HA2032: Corporate and Financial Accounting: Funds and Entity Analysis

VerifiedAdded on 2022/10/17

|12

|3269

|193

Report

AI Summary

This report provides a comprehensive analysis of corporate and financial accounting, examining the various sources of funds that companies utilize. The report delves into the specifics of owner's equity, including contributed equity, retained earnings, and reserves, and tracks the movement of these items over a three-year period for both Woolworths and Wesfarmers. It also investigates the liabilities section, covering borrowings, tax payable, trade payable, and provisions, with an analysis of the changes in these items. Furthermore, the report explores the merits and demerits of different funding sources. Finally, the report discusses the classification of companies into large and small proprietary entities and the implications of such classifications, including compliance and reporting requirements. The analysis provides insights into financial management practices and the impact of funding decisions on company performance.

1

Corporate and financial accounting

Corporate and financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

In the report, there is the consideration which is provided to the items which are included in the

two sources of the funds which are used by the company. There is the consideration of the

various items which are included in the owner’s equity and with that, there is the determination

of the changes which are taking place in the amount of the same. There is the determination of

the amounts which are included in the liabilities and in that also the change has been noted. The

reason which is responsible for the deviation is also identified. There is the determination of the

advantages and disadvantages of various sources which have been used. The large and small

company are classified as per some concept and that is identified with the implication that is

involved in this respect.

Executive summary

In the report, there is the consideration which is provided to the items which are included in the

two sources of the funds which are used by the company. There is the consideration of the

various items which are included in the owner’s equity and with that, there is the determination

of the changes which are taking place in the amount of the same. There is the determination of

the amounts which are included in the liabilities and in that also the change has been noted. The

reason which is responsible for the deviation is also identified. There is the determination of the

advantages and disadvantages of various sources which have been used. The large and small

company are classified as per some concept and that is identified with the implication that is

involved in this respect.

3

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part A...............................................................................................................................................4

i) Items under owners’ equity......................................................................................................4

ii) Movement in each item of equity............................................................................................5

iii) Items under the liability section.............................................................................................6

iv) Changes in items involved in liabilities.................................................................................7

v) Merits and demerits of the sources of funds............................................................................8

Part B...............................................................................................................................................8

Large and small proprietary company related concept................................................................8

Compliance and reporting requirements......................................................................................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part A...............................................................................................................................................4

i) Items under owners’ equity......................................................................................................4

ii) Movement in each item of equity............................................................................................5

iii) Items under the liability section.............................................................................................6

iv) Changes in items involved in liabilities.................................................................................7

v) Merits and demerits of the sources of funds............................................................................8

Part B...............................................................................................................................................8

Large and small proprietary company related concept................................................................8

Compliance and reporting requirements......................................................................................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

The company undertakes various operations and in that process, there is a large amount which is

spent and in that the company will be required to make the arrangement with the help of various

sources which are available. There is the identification of the equity and liability in the business

and in that the various other elements are also covered. The main items of the equity will be

considered in this report in relation to the Woolworth and Wesfarmers. There will be a proper

description which will be provided and in that the amount which is raised with the help of them

will be identified and taken into consideration. The changes which are involved will also be

taken into consideration. The liabilities which have been taken by the company will also be

considered and in that there will be various aspects which will be involved. There will be

consideration of the various changes which are taking place and with that the reason for the same

will also be involved in the report. The main merits and demerits which are faced because of

them will be included. The companies are classified in the small and large proprietary company

and the concept which will be followed for it will be discussed. After the determination, there

will be certain implications on them and they will also be taken into consideration.

Part A

i) Items under owners’ equity

Owner’s equity is the amount which is raised by the owner of the company and they are

considered as the funds of the company (Drover et al., 2017). They will be with the company and

are not required to be repaid. Under this also there are various categories which are included and

they are explained below.

Contributed equity: Contributed equity is the amount which is contributed by various investors

in the form of the equity of the company. In this, there will be equity issue which is made by the

company and then the shares which are provided are availed by the interested parties and they

will be paying an amount for the same. There will be consideration of the various aspects such as

profitability by the buyer before they invest in the company. This is the main source and there is

no additional cost which is to be incurred on the same.

Introduction

The company undertakes various operations and in that process, there is a large amount which is

spent and in that the company will be required to make the arrangement with the help of various

sources which are available. There is the identification of the equity and liability in the business

and in that the various other elements are also covered. The main items of the equity will be

considered in this report in relation to the Woolworth and Wesfarmers. There will be a proper

description which will be provided and in that the amount which is raised with the help of them

will be identified and taken into consideration. The changes which are involved will also be

taken into consideration. The liabilities which have been taken by the company will also be

considered and in that there will be various aspects which will be involved. There will be

consideration of the various changes which are taking place and with that the reason for the same

will also be involved in the report. The main merits and demerits which are faced because of

them will be included. The companies are classified in the small and large proprietary company

and the concept which will be followed for it will be discussed. After the determination, there

will be certain implications on them and they will also be taken into consideration.

Part A

i) Items under owners’ equity

Owner’s equity is the amount which is raised by the owner of the company and they are

considered as the funds of the company (Drover et al., 2017). They will be with the company and

are not required to be repaid. Under this also there are various categories which are included and

they are explained below.

Contributed equity: Contributed equity is the amount which is contributed by various investors

in the form of the equity of the company. In this, there will be equity issue which is made by the

company and then the shares which are provided are availed by the interested parties and they

will be paying an amount for the same. There will be consideration of the various aspects such as

profitability by the buyer before they invest in the company. This is the main source and there is

no additional cost which is to be incurred on the same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

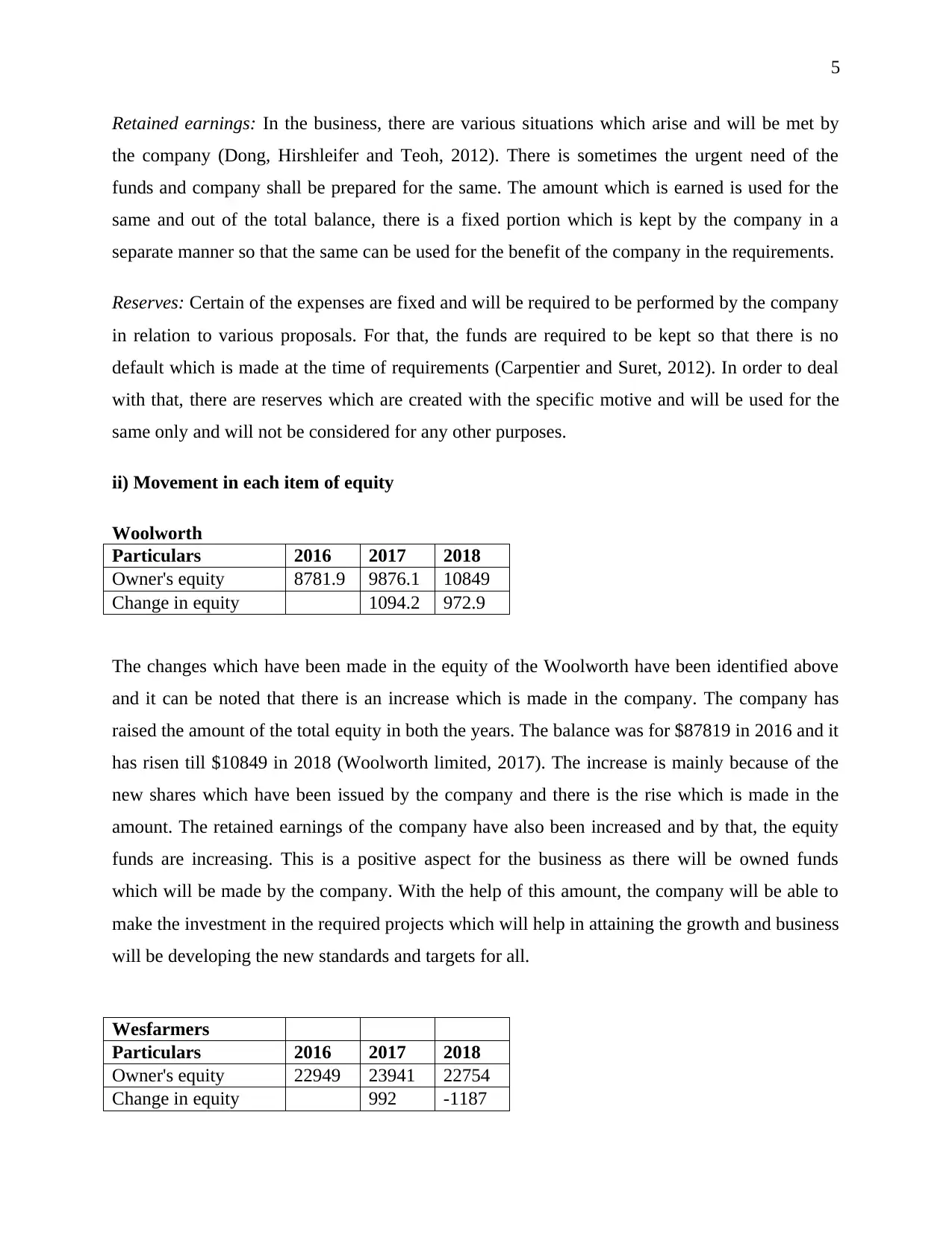

Retained earnings: In the business, there are various situations which arise and will be met by

the company (Dong, Hirshleifer and Teoh, 2012). There is sometimes the urgent need of the

funds and company shall be prepared for the same. The amount which is earned is used for the

same and out of the total balance, there is a fixed portion which is kept by the company in a

separate manner so that the same can be used for the benefit of the company in the requirements.

Reserves: Certain of the expenses are fixed and will be required to be performed by the company

in relation to various proposals. For that, the funds are required to be kept so that there is no

default which is made at the time of requirements (Carpentier and Suret, 2012). In order to deal

with that, there are reserves which are created with the specific motive and will be used for the

same only and will not be considered for any other purposes.

ii) Movement in each item of equity

Woolworth

Particulars 2016 2017 2018

Owner's equity 8781.9 9876.1 10849

Change in equity 1094.2 972.9

The changes which have been made in the equity of the Woolworth have been identified above

and it can be noted that there is an increase which is made in the company. The company has

raised the amount of the total equity in both the years. The balance was for $87819 in 2016 and it

has risen till $10849 in 2018 (Woolworth limited, 2017). The increase is mainly because of the

new shares which have been issued by the company and there is the rise which is made in the

amount. The retained earnings of the company have also been increased and by that, the equity

funds are increasing. This is a positive aspect for the business as there will be owned funds

which will be made by the company. With the help of this amount, the company will be able to

make the investment in the required projects which will help in attaining the growth and business

will be developing the new standards and targets for all.

Wesfarmers

Particulars 2016 2017 2018

Owner's equity 22949 23941 22754

Change in equity 992 -1187

Retained earnings: In the business, there are various situations which arise and will be met by

the company (Dong, Hirshleifer and Teoh, 2012). There is sometimes the urgent need of the

funds and company shall be prepared for the same. The amount which is earned is used for the

same and out of the total balance, there is a fixed portion which is kept by the company in a

separate manner so that the same can be used for the benefit of the company in the requirements.

Reserves: Certain of the expenses are fixed and will be required to be performed by the company

in relation to various proposals. For that, the funds are required to be kept so that there is no

default which is made at the time of requirements (Carpentier and Suret, 2012). In order to deal

with that, there are reserves which are created with the specific motive and will be used for the

same only and will not be considered for any other purposes.

ii) Movement in each item of equity

Woolworth

Particulars 2016 2017 2018

Owner's equity 8781.9 9876.1 10849

Change in equity 1094.2 972.9

The changes which have been made in the equity of the Woolworth have been identified above

and it can be noted that there is an increase which is made in the company. The company has

raised the amount of the total equity in both the years. The balance was for $87819 in 2016 and it

has risen till $10849 in 2018 (Woolworth limited, 2017). The increase is mainly because of the

new shares which have been issued by the company and there is the rise which is made in the

amount. The retained earnings of the company have also been increased and by that, the equity

funds are increasing. This is a positive aspect for the business as there will be owned funds

which will be made by the company. With the help of this amount, the company will be able to

make the investment in the required projects which will help in attaining the growth and business

will be developing the new standards and targets for all.

Wesfarmers

Particulars 2016 2017 2018

Owner's equity 22949 23941 22754

Change in equity 992 -1187

6

The changes have also been considered in the Wesfarmers which is also operating in the same

industry. There is an increase which is made from an amount of $22949 in 2016 to $23941 in

2017. This is the rise which is made because of the increase in the retained earnings and reserves

of the company. There is the need to maintain the same but the decline is faxed in the coming

year and balance declined to $22754 (Wesfarmers limited, 2017). This has taken place because

of the sudden decrease in the amount which is maintained as the retained earnings and the

company is suffering the overall decrease in equity because of the same.

iii) Items under the liability section

The liabilities are the debts of the company and they will be required to be paid off. They are

with the company to be used in the time of need but cannot be considered as the funds of the

company. The borrowings and other elements are covered in this and they have been identified

below for better understanding.

Borrowings: The main source which is covered is the borrowing in which an amount is taken as

the loan by the company from the lender. This will be used in the company for the development

but the company will be required to comply with the conditions which are specified in this

respect (Mande, Park and Son, 2012). There is the need to make the repayment as per the

amortization schedule which is made and there will be the additional interest which will also be

paid for the period the loan is undertaken.

Tax payable: There are various legal obligations which are to be met by the company. In that

most important is the payment of the tax which will be required to be made on the earnings

which are made by the company. There is the specified rate at which the same will be required to

pay on the due date which is specified. This will be also the liability of the company on the

income which is made.

Trade payable: There is the need to make the various purchases by the company and it is not

possible that all of them are made on cash. There are various purchases which are made on

credits and the amount which is there in relation to them will be paid after some time which is

allowed by the seller (Denis and McKeon, 2012). The other party is identified as the creditor to

whom the amount will be payable. This also provides the company with the liquidity and till

The changes have also been considered in the Wesfarmers which is also operating in the same

industry. There is an increase which is made from an amount of $22949 in 2016 to $23941 in

2017. This is the rise which is made because of the increase in the retained earnings and reserves

of the company. There is the need to maintain the same but the decline is faxed in the coming

year and balance declined to $22754 (Wesfarmers limited, 2017). This has taken place because

of the sudden decrease in the amount which is maintained as the retained earnings and the

company is suffering the overall decrease in equity because of the same.

iii) Items under the liability section

The liabilities are the debts of the company and they will be required to be paid off. They are

with the company to be used in the time of need but cannot be considered as the funds of the

company. The borrowings and other elements are covered in this and they have been identified

below for better understanding.

Borrowings: The main source which is covered is the borrowing in which an amount is taken as

the loan by the company from the lender. This will be used in the company for the development

but the company will be required to comply with the conditions which are specified in this

respect (Mande, Park and Son, 2012). There is the need to make the repayment as per the

amortization schedule which is made and there will be the additional interest which will also be

paid for the period the loan is undertaken.

Tax payable: There are various legal obligations which are to be met by the company. In that

most important is the payment of the tax which will be required to be made on the earnings

which are made by the company. There is the specified rate at which the same will be required to

pay on the due date which is specified. This will be also the liability of the company on the

income which is made.

Trade payable: There is the need to make the various purchases by the company and it is not

possible that all of them are made on cash. There are various purchases which are made on

credits and the amount which is there in relation to them will be paid after some time which is

allowed by the seller (Denis and McKeon, 2012). The other party is identified as the creditor to

whom the amount will be payable. This also provides the company with the liquidity and till

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

payment, the amount can be used for the benefit of the business.

Provisions: there are various amounts which will be received by the company in the coming

period and some level of the risk is involved in relation to them. The company is required to

consider the same in advance and for that, the provisions on the respective risk will be made.

These provide the company with the security and the amount will be safeguarded and will be

received in an adequate manner.

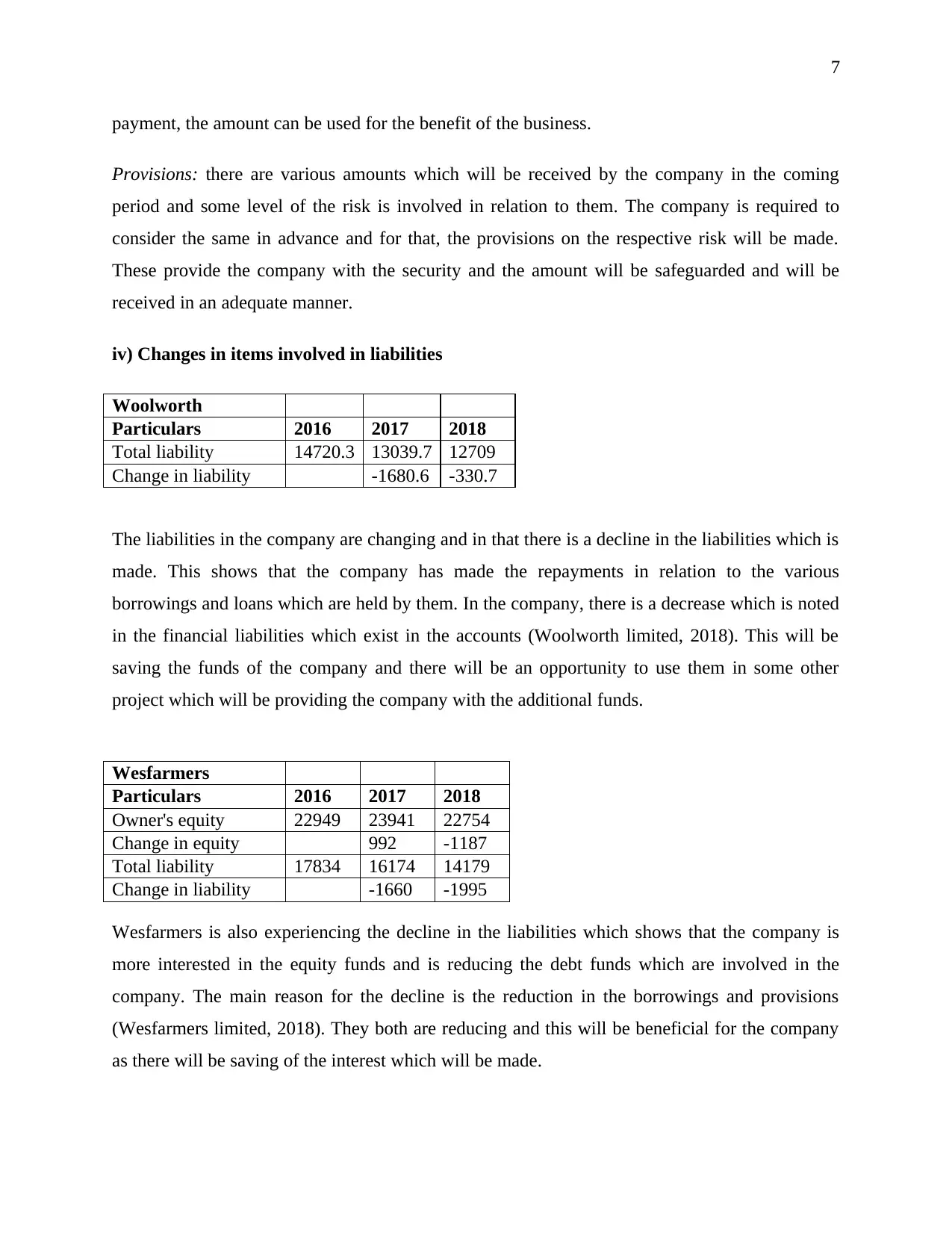

iv) Changes in items involved in liabilities

Woolworth

Particulars 2016 2017 2018

Total liability 14720.3 13039.7 12709

Change in liability -1680.6 -330.7

The liabilities in the company are changing and in that there is a decline in the liabilities which is

made. This shows that the company has made the repayments in relation to the various

borrowings and loans which are held by them. In the company, there is a decrease which is noted

in the financial liabilities which exist in the accounts (Woolworth limited, 2018). This will be

saving the funds of the company and there will be an opportunity to use them in some other

project which will be providing the company with the additional funds.

Wesfarmers

Particulars 2016 2017 2018

Owner's equity 22949 23941 22754

Change in equity 992 -1187

Total liability 17834 16174 14179

Change in liability -1660 -1995

Wesfarmers is also experiencing the decline in the liabilities which shows that the company is

more interested in the equity funds and is reducing the debt funds which are involved in the

company. The main reason for the decline is the reduction in the borrowings and provisions

(Wesfarmers limited, 2018). They both are reducing and this will be beneficial for the company

as there will be saving of the interest which will be made.

payment, the amount can be used for the benefit of the business.

Provisions: there are various amounts which will be received by the company in the coming

period and some level of the risk is involved in relation to them. The company is required to

consider the same in advance and for that, the provisions on the respective risk will be made.

These provide the company with the security and the amount will be safeguarded and will be

received in an adequate manner.

iv) Changes in items involved in liabilities

Woolworth

Particulars 2016 2017 2018

Total liability 14720.3 13039.7 12709

Change in liability -1680.6 -330.7

The liabilities in the company are changing and in that there is a decline in the liabilities which is

made. This shows that the company has made the repayments in relation to the various

borrowings and loans which are held by them. In the company, there is a decrease which is noted

in the financial liabilities which exist in the accounts (Woolworth limited, 2018). This will be

saving the funds of the company and there will be an opportunity to use them in some other

project which will be providing the company with the additional funds.

Wesfarmers

Particulars 2016 2017 2018

Owner's equity 22949 23941 22754

Change in equity 992 -1187

Total liability 17834 16174 14179

Change in liability -1660 -1995

Wesfarmers is also experiencing the decline in the liabilities which shows that the company is

more interested in the equity funds and is reducing the debt funds which are involved in the

company. The main reason for the decline is the reduction in the borrowings and provisions

(Wesfarmers limited, 2018). They both are reducing and this will be beneficial for the company

as there will be saving of the interest which will be made.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

v) Merits and demerits of the sources of funds

The collection of the funds is made with the help of the main funds which include the equity and

borrowings. In this, it is necessary that the merits and demerits which are there in relation to

them will have to be taken into account. The use of equity funds is a good option as there will be

no funds which will be required to be spent on them in an additional manner. They will be the

company’s amount and can be used by the company for any purpose and at any time (Yazdanfar

and Öhman, 2015). There will be no restriction on them but the amount which can be raised with

the help of them is limited. With the issuance of the shares, the ownership of the company is also

distributed and in order to maintain the same, there is a limit for the issue of shares.

The borrowings are also a good option as in that the amount which is required can be obtained

without any limit. There will be the availability of the funds in this method but the company will

be required to make the adequate payment of the interest in relation to the same. That will be the

additional cost and will be reducing the amount which is left with the company as profits. Due to

this, it is considered that there shall be more saving which shall be made by reducing the number

of borrowings.

Part B

Large and small proprietary company-related concept

The companies which are involved are required to be categorized in a specific manner and for

that, there are various concepts which are specified. There is the need to consider them and to

satisfy the conditions which are provided in this respect. There will be consideration of them and

that will help the company to be classified as the small or large proprietary company. The main

among them are as follows:

The number of the employees which are to be maintained is 100 or more in case of the period

from 1 July 2019 and for the period lying before this, there will be 50 or more employees

which will be hired.

The revenue which is required to be maintained should be $50 million or more and for the

period before 1 July 2019, this will be $25 million or more (ASIC, 2019).

The gross total assets of the company are required to be at the level of $25 million or more

v) Merits and demerits of the sources of funds

The collection of the funds is made with the help of the main funds which include the equity and

borrowings. In this, it is necessary that the merits and demerits which are there in relation to

them will have to be taken into account. The use of equity funds is a good option as there will be

no funds which will be required to be spent on them in an additional manner. They will be the

company’s amount and can be used by the company for any purpose and at any time (Yazdanfar

and Öhman, 2015). There will be no restriction on them but the amount which can be raised with

the help of them is limited. With the issuance of the shares, the ownership of the company is also

distributed and in order to maintain the same, there is a limit for the issue of shares.

The borrowings are also a good option as in that the amount which is required can be obtained

without any limit. There will be the availability of the funds in this method but the company will

be required to make the adequate payment of the interest in relation to the same. That will be the

additional cost and will be reducing the amount which is left with the company as profits. Due to

this, it is considered that there shall be more saving which shall be made by reducing the number

of borrowings.

Part B

Large and small proprietary company-related concept

The companies which are involved are required to be categorized in a specific manner and for

that, there are various concepts which are specified. There is the need to consider them and to

satisfy the conditions which are provided in this respect. There will be consideration of them and

that will help the company to be classified as the small or large proprietary company. The main

among them are as follows:

The number of the employees which are to be maintained is 100 or more in case of the period

from 1 July 2019 and for the period lying before this, there will be 50 or more employees

which will be hired.

The revenue which is required to be maintained should be $50 million or more and for the

period before 1 July 2019, this will be $25 million or more (ASIC, 2019).

The gross total assets of the company are required to be at the level of $25 million or more

9

after 1 July 209 and before that this will be $12.5 million or more.

All of the companies which will be fulfilling at least two of the conditions will be in the category

of the large proprietary company. If they are not completed then the company will be considered

to be the small proprietary company. There is the need for this classification so that other aspects

which are involved can also be made applicable in the required manner.

Compliance and reporting requirements

The classification of the companies will be made and then they will be lying under certain

conditions which need to be fulfilled. There are the laws which are applied and in them, certain

conditions are specified for the reporting and there is the need for compliance with them. This

will be requiring attainment of the proper knowledge about the same and then they will be used

in the company (Fu, Carson and Simnett, 2015). The main requirement is in relation to the

reporting and all of the entities which are considered as the large proprietary company will be

required to comply with the in a compulsory manner. They include the preparation of proper

accounts and reports. Once the reports are prepared they are required to be submitted within the

specified time limit. This is the condition which is to be fulfilled by all. With this, there will also

be the compulsory audit that will be considered and all of the accounts will have to be audited.

This will ensure that the preparation is made in an adequate manner and there will be proper

accounting is made.

The specified conditions are compulsory for the large companies and for the small companies it

will be beneficial if they comply with the same but it is not mandatory (Vanstraelen and

Schelleman, 2017). They can fulfill the conditions if they are interested as that will be in their

interest but if they are not willing then also it will not be an issue. All of the conditions which are

specified will have to be considered as per the classification.

Conclusion

The report has been made and in that there is the consideration of the various elements in relation

to the equity and liabilities for the Woolworth and Wesfarmers. In that, all of the required

information has been considered. The evaluation is made in an adequate manner and the change

which is taking place in the amounts that are involved have been covered. There are various

after 1 July 209 and before that this will be $12.5 million or more.

All of the companies which will be fulfilling at least two of the conditions will be in the category

of the large proprietary company. If they are not completed then the company will be considered

to be the small proprietary company. There is the need for this classification so that other aspects

which are involved can also be made applicable in the required manner.

Compliance and reporting requirements

The classification of the companies will be made and then they will be lying under certain

conditions which need to be fulfilled. There are the laws which are applied and in them, certain

conditions are specified for the reporting and there is the need for compliance with them. This

will be requiring attainment of the proper knowledge about the same and then they will be used

in the company (Fu, Carson and Simnett, 2015). The main requirement is in relation to the

reporting and all of the entities which are considered as the large proprietary company will be

required to comply with the in a compulsory manner. They include the preparation of proper

accounts and reports. Once the reports are prepared they are required to be submitted within the

specified time limit. This is the condition which is to be fulfilled by all. With this, there will also

be the compulsory audit that will be considered and all of the accounts will have to be audited.

This will ensure that the preparation is made in an adequate manner and there will be proper

accounting is made.

The specified conditions are compulsory for the large companies and for the small companies it

will be beneficial if they comply with the same but it is not mandatory (Vanstraelen and

Schelleman, 2017). They can fulfill the conditions if they are interested as that will be in their

interest but if they are not willing then also it will not be an issue. All of the conditions which are

specified will have to be considered as per the classification.

Conclusion

The report has been made and in that there is the consideration of the various elements in relation

to the equity and liabilities for the Woolworth and Wesfarmers. In that, all of the required

information has been considered. The evaluation is made in an adequate manner and the change

which is taking place in the amounts that are involved have been covered. There are various

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

reasons for the same and they have been taken into account. The identification of the reasons is

made and by that improvement will be made in the coming period. There is a consideration of

the benefits and disadvantages of various sources. The conditions which will help in proper

classification of the company as the large and small have been identified. The compliance

requirements have also been included and will be followed as per the requirements.

reasons for the same and they have been taken into account. The identification of the reasons is

made and by that improvement will be made in the coming period. There is a consideration of

the benefits and disadvantages of various sources. The conditions which will help in proper

classification of the company as the large and small have been identified. The compliance

requirements have also been included and will be followed as per the requirements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

References

ASIC. (2019) Are you a large or small proprietary company. [Online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-financial-

reports/are-you-a-large-or-small-proprietary-company/ [Accessed 24 September 2019]

Carpentier, C. and Suret, J.M. (2012) Entrepreneurial equity financing and securities regulation:

An empirical analysis. International Small Business Journal, 30(1), pp.41-64.

Denis, D.J. and McKeon, S.B. (2012) Debt financing and financial flexibility evidence from

proactive leverage increases. The Review of Financial Studies, 25(6), pp.1897-1929.

Dong, M., Hirshleifer, D. and Teoh, S.H. (2012) Overvalued equity and financing decisions. The

Review of Financial Studies, 25(12), pp.3645-3683.

Drover, W., Busenitz, L., Matusik, S., Townsend, D., Anglin, A. and Dushnitsky, G. (2017) A

review and road map of entrepreneurial equity financing research: venture capital, corporate

venture capital, angel investment, crowdfunding, and accelerators. Journal of

Management, 43(6), pp.1820-1853.

Fu, Y., Carson, E. and Simnett, R. (2015) Transparency report disclosure by Australian audit

firms and opportunities for research. Managerial Auditing Journal, 30(8/9), pp.870-910.

Mande, V., Park, Y.K. and Son, M. (2012) Equity or debt financing: does good corporate

governance matter?. Corporate Governance: An International Review, 20(2), pp.195-211.

Vanstraelen, A. and Schelleman, C. (2017) Auditing private companies: what do we

know?. Accounting and Business Research, 47(5), pp.565-584.

Wesfarmers limited. (2017) annual report. [Online] Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/j000901-ar17_interactive_final.pdf?

sfvrsn=4 [Accessed 24 September 2019]

Wesfarmers limited. (2018) annual report. [Online] Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-report.pdf?

References

ASIC. (2019) Are you a large or small proprietary company. [Online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-financial-

reports/are-you-a-large-or-small-proprietary-company/ [Accessed 24 September 2019]

Carpentier, C. and Suret, J.M. (2012) Entrepreneurial equity financing and securities regulation:

An empirical analysis. International Small Business Journal, 30(1), pp.41-64.

Denis, D.J. and McKeon, S.B. (2012) Debt financing and financial flexibility evidence from

proactive leverage increases. The Review of Financial Studies, 25(6), pp.1897-1929.

Dong, M., Hirshleifer, D. and Teoh, S.H. (2012) Overvalued equity and financing decisions. The

Review of Financial Studies, 25(12), pp.3645-3683.

Drover, W., Busenitz, L., Matusik, S., Townsend, D., Anglin, A. and Dushnitsky, G. (2017) A

review and road map of entrepreneurial equity financing research: venture capital, corporate

venture capital, angel investment, crowdfunding, and accelerators. Journal of

Management, 43(6), pp.1820-1853.

Fu, Y., Carson, E. and Simnett, R. (2015) Transparency report disclosure by Australian audit

firms and opportunities for research. Managerial Auditing Journal, 30(8/9), pp.870-910.

Mande, V., Park, Y.K. and Son, M. (2012) Equity or debt financing: does good corporate

governance matter?. Corporate Governance: An International Review, 20(2), pp.195-211.

Vanstraelen, A. and Schelleman, C. (2017) Auditing private companies: what do we

know?. Accounting and Business Research, 47(5), pp.565-584.

Wesfarmers limited. (2017) annual report. [Online] Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/j000901-ar17_interactive_final.pdf?

sfvrsn=4 [Accessed 24 September 2019]

Wesfarmers limited. (2018) annual report. [Online] Available at:

https://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-report.pdf?

12

sfvrsn=6 [Accessed 24 September 2019]

Woolworth limited. (2017) annual report. [Online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/188795_annual-report-2017.pdf [Accessed 24

September 2019]

Woolworth limited. (2018) annual report. [Online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf [Accessed 24

September 2019]

Yazdanfar, D. and Öhman, P. (2015) Debt financing and firm performance: an empirical study

based on Swedish data. The Journal of Risk Finance, 16(1), pp.102-118.

sfvrsn=6 [Accessed 24 September 2019]

Woolworth limited. (2017) annual report. [Online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/188795_annual-report-2017.pdf [Accessed 24

September 2019]

Woolworth limited. (2018) annual report. [Online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf [Accessed 24

September 2019]

Yazdanfar, D. and Öhman, P. (2015) Debt financing and firm performance: an empirical study

based on Swedish data. The Journal of Risk Finance, 16(1), pp.102-118.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.