Corporate Accounting and Reporting: Consolidation Report

VerifiedAdded on 2022/11/19

|6

|630

|100

Report

AI Summary

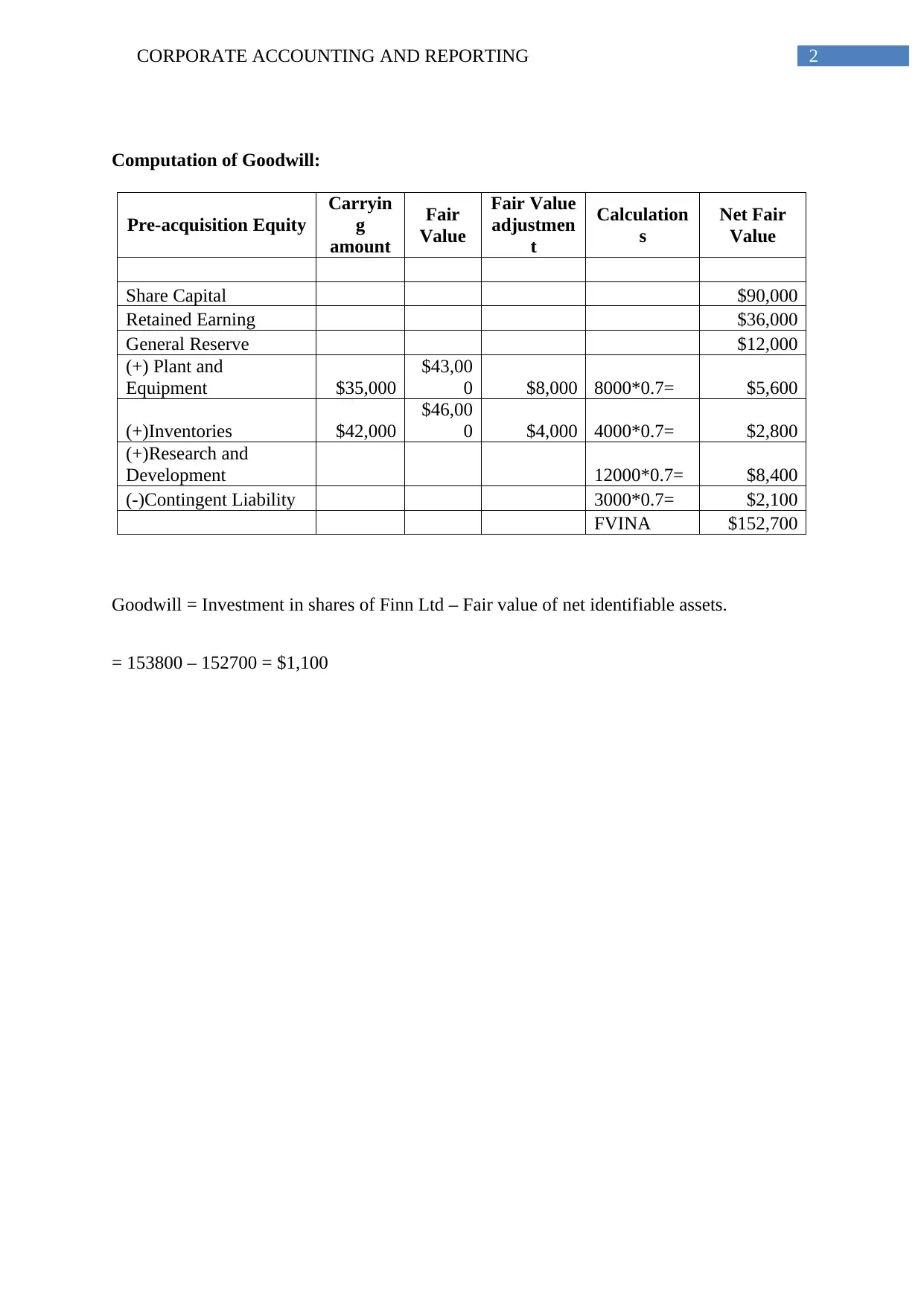

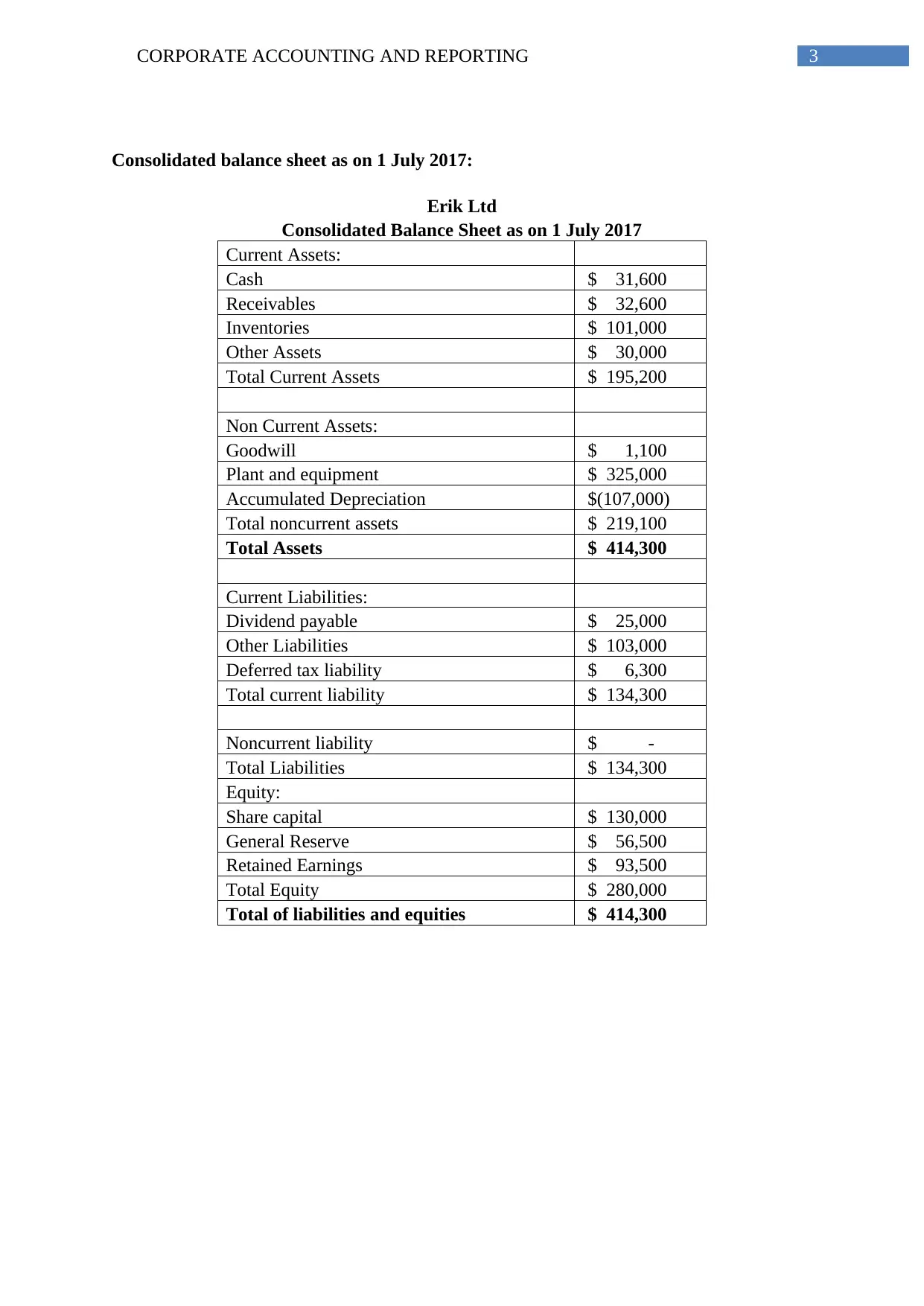

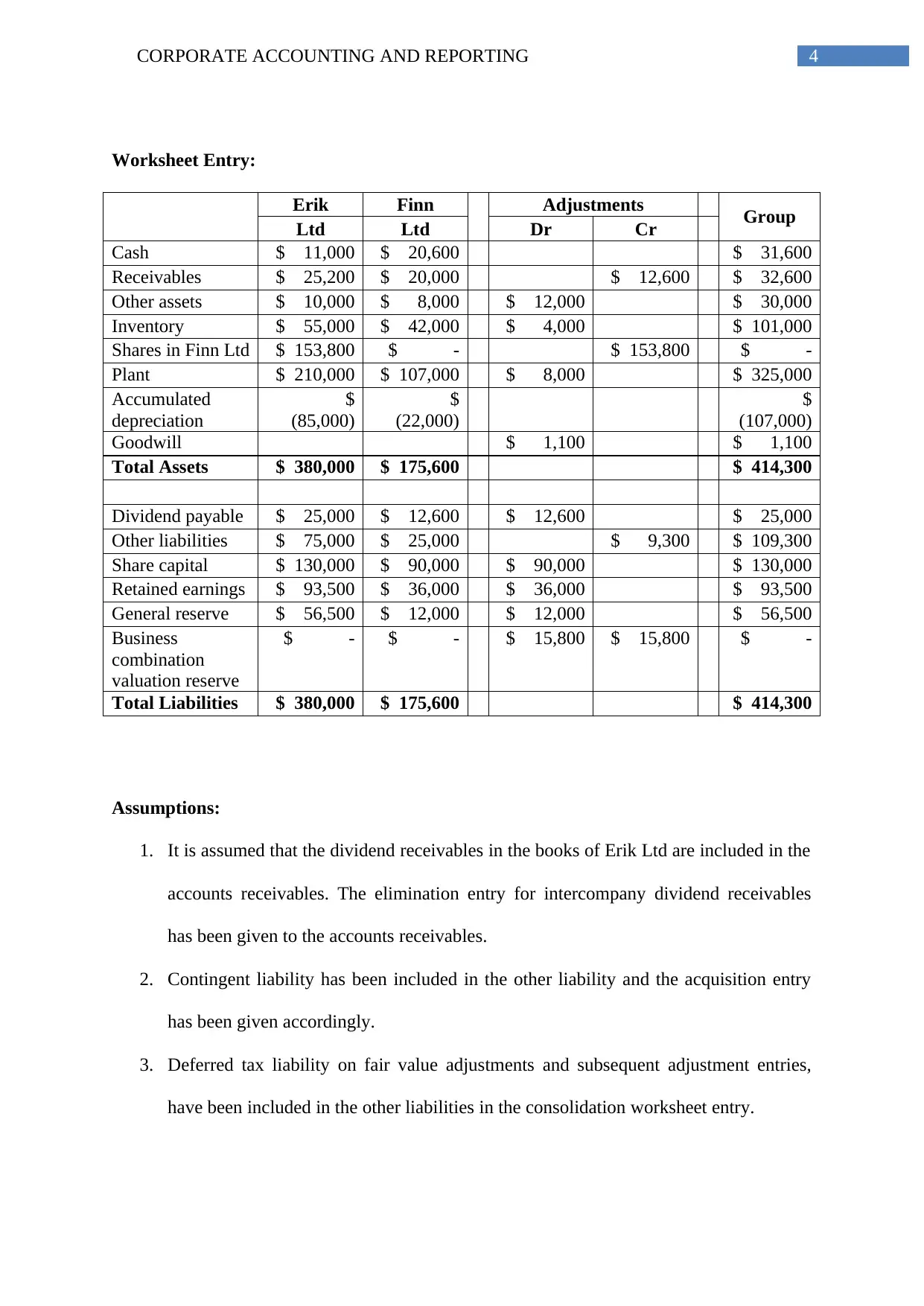

This report provides a detailed analysis of corporate accounting principles, specifically focusing on the computation of goodwill and the preparation of a consolidated balance sheet. The assignment involves calculating goodwill based on the fair value of net identifiable assets (FVINA) and the investment in shares. It includes a comprehensive worksheet entry demonstrating the consolidation process, adjustments for intercompany transactions, and the application of relevant accounting standards. The report also presents a consolidated balance sheet, reflecting the combined financial position of the parent and subsidiary company. Key assumptions, such as the treatment of dividend receivables and deferred tax liabilities, are clearly stated. The report concludes with a bibliography of relevant accounting literature, providing a strong foundation for the analysis and demonstrating a thorough understanding of the subject matter. This report is valuable for students studying corporate accounting as it provides a practical application of complex accounting concepts.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.