Corporate Accounting Analysis: BHP, Santos, Funtastic

VerifiedAdded on 2023/01/06

|31

|4693

|59

Report

AI Summary

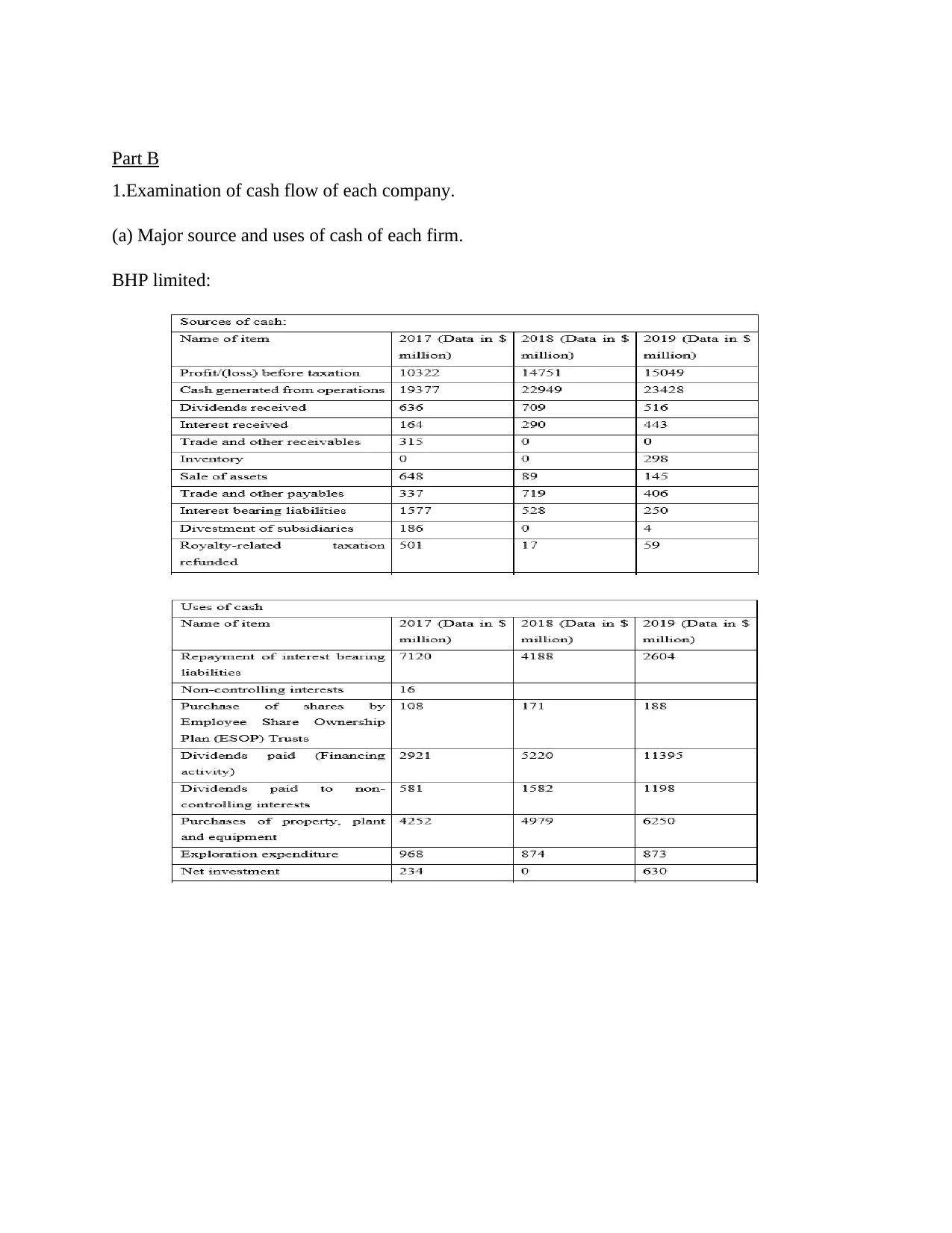

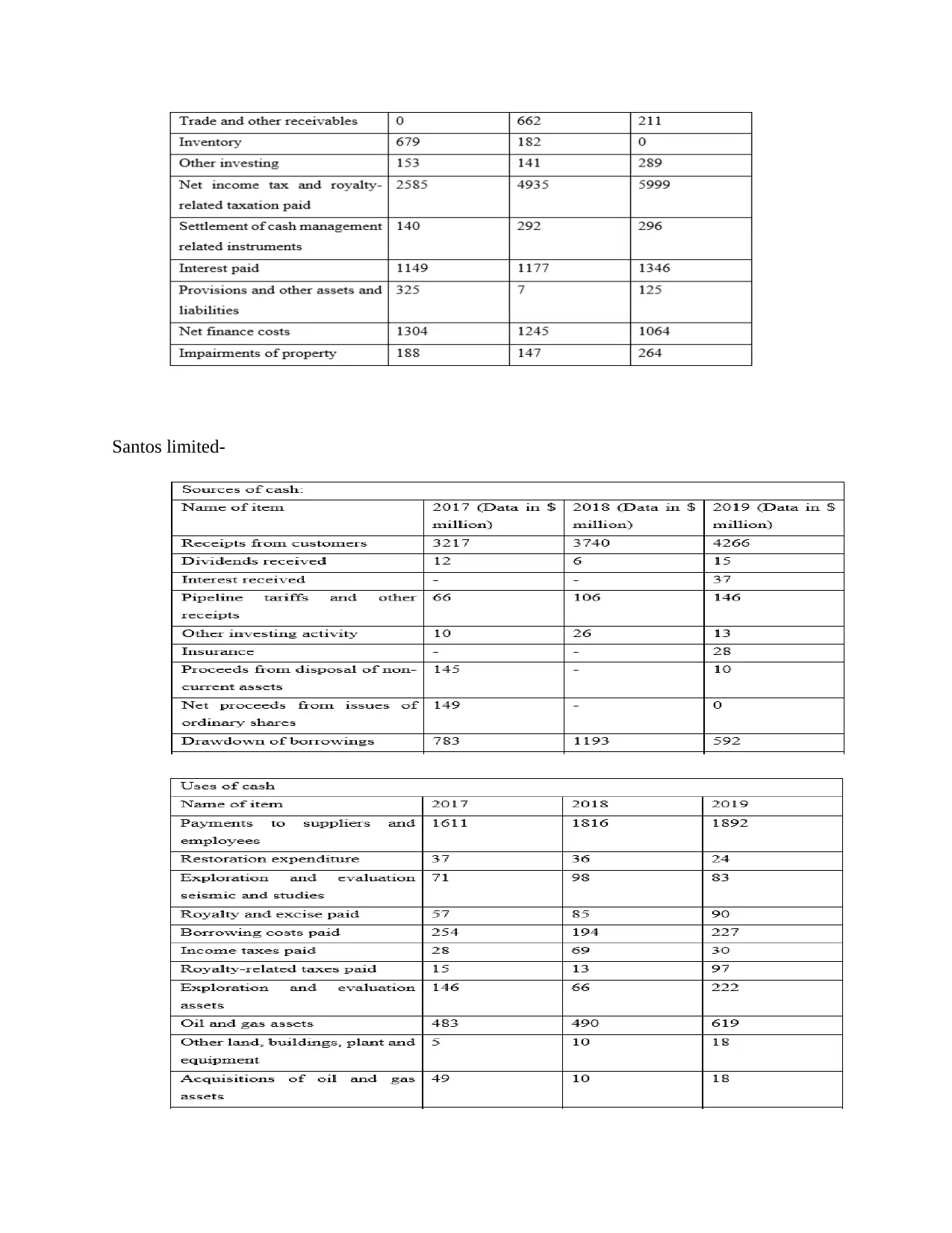

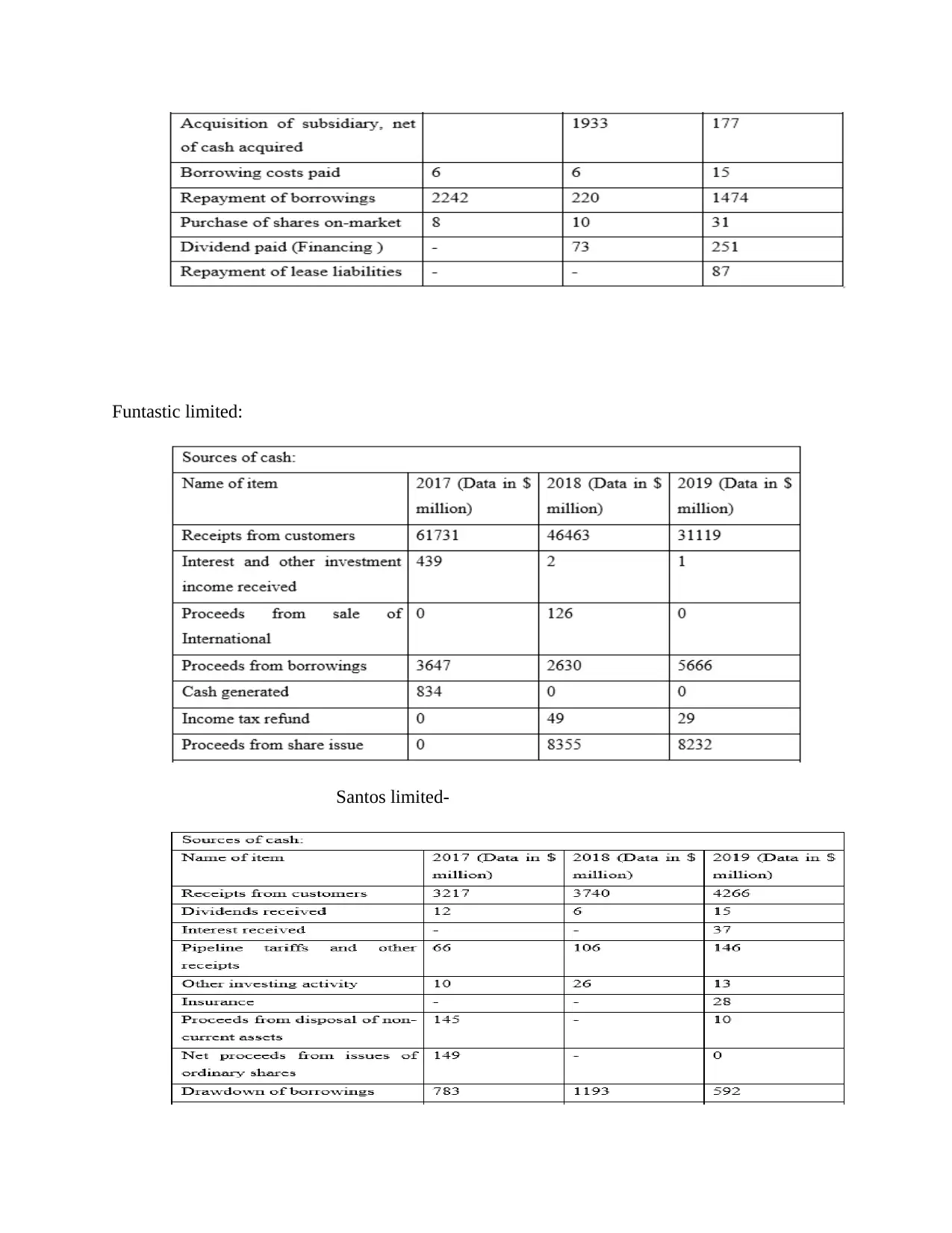

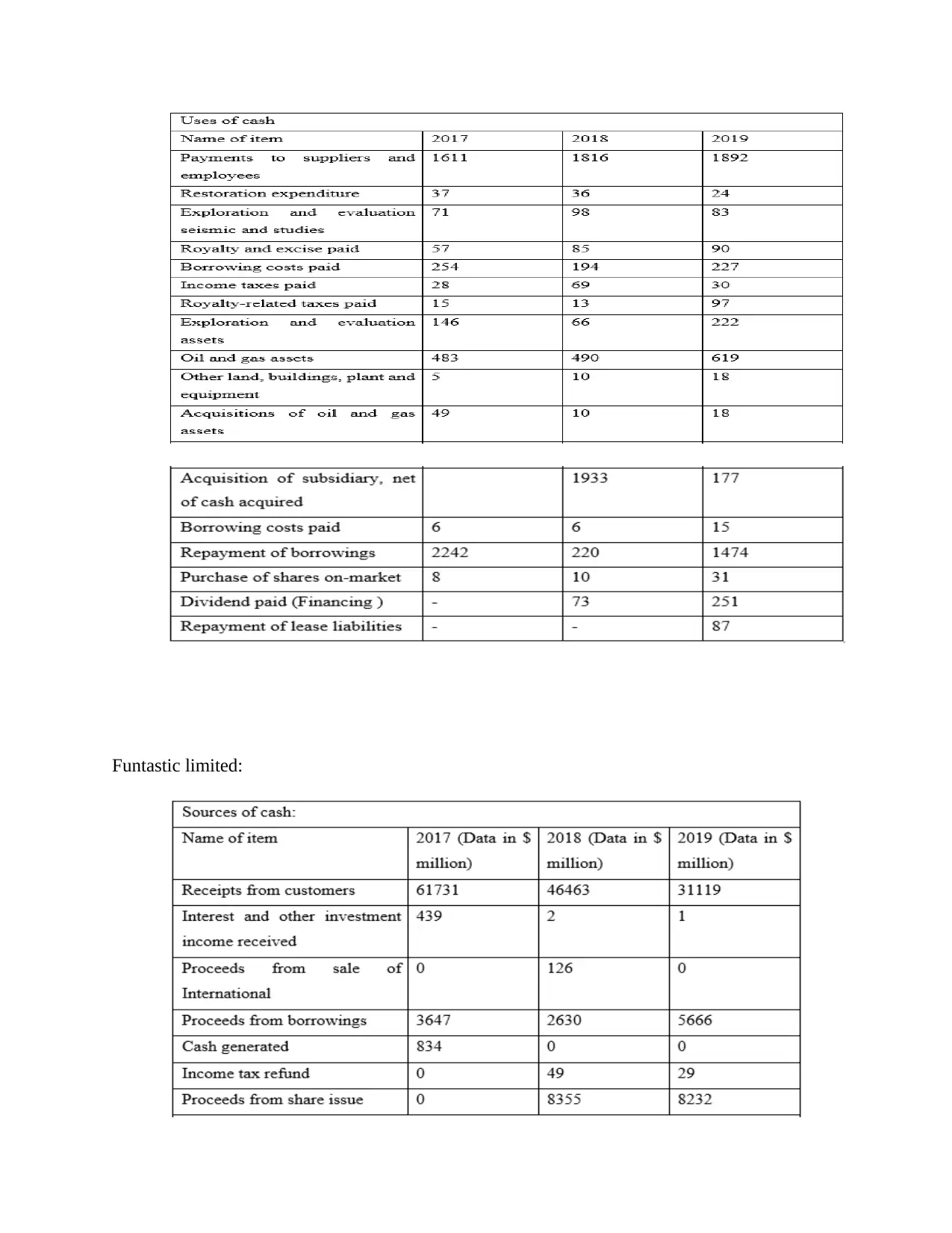

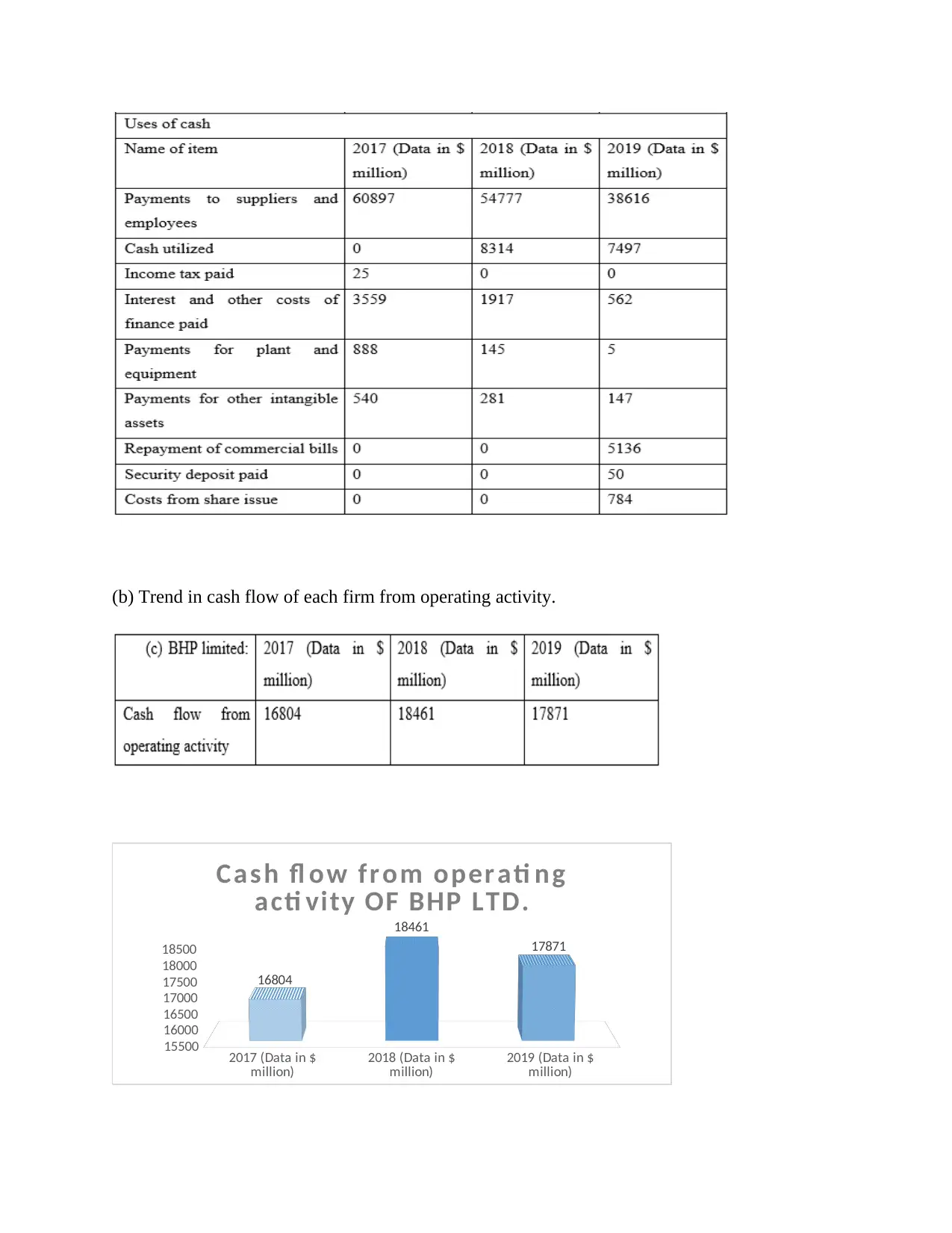

This report provides an in-depth analysis of corporate accounting, specifically focusing on the income statement and cash flow statement, and their significance for investors. The report details the components of each statement, including sales/revenues, cost of goods sold, gross profit, operating earnings, and net profit for the income statement, and cash flows from operating, investing, and financing activities for the cash flow statement. The study further examines and compares the consolidated cash flow statements of three companies: Santos Ltd, BHP Ltd, and Funtastic Ltd, from 2017 to 2019. The analysis includes an examination of the major sources and uses of cash for each firm, trends in cash flow from operating activities, and a comparison of cash flow from operations and net profit after tax. The report concludes by assessing whether each firm has sufficient cash flow to cover capital expenses, providing valuable insights into the financial performance and stability of the companies.

1 out of 31

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.