University Corporate Accounting: Financial Analysis of Four Banks

VerifiedAdded on 2023/06/05

|12

|2787

|190

Report

AI Summary

This report provides a comprehensive financial analysis of four banks, focusing on corporate accounting principles. It begins with an executive summary and an introduction outlining the scope of the analysis. The report delves into corporate regulations and accounting standards, emphasizing the importance of transparency and adherence to IFRS. It examines the roles of shareholders, the significance of financial reports, and the function of accounting standard-setting bodies like the AASB and IASB. The core of the report analyzes the owners' equity of the selected banks, including share capital, reserves, and retained earnings. It presents detailed data from 2014 to 2017, comparing the financial positions of each bank. Furthermore, the report investigates the debt and equity positions of the firms, assessing their financial leverage and cost of capital. The analysis covers AMP, Commonwealth Bank, Westpac, and Bendigo and Adelaide, highlighting their capital structures and providing insights into their financial health. The conclusion summarizes the key findings and implications of the analysis, offering a valuable overview of the banks' financial performance and compliance with accounting standards. This report is a valuable resource for anyone interested in understanding corporate accounting and the financial dynamics of the banking sector.

Corporate Accounting

Financial Analysis of four Banks

Financial analysis

[Type the author name]

University Name-

Financial Analysis of four Banks

Financial analysis

[Type the author name]

University Name-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Financial information is now completely noteworthy from past some years for

companies due to enlarged convolution in the businesses. Shareholders need annual reports of

the company so that they determine their progress and invest accordingly. This report has

revealed the key information which could be used by readers to determine the optimum

capital structure.

Financial information is now completely noteworthy from past some years for

companies due to enlarged convolution in the businesses. Shareholders need annual reports of

the company so that they determine their progress and invest accordingly. This report has

revealed the key information which could be used by readers to determine the optimum

capital structure.

Table of Contents

Executive Summary...............................................................................................................................2

Introduction...........................................................................................................................................4

Answer to question no-1........................................................................................................................4

CORPORATE REGULATION.............................................................................................................4

Answer to question no-2........................................................................................................................5

ACCOUNTING STANDARD SETTING.............................................................................................5

Answer to question no-3........................................................................................................................6

Owners’ Equity......................................................................................................................................6

Ordinary Share capital.......................................................................................................................8

Other Equity Instruments and retained earning..................................................................................8

Reserves............................................................................................................................................8

Retained profits.................................................................................................................................9

Answer to question no-4........................................................................................................................9

Debt and equity position of the four firms that you have selected.......................................................9

Conclusion.......................................................................................................................................10

References...........................................................................................................................................11

Executive Summary...............................................................................................................................2

Introduction...........................................................................................................................................4

Answer to question no-1........................................................................................................................4

CORPORATE REGULATION.............................................................................................................4

Answer to question no-2........................................................................................................................5

ACCOUNTING STANDARD SETTING.............................................................................................5

Answer to question no-3........................................................................................................................6

Owners’ Equity......................................................................................................................................6

Ordinary Share capital.......................................................................................................................8

Other Equity Instruments and retained earning..................................................................................8

Reserves............................................................................................................................................8

Retained profits.................................................................................................................................9

Answer to question no-4........................................................................................................................9

Debt and equity position of the four firms that you have selected.......................................................9

Conclusion.......................................................................................................................................10

References...........................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report has divulged the key information on the corporate regulation and

accounting standard which needs to be followed by company to make the business

transparent to its stakeholders. The details of the equity and debt capital structure of four

banks have also been discussed to identify the financial leverage and cost of capital

Answer to question no-1

CORPORATE REGULATION

With the ramified changes in time, disclosure of the financial information to the

stakeholders is very much required. It is analyzed that each and every company should follow

proper IFRs rules and accounting standards if these companies want to establish

harmonization in international and domestic accounting rules and frameworks while

preparing the financial statements (Mwangi, and Murigu, 2015). As shareholders plays an

important role for a company who takes decision that determined by the financial position of

the company. Companies are having external shareholders along with internal shareholders.

Financial report helps in assisting the information about the company for the shareholders.

They know whether the company is growing or fallen. The external holders such as

government, investors, business communities, shareholders does not associate with the day

to day functioning of the company so they desire to get the financial report of the company so

that they determine the actual position related to monetary and non-monetary administration

of the company. Financial reports consist of numerous things like solvency position,

profitability position, liquidity position and also market valuation of the company. The non-

monetary administration consists all the social responsibilities regarding towards the society,

and report on renewable development (Morris, 2017).

The managers are not allowed to disclose the information voluntarily regarding the financial

statements and reports of the company due to increased value of financial statements for the

shareholders so they must be extremely coordinated and managed. The managers are not to

communicate the information that doesn’t show the actual results or condition of the

company or having the estimate report that doesn’t show the actual position even if the

manager is permitted to disclose the information voluntarily. The financial report is

composed to perform distinct functions some of them are: determining the real financial

This report has divulged the key information on the corporate regulation and

accounting standard which needs to be followed by company to make the business

transparent to its stakeholders. The details of the equity and debt capital structure of four

banks have also been discussed to identify the financial leverage and cost of capital

Answer to question no-1

CORPORATE REGULATION

With the ramified changes in time, disclosure of the financial information to the

stakeholders is very much required. It is analyzed that each and every company should follow

proper IFRs rules and accounting standards if these companies want to establish

harmonization in international and domestic accounting rules and frameworks while

preparing the financial statements (Mwangi, and Murigu, 2015). As shareholders plays an

important role for a company who takes decision that determined by the financial position of

the company. Companies are having external shareholders along with internal shareholders.

Financial report helps in assisting the information about the company for the shareholders.

They know whether the company is growing or fallen. The external holders such as

government, investors, business communities, shareholders does not associate with the day

to day functioning of the company so they desire to get the financial report of the company so

that they determine the actual position related to monetary and non-monetary administration

of the company. Financial reports consist of numerous things like solvency position,

profitability position, liquidity position and also market valuation of the company. The non-

monetary administration consists all the social responsibilities regarding towards the society,

and report on renewable development (Morris, 2017).

The managers are not allowed to disclose the information voluntarily regarding the financial

statements and reports of the company due to increased value of financial statements for the

shareholders so they must be extremely coordinated and managed. The managers are not to

communicate the information that doesn’t show the actual results or condition of the

company or having the estimate report that doesn’t show the actual position even if the

manager is permitted to disclose the information voluntarily. The financial report is

composed to perform distinct functions some of them are: determining the real financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

condition of the company for the investors or we can say the providers of finance, showing

the shareholders about the company's growth and potential so that they can invest and make

trust on the company etc. In case, if the companies financial report is inadequate then the

owners and managers are allowed to disclose only that information which shows the potential

of the company, by not showing the weakness of the company so that the company remains

trustworthy for the shareholders, and the shareholders make investments in the company. For

continuing the stake of thee company, sometimes company announced incentives for the

managerial on performance based. Sometimes if the report is not properly maintain in such

case the manager may disclose only that statement that shows the profitability of the business

just to earn some incentive through these financial reports that shows the inaccurate financial

position of the company (Grant, 2016).

Hence, it is important to maintain the financial accounts and reports of the company. There

are various accounting standards are to be form for financial reporting so that consistency

remains. Shareholders can elucidate and evaluate the financial position by analyzing the

report if it maintains according to the consistency of standards. It will also help in

determining false representation and administration in the report so that these can be

corrected (Flannery, 2016).

Answer to question no-2

ACCOUNTING STANDARD SETTING

It is analyzed that Australian Accounting standards board have been set up for

monitoring and issue of the accounting standards guidelines for the corporation.

Accounting standards are rules and guidelines set up by government institutions like

IASB, to maintain accounting easy and understandable among all the companies and

industries. It describes all the guidelines related to the doing transaction in a manner.

Accounting Standards Board of Australia (AASB) is the governmental organization that

allocates the accounting standards for Australian body. Accounting standards are refined,

circulate and managed by this Australian government organization.

It impersonates an essential role all over the world in framing accounting standards process.

The International Accounting Standard Board (IASB) is a private organization that serves the

the shareholders about the company's growth and potential so that they can invest and make

trust on the company etc. In case, if the companies financial report is inadequate then the

owners and managers are allowed to disclose only that information which shows the potential

of the company, by not showing the weakness of the company so that the company remains

trustworthy for the shareholders, and the shareholders make investments in the company. For

continuing the stake of thee company, sometimes company announced incentives for the

managerial on performance based. Sometimes if the report is not properly maintain in such

case the manager may disclose only that statement that shows the profitability of the business

just to earn some incentive through these financial reports that shows the inaccurate financial

position of the company (Grant, 2016).

Hence, it is important to maintain the financial accounts and reports of the company. There

are various accounting standards are to be form for financial reporting so that consistency

remains. Shareholders can elucidate and evaluate the financial position by analyzing the

report if it maintains according to the consistency of standards. It will also help in

determining false representation and administration in the report so that these can be

corrected (Flannery, 2016).

Answer to question no-2

ACCOUNTING STANDARD SETTING

It is analyzed that Australian Accounting standards board have been set up for

monitoring and issue of the accounting standards guidelines for the corporation.

Accounting standards are rules and guidelines set up by government institutions like

IASB, to maintain accounting easy and understandable among all the companies and

industries. It describes all the guidelines related to the doing transaction in a manner.

Accounting Standards Board of Australia (AASB) is the governmental organization that

allocates the accounting standards for Australian body. Accounting standards are refined,

circulate and managed by this Australian government organization.

It impersonates an essential role all over the world in framing accounting standards process.

The International Accounting Standard Board (IASB) is a private organization that serves the

eminent aspects regarding the accounting standards all over the world for public concern.

IASB cooperate with other countries standards to set the standards world wide of financial

statements and reports (Ehiedu, 2014).

AASB got start changing its working system so that he can establish his way of accounting

standards globally in a different manner. It should be design in such a way so that IFRS

should also be considered in this to maintain the sufficient relationship with them. AASB

deals will the mechanics issues of standards that will help to IASB on the basis of this to

know how standards should be adumbrated and developed. IFRS is not became in forced in

some countries because of the national accounting standards of particular nation as well as

the laws are not up to mark in all countries regarding new accounting standards. However, if

new standards are embraced by countries it will adversely affect the accounting standards in

an adverse way (Bhimani, Silvola, & Sivabalan, (2016).

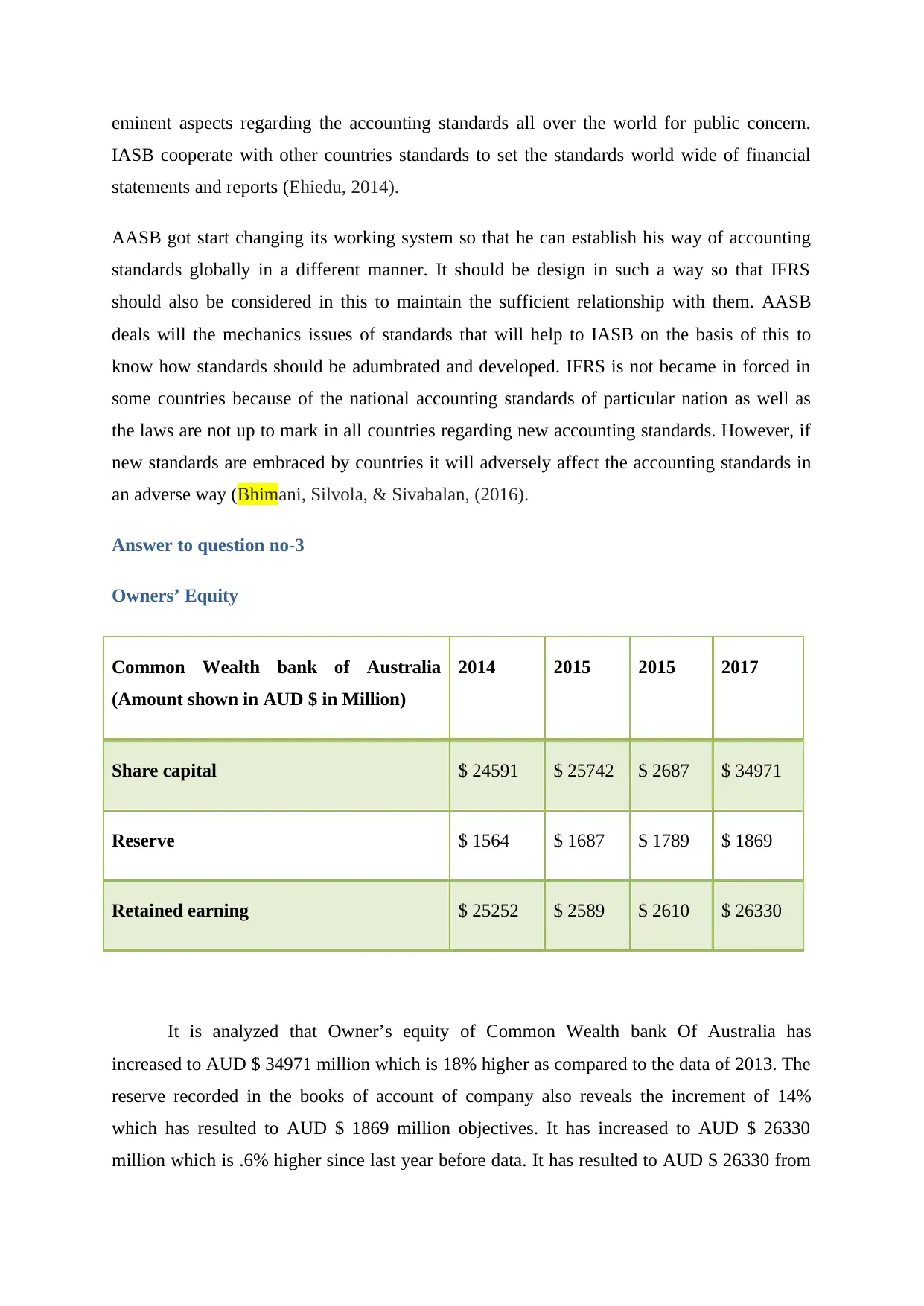

Answer to question no-3

Owners’ Equity

Common Wealth bank of Australia

(Amount shown in AUD $ in Million)

2014 2015 2015 2017

Share capital $ 24591 $ 25742 $ 2687 $ 34971

Reserve $ 1564 $ 1687 $ 1789 $ 1869

Retained earning $ 25252 $ 2589 $ 2610 $ 26330

It is analyzed that Owner’s equity of Common Wealth bank Of Australia has

increased to AUD $ 34971 million which is 18% higher as compared to the data of 2013. The

reserve recorded in the books of account of company also reveals the increment of 14%

which has resulted to AUD $ 1869 million objectives. It has increased to AUD $ 26330

million which is .6% higher since last year before data. It has resulted to AUD $ 26330 from

IASB cooperate with other countries standards to set the standards world wide of financial

statements and reports (Ehiedu, 2014).

AASB got start changing its working system so that he can establish his way of accounting

standards globally in a different manner. It should be design in such a way so that IFRS

should also be considered in this to maintain the sufficient relationship with them. AASB

deals will the mechanics issues of standards that will help to IASB on the basis of this to

know how standards should be adumbrated and developed. IFRS is not became in forced in

some countries because of the national accounting standards of particular nation as well as

the laws are not up to mark in all countries regarding new accounting standards. However, if

new standards are embraced by countries it will adversely affect the accounting standards in

an adverse way (Bhimani, Silvola, & Sivabalan, (2016).

Answer to question no-3

Owners’ Equity

Common Wealth bank of Australia

(Amount shown in AUD $ in Million)

2014 2015 2015 2017

Share capital $ 24591 $ 25742 $ 2687 $ 34971

Reserve $ 1564 $ 1687 $ 1789 $ 1869

Retained earning $ 25252 $ 2589 $ 2610 $ 26330

It is analyzed that Owner’s equity of Common Wealth bank Of Australia has

increased to AUD $ 34971 million which is 18% higher as compared to the data of 2013. The

reserve recorded in the books of account of company also reveals the increment of 14%

which has resulted to AUD $ 1869 million objectives. It has increased to AUD $ 26330

million which is .6% higher since last year before data. It has resulted to AUD $ 26330 from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

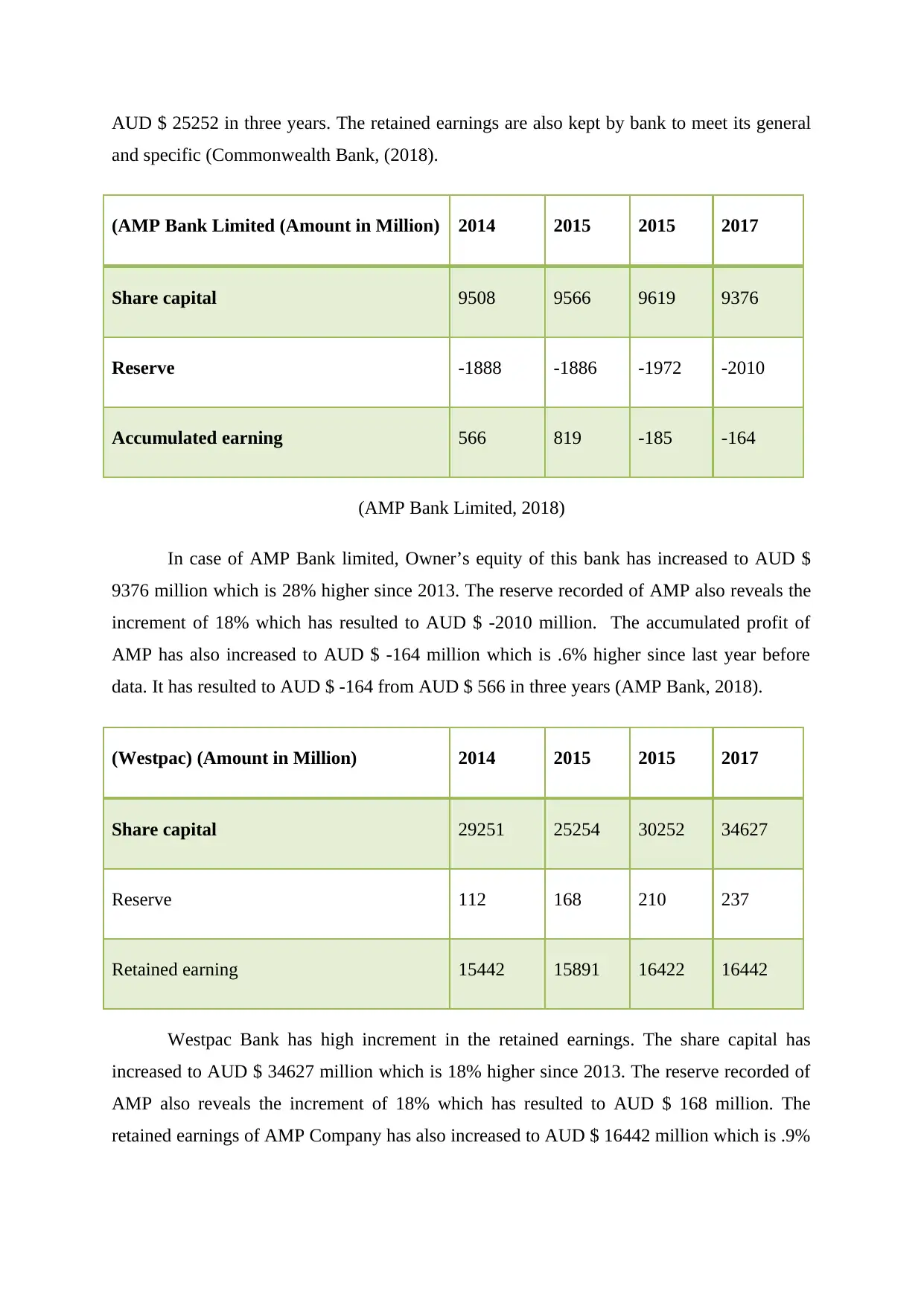

AUD $ 25252 in three years. The retained earnings are also kept by bank to meet its general

and specific (Commonwealth Bank, (2018).

(AMP Bank Limited (Amount in Million) 2014 2015 2015 2017

Share capital 9508 9566 9619 9376

Reserve -1888 -1886 -1972 -2010

Accumulated earning 566 819 -185 -164

(AMP Bank Limited, 2018)

In case of AMP Bank limited, Owner’s equity of this bank has increased to AUD $

9376 million which is 28% higher since 2013. The reserve recorded of AMP also reveals the

increment of 18% which has resulted to AUD $ -2010 million. The accumulated profit of

AMP has also increased to AUD $ -164 million which is .6% higher since last year before

data. It has resulted to AUD $ -164 from AUD $ 566 in three years (AMP Bank, 2018).

(Westpac) (Amount in Million) 2014 2015 2015 2017

Share capital 29251 25254 30252 34627

Reserve 112 168 210 237

Retained earning 15442 15891 16422 16442

Westpac Bank has high increment in the retained earnings. The share capital has

increased to AUD $ 34627 million which is 18% higher since 2013. The reserve recorded of

AMP also reveals the increment of 18% which has resulted to AUD $ 168 million. The

retained earnings of AMP Company has also increased to AUD $ 16442 million which is .9%

and specific (Commonwealth Bank, (2018).

(AMP Bank Limited (Amount in Million) 2014 2015 2015 2017

Share capital 9508 9566 9619 9376

Reserve -1888 -1886 -1972 -2010

Accumulated earning 566 819 -185 -164

(AMP Bank Limited, 2018)

In case of AMP Bank limited, Owner’s equity of this bank has increased to AUD $

9376 million which is 28% higher since 2013. The reserve recorded of AMP also reveals the

increment of 18% which has resulted to AUD $ -2010 million. The accumulated profit of

AMP has also increased to AUD $ -164 million which is .6% higher since last year before

data. It has resulted to AUD $ -164 from AUD $ 566 in three years (AMP Bank, 2018).

(Westpac) (Amount in Million) 2014 2015 2015 2017

Share capital 29251 25254 30252 34627

Reserve 112 168 210 237

Retained earning 15442 15891 16422 16442

Westpac Bank has high increment in the retained earnings. The share capital has

increased to AUD $ 34627 million which is 18% higher since 2013. The reserve recorded of

AMP also reveals the increment of 18% which has resulted to AUD $ 168 million. The

retained earnings of AMP Company has also increased to AUD $ 16442 million which is .9%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

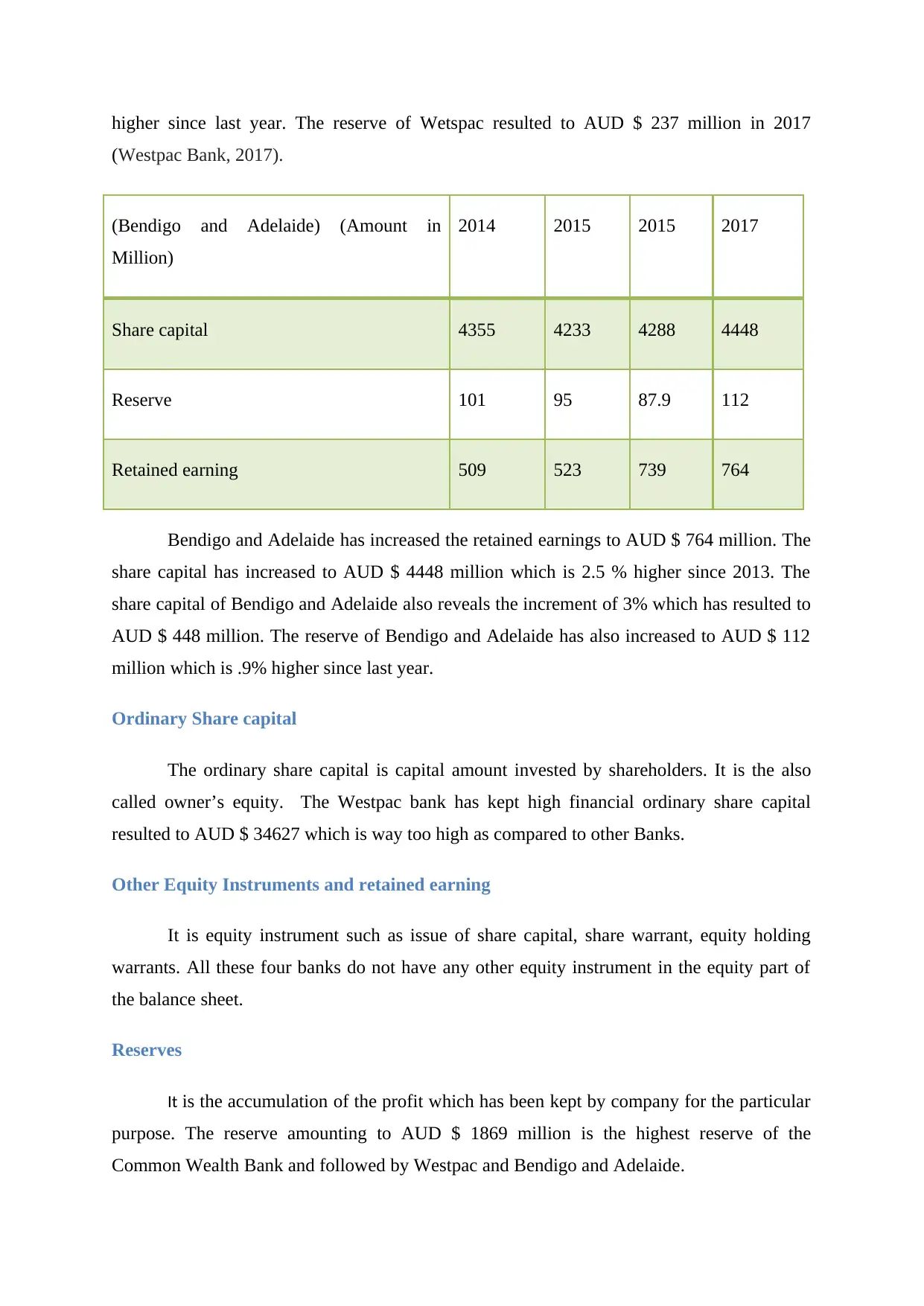

higher since last year. The reserve of Wetspac resulted to AUD $ 237 million in 2017

(Westpac Bank, 2017).

(Bendigo and Adelaide) (Amount in

Million)

2014 2015 2015 2017

Share capital 4355 4233 4288 4448

Reserve 101 95 87.9 112

Retained earning 509 523 739 764

Bendigo and Adelaide has increased the retained earnings to AUD $ 764 million. The

share capital has increased to AUD $ 4448 million which is 2.5 % higher since 2013. The

share capital of Bendigo and Adelaide also reveals the increment of 3% which has resulted to

AUD $ 448 million. The reserve of Bendigo and Adelaide has also increased to AUD $ 112

million which is .9% higher since last year.

Ordinary Share capital

The ordinary share capital is capital amount invested by shareholders. It is the also

called owner’s equity. The Westpac bank has kept high financial ordinary share capital

resulted to AUD $ 34627 which is way too high as compared to other Banks.

Other Equity Instruments and retained earning

It is equity instrument such as issue of share capital, share warrant, equity holding

warrants. All these four banks do not have any other equity instrument in the equity part of

the balance sheet.

Reserves

It is the accumulation of the profit which has been kept by company for the particular

purpose. The reserve amounting to AUD $ 1869 million is the highest reserve of the

Common Wealth Bank and followed by Westpac and Bendigo and Adelaide.

(Westpac Bank, 2017).

(Bendigo and Adelaide) (Amount in

Million)

2014 2015 2015 2017

Share capital 4355 4233 4288 4448

Reserve 101 95 87.9 112

Retained earning 509 523 739 764

Bendigo and Adelaide has increased the retained earnings to AUD $ 764 million. The

share capital has increased to AUD $ 4448 million which is 2.5 % higher since 2013. The

share capital of Bendigo and Adelaide also reveals the increment of 3% which has resulted to

AUD $ 448 million. The reserve of Bendigo and Adelaide has also increased to AUD $ 112

million which is .9% higher since last year.

Ordinary Share capital

The ordinary share capital is capital amount invested by shareholders. It is the also

called owner’s equity. The Westpac bank has kept high financial ordinary share capital

resulted to AUD $ 34627 which is way too high as compared to other Banks.

Other Equity Instruments and retained earning

It is equity instrument such as issue of share capital, share warrant, equity holding

warrants. All these four banks do not have any other equity instrument in the equity part of

the balance sheet.

Reserves

It is the accumulation of the profit which has been kept by company for the particular

purpose. The reserve amounting to AUD $ 1869 million is the highest reserve of the

Common Wealth Bank and followed by Westpac and Bendigo and Adelaide.

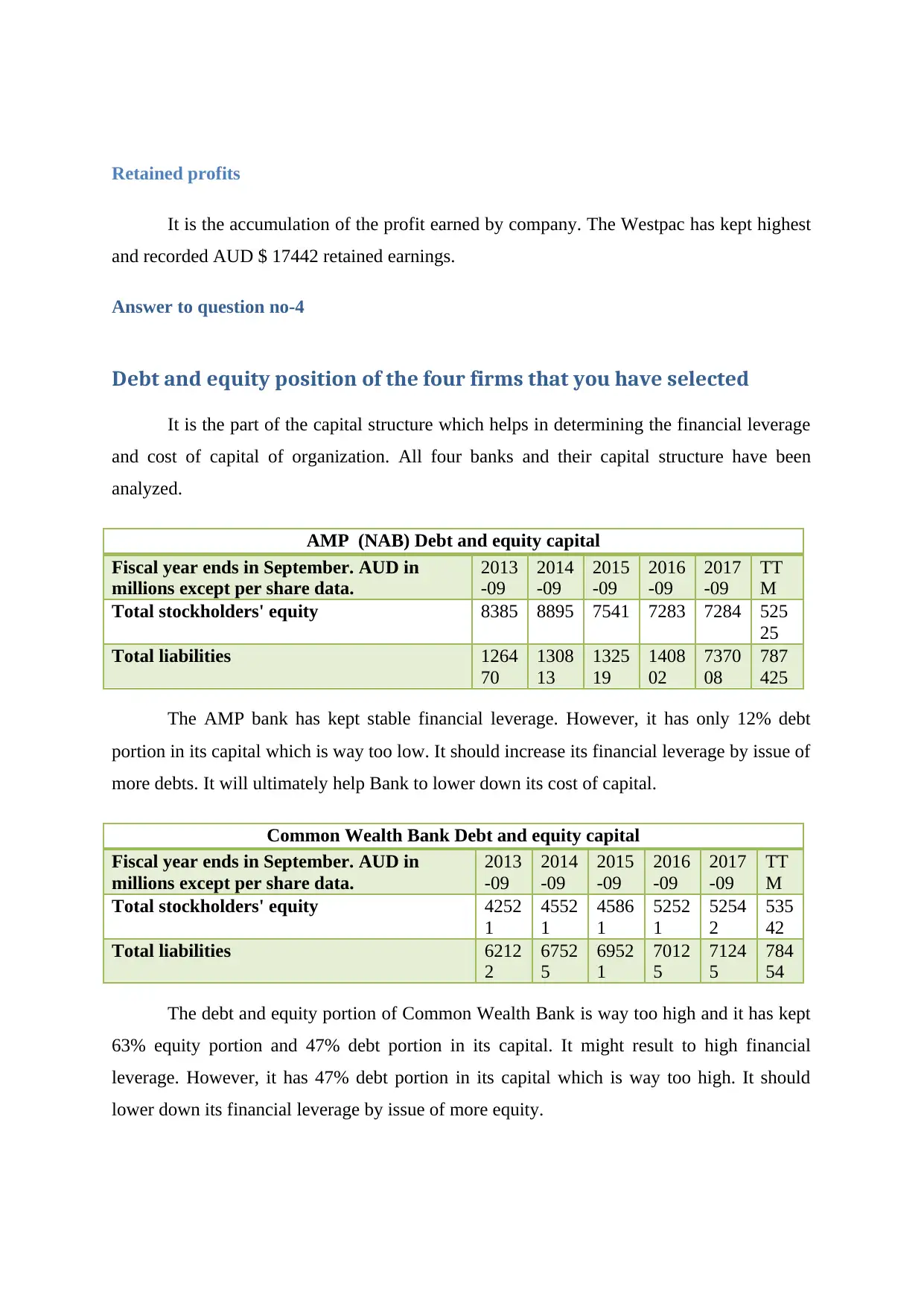

Retained profits

It is the accumulation of the profit earned by company. The Westpac has kept highest

and recorded AUD $ 17442 retained earnings.

Answer to question no-4

Debt and equity position of the four firms that you have selected

It is the part of the capital structure which helps in determining the financial leverage

and cost of capital of organization. All four banks and their capital structure have been

analyzed.

AMP (NAB) Debt and equity capital

Fiscal year ends in September. AUD in

millions except per share data.

2013

-09

2014

-09

2015

-09

2016

-09

2017

-09

TT

M

Total stockholders' equity 8385 8895 7541 7283 7284 525

25

Total liabilities 1264

70

1308

13

1325

19

1408

02

7370

08

787

425

The AMP bank has kept stable financial leverage. However, it has only 12% debt

portion in its capital which is way too low. It should increase its financial leverage by issue of

more debts. It will ultimately help Bank to lower down its cost of capital.

Common Wealth Bank Debt and equity capital

Fiscal year ends in September. AUD in

millions except per share data.

2013

-09

2014

-09

2015

-09

2016

-09

2017

-09

TT

M

Total stockholders' equity 4252

1

4552

1

4586

1

5252

1

5254

2

535

42

Total liabilities 6212

2

6752

5

6952

1

7012

5

7124

5

784

54

The debt and equity portion of Common Wealth Bank is way too high and it has kept

63% equity portion and 47% debt portion in its capital. It might result to high financial

leverage. However, it has 47% debt portion in its capital which is way too high. It should

lower down its financial leverage by issue of more equity.

It is the accumulation of the profit earned by company. The Westpac has kept highest

and recorded AUD $ 17442 retained earnings.

Answer to question no-4

Debt and equity position of the four firms that you have selected

It is the part of the capital structure which helps in determining the financial leverage

and cost of capital of organization. All four banks and their capital structure have been

analyzed.

AMP (NAB) Debt and equity capital

Fiscal year ends in September. AUD in

millions except per share data.

2013

-09

2014

-09

2015

-09

2016

-09

2017

-09

TT

M

Total stockholders' equity 8385 8895 7541 7283 7284 525

25

Total liabilities 1264

70

1308

13

1325

19

1408

02

7370

08

787

425

The AMP bank has kept stable financial leverage. However, it has only 12% debt

portion in its capital which is way too low. It should increase its financial leverage by issue of

more debts. It will ultimately help Bank to lower down its cost of capital.

Common Wealth Bank Debt and equity capital

Fiscal year ends in September. AUD in

millions except per share data.

2013

-09

2014

-09

2015

-09

2016

-09

2017

-09

TT

M

Total stockholders' equity 4252

1

4552

1

4586

1

5252

1

5254

2

535

42

Total liabilities 6212

2

6752

5

6952

1

7012

5

7124

5

784

54

The debt and equity portion of Common Wealth Bank is way too high and it has kept

63% equity portion and 47% debt portion in its capital. It might result to high financial

leverage. However, it has 47% debt portion in its capital which is way too high. It should

lower down its financial leverage by issue of more equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

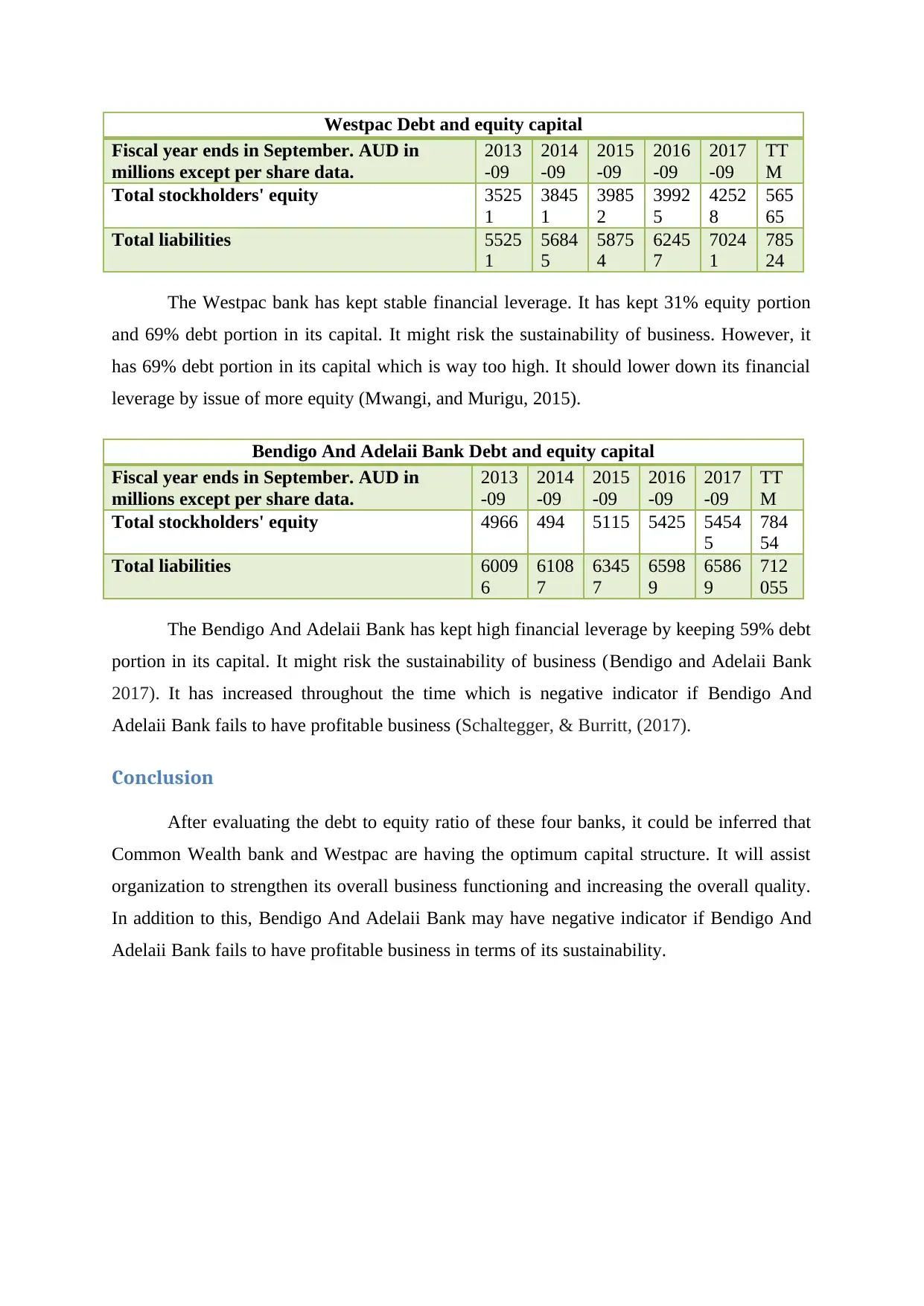

Westpac Debt and equity capital

Fiscal year ends in September. AUD in

millions except per share data.

2013

-09

2014

-09

2015

-09

2016

-09

2017

-09

TT

M

Total stockholders' equity 3525

1

3845

1

3985

2

3992

5

4252

8

565

65

Total liabilities 5525

1

5684

5

5875

4

6245

7

7024

1

785

24

The Westpac bank has kept stable financial leverage. It has kept 31% equity portion

and 69% debt portion in its capital. It might risk the sustainability of business. However, it

has 69% debt portion in its capital which is way too high. It should lower down its financial

leverage by issue of more equity (Mwangi, and Murigu, 2015).

Bendigo And Adelaii Bank Debt and equity capital

Fiscal year ends in September. AUD in

millions except per share data.

2013

-09

2014

-09

2015

-09

2016

-09

2017

-09

TT

M

Total stockholders' equity 4966 494 5115 5425 5454

5

784

54

Total liabilities 6009

6

6108

7

6345

7

6598

9

6586

9

712

055

The Bendigo And Adelaii Bank has kept high financial leverage by keeping 59% debt

portion in its capital. It might risk the sustainability of business (Bendigo and Adelaii Bank

2017). It has increased throughout the time which is negative indicator if Bendigo And

Adelaii Bank fails to have profitable business (Schaltegger, & Burritt, (2017).

Conclusion

After evaluating the debt to equity ratio of these four banks, it could be inferred that

Common Wealth bank and Westpac are having the optimum capital structure. It will assist

organization to strengthen its overall business functioning and increasing the overall quality.

In addition to this, Bendigo And Adelaii Bank may have negative indicator if Bendigo And

Adelaii Bank fails to have profitable business in terms of its sustainability.

Fiscal year ends in September. AUD in

millions except per share data.

2013

-09

2014

-09

2015

-09

2016

-09

2017

-09

TT

M

Total stockholders' equity 3525

1

3845

1

3985

2

3992

5

4252

8

565

65

Total liabilities 5525

1

5684

5

5875

4

6245

7

7024

1

785

24

The Westpac bank has kept stable financial leverage. It has kept 31% equity portion

and 69% debt portion in its capital. It might risk the sustainability of business. However, it

has 69% debt portion in its capital which is way too high. It should lower down its financial

leverage by issue of more equity (Mwangi, and Murigu, 2015).

Bendigo And Adelaii Bank Debt and equity capital

Fiscal year ends in September. AUD in

millions except per share data.

2013

-09

2014

-09

2015

-09

2016

-09

2017

-09

TT

M

Total stockholders' equity 4966 494 5115 5425 5454

5

784

54

Total liabilities 6009

6

6108

7

6345

7

6598

9

6586

9

712

055

The Bendigo And Adelaii Bank has kept high financial leverage by keeping 59% debt

portion in its capital. It might risk the sustainability of business (Bendigo and Adelaii Bank

2017). It has increased throughout the time which is negative indicator if Bendigo And

Adelaii Bank fails to have profitable business (Schaltegger, & Burritt, (2017).

Conclusion

After evaluating the debt to equity ratio of these four banks, it could be inferred that

Common Wealth bank and Westpac are having the optimum capital structure. It will assist

organization to strengthen its overall business functioning and increasing the overall quality.

In addition to this, Bendigo And Adelaii Bank may have negative indicator if Bendigo And

Adelaii Bank fails to have profitable business in terms of its sustainability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

AMP Bank, (2018) Annual Report [online] Available from

http://shareholder.anz.com/pages/annual-report-archive., [Accessed on 25th September 2018]

Bendigo and Adelaii Bank (2017)., Annual report., [Online]., Available from

https://www.bendigoadelaide.com.au/public/shareholders/annual_reports.asp, [Accessed 25th

September, 2018].

Bhimani, A., Silvola, H., & Sivabalan, P. (2016). Voluntary corporate social responsibility

reporting: A study of early and late reporter motivations and outcomes. Journal of

Management Accounting Research, 28(2), 77-101.

Commonwealth Bank, (2018) Annual Report [online] Available from

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-

reports/annual_report_2017_14_aug_2017.pdf [Accessed on 25th September 2018]

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: The

financial statement analysis (FSA) approach. Research Journal of Finance and

Accounting, 5(5), pp.81-90.

Flannery, M.J., 2016. Stabilizing large financial institutions with contingent capital

certificates. Quarterly Journal of Finance, 6(02), p.16-106.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. 2nd ed, Australia:

John Wiley & Sons.

Morris, R. D. (2017). Discussion of: The Phoenix Rises: The Australian Accounting

Standards Board and IFRS Adoption. Journal of International Accounting Research, 16(2),

155-157.

Mwangi, M. and Murigu, J.W., 2015. The determinants of financial performance in general

insurance companies in Kenya. European Scientific Journal, ESJ, 11(1).81-90.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

AMP Bank, (2018) Annual Report [online] Available from

http://shareholder.anz.com/pages/annual-report-archive., [Accessed on 25th September 2018]

Bendigo and Adelaii Bank (2017)., Annual report., [Online]., Available from

https://www.bendigoadelaide.com.au/public/shareholders/annual_reports.asp, [Accessed 25th

September, 2018].

Bhimani, A., Silvola, H., & Sivabalan, P. (2016). Voluntary corporate social responsibility

reporting: A study of early and late reporter motivations and outcomes. Journal of

Management Accounting Research, 28(2), 77-101.

Commonwealth Bank, (2018) Annual Report [online] Available from

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-

reports/annual_report_2017_14_aug_2017.pdf [Accessed on 25th September 2018]

Ehiedu, V.C., 2014. The impact of liquidity on profitability of some selected companies: The

financial statement analysis (FSA) approach. Research Journal of Finance and

Accounting, 5(5), pp.81-90.

Flannery, M.J., 2016. Stabilizing large financial institutions with contingent capital

certificates. Quarterly Journal of Finance, 6(02), p.16-106.

Grant, R.M., 2016. Contemporary strategy analysis: Text and cases edition. 2nd ed, Australia:

John Wiley & Sons.

Morris, R. D. (2017). Discussion of: The Phoenix Rises: The Australian Accounting

Standards Board and IFRS Adoption. Journal of International Accounting Research, 16(2),

155-157.

Mwangi, M. and Murigu, J.W., 2015. The determinants of financial performance in general

insurance companies in Kenya. European Scientific Journal, ESJ, 11(1).81-90.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Westpac Bank, (2018) Annual Report [online] Available from

https://www.google.co.in/search?ei=LEyjW-3hBs-

hyAOMp56oBA&q=wetpac+bank+annual+report&oq=wetpac+bank+annual+report&gs_l=p

sy-ab.3..0i13k1l3j0i13i30k1l2j0i22i30k1l5.2063.4535.0.4630.14.11.0.0.0.0.288.1327.2-

5.5.0....0...1.1.64.psy-ab..9.5.1320....0.3S0qMxJ0Rz0., [Accessed on 25th September 2018]

https://www.google.co.in/search?ei=LEyjW-3hBs-

hyAOMp56oBA&q=wetpac+bank+annual+report&oq=wetpac+bank+annual+report&gs_l=p

sy-ab.3..0i13k1l3j0i13i30k1l2j0i22i30k1l5.2063.4535.0.4630.14.11.0.0.0.0.288.1327.2-

5.5.0....0...1.1.64.psy-ab..9.5.1320....0.3S0qMxJ0Rz0., [Accessed on 25th September 2018]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.