).

Owners’ equity:

Part I:

As required, the following table briefly interprets the Owner’s Equity of the selected

companies:

Perpetual Resources Ltd

Owner's equity:

(Amounts in $000 )

Particulars 2017 2016 Understanding Change Ch

ang

Introduction:

In the present era there is huge improvement in the reporting of the financial transaction of

the company. The users of the financial statement through reading and analysing of the

financial statement can obtain the insight of the business. In the report we will analyse the

reporting of the shareholder equity of the Perpetual Resource limited and Hill End Gold Ltd

and changes in the item over the past. It also analysis changes in the debt position of the

company in the recent past. Further the report discusses the items of the cash flow and the

way liquidity position of the company can be identified through analysing each item of the

equity. The report also states the reporting of the other comprehensive statement of both the

company and the reason why the items are not reported as regular operation. The reporting of

the taxation of the both the company can also be understood in the report.

Perpetual Resources Ltd

Perpetual Resources Limited was founded in the year 2011 with headquarter situated at

NSW, Australia. The company as nagged in the business of exploration of the gold project.

The main purpose or focus of the company is to implement the exploration and development

of a program for A to Z project.

Hill End Gold Ltd

The company has been founded in the year 1996 with headquartered situated at Sydney,

Australia. Hill End Gold Ltd is also spread geographically with their subsidiaries such as

Pure Alumina Pty Ltd, Hegel Investments Pty Ltd. The company has mainly been engaged in

the exploration of gold across Australia (Hillendgold.com.au. 2018).

Owners’ equity:

Part I:

As required, the following table briefly interprets the Owner’s Equity of the selected

companies:

Perpetual Resources Ltd

Owner's equity:

(Amounts in $000 )

Particulars 2017 2016 Understanding Change Ch

ang

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

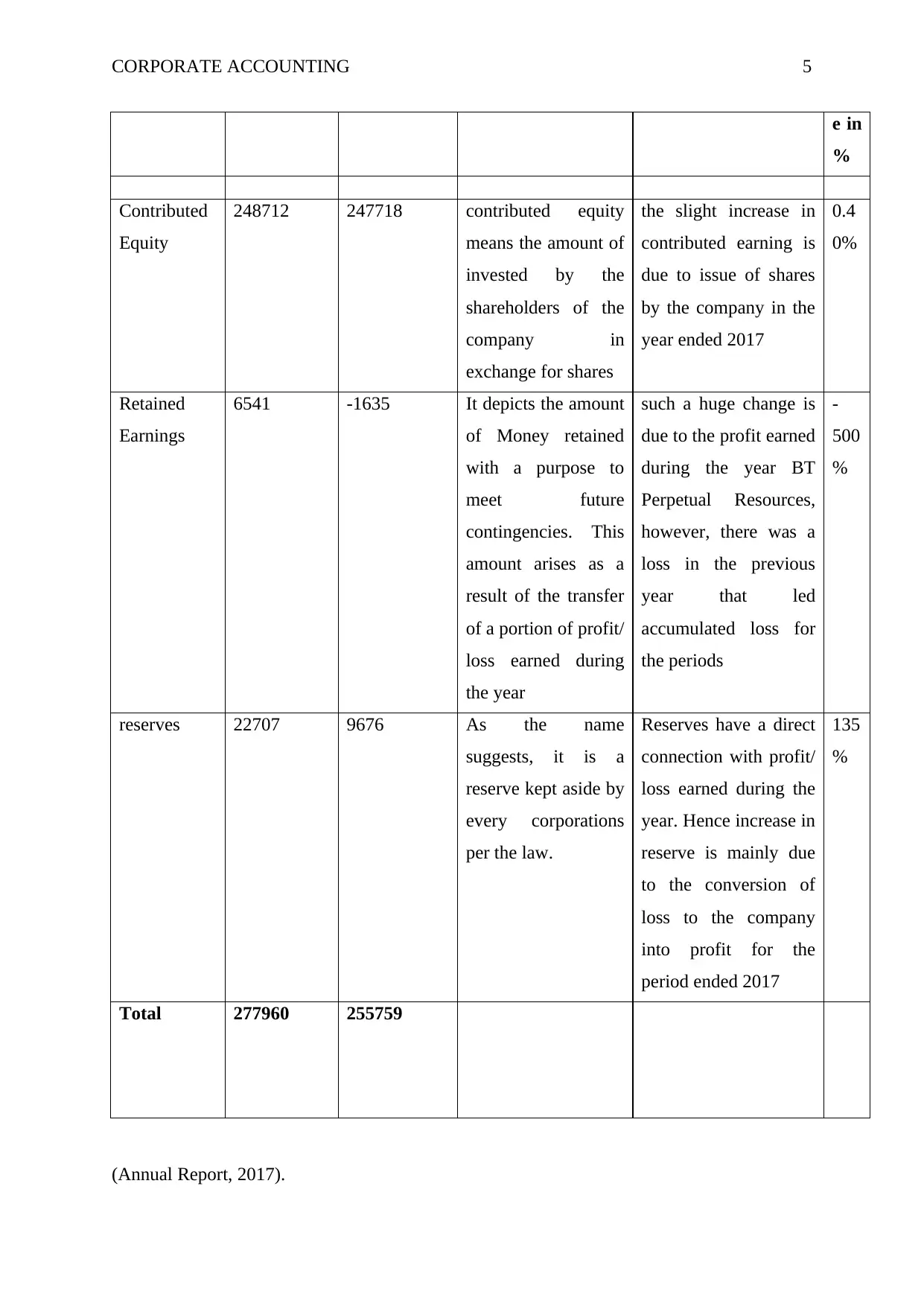

CORPORATE ACCOUNTING 5

e in

%

Contributed

Equity

248712 247718 contributed equity

means the amount of

invested by the

shareholders of the

company in

exchange for shares

the slight increase in

contributed earning is

due to issue of shares

by the company in the

year ended 2017

0.4

0%

Retained

Earnings

6541 -1635 It depicts the amount

of Money retained

with a purpose to

meet future

contingencies. This

amount arises as a

result of the transfer

of a portion of profit/

loss earned during

the year

such a huge change is

due to the profit earned

during the year BT

Perpetual Resources,

however, there was a

loss in the previous

year that led

accumulated loss for

the periods

-

500

%

reserves 22707 9676 As the name

suggests, it is a

reserve kept aside by

every corporations

per the law.

Reserves have a direct

connection with profit/

loss earned during the

year. Hence increase in

reserve is mainly due

to the conversion of

loss to the company

into profit for the

period ended 2017

135

%

Total 277960 255759

(Annual Report, 2017).

e in

%

Contributed

Equity

248712 247718 contributed equity

means the amount of

invested by the

shareholders of the

company in

exchange for shares

the slight increase in

contributed earning is

due to issue of shares

by the company in the

year ended 2017

0.4

0%

Retained

Earnings

6541 -1635 It depicts the amount

of Money retained

with a purpose to

meet future

contingencies. This

amount arises as a

result of the transfer

of a portion of profit/

loss earned during

the year

such a huge change is

due to the profit earned

during the year BT

Perpetual Resources,

however, there was a

loss in the previous

year that led

accumulated loss for

the periods

-

500

%

reserves 22707 9676 As the name

suggests, it is a

reserve kept aside by

every corporations

per the law.

Reserves have a direct

connection with profit/

loss earned during the

year. Hence increase in

reserve is mainly due

to the conversion of

loss to the company

into profit for the

period ended 2017

135

%

Total 277960 255759

(Annual Report, 2017).

CORPORATE ACCOUNTING 6

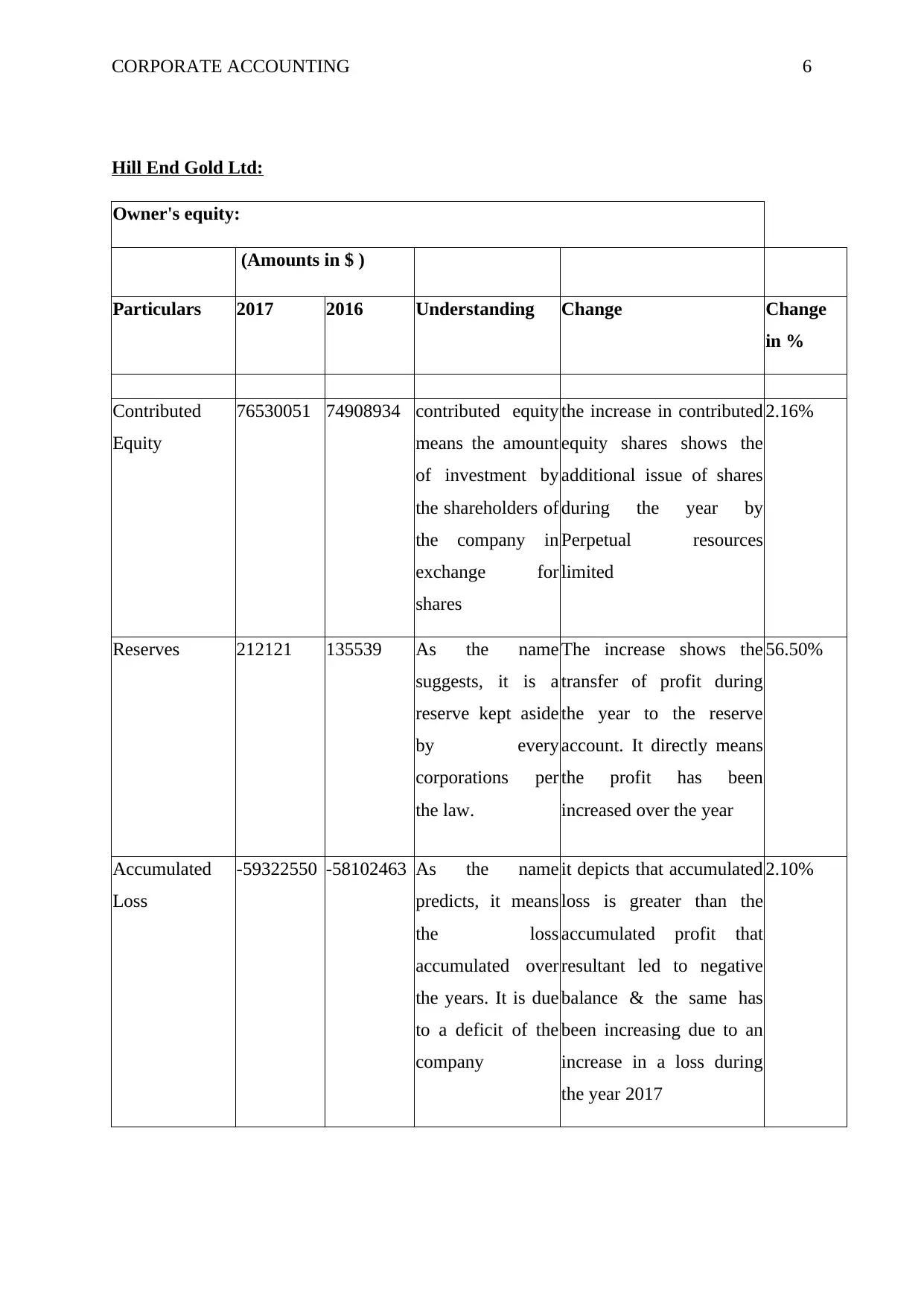

Hill End Gold Ltd:

Owner's equity:

(Amounts in $ )

Particulars 2017 2016 Understanding Change Change

in %

Contributed

Equity

76530051 74908934 contributed equity

means the amount

of investment by

the shareholders of

the company in

exchange for

shares

the increase in contributed

equity shares shows the

additional issue of shares

during the year by

Perpetual resources

limited

2.16%

Reserves 212121 135539 As the name

suggests, it is a

reserve kept aside

by every

corporations per

the law.

The increase shows the

transfer of profit during

the year to the reserve

account. It directly means

the profit has been

increased over the year

56.50%

Accumulated

Loss

-59322550 -58102463 As the name

predicts, it means

the loss

accumulated over

the years. It is due

to a deficit of the

company

it depicts that accumulated

loss is greater than the

accumulated profit that

resultant led to negative

balance & the same has

been increasing due to an

increase in a loss during

the year 2017

2.10%

Hill End Gold Ltd:

Owner's equity:

(Amounts in $ )

Particulars 2017 2016 Understanding Change Change

in %

Contributed

Equity

76530051 74908934 contributed equity

means the amount

of investment by

the shareholders of

the company in

exchange for

shares

the increase in contributed

equity shares shows the

additional issue of shares

during the year by

Perpetual resources

limited

2.16%

Reserves 212121 135539 As the name

suggests, it is a

reserve kept aside

by every

corporations per

the law.

The increase shows the

transfer of profit during

the year to the reserve

account. It directly means

the profit has been

increased over the year

56.50%

Accumulated

Loss

-59322550 -58102463 As the name

predicts, it means

the loss

accumulated over

the years. It is due

to a deficit of the

company

it depicts that accumulated

loss is greater than the

accumulated profit that

resultant led to negative

balance & the same has

been increasing due to an

increase in a loss during

the year 2017

2.10%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE ACCOUNTING 7

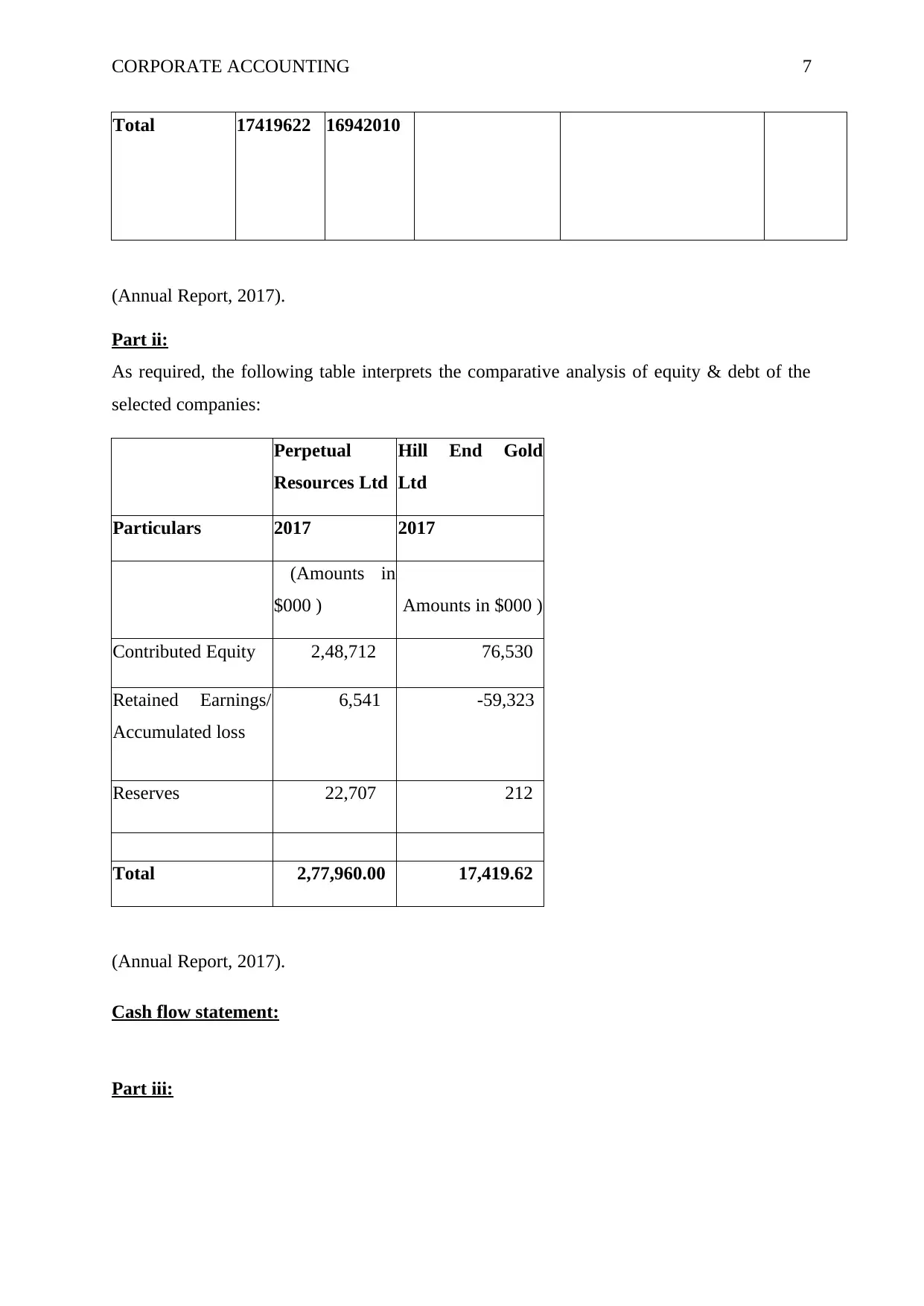

Total 17419622 16942010

(Annual Report, 2017).

Part ii:

As required, the following table interprets the comparative analysis of equity & debt of the

selected companies:

Perpetual

Resources Ltd

Hill End Gold

Ltd

Particulars 2017 2017

(Amounts in

$000 ) Amounts in $000 )

Contributed Equity 2,48,712 76,530

Retained Earnings/

Accumulated loss

6,541 -59,323

Reserves 22,707 212

Total 2,77,960.00 17,419.62

(Annual Report, 2017).

Cash flow statement:

Part iii:

Total 17419622 16942010

(Annual Report, 2017).

Part ii:

As required, the following table interprets the comparative analysis of equity & debt of the

selected companies:

Perpetual

Resources Ltd

Hill End Gold

Ltd

Particulars 2017 2017

(Amounts in

$000 ) Amounts in $000 )

Contributed Equity 2,48,712 76,530

Retained Earnings/

Accumulated loss

6,541 -59,323

Reserves 22,707 212

Total 2,77,960.00 17,419.62

(Annual Report, 2017).

Cash flow statement:

Part iii:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING 8

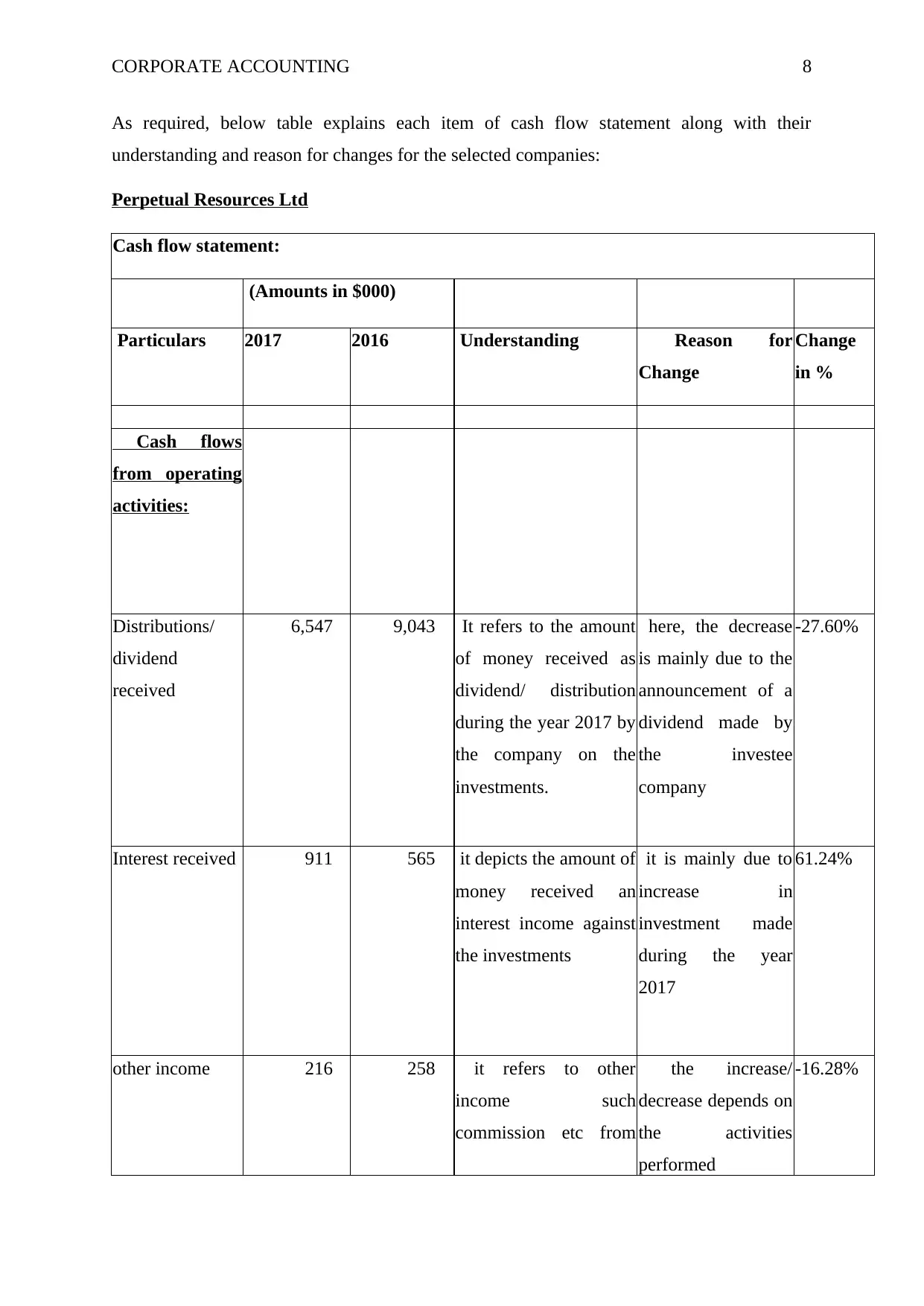

As required, below table explains each item of cash flow statement along with their

understanding and reason for changes for the selected companies:

Perpetual Resources Ltd

Cash flow statement:

(Amounts in $000)

Particulars 2017 2016 Understanding Reason for

Change

Change

in %

Cash flows

from operating

activities:

Distributions/

dividend

received

6,547 9,043 It refers to the amount

of money received as

dividend/ distribution

during the year 2017 by

the company on the

investments.

here, the decrease

is mainly due to the

announcement of a

dividend made by

the investee

company

-27.60%

Interest received 911 565 it depicts the amount of

money received an

interest income against

the investments

it is mainly due to

increase in

investment made

during the year

2017

61.24%

other income 216 258 it refers to other

income such

commission etc from

the increase/

decrease depends on

the activities

performed

-16.28%

As required, below table explains each item of cash flow statement along with their

understanding and reason for changes for the selected companies:

Perpetual Resources Ltd

Cash flow statement:

(Amounts in $000)

Particulars 2017 2016 Understanding Reason for

Change

Change

in %

Cash flows

from operating

activities:

Distributions/

dividend

received

6,547 9,043 It refers to the amount

of money received as

dividend/ distribution

during the year 2017 by

the company on the

investments.

here, the decrease

is mainly due to the

announcement of a

dividend made by

the investee

company

-27.60%

Interest received 911 565 it depicts the amount of

money received an

interest income against

the investments

it is mainly due to

increase in

investment made

during the year

2017

61.24%

other income 216 258 it refers to other

income such

commission etc from

the increase/

decrease depends on

the activities

performed

-16.28%

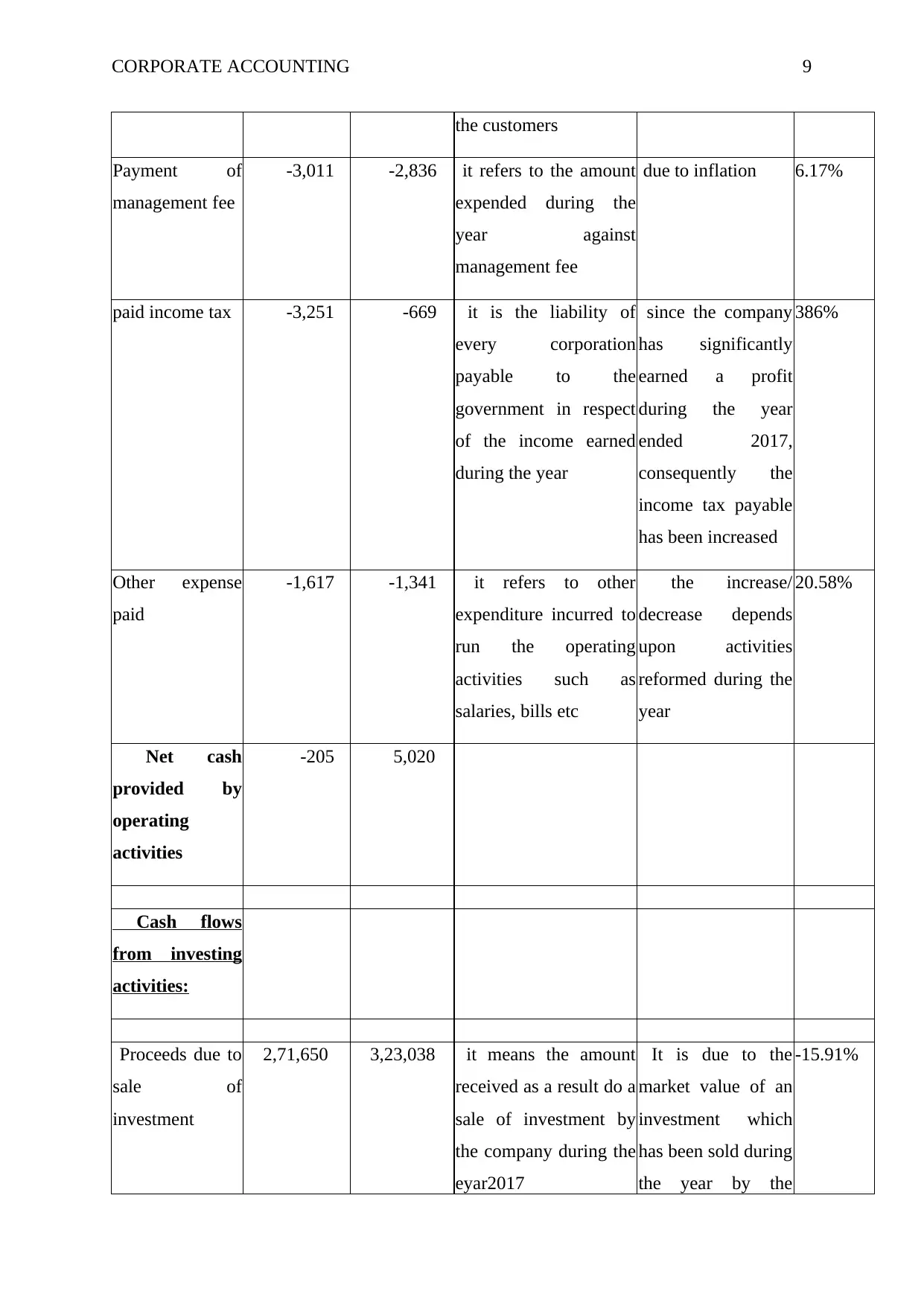

CORPORATE ACCOUNTING 9

the customers

Payment of

management fee

-3,011 -2,836 it refers to the amount

expended during the

year against

management fee

due to inflation 6.17%

paid income tax -3,251 -669 it is the liability of

every corporation

payable to the

government in respect

of the income earned

during the year

since the company

has significantly

earned a profit

during the year

ended 2017,

consequently the

income tax payable

has been increased

386%

Other expense

paid

-1,617 -1,341 it refers to other

expenditure incurred to

run the operating

activities such as

salaries, bills etc

the increase/

decrease depends

upon activities

reformed during the

year

20.58%

Net cash

provided by

operating

activities

-205 5,020

Cash flows

from investing

activities:

Proceeds due to

sale of

investment

2,71,650 3,23,038 it means the amount

received as a result do a

sale of investment by

the company during the

eyar2017

It is due to the

market value of an

investment which

has been sold during

the year by the

-15.91%

the customers

Payment of

management fee

-3,011 -2,836 it refers to the amount

expended during the

year against

management fee

due to inflation 6.17%

paid income tax -3,251 -669 it is the liability of

every corporation

payable to the

government in respect

of the income earned

during the year

since the company

has significantly

earned a profit

during the year

ended 2017,

consequently the

income tax payable

has been increased

386%

Other expense

paid

-1,617 -1,341 it refers to other

expenditure incurred to

run the operating

activities such as

salaries, bills etc

the increase/

decrease depends

upon activities

reformed during the

year

20.58%

Net cash

provided by

operating

activities

-205 5,020

Cash flows

from investing

activities:

Proceeds due to

sale of

investment

2,71,650 3,23,038 it means the amount

received as a result do a

sale of investment by

the company during the

eyar2017

It is due to the

market value of an

investment which

has been sold during

the year by the

-15.91%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

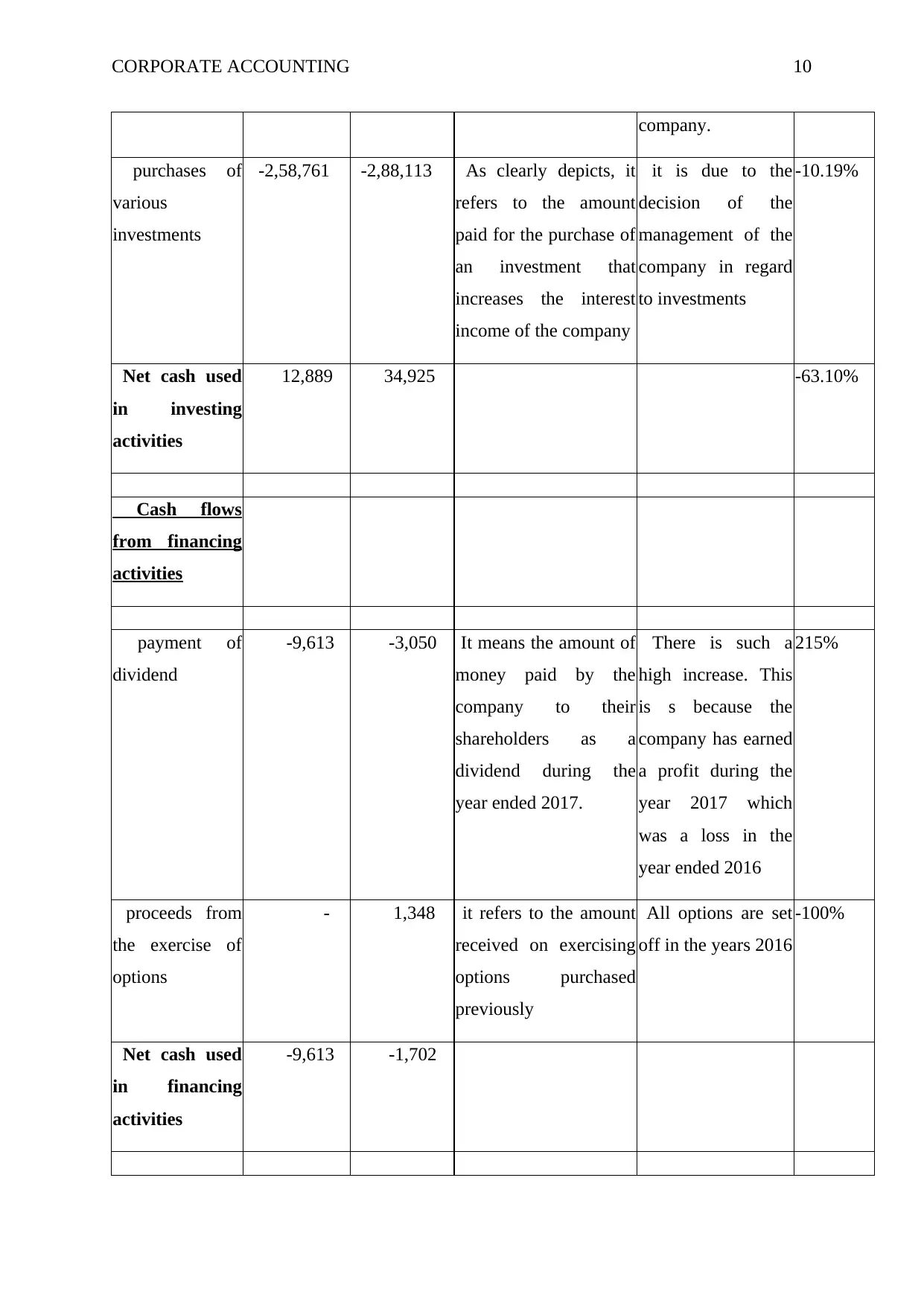

CORPORATE ACCOUNTING 10

company.

purchases of

various

investments

-2,58,761 -2,88,113 As clearly depicts, it

refers to the amount

paid for the purchase of

an investment that

increases the interest

income of the company

it is due to the

decision of the

management of the

company in regard

to investments

-10.19%

Net cash used

in investing

activities

12,889 34,925 -63.10%

Cash flows

from financing

activities

payment of

dividend

-9,613 -3,050 It means the amount of

money paid by the

company to their

shareholders as a

dividend during the

year ended 2017.

There is such a

high increase. This

is s because the

company has earned

a profit during the

year 2017 which

was a loss in the

year ended 2016

215%

proceeds from

the exercise of

options

- 1,348 it refers to the amount

received on exercising

options purchased

previously

All options are set

off in the years 2016

-100%

Net cash used

in financing

activities

-9,613 -1,702

company.

purchases of

various

investments

-2,58,761 -2,88,113 As clearly depicts, it

refers to the amount

paid for the purchase of

an investment that

increases the interest

income of the company

it is due to the

decision of the

management of the

company in regard

to investments

-10.19%

Net cash used

in investing

activities

12,889 34,925 -63.10%

Cash flows

from financing

activities

payment of

dividend

-9,613 -3,050 It means the amount of

money paid by the

company to their

shareholders as a

dividend during the

year ended 2017.

There is such a

high increase. This

is s because the

company has earned

a profit during the

year 2017 which

was a loss in the

year ended 2016

215%

proceeds from

the exercise of

options

- 1,348 it refers to the amount

received on exercising

options purchased

previously

All options are set

off in the years 2016

-100%

Net cash used

in financing

activities

-9,613 -1,702

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE ACCOUNTING 11

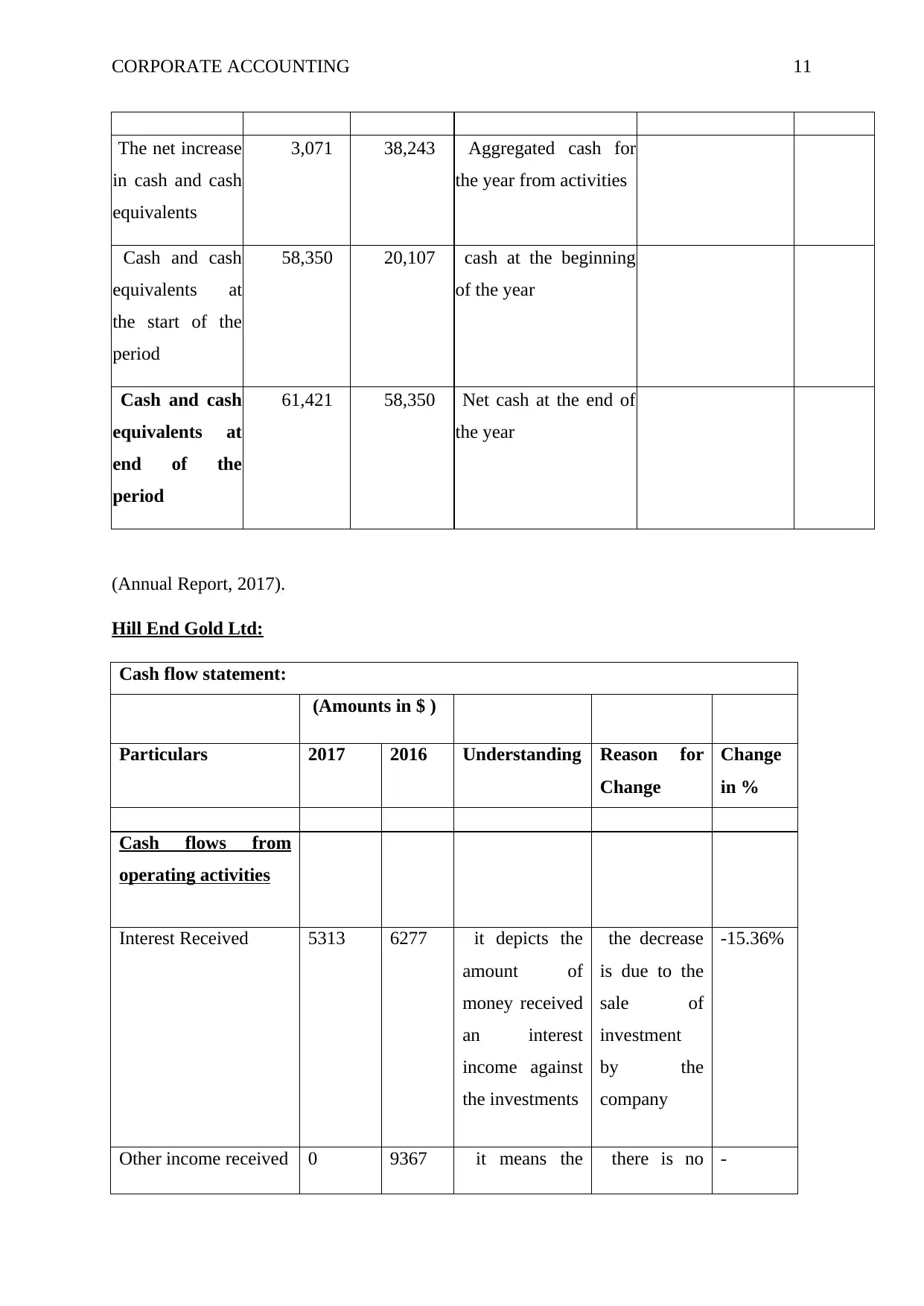

The net increase

in cash and cash

equivalents

3,071 38,243 Aggregated cash for

the year from activities

Cash and cash

equivalents at

the start of the

period

58,350 20,107 cash at the beginning

of the year

Cash and cash

equivalents at

end of the

period

61,421 58,350 Net cash at the end of

the year

(Annual Report, 2017).

Hill End Gold Ltd:

Cash flow statement:

(Amounts in $ )

Particulars 2017 2016 Understanding Reason for

Change

Change

in %

Cash flows from

operating activities

Interest Received 5313 6277 it depicts the

amount of

money received

an interest

income against

the investments

the decrease

is due to the

sale of

investment

by the

company

-15.36%

Other income received 0 9367 it means the there is no -

The net increase

in cash and cash

equivalents

3,071 38,243 Aggregated cash for

the year from activities

Cash and cash

equivalents at

the start of the

period

58,350 20,107 cash at the beginning

of the year

Cash and cash

equivalents at

end of the

period

61,421 58,350 Net cash at the end of

the year

(Annual Report, 2017).

Hill End Gold Ltd:

Cash flow statement:

(Amounts in $ )

Particulars 2017 2016 Understanding Reason for

Change

Change

in %

Cash flows from

operating activities

Interest Received 5313 6277 it depicts the

amount of

money received

an interest

income against

the investments

the decrease

is due to the

sale of

investment

by the

company

-15.36%

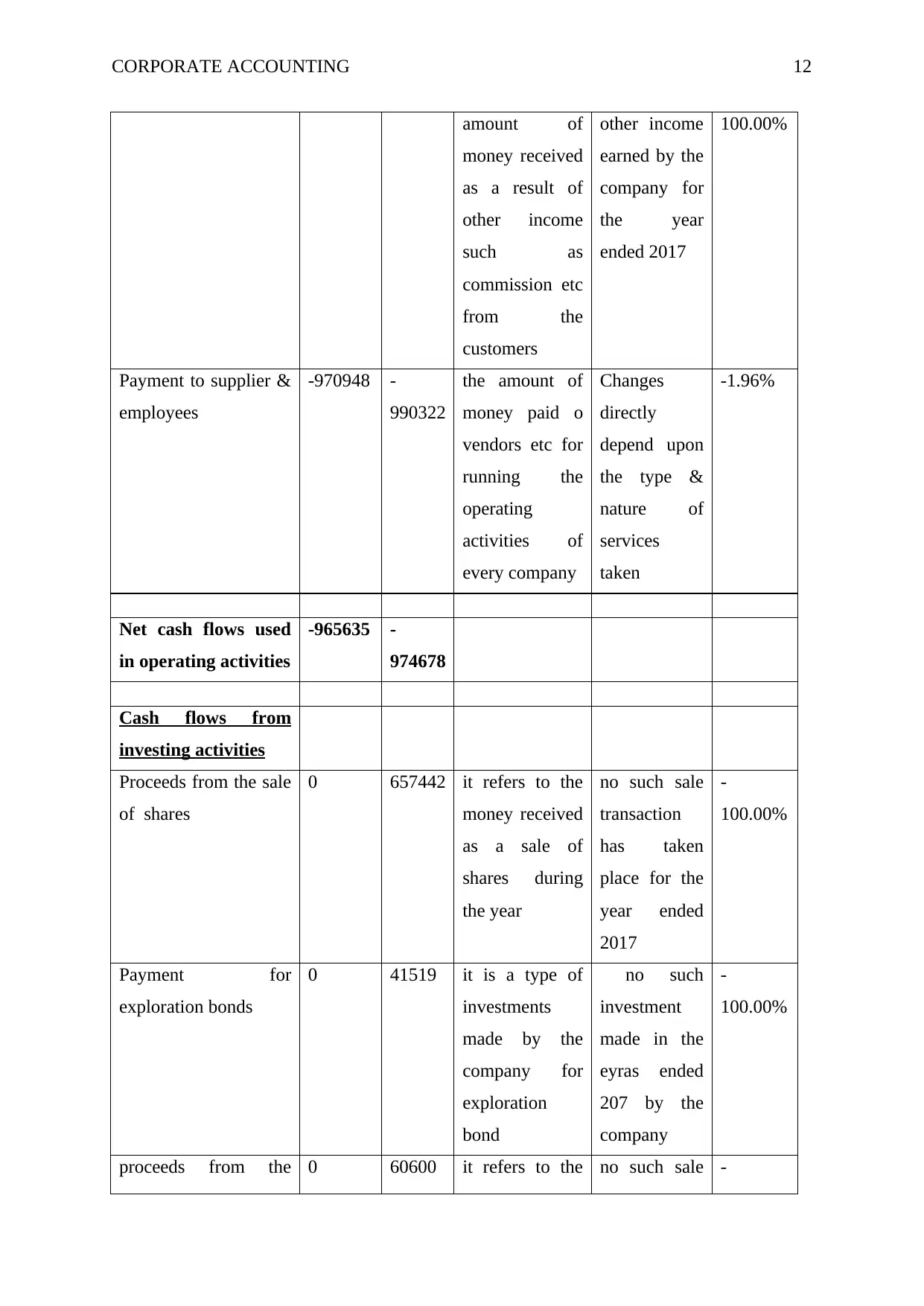

Other income received 0 9367 it means the there is no -

CORPORATE ACCOUNTING 12

amount of

money received

as a result of

other income

such as

commission etc

from the

customers

other income

earned by the

company for

the year

ended 2017

100.00%

Payment to supplier &

employees

-970948 -

990322

the amount of

money paid o

vendors etc for

running the

operating

activities of

every company

Changes

directly

depend upon

the type &

nature of

services

taken

-1.96%

Net cash flows used

in operating activities

-965635 -

974678

Cash flows from

investing activities

Proceeds from the sale

of shares

0 657442 it refers to the

money received

as a sale of

shares during

the year

no such sale

transaction

has taken

place for the

year ended

2017

-

100.00%

Payment for

exploration bonds

0 41519 it is a type of

investments

made by the

company for

exploration

bond

no such

investment

made in the

eyras ended

207 by the

company

-

100.00%

proceeds from the 0 60600 it refers to the no such sale -

amount of

money received

as a result of

other income

such as

commission etc

from the

customers

other income

earned by the

company for

the year

ended 2017

100.00%

Payment to supplier &

employees

-970948 -

990322

the amount of

money paid o

vendors etc for

running the

operating

activities of

every company

Changes

directly

depend upon

the type &

nature of

services

taken

-1.96%

Net cash flows used

in operating activities

-965635 -

974678

Cash flows from

investing activities

Proceeds from the sale

of shares

0 657442 it refers to the

money received

as a sale of

shares during

the year

no such sale

transaction

has taken

place for the

year ended

2017

-

100.00%

Payment for

exploration bonds

0 41519 it is a type of

investments

made by the

company for

exploration

bond

no such

investment

made in the

eyras ended

207 by the

company

-

100.00%

proceeds from the 0 60600 it refers to the no such sale -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.