Corporate Accounting Assignment - Fair Value and Impairment

VerifiedAdded on 2023/01/05

|13

|2757

|96

Report

AI Summary

This report delves into the intricacies of corporate accounting, focusing on fair value measurement and impairment loss. Part 1 provides an in-depth explanation of fair value accounting, detailing its principles, the role of IFRS 13, valuation techniques (market, income, and cost approaches), and disclosure requirements. The report emphasizes the importance of market participant assumptions and the fair value hierarchy. Part 2 applies these concepts to a case study involving Gali Ltd, a Cash Generating Unit (CGU). It includes detailed calculations for impairment loss, allocation of the loss across assets (Goodwill, Patent, Equipment, Building), and presents the corresponding journal entries. The report adheres to accounting standards and provides clear explanations of the methods used to determine values, such as the recoverable amount and carrying amount of assets. The analysis includes the impact of impairment on asset values and the allocation of losses based on asset carrying amounts. This report is a comprehensive guide to understanding and applying fair value and impairment accounting principles.

Running head: REPORT 1

CORPORATE ACCOUNTING

STUDENT DETAILS:

6/9/2019

CORPORATE ACCOUNTING

STUDENT DETAILS:

6/9/2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 2

Part-1

The fair value accounting utilizes the current market value as a base to identify some liabilities as

well as assets. The fair value is considered as projected cost at which the asset may be traded or

the liabilities settled in the arranged transactions to the 3rd person in the present conditions of

market. The meaning of fair value involves some concepts, such as orderly transaction, third

party, the present market conditions as well as intention (Wingard, Bosman and Amisi, 2016).

The best measurement of fair value is depended on the price provided in the active marketplace.

The active marketplace is a place where there is the adequately higher volume of the transaction

to render constant data related to the prices. In the following parts, the accounting of fair value

measurement is discussed and critically examined.

The marketplace from that the fair value is resulting, must be a principal marketplace for liability

and asset, as the great dealing volume connected to this marketplace must most probably lead to

a great price for a trader. A marketplace where the businesses usually sell the asset types in the

question and settle the liability is supposed to be a main marketplace (Bassemir, 2018). Further,

in the accounting related to fair value, there are various common methods allowed to derive the

fair value of asset that are Cost approach, income approach and market approach. Generally

Accepted Accounting Principles renders the pecking order of sources of data, which range from

Level one or best level to Level three or worst level. The common intention of the data’s level is

to step accountants by the sequence of the substitutes of valuation, wherever the solution nearer

to Level one are chosen above Level three.

Part-1

The fair value accounting utilizes the current market value as a base to identify some liabilities as

well as assets. The fair value is considered as projected cost at which the asset may be traded or

the liabilities settled in the arranged transactions to the 3rd person in the present conditions of

market. The meaning of fair value involves some concepts, such as orderly transaction, third

party, the present market conditions as well as intention (Wingard, Bosman and Amisi, 2016).

The best measurement of fair value is depended on the price provided in the active marketplace.

The active marketplace is a place where there is the adequately higher volume of the transaction

to render constant data related to the prices. In the following parts, the accounting of fair value

measurement is discussed and critically examined.

The marketplace from that the fair value is resulting, must be a principal marketplace for liability

and asset, as the great dealing volume connected to this marketplace must most probably lead to

a great price for a trader. A marketplace where the businesses usually sell the asset types in the

question and settle the liability is supposed to be a main marketplace (Bassemir, 2018). Further,

in the accounting related to fair value, there are various common methods allowed to derive the

fair value of asset that are Cost approach, income approach and market approach. Generally

Accepted Accounting Principles renders the pecking order of sources of data, which range from

Level one or best level to Level three or worst level. The common intention of the data’s level is

to step accountants by the sequence of the substitutes of valuation, wherever the solution nearer

to Level one are chosen above Level three.

REPORT 3

Furthermore, IFRS 13 ‘the Fair Value Measurement’ describes the fair value, sets in the separate

International financial reporting standard, the framework for assessing the fair value, as well as

needs disclosure in relation to the measurements of fair value. This standard was published in

year 2011. IFRS 13 became effective from the 1/1/2013. This standard is applicable while other

Standard allows or needs the disclosure of fair value, measurement of fair value and

measurements on the basis of fair value, like cost reduces from the fair value for selling), apart

from the particular situations where other Standards regulate. For an instance, this accounting

standard does not mention disclosure and measurement provisions to make the share-based

payment transaction, impairment of asset and lease. This accounting standard does not develop

the requirements related to disclosure for the fair value in respect of the retirement plan along

with the employee benefits (Ball, Li and Shivakumar, 2015).

Moreover, IFRS 13 describes the fair value as a price, which will be attained to sell the asset or

make payment for transferring the liability in the arranged dealing amid marketplace contributors

at the date of measurement (the present price). While assessing the fair value, the organization

utilizes the assumption that marketplace contributors will utilize while pricing the assets or the

liabilities in present market condition, involving the assumption in relation to the risks. As the

outcome, the intention of an organization to hold the assets and for settling or else fulfill the

liabilities is not applicable at the time of assessing the fair value.

Additionally, the main purpose of the fair value measurement is for estimating the prices at

which the orderly transactions for transferring the liabilities or for selling the assets will occur

among the contributors of market at date of assessment in the present market condition. In this

way, the fair value measurement needs the organization to measure the specific liability or asset,

which is a matter of a measurement (constantly with the unit of accounts), and the main (and

Furthermore, IFRS 13 ‘the Fair Value Measurement’ describes the fair value, sets in the separate

International financial reporting standard, the framework for assessing the fair value, as well as

needs disclosure in relation to the measurements of fair value. This standard was published in

year 2011. IFRS 13 became effective from the 1/1/2013. This standard is applicable while other

Standard allows or needs the disclosure of fair value, measurement of fair value and

measurements on the basis of fair value, like cost reduces from the fair value for selling), apart

from the particular situations where other Standards regulate. For an instance, this accounting

standard does not mention disclosure and measurement provisions to make the share-based

payment transaction, impairment of asset and lease. This accounting standard does not develop

the requirements related to disclosure for the fair value in respect of the retirement plan along

with the employee benefits (Ball, Li and Shivakumar, 2015).

Moreover, IFRS 13 describes the fair value as a price, which will be attained to sell the asset or

make payment for transferring the liability in the arranged dealing amid marketplace contributors

at the date of measurement (the present price). While assessing the fair value, the organization

utilizes the assumption that marketplace contributors will utilize while pricing the assets or the

liabilities in present market condition, involving the assumption in relation to the risks. As the

outcome, the intention of an organization to hold the assets and for settling or else fulfill the

liabilities is not applicable at the time of assessing the fair value.

Additionally, the main purpose of the fair value measurement is for estimating the prices at

which the orderly transactions for transferring the liabilities or for selling the assets will occur

among the contributors of market at date of assessment in the present market condition. In this

way, the fair value measurement needs the organization to measure the specific liability or asset,

which is a matter of a measurement (constantly with the unit of accounts), and the main (and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 4

most beneficial) marketplace for the liability or asset. It also requires to assess the valuation

techniques relevant for a measurement, regarding an accessibility of information with that to

establish the inputs for stating the assumption that marketplace contributors would utilize while

pricing the liability or asset and a level of the fair value pecking order within that the inputs are

categorized. Additionally, measurement is also required for the non-financial assets, the

valuation principle that is proper for the measurements (constantly with the higher and better

exercise)

IFRS 13 renders various guidance on the fair value’s measurement. According to these guidance,

the organization considers the features of the liabilities or assets being evaluated which the

marketplace contributors will consider at the time of pricing of liability and asset at the date of

measurement (for an example, the condition as well as place of the assets and the restriction on

the utilization and sale of the assets). Also, the measurement of fair value supposes the

transactions occurring in a key marketplace for the liabilities or assets. On the other hand, in

absence of the key marketplace, the most beneficial marketplace for the liabilities or assets.

Further, the fair value measurement supposes the methodical or arranged transactions among

marketplace contributors at a date of measurement as per the present marketplace conditions.

The liability’s fair value shows the non-performance risks (risks that company would not

conform to the obligations), involving the personal credit risk of company as well as supposing

the similar non-performance risks prior to as well as subsequent the relocation of the liabilities.

Additionally, the fair value measurement of the non-financial assets considers the high as well as

good exercise. A fair value measurement of the non-financial liabilities or financial liabilities or

the own equity instruments of corporation supposes this is shifted to the marketplace participants

at the date of measurement, without the settlements, extinguishment, and termination at a date of

most beneficial) marketplace for the liability or asset. It also requires to assess the valuation

techniques relevant for a measurement, regarding an accessibility of information with that to

establish the inputs for stating the assumption that marketplace contributors would utilize while

pricing the liability or asset and a level of the fair value pecking order within that the inputs are

categorized. Additionally, measurement is also required for the non-financial assets, the

valuation principle that is proper for the measurements (constantly with the higher and better

exercise)

IFRS 13 renders various guidance on the fair value’s measurement. According to these guidance,

the organization considers the features of the liabilities or assets being evaluated which the

marketplace contributors will consider at the time of pricing of liability and asset at the date of

measurement (for an example, the condition as well as place of the assets and the restriction on

the utilization and sale of the assets). Also, the measurement of fair value supposes the

transactions occurring in a key marketplace for the liabilities or assets. On the other hand, in

absence of the key marketplace, the most beneficial marketplace for the liabilities or assets.

Further, the fair value measurement supposes the methodical or arranged transactions among

marketplace contributors at a date of measurement as per the present marketplace conditions.

The liability’s fair value shows the non-performance risks (risks that company would not

conform to the obligations), involving the personal credit risk of company as well as supposing

the similar non-performance risks prior to as well as subsequent the relocation of the liabilities.

Additionally, the fair value measurement of the non-financial assets considers the high as well as

good exercise. A fair value measurement of the non-financial liabilities or financial liabilities or

the own equity instruments of corporation supposes this is shifted to the marketplace participants

at the date of measurement, without the settlements, extinguishment, and termination at a date of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 5

measurement. Moreover, the optional exception is applicable for some financial liabilities along

with financial assets with offsetting the position in marketplace risk and counterparty credit

risks; rendered situations are fulfilled (further disclosures are essential).

The corporation utilizes the techniques for valuation, which are relevant in relation to the

circumstances and for which enough information are obtainable to assess the fair value,

maximizing a utilization of proper visible inputs as well as reducing the utilization of

unobservable input. The main purpose of utilizing the technique of valuation is to forecast the

price at which the arranged dealings to sell assets and to transfer liabilities will occur among

market contributors and a measurement date in the present market position (Flip, et. al, 2017).

There are three valuation techniques, which are used widely. These techniques of valuation are

the market approach, income approach and cost approach. The market approach uses price as

well as relevant data produced through the market transactions including recognized or similar

(comparable) asset, liability, and the group of liabilities as well as assets (for an example, the

business of company). The income approach converts the upcoming amounts (cash flow,

incomes along with the expenses) to the separate present amount or discounted amount, stating

the market expectation in relation to the amount of upcoming period (Ghio, Filip and Jeny,

2018). On the other hand, the cost approach states the amount, which will be required presently

to replace service’s capability of the assets (the present replacement cost). In certain matters, the

single valuation technique would be relevant, where in other multiple valuation techniques

would be proper (Kenyon and Kenyon, 2016).

IFRS 13 needs the corporation for disclosing the data, which are helpful for the users of the

financial statements for the purpose of fair value measurement utilizing proper unobservable

input (Level three), the effects of the measurement over the profits and losses or other inclusive

measurement. Moreover, the optional exception is applicable for some financial liabilities along

with financial assets with offsetting the position in marketplace risk and counterparty credit

risks; rendered situations are fulfilled (further disclosures are essential).

The corporation utilizes the techniques for valuation, which are relevant in relation to the

circumstances and for which enough information are obtainable to assess the fair value,

maximizing a utilization of proper visible inputs as well as reducing the utilization of

unobservable input. The main purpose of utilizing the technique of valuation is to forecast the

price at which the arranged dealings to sell assets and to transfer liabilities will occur among

market contributors and a measurement date in the present market position (Flip, et. al, 2017).

There are three valuation techniques, which are used widely. These techniques of valuation are

the market approach, income approach and cost approach. The market approach uses price as

well as relevant data produced through the market transactions including recognized or similar

(comparable) asset, liability, and the group of liabilities as well as assets (for an example, the

business of company). The income approach converts the upcoming amounts (cash flow,

incomes along with the expenses) to the separate present amount or discounted amount, stating

the market expectation in relation to the amount of upcoming period (Ghio, Filip and Jeny,

2018). On the other hand, the cost approach states the amount, which will be required presently

to replace service’s capability of the assets (the present replacement cost). In certain matters, the

single valuation technique would be relevant, where in other multiple valuation techniques

would be proper (Kenyon and Kenyon, 2016).

IFRS 13 needs the corporation for disclosing the data, which are helpful for the users of the

financial statements for the purpose of fair value measurement utilizing proper unobservable

input (Level three), the effects of the measurement over the profits and losses or other inclusive

REPORT 6

incomes for a period (Pandya, 2016). It is also useful for the liabilities as well as assets, which

are evaluated at the fair value on the non-recurring bases or recurring bases in the financial

statements of the company after initial recording, the valuation techniques as well as the inputs

utilized to establish the measurements

Besides, the disclosure requirements are not essential in relation to the plan assets valued at the

fair value in relation to the IAS 19 ‘Employee Benefits’, the assets in relation to that the

recoverable amount is fair value less disposal cost according to the IAS 36 ‘Impairment of

Assets’, and the retirement benefit plans investment valued at the fair value according to the IAS

26 ‘Accounting as well as reporting through the Retirement Benefit Plans’.

Wherever the disclosure is needed to be rendered for all the classes of liabilities as well as the

assets of company, the corporation evaluates proper and relevant classes according to the nature,

attributes and risk of the liabilities as well as the assets of an entity, and the level of fair value

pecking order where the fair value measurements are categorized (Busso, 2018). In the addition

of this, measuring the proper classes of asset along with liability for which disclosure in relation

to fair value measurements must be rendered needs judgments. Besides, the class of liabilities

and assets would need great disaggregation than a line items represented in the financial

statements of the company. There are various classes, which can require to be higher for the fair

value measurements categorized in the level three (Sundgren, Mäki and Somoza-López, 2018).

As per the above discussion, it can be concluded that IFRS 13 is new significant standard of

accounting of fair value measurement. In this way, IFRS 13 also needs extensive disclosure for

helping the readers of the financial statements assessment, techniques of valuation and input used

incomes for a period (Pandya, 2016). It is also useful for the liabilities as well as assets, which

are evaluated at the fair value on the non-recurring bases or recurring bases in the financial

statements of the company after initial recording, the valuation techniques as well as the inputs

utilized to establish the measurements

Besides, the disclosure requirements are not essential in relation to the plan assets valued at the

fair value in relation to the IAS 19 ‘Employee Benefits’, the assets in relation to that the

recoverable amount is fair value less disposal cost according to the IAS 36 ‘Impairment of

Assets’, and the retirement benefit plans investment valued at the fair value according to the IAS

26 ‘Accounting as well as reporting through the Retirement Benefit Plans’.

Wherever the disclosure is needed to be rendered for all the classes of liabilities as well as the

assets of company, the corporation evaluates proper and relevant classes according to the nature,

attributes and risk of the liabilities as well as the assets of an entity, and the level of fair value

pecking order where the fair value measurements are categorized (Busso, 2018). In the addition

of this, measuring the proper classes of asset along with liability for which disclosure in relation

to fair value measurements must be rendered needs judgments. Besides, the class of liabilities

and assets would need great disaggregation than a line items represented in the financial

statements of the company. There are various classes, which can require to be higher for the fair

value measurements categorized in the level three (Sundgren, Mäki and Somoza-López, 2018).

As per the above discussion, it can be concluded that IFRS 13 is new significant standard of

accounting of fair value measurement. In this way, IFRS 13 also needs extensive disclosure for

helping the readers of the financial statements assessment, techniques of valuation and input used

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 7

for measuring the fair value. This accounting standard does not measure while the asset, the

liabilities or the personal equity instruments related to entity are determined at the fair value.

for measuring the fair value. This accounting standard does not measure while the asset, the

liabilities or the personal equity instruments related to entity are determined at the fair value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 8

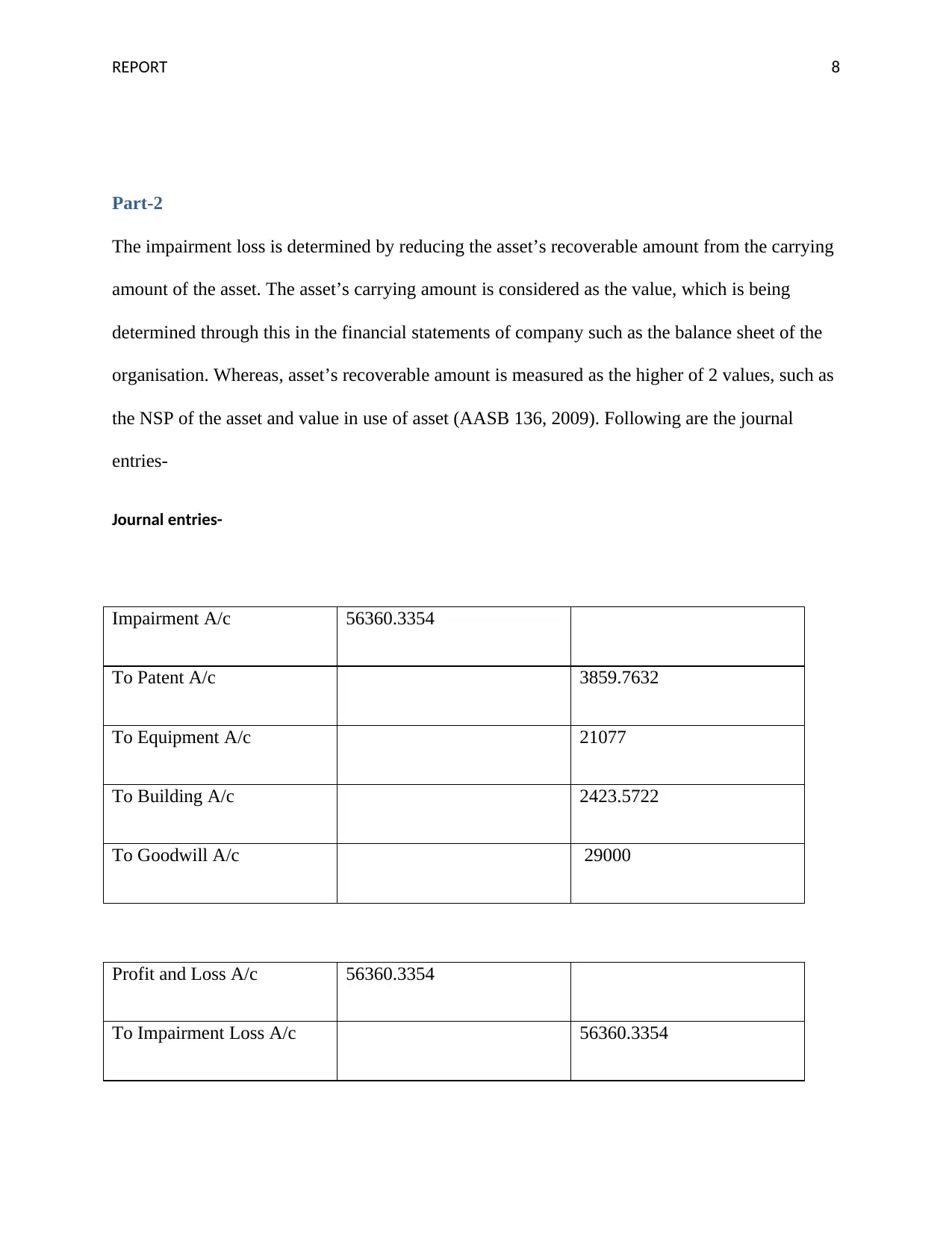

Part-2

The impairment loss is determined by reducing the asset’s recoverable amount from the carrying

amount of the asset. The asset’s carrying amount is considered as the value, which is being

determined through this in the financial statements of company such as the balance sheet of the

organisation. Whereas, asset’s recoverable amount is measured as the higher of 2 values, such as

the NSP of the asset and value in use of asset (AASB 136, 2009). Following are the journal

entries-

Journal entries-

Impairment A/c 56360.3354

To Patent A/c 3859.7632

To Equipment A/c 21077

To Building A/c 2423.5722

To Goodwill A/c 29000

Profit and Loss A/c 56360.3354

To Impairment Loss A/c 56360.3354

Part-2

The impairment loss is determined by reducing the asset’s recoverable amount from the carrying

amount of the asset. The asset’s carrying amount is considered as the value, which is being

determined through this in the financial statements of company such as the balance sheet of the

organisation. Whereas, asset’s recoverable amount is measured as the higher of 2 values, such as

the NSP of the asset and value in use of asset (AASB 136, 2009). Following are the journal

entries-

Journal entries-

Impairment A/c 56360.3354

To Patent A/c 3859.7632

To Equipment A/c 21077

To Building A/c 2423.5722

To Goodwill A/c 29000

Profit and Loss A/c 56360.3354

To Impairment Loss A/c 56360.3354

REPORT 9

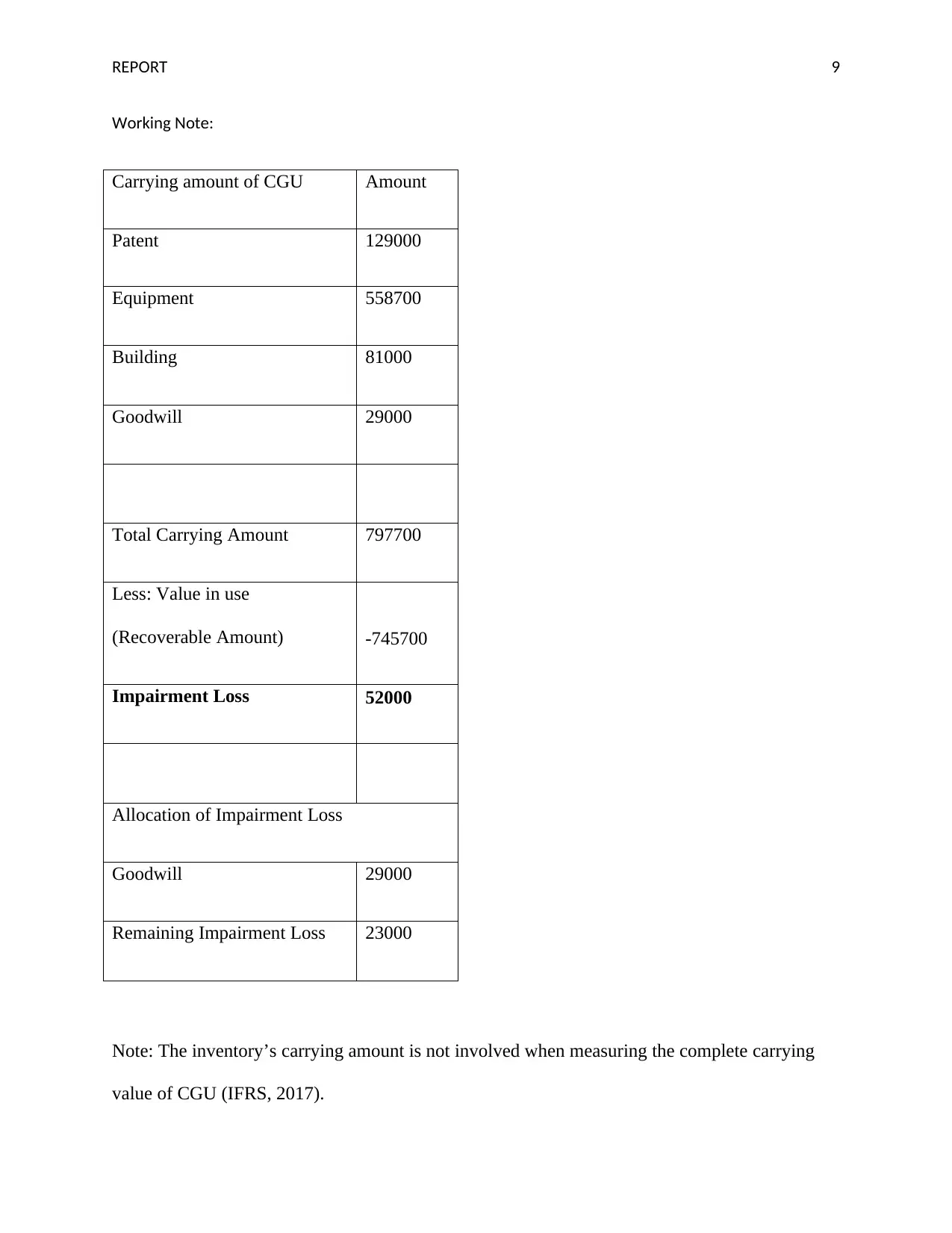

Working Note:

Carrying amount of CGU Amount

Patent 129000

Equipment 558700

Building 81000

Goodwill 29000

Total Carrying Amount 797700

Less: Value in use

(Recoverable Amount) -745700

Impairment Loss 52000

Allocation of Impairment Loss

Goodwill 29000

Remaining Impairment Loss 23000

Note: The inventory’s carrying amount is not involved when measuring the complete carrying

value of CGU (IFRS, 2017).

Working Note:

Carrying amount of CGU Amount

Patent 129000

Equipment 558700

Building 81000

Goodwill 29000

Total Carrying Amount 797700

Less: Value in use

(Recoverable Amount) -745700

Impairment Loss 52000

Allocation of Impairment Loss

Goodwill 29000

Remaining Impairment Loss 23000

Note: The inventory’s carrying amount is not involved when measuring the complete carrying

value of CGU (IFRS, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 10

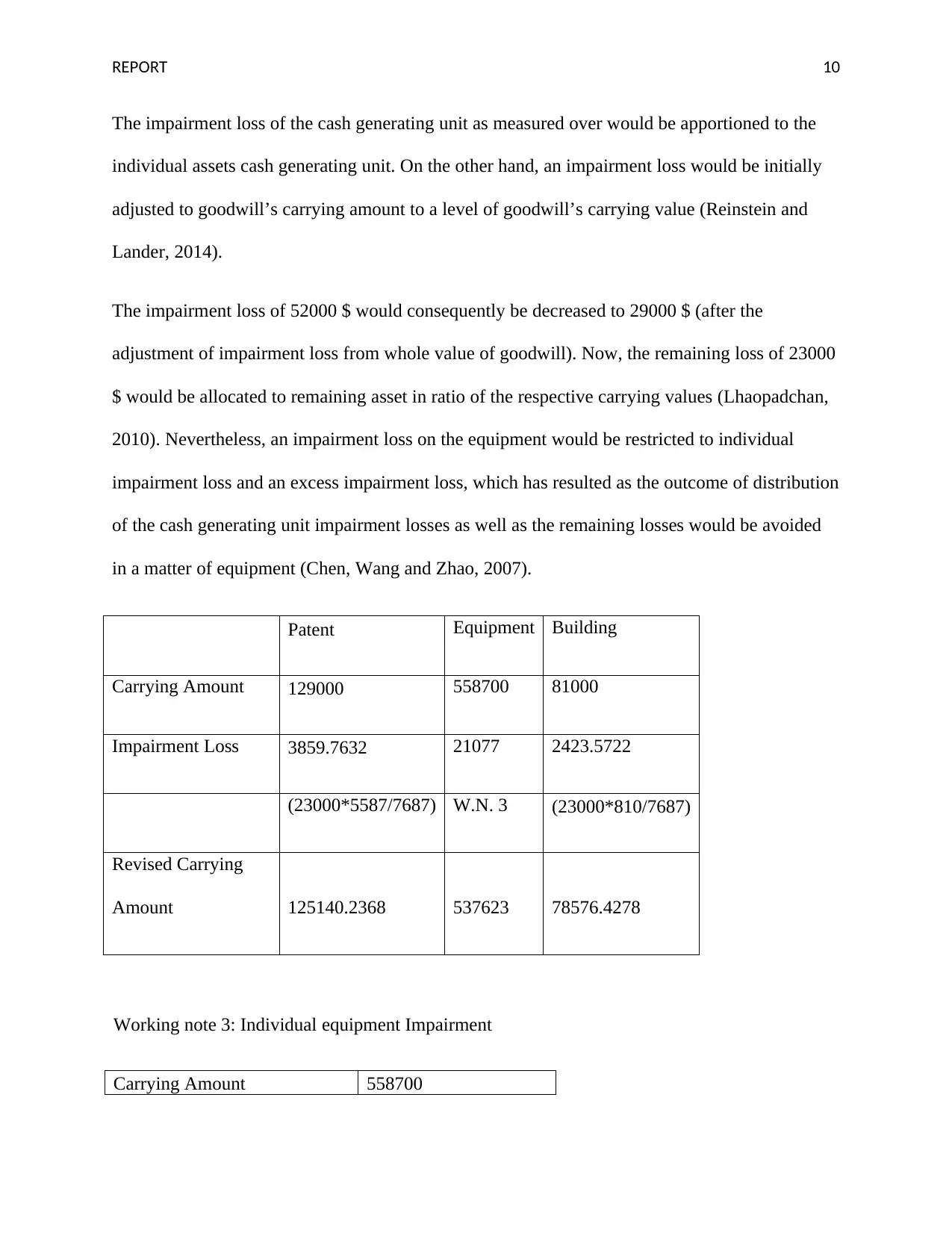

The impairment loss of the cash generating unit as measured over would be apportioned to the

individual assets cash generating unit. On the other hand, an impairment loss would be initially

adjusted to goodwill’s carrying amount to a level of goodwill’s carrying value (Reinstein and

Lander, 2014).

The impairment loss of 52000 $ would consequently be decreased to 29000 $ (after the

adjustment of impairment loss from whole value of goodwill). Now, the remaining loss of 23000

$ would be allocated to remaining asset in ratio of the respective carrying values (Lhaopadchan,

2010). Nevertheless, an impairment loss on the equipment would be restricted to individual

impairment loss and an excess impairment loss, which has resulted as the outcome of distribution

of the cash generating unit impairment losses as well as the remaining losses would be avoided

in a matter of equipment (Chen, Wang and Zhao, 2007).

Patent Equipment Building

Carrying Amount 129000 558700 81000

Impairment Loss 3859.7632 21077 2423.5722

(23000*5587/7687) W.N. 3 (23000*810/7687)

Revised Carrying

Amount 125140.2368 537623 78576.4278

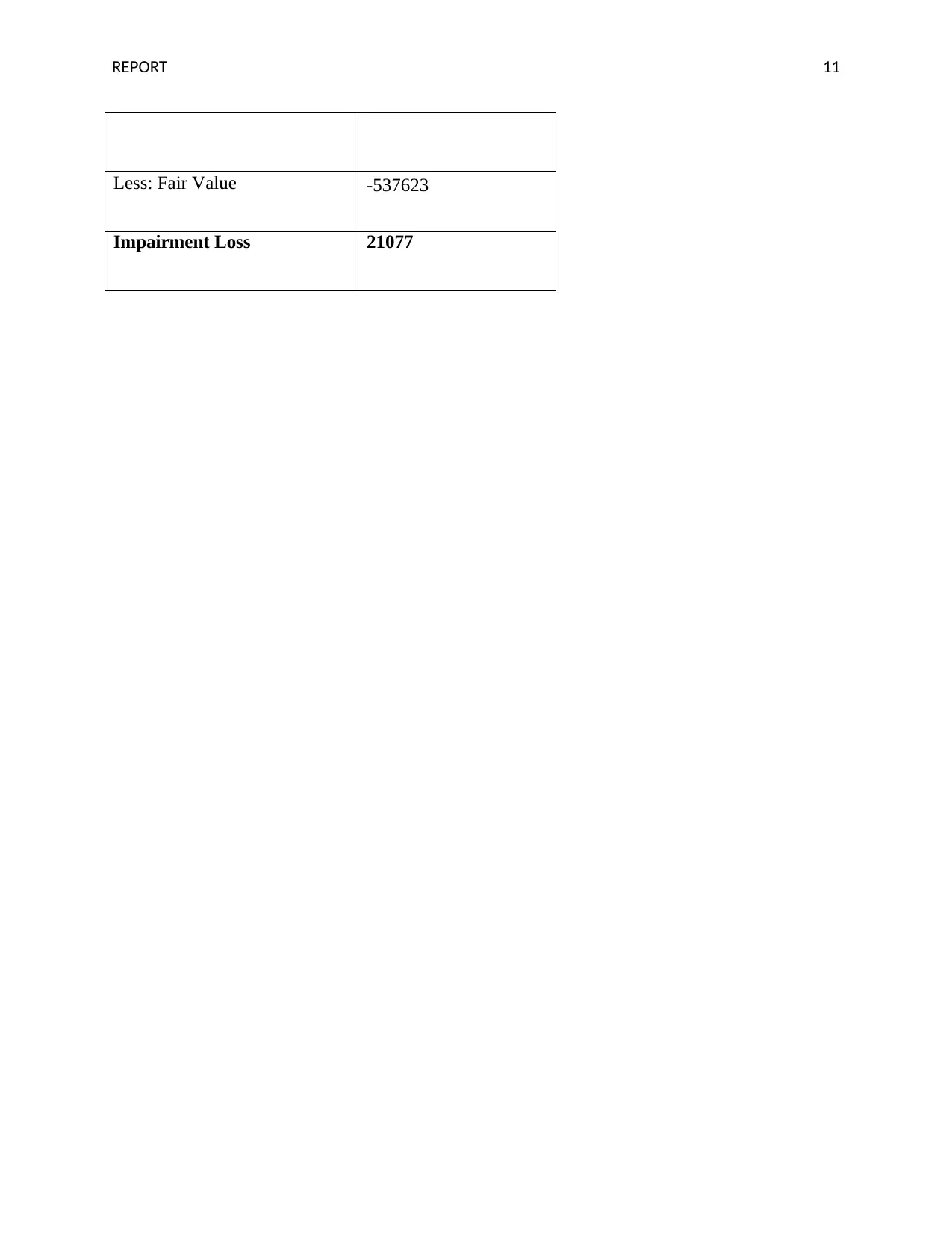

Working note 3: Individual equipment Impairment

Carrying Amount 558700

The impairment loss of the cash generating unit as measured over would be apportioned to the

individual assets cash generating unit. On the other hand, an impairment loss would be initially

adjusted to goodwill’s carrying amount to a level of goodwill’s carrying value (Reinstein and

Lander, 2014).

The impairment loss of 52000 $ would consequently be decreased to 29000 $ (after the

adjustment of impairment loss from whole value of goodwill). Now, the remaining loss of 23000

$ would be allocated to remaining asset in ratio of the respective carrying values (Lhaopadchan,

2010). Nevertheless, an impairment loss on the equipment would be restricted to individual

impairment loss and an excess impairment loss, which has resulted as the outcome of distribution

of the cash generating unit impairment losses as well as the remaining losses would be avoided

in a matter of equipment (Chen, Wang and Zhao, 2007).

Patent Equipment Building

Carrying Amount 129000 558700 81000

Impairment Loss 3859.7632 21077 2423.5722

(23000*5587/7687) W.N. 3 (23000*810/7687)

Revised Carrying

Amount 125140.2368 537623 78576.4278

Working note 3: Individual equipment Impairment

Carrying Amount 558700

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 11

Less: Fair Value -537623

Impairment Loss 21077

Less: Fair Value -537623

Impairment Loss 21077

REPORT 12

References

AASB, C. A. S. (2014). Impairment of Assets. Disclosure, 126, 133

Ball, R., Li, X. and Shivakumar, L. (2015) Contractibility and transparency of financial

statement information prepared under IFRS: Evidence from debt contracts around IFRS

adoption. Journal of Accounting Research, 53(5), pp.915-963.

Bassemir, M. (2018) Why do private firms adopt IFRS?. Accounting and Business

Research, 48(3), pp.237-263.

Busso, D. (2018) Does IFRS 13 Improve the Disclosure of the Fair Value Measurement? An

empirical analysis of the real estate sector in Europe. GSTF Journal on Business Review

(GBR), 3(4).

Chen, S., Wang, Y., and Zhao, Z. (2007). Evidence of Asset Impairment Reversals from China:

Economic Reality or Earnings Management?.

Filip, A., Hammami, A., Huang, Z., Jeny, A., Magnan, M. and Moldovan, R. (2017) Literature

Review on the Effect of Implementation of IFRS 13 Fair Value Measurement. working paper.

Ghio, A., Filip, A. and Jeny, A. (2018) Fair Value Disclosures and Fair Value Hierarchy:

Literature Review on the Implementation of IFRS 13 and SFAS 157.

References

AASB, C. A. S. (2014). Impairment of Assets. Disclosure, 126, 133

Ball, R., Li, X. and Shivakumar, L. (2015) Contractibility and transparency of financial

statement information prepared under IFRS: Evidence from debt contracts around IFRS

adoption. Journal of Accounting Research, 53(5), pp.915-963.

Bassemir, M. (2018) Why do private firms adopt IFRS?. Accounting and Business

Research, 48(3), pp.237-263.

Busso, D. (2018) Does IFRS 13 Improve the Disclosure of the Fair Value Measurement? An

empirical analysis of the real estate sector in Europe. GSTF Journal on Business Review

(GBR), 3(4).

Chen, S., Wang, Y., and Zhao, Z. (2007). Evidence of Asset Impairment Reversals from China:

Economic Reality or Earnings Management?.

Filip, A., Hammami, A., Huang, Z., Jeny, A., Magnan, M. and Moldovan, R. (2017) Literature

Review on the Effect of Implementation of IFRS 13 Fair Value Measurement. working paper.

Ghio, A., Filip, A. and Jeny, A. (2018) Fair Value Disclosures and Fair Value Hierarchy:

Literature Review on the Implementation of IFRS 13 and SFAS 157.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.