Corporate Accounting: Analysis of Financial Statements and Tax

VerifiedAdded on 2024/04/24

|23

|3758

|127

Report

AI Summary

This report provides an analysis of corporate accounting principles through the examination of financial statements from three Australian companies: Australian Agricultural Company Limited, Australia Bauxite Limited, and Australian Dairy Farms Group. The analysis covers key aspects such as equity and liabilities, cash flow statements, comprehensive income, and corporate income tax implications over a three-year period (2015-2017). The report assesses the financial stability and performance of each company by evaluating trends in retained earnings, debt levels, operating activities, investing activities, and financing activities. It also discusses the differences between profit statements and comprehensive income statements, as well as the relevance of comprehensive income items for evaluating managerial performance. Finally, the report addresses corporate income tax liabilities for each company based on their reported income.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary:

This report has been prepared so that information regarding the interim financial statements of

the company can be analysed. In this report the annual financial statements of three companies

have been analysed so that their financial stability in the market can be analysed. The report has

focuses on the financial statements of the company to analyse the implications in the corporate

accounting. The items have been analysed of the equity, debt, cash flow and the comprehensive

income statement. The issues regarding the corporate income tax has also been referred.

2

This report has been prepared so that information regarding the interim financial statements of

the company can be analysed. In this report the annual financial statements of three companies

have been analysed so that their financial stability in the market can be analysed. The report has

focuses on the financial statements of the company to analyse the implications in the corporate

accounting. The items have been analysed of the equity, debt, cash flow and the comprehensive

income statement. The issues regarding the corporate income tax has also been referred.

2

Contents

Executive Summary:........................................................................................................................2

Introduction:....................................................................................................................................5

Equity and liability:.........................................................................................................................6

1):.................................................................................................................................................6

2):.................................................................................................................................................6

3):.................................................................................................................................................7

Australian Agricultural Limited:.................................................................................................7

Cash Flow Statement.......................................................................................................................7

4):.....................................................................................................................................................7

5):.....................................................................................................................................................8

6):...................................................................................................................................................11

Other compressive income:...........................................................................................................12

7):...............................................................................................................................................12

8):...............................................................................................................................................12

9):...............................................................................................................................................14

10):.............................................................................................................................................15

Corporate Income Tax:..................................................................................................................16

11):.............................................................................................................................................16

3

Executive Summary:........................................................................................................................2

Introduction:....................................................................................................................................5

Equity and liability:.........................................................................................................................6

1):.................................................................................................................................................6

2):.................................................................................................................................................6

3):.................................................................................................................................................7

Australian Agricultural Limited:.................................................................................................7

Cash Flow Statement.......................................................................................................................7

4):.....................................................................................................................................................7

5):.....................................................................................................................................................8

6):...................................................................................................................................................11

Other compressive income:...........................................................................................................12

7):...............................................................................................................................................12

8):...............................................................................................................................................12

9):...............................................................................................................................................14

10):.............................................................................................................................................15

Corporate Income Tax:..................................................................................................................16

11):.............................................................................................................................................16

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

12):.............................................................................................................................................17

13):.............................................................................................................................................18

14):.............................................................................................................................................19

15):.............................................................................................................................................19

16):.............................................................................................................................................20

17):.............................................................................................................................................21

Conclusion:....................................................................................................................................22

References:....................................................................................................................................23

4

13):.............................................................................................................................................18

14):.............................................................................................................................................19

15):.............................................................................................................................................19

16):.............................................................................................................................................20

17):.............................................................................................................................................21

Conclusion:....................................................................................................................................22

References:....................................................................................................................................23

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction:

This report is prepared so that the knowledge can be gained regarding the corporate accounting

and the financial information. In this report three companies Australian Agricultural Company

Limited, Australia Bauxite Limited and Australian Dairy Farms Group are taken. The annual

report of the past three years has been analysed so that the information about the equity, debt, the

activities of the cash flow statements, the items of the comprehensive statement and the

calculation of the book and the cash tax will be evaluated.

Australian Agricultural Limited: It is the beef and the agricultural company which was

founded in the 1824 and has the headquartered in the Brisbane, Australia. The company operates

feedlots and it covers the large area of the land around 7 million hectares.

Australian Bauxite Limited: This Company was founded in the year 2009 and has the

headquartered in the New South Wales, Australia. The company has been dealing into the

industries like fertilisers and the cement and selling the tonnes of the bauxite around 30000

amounting.

Australian Dairy Farms Group: This Company was operating the processing segments of the

dairy farms and was founded in the 1992 and has the headquartered in the Australia. It is the

Australian national body which mainly funds the products of the dairy and the other dairy

snacks.

5

This report is prepared so that the knowledge can be gained regarding the corporate accounting

and the financial information. In this report three companies Australian Agricultural Company

Limited, Australia Bauxite Limited and Australian Dairy Farms Group are taken. The annual

report of the past three years has been analysed so that the information about the equity, debt, the

activities of the cash flow statements, the items of the comprehensive statement and the

calculation of the book and the cash tax will be evaluated.

Australian Agricultural Limited: It is the beef and the agricultural company which was

founded in the 1824 and has the headquartered in the Brisbane, Australia. The company operates

feedlots and it covers the large area of the land around 7 million hectares.

Australian Bauxite Limited: This Company was founded in the year 2009 and has the

headquartered in the New South Wales, Australia. The company has been dealing into the

industries like fertilisers and the cement and selling the tonnes of the bauxite around 30000

amounting.

Australian Dairy Farms Group: This Company was operating the processing segments of the

dairy farms and was founded in the 1992 and has the headquartered in the Australia. It is the

Australian national body which mainly funds the products of the dairy and the other dairy

snacks.

5

Equity and liability:

1):

Australian Agricultural Limited: The items recorded in the equity are retained earnings which

have increased from last past three from the negative balance of the 8969 in the year 2015 to the

130424 in the year 2017. The contributed equity and reserves are also recorded. The total equity

of the company has increased from the last three years in the year 2017 with the amount of the

1017743 from the 762298.

Australian Bauxite Limited: The items recorded in the equity are accumulated losses, issued

capital and the reserve. There is no as such major difference is there but the total equity of the

company has increased from the last year. In the year 2015 the equity of the company was

16884000 which has increased in the year 2017 with the 17315000.

Australian Dairy Farms Group: In this company the items of the equity which are recorded are

reserves, retained earnings and the issued capital. The major change has been occurred is in the

reserves as it was 5056 in the year 2015 but in the year 2016 it was nil and in the year 2017 it

was 363360. The total equity of the company has risen as in the year 2015 it was 27446181 and

in the year 2017 it was 28664198.

2):

Australian Agricultural Limited: The items recorded in the debt are the borrowing and the long

term liabilities of the company. As equity of the company is increasing so the debt of the

company is also increasing. The total debt in the year 2015 was 451793 which have increased in

the year 2016 with the 496983 and in the year 2017 it was 1017743.

Australian Bauxite Limited: The debt recorded in this company was trade and other payables,

employees benefit provisions, and the other liabilities. The debt of the company has declined in

the year 2016 as in the year 2015 it was 2877052 which has declined with the 1508517. In the

year 2017 the debt of the company has increased with the amount of the 1565000.

6

1):

Australian Agricultural Limited: The items recorded in the equity are retained earnings which

have increased from last past three from the negative balance of the 8969 in the year 2015 to the

130424 in the year 2017. The contributed equity and reserves are also recorded. The total equity

of the company has increased from the last three years in the year 2017 with the amount of the

1017743 from the 762298.

Australian Bauxite Limited: The items recorded in the equity are accumulated losses, issued

capital and the reserve. There is no as such major difference is there but the total equity of the

company has increased from the last year. In the year 2015 the equity of the company was

16884000 which has increased in the year 2017 with the 17315000.

Australian Dairy Farms Group: In this company the items of the equity which are recorded are

reserves, retained earnings and the issued capital. The major change has been occurred is in the

reserves as it was 5056 in the year 2015 but in the year 2016 it was nil and in the year 2017 it

was 363360. The total equity of the company has risen as in the year 2015 it was 27446181 and

in the year 2017 it was 28664198.

2):

Australian Agricultural Limited: The items recorded in the debt are the borrowing and the long

term liabilities of the company. As equity of the company is increasing so the debt of the

company is also increasing. The total debt in the year 2015 was 451793 which have increased in

the year 2016 with the 496983 and in the year 2017 it was 1017743.

Australian Bauxite Limited: The debt recorded in this company was trade and other payables,

employees benefit provisions, and the other liabilities. The debt of the company has declined in

the year 2016 as in the year 2015 it was 2877052 which has declined with the 1508517. In the

year 2017 the debt of the company has increased with the amount of the 1565000.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

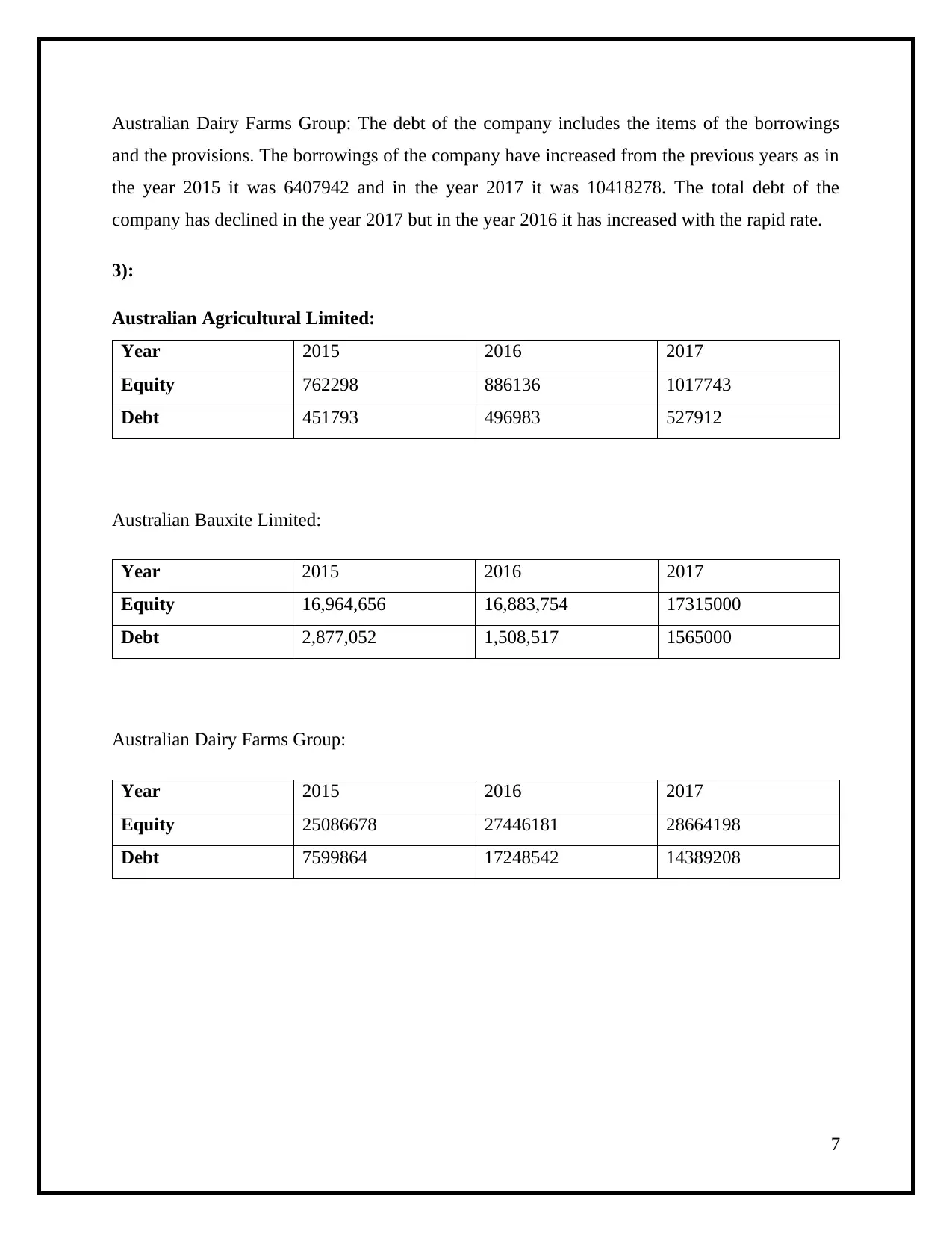

Australian Dairy Farms Group: The debt of the company includes the items of the borrowings

and the provisions. The borrowings of the company have increased from the previous years as in

the year 2015 it was 6407942 and in the year 2017 it was 10418278. The total debt of the

company has declined in the year 2017 but in the year 2016 it has increased with the rapid rate.

3):

Australian Agricultural Limited:

Year 2015 2016 2017

Equity 762298 886136 1017743

Debt 451793 496983 527912

Australian Bauxite Limited:

Year 2015 2016 2017

Equity 16,964,656 16,883,754 17315000

Debt 2,877,052 1,508,517 1565000

Australian Dairy Farms Group:

Year 2015 2016 2017

Equity 25086678 27446181 28664198

Debt 7599864 17248542 14389208

7

and the provisions. The borrowings of the company have increased from the previous years as in

the year 2015 it was 6407942 and in the year 2017 it was 10418278. The total debt of the

company has declined in the year 2017 but in the year 2016 it has increased with the rapid rate.

3):

Australian Agricultural Limited:

Year 2015 2016 2017

Equity 762298 886136 1017743

Debt 451793 496983 527912

Australian Bauxite Limited:

Year 2015 2016 2017

Equity 16,964,656 16,883,754 17315000

Debt 2,877,052 1,508,517 1565000

Australian Dairy Farms Group:

Year 2015 2016 2017

Equity 25086678 27446181 28664198

Debt 7599864 17248542 14389208

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

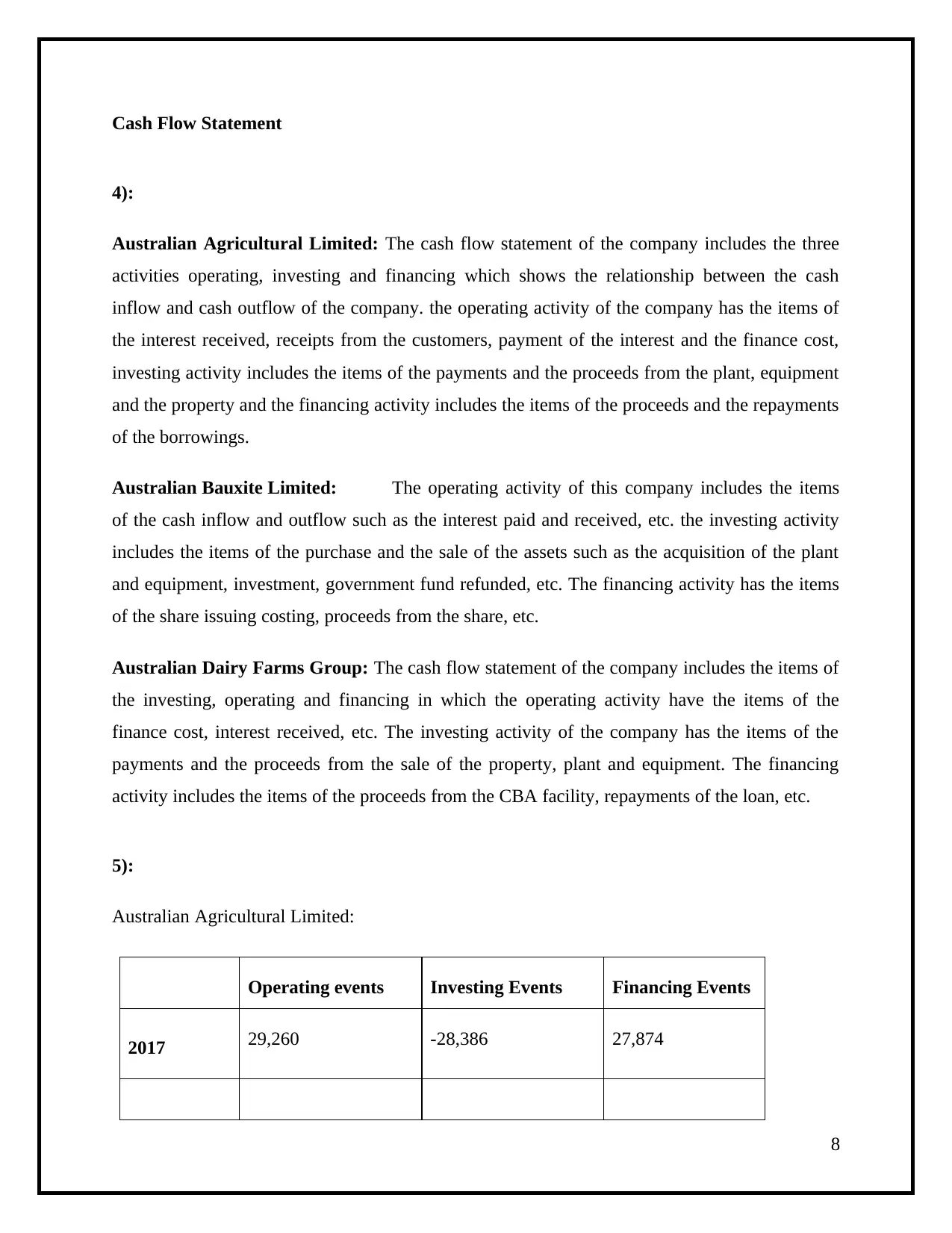

Cash Flow Statement

4):

Australian Agricultural Limited: The cash flow statement of the company includes the three

activities operating, investing and financing which shows the relationship between the cash

inflow and cash outflow of the company. the operating activity of the company has the items of

the interest received, receipts from the customers, payment of the interest and the finance cost,

investing activity includes the items of the payments and the proceeds from the plant, equipment

and the property and the financing activity includes the items of the proceeds and the repayments

of the borrowings.

Australian Bauxite Limited: The operating activity of this company includes the items

of the cash inflow and outflow such as the interest paid and received, etc. the investing activity

includes the items of the purchase and the sale of the assets such as the acquisition of the plant

and equipment, investment, government fund refunded, etc. The financing activity has the items

of the share issuing costing, proceeds from the share, etc.

Australian Dairy Farms Group: The cash flow statement of the company includes the items of

the investing, operating and financing in which the operating activity have the items of the

finance cost, interest received, etc. The investing activity of the company has the items of the

payments and the proceeds from the sale of the property, plant and equipment. The financing

activity includes the items of the proceeds from the CBA facility, repayments of the loan, etc.

5):

Australian Agricultural Limited:

Operating events Investing Events Financing Events

2017 29,260 -28,386 27,874

8

4):

Australian Agricultural Limited: The cash flow statement of the company includes the three

activities operating, investing and financing which shows the relationship between the cash

inflow and cash outflow of the company. the operating activity of the company has the items of

the interest received, receipts from the customers, payment of the interest and the finance cost,

investing activity includes the items of the payments and the proceeds from the plant, equipment

and the property and the financing activity includes the items of the proceeds and the repayments

of the borrowings.

Australian Bauxite Limited: The operating activity of this company includes the items

of the cash inflow and outflow such as the interest paid and received, etc. the investing activity

includes the items of the purchase and the sale of the assets such as the acquisition of the plant

and equipment, investment, government fund refunded, etc. The financing activity has the items

of the share issuing costing, proceeds from the share, etc.

Australian Dairy Farms Group: The cash flow statement of the company includes the items of

the investing, operating and financing in which the operating activity have the items of the

finance cost, interest received, etc. The investing activity of the company has the items of the

payments and the proceeds from the sale of the property, plant and equipment. The financing

activity includes the items of the proceeds from the CBA facility, repayments of the loan, etc.

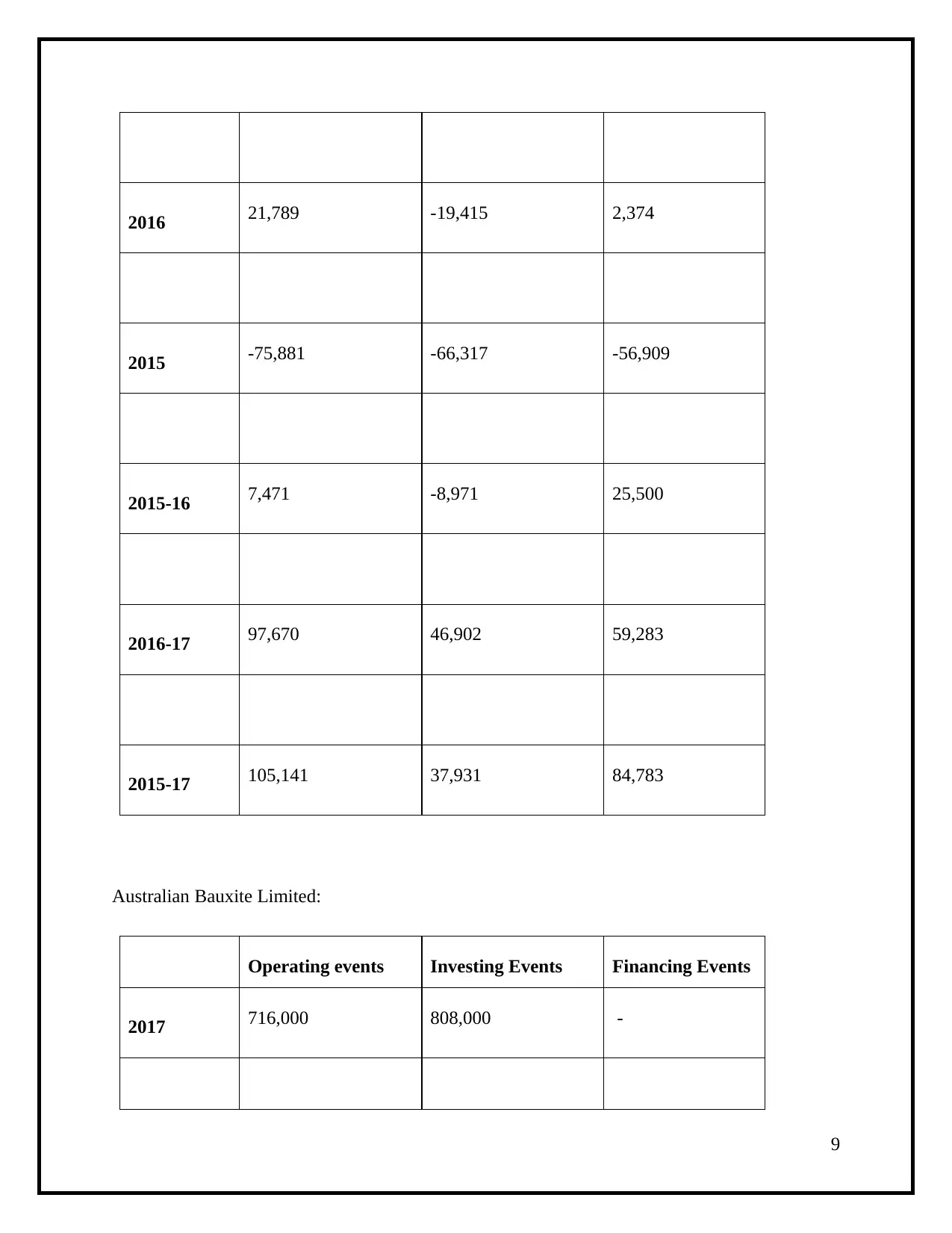

5):

Australian Agricultural Limited:

Operating events Investing Events Financing Events

2017 29,260 -28,386 27,874

8

2016 21,789 -19,415 2,374

2015 -75,881 -66,317 -56,909

2015-16 7,471 -8,971 25,500

2016-17 97,670 46,902 59,283

2015-17 105,141 37,931 84,783

Australian Bauxite Limited:

Operating events Investing Events Financing Events

2017 716,000 808,000 -

9

2015 -75,881 -66,317 -56,909

2015-16 7,471 -8,971 25,500

2016-17 97,670 46,902 59,283

2015-17 105,141 37,931 84,783

Australian Bauxite Limited:

Operating events Investing Events Financing Events

2017 716,000 808,000 -

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

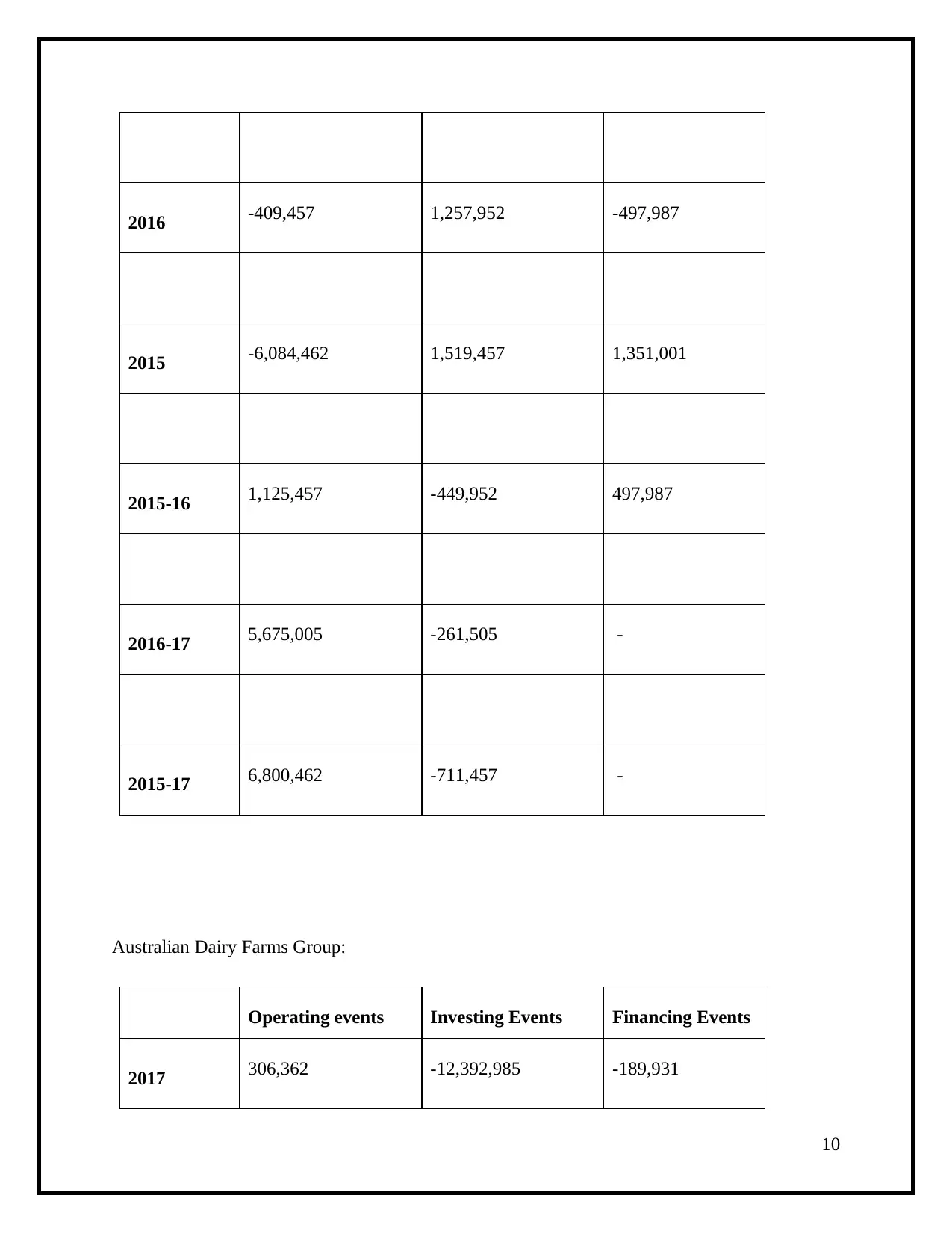

2016 -409,457 1,257,952 -497,987

2015 -6,084,462 1,519,457 1,351,001

2015-16 1,125,457 -449,952 497,987

2016-17 5,675,005 -261,505 -

2015-17 6,800,462 -711,457 -

Australian Dairy Farms Group:

Operating events Investing Events Financing Events

2017 306,362 -12,392,985 -189,931

10

2015 -6,084,462 1,519,457 1,351,001

2015-16 1,125,457 -449,952 497,987

2016-17 5,675,005 -261,505 -

2015-17 6,800,462 -711,457 -

Australian Dairy Farms Group:

Operating events Investing Events Financing Events

2017 306,362 -12,392,985 -189,931

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

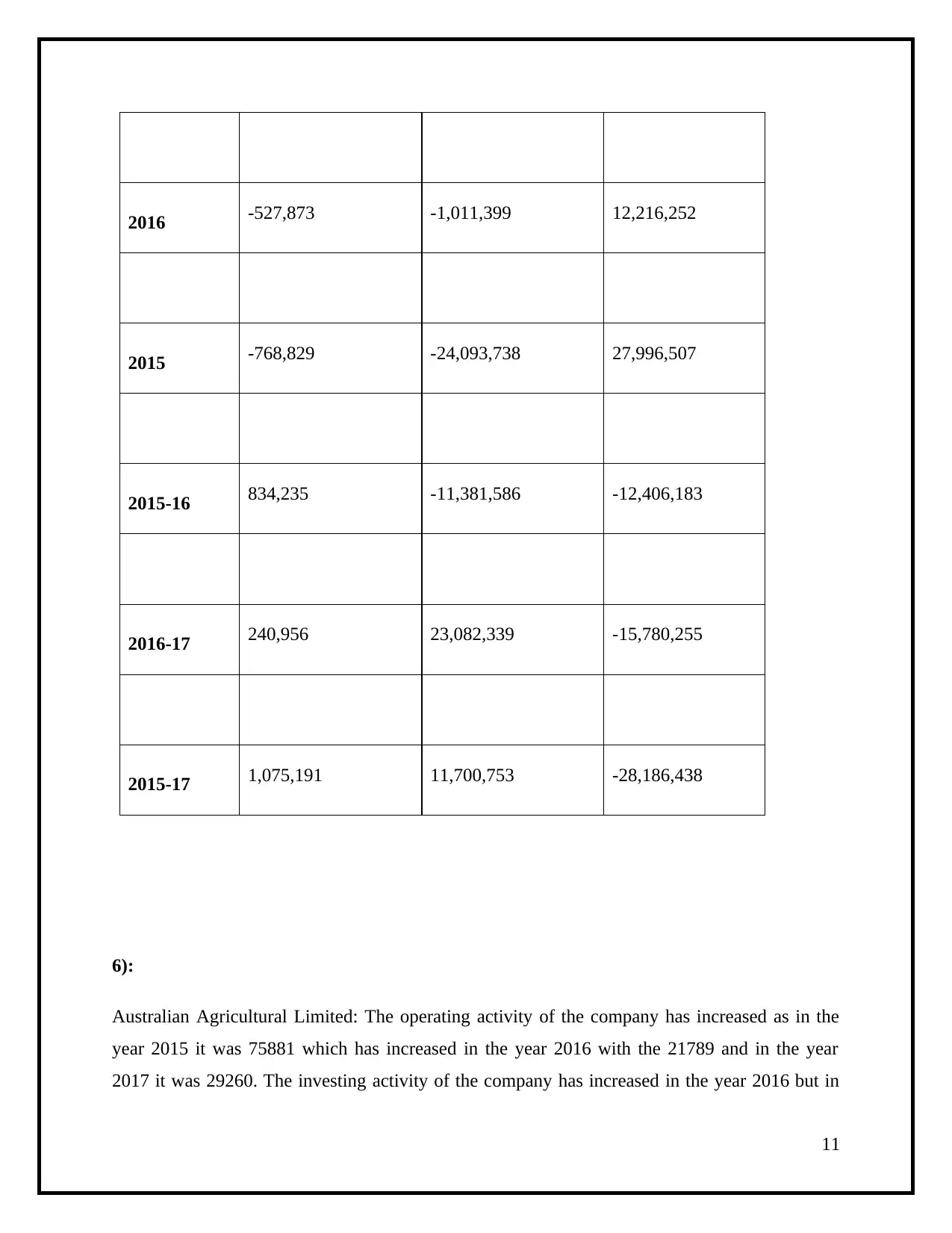

2016 -527,873 -1,011,399 12,216,252

2015 -768,829 -24,093,738 27,996,507

2015-16 834,235 -11,381,586 -12,406,183

2016-17 240,956 23,082,339 -15,780,255

2015-17 1,075,191 11,700,753 -28,186,438

6):

Australian Agricultural Limited: The operating activity of the company has increased as in the

year 2015 it was 75881 which has increased in the year 2016 with the 21789 and in the year

2017 it was 29260. The investing activity of the company has increased in the year 2016 but in

11

2015 -768,829 -24,093,738 27,996,507

2015-16 834,235 -11,381,586 -12,406,183

2016-17 240,956 23,082,339 -15,780,255

2015-17 1,075,191 11,700,753 -28,186,438

6):

Australian Agricultural Limited: The operating activity of the company has increased as in the

year 2015 it was 75881 which has increased in the year 2016 with the 21789 and in the year

2017 it was 29260. The investing activity of the company has increased in the year 2016 but in

11

the year 2017 it has again declined. In the year 2015 it was 66317 2016 it was 19415 and in the

year 2017 it was 28386. The financing activity of the company has increased as in the year 2015

it was 56909 and in the year 2017 it was 27874.

Australian Bauxite Limited: The operating activity of the company has increased from the

previous year as in the year 2015 it has the negative balance of the 6084462 and in the year 2016

it was 409457 and in the year 2017 it was 716000. The investing activity of the company has

also increased as in the year 2015 it was 1519457 and in the year 2016 it was 1257952 and in the

year 2017 it was 808000. The financing activity of the company has declining as in the year 2015

it was 1351001, 2016 it was 497987 with the negative balance and in the year 2017 it was nil.

Australian Dairy Farms Group: The operating activity of the company has increased in the year

2016 but in the year 2017 it was declined. The investing activity of the company has declined in

the year 2016 but it has increased in the year 2017. The financing activity of the company has

increased from the last three years. In the year 2017 it was 189931 and in the year 2015 it was

27996507.

Other compressive income:

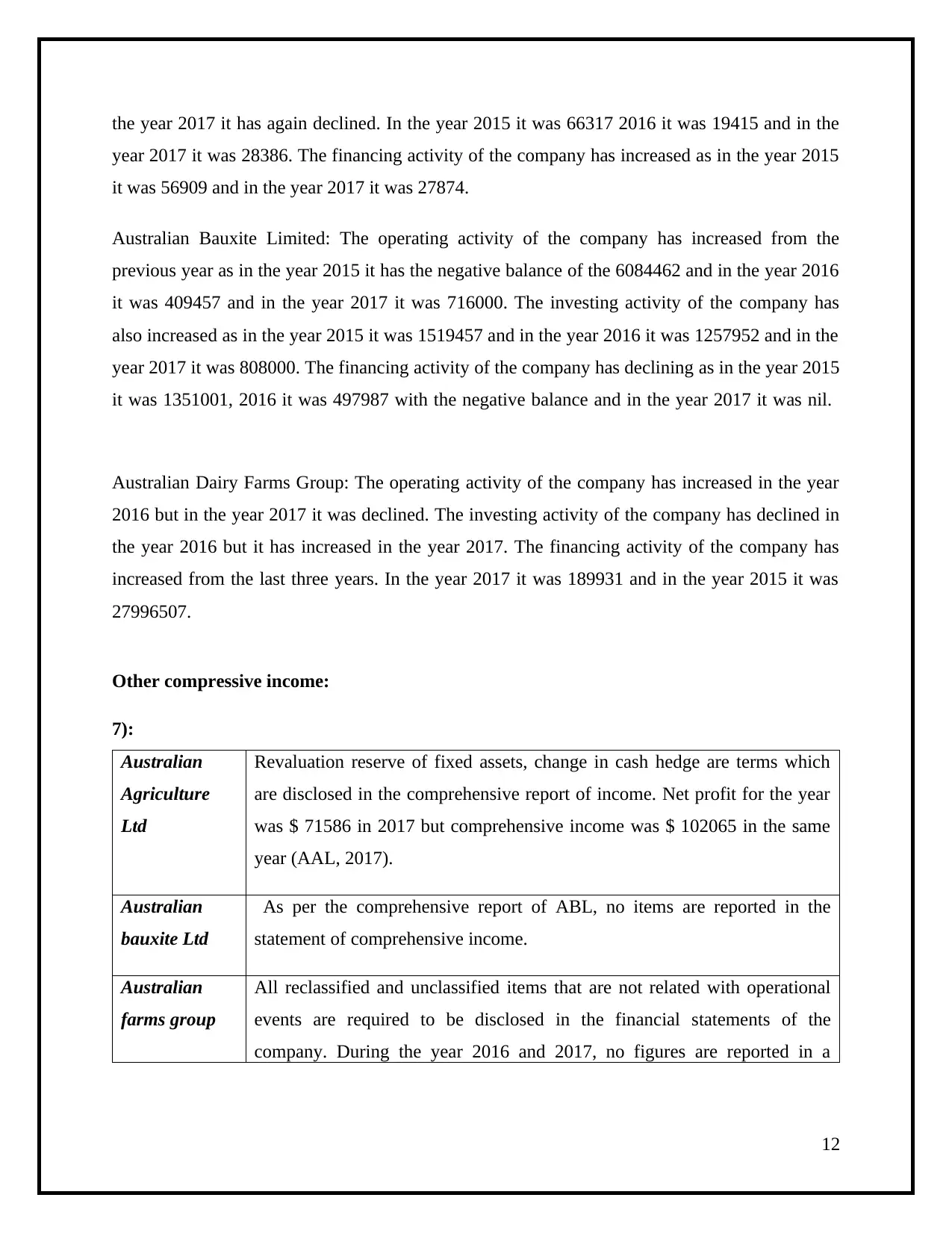

7):

Australian

Agriculture

Ltd

Revaluation reserve of fixed assets, change in cash hedge are terms which

are disclosed in the comprehensive report of income. Net profit for the year

was $ 71586 in 2017 but comprehensive income was $ 102065 in the same

year (AAL, 2017).

Australian

bauxite Ltd

As per the comprehensive report of ABL, no items are reported in the

statement of comprehensive income.

Australian

farms group

All reclassified and unclassified items that are not related with operational

events are required to be disclosed in the financial statements of the

company. During the year 2016 and 2017, no figures are reported in a

12

year 2017 it was 28386. The financing activity of the company has increased as in the year 2015

it was 56909 and in the year 2017 it was 27874.

Australian Bauxite Limited: The operating activity of the company has increased from the

previous year as in the year 2015 it has the negative balance of the 6084462 and in the year 2016

it was 409457 and in the year 2017 it was 716000. The investing activity of the company has

also increased as in the year 2015 it was 1519457 and in the year 2016 it was 1257952 and in the

year 2017 it was 808000. The financing activity of the company has declining as in the year 2015

it was 1351001, 2016 it was 497987 with the negative balance and in the year 2017 it was nil.

Australian Dairy Farms Group: The operating activity of the company has increased in the year

2016 but in the year 2017 it was declined. The investing activity of the company has declined in

the year 2016 but it has increased in the year 2017. The financing activity of the company has

increased from the last three years. In the year 2017 it was 189931 and in the year 2015 it was

27996507.

Other compressive income:

7):

Australian

Agriculture

Ltd

Revaluation reserve of fixed assets, change in cash hedge are terms which

are disclosed in the comprehensive report of income. Net profit for the year

was $ 71586 in 2017 but comprehensive income was $ 102065 in the same

year (AAL, 2017).

Australian

bauxite Ltd

As per the comprehensive report of ABL, no items are reported in the

statement of comprehensive income.

Australian

farms group

All reclassified and unclassified items that are not related with operational

events are required to be disclosed in the financial statements of the

company. During the year 2016 and 2017, no figures are reported in a

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.