Corporate Accounting: Impairment of Cash Generating Units (CGUs)

VerifiedAdded on 2023/06/13

|6

|1138

|432

Report

AI Summary

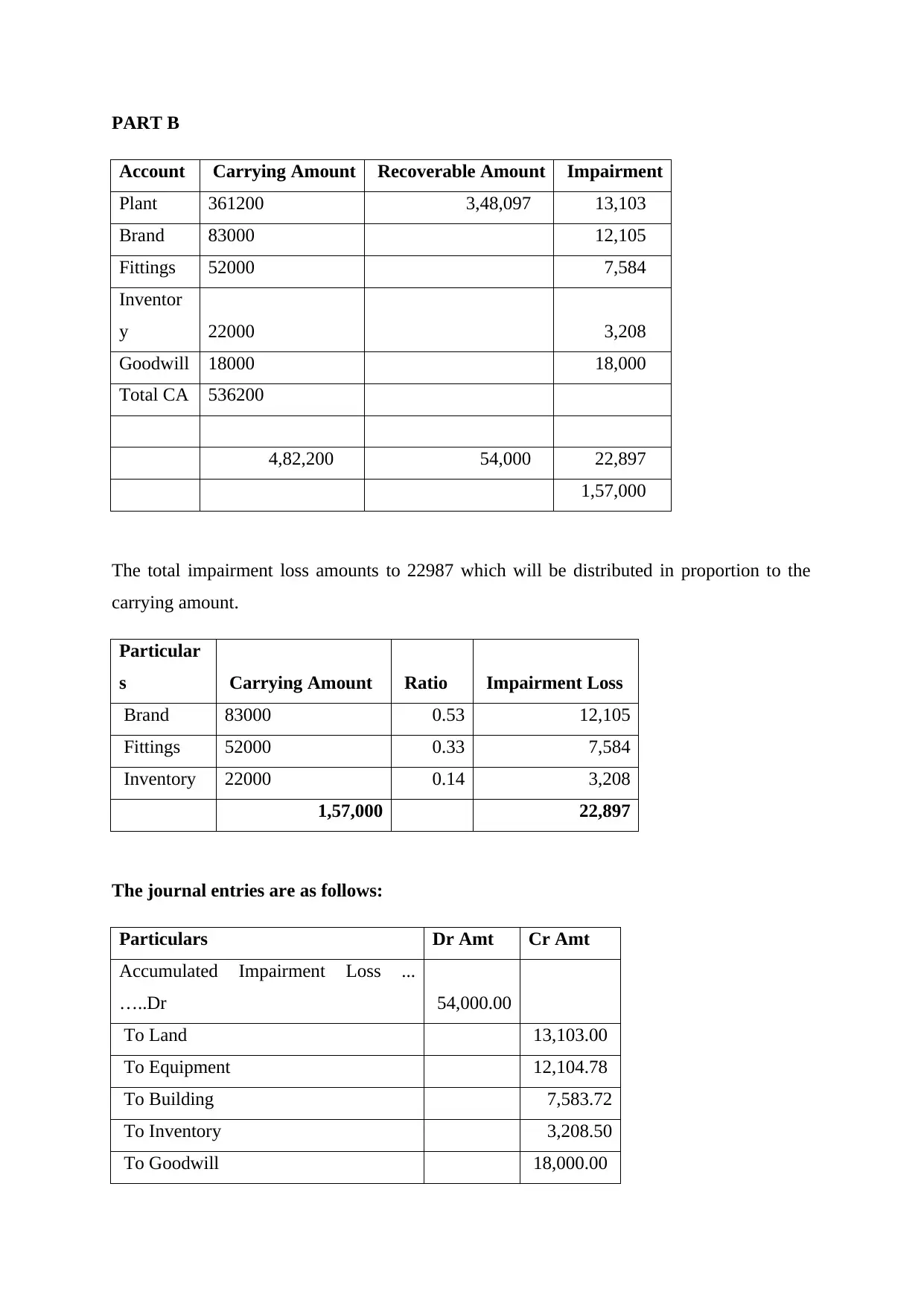

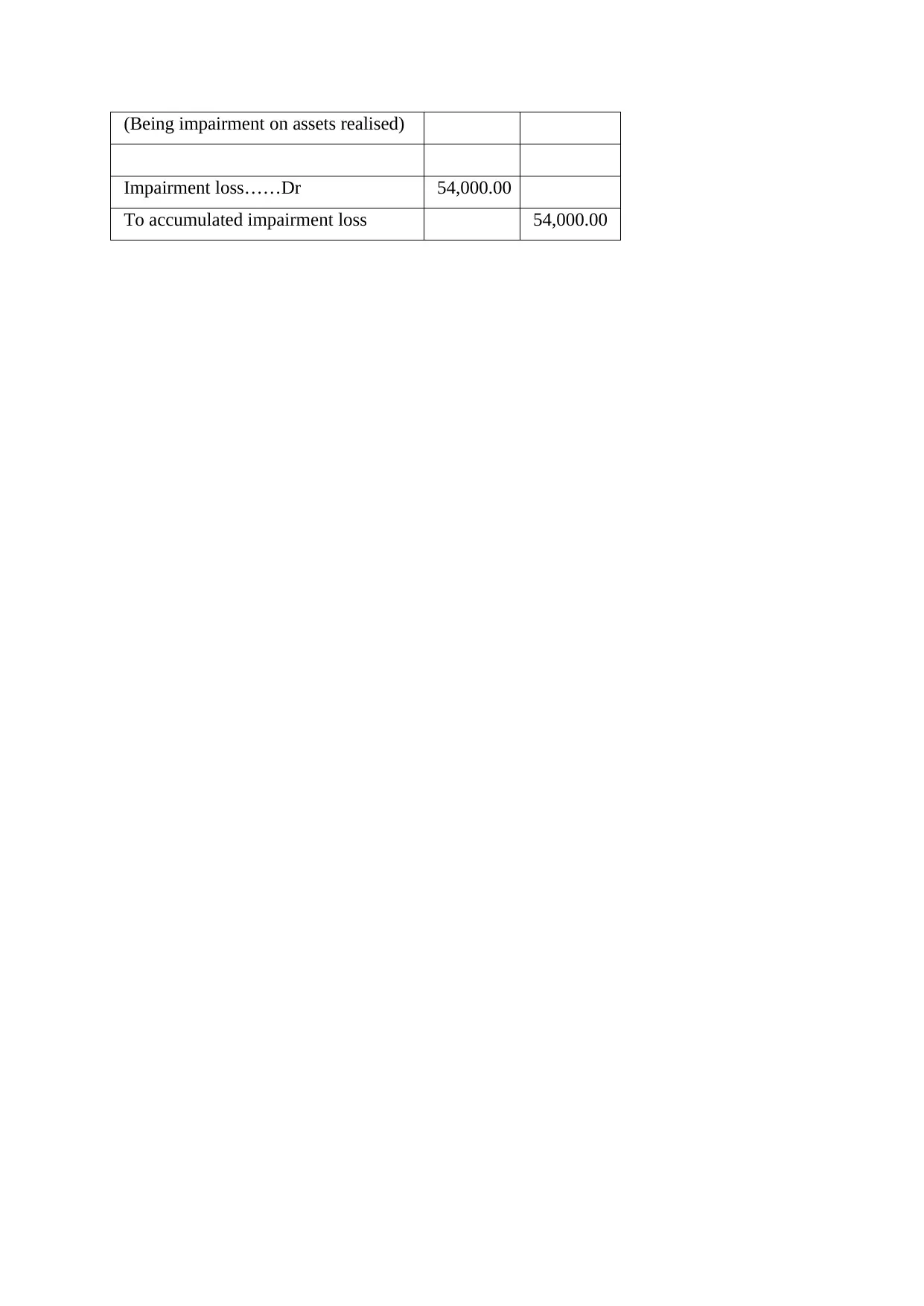

This report provides a comprehensive analysis of impairment in corporate accounting, focusing on the identification, calculation, and reporting of impairment losses for both individual assets and cash-generating units (CGUs). It details the process of comparing the carrying amount of assets with their recoverable amount to determine impairment, emphasizing the importance of fair value assessment and the allocation of impairment losses across CGU assets. The report includes a practical example demonstrating the calculation of impairment loss, its distribution among assets, and the corresponding journal entries. It also highlights the disclosure requirements for impairment losses and reversals in financial statements, ensuring compliance with accounting standards. The document also includes a bibliography of accounting resources.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.