Corporate Accounting: Goodwill Measurement and Business Combination

VerifiedAdded on 2023/01/16

|10

|2233

|62

Report

AI Summary

This report delves into the intricacies of corporate accounting, focusing on the recognition and measurement of goodwill and gain amounts arising from business combinations, as per AASB-3/IFRS-3. The report is divided into two parts: the first part provides an essay on the principles of goodwill accounting and the second part presents a numerical analysis of the acquisition of Davis Ltd. by Alma Ltd. The analysis includes the calculation of net fair value, the determination of goodwill or gain, and the preparation of acquisition analysis and consolidation worksheet entries. The report explains the key aspects of AASB-3, including the definition of business combinations, the measurement of consideration transferred, the treatment of non-controlling interests, and the recognition of bargain purchases. The report also provides a detailed case study involving the acquisition of Davis Ltd., including the calculation of goodwill and the journal entries required to record the transaction. The report concludes with a summary of the key concepts and their practical applications in corporate accounting.

Corporate

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The term corporate accounting refers to thorough evaluation of key financial aspects of

accounting as well as farming of financial documents in the relevance of specific rules and

regulations specified by relevant governing body. Management staff and accounting personnel

both contributes in corporate accounting. Here considerable difference in ordinary accounting

and corporate accounting is that corporate accounting specifically deals with compliance of

accounting policies, standards and rules in public listed corporation not in respect of ordinary

firms. In Australia, International-Accounting Standards-Board (IASB) is principle body which

regulates the compliances of all the standards issued by it (Schaltegger, Etxeberria and Ortas,

2017).

The whole study is divided in two parts, wherein first part contains an essay on

acknowledgement and measuring process of goodwill and gain amount through deal acquisition

in event of business-combination as per AASB-3/IFRS-3. While second part consists of numeral

task to prepare acquisition analysis and consolidation worksheet entries in context of acquisition

of Davis Ltd by corporation Alma limited.

TASK

PART A

Recognition and measure of goodwill or gain amount from bargain purchase under business

combination:

AASB 3: Business Combination deals with the accounting practices to be followed inn

case of business combination. Core objective it is to enhance relevancy, reliableness, efficiency

and comparison of accountancy data which a organization give in annual financial statements

regarding event of business combination and respective outcome. This standard provides

guideline for effecting business concern collection event in books of both companies. Main issue

in business-combination is assessment of goodwill or gain due to business acquisition.

Provisions stated in this standard specifies the appropriate recognition of goodwill or gain step

wise and measurement criteria for assessing business goodwill (Bugeja and Loyeung, 2015).

This also determines amounts which are to be included in computation of goodwill/gain as well

as specific items to be excluded from computation.

The term corporate accounting refers to thorough evaluation of key financial aspects of

accounting as well as farming of financial documents in the relevance of specific rules and

regulations specified by relevant governing body. Management staff and accounting personnel

both contributes in corporate accounting. Here considerable difference in ordinary accounting

and corporate accounting is that corporate accounting specifically deals with compliance of

accounting policies, standards and rules in public listed corporation not in respect of ordinary

firms. In Australia, International-Accounting Standards-Board (IASB) is principle body which

regulates the compliances of all the standards issued by it (Schaltegger, Etxeberria and Ortas,

2017).

The whole study is divided in two parts, wherein first part contains an essay on

acknowledgement and measuring process of goodwill and gain amount through deal acquisition

in event of business-combination as per AASB-3/IFRS-3. While second part consists of numeral

task to prepare acquisition analysis and consolidation worksheet entries in context of acquisition

of Davis Ltd by corporation Alma limited.

TASK

PART A

Recognition and measure of goodwill or gain amount from bargain purchase under business

combination:

AASB 3: Business Combination deals with the accounting practices to be followed inn

case of business combination. Core objective it is to enhance relevancy, reliableness, efficiency

and comparison of accountancy data which a organization give in annual financial statements

regarding event of business combination and respective outcome. This standard provides

guideline for effecting business concern collection event in books of both companies. Main issue

in business-combination is assessment of goodwill or gain due to business acquisition.

Provisions stated in this standard specifies the appropriate recognition of goodwill or gain step

wise and measurement criteria for assessing business goodwill (Bugeja and Loyeung, 2015).

This also determines amounts which are to be included in computation of goodwill/gain as well

as specific items to be excluded from computation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per AASB-3, event of business acquisition is defined as contract, specific agreement

or financial event under which acquirer corporation acquires percentage/share in ownership or

full ownership in other corporation. Must requirement here is legal agreement and financial deal

between corporations wherein ownerships exchanged from one corporation to another

corporation. Provisions of this standard states that goodwill amount is measured as the difference

amount between:

(a) Aggregate amount of:

1. the sum of money in order to purchase the consideration that is needed to be paid

(normally at fair-value),

2. Figure of non-controlling interest or NCI (if any), and

3. Acquisition date present value are the figure which are related with acquirer's

antecedently holding the equity shares interest in other corporation (acquiree),

under process of business combination.

(b) Net amount of identifiable assets amount and amount of liabilities assumed as on the

date of acquisition.

The above points can be summarised in an equation, as follows:

Goodwill = Amount of

Consideration

transferred

+ non-controlling

interests figure

+ Previous held

equity interests

(Fair value)

- Net assets

recognised

If amount of difference from above measurement is negative figure, overall resulting gain

amount is bargain-purchase in term of profit or loss, that may incur in cases like forced seller

performing under compulsion. Although, before any amount of bargaining purchase-gain is

recognized in profit/loss, acquirer company must attempt a significant review for proper and

complete ascertain the actual value of assets and liabilities as well as all the measurements

effectively indicate considerations of provided information (Bepari, Rahman and Mollik, 2014).

According to the provisions of AASB 3, under a process of business combination

wherein acquirer corporation and acquiree corporation or any its former-owners) significantly

exchanges only their equity holding interests, fair value as on acquisition-date of the acquiree

corporation’s equity holding interests can be quite more faithfully assessable than fair value of

acquirer corporation's equity holding interests' fair value. Thereby, acquirer corporation shall

ascertain net amount of acquired goodwill on the basis of acquiree corporation'sfair-value as on

or financial event under which acquirer corporation acquires percentage/share in ownership or

full ownership in other corporation. Must requirement here is legal agreement and financial deal

between corporations wherein ownerships exchanged from one corporation to another

corporation. Provisions of this standard states that goodwill amount is measured as the difference

amount between:

(a) Aggregate amount of:

1. the sum of money in order to purchase the consideration that is needed to be paid

(normally at fair-value),

2. Figure of non-controlling interest or NCI (if any), and

3. Acquisition date present value are the figure which are related with acquirer's

antecedently holding the equity shares interest in other corporation (acquiree),

under process of business combination.

(b) Net amount of identifiable assets amount and amount of liabilities assumed as on the

date of acquisition.

The above points can be summarised in an equation, as follows:

Goodwill = Amount of

Consideration

transferred

+ non-controlling

interests figure

+ Previous held

equity interests

(Fair value)

- Net assets

recognised

If amount of difference from above measurement is negative figure, overall resulting gain

amount is bargain-purchase in term of profit or loss, that may incur in cases like forced seller

performing under compulsion. Although, before any amount of bargaining purchase-gain is

recognized in profit/loss, acquirer company must attempt a significant review for proper and

complete ascertain the actual value of assets and liabilities as well as all the measurements

effectively indicate considerations of provided information (Bepari, Rahman and Mollik, 2014).

According to the provisions of AASB 3, under a process of business combination

wherein acquirer corporation and acquiree corporation or any its former-owners) significantly

exchanges only their equity holding interests, fair value as on acquisition-date of the acquiree

corporation’s equity holding interests can be quite more faithfully assessable than fair value of

acquirer corporation's equity holding interests' fair value. Thereby, acquirer corporation shall

ascertain net amount of acquired goodwill on the basis of acquiree corporation'sfair-value as on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

date of the initial acquisition rather than fair value of equity holding interest transferred as at

acquisition date. For determining certain amount of acquired goodwill under a process business

combination where no significant amount of consideration transferred, acquirer corporation shall

apply acquirer corporation’s interest at fair value (as on acquisition-date) in acquiree corporation

in stead of actual value amount of circumstance movement as on acquiring time frame (Kabir

and Rahman, 2016).

Eventually an acquirer corporation make bargain purchase that is regarded as business

combination where aggregate amount of point (b) is greater than amount assessed in point (a)

[As discussed above]. In case such excess remains even after acquisition date then acquirer

corporation shall recognize assessed gain in P&L as on acquisition-date. Such amount of gain

will be provided to acquirer corporation.

Before identifying a profit on an acquisition bargain, acquirer corporation shall re-

evaluate whether it appropriately identified all obtained assets as well as all presumed liabilities,

and must identify any further specific assets or liabilities found in that analysis. The purchaser

must then check for all following processes for calculating the quantities that this Norm needs to

be recognized as on acquisition-date:

Identifiable acquired incomes/assets and liabilities/obligation assumed;

Any NCI in acquiree corporation

With respect to business combination done in several stages, acquirer corporation’s

formerly acquired equity holding interest in another corporation (acquiree), as well as

Net amount of purchase consideration transferred (Kabir, Rahman and Su, 2017).

Main aim of such review is ensuring that all the measurements adequately shown key

considerations of aggregate accessible information as on acquisition-date. The net consideration

acquired in business combination must be determined at faithful price, assessed as sum of the

equal consolidation-date amounts of the assets acquired by the purchaser, the obligations accrued

by acquirer corporation to acquiree corporation's former equity holding interests provided by

acquirer. The consideration exchanged may involve the acquirer corporation's assets or

obligations which have bearing sums that vary as on acquisition date from the reasonable values

(for instance, non-monetary assets or any business). The purchaser corporation shall, at purchase

date, re-evaluate the all acquired assets/liabilities assigned to their reasonable values and

recognize the resultant gains/losses in P&L if any.

acquisition date. For determining certain amount of acquired goodwill under a process business

combination where no significant amount of consideration transferred, acquirer corporation shall

apply acquirer corporation’s interest at fair value (as on acquisition-date) in acquiree corporation

in stead of actual value amount of circumstance movement as on acquiring time frame (Kabir

and Rahman, 2016).

Eventually an acquirer corporation make bargain purchase that is regarded as business

combination where aggregate amount of point (b) is greater than amount assessed in point (a)

[As discussed above]. In case such excess remains even after acquisition date then acquirer

corporation shall recognize assessed gain in P&L as on acquisition-date. Such amount of gain

will be provided to acquirer corporation.

Before identifying a profit on an acquisition bargain, acquirer corporation shall re-

evaluate whether it appropriately identified all obtained assets as well as all presumed liabilities,

and must identify any further specific assets or liabilities found in that analysis. The purchaser

must then check for all following processes for calculating the quantities that this Norm needs to

be recognized as on acquisition-date:

Identifiable acquired incomes/assets and liabilities/obligation assumed;

Any NCI in acquiree corporation

With respect to business combination done in several stages, acquirer corporation’s

formerly acquired equity holding interest in another corporation (acquiree), as well as

Net amount of purchase consideration transferred (Kabir, Rahman and Su, 2017).

Main aim of such review is ensuring that all the measurements adequately shown key

considerations of aggregate accessible information as on acquisition-date. The net consideration

acquired in business combination must be determined at faithful price, assessed as sum of the

equal consolidation-date amounts of the assets acquired by the purchaser, the obligations accrued

by acquirer corporation to acquiree corporation's former equity holding interests provided by

acquirer. The consideration exchanged may involve the acquirer corporation's assets or

obligations which have bearing sums that vary as on acquisition date from the reasonable values

(for instance, non-monetary assets or any business). The purchaser corporation shall, at purchase

date, re-evaluate the all acquired assets/liabilities assigned to their reasonable values and

recognize the resultant gains/losses in P&L if any.

Although, in some cases transferred assets/liabilities left within consolidated enterprise

after the entire business-combination (since assets/liabilities initially transferred to other

corporation acquiree instead of former-owners), while acquirer thus holds controlling of them. In

such circumstances, acquirer corporation shall assess all acquired assets/liabilities at respective

carrying figures just before acquisition-date and not recognize loss/gain on acquisition of

assets/liabilities it currently controlling both pre and post business combination (Su and Wells,

2018).

Any assets or liabilities arising from a contingent consideration scheme shall be

considered as part of acquirer's transition in return of the acquiree corporation. The purchaser

shall accept as component of compensation exchanged in return for the seller the acquisition-day

of contingent consideration at fair-value. The acquéreur shall, in accordance with the terms and

conditions of equity instrument and financial-liability in para11 of AASB-132 Financial

Instruments, categorize a duty to to make payment contingent consideration which satisfies

definition of financial instrument as financial liability or equity. Acquirer corporation shall, when

the conditions stipulated are satisfied, categorize as asset a right to go back the earlier transferred

payment. The guidelines on corresponding contingent consideration reporting are provided in

para 58 (d'Arcy and Tarca, 2018).

The purchaser should re-measure antecedently include equity-interest in purchased at fair

measure acquiring date, under business combination accomplished by phases and accept the

resultant benefit or lost, if any, by profit, loss or other comprehensive profits, if relevant. The

acquirer may have recorded adjustments in the valuation of its share in the acquired interest in

detailed profits during previous reporting periods. If so, it will be identifiable on same terms

element if the acquisition has been prepare, explicitly from the antecedently stake, of the sums

that were recognized in other full revenues (Su and Wells, 2018).

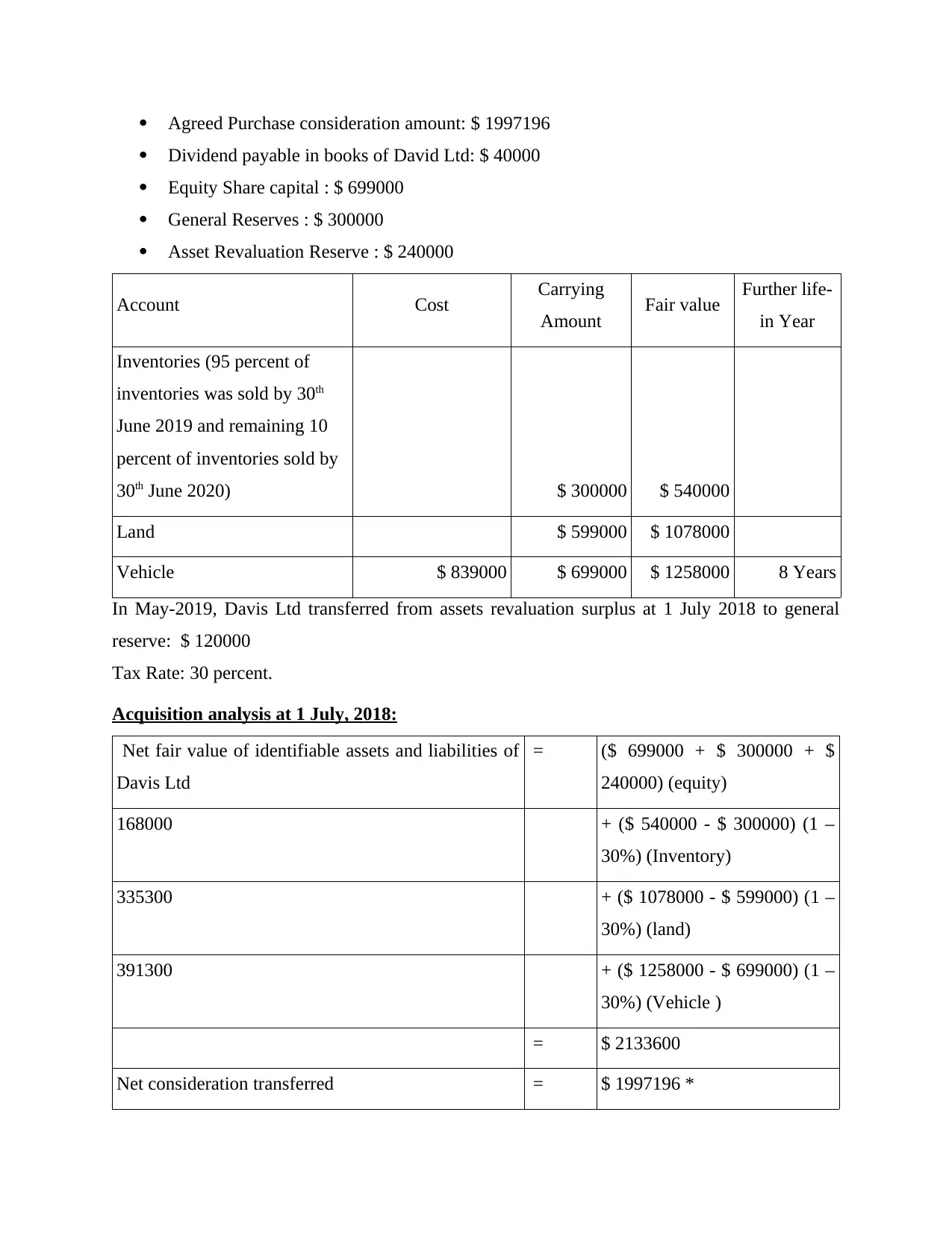

PART B

As per the analysis of given case study following facts has been identified related to

business combination in context of Alma Ltd and Davis Ltd, as follows:

Alma Ltd (Acquirer Corporation) - - - - - - - - - - - - - - - - →Davis Ltd (Target Corporation)

[Acquired all the assets]

Date of the Acquisition: 1-July, 2018

after the entire business-combination (since assets/liabilities initially transferred to other

corporation acquiree instead of former-owners), while acquirer thus holds controlling of them. In

such circumstances, acquirer corporation shall assess all acquired assets/liabilities at respective

carrying figures just before acquisition-date and not recognize loss/gain on acquisition of

assets/liabilities it currently controlling both pre and post business combination (Su and Wells,

2018).

Any assets or liabilities arising from a contingent consideration scheme shall be

considered as part of acquirer's transition in return of the acquiree corporation. The purchaser

shall accept as component of compensation exchanged in return for the seller the acquisition-day

of contingent consideration at fair-value. The acquéreur shall, in accordance with the terms and

conditions of equity instrument and financial-liability in para11 of AASB-132 Financial

Instruments, categorize a duty to to make payment contingent consideration which satisfies

definition of financial instrument as financial liability or equity. Acquirer corporation shall, when

the conditions stipulated are satisfied, categorize as asset a right to go back the earlier transferred

payment. The guidelines on corresponding contingent consideration reporting are provided in

para 58 (d'Arcy and Tarca, 2018).

The purchaser should re-measure antecedently include equity-interest in purchased at fair

measure acquiring date, under business combination accomplished by phases and accept the

resultant benefit or lost, if any, by profit, loss or other comprehensive profits, if relevant. The

acquirer may have recorded adjustments in the valuation of its share in the acquired interest in

detailed profits during previous reporting periods. If so, it will be identifiable on same terms

element if the acquisition has been prepare, explicitly from the antecedently stake, of the sums

that were recognized in other full revenues (Su and Wells, 2018).

PART B

As per the analysis of given case study following facts has been identified related to

business combination in context of Alma Ltd and Davis Ltd, as follows:

Alma Ltd (Acquirer Corporation) - - - - - - - - - - - - - - - - →Davis Ltd (Target Corporation)

[Acquired all the assets]

Date of the Acquisition: 1-July, 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Agreed Purchase consideration amount: $ 1997196

Dividend payable in books of David Ltd: $ 40000

Equity Share capital : $ 699000

General Reserves : $ 300000

Asset Revaluation Reserve : $ 240000

Account Cost Carrying

Amount Fair value Further life-

in Year

Inventories (95 percent of

inventories was sold by 30th

June 2019 and remaining 10

percent of inventories sold by

30th June 2020) $ 300000 $ 540000

Land $ 599000 $ 1078000

Vehicle $ 839000 $ 699000 $ 1258000 8 Years

In May-2019, Davis Ltd transferred from assets revaluation surplus at 1 July 2018 to general

reserve: $ 120000

Tax Rate: 30 percent.

Acquisition analysis at 1 July, 2018:

Net fair value of identifiable assets and liabilities of

Davis Ltd

= ($ 699000 + $ 300000 + $

240000) (equity)

168000 + ($ 540000 - $ 300000) (1 –

30%) (Inventory)

335300 + ($ 1078000 - $ 599000) (1 –

30%) (land)

391300 + ($ 1258000 - $ 699000) (1 –

30%) (Vehicle )

= $ 2133600

Net consideration transferred = $ 1997196 *

Dividend payable in books of David Ltd: $ 40000

Equity Share capital : $ 699000

General Reserves : $ 300000

Asset Revaluation Reserve : $ 240000

Account Cost Carrying

Amount Fair value Further life-

in Year

Inventories (95 percent of

inventories was sold by 30th

June 2019 and remaining 10

percent of inventories sold by

30th June 2020) $ 300000 $ 540000

Land $ 599000 $ 1078000

Vehicle $ 839000 $ 699000 $ 1258000 8 Years

In May-2019, Davis Ltd transferred from assets revaluation surplus at 1 July 2018 to general

reserve: $ 120000

Tax Rate: 30 percent.

Acquisition analysis at 1 July, 2018:

Net fair value of identifiable assets and liabilities of

Davis Ltd

= ($ 699000 + $ 300000 + $

240000) (equity)

168000 + ($ 540000 - $ 300000) (1 –

30%) (Inventory)

335300 + ($ 1078000 - $ 599000) (1 –

30%) (land)

391300 + ($ 1258000 - $ 699000) (1 –

30%) (Vehicle )

= $ 2133600

Net consideration transferred = $ 1997196 *

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

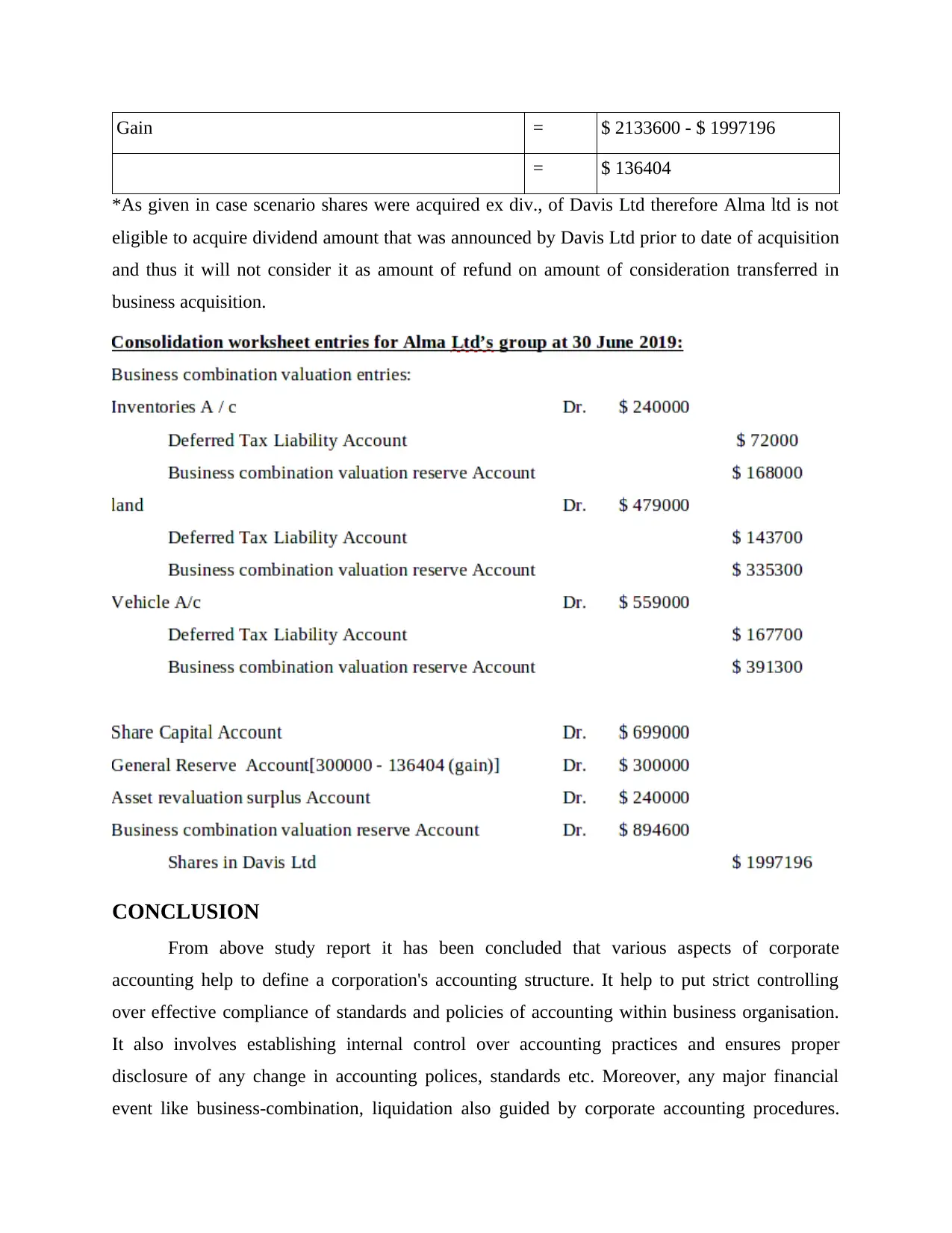

Gain = $ 2133600 - $ 1997196

= $ 136404

*As given in case scenario shares were acquired ex div., of Davis Ltd therefore Alma ltd is not

eligible to acquire dividend amount that was announced by Davis Ltd prior to date of acquisition

and thus it will not consider it as amount of refund on amount of consideration transferred in

business acquisition.

CONCLUSION

From above study report it has been concluded that various aspects of corporate

accounting help to define a corporation's accounting structure. It help to put strict controlling

over effective compliance of standards and policies of accounting within business organisation.

It also involves establishing internal control over accounting practices and ensures proper

disclosure of any change in accounting polices, standards etc. Moreover, any major financial

event like business-combination, liquidation also guided by corporate accounting procedures.

= $ 136404

*As given in case scenario shares were acquired ex div., of Davis Ltd therefore Alma ltd is not

eligible to acquire dividend amount that was announced by Davis Ltd prior to date of acquisition

and thus it will not consider it as amount of refund on amount of consideration transferred in

business acquisition.

CONCLUSION

From above study report it has been concluded that various aspects of corporate

accounting help to define a corporation's accounting structure. It help to put strict controlling

over effective compliance of standards and policies of accounting within business organisation.

It also involves establishing internal control over accounting practices and ensures proper

disclosure of any change in accounting polices, standards etc. Moreover, any major financial

event like business-combination, liquidation also guided by corporate accounting procedures.

Management in listed company coordinate with accounting staff to ensure the effective

compliance of adopted accounting standards and policies.

compliance of adopted accounting standards and policies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development. 25(2),

pp. 113-122.

Bugeja, M. and Loyeung, A., 2015. What drives the allocation of the purchase price to

goodwill?. Journal of Contemporary Accounting & Economics. 11(3). pp. 245-261.

Bepari, M.K., Rahman, S.F. and Mollik, A.T., 2014. Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial

crisis and other firm characteristics. Journal of Accounting and Organizational

Change. 10(1). pp. 116-149.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics. 12(3). pp. 290-308.

Kabir, H., Rahman, A. and Su, L., 2017. The association between goodwill impairment loss and

goodwill impairment test-related disclosures in Australia. In 8th Conference on

Financial Markets and Corporate Governance (FMCG).

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting

Research Journal.

d'Arcy, A. and Tarca, A., 2018. Reviewing IFRS goodwill accounting research: Implementation

effects and cross-country differences. The International Journal of Accounting, 53(3).

pp. 203-226.

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting

Research Journal.

Books and Journals:

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development. 25(2),

pp. 113-122.

Bugeja, M. and Loyeung, A., 2015. What drives the allocation of the purchase price to

goodwill?. Journal of Contemporary Accounting & Economics. 11(3). pp. 245-261.

Bepari, M.K., Rahman, S.F. and Mollik, A.T., 2014. Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial

crisis and other firm characteristics. Journal of Accounting and Organizational

Change. 10(1). pp. 116-149.

Kabir, H. and Rahman, A., 2016. The role of corporate governance in accounting discretion

under IFRS: Goodwill impairment in Australia. Journal of Contemporary Accounting &

Economics. 12(3). pp. 290-308.

Kabir, H., Rahman, A. and Su, L., 2017. The association between goodwill impairment loss and

goodwill impairment test-related disclosures in Australia. In 8th Conference on

Financial Markets and Corporate Governance (FMCG).

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting

Research Journal.

d'Arcy, A. and Tarca, A., 2018. Reviewing IFRS goodwill accounting research: Implementation

effects and cross-country differences. The International Journal of Accounting, 53(3).

pp. 203-226.

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting

Research Journal.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.