Corporate Accounting: Case Study of Foreign Currency and Financials

VerifiedAdded on 2020/05/04

|8

|1126

|215

Case Study

AI Summary

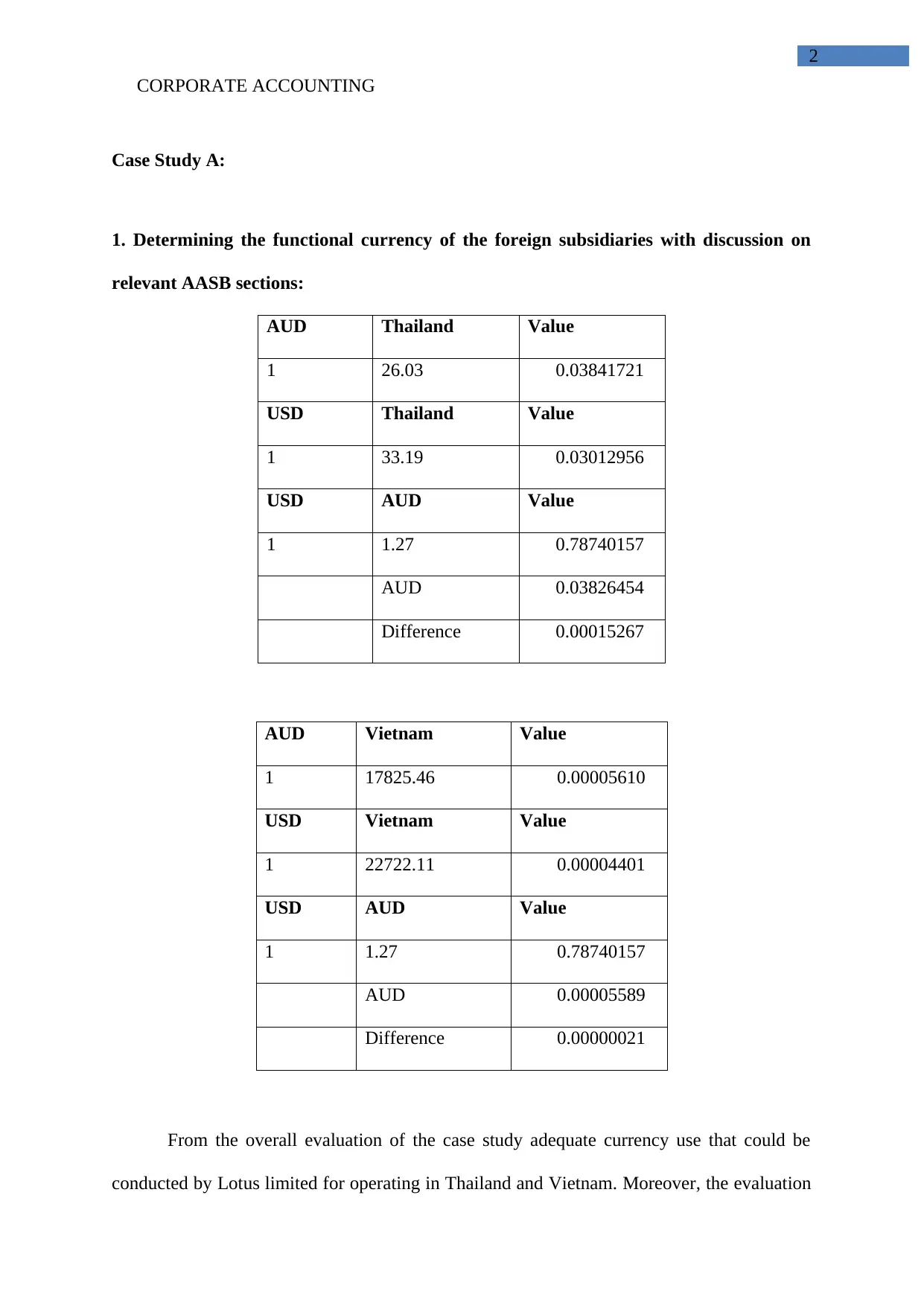

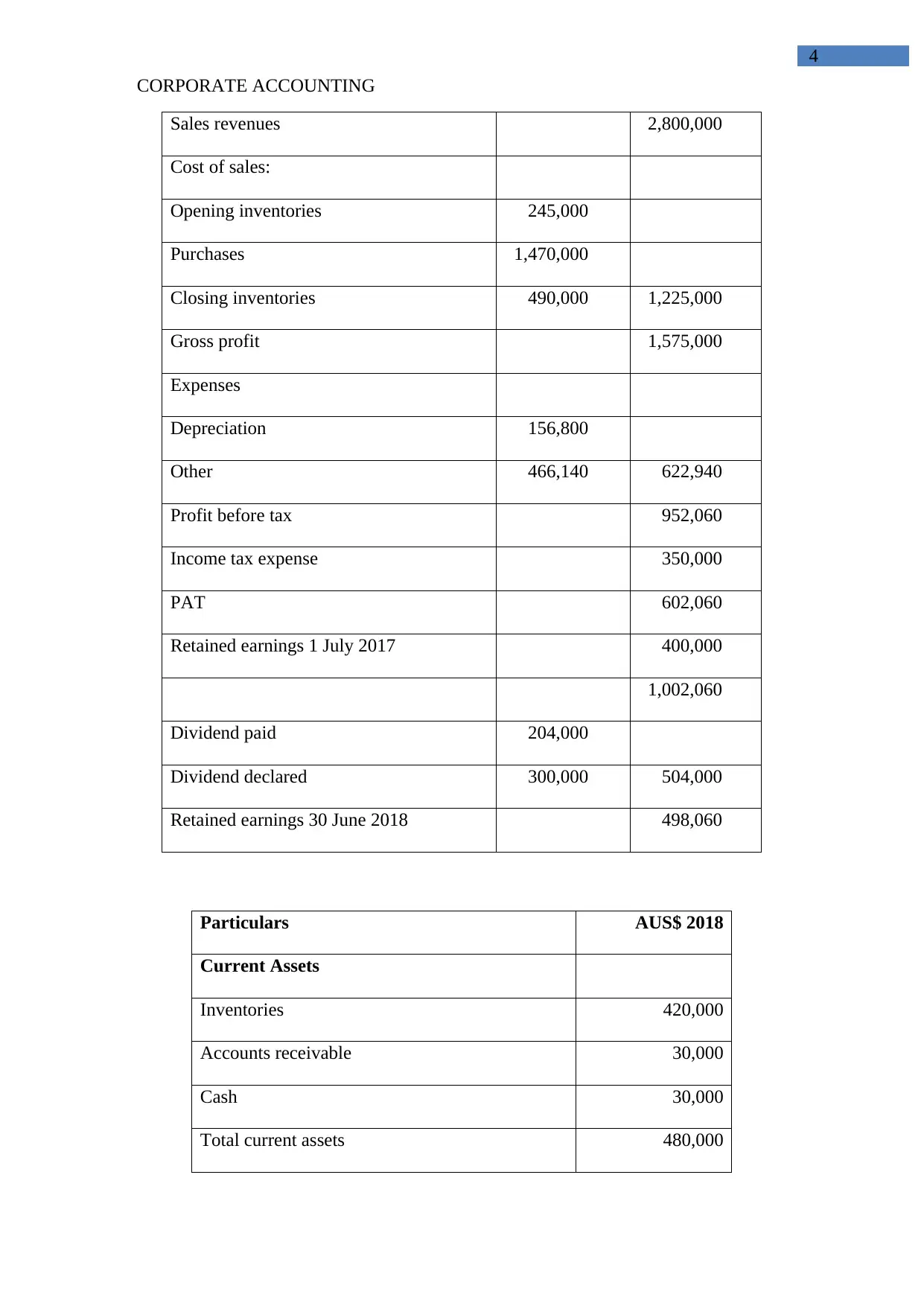

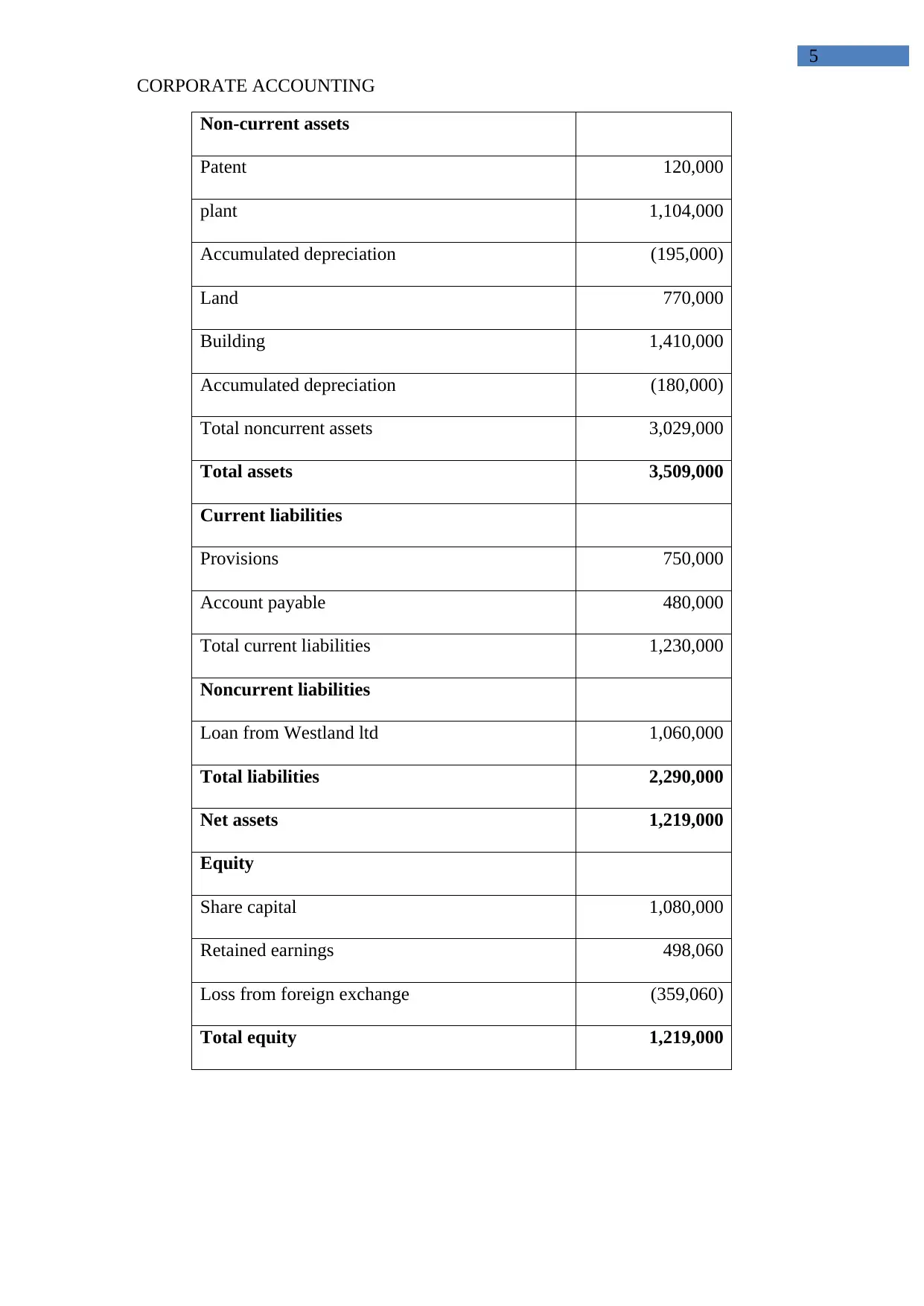

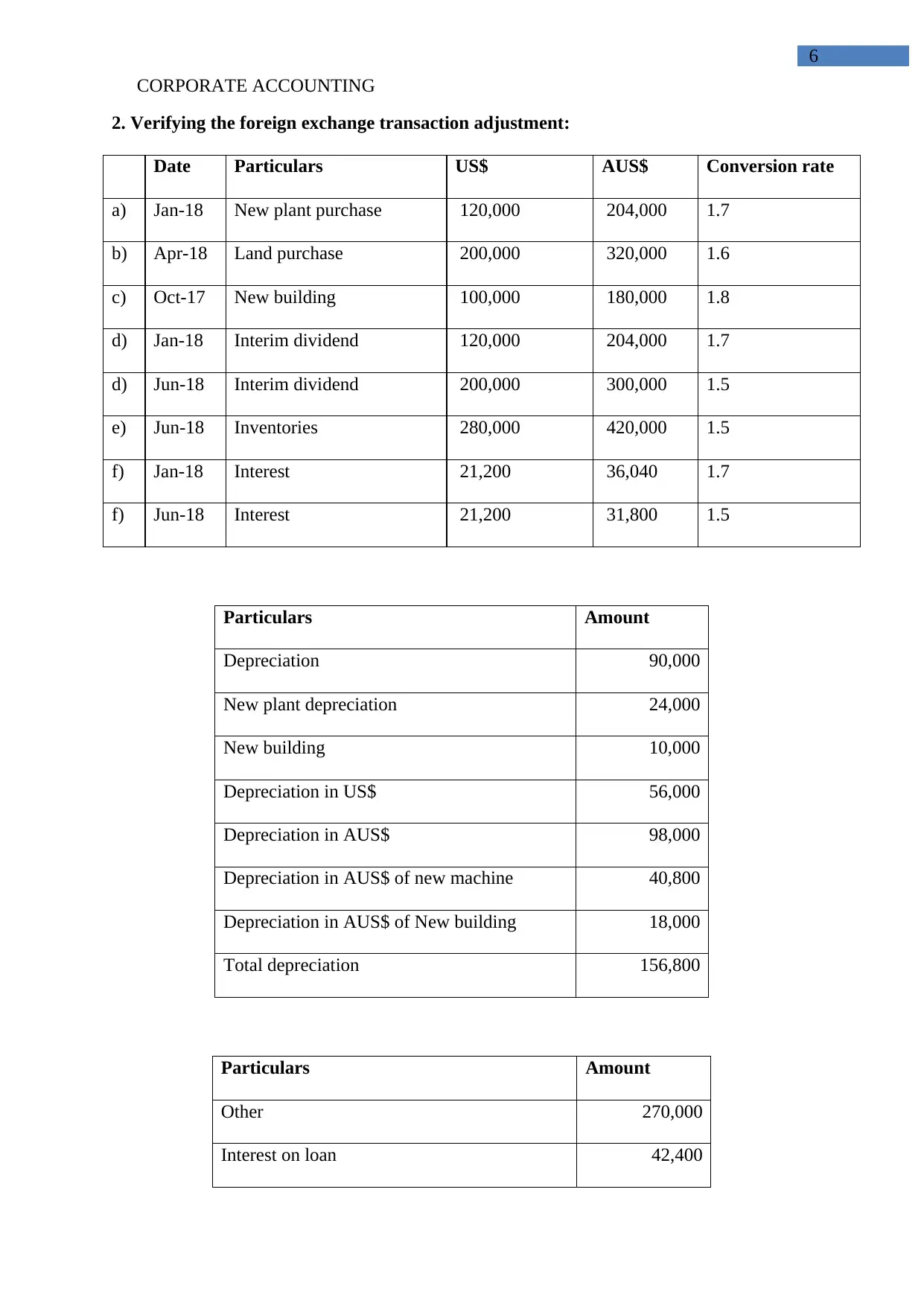

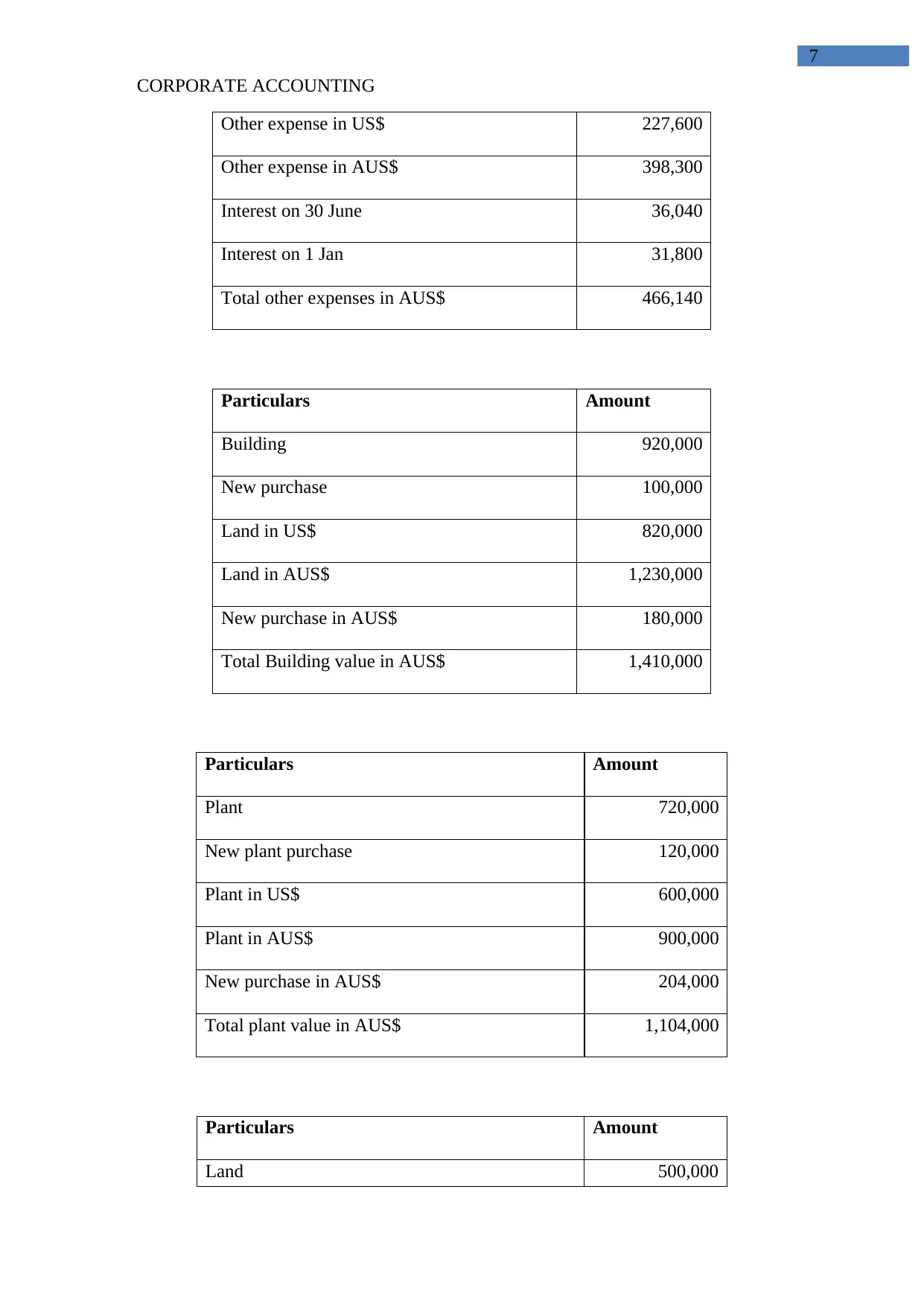

This case study assignment focuses on corporate accounting, specifically addressing foreign currency transactions and the preparation of financial statements under Australian Accounting Standards (AASB). Case Study A analyzes the functional currency of foreign subsidiaries of Lotus Limited in Thailand and Vietnam, evaluating currency usage and its impact on income generation. It references relevant AASB sections, particularly AASB 121, concerning foreign exchange rates and their impact. Case Study B involves preparing the financial statements of BULL LIMITED in Australian dollars for the year ended June 30, 2018, including the profit and loss statement, balance sheet, and retained earnings statement. It also includes a verification of foreign exchange transaction adjustments for various assets and liabilities. The assignment demonstrates the application of accounting principles in a global context and provides insights into financial reporting practices.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.