Financial Statement Analysis: Harvey Norman and JB Hi-Fi Comparison

VerifiedAdded on 2023/06/05

|22

|4491

|194

Report

AI Summary

This report provides a comprehensive financial analysis of Harvey Norman and JB Hi-Fi, focusing on their capital structure, cash flow statements, and deferred tax payments. The analysis compares the companies' financial leverage, cost of capital, and cash flow activities, including operating, investing, and financing activities. It examines key metrics such as debt-to-equity ratios, retained earnings, and cash tax rates to assess their financial health and sustainability. The report identifies that JB Hi-Fi has a higher debt-to-equity ratio, potentially benefiting from lower cost of capital due to high profitability, while Harvey Norman's lower debt portion may impact its financial leverage and cost of capital. The analysis also highlights differences in cash flow management, with JB Hi-Fi showing higher cash inflow from operating activities and Harvey Norman experiencing higher cash outflow from investing and financial activities. Desklib offers a wide range of similar solved assignments and past papers for students.

Running Head: Corporate Accounting and analysis 0

Corporate Accounting and analysis

Corporate Accounting and analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE ACCOUNTING

Executive Summary

With the ramified economic changes, every organization needs to follow proper

accounting standards and laws while formulating the financial statement and keeping the

business more transparent towards the stakeholders. It is analyzed that company need to

establish the proper equilibrium between its debt capital and equity capital if it wants to

maintain sustainable business practice. In this report, two companies named Harvey Norman

and JB Hi-Fi Company have been chosen to prepare the report. This financial analysis have

been made to evaluate the consolidated financial statement of two companies to evaluate the

deferred tax payment, cash tax payment rate, cash analysis statement and capital structure of

company.

Executive Summary

With the ramified economic changes, every organization needs to follow proper

accounting standards and laws while formulating the financial statement and keeping the

business more transparent towards the stakeholders. It is analyzed that company need to

establish the proper equilibrium between its debt capital and equity capital if it wants to

maintain sustainable business practice. In this report, two companies named Harvey Norman

and JB Hi-Fi Company have been chosen to prepare the report. This financial analysis have

been made to evaluate the consolidated financial statement of two companies to evaluate the

deferred tax payment, cash tax payment rate, cash analysis statement and capital structure of

company.

Running Head: CORPORATE ACCOUNTING

Table of Contents

Executive Summary...............................................................................................................................1

Introduction...........................................................................................................................................4

Answer given to the question no-1........................................................................................................5

Owners’ Equity......................................................................................................................................5

Other Equity Instruments...................................................................................................................6

Reserves............................................................................................................................................6

Retained profits.................................................................................................................................6

Answer given to the question no-2........................................................................................................7

Comparative analysis of JB Hi-Fi Company and Harvey Norman Company both............................7

Answer given to the question no-3........................................................................................................8

Comparative analysis of the cash flow statement of JB Hi-Fi Company and Harvey Norman

Company...........................................................................................................................................8

Answer given to the question no-4......................................................................................................14

Cash outflow from three activities comparative analysis................................................................14

Answer given to the question no-5......................................................................................................16

Comparative analysis of cash flow activities from these three activities.........................................16

Answer given to the question no- 6.....................................................................................................16

Income statement.................................................................................................................................16

Answer given to the question no -7.....................................................................................................17

Answer given to the question no-8......................................................................................................17

Answer given to the question no-9......................................................................................................18

Answer given to the question no-10....................................................................................................18

Answer given to the question no-11....................................................................................................18

Answer given to the question no-12....................................................................................................18

Table of Contents

Executive Summary...............................................................................................................................1

Introduction...........................................................................................................................................4

Answer given to the question no-1........................................................................................................5

Owners’ Equity......................................................................................................................................5

Other Equity Instruments...................................................................................................................6

Reserves............................................................................................................................................6

Retained profits.................................................................................................................................6

Answer given to the question no-2........................................................................................................7

Comparative analysis of JB Hi-Fi Company and Harvey Norman Company both............................7

Answer given to the question no-3........................................................................................................8

Comparative analysis of the cash flow statement of JB Hi-Fi Company and Harvey Norman

Company...........................................................................................................................................8

Answer given to the question no-4......................................................................................................14

Cash outflow from three activities comparative analysis................................................................14

Answer given to the question no-5......................................................................................................16

Comparative analysis of cash flow activities from these three activities.........................................16

Answer given to the question no- 6.....................................................................................................16

Income statement.................................................................................................................................16

Answer given to the question no -7.....................................................................................................17

Answer given to the question no-8......................................................................................................17

Answer given to the question no-9......................................................................................................18

Answer given to the question no-10....................................................................................................18

Answer given to the question no-11....................................................................................................18

Answer given to the question no-12....................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE ACCOUNTING

Answer given to the question no-13....................................................................................................18

Answer given to the question no-14....................................................................................................19

Answer given to the question no-15....................................................................................................19

Answer given to the question no-16....................................................................................................19

Conclusion...........................................................................................................................................20

References...........................................................................................................................................21

Answer given to the question no-13....................................................................................................18

Answer given to the question no-14....................................................................................................19

Answer given to the question no-15....................................................................................................19

Answer given to the question no-16....................................................................................................19

Conclusion...........................................................................................................................................20

References...........................................................................................................................................21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE ACCOUNTING

Introduction

The financial analysis is the tool which is used to evaluate the business sustainability,

financial leverage and cost of capital of organization. In this report, Harvey Norman and JB

Hi-Fi Company has been selected to analyse the capital structure, inflow and outflow of cash

from the cash flow statement and changes in the cash tax rate as per the income tax rules and

regulation and accounting taxation rules. This report has focused on the financial statement

of these two companies and analysis what changes company might face in its accounting

financial recording of these two companies. It has been analyzed that Harvey Norman has

faced high cash outflow from its business due to its increased investment in its other business.

JB HI Fi Company

The JB Hi-Fi Company has international business functioning and operated its business in

offering DVD, CD and other electronic computer peripherals. The main objective of

company is to achieve 30 % market share in the electronic computer peripherals retail

industry (JB Hi Fi, 2018).

HARVEY NORMAN LIMITED

Harvey Norman Company has been offering furniture and fixtures products such as

DVD, CD and other electronic computer peripherals to its clients in Australia. This company

has indulged in maintaining the high quality of computer peripherals and other deals to its

clients in Australia (Harvey Norman, 2016).

Introduction

The financial analysis is the tool which is used to evaluate the business sustainability,

financial leverage and cost of capital of organization. In this report, Harvey Norman and JB

Hi-Fi Company has been selected to analyse the capital structure, inflow and outflow of cash

from the cash flow statement and changes in the cash tax rate as per the income tax rules and

regulation and accounting taxation rules. This report has focused on the financial statement

of these two companies and analysis what changes company might face in its accounting

financial recording of these two companies. It has been analyzed that Harvey Norman has

faced high cash outflow from its business due to its increased investment in its other business.

JB HI Fi Company

The JB Hi-Fi Company has international business functioning and operated its business in

offering DVD, CD and other electronic computer peripherals. The main objective of

company is to achieve 30 % market share in the electronic computer peripherals retail

industry (JB Hi Fi, 2018).

HARVEY NORMAN LIMITED

Harvey Norman Company has been offering furniture and fixtures products such as

DVD, CD and other electronic computer peripherals to its clients in Australia. This company

has indulged in maintaining the high quality of computer peripherals and other deals to its

clients in Australia (Harvey Norman, 2016).

Running Head: CORPORATE ACCOUNTING

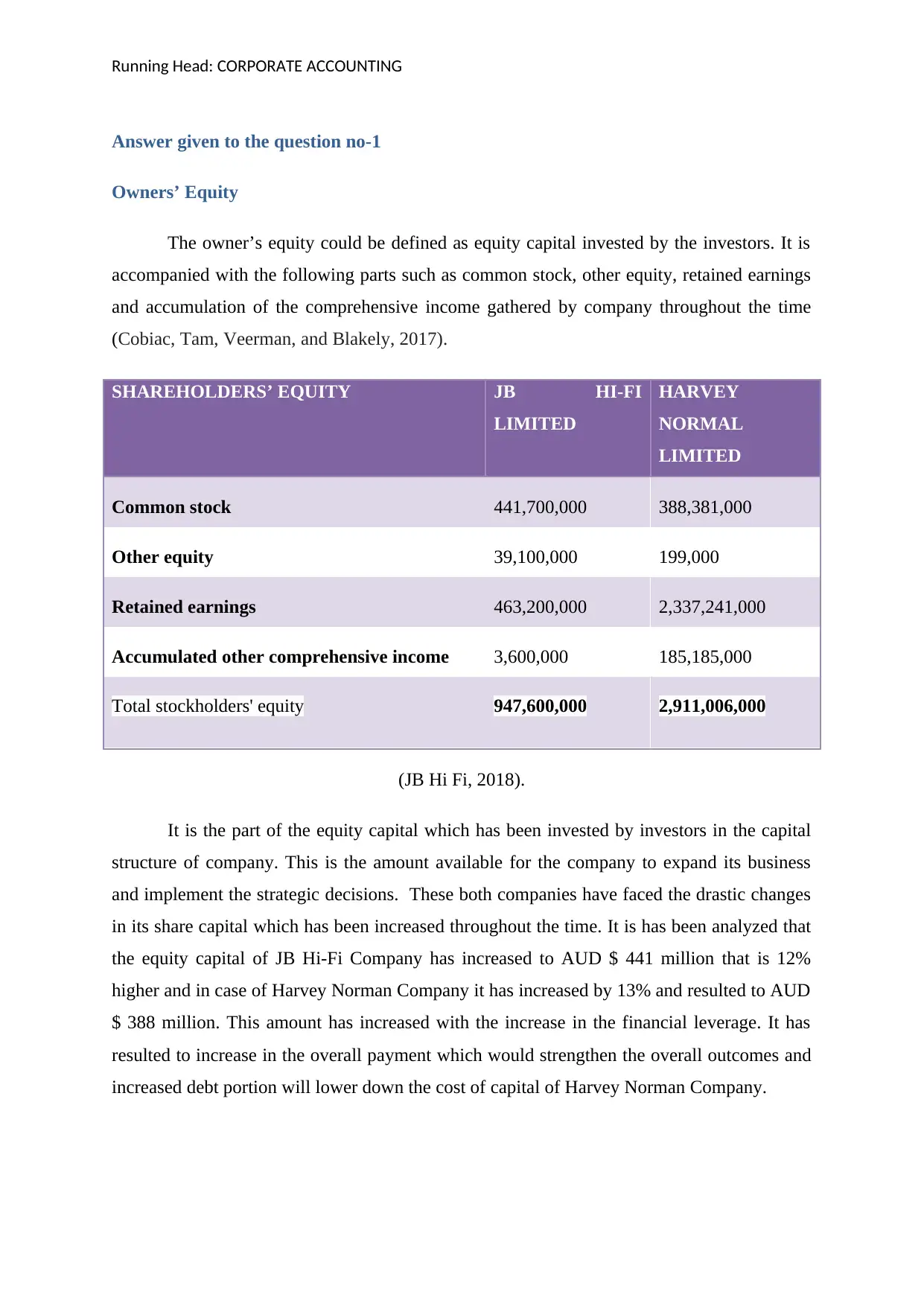

Answer given to the question no-1

Owners’ Equity

The owner’s equity could be defined as equity capital invested by the investors. It is

accompanied with the following parts such as common stock, other equity, retained earnings

and accumulation of the comprehensive income gathered by company throughout the time

(Cobiac, Tam, Veerman, and Blakely, 2017).

SHAREHOLDERS’ EQUITY JB HI-FI

LIMITED

HARVEY

NORMAL

LIMITED

Common stock 441,700,000 388,381,000

Other equity 39,100,000 199,000

Retained earnings 463,200,000 2,337,241,000

Accumulated other comprehensive income 3,600,000 185,185,000

Total stockholders' equity 947,600,000 2,911,006,000

(JB Hi Fi, 2018).

It is the part of the equity capital which has been invested by investors in the capital

structure of company. This is the amount available for the company to expand its business

and implement the strategic decisions. These both companies have faced the drastic changes

in its share capital which has been increased throughout the time. It is has been analyzed that

the equity capital of JB Hi-Fi Company has increased to AUD $ 441 million that is 12%

higher and in case of Harvey Norman Company it has increased by 13% and resulted to AUD

$ 388 million. This amount has increased with the increase in the financial leverage. It has

resulted to increase in the overall payment which would strengthen the overall outcomes and

increased debt portion will lower down the cost of capital of Harvey Norman Company.

Answer given to the question no-1

Owners’ Equity

The owner’s equity could be defined as equity capital invested by the investors. It is

accompanied with the following parts such as common stock, other equity, retained earnings

and accumulation of the comprehensive income gathered by company throughout the time

(Cobiac, Tam, Veerman, and Blakely, 2017).

SHAREHOLDERS’ EQUITY JB HI-FI

LIMITED

HARVEY

NORMAL

LIMITED

Common stock 441,700,000 388,381,000

Other equity 39,100,000 199,000

Retained earnings 463,200,000 2,337,241,000

Accumulated other comprehensive income 3,600,000 185,185,000

Total stockholders' equity 947,600,000 2,911,006,000

(JB Hi Fi, 2018).

It is the part of the equity capital which has been invested by investors in the capital

structure of company. This is the amount available for the company to expand its business

and implement the strategic decisions. These both companies have faced the drastic changes

in its share capital which has been increased throughout the time. It is has been analyzed that

the equity capital of JB Hi-Fi Company has increased to AUD $ 441 million that is 12%

higher and in case of Harvey Norman Company it has increased by 13% and resulted to AUD

$ 388 million. This amount has increased with the increase in the financial leverage. It has

resulted to increase in the overall payment which would strengthen the overall outcomes and

increased debt portion will lower down the cost of capital of Harvey Norman Company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE ACCOUNTING

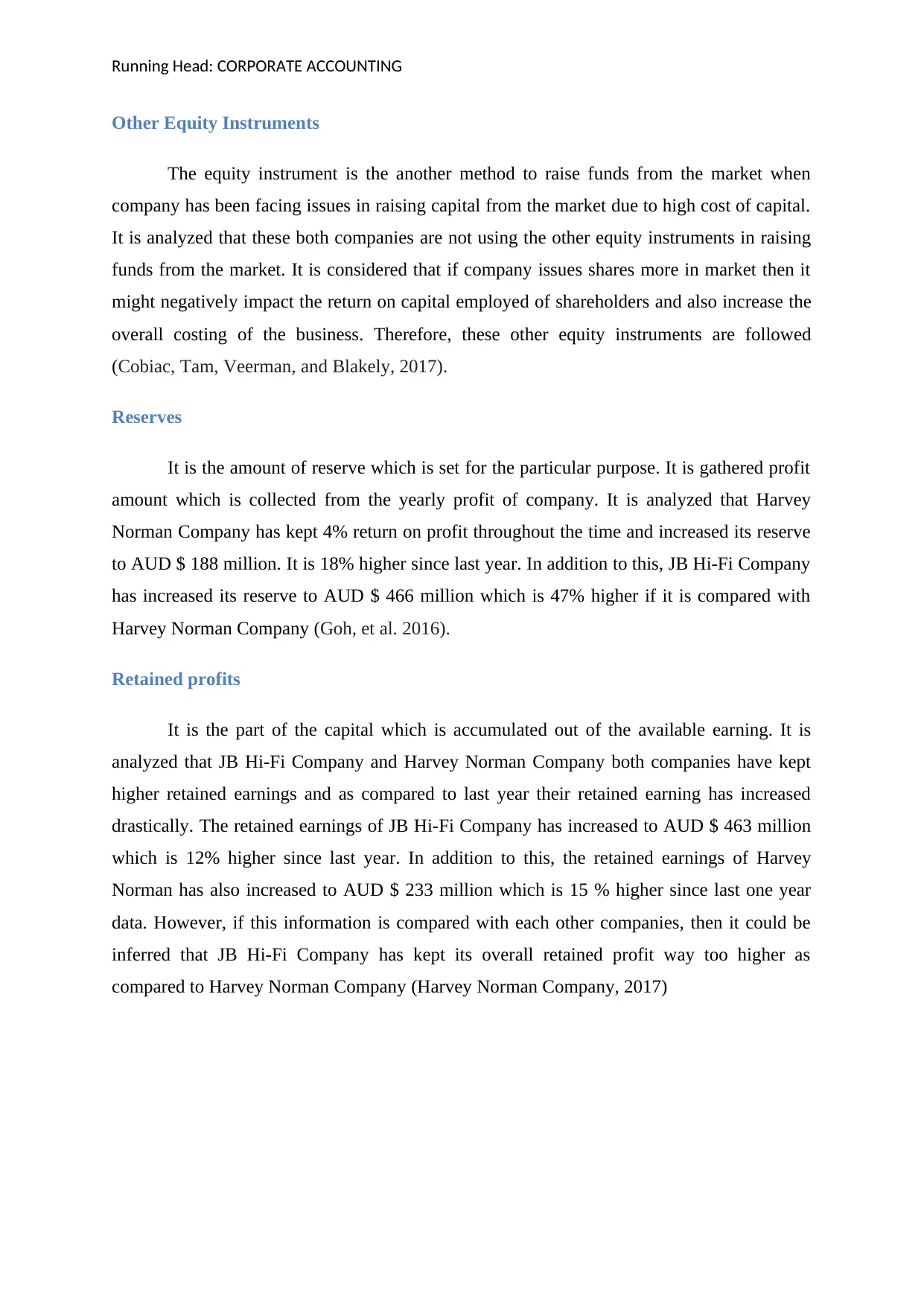

Other Equity Instruments

The equity instrument is the another method to raise funds from the market when

company has been facing issues in raising capital from the market due to high cost of capital.

It is analyzed that these both companies are not using the other equity instruments in raising

funds from the market. It is considered that if company issues shares more in market then it

might negatively impact the return on capital employed of shareholders and also increase the

overall costing of the business. Therefore, these other equity instruments are followed

(Cobiac, Tam, Veerman, and Blakely, 2017).

Reserves

It is the amount of reserve which is set for the particular purpose. It is gathered profit

amount which is collected from the yearly profit of company. It is analyzed that Harvey

Norman Company has kept 4% return on profit throughout the time and increased its reserve

to AUD $ 188 million. It is 18% higher since last year. In addition to this, JB Hi-Fi Company

has increased its reserve to AUD $ 466 million which is 47% higher if it is compared with

Harvey Norman Company (Goh, et al. 2016).

Retained profits

It is the part of the capital which is accumulated out of the available earning. It is

analyzed that JB Hi-Fi Company and Harvey Norman Company both companies have kept

higher retained earnings and as compared to last year their retained earning has increased

drastically. The retained earnings of JB Hi-Fi Company has increased to AUD $ 463 million

which is 12% higher since last year. In addition to this, the retained earnings of Harvey

Norman has also increased to AUD $ 233 million which is 15 % higher since last one year

data. However, if this information is compared with each other companies, then it could be

inferred that JB Hi-Fi Company has kept its overall retained profit way too higher as

compared to Harvey Norman Company (Harvey Norman Company, 2017)

Other Equity Instruments

The equity instrument is the another method to raise funds from the market when

company has been facing issues in raising capital from the market due to high cost of capital.

It is analyzed that these both companies are not using the other equity instruments in raising

funds from the market. It is considered that if company issues shares more in market then it

might negatively impact the return on capital employed of shareholders and also increase the

overall costing of the business. Therefore, these other equity instruments are followed

(Cobiac, Tam, Veerman, and Blakely, 2017).

Reserves

It is the amount of reserve which is set for the particular purpose. It is gathered profit

amount which is collected from the yearly profit of company. It is analyzed that Harvey

Norman Company has kept 4% return on profit throughout the time and increased its reserve

to AUD $ 188 million. It is 18% higher since last year. In addition to this, JB Hi-Fi Company

has increased its reserve to AUD $ 466 million which is 47% higher if it is compared with

Harvey Norman Company (Goh, et al. 2016).

Retained profits

It is the part of the capital which is accumulated out of the available earning. It is

analyzed that JB Hi-Fi Company and Harvey Norman Company both companies have kept

higher retained earnings and as compared to last year their retained earning has increased

drastically. The retained earnings of JB Hi-Fi Company has increased to AUD $ 463 million

which is 12% higher since last year. In addition to this, the retained earnings of Harvey

Norman has also increased to AUD $ 233 million which is 15 % higher since last one year

data. However, if this information is compared with each other companies, then it could be

inferred that JB Hi-Fi Company has kept its overall retained profit way too higher as

compared to Harvey Norman Company (Harvey Norman Company, 2017)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE ACCOUNTING

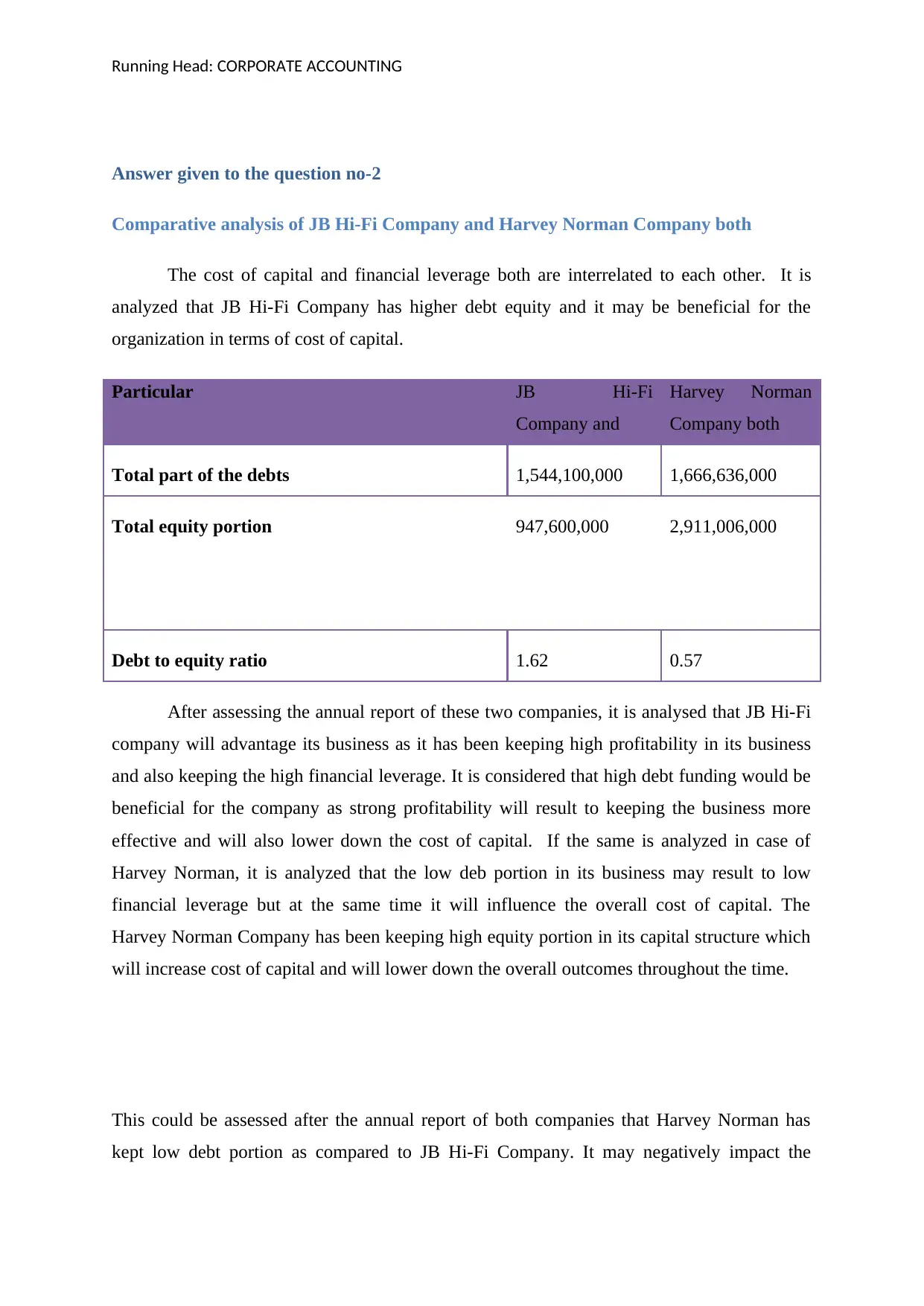

Answer given to the question no-2

Comparative analysis of JB Hi-Fi Company and Harvey Norman Company both

The cost of capital and financial leverage both are interrelated to each other. It is

analyzed that JB Hi-Fi Company has higher debt equity and it may be beneficial for the

organization in terms of cost of capital.

Particular JB Hi-Fi

Company and

Harvey Norman

Company both

Total part of the debts 1,544,100,000 1,666,636,000

Total equity portion 947,600,000 2,911,006,000

Debt to equity ratio 1.62 0.57

After assessing the annual report of these two companies, it is analysed that JB Hi-Fi

company will advantage its business as it has been keeping high profitability in its business

and also keeping the high financial leverage. It is considered that high debt funding would be

beneficial for the company as strong profitability will result to keeping the business more

effective and will also lower down the cost of capital. If the same is analyzed in case of

Harvey Norman, it is analyzed that the low deb portion in its business may result to low

financial leverage but at the same time it will influence the overall cost of capital. The

Harvey Norman Company has been keeping high equity portion in its capital structure which

will increase cost of capital and will lower down the overall outcomes throughout the time.

This could be assessed after the annual report of both companies that Harvey Norman has

kept low debt portion as compared to JB Hi-Fi Company. It may negatively impact the

Answer given to the question no-2

Comparative analysis of JB Hi-Fi Company and Harvey Norman Company both

The cost of capital and financial leverage both are interrelated to each other. It is

analyzed that JB Hi-Fi Company has higher debt equity and it may be beneficial for the

organization in terms of cost of capital.

Particular JB Hi-Fi

Company and

Harvey Norman

Company both

Total part of the debts 1,544,100,000 1,666,636,000

Total equity portion 947,600,000 2,911,006,000

Debt to equity ratio 1.62 0.57

After assessing the annual report of these two companies, it is analysed that JB Hi-Fi

company will advantage its business as it has been keeping high profitability in its business

and also keeping the high financial leverage. It is considered that high debt funding would be

beneficial for the company as strong profitability will result to keeping the business more

effective and will also lower down the cost of capital. If the same is analyzed in case of

Harvey Norman, it is analyzed that the low deb portion in its business may result to low

financial leverage but at the same time it will influence the overall cost of capital. The

Harvey Norman Company has been keeping high equity portion in its capital structure which

will increase cost of capital and will lower down the overall outcomes throughout the time.

This could be assessed after the annual report of both companies that Harvey Norman has

kept low debt portion as compared to JB Hi-Fi Company. It may negatively impact the

Running Head: CORPORATE ACCOUNTING

business functioning and may also negatively impact the return on capital employed of

Harvey Norman. Company needs to establish the equilibrium point at which it will have

balanced cost of capital and financial leverage (Harvey Norman, (2018).

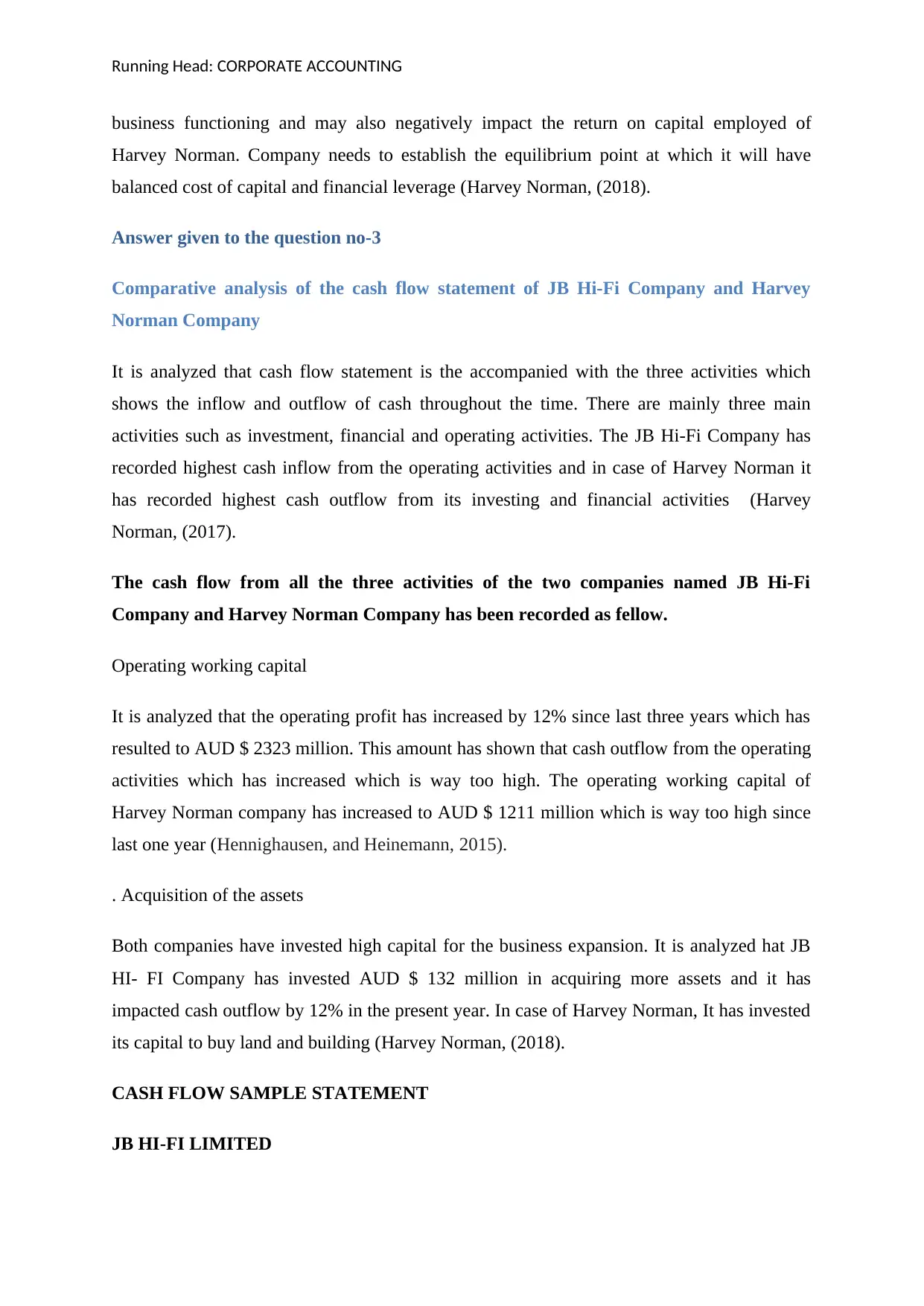

Answer given to the question no-3

Comparative analysis of the cash flow statement of JB Hi-Fi Company and Harvey

Norman Company

It is analyzed that cash flow statement is the accompanied with the three activities which

shows the inflow and outflow of cash throughout the time. There are mainly three main

activities such as investment, financial and operating activities. The JB Hi-Fi Company has

recorded highest cash inflow from the operating activities and in case of Harvey Norman it

has recorded highest cash outflow from its investing and financial activities (Harvey

Norman, (2017).

The cash flow from all the three activities of the two companies named JB Hi-Fi

Company and Harvey Norman Company has been recorded as fellow.

Operating working capital

It is analyzed that the operating profit has increased by 12% since last three years which has

resulted to AUD $ 2323 million. This amount has shown that cash outflow from the operating

activities which has increased which is way too high. The operating working capital of

Harvey Norman company has increased to AUD $ 1211 million which is way too high since

last one year (Hennighausen, and Heinemann, 2015).

. Acquisition of the assets

Both companies have invested high capital for the business expansion. It is analyzed hat JB

HI- FI Company has invested AUD $ 132 million in acquiring more assets and it has

impacted cash outflow by 12% in the present year. In case of Harvey Norman, It has invested

its capital to buy land and building (Harvey Norman, (2018).

CASH FLOW SAMPLE STATEMENT

JB HI-FI LIMITED

business functioning and may also negatively impact the return on capital employed of

Harvey Norman. Company needs to establish the equilibrium point at which it will have

balanced cost of capital and financial leverage (Harvey Norman, (2018).

Answer given to the question no-3

Comparative analysis of the cash flow statement of JB Hi-Fi Company and Harvey

Norman Company

It is analyzed that cash flow statement is the accompanied with the three activities which

shows the inflow and outflow of cash throughout the time. There are mainly three main

activities such as investment, financial and operating activities. The JB Hi-Fi Company has

recorded highest cash inflow from the operating activities and in case of Harvey Norman it

has recorded highest cash outflow from its investing and financial activities (Harvey

Norman, (2017).

The cash flow from all the three activities of the two companies named JB Hi-Fi

Company and Harvey Norman Company has been recorded as fellow.

Operating working capital

It is analyzed that the operating profit has increased by 12% since last three years which has

resulted to AUD $ 2323 million. This amount has shown that cash outflow from the operating

activities which has increased which is way too high. The operating working capital of

Harvey Norman company has increased to AUD $ 1211 million which is way too high since

last one year (Hennighausen, and Heinemann, 2015).

. Acquisition of the assets

Both companies have invested high capital for the business expansion. It is analyzed hat JB

HI- FI Company has invested AUD $ 132 million in acquiring more assets and it has

impacted cash outflow by 12% in the present year. In case of Harvey Norman, It has invested

its capital to buy land and building (Harvey Norman, (2018).

CASH FLOW SAMPLE STATEMENT

JB HI-FI LIMITED

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: CORPORATE ACCOUNTING

2018 ($ IN

000,000)

2017 ($ IN

000,000)

CASH FLOWS AS REPORTED BY THE

INVESTING ACTIVITIES

Payment made for business combination (net basis) - (836.6)

Acquisition of plant & equipment (54.4) (49.1)

cash received from sale of plant & equipment 0.4 0.2

CASH USED BY INVESTING ACTIVITIES (54.4) (885.5)

% CHANGE 93.85%

CASH FLOWS AS REPORTED BY THE

OPERATING ACTIVITIES

Receipts from customers 7551.9 6205.5

Payments made to employees and suppliers (7130.5) (5908.8)

Receipt of interest 0.5 1.7

Payment of interest and other finance cost (15.0) (9.3)

Payment of income taxes (114.8) (98.5)

CASH GENERATED BY OPERATING ACTIVITIES 292.1 190.6

% CHANGE 53.25%

CASH FLOWS REPORTED BY FINANCING

ACTIVITIES

Cash receipt on issue of shares 3.0 395.9

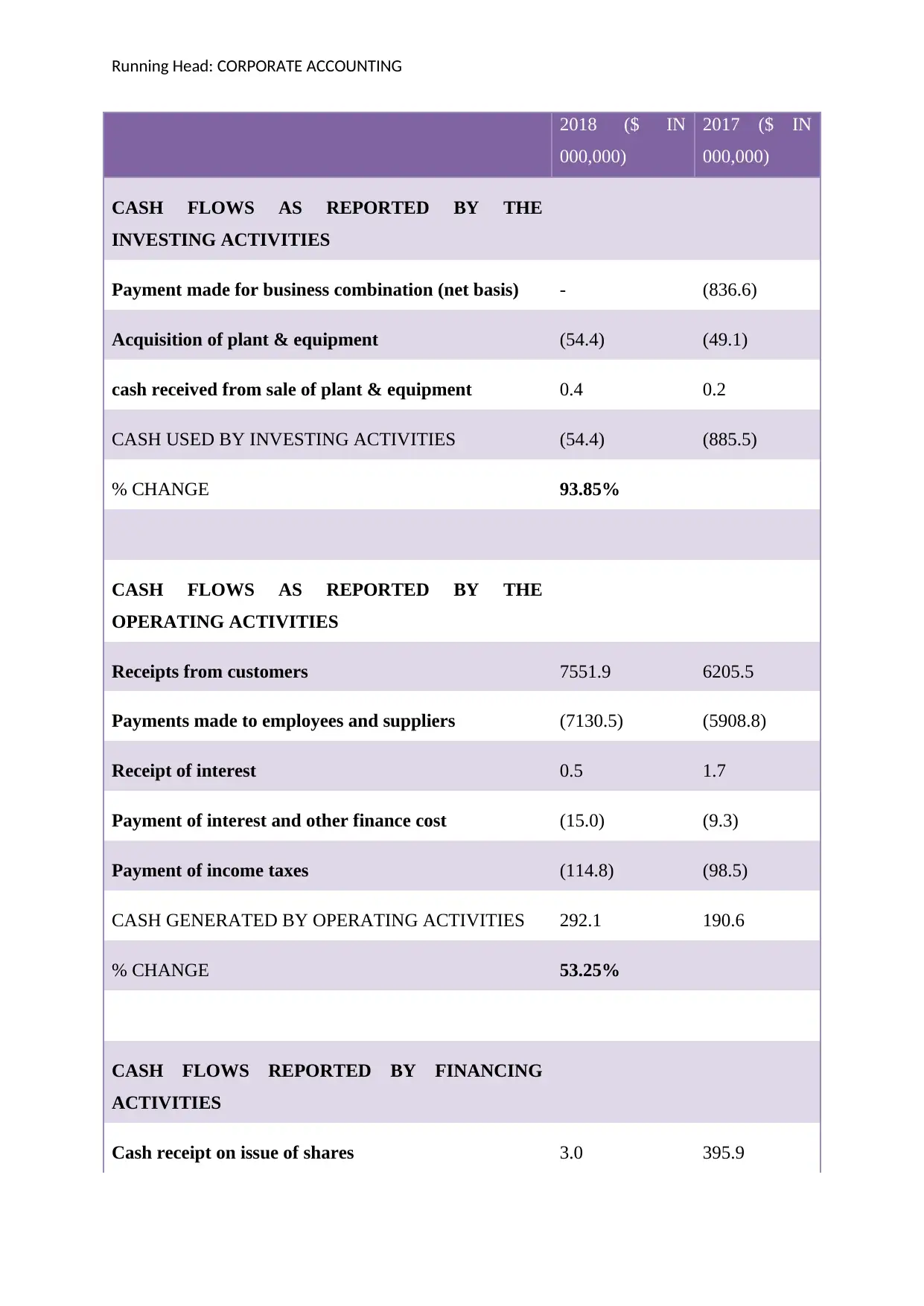

2018 ($ IN

000,000)

2017 ($ IN

000,000)

CASH FLOWS AS REPORTED BY THE

INVESTING ACTIVITIES

Payment made for business combination (net basis) - (836.6)

Acquisition of plant & equipment (54.4) (49.1)

cash received from sale of plant & equipment 0.4 0.2

CASH USED BY INVESTING ACTIVITIES (54.4) (885.5)

% CHANGE 93.85%

CASH FLOWS AS REPORTED BY THE

OPERATING ACTIVITIES

Receipts from customers 7551.9 6205.5

Payments made to employees and suppliers (7130.5) (5908.8)

Receipt of interest 0.5 1.7

Payment of interest and other finance cost (15.0) (9.3)

Payment of income taxes (114.8) (98.5)

CASH GENERATED BY OPERATING ACTIVITIES 292.1 190.6

% CHANGE 53.25%

CASH FLOWS REPORTED BY FINANCING

ACTIVITIES

Cash receipt on issue of shares 3.0 395.9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: CORPORATE ACCOUNTING

(Repayment) or proceeds of borrowings (89.7) 450.0

Payment for issue costs of debt (0.8) (1.7)

Cost of share issue - (9.2)

Dividend payment made to the company’s owners (151.6) (119.1)

Cash (used) or generated by financing activities (239.1) 715.9

% CHANGE (133.40 %)

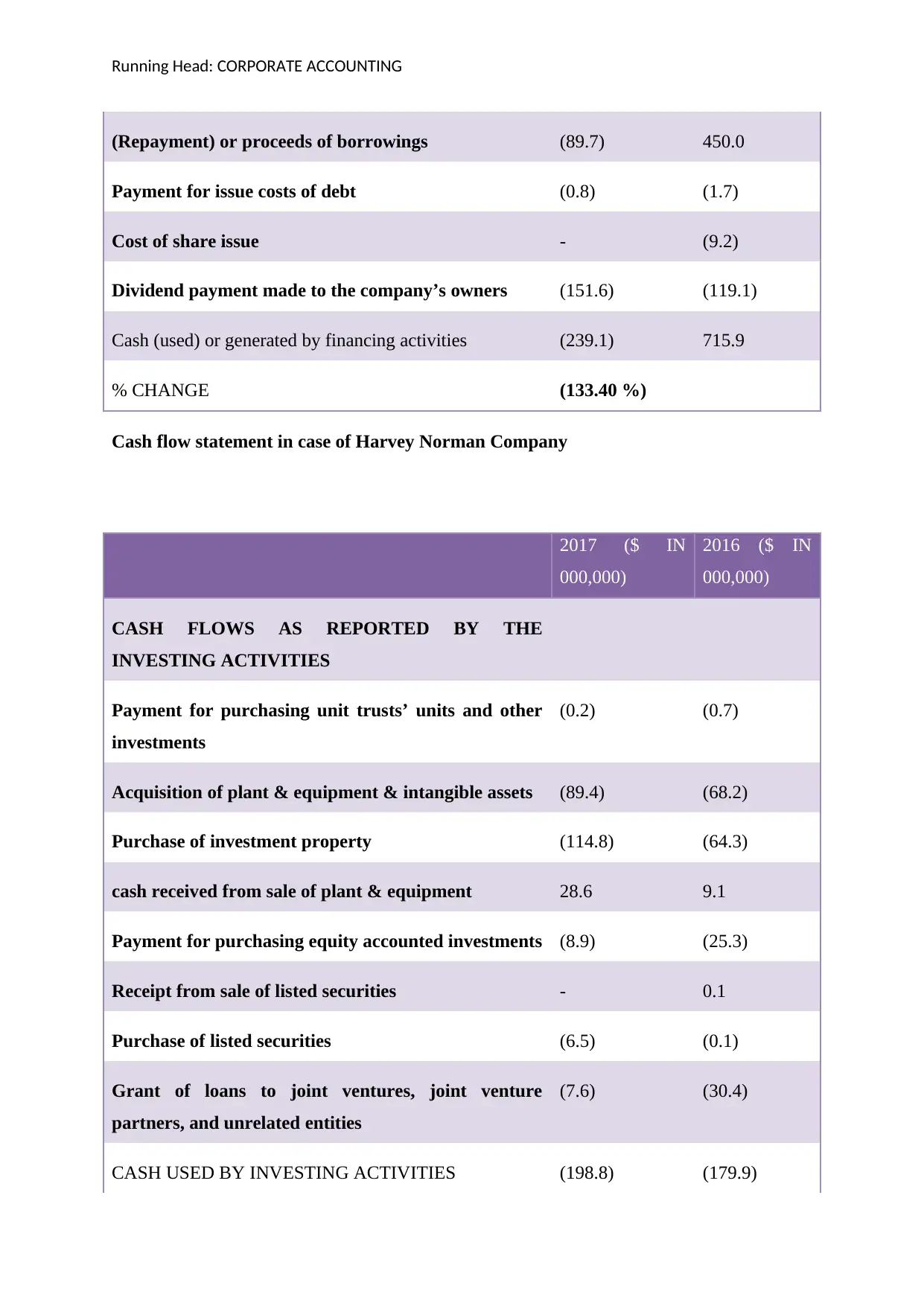

Cash flow statement in case of Harvey Norman Company

2017 ($ IN

000,000)

2016 ($ IN

000,000)

CASH FLOWS AS REPORTED BY THE

INVESTING ACTIVITIES

Payment for purchasing unit trusts’ units and other

investments

(0.2) (0.7)

Acquisition of plant & equipment & intangible assets (89.4) (68.2)

Purchase of investment property (114.8) (64.3)

cash received from sale of plant & equipment 28.6 9.1

Payment for purchasing equity accounted investments (8.9) (25.3)

Receipt from sale of listed securities - 0.1

Purchase of listed securities (6.5) (0.1)

Grant of loans to joint ventures, joint venture

partners, and unrelated entities

(7.6) (30.4)

CASH USED BY INVESTING ACTIVITIES (198.8) (179.9)

(Repayment) or proceeds of borrowings (89.7) 450.0

Payment for issue costs of debt (0.8) (1.7)

Cost of share issue - (9.2)

Dividend payment made to the company’s owners (151.6) (119.1)

Cash (used) or generated by financing activities (239.1) 715.9

% CHANGE (133.40 %)

Cash flow statement in case of Harvey Norman Company

2017 ($ IN

000,000)

2016 ($ IN

000,000)

CASH FLOWS AS REPORTED BY THE

INVESTING ACTIVITIES

Payment for purchasing unit trusts’ units and other

investments

(0.2) (0.7)

Acquisition of plant & equipment & intangible assets (89.4) (68.2)

Purchase of investment property (114.8) (64.3)

cash received from sale of plant & equipment 28.6 9.1

Payment for purchasing equity accounted investments (8.9) (25.3)

Receipt from sale of listed securities - 0.1

Purchase of listed securities (6.5) (0.1)

Grant of loans to joint ventures, joint venture

partners, and unrelated entities

(7.6) (30.4)

CASH USED BY INVESTING ACTIVITIES (198.8) (179.9)

Running Head: CORPORATE ACCOUNTING

% CHANGE (10.51 %)

CASH FLOWS AS REPORTED BY THE

OPERATING ACTIVITIES

Receipts from franchisee 882.5 949.2

Receipts from customers 1992.9 1932.4

Payments made to employees and suppliers (2252.9) (2267.6)

Receipt of distribution from joint venture 11.5 10.6

Payment of GST (44.6) (52.2)

Receipt of interest 5.0 7.6

Payment of interest and other finance cost (19.4) (28.8)

Payment of income taxes (152.5) (115.5)

Receipt of dividend 2.7 2.1

CASH GENERATED BY OPERATING ACTIVITIES 425.1 437.7

% CHANGE (2.88 %)

CASH FLOWS REPORTED BY FINANCING

ACTIVITIES

Cash receipt on issue of shares 1.0 5.0

(Repayment) or proceeds of borrowings (15.3) 0.3

Proceeds from syndicated facilities 70.0 -

Loan receiver or (repaid) to related parties 2.1 (45.9)

% CHANGE (10.51 %)

CASH FLOWS AS REPORTED BY THE

OPERATING ACTIVITIES

Receipts from franchisee 882.5 949.2

Receipts from customers 1992.9 1932.4

Payments made to employees and suppliers (2252.9) (2267.6)

Receipt of distribution from joint venture 11.5 10.6

Payment of GST (44.6) (52.2)

Receipt of interest 5.0 7.6

Payment of interest and other finance cost (19.4) (28.8)

Payment of income taxes (152.5) (115.5)

Receipt of dividend 2.7 2.1

CASH GENERATED BY OPERATING ACTIVITIES 425.1 437.7

% CHANGE (2.88 %)

CASH FLOWS REPORTED BY FINANCING

ACTIVITIES

Cash receipt on issue of shares 1.0 5.0

(Repayment) or proceeds of borrowings (15.3) 0.3

Proceeds from syndicated facilities 70.0 -

Loan receiver or (repaid) to related parties 2.1 (45.9)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.