BAO2203 Corporate Accounting Assignment: Consolidation and Impairment

VerifiedAdded on 2022/11/13

|14

|1943

|180

Homework Assignment

AI Summary

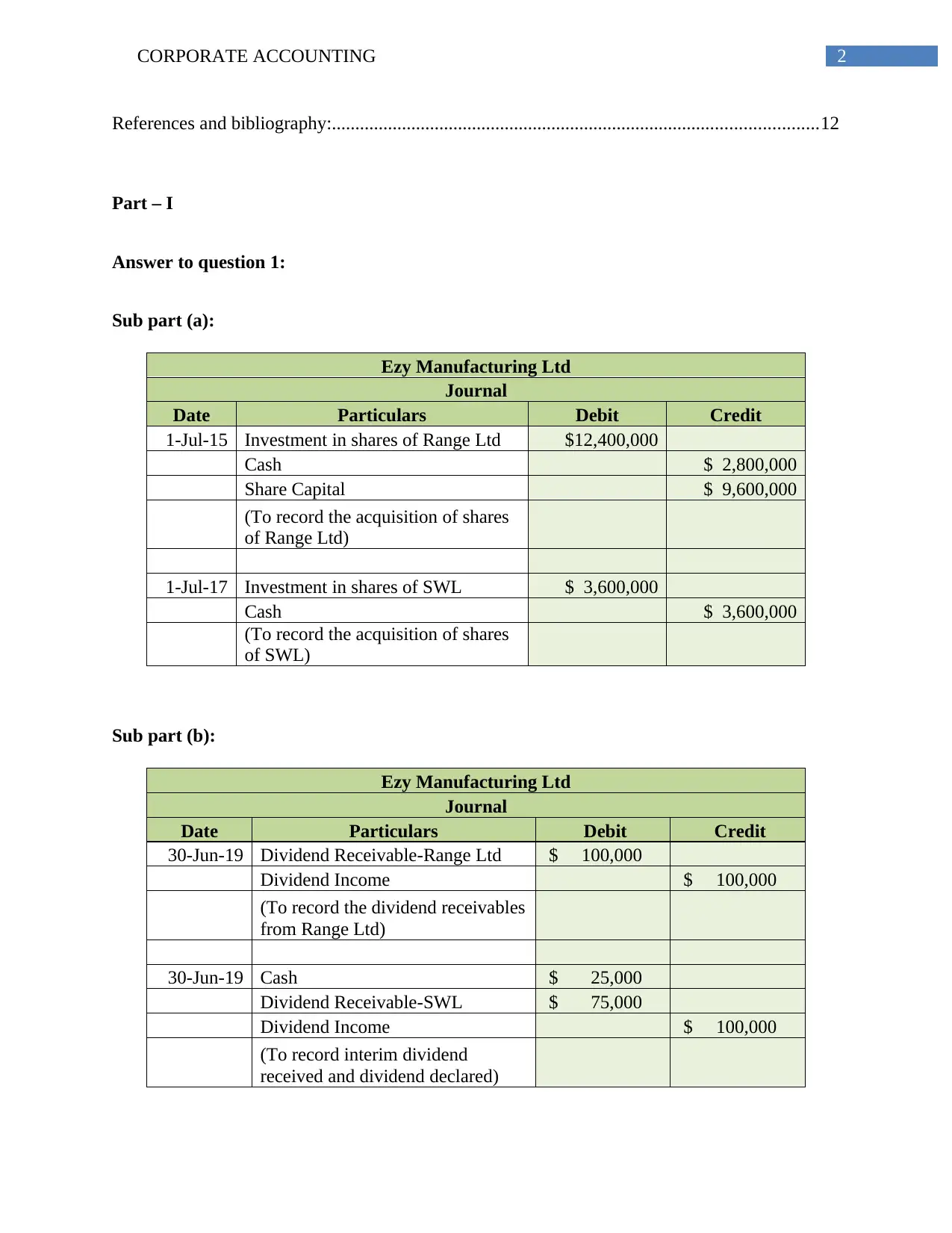

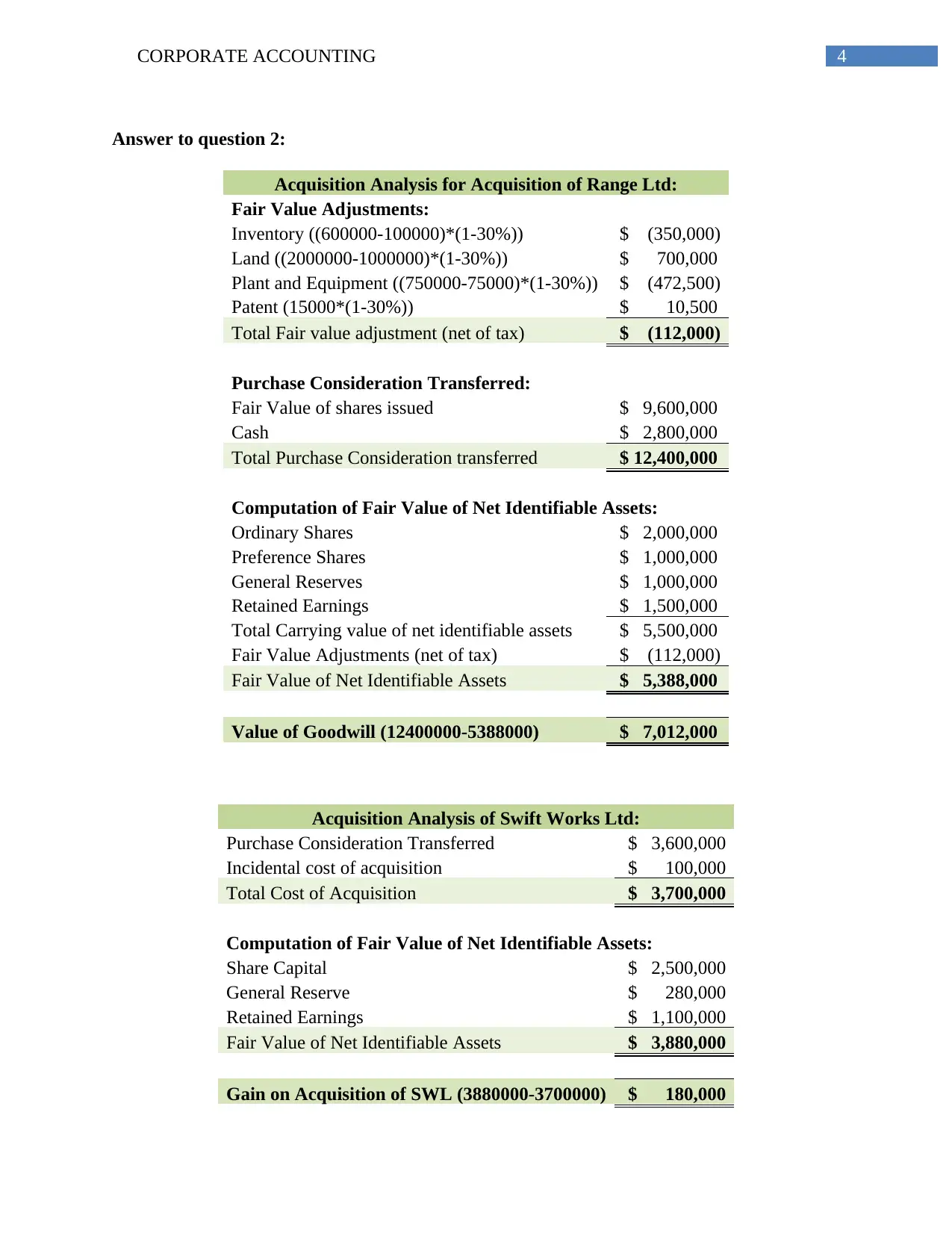

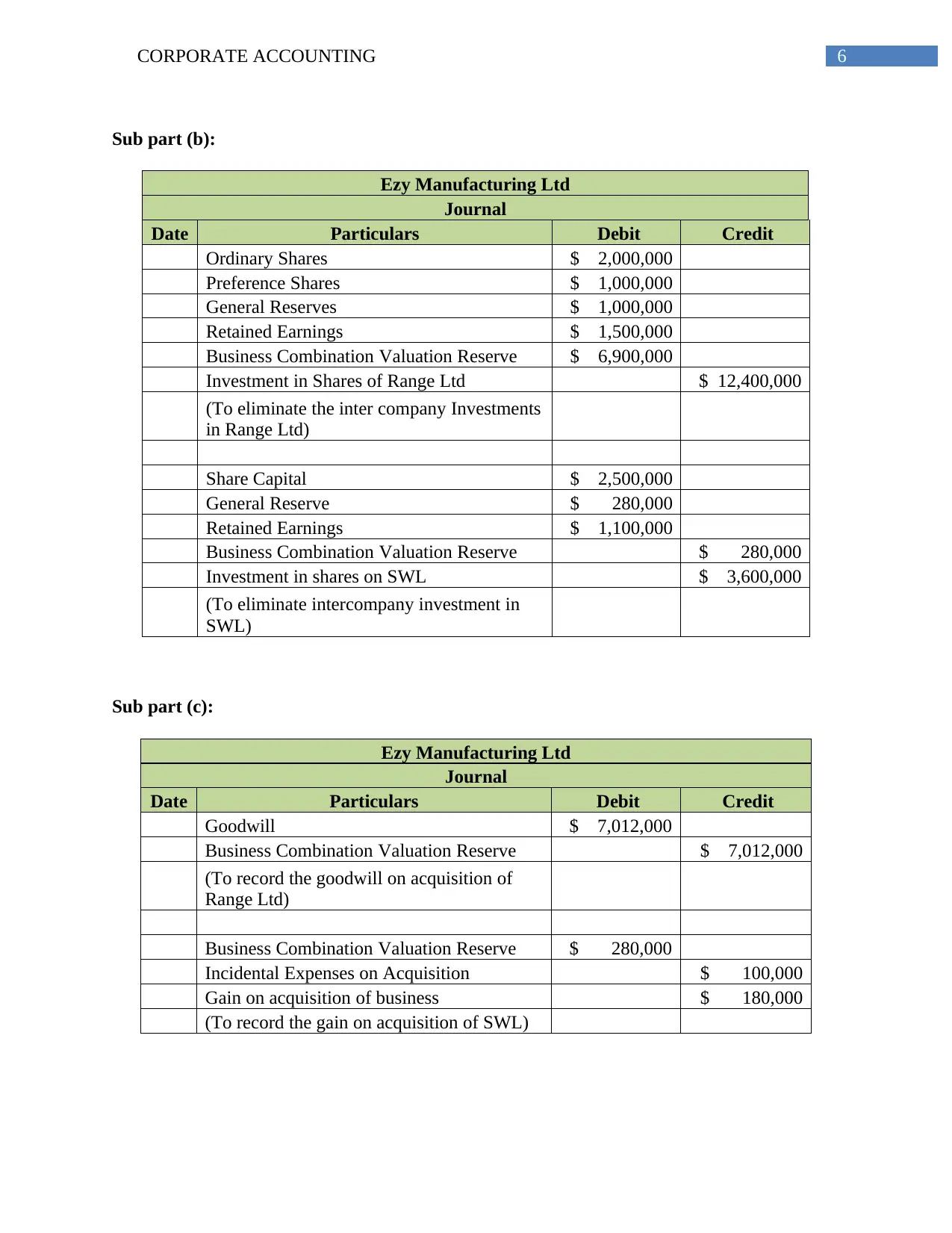

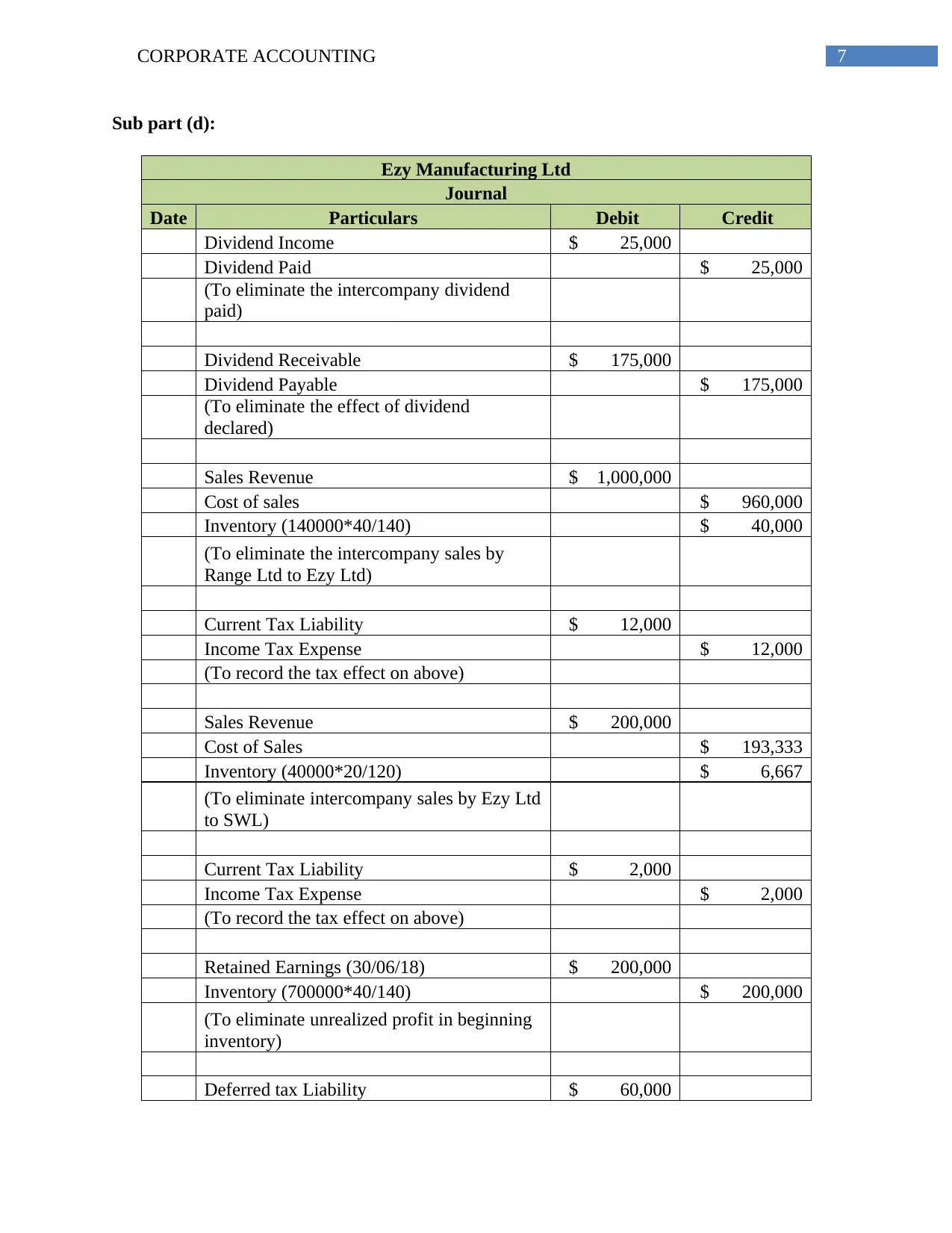

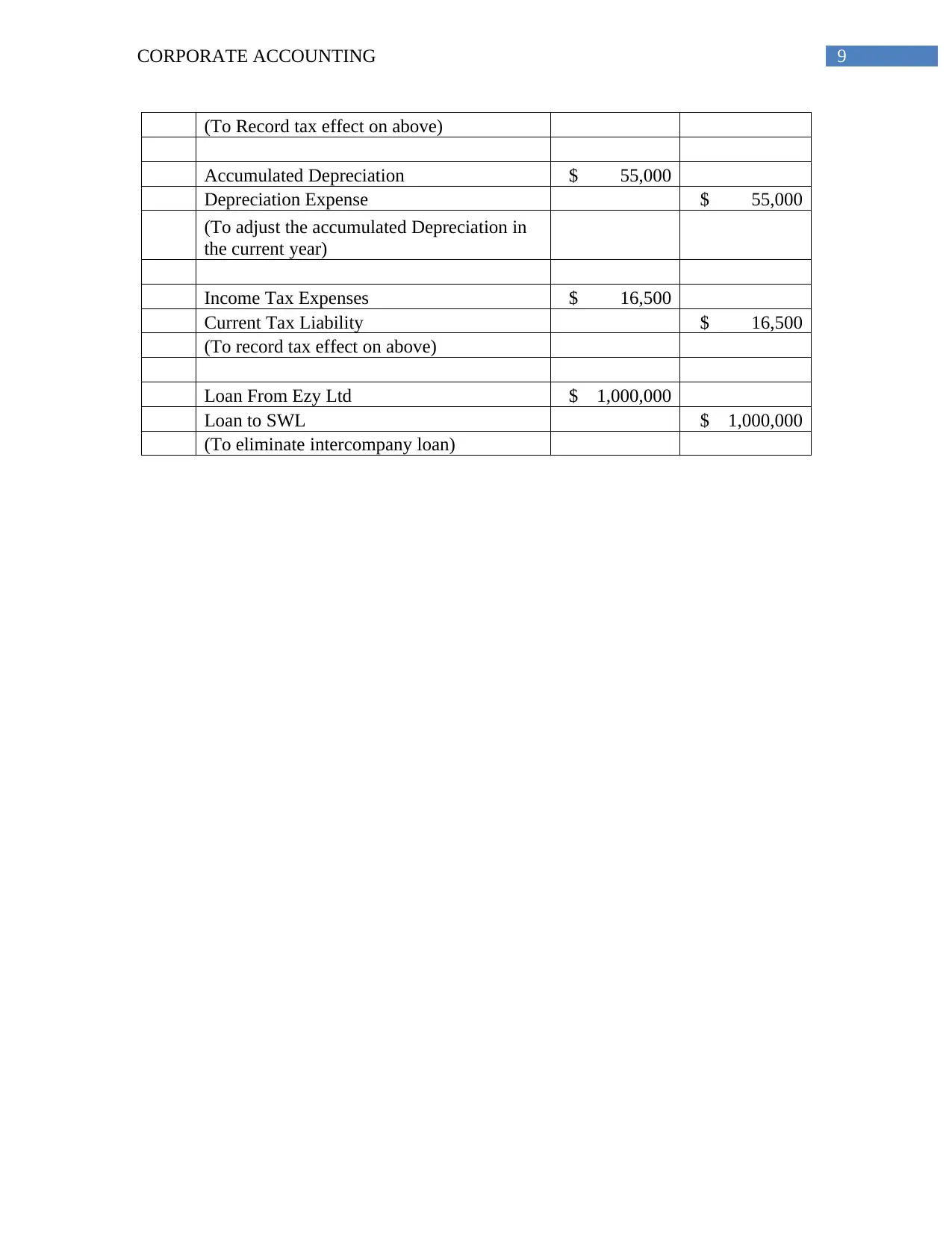

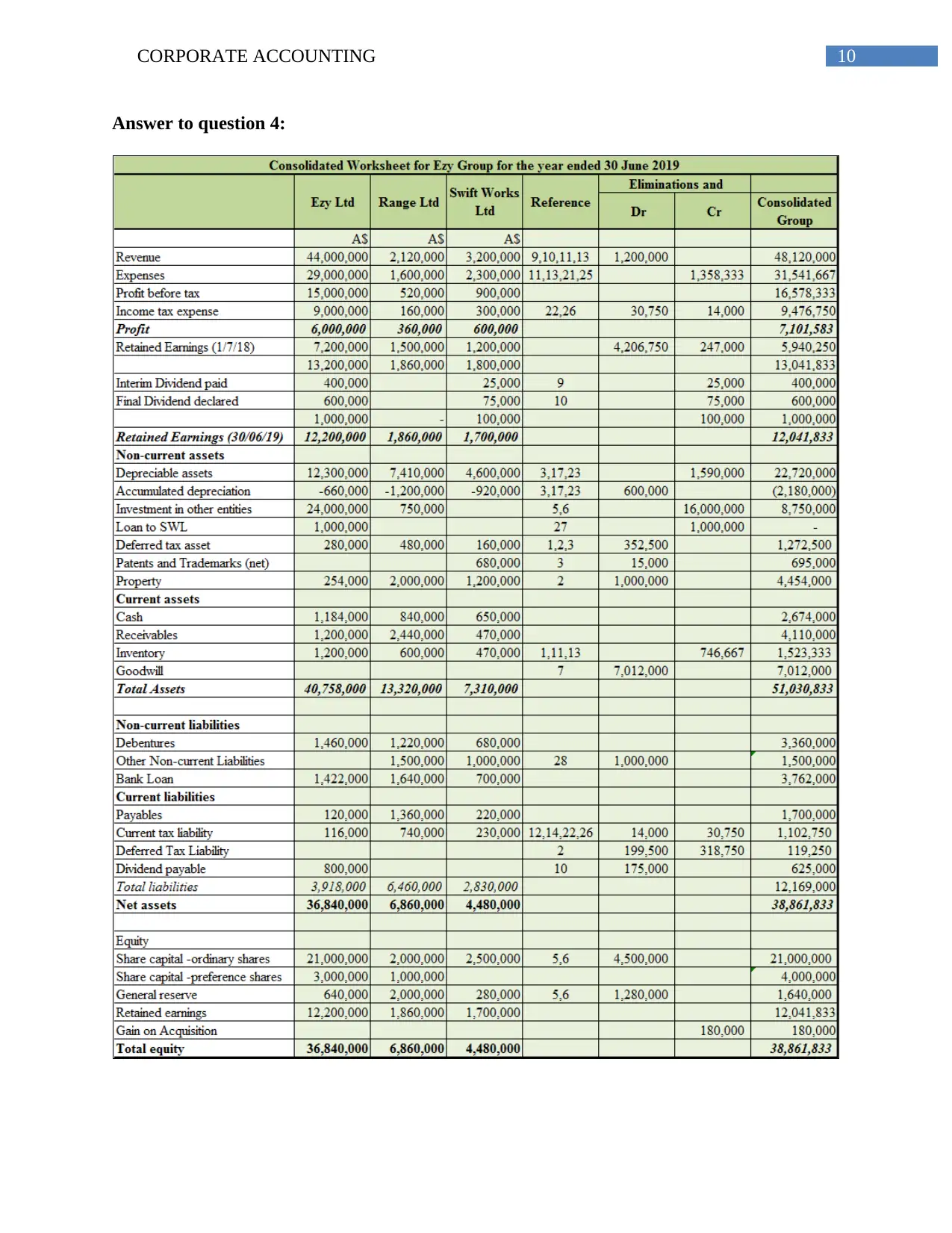

This assignment solution addresses corporate accounting principles, specifically focusing on the consolidation of financial statements and the impairment of assets. Part I delves into the acquisition of Range Pty Ltd and Swift Works Ltd by Ezy Manufacturing Ltd, including journal entries for share acquisitions, dividend income, and the calculation of goodwill. It also includes detailed acquisition analyses, fair value adjustments, and elimination of intercompany transactions. Part II examines asset impairment, discussing impairment testing, its effects on financial statements, and the impact of discount rates. The solution references the Myer Holdings Limited 2018 Annual Report to illustrate impairment practices and provides insights into the prohibition of impairment reversals. The assignment covers various accounting standards and principles, including AASB 3 and IAS 36, providing a comprehensive understanding of consolidation and impairment accounting.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.