Semester 2 ACT305 Corporate Accounting: Consolidation Assignment

VerifiedAdded on 2023/06/07

|18

|3270

|337

Homework Assignment

AI Summary

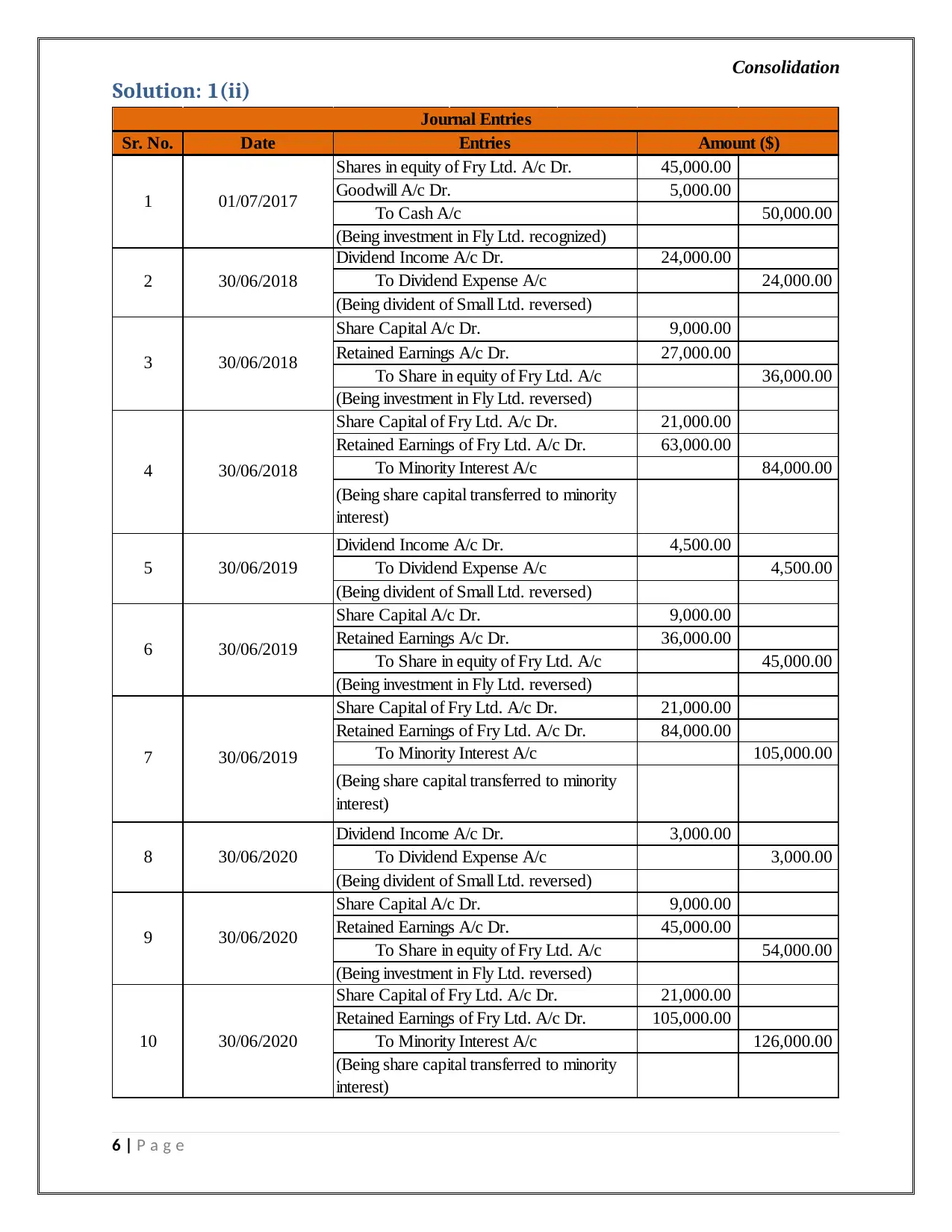

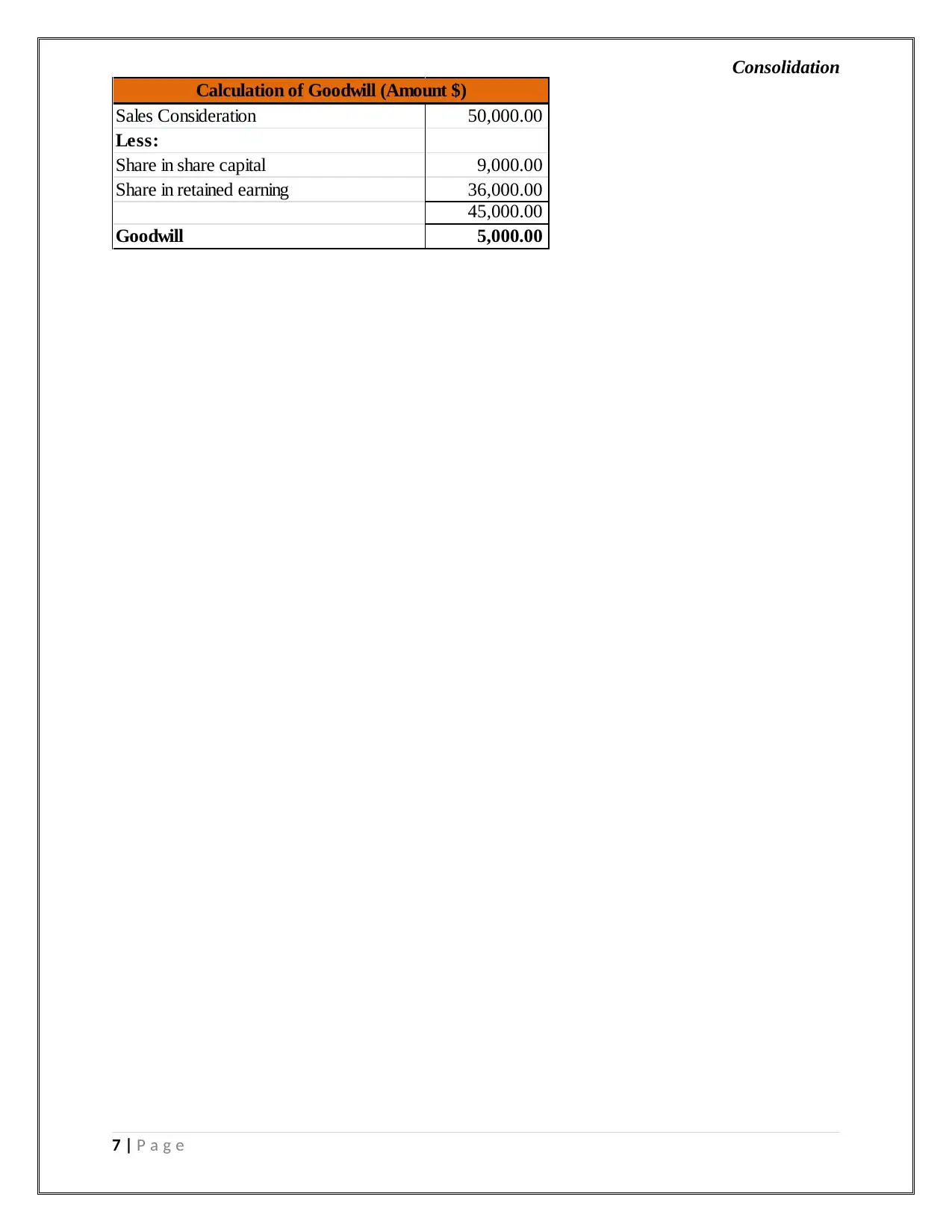

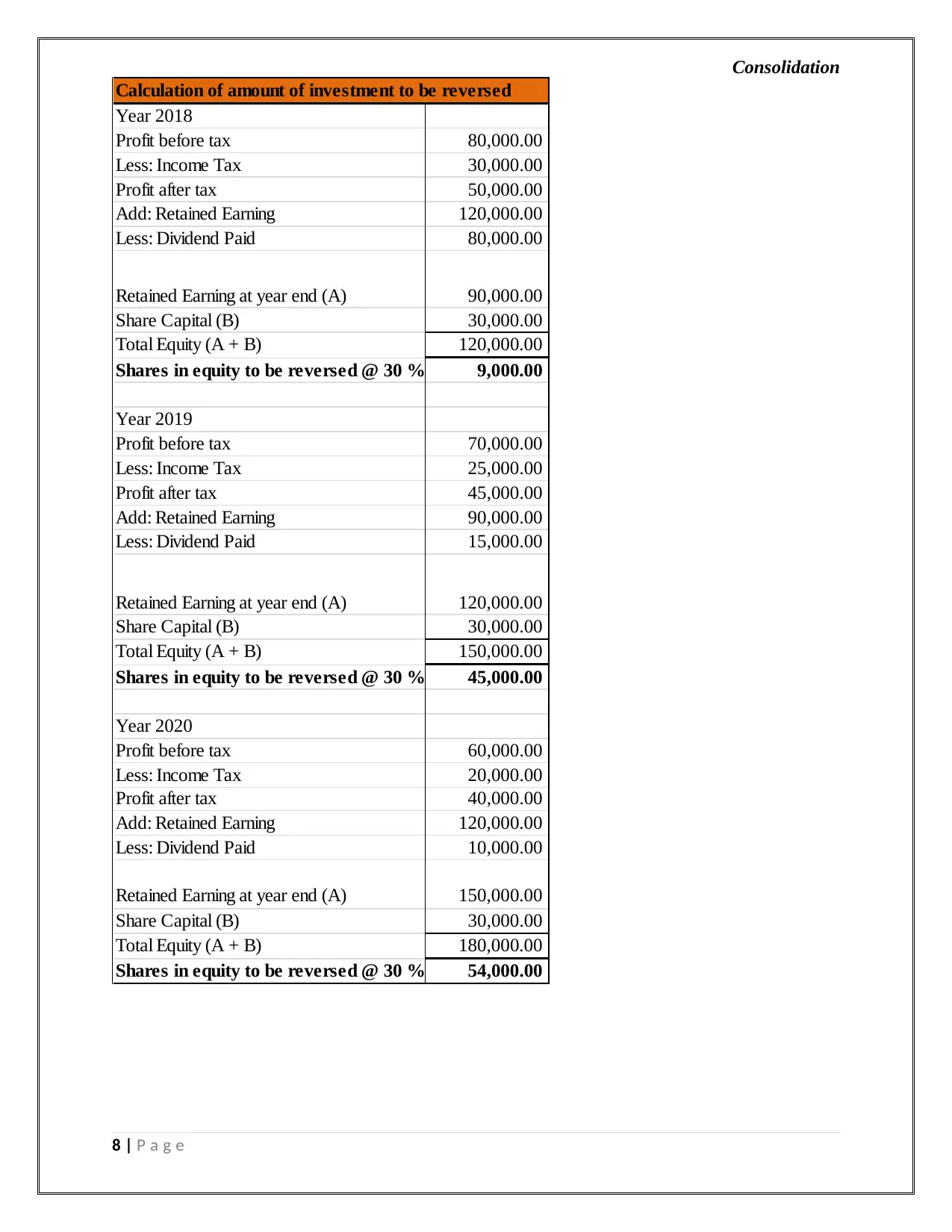

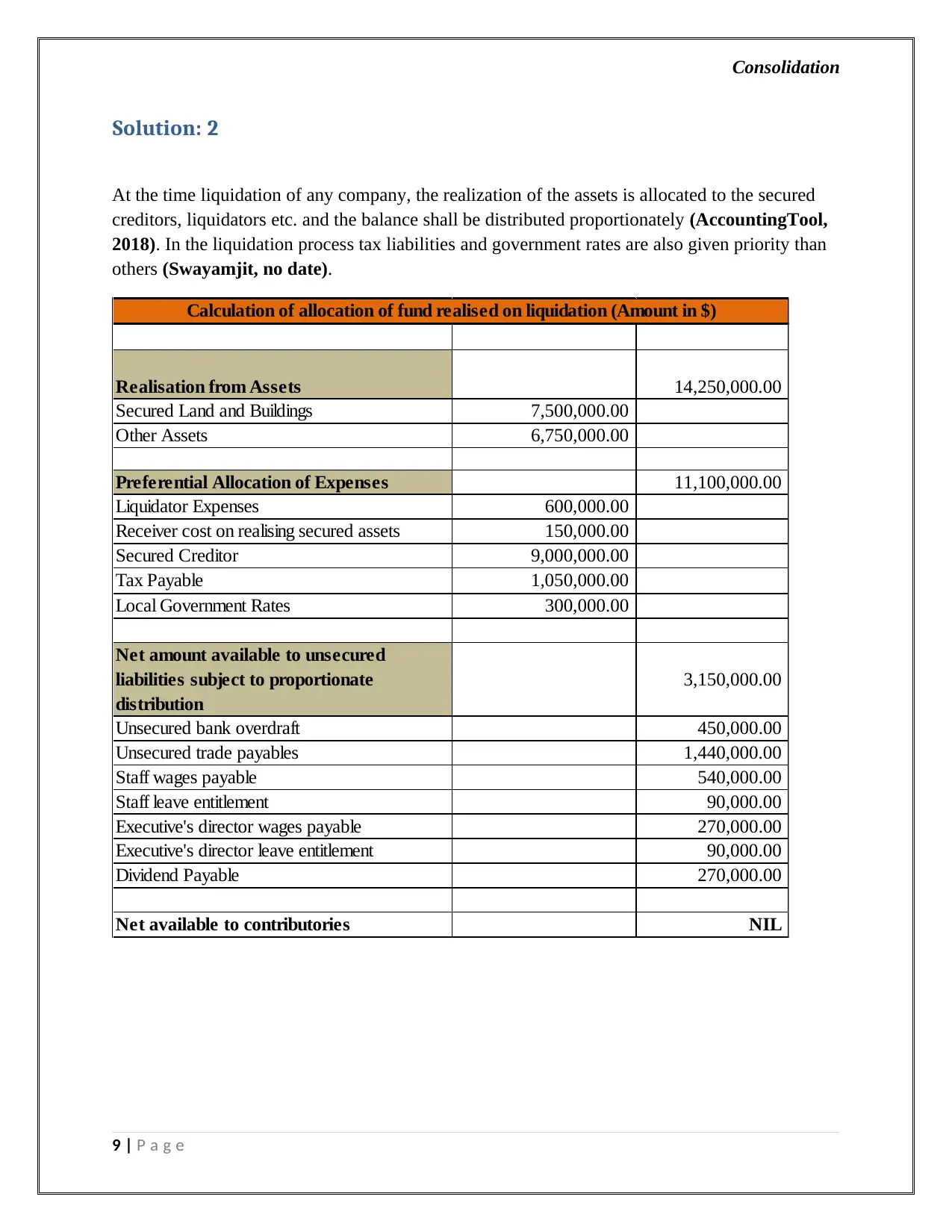

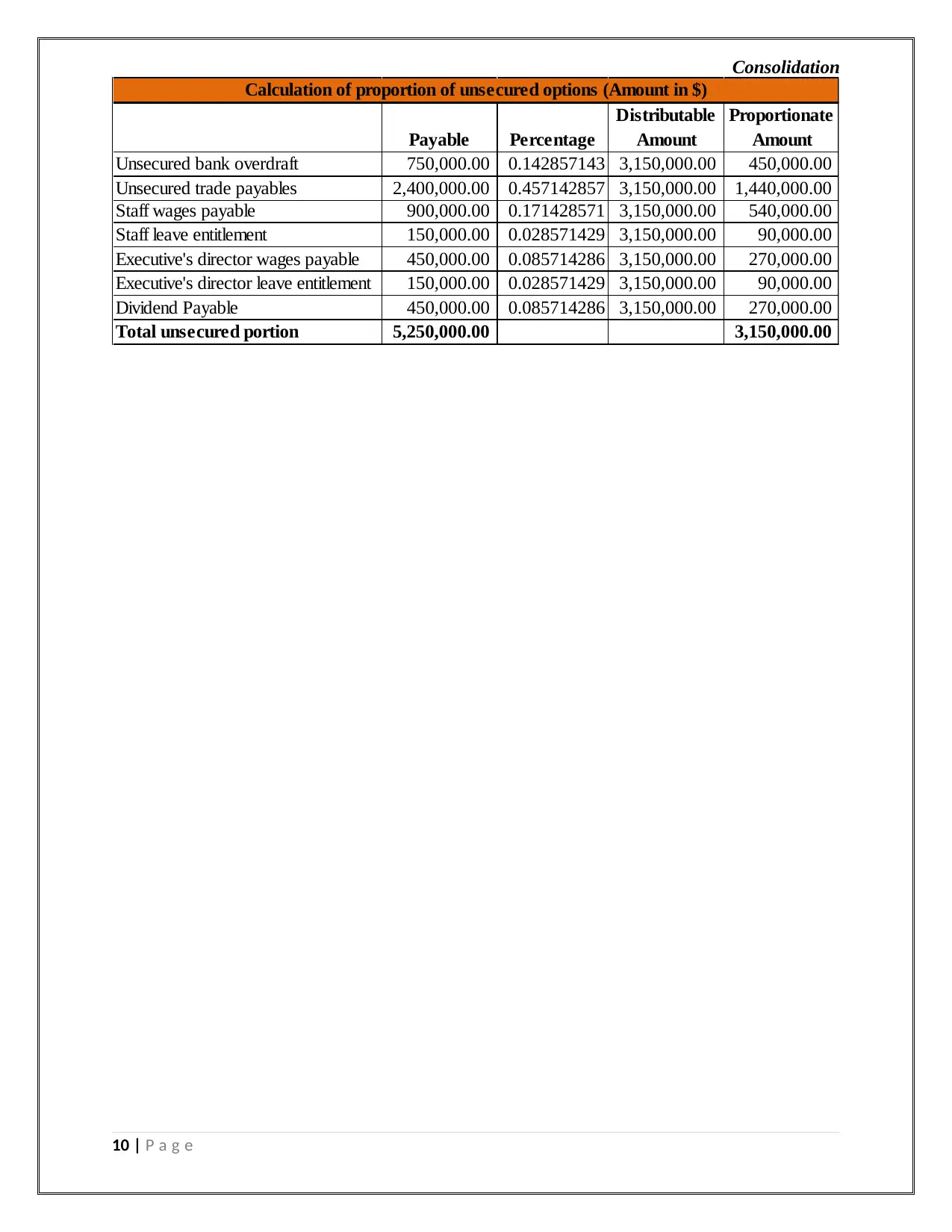

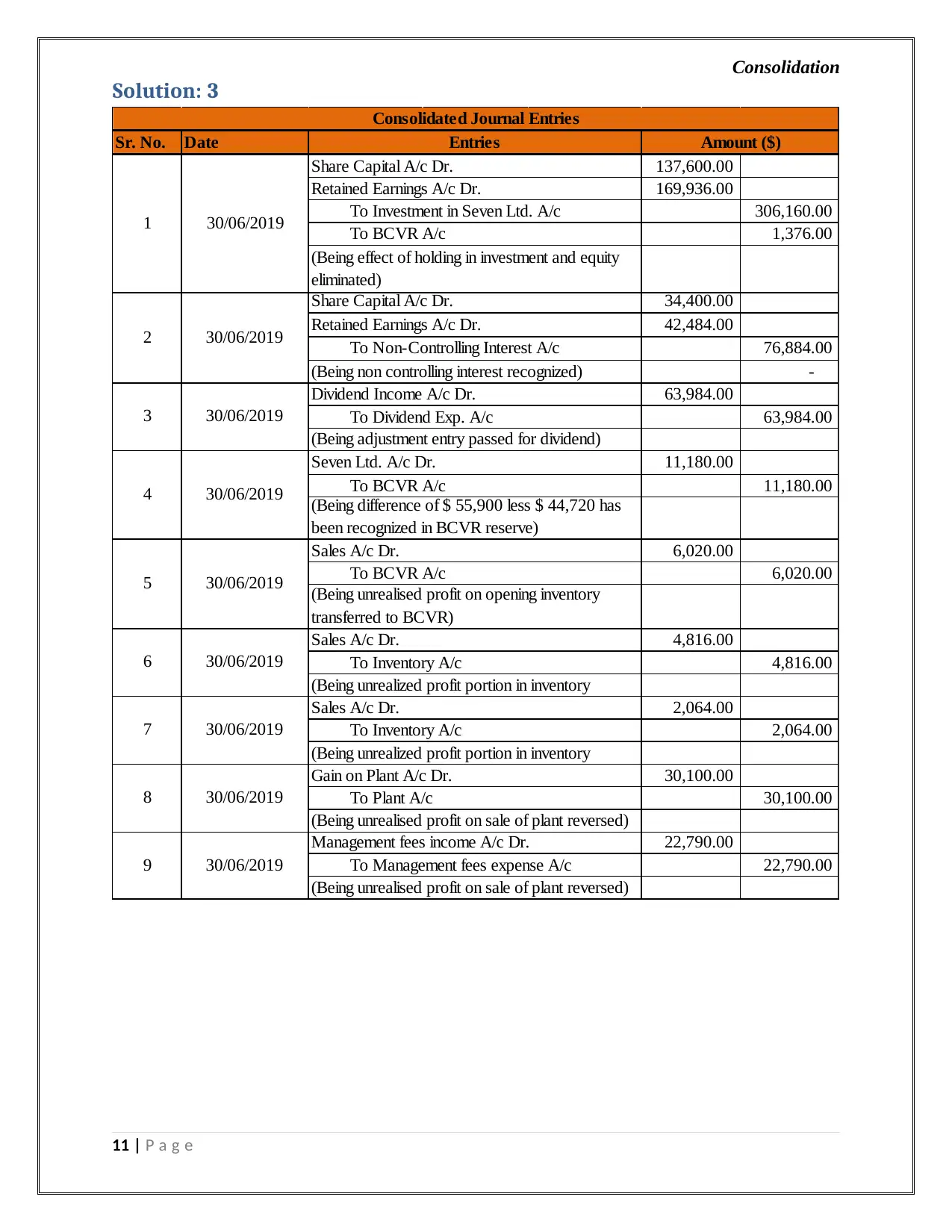

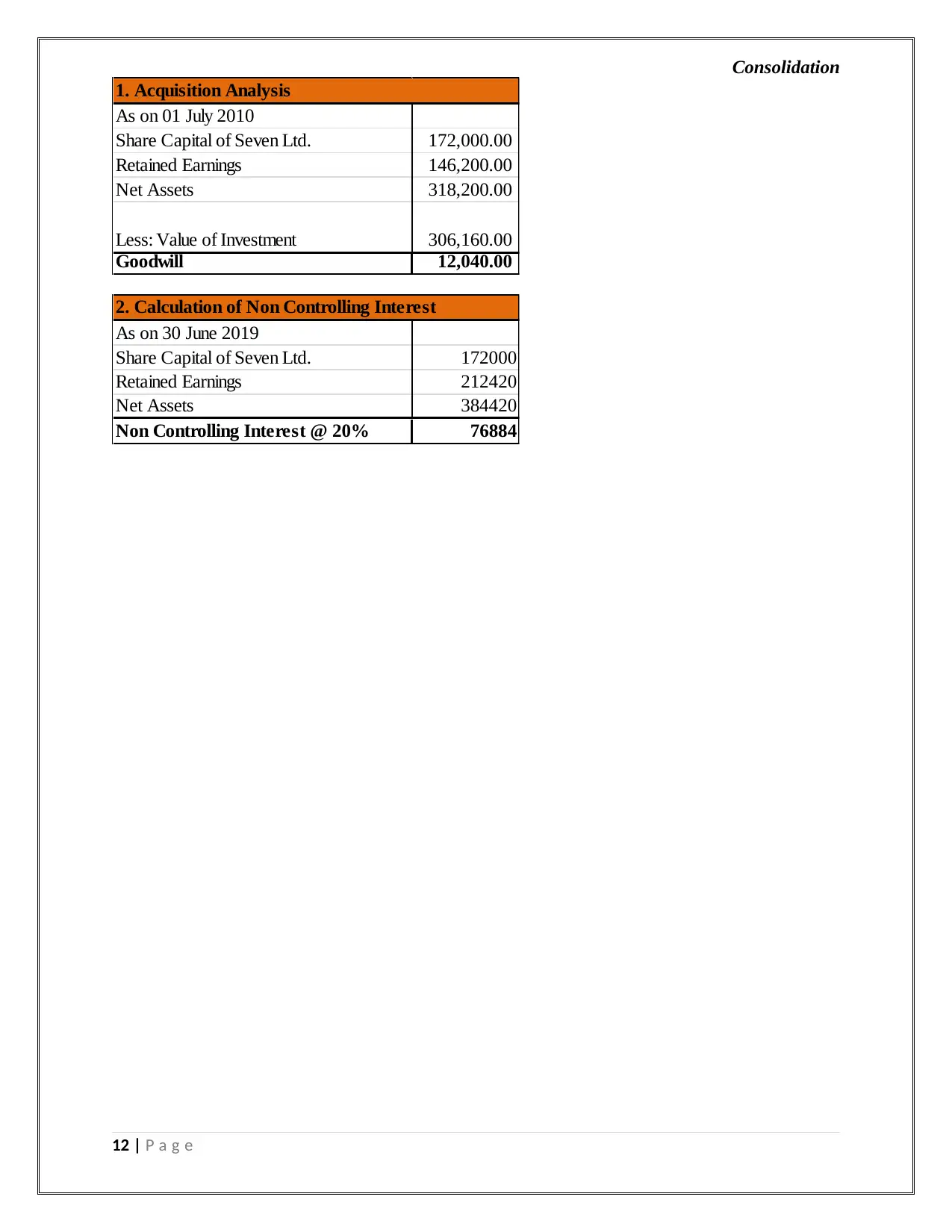

This document presents a detailed solution to a corporate accounting consolidation assignment, addressing several key areas. The solution begins by outlining the accounting treatment for investments in joint ventures, including journal entries for profit sharing and dividend payments, and calculating the investment value over multiple years. It then moves on to the consolidation of financial statements, including the calculation of goodwill and the reversal of investment in equity, and the allocation of funds during liquidation, detailing the distribution of assets to various stakeholders, including secured creditors, liquidators, and unsecured creditors, with a focus on preferential allocation. Furthermore, the assignment provides journal entries for consolidation, acquisition analysis, and calculation of non-controlling interest. Finally, the report analyzes a business scenario from the perspective of AASB 10, discussing the consolidation requirements for a company based on its investments and loans to other entities, and the factors influencing the decision to consolidate financial statements.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.