Corporate Accounting Solutions - Finance Module Assignment, Semester 1

VerifiedAdded on 2020/05/08

|11

|1820

|239

Homework Assignment

AI Summary

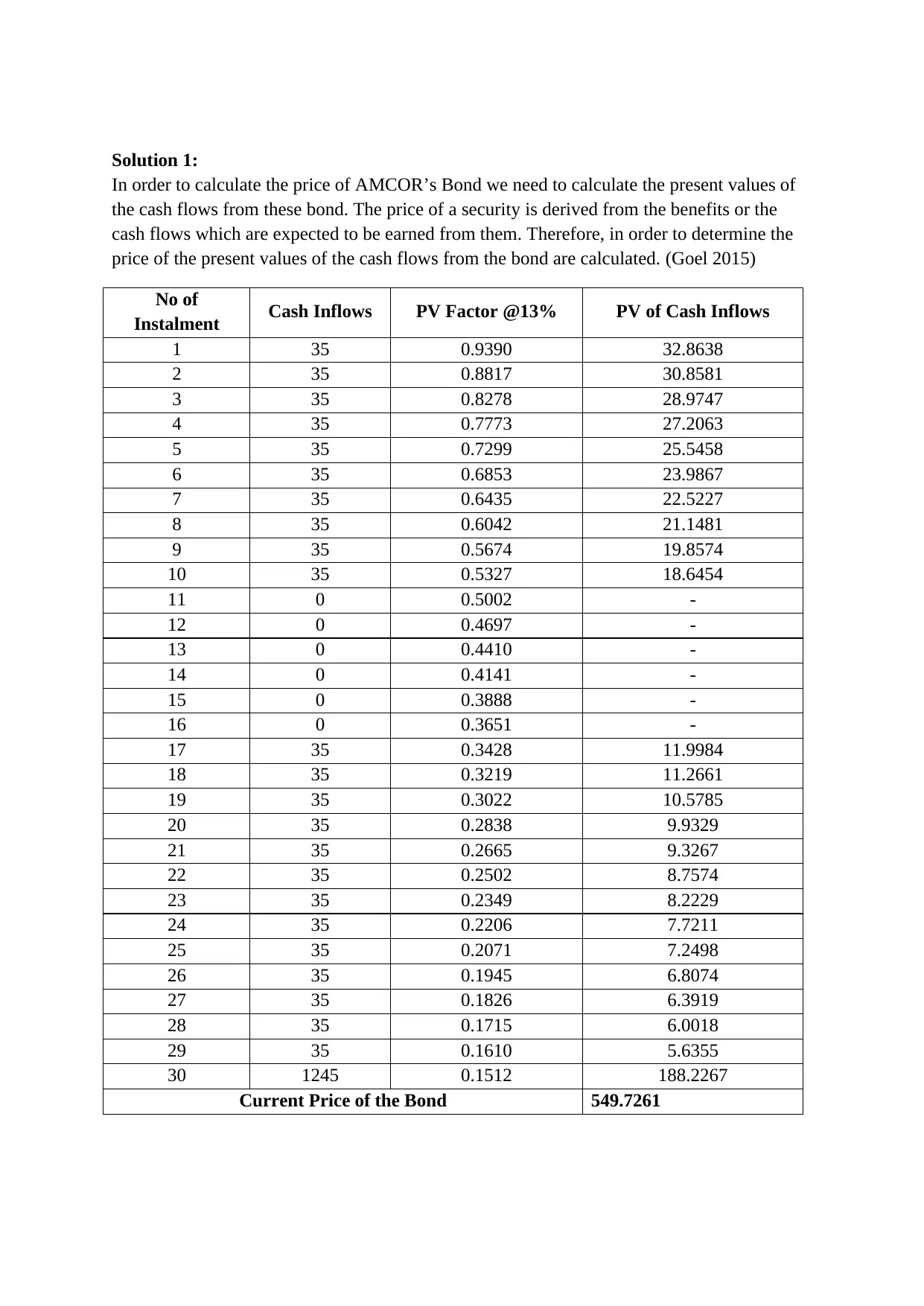

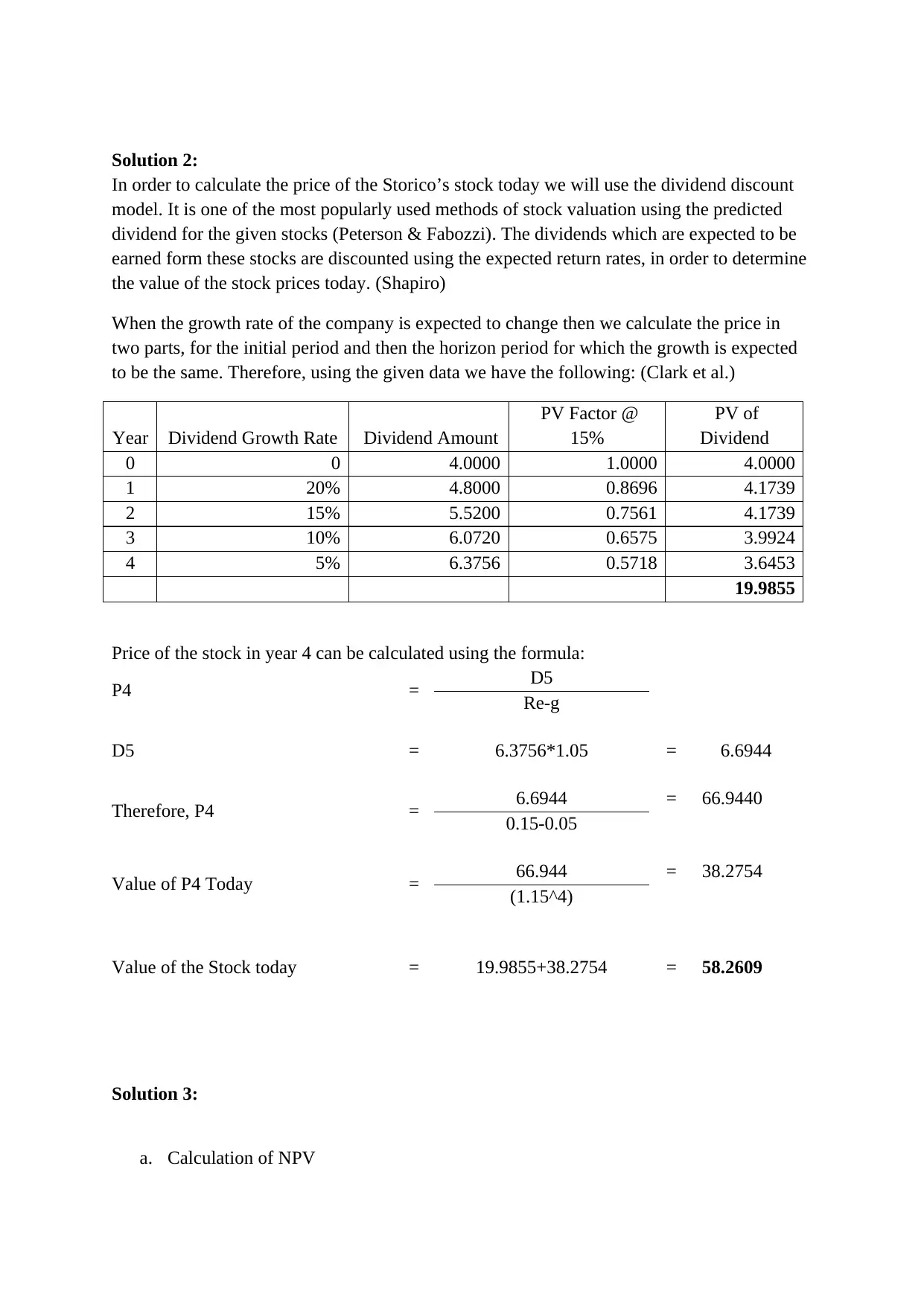

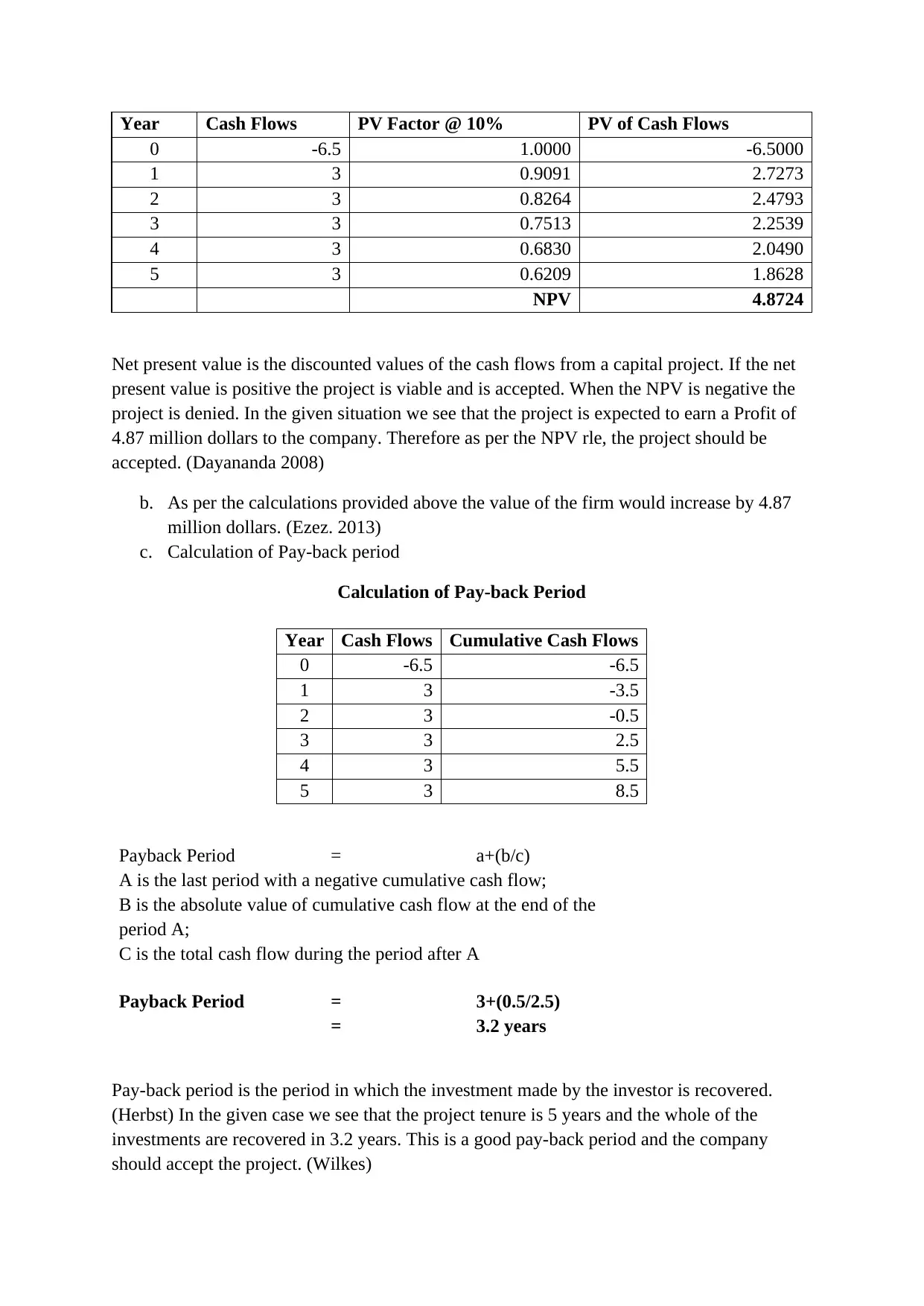

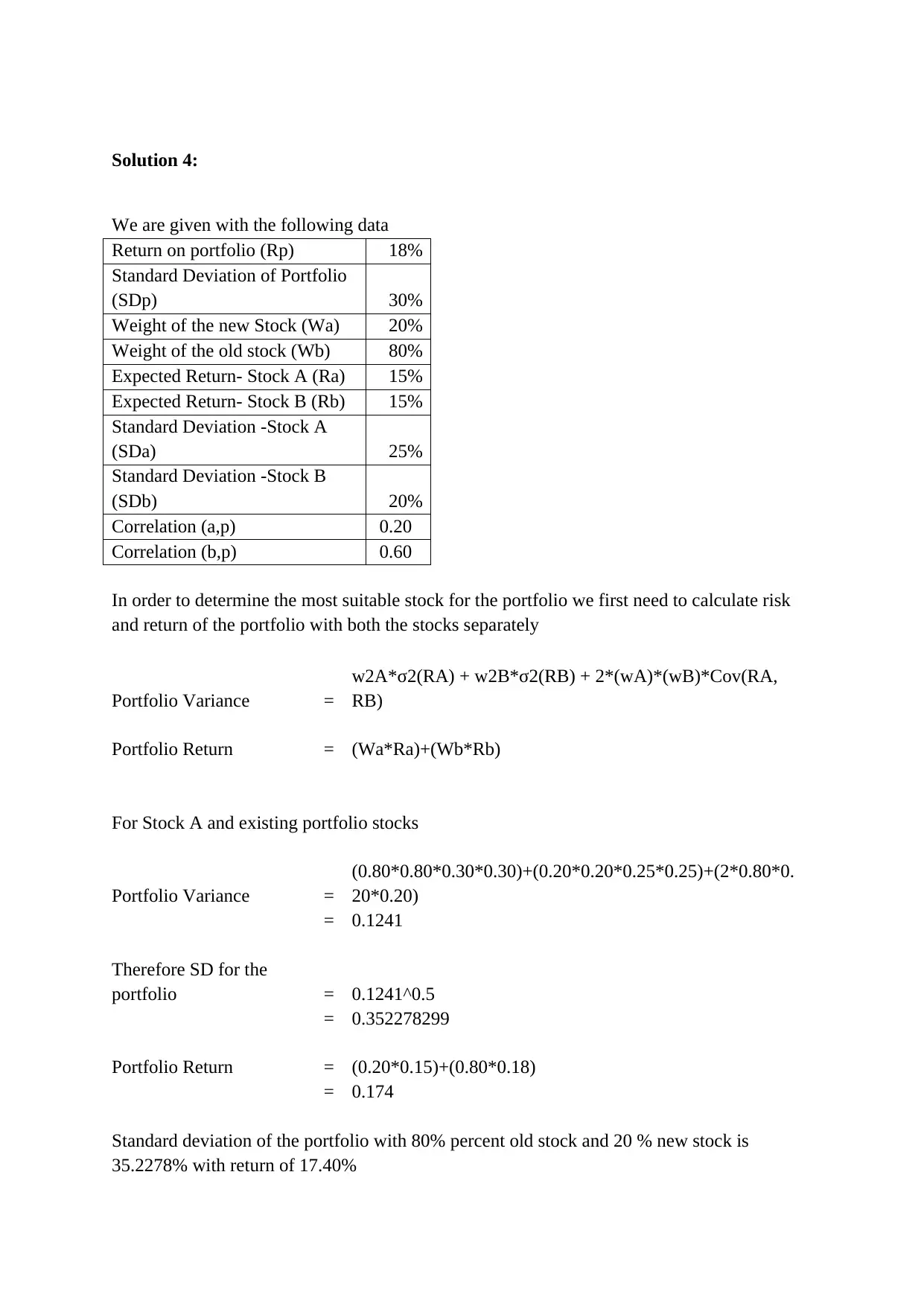

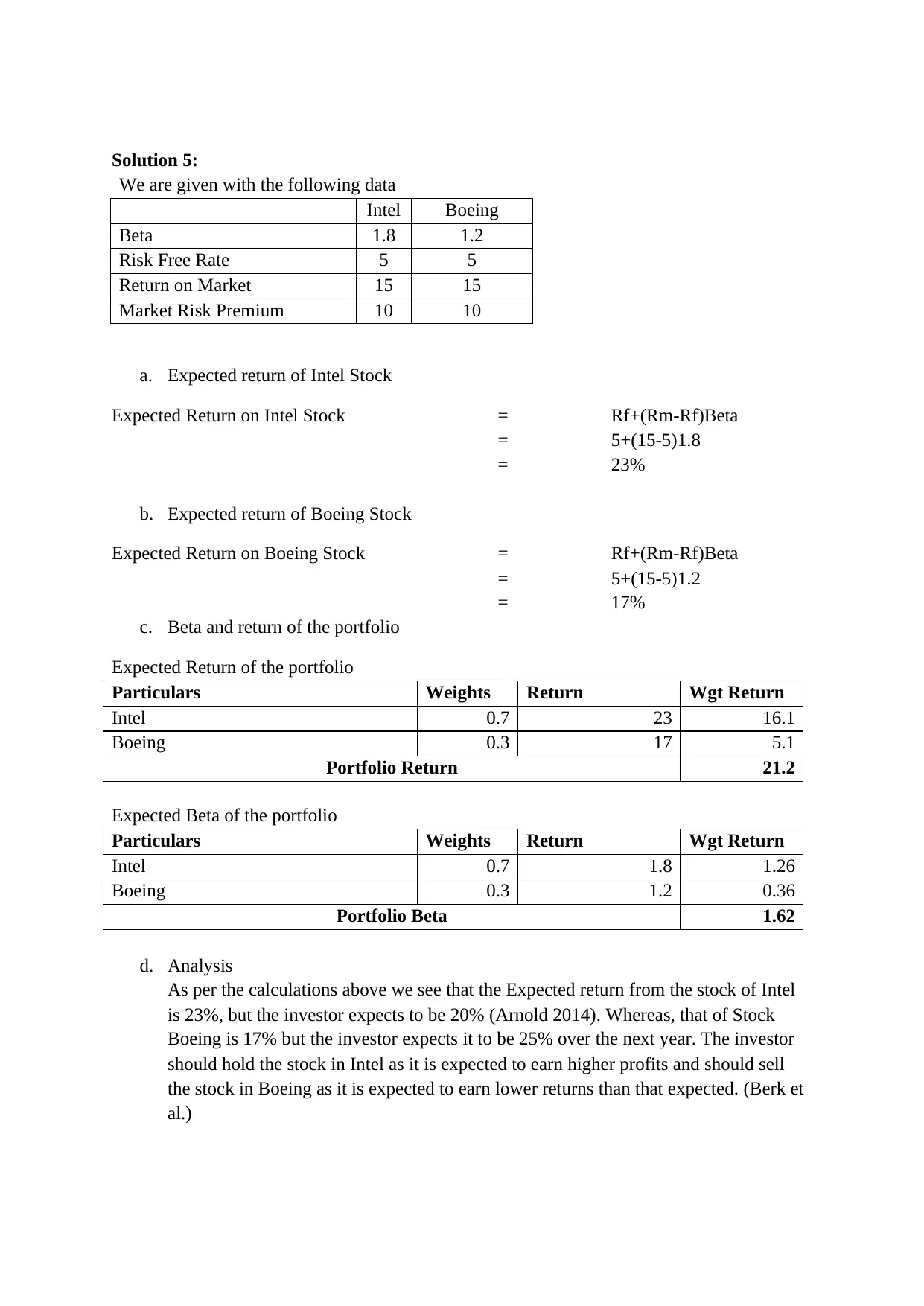

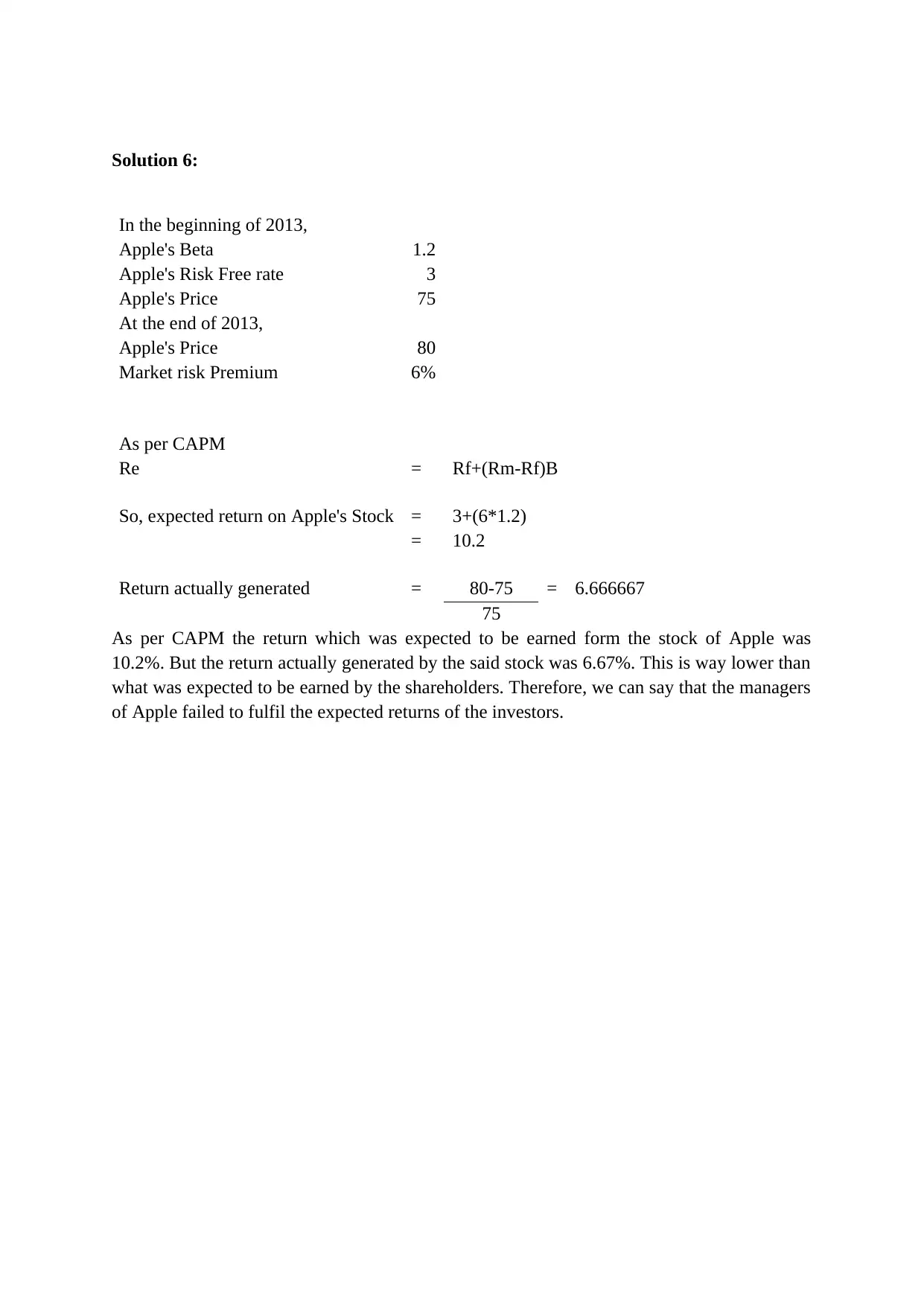

This document presents a comprehensive solution to a corporate accounting assignment, addressing various financial concepts and calculations. The solutions begin with bond valuation, determining the current price based on discounted cash flows. Next, it delves into stock valuation using the dividend discount model, considering different growth rates and present values. The assignment then proceeds to calculate the Net Present Value (NPV) of a capital project, alongside a payback period analysis, to assess its financial viability. Furthermore, the document explores portfolio management, calculating risk and return for different stock combinations to determine the optimal investment strategy. Finally, it applies the Capital Asset Pricing Model (CAPM) to determine expected returns and evaluate managerial performance in relation to investor expectations. The assignment utilizes provided data, formulas, and references to support the financial analysis and recommendations.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.