HA2032 Corporate Accounting: Consolidation Accounting and Takeover

VerifiedAdded on 2023/03/31

|9

|2841

|480

Report

AI Summary

This report delves into the intricacies of corporate accounting, focusing on consolidation processes during company takeovers, using the case of JKY Limited's acquisition of FAB Limited. It examines different accounting methods, including the equity and consolidation methods, highlighting their respective applications and drawbacks. The report further discusses the treatment of intra-group transactions, particularly unrealized profits arising from inventory sales between parent and subsidiary companies, and emphasizes the importance of eliminating these profits to ensure accurate consolidated financial statements. Additionally, it addresses the disclosure requirements for non-controlling interests (NCI) and their impact on the consolidation process, emphasizing the need for separate and distinct presentation of NCI in financial statements. The report also highlights the importance of adhering to accounting standards to provide stakeholders with reliable and transparent financial information.

Running head: Corporate Accounting

Corporate Accounting

Name of the Student

Name of the University

Author Note

Corporate Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Corporate Accounting

Executive Summary

The report show about the consolidation process how it help the company at the time

of the acquiring the company. It show about the transaction happen between the

parent and subsidiary company and also how to deal with the unrealised profit and

also the accounting and the disclosure which is to be done by the company in

regards of thee non-controlling interest

Corporate Accounting

Executive Summary

The report show about the consolidation process how it help the company at the time

of the acquiring the company. It show about the transaction happen between the

parent and subsidiary company and also how to deal with the unrealised profit and

also the accounting and the disclosure which is to be done by the company in

regards of thee non-controlling interest

2

Corporate Accounting

Table of Contents

Introduction...................................................................................................................3

Section A.......................................................................................................................3

Section B.......................................................................................................................5

Section C......................................................................................................................6

Conclusion....................................................................................................................7

References...................................................................................................................9

Corporate Accounting

Table of Contents

Introduction...................................................................................................................3

Section A.......................................................................................................................3

Section B.......................................................................................................................5

Section C......................................................................................................................6

Conclusion....................................................................................................................7

References...................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Corporate Accounting

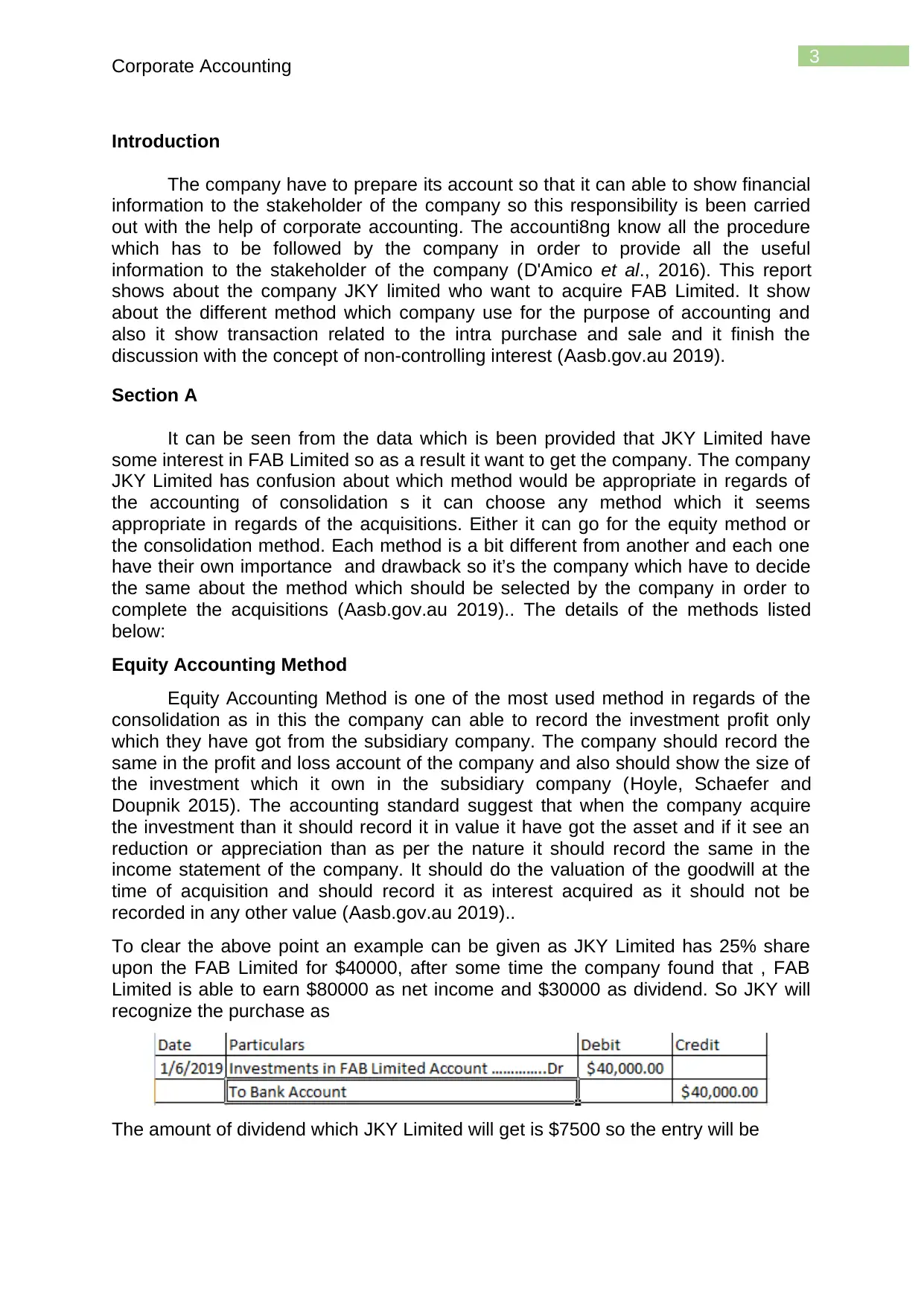

Introduction

The company have to prepare its account so that it can able to show financial

information to the stakeholder of the company so this responsibility is been carried

out with the help of corporate accounting. The accounti8ng know all the procedure

which has to be followed by the company in order to provide all the useful

information to the stakeholder of the company (D'Amico et al., 2016). This report

shows about the company JKY limited who want to acquire FAB Limited. It show

about the different method which company use for the purpose of accounting and

also it show transaction related to the intra purchase and sale and it finish the

discussion with the concept of non-controlling interest (Aasb.gov.au 2019).

Section A

It can be seen from the data which is been provided that JKY Limited have

some interest in FAB Limited so as a result it want to get the company. The company

JKY Limited has confusion about which method would be appropriate in regards of

the accounting of consolidation s it can choose any method which it seems

appropriate in regards of the acquisitions. Either it can go for the equity method or

the consolidation method. Each method is a bit different from another and each one

have their own importance and drawback so it’s the company which have to decide

the same about the method which should be selected by the company in order to

complete the acquisitions (Aasb.gov.au 2019).. The details of the methods listed

below:

Equity Accounting Method

Equity Accounting Method is one of the most used method in regards of the

consolidation as in this the company can able to record the investment profit only

which they have got from the subsidiary company. The company should record the

same in the profit and loss account of the company and also should show the size of

the investment which it own in the subsidiary company (Hoyle, Schaefer and

Doupnik 2015). The accounting standard suggest that when the company acquire

the investment than it should record it in value it have got the asset and if it see an

reduction or appreciation than as per the nature it should record the same in the

income statement of the company. It should do the valuation of the goodwill at the

time of acquisition and should record it as interest acquired as it should not be

recorded in any other value (Aasb.gov.au 2019)..

To clear the above point an example can be given as JKY Limited has 25% share

upon the FAB Limited for $40000, after some time the company found that , FAB

Limited is able to earn $80000 as net income and $30000 as dividend. So JKY will

recognize the purchase as

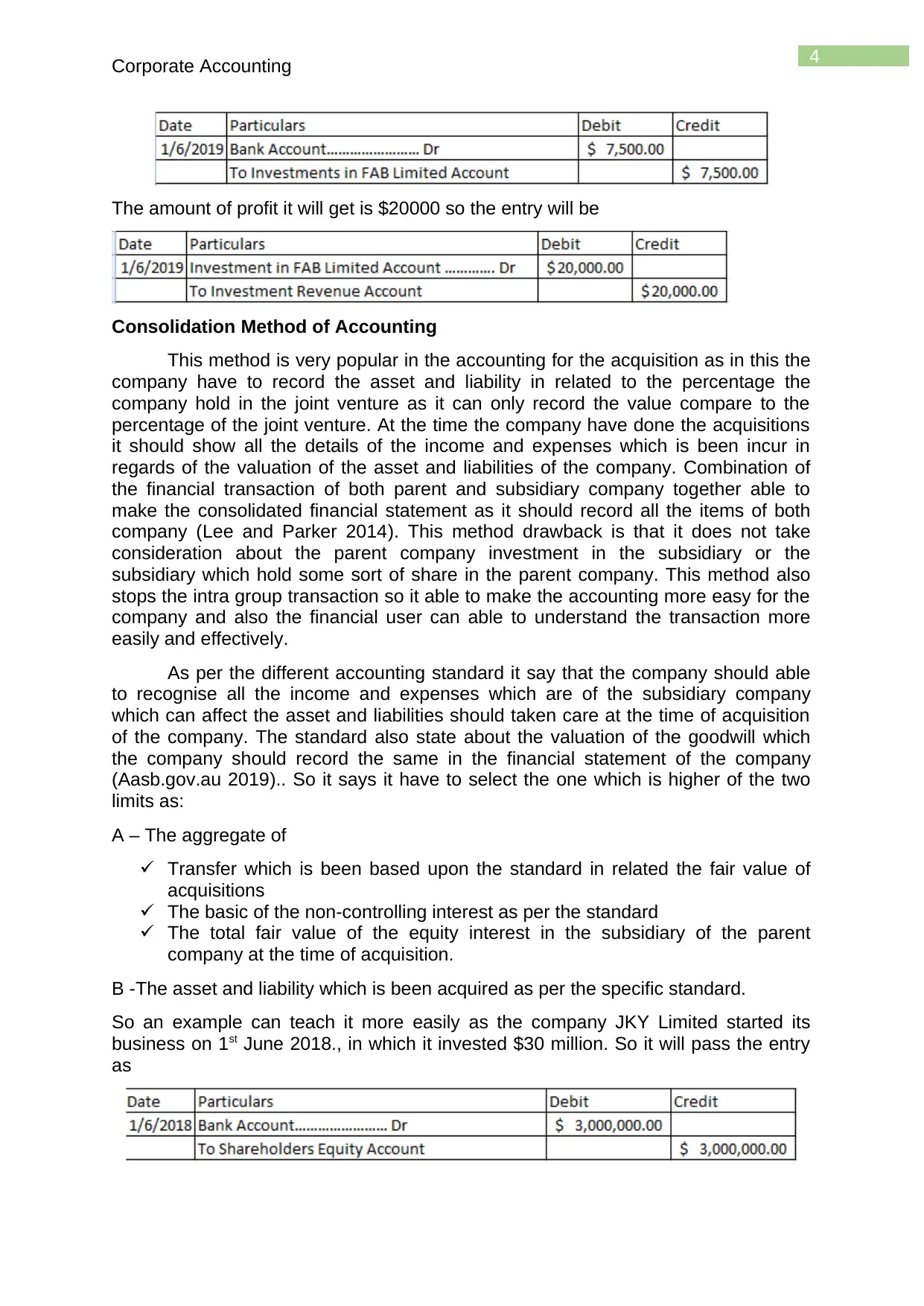

The amount of dividend which JKY Limited will get is $7500 so the entry will be

Corporate Accounting

Introduction

The company have to prepare its account so that it can able to show financial

information to the stakeholder of the company so this responsibility is been carried

out with the help of corporate accounting. The accounti8ng know all the procedure

which has to be followed by the company in order to provide all the useful

information to the stakeholder of the company (D'Amico et al., 2016). This report

shows about the company JKY limited who want to acquire FAB Limited. It show

about the different method which company use for the purpose of accounting and

also it show transaction related to the intra purchase and sale and it finish the

discussion with the concept of non-controlling interest (Aasb.gov.au 2019).

Section A

It can be seen from the data which is been provided that JKY Limited have

some interest in FAB Limited so as a result it want to get the company. The company

JKY Limited has confusion about which method would be appropriate in regards of

the accounting of consolidation s it can choose any method which it seems

appropriate in regards of the acquisitions. Either it can go for the equity method or

the consolidation method. Each method is a bit different from another and each one

have their own importance and drawback so it’s the company which have to decide

the same about the method which should be selected by the company in order to

complete the acquisitions (Aasb.gov.au 2019).. The details of the methods listed

below:

Equity Accounting Method

Equity Accounting Method is one of the most used method in regards of the

consolidation as in this the company can able to record the investment profit only

which they have got from the subsidiary company. The company should record the

same in the profit and loss account of the company and also should show the size of

the investment which it own in the subsidiary company (Hoyle, Schaefer and

Doupnik 2015). The accounting standard suggest that when the company acquire

the investment than it should record it in value it have got the asset and if it see an

reduction or appreciation than as per the nature it should record the same in the

income statement of the company. It should do the valuation of the goodwill at the

time of acquisition and should record it as interest acquired as it should not be

recorded in any other value (Aasb.gov.au 2019)..

To clear the above point an example can be given as JKY Limited has 25% share

upon the FAB Limited for $40000, after some time the company found that , FAB

Limited is able to earn $80000 as net income and $30000 as dividend. So JKY will

recognize the purchase as

The amount of dividend which JKY Limited will get is $7500 so the entry will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Corporate Accounting

The amount of profit it will get is $20000 so the entry will be

Consolidation Method of Accounting

This method is very popular in the accounting for the acquisition as in this the

company have to record the asset and liability in related to the percentage the

company hold in the joint venture as it can only record the value compare to the

percentage of the joint venture. At the time the company have done the acquisitions

it should show all the details of the income and expenses which is been incur in

regards of the valuation of the asset and liabilities of the company. Combination of

the financial transaction of both parent and subsidiary company together able to

make the consolidated financial statement as it should record all the items of both

company (Lee and Parker 2014). This method drawback is that it does not take

consideration about the parent company investment in the subsidiary or the

subsidiary which hold some sort of share in the parent company. This method also

stops the intra group transaction so it able to make the accounting more easy for the

company and also the financial user can able to understand the transaction more

easily and effectively.

As per the different accounting standard it say that the company should able

to recognise all the income and expenses which are of the subsidiary company

which can affect the asset and liabilities should taken care at the time of acquisition

of the company. The standard also state about the valuation of the goodwill which

the company should record the same in the financial statement of the company

(Aasb.gov.au 2019).. So it says it have to select the one which is higher of the two

limits as:

A – The aggregate of

Transfer which is been based upon the standard in related the fair value of

acquisitions

The basic of the non-controlling interest as per the standard

The total fair value of the equity interest in the subsidiary of the parent

company at the time of acquisition.

B -The asset and liability which is been acquired as per the specific standard.

So an example can teach it more easily as the company JKY Limited started its

business on 1st June 2018., in which it invested $30 million. So it will pass the entry

as

Corporate Accounting

The amount of profit it will get is $20000 so the entry will be

Consolidation Method of Accounting

This method is very popular in the accounting for the acquisition as in this the

company have to record the asset and liability in related to the percentage the

company hold in the joint venture as it can only record the value compare to the

percentage of the joint venture. At the time the company have done the acquisitions

it should show all the details of the income and expenses which is been incur in

regards of the valuation of the asset and liabilities of the company. Combination of

the financial transaction of both parent and subsidiary company together able to

make the consolidated financial statement as it should record all the items of both

company (Lee and Parker 2014). This method drawback is that it does not take

consideration about the parent company investment in the subsidiary or the

subsidiary which hold some sort of share in the parent company. This method also

stops the intra group transaction so it able to make the accounting more easy for the

company and also the financial user can able to understand the transaction more

easily and effectively.

As per the different accounting standard it say that the company should able

to recognise all the income and expenses which are of the subsidiary company

which can affect the asset and liabilities should taken care at the time of acquisition

of the company. The standard also state about the valuation of the goodwill which

the company should record the same in the financial statement of the company

(Aasb.gov.au 2019).. So it says it have to select the one which is higher of the two

limits as:

A – The aggregate of

Transfer which is been based upon the standard in related the fair value of

acquisitions

The basic of the non-controlling interest as per the standard

The total fair value of the equity interest in the subsidiary of the parent

company at the time of acquisition.

B -The asset and liability which is been acquired as per the specific standard.

So an example can teach it more easily as the company JKY Limited started its

business on 1st June 2018., in which it invested $30 million. So it will pass the entry

as

5

Corporate Accounting

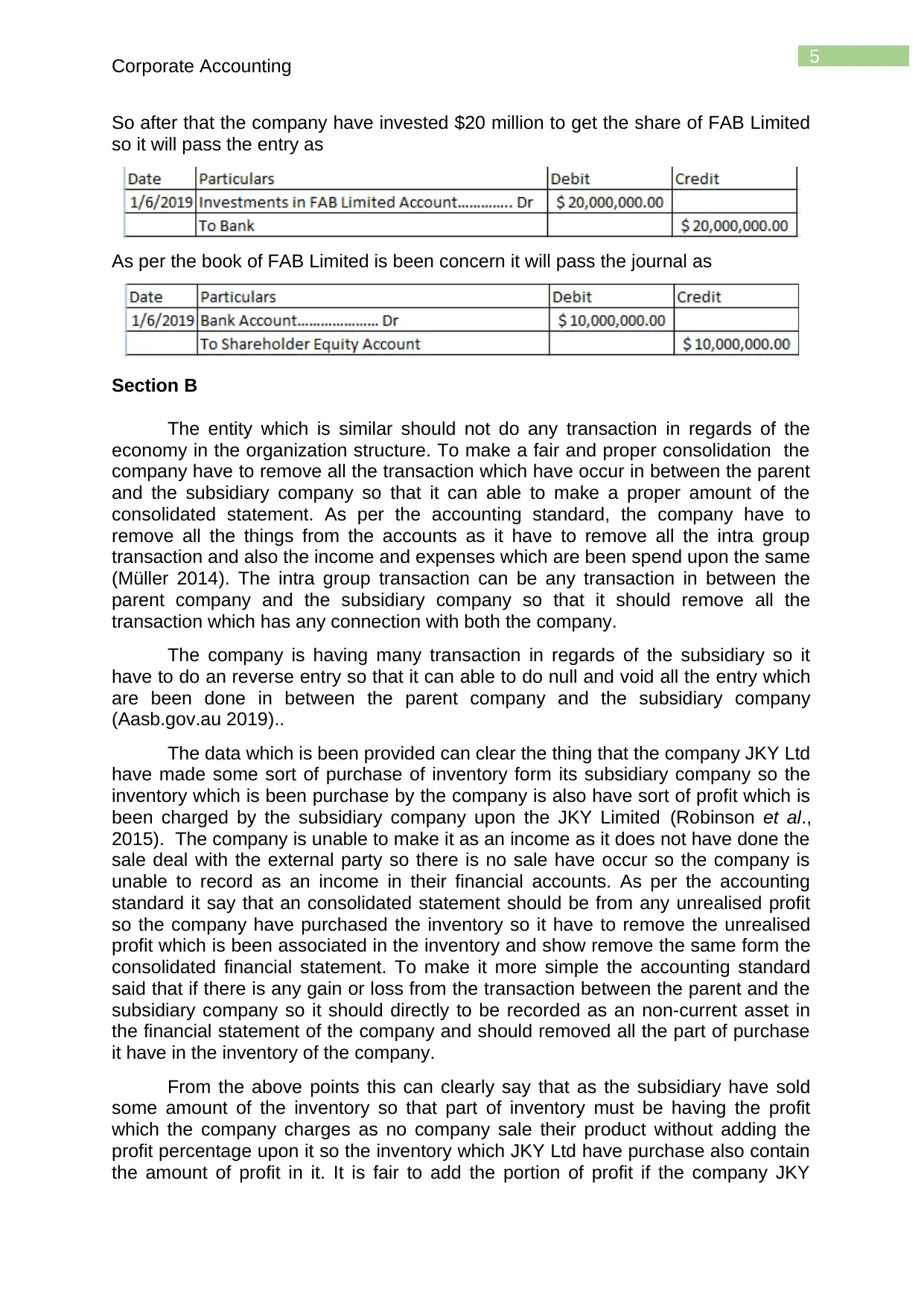

So after that the company have invested $20 million to get the share of FAB Limited

so it will pass the entry as

As per the book of FAB Limited is been concern it will pass the journal as

Section B

The entity which is similar should not do any transaction in regards of the

economy in the organization structure. To make a fair and proper consolidation the

company have to remove all the transaction which have occur in between the parent

and the subsidiary company so that it can able to make a proper amount of the

consolidated statement. As per the accounting standard, the company have to

remove all the things from the accounts as it have to remove all the intra group

transaction and also the income and expenses which are been spend upon the same

(Müller 2014). The intra group transaction can be any transaction in between the

parent company and the subsidiary company so that it should remove all the

transaction which has any connection with both the company.

The company is having many transaction in regards of the subsidiary so it

have to do an reverse entry so that it can able to do null and void all the entry which

are been done in between the parent company and the subsidiary company

(Aasb.gov.au 2019)..

The data which is been provided can clear the thing that the company JKY Ltd

have made some sort of purchase of inventory form its subsidiary company so the

inventory which is been purchase by the company is also have sort of profit which is

been charged by the subsidiary company upon the JKY Limited (Robinson et al.,

2015). The company is unable to make it as an income as it does not have done the

sale deal with the external party so there is no sale have occur so the company is

unable to record as an income in their financial accounts. As per the accounting

standard it say that an consolidated statement should be from any unrealised profit

so the company have purchased the inventory so it have to remove the unrealised

profit which is been associated in the inventory and show remove the same form the

consolidated financial statement. To make it more simple the accounting standard

said that if there is any gain or loss from the transaction between the parent and the

subsidiary company so it should directly to be recorded as an non-current asset in

the financial statement of the company and should removed all the part of purchase

it have in the inventory of the company.

From the above points this can clearly say that as the subsidiary have sold

some amount of the inventory so that part of inventory must be having the profit

which the company charges as no company sale their product without adding the

profit percentage upon it so the inventory which JKY Ltd have purchase also contain

the amount of profit in it. It is fair to add the portion of profit if the company JKY

Corporate Accounting

So after that the company have invested $20 million to get the share of FAB Limited

so it will pass the entry as

As per the book of FAB Limited is been concern it will pass the journal as

Section B

The entity which is similar should not do any transaction in regards of the

economy in the organization structure. To make a fair and proper consolidation the

company have to remove all the transaction which have occur in between the parent

and the subsidiary company so that it can able to make a proper amount of the

consolidated statement. As per the accounting standard, the company have to

remove all the things from the accounts as it have to remove all the intra group

transaction and also the income and expenses which are been spend upon the same

(Müller 2014). The intra group transaction can be any transaction in between the

parent company and the subsidiary company so that it should remove all the

transaction which has any connection with both the company.

The company is having many transaction in regards of the subsidiary so it

have to do an reverse entry so that it can able to do null and void all the entry which

are been done in between the parent company and the subsidiary company

(Aasb.gov.au 2019)..

The data which is been provided can clear the thing that the company JKY Ltd

have made some sort of purchase of inventory form its subsidiary company so the

inventory which is been purchase by the company is also have sort of profit which is

been charged by the subsidiary company upon the JKY Limited (Robinson et al.,

2015). The company is unable to make it as an income as it does not have done the

sale deal with the external party so there is no sale have occur so the company is

unable to record as an income in their financial accounts. As per the accounting

standard it say that an consolidated statement should be from any unrealised profit

so the company have purchased the inventory so it have to remove the unrealised

profit which is been associated in the inventory and show remove the same form the

consolidated financial statement. To make it more simple the accounting standard

said that if there is any gain or loss from the transaction between the parent and the

subsidiary company so it should directly to be recorded as an non-current asset in

the financial statement of the company and should removed all the part of purchase

it have in the inventory of the company.

From the above points this can clearly say that as the subsidiary have sold

some amount of the inventory so that part of inventory must be having the profit

which the company charges as no company sale their product without adding the

profit percentage upon it so the inventory which JKY Ltd have purchase also contain

the amount of profit in it. It is fair to add the portion of profit if the company JKY

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Corporate Accounting

Limited could have able to generated cash for the part of inventory which they have

purchase from the subsidiary and also add a good sign to the group profit of the

company but as the case suggest it does not able to enter into agreement of the sale

of the inventory which it got from the subsidiary company. As the company have not

able to sale but the subsidiary have recorded the profit which they have earn form

the parent company as a result the overall group profit have an unrealised profit in its

which is not a good sign for the company overall profit. As due to the subsidiary the

company overall profit is been overstated and it show an increase value so this can

do fraud with the company financial user as they are not aware about the overstated

profit by the company. So this above point can be more clear with an proper example

as it can be seen that the company have purchased the good so let assume the

amount was $50000 which they does not able to sale in the current period and a

result it able to show in the end of the year. The subsidiary company holds a 50%

profit in the goods they have sold to the JKY Limited so the profit which the

subsidiary company could able to earn is $16667 (50/150* $50000). So this clear

that the group profit of the company is been overstated by $16667 so the company

have to make an proper adjustment entry in regard to eliminate the part of profit so

the entry will be

Consolidated Profit Account Dr $16667

To Consolidated Inventory Account $16667

So this entry rectifies the error which was done by the subsidiary company in regards

of the unrealised profit for the firm. So it show that each company should remove the

unrealised profit which they have earn so it show also what is to be done in regards

of the unrealised gain related to the non-controlling interest of the company. To

record the gain there can be various method as the company can able to record the

gain in the non-controlling interest so that it will null and void all the profit which the

company is able to get from the selling of their product. Otherwise they can able to

go for that they does not record any amount of the profit so that it will not affect the

overall profit of the group and the non-controlling should be there in the capital and

reserve which the company get from the acquiring the subsidiary company.

Section C

Effects of the NCI disclosure requirement in regards to the separate item in the

process of consolidation:

The company should do the presentation of the non-controlling asset

differently and separately in regards of the interest which they have earn form the

equity which they hold in the parent company. The company which is acquiring the

other company cannot able to record anything related to the Non-controlling Interest

as it is directly related to the equity of the subsidiary company so this should not be

recorded in the financial statement of the parent company (Aasb.gov.au 2019).. This

section of the standard help the parent company to get more knowledge about how

they should record each kind of interest which they are able to get from its subsidiary

company and also able to know how they should report in the consolidated financial

statement so that there is not error of accounting is been done by the parent

company. As the consolidated statement is been concern it show that the entity

should report non-controlling interest differently as it should also take into

consideration about the subsidiary interest as it hold some amount of equity in the

Corporate Accounting

Limited could have able to generated cash for the part of inventory which they have

purchase from the subsidiary and also add a good sign to the group profit of the

company but as the case suggest it does not able to enter into agreement of the sale

of the inventory which it got from the subsidiary company. As the company have not

able to sale but the subsidiary have recorded the profit which they have earn form

the parent company as a result the overall group profit have an unrealised profit in its

which is not a good sign for the company overall profit. As due to the subsidiary the

company overall profit is been overstated and it show an increase value so this can

do fraud with the company financial user as they are not aware about the overstated

profit by the company. So this above point can be more clear with an proper example

as it can be seen that the company have purchased the good so let assume the

amount was $50000 which they does not able to sale in the current period and a

result it able to show in the end of the year. The subsidiary company holds a 50%

profit in the goods they have sold to the JKY Limited so the profit which the

subsidiary company could able to earn is $16667 (50/150* $50000). So this clear

that the group profit of the company is been overstated by $16667 so the company

have to make an proper adjustment entry in regard to eliminate the part of profit so

the entry will be

Consolidated Profit Account Dr $16667

To Consolidated Inventory Account $16667

So this entry rectifies the error which was done by the subsidiary company in regards

of the unrealised profit for the firm. So it show that each company should remove the

unrealised profit which they have earn so it show also what is to be done in regards

of the unrealised gain related to the non-controlling interest of the company. To

record the gain there can be various method as the company can able to record the

gain in the non-controlling interest so that it will null and void all the profit which the

company is able to get from the selling of their product. Otherwise they can able to

go for that they does not record any amount of the profit so that it will not affect the

overall profit of the group and the non-controlling should be there in the capital and

reserve which the company get from the acquiring the subsidiary company.

Section C

Effects of the NCI disclosure requirement in regards to the separate item in the

process of consolidation:

The company should do the presentation of the non-controlling asset

differently and separately in regards of the interest which they have earn form the

equity which they hold in the parent company. The company which is acquiring the

other company cannot able to record anything related to the Non-controlling Interest

as it is directly related to the equity of the subsidiary company so this should not be

recorded in the financial statement of the parent company (Aasb.gov.au 2019).. This

section of the standard help the parent company to get more knowledge about how

they should record each kind of interest which they are able to get from its subsidiary

company and also able to know how they should report in the consolidated financial

statement so that there is not error of accounting is been done by the parent

company. As the consolidated statement is been concern it show that the entity

should report non-controlling interest differently as it should also take into

consideration about the subsidiary interest as it hold some amount of equity in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Corporate Accounting

parent company so it should report the same in regards of the prescribed standard.

The company should able to know the amount which is to be recorded by them in

non-controlling interest. This separate presentation is been prescribed by the

account standard so that it can able to make the consolidation accounting simple

and as the adjustment are very easy and proper notes is been given for all the entry

so this help them to give a proper understanding of the financial statement to the

stakeholders of the company and also to the investors which own some sort of

interest in the group business of the company (Aasb.gov.au 2019).

The parent company hold some sort of power upon the subsidiary company

as it able to control the management and the business of the subsidiary so it been

called as equity transaction it means the ownership which the parent company have

upon the subsidiary company. This principle is not there if the parent company does

not able full control over the business of subsidiary company. So if the holding power

is been changed it means that is some sort of change which have came in the equity

which the parent company holds in the subsidiary company so it should reported as

it will affect the controlling and non-controlling interest as it is been done by the

company so this should be immediately recorded as the shareholder in regards of

the parent company.

Effects of the change upon the disclosure in the annual report:

As per the accounting standard an company should the investment which they

done or invested in the joint venture as in cost, it should give proper details of all the

transaction which have happen in regards of the consolidation of the financial

statement of the company. It should show all the important accounting principles and

policy which they used and also the judgement and the estimation which they have

done in some point so that the user can get a transparent information about the

process of the consolidation. Company should disclose all the material information

and the nature of the transaction in regards of the subsidiary company in their annual

report.

As per the accounting standard each company should have same accounting

year ending so that an proper analysis can be take place in the two but if there is

difference in both date that it should be recorded and proper justification should be

given as when there is such a change in the accounting date of both the parent as

well as subsidiary company. As per the rule an company should hold a prescribed

percentage upon the subsidiary company so if the company is not able to meet the

said criteria that it should disclose it in the annual report so that the financial user

can be aware of the pare t company holding in the subsidiary company and able to

take thier decision accordingly.

Conclusion

The above have concluded as how the consolidation method is to be carried

by the company and it show about the different methods which can be used by the

company in regards of the consolidated accounts. It also show about the intra

transaction affect upon the consolidated financial statement and how the company

should able to eliminate the unrealised profit from the firm , it also show about the

non-controlling interest and how it should be disclosed by the company in their

annual report.

Corporate Accounting

parent company so it should report the same in regards of the prescribed standard.

The company should able to know the amount which is to be recorded by them in

non-controlling interest. This separate presentation is been prescribed by the

account standard so that it can able to make the consolidation accounting simple

and as the adjustment are very easy and proper notes is been given for all the entry

so this help them to give a proper understanding of the financial statement to the

stakeholders of the company and also to the investors which own some sort of

interest in the group business of the company (Aasb.gov.au 2019).

The parent company hold some sort of power upon the subsidiary company

as it able to control the management and the business of the subsidiary so it been

called as equity transaction it means the ownership which the parent company have

upon the subsidiary company. This principle is not there if the parent company does

not able full control over the business of subsidiary company. So if the holding power

is been changed it means that is some sort of change which have came in the equity

which the parent company holds in the subsidiary company so it should reported as

it will affect the controlling and non-controlling interest as it is been done by the

company so this should be immediately recorded as the shareholder in regards of

the parent company.

Effects of the change upon the disclosure in the annual report:

As per the accounting standard an company should the investment which they

done or invested in the joint venture as in cost, it should give proper details of all the

transaction which have happen in regards of the consolidation of the financial

statement of the company. It should show all the important accounting principles and

policy which they used and also the judgement and the estimation which they have

done in some point so that the user can get a transparent information about the

process of the consolidation. Company should disclose all the material information

and the nature of the transaction in regards of the subsidiary company in their annual

report.

As per the accounting standard each company should have same accounting

year ending so that an proper analysis can be take place in the two but if there is

difference in both date that it should be recorded and proper justification should be

given as when there is such a change in the accounting date of both the parent as

well as subsidiary company. As per the rule an company should hold a prescribed

percentage upon the subsidiary company so if the company is not able to meet the

said criteria that it should disclose it in the annual report so that the financial user

can be aware of the pare t company holding in the subsidiary company and able to

take thier decision accordingly.

Conclusion

The above have concluded as how the consolidation method is to be carried

by the company and it show about the different methods which can be used by the

company in regards of the consolidated accounts. It also show about the intra

transaction affect upon the consolidated financial statement and how the company

should able to eliminate the unrealised profit from the firm , it also show about the

non-controlling interest and how it should be disclosed by the company in their

annual report.

8

Corporate Accounting

References

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 30

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

30 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 30

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 30 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed

30 May 2019].

D'Amico, E., Coluccia, D., Fontana, S. and Solimene, S., 2016. Factors influencing

corporate environmental disclosure. Business Strategy and the Environment, 25(3),

pp.178-192.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Lee, T.A. and Parker, R.H., 2014. Company financial statements: an essay in

business history 1830–1950. In Evolution of Corporate Financial Reporting (RLE

Accounting)(pp. 27-51). Routledge.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated

financial reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International

financial statement analysis. John Wiley & Sons.

Corporate Accounting

References

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 30

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed

30 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 30

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 30 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed

30 May 2019].

D'Amico, E., Coluccia, D., Fontana, S. and Solimene, S., 2016. Factors influencing

corporate environmental disclosure. Business Strategy and the Environment, 25(3),

pp.178-192.

Hoyle, J.B., Schaefer, T. and Doupnik, T., 2015. Advanced accounting. McGraw Hill.

Lee, T.A. and Parker, R.H., 2014. Company financial statements: an essay in

business history 1830–1950. In Evolution of Corporate Financial Reporting (RLE

Accounting)(pp. 27-51). Routledge.

Müller, V.O., 2014. The impact of IFRS adoption on the quality of consolidated

financial reporting. Procedia-Social and Behavioral Sciences, 109, pp.976-982.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International

financial statement analysis. John Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.