Corporate Accounting: A Financial Analysis of Insurance Australia

VerifiedAdded on 2024/05/14

|13

|2829

|300

Report

AI Summary

This report provides a detailed analysis of the corporate accounting practices of Insurance Australia Group Limited (IAG), an ASX-listed public company. It focuses on IAG's cash flow statement, examining operating, investing, and financing activities over three years, revealing instability across these categories. The analysis extends to the statement of other comprehensive income, dissecting items such as net movements in foreign currency translation reserves and re-measurements of defined benefit plans, explaining their exclusion from the profit and loss statement. Furthermore, the report investigates IAG's corporate income tax accounting, comparing the reported tax expense with the expected rate and exploring deferred tax assets reported on the balance sheet. This thorough evaluation offers insights into IAG's financial strategies and accounting methodologies. Desklib provides access to similar solved assignments and resources for students.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

1. CASH FLOWS STATEMENT...................................................................................................3

2. OTHER COMPREHENSIVE INCOME STATEMENT............................................................6

3. ACCOUNTING FOR CROPORATE INCOME TAX...............................................................8

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2

Introduction......................................................................................................................................3

1. CASH FLOWS STATEMENT...................................................................................................3

2. OTHER COMPREHENSIVE INCOME STATEMENT............................................................6

3. ACCOUNTING FOR CROPORATE INCOME TAX...............................................................8

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2

Introduction

The corporate accounting done in a company can be understood in the easiest way from the

evaluation and analysis of the accounting treatments of a company and its financial statements.

This report is a discussion about the Insurance Australia Group Limited. The Insurance Australia

Group Limited is an ASX listed public company operating in different areas around the globe

such as Australia, Asia and New Zealand. The report will be conducting an in-depth analysis of

the cash flows statement of the company during the past three years along with discussing about

the details of the statement of other compressive income. A discussion has also been made about

how Insurance Australia Group Limited accounts for corporate taxes.

3

The corporate accounting done in a company can be understood in the easiest way from the

evaluation and analysis of the accounting treatments of a company and its financial statements.

This report is a discussion about the Insurance Australia Group Limited. The Insurance Australia

Group Limited is an ASX listed public company operating in different areas around the globe

such as Australia, Asia and New Zealand. The report will be conducting an in-depth analysis of

the cash flows statement of the company during the past three years along with discussing about

the details of the statement of other compressive income. A discussion has also been made about

how Insurance Australia Group Limited accounts for corporate taxes.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

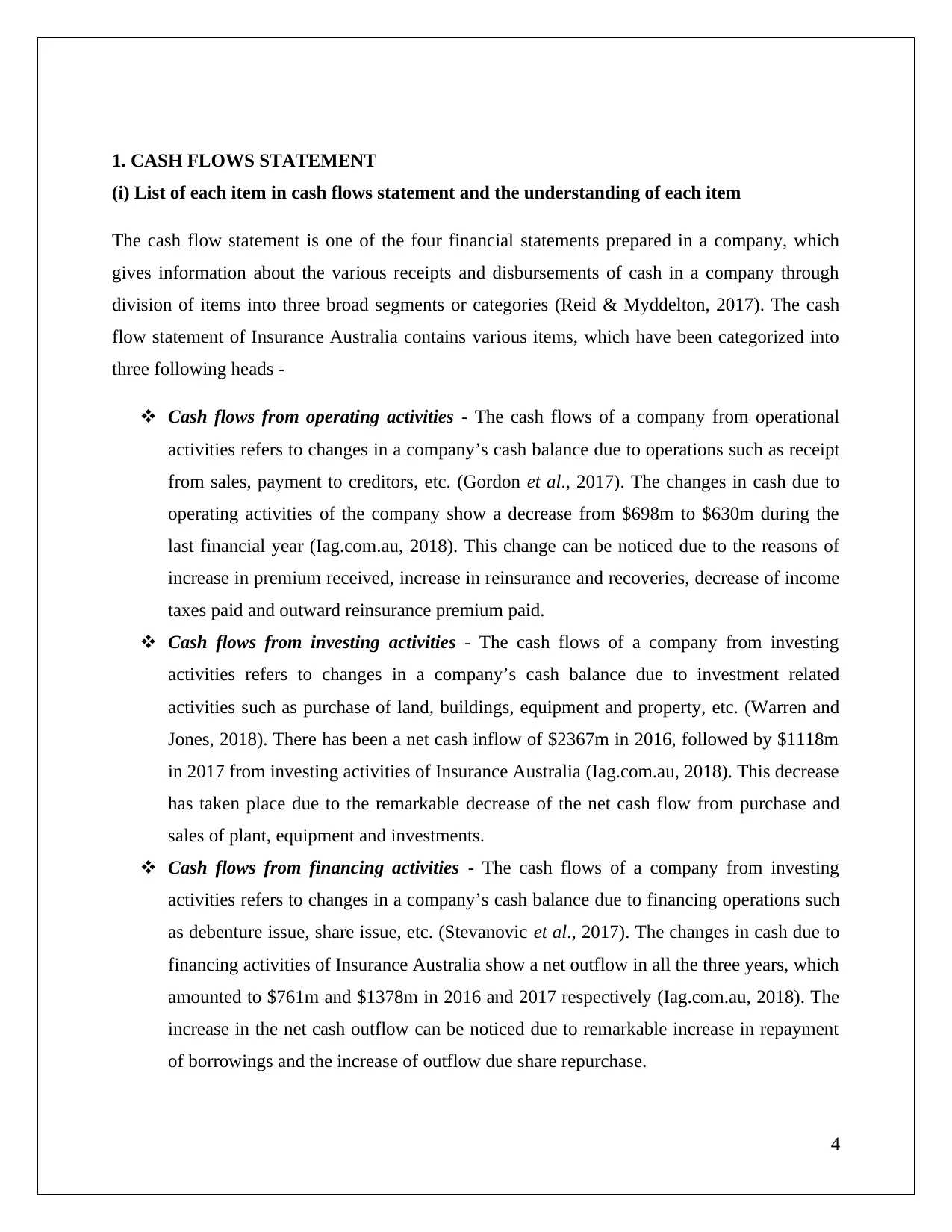

1. CASH FLOWS STATEMENT

(i) List of each item in cash flows statement and the understanding of each item

The cash flow statement is one of the four financial statements prepared in a company, which

gives information about the various receipts and disbursements of cash in a company through

division of items into three broad segments or categories (Reid & Myddelton, 2017). The cash

flow statement of Insurance Australia contains various items, which have been categorized into

three following heads -

Cash flows from operating activities - The cash flows of a company from operational

activities refers to changes in a company’s cash balance due to operations such as receipt

from sales, payment to creditors, etc. (Gordon et al., 2017). The changes in cash due to

operating activities of the company show a decrease from $698m to $630m during the

last financial year (Iag.com.au, 2018). This change can be noticed due to the reasons of

increase in premium received, increase in reinsurance and recoveries, decrease of income

taxes paid and outward reinsurance premium paid.

Cash flows from investing activities - The cash flows of a company from investing

activities refers to changes in a company’s cash balance due to investment related

activities such as purchase of land, buildings, equipment and property, etc. (Warren and

Jones, 2018). There has been a net cash inflow of $2367m in 2016, followed by $1118m

in 2017 from investing activities of Insurance Australia (Iag.com.au, 2018). This decrease

has taken place due to the remarkable decrease of the net cash flow from purchase and

sales of plant, equipment and investments.

Cash flows from financing activities - The cash flows of a company from investing

activities refers to changes in a company’s cash balance due to financing operations such

as debenture issue, share issue, etc. (Stevanovic et al., 2017). The changes in cash due to

financing activities of Insurance Australia show a net outflow in all the three years, which

amounted to $761m and $1378m in 2016 and 2017 respectively (Iag.com.au, 2018). The

increase in the net cash outflow can be noticed due to remarkable increase in repayment

of borrowings and the increase of outflow due share repurchase.

4

(i) List of each item in cash flows statement and the understanding of each item

The cash flow statement is one of the four financial statements prepared in a company, which

gives information about the various receipts and disbursements of cash in a company through

division of items into three broad segments or categories (Reid & Myddelton, 2017). The cash

flow statement of Insurance Australia contains various items, which have been categorized into

three following heads -

Cash flows from operating activities - The cash flows of a company from operational

activities refers to changes in a company’s cash balance due to operations such as receipt

from sales, payment to creditors, etc. (Gordon et al., 2017). The changes in cash due to

operating activities of the company show a decrease from $698m to $630m during the

last financial year (Iag.com.au, 2018). This change can be noticed due to the reasons of

increase in premium received, increase in reinsurance and recoveries, decrease of income

taxes paid and outward reinsurance premium paid.

Cash flows from investing activities - The cash flows of a company from investing

activities refers to changes in a company’s cash balance due to investment related

activities such as purchase of land, buildings, equipment and property, etc. (Warren and

Jones, 2018). There has been a net cash inflow of $2367m in 2016, followed by $1118m

in 2017 from investing activities of Insurance Australia (Iag.com.au, 2018). This decrease

has taken place due to the remarkable decrease of the net cash flow from purchase and

sales of plant, equipment and investments.

Cash flows from financing activities - The cash flows of a company from investing

activities refers to changes in a company’s cash balance due to financing operations such

as debenture issue, share issue, etc. (Stevanovic et al., 2017). The changes in cash due to

financing activities of Insurance Australia show a net outflow in all the three years, which

amounted to $761m and $1378m in 2016 and 2017 respectively (Iag.com.au, 2018). The

increase in the net cash outflow can be noticed due to remarkable increase in repayment

of borrowings and the increase of outflow due share repurchase.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

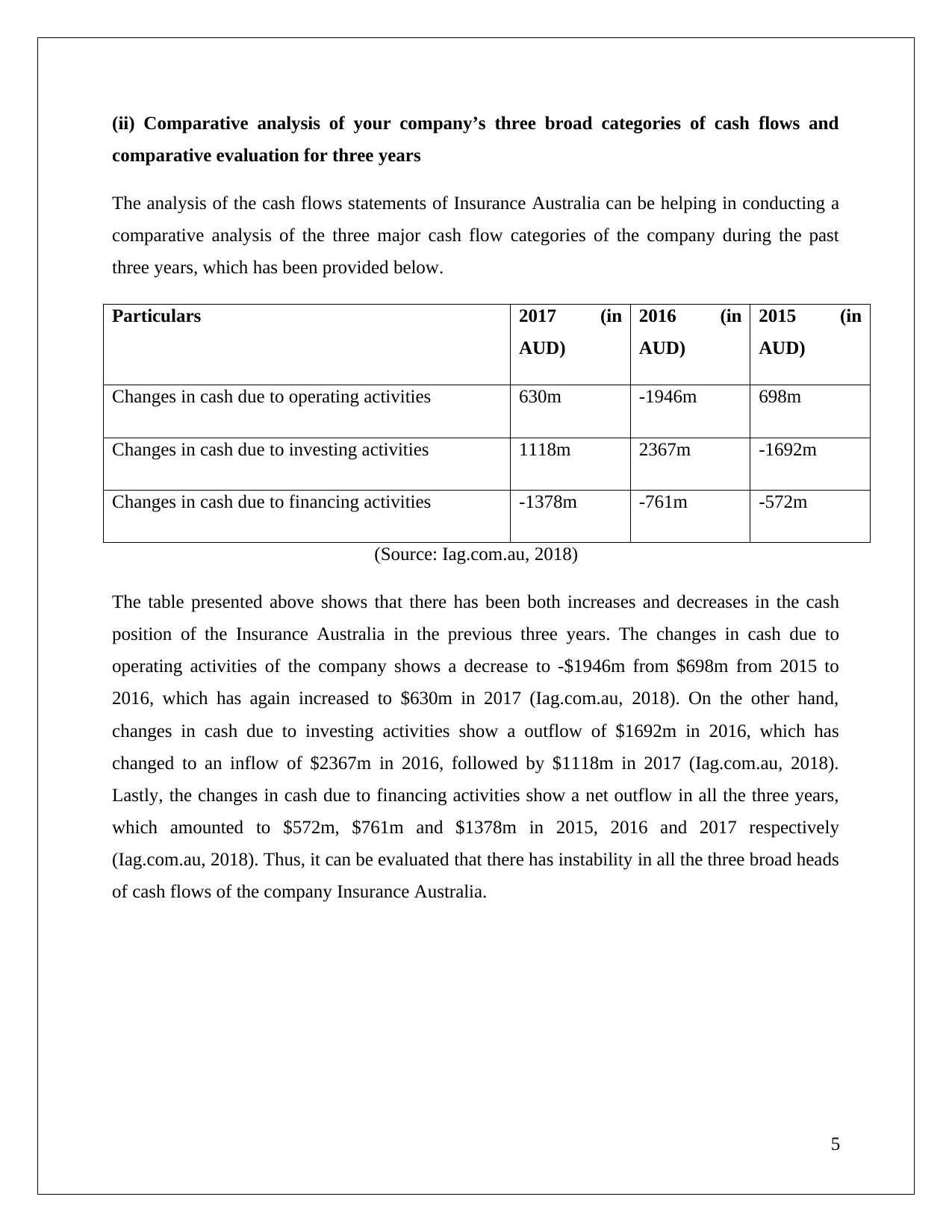

(ii) Comparative analysis of your company’s three broad categories of cash flows and

comparative evaluation for three years

The analysis of the cash flows statements of Insurance Australia can be helping in conducting a

comparative analysis of the three major cash flow categories of the company during the past

three years, which has been provided below.

Particulars 2017 (in

AUD)

2016 (in

AUD)

2015 (in

AUD)

Changes in cash due to operating activities 630m -1946m 698m

Changes in cash due to investing activities 1118m 2367m -1692m

Changes in cash due to financing activities -1378m -761m -572m

(Source: Iag.com.au, 2018)

The table presented above shows that there has been both increases and decreases in the cash

position of the Insurance Australia in the previous three years. The changes in cash due to

operating activities of the company shows a decrease to -$1946m from $698m from 2015 to

2016, which has again increased to $630m in 2017 (Iag.com.au, 2018). On the other hand,

changes in cash due to investing activities show a outflow of $1692m in 2016, which has

changed to an inflow of $2367m in 2016, followed by $1118m in 2017 (Iag.com.au, 2018).

Lastly, the changes in cash due to financing activities show a net outflow in all the three years,

which amounted to $572m, $761m and $1378m in 2015, 2016 and 2017 respectively

(Iag.com.au, 2018). Thus, it can be evaluated that there has instability in all the three broad heads

of cash flows of the company Insurance Australia.

5

comparative evaluation for three years

The analysis of the cash flows statements of Insurance Australia can be helping in conducting a

comparative analysis of the three major cash flow categories of the company during the past

three years, which has been provided below.

Particulars 2017 (in

AUD)

2016 (in

AUD)

2015 (in

AUD)

Changes in cash due to operating activities 630m -1946m 698m

Changes in cash due to investing activities 1118m 2367m -1692m

Changes in cash due to financing activities -1378m -761m -572m

(Source: Iag.com.au, 2018)

The table presented above shows that there has been both increases and decreases in the cash

position of the Insurance Australia in the previous three years. The changes in cash due to

operating activities of the company shows a decrease to -$1946m from $698m from 2015 to

2016, which has again increased to $630m in 2017 (Iag.com.au, 2018). On the other hand,

changes in cash due to investing activities show a outflow of $1692m in 2016, which has

changed to an inflow of $2367m in 2016, followed by $1118m in 2017 (Iag.com.au, 2018).

Lastly, the changes in cash due to financing activities show a net outflow in all the three years,

which amounted to $572m, $761m and $1378m in 2015, 2016 and 2017 respectively

(Iag.com.au, 2018). Thus, it can be evaluated that there has instability in all the three broad heads

of cash flows of the company Insurance Australia.

5

2. OTHER COMPREHENSIVE INCOME STATEMENT

(iii) Items that have been reported in the other comprehensive income statement

The other comprehensive income statement refers to a financial statement of a company, which

is prepared in the company in order to record the income that a company earns from the sources

of income, which are not generated from the normal business operations (Mechelli & Cimini,

2014). The analysis of the other income statement of Insurance Australia shows that there are

only three items included as other income of the company, which are as follows -

Net movements in foreign the reserves of currency translation

Re-measurement of the defined benefit plans

Other comprehensive income

All these three items are inclusive of taxes or net of taxes (Iag.com.au, 2018).

(iv) Understanding of each item reported in the other comprehensive income statement

The analysis of the other comprehensive income statement of Insurance Australia indicates three

items, the understanding of which has been provided in the points stated below -

The item “net movements in the foreign currency translation reserve, net of tax” refers to

the differences that take place due to the dissimilarity of exchange rates in the translation

of volume of units from one currency to the other. This item in the other income

statement of Insurance Australia amounted to $65 million in 2016, which has reduced to

-$16 million in 2017 (Iag.com.au, 2018).

Another item in Insurance Australia’s other income statement is the “re-measurement of

the defined benefit plans”. This item is nothing but the re-measurements carried out over

the net defined benefit asset or liability, comprising of actuarial losses or gains. This

item had a negative of $32 million in 2017, which can be noticed to changed to a

positive figure of $25 million in 2017 (Iag.com.au, 2018).

The last item in Insurance Australia’s other income statement is the other comprehensive

income, which is the figure of the net income earned in a company from various other

sources apart from the normal business operations. This item in the other income

6

(iii) Items that have been reported in the other comprehensive income statement

The other comprehensive income statement refers to a financial statement of a company, which

is prepared in the company in order to record the income that a company earns from the sources

of income, which are not generated from the normal business operations (Mechelli & Cimini,

2014). The analysis of the other income statement of Insurance Australia shows that there are

only three items included as other income of the company, which are as follows -

Net movements in foreign the reserves of currency translation

Re-measurement of the defined benefit plans

Other comprehensive income

All these three items are inclusive of taxes or net of taxes (Iag.com.au, 2018).

(iv) Understanding of each item reported in the other comprehensive income statement

The analysis of the other comprehensive income statement of Insurance Australia indicates three

items, the understanding of which has been provided in the points stated below -

The item “net movements in the foreign currency translation reserve, net of tax” refers to

the differences that take place due to the dissimilarity of exchange rates in the translation

of volume of units from one currency to the other. This item in the other income

statement of Insurance Australia amounted to $65 million in 2016, which has reduced to

-$16 million in 2017 (Iag.com.au, 2018).

Another item in Insurance Australia’s other income statement is the “re-measurement of

the defined benefit plans”. This item is nothing but the re-measurements carried out over

the net defined benefit asset or liability, comprising of actuarial losses or gains. This

item had a negative of $32 million in 2017, which can be noticed to changed to a

positive figure of $25 million in 2017 (Iag.com.au, 2018).

The last item in Insurance Australia’s other income statement is the other comprehensive

income, which is the figure of the net income earned in a company from various other

sources apart from the normal business operations. This item in the other income

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statement of the company amounted to $33 million in 2016, which has reduced to $9

million during 2017 (Iag.com.au, 2018).

(v) Why these items have not been reported in Profit and Loss Statement / Income

statement

The statement of other income accounts for the recording of those expenses and income of a

company, which are incurred and earned from any kind of operation other than the ones that are

the normal business operations (Nejad & Ahmad, 2017). These items, however, cannot be

mentioned in the income statement of a company. They are included in the other income

statement of a company, as they have an impact over the overall earnings of a business. The

reason for which the items such as net movements in the foreign currency, re-measurement of the

defined benefit, etc. are not mentioned in Insurance Australia’s income statement is that these

items do not have an impact over the net income after taxes of the company. These items also do

not affect the retained profit in the company. Therefore, as there is no impact on either of these

two factors, these items are excluded from the income statement.

7

million during 2017 (Iag.com.au, 2018).

(v) Why these items have not been reported in Profit and Loss Statement / Income

statement

The statement of other income accounts for the recording of those expenses and income of a

company, which are incurred and earned from any kind of operation other than the ones that are

the normal business operations (Nejad & Ahmad, 2017). These items, however, cannot be

mentioned in the income statement of a company. They are included in the other income

statement of a company, as they have an impact over the overall earnings of a business. The

reason for which the items such as net movements in the foreign currency, re-measurement of the

defined benefit, etc. are not mentioned in Insurance Australia’s income statement is that these

items do not have an impact over the net income after taxes of the company. These items also do

not affect the retained profit in the company. Therefore, as there is no impact on either of these

two factors, these items are excluded from the income statement.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. ACCOUNTING FOR CROPORATE INCOME TAX

(vi) Firm’s tax expense in its latest financial statements

Income tax expenses can be referred to as the expense or the amount that a firm pays to the

government of the country in which it operates and is recorded under the income statement of

every firm (Lee et al., 2017). The tax expense of Insurance Australia, as recorded in the

company’s income statement, amounts to $329 million during the past accounting year 2017

(Iag.com.au, 2018). The latest financial statements of the company Insurance Australia Group

Limited also show that the income tax expense of the company had amounted to $218 million

during the year 2016 (Iag.com.au, 2018).

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm

As per the rate of tax, which is mandatory to be paid to the government of all the public limited

companies listed under the ASX, is 30% (Burkhauser, Hahn & Wilkins, 2015). The company

Insurance Australia Group Limited is also liable to be paying income tax on the accounting profit

earned by it at the rate of 30%. However, if the figure of the tax expense of Insurance Australia

Group’s latest financial reports is considered, it can be reviewed that the tax expense stated in the

income statement of the company is higher than the taxable amount if the tax rate is 30%

(Iag.com.au, 2018). This shows that the figure of tax expense of Insurance Australia Group

Limited is not the same as the tax rate times of its accounting income.

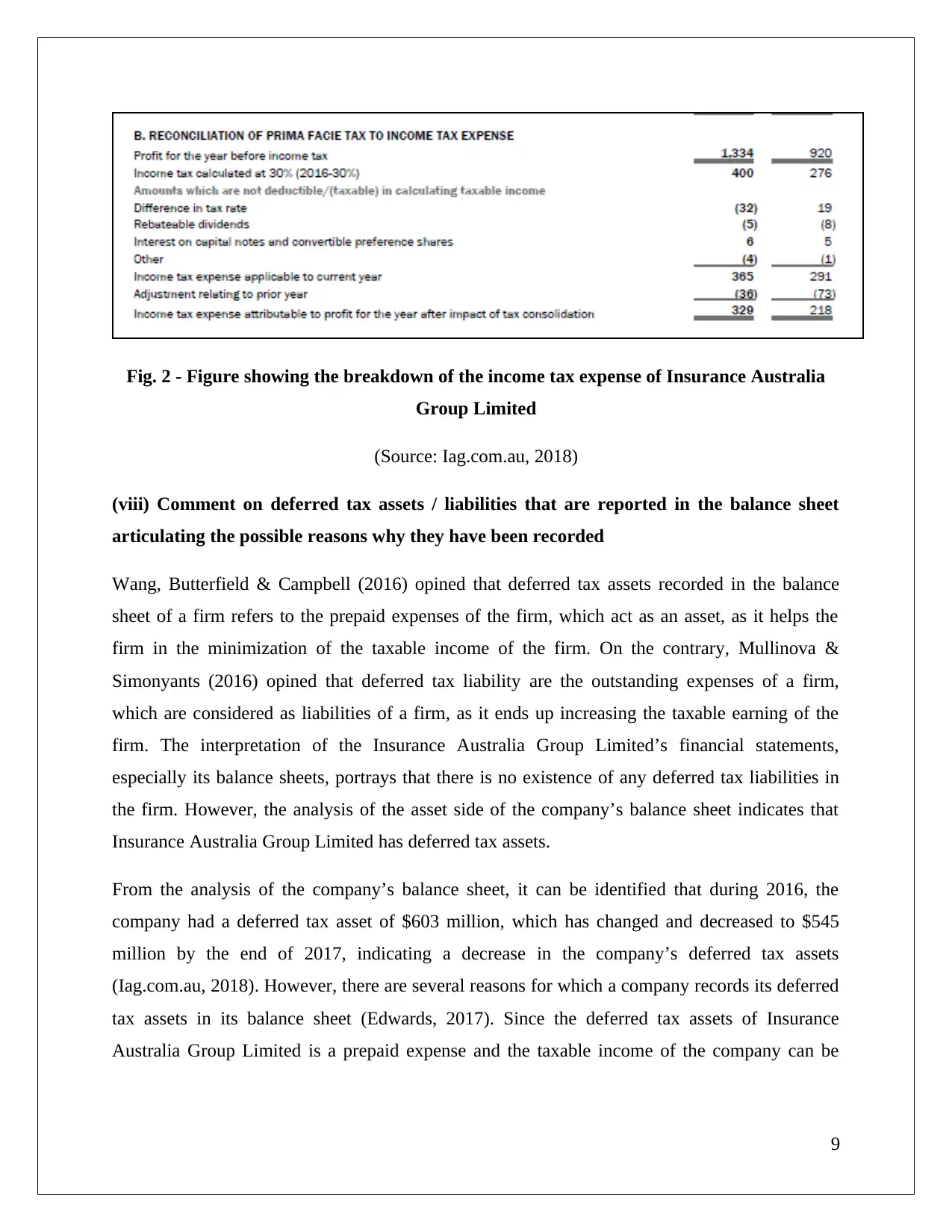

However, the analysis of the notes to accounts of the company shows why and how the figure is

different. The taxes of the company have been calculated at 30% tax rate itself. However, the

difference has taken place since the company has adjusted amounts that are not taxable such as

difference in the rate of tax, rebateable dividends, etc., due to which the company tax rate times

of accounting income and the tax expense figure of Insurance Australia during the previous

financial year differ from one another. The following image shows the breakdown of the tax

expense of Insurance Australia Group Limited during the last two years -

8

(vi) Firm’s tax expense in its latest financial statements

Income tax expenses can be referred to as the expense or the amount that a firm pays to the

government of the country in which it operates and is recorded under the income statement of

every firm (Lee et al., 2017). The tax expense of Insurance Australia, as recorded in the

company’s income statement, amounts to $329 million during the past accounting year 2017

(Iag.com.au, 2018). The latest financial statements of the company Insurance Australia Group

Limited also show that the income tax expense of the company had amounted to $218 million

during the year 2016 (Iag.com.au, 2018).

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm

As per the rate of tax, which is mandatory to be paid to the government of all the public limited

companies listed under the ASX, is 30% (Burkhauser, Hahn & Wilkins, 2015). The company

Insurance Australia Group Limited is also liable to be paying income tax on the accounting profit

earned by it at the rate of 30%. However, if the figure of the tax expense of Insurance Australia

Group’s latest financial reports is considered, it can be reviewed that the tax expense stated in the

income statement of the company is higher than the taxable amount if the tax rate is 30%

(Iag.com.au, 2018). This shows that the figure of tax expense of Insurance Australia Group

Limited is not the same as the tax rate times of its accounting income.

However, the analysis of the notes to accounts of the company shows why and how the figure is

different. The taxes of the company have been calculated at 30% tax rate itself. However, the

difference has taken place since the company has adjusted amounts that are not taxable such as

difference in the rate of tax, rebateable dividends, etc., due to which the company tax rate times

of accounting income and the tax expense figure of Insurance Australia during the previous

financial year differ from one another. The following image shows the breakdown of the tax

expense of Insurance Australia Group Limited during the last two years -

8

Fig. 2 - Figure showing the breakdown of the income tax expense of Insurance Australia

Group Limited

(Source: Iag.com.au, 2018)

(viii) Comment on deferred tax assets / liabilities that are reported in the balance sheet

articulating the possible reasons why they have been recorded

Wang, Butterfield & Campbell (2016) opined that deferred tax assets recorded in the balance

sheet of a firm refers to the prepaid expenses of the firm, which act as an asset, as it helps the

firm in the minimization of the taxable income of the firm. On the contrary, Mullinova &

Simonyants (2016) opined that deferred tax liability are the outstanding expenses of a firm,

which are considered as liabilities of a firm, as it ends up increasing the taxable earning of the

firm. The interpretation of the Insurance Australia Group Limited’s financial statements,

especially its balance sheets, portrays that there is no existence of any deferred tax liabilities in

the firm. However, the analysis of the asset side of the company’s balance sheet indicates that

Insurance Australia Group Limited has deferred tax assets.

From the analysis of the company’s balance sheet, it can be identified that during 2016, the

company had a deferred tax asset of $603 million, which has changed and decreased to $545

million by the end of 2017, indicating a decrease in the company’s deferred tax assets

(Iag.com.au, 2018). However, there are several reasons for which a company records its deferred

tax assets in its balance sheet (Edwards, 2017). Since the deferred tax assets of Insurance

Australia Group Limited is a prepaid expense and the taxable income of the company can be

9

Group Limited

(Source: Iag.com.au, 2018)

(viii) Comment on deferred tax assets / liabilities that are reported in the balance sheet

articulating the possible reasons why they have been recorded

Wang, Butterfield & Campbell (2016) opined that deferred tax assets recorded in the balance

sheet of a firm refers to the prepaid expenses of the firm, which act as an asset, as it helps the

firm in the minimization of the taxable income of the firm. On the contrary, Mullinova &

Simonyants (2016) opined that deferred tax liability are the outstanding expenses of a firm,

which are considered as liabilities of a firm, as it ends up increasing the taxable earning of the

firm. The interpretation of the Insurance Australia Group Limited’s financial statements,

especially its balance sheets, portrays that there is no existence of any deferred tax liabilities in

the firm. However, the analysis of the asset side of the company’s balance sheet indicates that

Insurance Australia Group Limited has deferred tax assets.

From the analysis of the company’s balance sheet, it can be identified that during 2016, the

company had a deferred tax asset of $603 million, which has changed and decreased to $545

million by the end of 2017, indicating a decrease in the company’s deferred tax assets

(Iag.com.au, 2018). However, there are several reasons for which a company records its deferred

tax assets in its balance sheet (Edwards, 2017). Since the deferred tax assets of Insurance

Australia Group Limited is a prepaid expense and the taxable income of the company can be

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reducing in future due to this prepaid expense, it can be articulated that the company records

deferred tax assets in its balance sheet, as it can reducing its taxable income.

10

deferred tax assets in its balance sheet, as it can reducing its taxable income.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

Hence, the above discussions help in gathering information about Insurance Australia Group

Limited’s movements in net cash position in the past three years along with articulating the

reasons behind the movements. The report also helps in understanding the items listed under the

company’s other income statement and the treatment of tax in the company. The deferred tax

assets present in the company have also been evaluated through this report, stating the reasons

for including it in the company’s balance sheet.

11

Hence, the above discussions help in gathering information about Insurance Australia Group

Limited’s movements in net cash position in the past three years along with articulating the

reasons behind the movements. The report also helps in understanding the items listed under the

company’s other income statement and the treatment of tax in the company. The deferred tax

assets present in the company have also been evaluated through this report, stating the reasons

for including it in the company’s balance sheet.

11

References

Burkhauser, R. V., Hahn, M. H., & Wilkins, R. (2015). Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), 181-205.

Edwards, A. (2017). The deferred tax asset valuation allowance and firm

creditworthiness. Journal of the American Taxation Association.

Gordon, E. A., Henry, E., Jorgensen, B. N., & Linthicum, C. L. (2017). Flexibility in cash-flow

classification under IFRS: determinants and consequences. Review of Accounting Studies, 22(2),

839-872.

Iag.com.au (2018). IAG Limited. [online] Available at: https://www.iag.com.au/ [Accessed 23

May 2018].

Lee, B. B., Shin, H., Vetter, W., & Kim, D. W. (2017). Management of income statement

variables to report small positive earnings numbers. Asian Review of Accounting, 25(1), 58-84.

Mechelli, A., & Cimini, R. (2014). Is comprehensive income value relevant and does location

matter? A European study. Accounting in Europe, 11(1), 59-87.

Mullinova, S., & Simonyants, N. (2016). Reflection of a deferred tax liability in the credit union

reporting according to IFRS (IAS) 12" Income taxes". Modern European Researches, (1), 83-88.

Nejad, M. Y., & Ahmad, A. (2017). Value Relevance of available-for-sale financial instruments

(AFS) and revaluation surplus of PPE (REV) components of other comprehensive income.

In SHS Web of Conferences (Vol. 34). EDP Sciences.

Reid, W., & Myddelton, D. R. (2017). Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Stevanovic, S., Belopavlovic, G., & Lazarevic-Moravcevic, M. (2017). Creative Cash Flow

Reporting–the Motivation and Opportunities. Economic analysis, 46(1-2), 28-39.

Wang, Y., Butterfield, S., & Campbell, M. (2016). Deferred tax items as earnings management

indicators. International Management Review, 12(2), 37.4

12

Burkhauser, R. V., Hahn, M. H., & Wilkins, R. (2015). Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), 181-205.

Edwards, A. (2017). The deferred tax asset valuation allowance and firm

creditworthiness. Journal of the American Taxation Association.

Gordon, E. A., Henry, E., Jorgensen, B. N., & Linthicum, C. L. (2017). Flexibility in cash-flow

classification under IFRS: determinants and consequences. Review of Accounting Studies, 22(2),

839-872.

Iag.com.au (2018). IAG Limited. [online] Available at: https://www.iag.com.au/ [Accessed 23

May 2018].

Lee, B. B., Shin, H., Vetter, W., & Kim, D. W. (2017). Management of income statement

variables to report small positive earnings numbers. Asian Review of Accounting, 25(1), 58-84.

Mechelli, A., & Cimini, R. (2014). Is comprehensive income value relevant and does location

matter? A European study. Accounting in Europe, 11(1), 59-87.

Mullinova, S., & Simonyants, N. (2016). Reflection of a deferred tax liability in the credit union

reporting according to IFRS (IAS) 12" Income taxes". Modern European Researches, (1), 83-88.

Nejad, M. Y., & Ahmad, A. (2017). Value Relevance of available-for-sale financial instruments

(AFS) and revaluation surplus of PPE (REV) components of other comprehensive income.

In SHS Web of Conferences (Vol. 34). EDP Sciences.

Reid, W., & Myddelton, D. R. (2017). Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Stevanovic, S., Belopavlovic, G., & Lazarevic-Moravcevic, M. (2017). Creative Cash Flow

Reporting–the Motivation and Opportunities. Economic analysis, 46(1-2), 28-39.

Wang, Y., Butterfield, S., & Campbell, M. (2016). Deferred tax items as earnings management

indicators. International Management Review, 12(2), 37.4

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.