Corporate Accounting Project: 200109 Corporate Accounting Spring 2019

VerifiedAdded on 2022/10/01

|7

|540

|96

Project

AI Summary

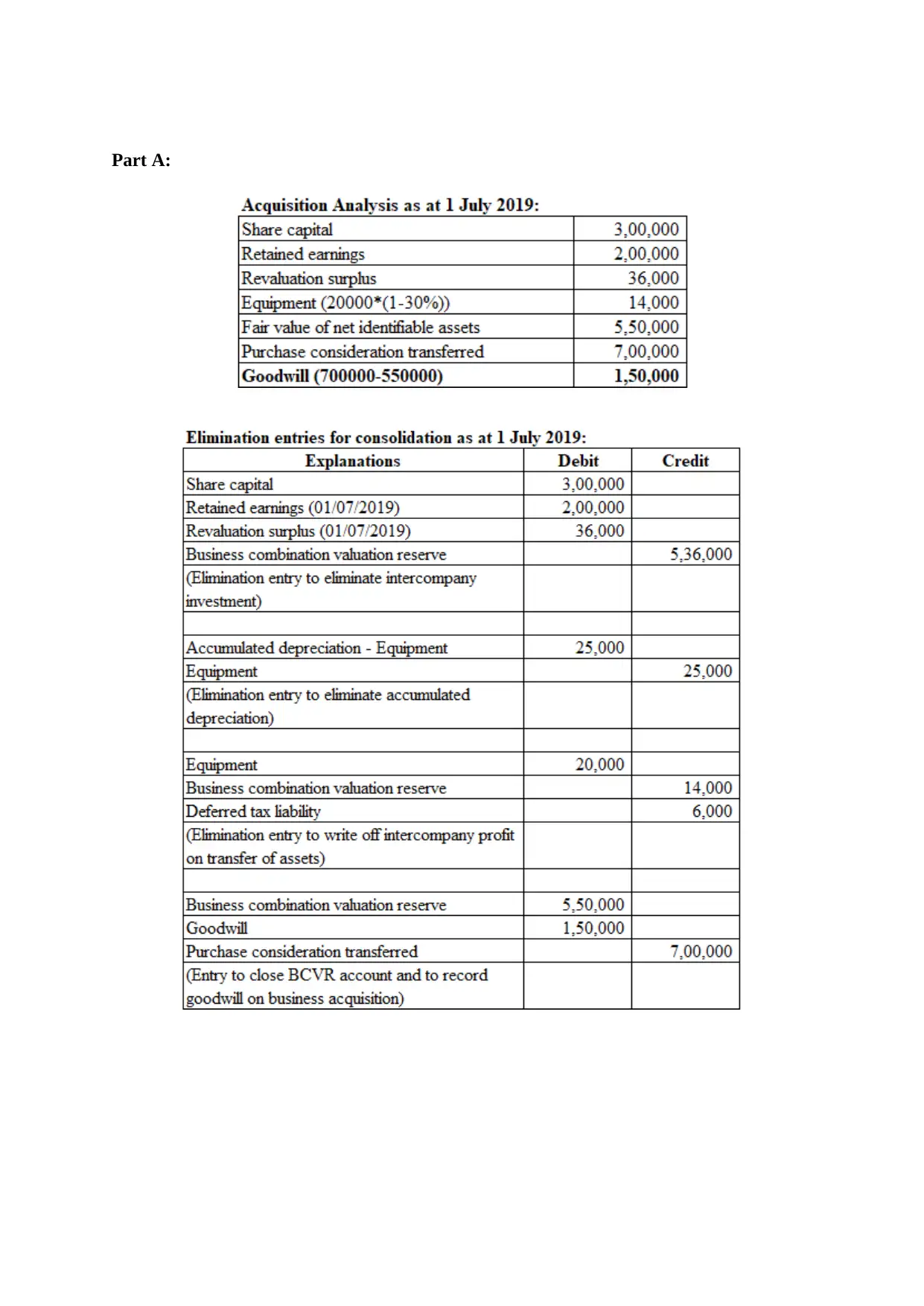

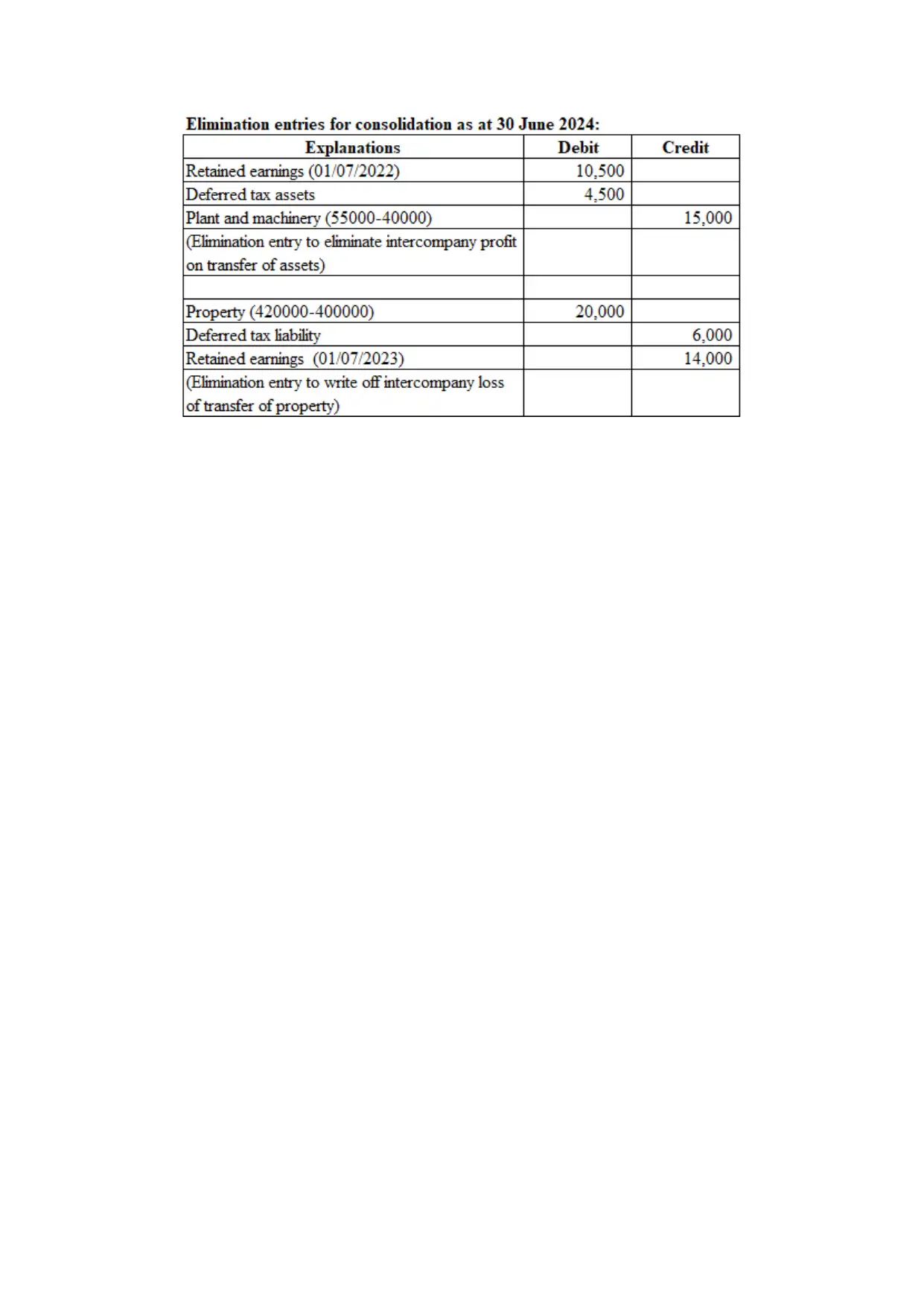

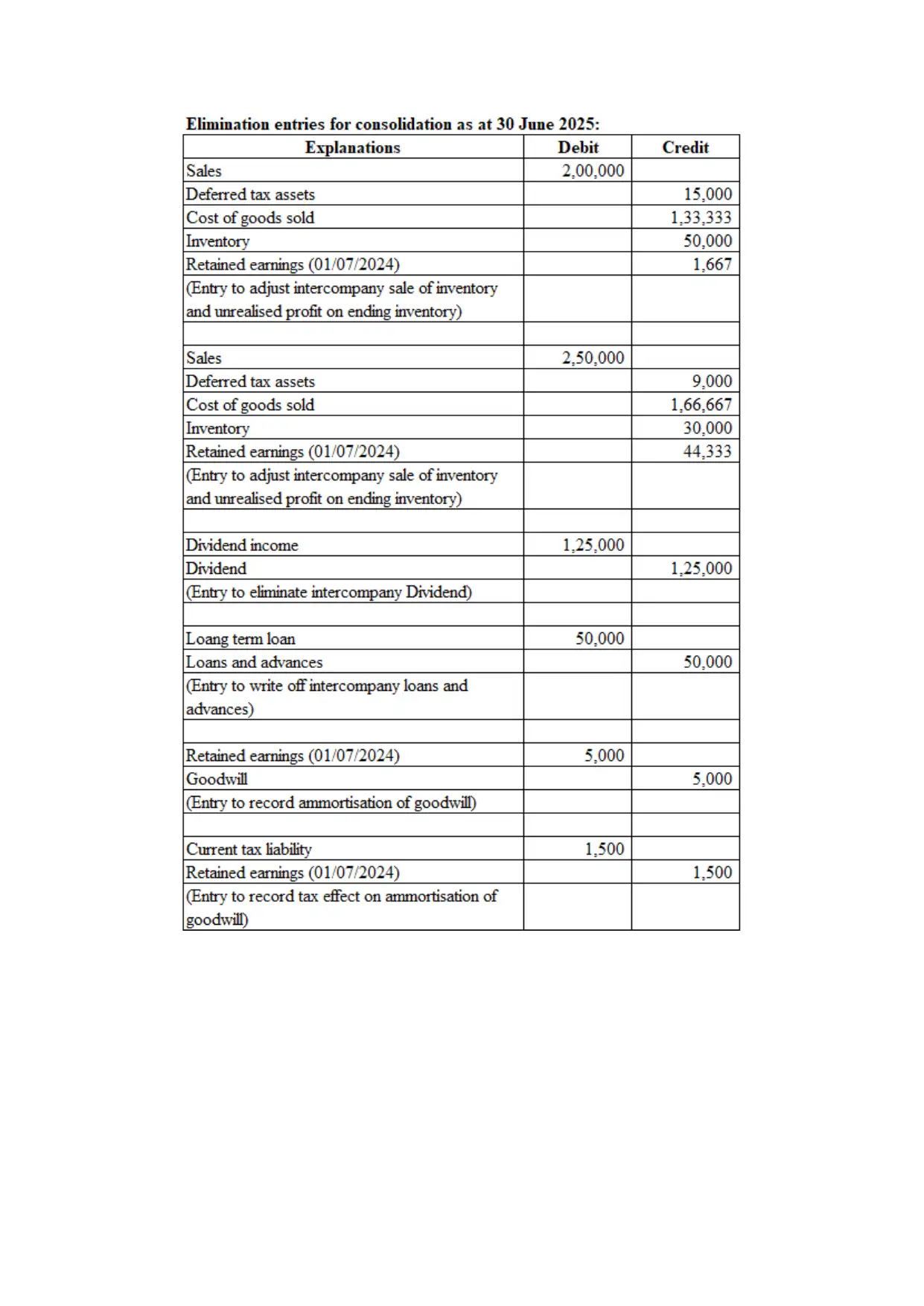

This project analyzes the acquisition of a subsidiary and the subsequent consolidation of financial statements, focusing on the case of Sunnybank Ltd acquiring Sunnybank Hills Ltd. It involves preparing consolidation elimination journals, addressing the fair valuation of assets, and discussing business combinations. The solution references relevant accounting standards like AASB 112 and AASB 10, explaining how deferred tax liabilities and assets are treated, and how tax losses of a subsidiary can be utilized by the parent company. The project covers aspects like share capital, retained earnings, and revaluation surplus, with a detailed explanation of the financial implications of the acquisition, including the adjustment of deferred tax liabilities and assets, and the utilization of tax losses. The solution presents a comprehensive understanding of corporate accounting principles, including the impact of mergers and acquisitions on financial reporting, and the application of relevant accounting standards.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.