Financial Accounting: Analyzing Impairment of Cash Generating Units

VerifiedAdded on 2020/05/16

|6

|1457

|34

Homework Assignment

AI Summary

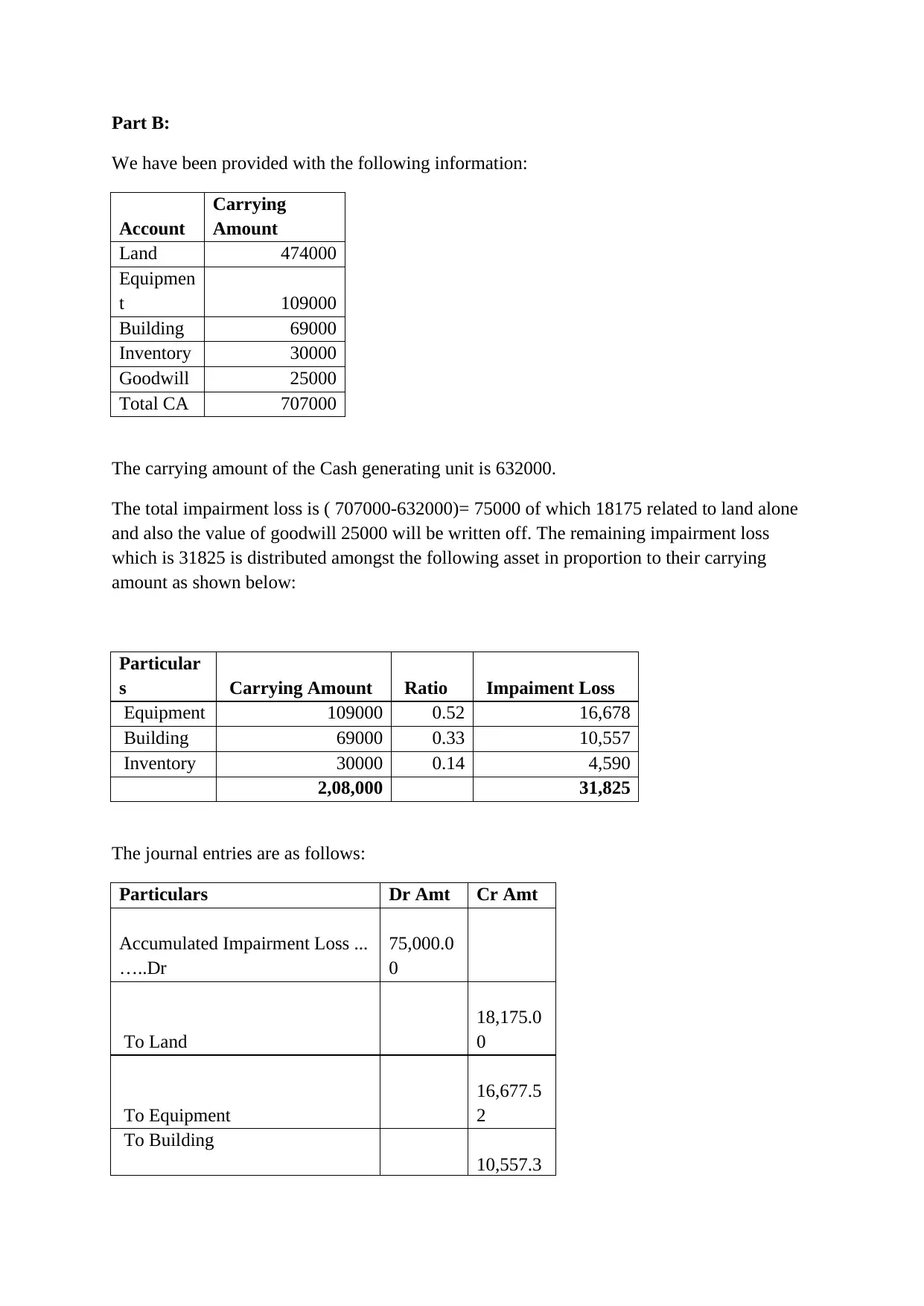

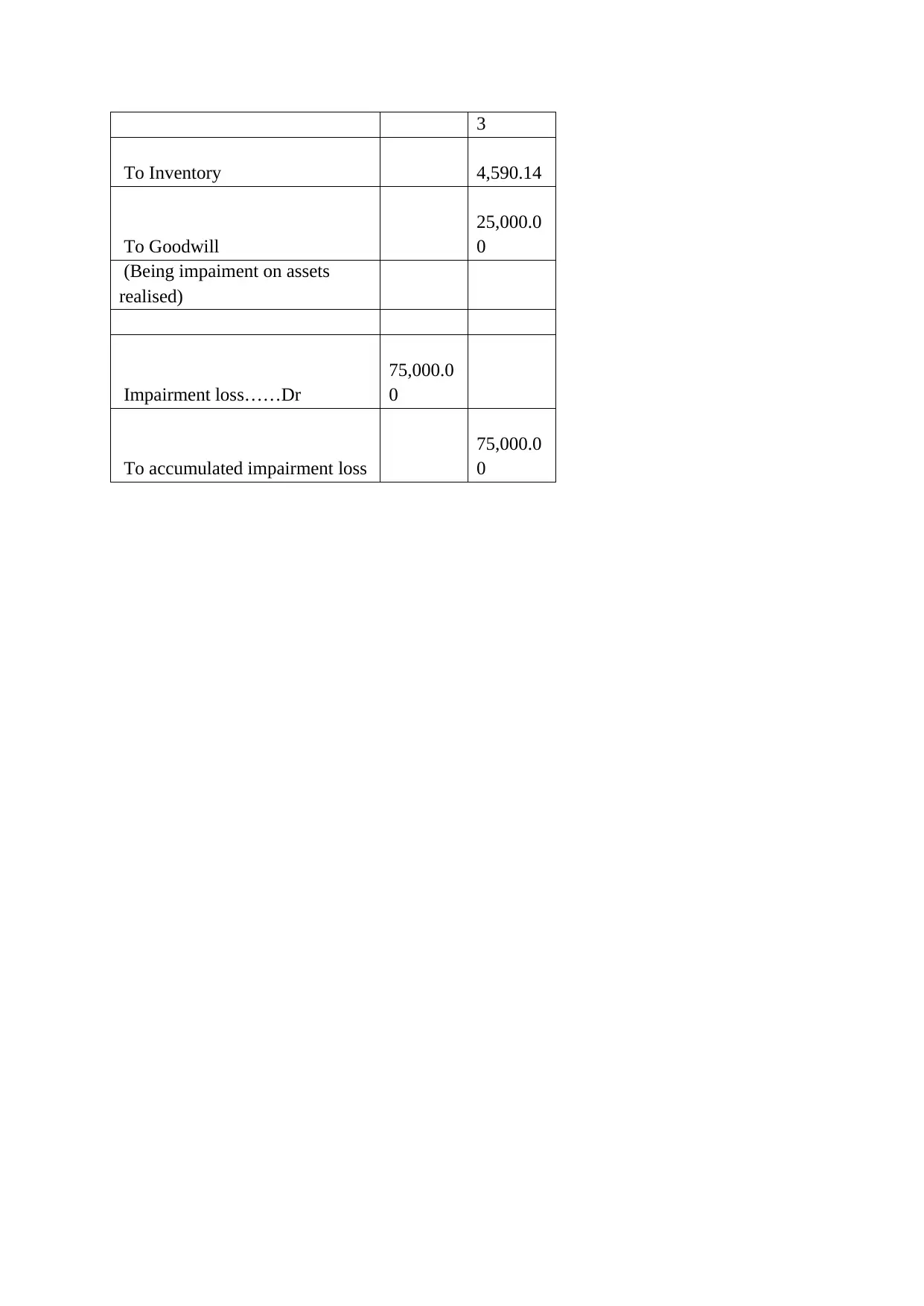

This assignment explores the concept of asset impairment, particularly within the context of cash generating units (CGUs). It defines impairment as the re-recording of assets when their carrying value exceeds their recoverable amount. The assignment explains the importance of determining the recoverable amount for individual assets or entire CGUs, especially when cash flows depend on multiple assets. It details the composition of a CGU, emphasizing that it comprises assets generating future cash flows, and highlights the influence of management policies and external factors on revenue generation. The assignment also covers reporting requirements, including disclosures for asset transfers and adjustments for impairment losses. Furthermore, it describes the calculation of impairment loss, its allocation to assets, and the specific considerations for non-cash generating assets within a CGU. The assignment includes a practical example with carrying amounts, impairment loss calculations, and corresponding journal entries to illustrate the accounting treatment of impairment. It emphasizes the importance of proper calculations, loss recording, and financial statement disclosures to ensure accurate financial reporting. The assignment concludes with a discussion of the relevant accounting standards and the importance of thoroughness in the impairment process. Finally, references are provided to support the concepts discussed in the assignment.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.