HI5020 Corporate Accounting: Cash Flow Statement Analysis - T1 2019

VerifiedAdded on 2023/04/03

|12

|3314

|245

Report

AI Summary

This report delves into the importance of cash flow statements in making informed business decisions, particularly for investors evaluating a company's financial stability and ability to meet short-term obligations. It examines the various sections of cash flow statements, including operating, investing, and financing activities, detailing the sources and uses of cash and cash equivalents within each section. The analysis includes a comparison of cash flow statements from different firms to determine their respective financial strengths and their capacities to repay short-term loans, with specific examples from Fantastic Ltd, Santos Ltd, and BHP Ltd. The report also covers trends in cash flow from operations, capital expenditure, dividends, net borrowing, and working capital, highlighting the difference between cash from operations and net income, and discussing the impact of working capital on cash flows. Ultimately, the report aims to provide a comprehensive understanding of how cash flow statements can be used to assess a company's financial health and investment potential.

Cash Flow Statement 1

ISSUES IN CASH FLOW STATEMENT

By (Name)

The Name of the Class

Professor

The Name of the School

The City and State

Date

ISSUES IN CASH FLOW STATEMENT

By (Name)

The Name of the Class

Professor

The Name of the School

The City and State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash Flow Statement 2

Issues in Cash Flow Statement

Abstract

Business decisions are made based on its financial information. Information is always

considered as the most important tool for decision making. Managers will need financial

information to make decisions on whether to expand the business, whether to pay out

dividend or to invest the available funds. Investors also need financial information to

predict the going concern of a business. Investors will be willing to invest on a business

only if the business will continue to operate in the foreseeable future and if such

business will be able to generate enough cash flow to repay its debts. This paper will

discuss the importance of cash flow statement and how can investors use cash flow

statements to analyze business’ financial stability and evaluate the ability of the

business to meet its short term obligations. The paper will also cover different sections

of activities of cash flow statement such as operating activities, investing activities and

financing activities. Sources and uses of cash and cash equivalent from each section

will also be discussed widely. In the paper, cash flow statements for different firms will

be analyzed to determine their various sources and applications of cash and cash

equivalent. Comparison will also be made based on cash flow statements to determine

the financial strengths of different businesses and their ability to repay short-term loans.

Issues in Cash Flow Statement

Abstract

Business decisions are made based on its financial information. Information is always

considered as the most important tool for decision making. Managers will need financial

information to make decisions on whether to expand the business, whether to pay out

dividend or to invest the available funds. Investors also need financial information to

predict the going concern of a business. Investors will be willing to invest on a business

only if the business will continue to operate in the foreseeable future and if such

business will be able to generate enough cash flow to repay its debts. This paper will

discuss the importance of cash flow statement and how can investors use cash flow

statements to analyze business’ financial stability and evaluate the ability of the

business to meet its short term obligations. The paper will also cover different sections

of activities of cash flow statement such as operating activities, investing activities and

financing activities. Sources and uses of cash and cash equivalent from each section

will also be discussed widely. In the paper, cash flow statements for different firms will

be analyzed to determine their various sources and applications of cash and cash

equivalent. Comparison will also be made based on cash flow statements to determine

the financial strengths of different businesses and their ability to repay short-term loans.

Cash Flow Statement 3

Table of contents

Introduction………………………………………………………………………………………4

Importance of income and cash flow statements to investors……………………………...4

Major sources and uses of cash……………………………………………………………….4

Trends of cash flow from operations………………………………...………………….…….5

Difference between cash from operations and net income………………………………...5

Financing capital expenditure……………………………………………………………….....5

Payments of dividends………………………………………………………………………….5

Working capital…………………………………………………………………………………..6

Items affected by cash flows………………………………………………….………………..6

Trends in capital expenditure……………………………………………………..……………6

Trends in dividends……………………………………………………………..………………6

Trends in net borrowing………………………………………..............................................7

Trends in working capital …………………………………………………………….………..8

Comparing financial strength of firms…………………………………………………...…….8

Best firm for lending…………………………………………………………………………….9

Conclusion ……………………………………………………………………….……………...9

References ………………………………………………………………………………….…11

Table of contents

Introduction………………………………………………………………………………………4

Importance of income and cash flow statements to investors……………………………...4

Major sources and uses of cash……………………………………………………………….4

Trends of cash flow from operations………………………………...………………….…….5

Difference between cash from operations and net income………………………………...5

Financing capital expenditure……………………………………………………………….....5

Payments of dividends………………………………………………………………………….5

Working capital…………………………………………………………………………………..6

Items affected by cash flows………………………………………………….………………..6

Trends in capital expenditure……………………………………………………..……………6

Trends in dividends……………………………………………………………..………………6

Trends in net borrowing………………………………………..............................................7

Trends in working capital …………………………………………………………….………..8

Comparing financial strength of firms…………………………………………………...…….8

Best firm for lending…………………………………………………………………………….9

Conclusion ……………………………………………………………………….……………...9

References ………………………………………………………………………………….…11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash Flow Statement 4

Introduction

Information is considered as the most crucial tool for financial decisions. There

are both external users and internal users to the business financial information.

Managers are examples of internal users and they depend on such information to make

decisions relating to their departments. Investors are an example of external users of

financial information. They use the audited accounts of the firm to determine the ability

of the firm to generate profit and pay its liabilities. All what they want is an assurance

that the firm will be able to pay them back should they invest their funds into the

business (Wahlen, et al., 2014). Businesses are therefore required to prepare their

financial accounts in a clear and understandable format so that all the users can be able

to read, analyze and make reasonable conclusions from those accounts. Cash flow

statement is one of the organization’s documents that carry a lot of relevant financial

information for decision makers. This statement gives a picture of the organization’s

ability to generate cash and put it into reasonable uses. The investors use cash flow

statement to determine the firm’s ability to pay back its current debts using current

assets and thus be able to decide on which company to lend money to and how much

to lend (Gupta et al., 2014 pp.649-660)

Part A

Income statement and statement of cash flow are the two most important

financial tools for communicating entity’s financial data. The two documents usually

show the ability of the company to generate income from its day to day operations and

to put the surplus cash into a profitable use (Haller, 2014). While income statement

shows the profit made by the company, statement of cash flow shows the company’s

cash movement both in and out of the organization (Lee, 2014)

Investors are always willing to invest their funds in a business which has a good

financial history. They will also prefer a fast growing business which is able to repay

their loans in the most convenient way possible. Therefore, investors will rely on the

income statement to determine whether the company is able to make profits or not.

Because it is out of profit that a company can be able to pay back its obligations. A

company which is able to make more profit is likely to attract a lot of investors since

ability of a company to continue making profit is one of the key indicators of a good

economic performance (Du,et al., 2015, pp.284-299).

While income statement will show the ability of the firm to generate profit from its

operations, cash flow will show the sources and applications of cash and cash

equivalent of the firm. The two statements are therefore used to complement each other

and both give a whole pack of information sufficient for financial decisions (Ajak and

Topal, 2015). Most investors are interested to know how a company has been paying

Introduction

Information is considered as the most crucial tool for financial decisions. There

are both external users and internal users to the business financial information.

Managers are examples of internal users and they depend on such information to make

decisions relating to their departments. Investors are an example of external users of

financial information. They use the audited accounts of the firm to determine the ability

of the firm to generate profit and pay its liabilities. All what they want is an assurance

that the firm will be able to pay them back should they invest their funds into the

business (Wahlen, et al., 2014). Businesses are therefore required to prepare their

financial accounts in a clear and understandable format so that all the users can be able

to read, analyze and make reasonable conclusions from those accounts. Cash flow

statement is one of the organization’s documents that carry a lot of relevant financial

information for decision makers. This statement gives a picture of the organization’s

ability to generate cash and put it into reasonable uses. The investors use cash flow

statement to determine the firm’s ability to pay back its current debts using current

assets and thus be able to decide on which company to lend money to and how much

to lend (Gupta et al., 2014 pp.649-660)

Part A

Income statement and statement of cash flow are the two most important

financial tools for communicating entity’s financial data. The two documents usually

show the ability of the company to generate income from its day to day operations and

to put the surplus cash into a profitable use (Haller, 2014). While income statement

shows the profit made by the company, statement of cash flow shows the company’s

cash movement both in and out of the organization (Lee, 2014)

Investors are always willing to invest their funds in a business which has a good

financial history. They will also prefer a fast growing business which is able to repay

their loans in the most convenient way possible. Therefore, investors will rely on the

income statement to determine whether the company is able to make profits or not.

Because it is out of profit that a company can be able to pay back its obligations. A

company which is able to make more profit is likely to attract a lot of investors since

ability of a company to continue making profit is one of the key indicators of a good

economic performance (Du,et al., 2015, pp.284-299).

While income statement will show the ability of the firm to generate profit from its

operations, cash flow will show the sources and applications of cash and cash

equivalent of the firm. The two statements are therefore used to complement each other

and both give a whole pack of information sufficient for financial decisions (Ajak and

Topal, 2015). Most investors are interested to know how a company has been paying

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash Flow Statement 5

out dividends in the past and such information will be available in the cash flow

statement. Others will be interested in knowing the composition of the company’s

finances, whether it gets more from the operating activities, investing activities or

financing activities. All this information will be retrieved from the statement of cash flow

(Collier, 2015).

Part B

1. Analysis for the cash flows

a. The major sources of cash for Fantastic ltd and Santos ltd are receipts from

customers while BHP ltd draws most of its cash from operating activities. The

major use of cash for BHP ltd is in purchasing property, plant and equipment.

Both Fantastic and Santos use their cash and cash equivalent in payment of

suppliers and employees.

b. Both Fantastic ltd and BHP ltd have almost the same trend. They have a

slight improvement from the year 2016 to 2017 but they both experienced a

drop in the year 2018. Santos ltd had a steady improvement from the year

2016 up to the year 2018.

c. For BHP Ltd, cash flow from operations is greater than the net income. This is

because net income is arrived at by subtracting some of the expenses which

are not in cash form. An expense such as depreciation, impairments of

property and other equipment does not involve any movement of cash out. As

a result, such expenses are reversed back in order to arrive at the cash

generated from operations. Cash flow statement only shows the movement of

cash in and out the firm and does not put into consideration any expense

which does not involve movement of cash.

d. The firm was able to generate enough cash from operations to finance its

capital expenditure because the cash generated from operations is more than

the amounts spend on capital expenditure as indicated below;

2018 2017 2016

Cash generated from operations 22,949 18,612 12,091

Purchase of property, plant and

equipment

(4,979) (3,697) (5,707)

Surplus cash 17,970 14,915 6,384

The firm was able to generate, in US $ 22,949,000 in the year 2018,

18,612,000 in 2017 and 12,091,000 in the year 2016. The capital expenditure

for the firm was as indicated in the above table. The firm was therefore able to

out dividends in the past and such information will be available in the cash flow

statement. Others will be interested in knowing the composition of the company’s

finances, whether it gets more from the operating activities, investing activities or

financing activities. All this information will be retrieved from the statement of cash flow

(Collier, 2015).

Part B

1. Analysis for the cash flows

a. The major sources of cash for Fantastic ltd and Santos ltd are receipts from

customers while BHP ltd draws most of its cash from operating activities. The

major use of cash for BHP ltd is in purchasing property, plant and equipment.

Both Fantastic and Santos use their cash and cash equivalent in payment of

suppliers and employees.

b. Both Fantastic ltd and BHP ltd have almost the same trend. They have a

slight improvement from the year 2016 to 2017 but they both experienced a

drop in the year 2018. Santos ltd had a steady improvement from the year

2016 up to the year 2018.

c. For BHP Ltd, cash flow from operations is greater than the net income. This is

because net income is arrived at by subtracting some of the expenses which

are not in cash form. An expense such as depreciation, impairments of

property and other equipment does not involve any movement of cash out. As

a result, such expenses are reversed back in order to arrive at the cash

generated from operations. Cash flow statement only shows the movement of

cash in and out the firm and does not put into consideration any expense

which does not involve movement of cash.

d. The firm was able to generate enough cash from operations to finance its

capital expenditure because the cash generated from operations is more than

the amounts spend on capital expenditure as indicated below;

2018 2017 2016

Cash generated from operations 22,949 18,612 12,091

Purchase of property, plant and

equipment

(4,979) (3,697) (5,707)

Surplus cash 17,970 14,915 6,384

The firm was able to generate, in US $ 22,949,000 in the year 2018,

18,612,000 in 2017 and 12,091,000 in the year 2016. The capital expenditure

for the firm was as indicated in the above table. The firm was therefore able to

Cash Flow Statement 6

meet all the capital expenditure using its cash from operations and still have

surplus of $17,970,000 in the year 2018, $14,915,000 in 2017 and $

6,384,000 in the year 2016.

This indicates a strong financial strength of BHP Ltd as cash from operations

are the main source which a firm should depend on for its expansion and

investments.

e. The cash generated from operations was enough to cover both the capital

expenditures and pay dividends to the shareholders. The firm was able to pay

dividends for all the three years which was paid by cash from operations.

In the year 2018, the company paid dividends of $(5,220+1,582)

=$6,802,000. The firm was still able to pay dividends from cash generated

from operations because after spending on capital a surplus of $17,970,000

was still available which is enough to cover for the dividends paid that year.

The dividends for the year 2017 was amounting to $(2,921+575) =

$3,496,000 which is less than the surplus cash from operations for that year

after the firm’s capital expenditure.

In the year 2016, the firm paid out dividends worthy $(4,130+62) =

$4,192,000. The firm’s surplus for that year after capital expenditure was

$6,384,000 which will be able to meet the payment for dividends for that year.

f. From the above calculations, the cash generated from operations was in

excess. The firm was able to meet the cost of capital and dividends and still

be in a position to invest the remaining cash. From its statement of cash flow,

we can see that the firm invested on purchase of shares by Employee Share

Ownership Plan (ESOP) Trust. This indicates that the firm invested the

excess of the cash from operations.

g. The firm used working capital as sources of cash. From the statement of cash

flow for BHP ltd, the firm has factored the changes in assets and liabilities as

sources and uses of cash. Decrease in trade and other receivables were

treated as a source of cash while increase in trade and other payables was

treated as uses of cash.

h. The other major items which affected cash flows were dividends paid and

received, interests both paid and received, taxes and royalty paid and

purchases of property, plant and equipment.

i. Fantastic ltd spent $145,000 on capital expenditure in the year 2018,

$888,000 in 2017 and $884,000 in the year 2016. The expenditure for the

meet all the capital expenditure using its cash from operations and still have

surplus of $17,970,000 in the year 2018, $14,915,000 in 2017 and $

6,384,000 in the year 2016.

This indicates a strong financial strength of BHP Ltd as cash from operations

are the main source which a firm should depend on for its expansion and

investments.

e. The cash generated from operations was enough to cover both the capital

expenditures and pay dividends to the shareholders. The firm was able to pay

dividends for all the three years which was paid by cash from operations.

In the year 2018, the company paid dividends of $(5,220+1,582)

=$6,802,000. The firm was still able to pay dividends from cash generated

from operations because after spending on capital a surplus of $17,970,000

was still available which is enough to cover for the dividends paid that year.

The dividends for the year 2017 was amounting to $(2,921+575) =

$3,496,000 which is less than the surplus cash from operations for that year

after the firm’s capital expenditure.

In the year 2016, the firm paid out dividends worthy $(4,130+62) =

$4,192,000. The firm’s surplus for that year after capital expenditure was

$6,384,000 which will be able to meet the payment for dividends for that year.

f. From the above calculations, the cash generated from operations was in

excess. The firm was able to meet the cost of capital and dividends and still

be in a position to invest the remaining cash. From its statement of cash flow,

we can see that the firm invested on purchase of shares by Employee Share

Ownership Plan (ESOP) Trust. This indicates that the firm invested the

excess of the cash from operations.

g. The firm used working capital as sources of cash. From the statement of cash

flow for BHP ltd, the firm has factored the changes in assets and liabilities as

sources and uses of cash. Decrease in trade and other receivables were

treated as a source of cash while increase in trade and other payables was

treated as uses of cash.

h. The other major items which affected cash flows were dividends paid and

received, interests both paid and received, taxes and royalty paid and

purchases of property, plant and equipment.

i. Fantastic ltd spent $145,000 on capital expenditure in the year 2018,

$888,000 in 2017 and $884,000 in the year 2016. The expenditure for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

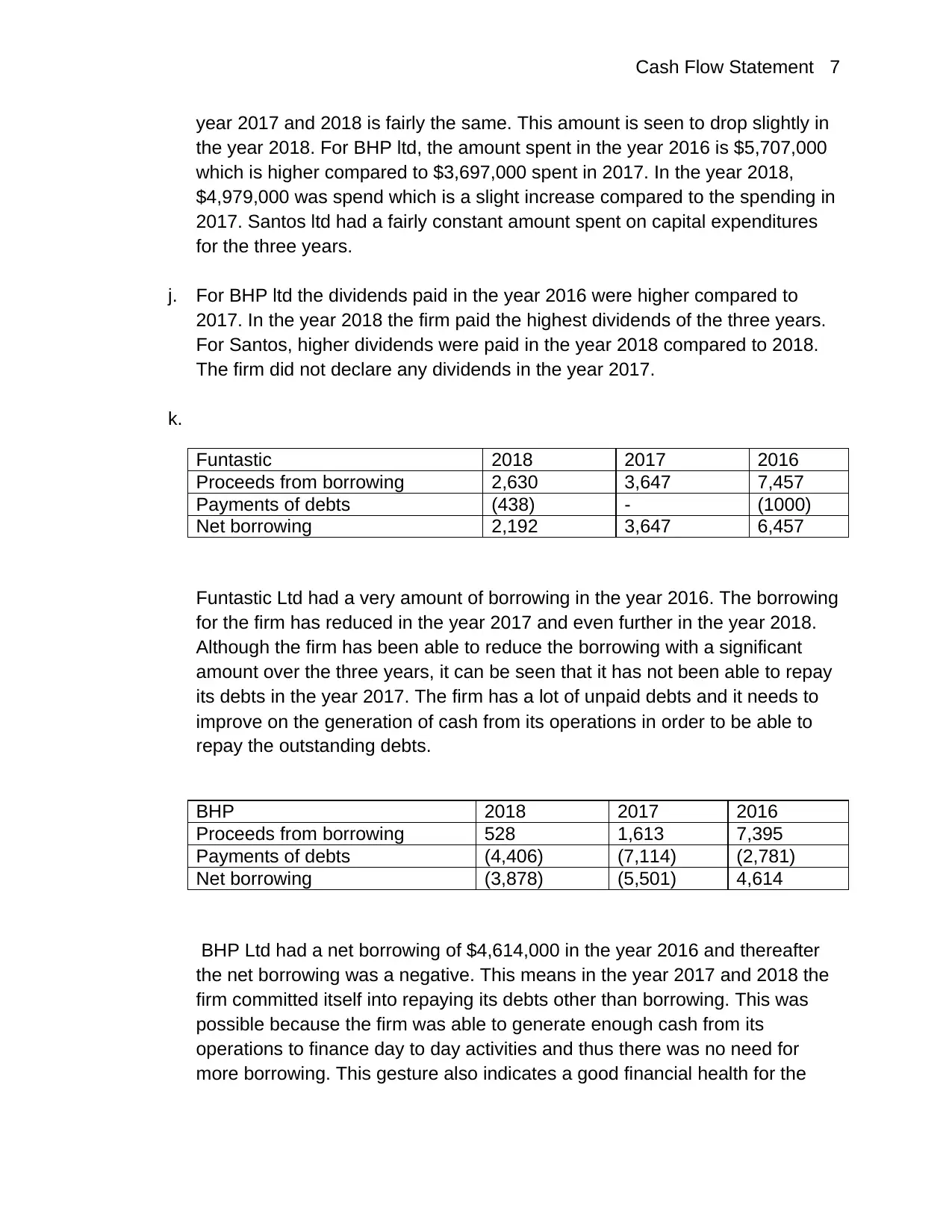

Cash Flow Statement 7

year 2017 and 2018 is fairly the same. This amount is seen to drop slightly in

the year 2018. For BHP ltd, the amount spent in the year 2016 is $5,707,000

which is higher compared to $3,697,000 spent in 2017. In the year 2018,

$4,979,000 was spend which is a slight increase compared to the spending in

2017. Santos ltd had a fairly constant amount spent on capital expenditures

for the three years.

j. For BHP ltd the dividends paid in the year 2016 were higher compared to

2017. In the year 2018 the firm paid the highest dividends of the three years.

For Santos, higher dividends were paid in the year 2018 compared to 2018.

The firm did not declare any dividends in the year 2017.

k.

Funtastic 2018 2017 2016

Proceeds from borrowing 2,630 3,647 7,457

Payments of debts (438) - (1000)

Net borrowing 2,192 3,647 6,457

Funtastic Ltd had a very amount of borrowing in the year 2016. The borrowing

for the firm has reduced in the year 2017 and even further in the year 2018.

Although the firm has been able to reduce the borrowing with a significant

amount over the three years, it can be seen that it has not been able to repay

its debts in the year 2017. The firm has a lot of unpaid debts and it needs to

improve on the generation of cash from its operations in order to be able to

repay the outstanding debts.

BHP 2018 2017 2016

Proceeds from borrowing 528 1,613 7,395

Payments of debts (4,406) (7,114) (2,781)

Net borrowing (3,878) (5,501) 4,614

BHP Ltd had a net borrowing of $4,614,000 in the year 2016 and thereafter

the net borrowing was a negative. This means in the year 2017 and 2018 the

firm committed itself into repaying its debts other than borrowing. This was

possible because the firm was able to generate enough cash from its

operations to finance day to day activities and thus there was no need for

more borrowing. This gesture also indicates a good financial health for the

year 2017 and 2018 is fairly the same. This amount is seen to drop slightly in

the year 2018. For BHP ltd, the amount spent in the year 2016 is $5,707,000

which is higher compared to $3,697,000 spent in 2017. In the year 2018,

$4,979,000 was spend which is a slight increase compared to the spending in

2017. Santos ltd had a fairly constant amount spent on capital expenditures

for the three years.

j. For BHP ltd the dividends paid in the year 2016 were higher compared to

2017. In the year 2018 the firm paid the highest dividends of the three years.

For Santos, higher dividends were paid in the year 2018 compared to 2018.

The firm did not declare any dividends in the year 2017.

k.

Funtastic 2018 2017 2016

Proceeds from borrowing 2,630 3,647 7,457

Payments of debts (438) - (1000)

Net borrowing 2,192 3,647 6,457

Funtastic Ltd had a very amount of borrowing in the year 2016. The borrowing

for the firm has reduced in the year 2017 and even further in the year 2018.

Although the firm has been able to reduce the borrowing with a significant

amount over the three years, it can be seen that it has not been able to repay

its debts in the year 2017. The firm has a lot of unpaid debts and it needs to

improve on the generation of cash from its operations in order to be able to

repay the outstanding debts.

BHP 2018 2017 2016

Proceeds from borrowing 528 1,613 7,395

Payments of debts (4,406) (7,114) (2,781)

Net borrowing (3,878) (5,501) 4,614

BHP Ltd had a net borrowing of $4,614,000 in the year 2016 and thereafter

the net borrowing was a negative. This means in the year 2017 and 2018 the

firm committed itself into repaying its debts other than borrowing. This was

possible because the firm was able to generate enough cash from its

operations to finance day to day activities and thus there was no need for

more borrowing. This gesture also indicates a good financial health for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

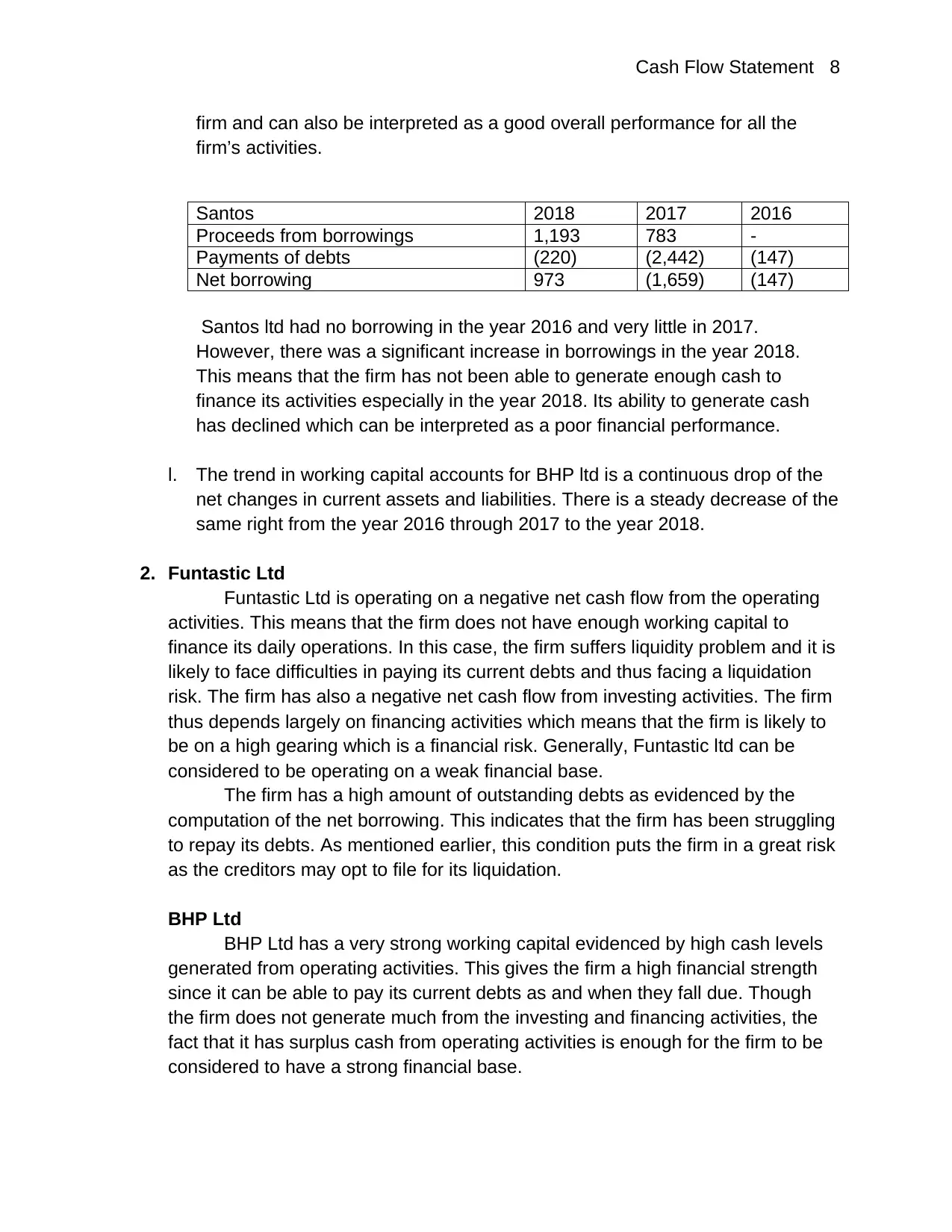

Cash Flow Statement 8

firm and can also be interpreted as a good overall performance for all the

firm’s activities.

Santos 2018 2017 2016

Proceeds from borrowings 1,193 783 -

Payments of debts (220) (2,442) (147)

Net borrowing 973 (1,659) (147)

Santos ltd had no borrowing in the year 2016 and very little in 2017.

However, there was a significant increase in borrowings in the year 2018.

This means that the firm has not been able to generate enough cash to

finance its activities especially in the year 2018. Its ability to generate cash

has declined which can be interpreted as a poor financial performance.

l. The trend in working capital accounts for BHP ltd is a continuous drop of the

net changes in current assets and liabilities. There is a steady decrease of the

same right from the year 2016 through 2017 to the year 2018.

2. Funtastic Ltd

Funtastic Ltd is operating on a negative net cash flow from the operating

activities. This means that the firm does not have enough working capital to

finance its daily operations. In this case, the firm suffers liquidity problem and it is

likely to face difficulties in paying its current debts and thus facing a liquidation

risk. The firm has also a negative net cash flow from investing activities. The firm

thus depends largely on financing activities which means that the firm is likely to

be on a high gearing which is a financial risk. Generally, Funtastic ltd can be

considered to be operating on a weak financial base.

The firm has a high amount of outstanding debts as evidenced by the

computation of the net borrowing. This indicates that the firm has been struggling

to repay its debts. As mentioned earlier, this condition puts the firm in a great risk

as the creditors may opt to file for its liquidation.

BHP Ltd

BHP Ltd has a very strong working capital evidenced by high cash levels

generated from operating activities. This gives the firm a high financial strength

since it can be able to pay its current debts as and when they fall due. Though

the firm does not generate much from the investing and financing activities, the

fact that it has surplus cash from operating activities is enough for the firm to be

considered to have a strong financial base.

firm and can also be interpreted as a good overall performance for all the

firm’s activities.

Santos 2018 2017 2016

Proceeds from borrowings 1,193 783 -

Payments of debts (220) (2,442) (147)

Net borrowing 973 (1,659) (147)

Santos ltd had no borrowing in the year 2016 and very little in 2017.

However, there was a significant increase in borrowings in the year 2018.

This means that the firm has not been able to generate enough cash to

finance its activities especially in the year 2018. Its ability to generate cash

has declined which can be interpreted as a poor financial performance.

l. The trend in working capital accounts for BHP ltd is a continuous drop of the

net changes in current assets and liabilities. There is a steady decrease of the

same right from the year 2016 through 2017 to the year 2018.

2. Funtastic Ltd

Funtastic Ltd is operating on a negative net cash flow from the operating

activities. This means that the firm does not have enough working capital to

finance its daily operations. In this case, the firm suffers liquidity problem and it is

likely to face difficulties in paying its current debts and thus facing a liquidation

risk. The firm has also a negative net cash flow from investing activities. The firm

thus depends largely on financing activities which means that the firm is likely to

be on a high gearing which is a financial risk. Generally, Funtastic ltd can be

considered to be operating on a weak financial base.

The firm has a high amount of outstanding debts as evidenced by the

computation of the net borrowing. This indicates that the firm has been struggling

to repay its debts. As mentioned earlier, this condition puts the firm in a great risk

as the creditors may opt to file for its liquidation.

BHP Ltd

BHP Ltd has a very strong working capital evidenced by high cash levels

generated from operating activities. This gives the firm a high financial strength

since it can be able to pay its current debts as and when they fall due. Though

the firm does not generate much from the investing and financing activities, the

fact that it has surplus cash from operating activities is enough for the firm to be

considered to have a strong financial base.

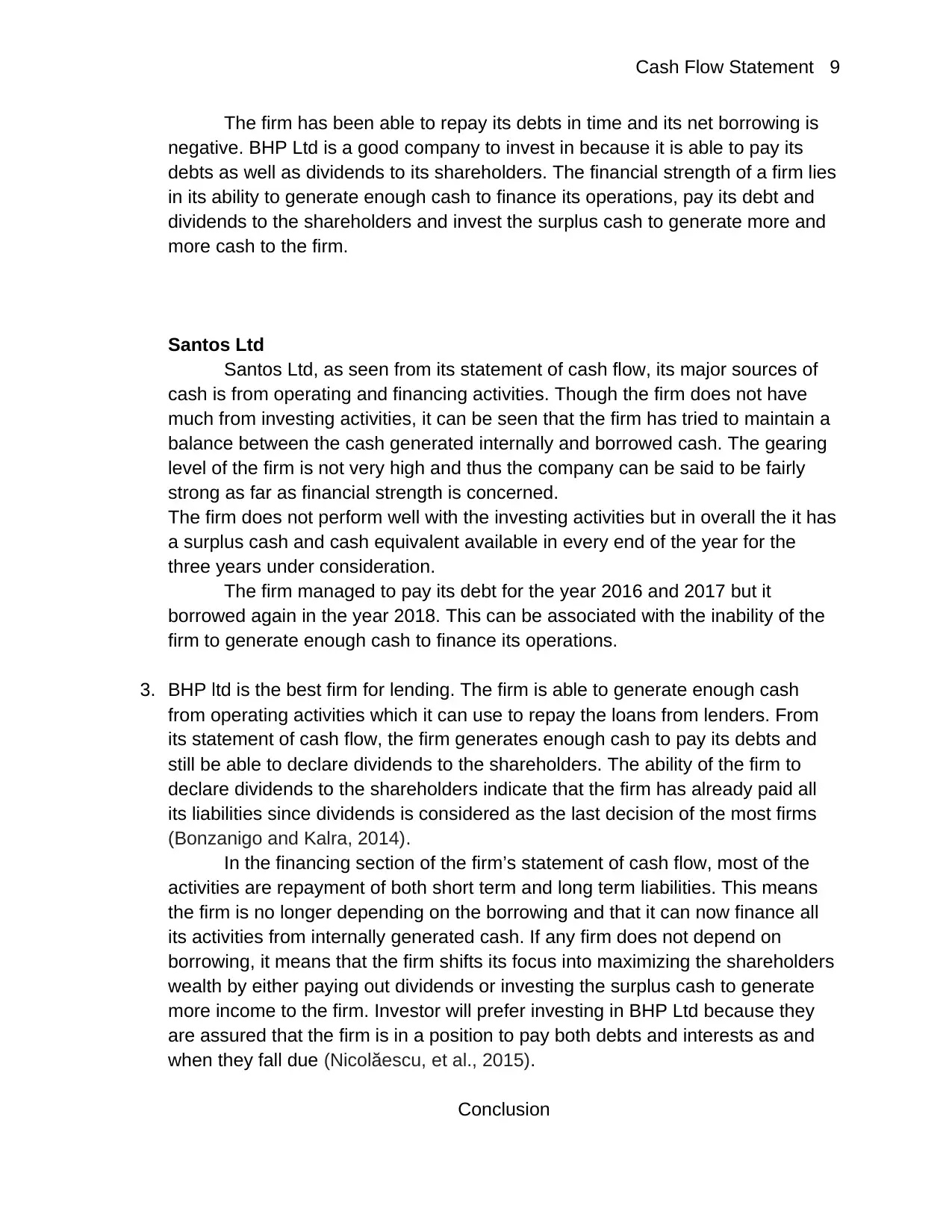

Cash Flow Statement 9

The firm has been able to repay its debts in time and its net borrowing is

negative. BHP Ltd is a good company to invest in because it is able to pay its

debts as well as dividends to its shareholders. The financial strength of a firm lies

in its ability to generate enough cash to finance its operations, pay its debt and

dividends to the shareholders and invest the surplus cash to generate more and

more cash to the firm.

Santos Ltd

Santos Ltd, as seen from its statement of cash flow, its major sources of

cash is from operating and financing activities. Though the firm does not have

much from investing activities, it can be seen that the firm has tried to maintain a

balance between the cash generated internally and borrowed cash. The gearing

level of the firm is not very high and thus the company can be said to be fairly

strong as far as financial strength is concerned.

The firm does not perform well with the investing activities but in overall the it has

a surplus cash and cash equivalent available in every end of the year for the

three years under consideration.

The firm managed to pay its debt for the year 2016 and 2017 but it

borrowed again in the year 2018. This can be associated with the inability of the

firm to generate enough cash to finance its operations.

3. BHP ltd is the best firm for lending. The firm is able to generate enough cash

from operating activities which it can use to repay the loans from lenders. From

its statement of cash flow, the firm generates enough cash to pay its debts and

still be able to declare dividends to the shareholders. The ability of the firm to

declare dividends to the shareholders indicate that the firm has already paid all

its liabilities since dividends is considered as the last decision of the most firms

(Bonzanigo and Kalra, 2014).

In the financing section of the firm’s statement of cash flow, most of the

activities are repayment of both short term and long term liabilities. This means

the firm is no longer depending on the borrowing and that it can now finance all

its activities from internally generated cash. If any firm does not depend on

borrowing, it means that the firm shifts its focus into maximizing the shareholders

wealth by either paying out dividends or investing the surplus cash to generate

more income to the firm. Investor will prefer investing in BHP Ltd because they

are assured that the firm is in a position to pay both debts and interests as and

when they fall due (Nicolăescu, et al., 2015).

Conclusion

The firm has been able to repay its debts in time and its net borrowing is

negative. BHP Ltd is a good company to invest in because it is able to pay its

debts as well as dividends to its shareholders. The financial strength of a firm lies

in its ability to generate enough cash to finance its operations, pay its debt and

dividends to the shareholders and invest the surplus cash to generate more and

more cash to the firm.

Santos Ltd

Santos Ltd, as seen from its statement of cash flow, its major sources of

cash is from operating and financing activities. Though the firm does not have

much from investing activities, it can be seen that the firm has tried to maintain a

balance between the cash generated internally and borrowed cash. The gearing

level of the firm is not very high and thus the company can be said to be fairly

strong as far as financial strength is concerned.

The firm does not perform well with the investing activities but in overall the it has

a surplus cash and cash equivalent available in every end of the year for the

three years under consideration.

The firm managed to pay its debt for the year 2016 and 2017 but it

borrowed again in the year 2018. This can be associated with the inability of the

firm to generate enough cash to finance its operations.

3. BHP ltd is the best firm for lending. The firm is able to generate enough cash

from operating activities which it can use to repay the loans from lenders. From

its statement of cash flow, the firm generates enough cash to pay its debts and

still be able to declare dividends to the shareholders. The ability of the firm to

declare dividends to the shareholders indicate that the firm has already paid all

its liabilities since dividends is considered as the last decision of the most firms

(Bonzanigo and Kalra, 2014).

In the financing section of the firm’s statement of cash flow, most of the

activities are repayment of both short term and long term liabilities. This means

the firm is no longer depending on the borrowing and that it can now finance all

its activities from internally generated cash. If any firm does not depend on

borrowing, it means that the firm shifts its focus into maximizing the shareholders

wealth by either paying out dividends or investing the surplus cash to generate

more income to the firm. Investor will prefer investing in BHP Ltd because they

are assured that the firm is in a position to pay both debts and interests as and

when they fall due (Nicolăescu, et al., 2015).

Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash Flow Statement 10

Cash flow statement and income statement still remains to be the most

relevant document to be referenced when making financial decisions. Most of the

lending decisions depend largely on the information derived from the cash flow.

From cash flow statement, one is able to determine the major sources of cash for

the firm and also see the uses in which such cash is committed to. Investors use

cash flow statement to gauge the firm’s ability to pay its debts and decide on

whether or not to invest their capital to such firms. The firm’s financial strength is

best measured by use of cash flow statement and income statement combined.

The combination of all business accounts will provide information for all

stakeholders to make their decisions. A business has both internal and external

stakeholders who depend on business accounts to make their decisions. The

paper has identified several uses of cash flow statement and how it is used in

making various financial decisions.

Cash flow statement and income statement still remains to be the most

relevant document to be referenced when making financial decisions. Most of the

lending decisions depend largely on the information derived from the cash flow.

From cash flow statement, one is able to determine the major sources of cash for

the firm and also see the uses in which such cash is committed to. Investors use

cash flow statement to gauge the firm’s ability to pay its debts and decide on

whether or not to invest their capital to such firms. The firm’s financial strength is

best measured by use of cash flow statement and income statement combined.

The combination of all business accounts will provide information for all

stakeholders to make their decisions. A business has both internal and external

stakeholders who depend on business accounts to make their decisions. The

paper has identified several uses of cash flow statement and how it is used in

making various financial decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash Flow Statement 11

References

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information

for decision making. John Wiley & Sons.

Du, N., Stevens, K. and McEnroe, J., 2015. The effects of comprehensive

income on investors’ judgments: An investigation of one-statement vs. two-

statement presentation formats. Accounting Research Journal, 28(3), pp.284-

299.

Gupta, J., Wilson, N., Gregoriou, A. and Healy, J., 2014. The value of operating

cash flow in modelling credit risk for SMEs. Applied Financial Economics, 24(9),

pp.649-660.

Lee, T.A., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an

Accounting Practice. Routledge.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial

statement analysis and valuation. Nelson Education.

Haller, A. and van Staden, C., 2014. The value added statement–an appropriate

instrument for Integrated Reporting. Accounting, Auditing & Accountability

Journal, 27(7), pp.1190-1216.

Ajak, A.D. and Topal, E., 2015. Real option in action: An example of flexible decision

making at a mine operational level. Resources Policy, 45, pp.109-120.

Cascino, S., Clatworthy, M., Garcia Osma, B., Gassen, J., Imam, S. and Jeanjean,

T., 2014. Who uses financial reports and for what purpose? Evidence from capital

providers. Accounting in Europe, 11(2), pp.185-209.

References

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information

for decision making. John Wiley & Sons.

Du, N., Stevens, K. and McEnroe, J., 2015. The effects of comprehensive

income on investors’ judgments: An investigation of one-statement vs. two-

statement presentation formats. Accounting Research Journal, 28(3), pp.284-

299.

Gupta, J., Wilson, N., Gregoriou, A. and Healy, J., 2014. The value of operating

cash flow in modelling credit risk for SMEs. Applied Financial Economics, 24(9),

pp.649-660.

Lee, T.A., 2014. Cash Flow Reporting (RLE Accounting): A Recent History of an

Accounting Practice. Routledge.

Wahlen, J.M., Baginski, S.P. and Bradshaw, M., 2014. Financial reporting, financial

statement analysis and valuation. Nelson Education.

Haller, A. and van Staden, C., 2014. The value added statement–an appropriate

instrument for Integrated Reporting. Accounting, Auditing & Accountability

Journal, 27(7), pp.1190-1216.

Ajak, A.D. and Topal, E., 2015. Real option in action: An example of flexible decision

making at a mine operational level. Resources Policy, 45, pp.109-120.

Cascino, S., Clatworthy, M., Garcia Osma, B., Gassen, J., Imam, S. and Jeanjean,

T., 2014. Who uses financial reports and for what purpose? Evidence from capital

providers. Accounting in Europe, 11(2), pp.185-209.

Cash Flow Statement 12

Easton, M. and Sommers, Z., 2018. Financial Statement Analysis & Valuation, 5e.

Kim, J.B., Li, L., Lu, L.Y. and Yu, Y., 2016. Financial statement comparability and

expected crash risk. Journal of Accounting and Economics, 61(2-3), pp.294-312.

Karadag, H., 2015. Financial management challenges in small and medium-sized

enterprises: A strategic management approach. EMAJ: Emerging Markets

Journal, 5(1), pp.26-40.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Trönnberg, C.C. and Hemlin, S., 2014. Lending decision making in banks: A critical

incident study of loan officers. European Management Journal, 32(2), pp.362-372.

Bonzanigo, L. and Kalra, N., 2014. Making informed investment decisions in an

uncertain world: a short demonstration. The World Bank.

Nicolăescu, E., Alpopi, C. and Zaharia, C., 2015. Measuring corporate sustainability

performance. Sustainability, 7(1), pp.851-865.

Arifeen, N., Hussain, M., Kazmi, S., Mubin, M., Mughal, S.L. and Qadri, W., 2014.

Measuring Business Performance: Comparison of Financial, Non Financial and

Qualitative Indicators. European Journal of Business and Management, 6(4), pp.38-

45.

Easton, M. and Sommers, Z., 2018. Financial Statement Analysis & Valuation, 5e.

Kim, J.B., Li, L., Lu, L.Y. and Yu, Y., 2016. Financial statement comparability and

expected crash risk. Journal of Accounting and Economics, 61(2-3), pp.294-312.

Karadag, H., 2015. Financial management challenges in small and medium-sized

enterprises: A strategic management approach. EMAJ: Emerging Markets

Journal, 5(1), pp.26-40.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Trönnberg, C.C. and Hemlin, S., 2014. Lending decision making in banks: A critical

incident study of loan officers. European Management Journal, 32(2), pp.362-372.

Bonzanigo, L. and Kalra, N., 2014. Making informed investment decisions in an

uncertain world: a short demonstration. The World Bank.

Nicolăescu, E., Alpopi, C. and Zaharia, C., 2015. Measuring corporate sustainability

performance. Sustainability, 7(1), pp.851-865.

Arifeen, N., Hussain, M., Kazmi, S., Mubin, M., Mughal, S.L. and Qadri, W., 2014.

Measuring Business Performance: Comparison of Financial, Non Financial and

Qualitative Indicators. European Journal of Business and Management, 6(4), pp.38-

45.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.